Cognitive Media Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.74 Billion |

| Market Size (2031) | USD 45.48 Billion |

| Growth Rate (2026 - 2031) | 19.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Media Market Analysis by Mordor Intelligence

The Cognitive Media Market size is expected to grow from USD 15.70 billion in 2025 to USD 18.74 billion in 2026 and is forecast to reach USD 45.48 billion by 2031 at 19.4% CAGR over 2026-2031.

Expanding AI capabilities, lower cloud-GPU pricing, and the shift toward hyper-personalized digital experiences are moving the market from early experimentation to mainstream adoption. Media companies increasingly rely on large-language-model pipelines to automate editing, captioning, and localization tasks, cutting turnaround times for multi-language releases. AI-native ad formats that build entire campaigns from a single product image are widening revenue streams, while edge deployments are reducing latency for interactive and live use-cases. North America continues to anchor global spending thanks to heavy R&D outlays by platform leaders, yet rapid infrastructure rollouts in Japan and China are propelling Asia-Pacific toward the fastest regional growth trajectory.

Key Report Takeaways

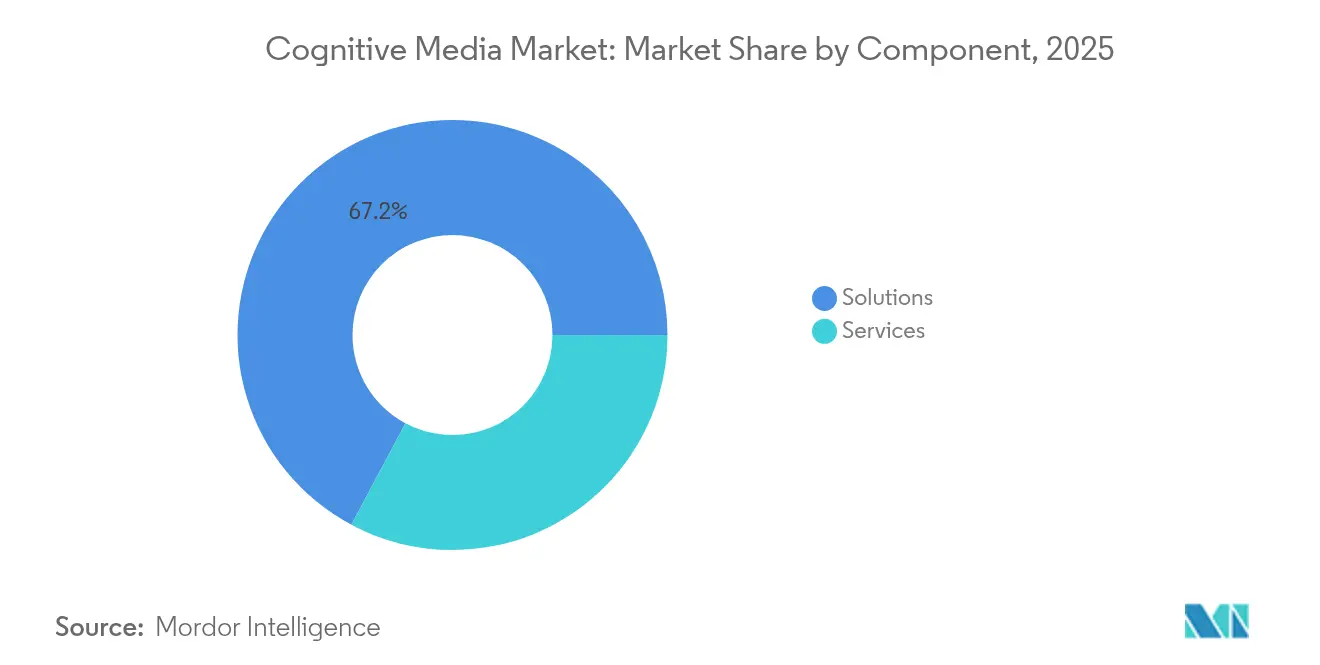

- By component, solutions held 67.20% of the cognitive media market share in 2025; services are projected to grow at a 23.30% CAGR to 2031.

- By deployment, the cloud model accounted for 81.30% of the cognitive media market size in 2025 and is forecast to expand at a 20.50% CAGR.

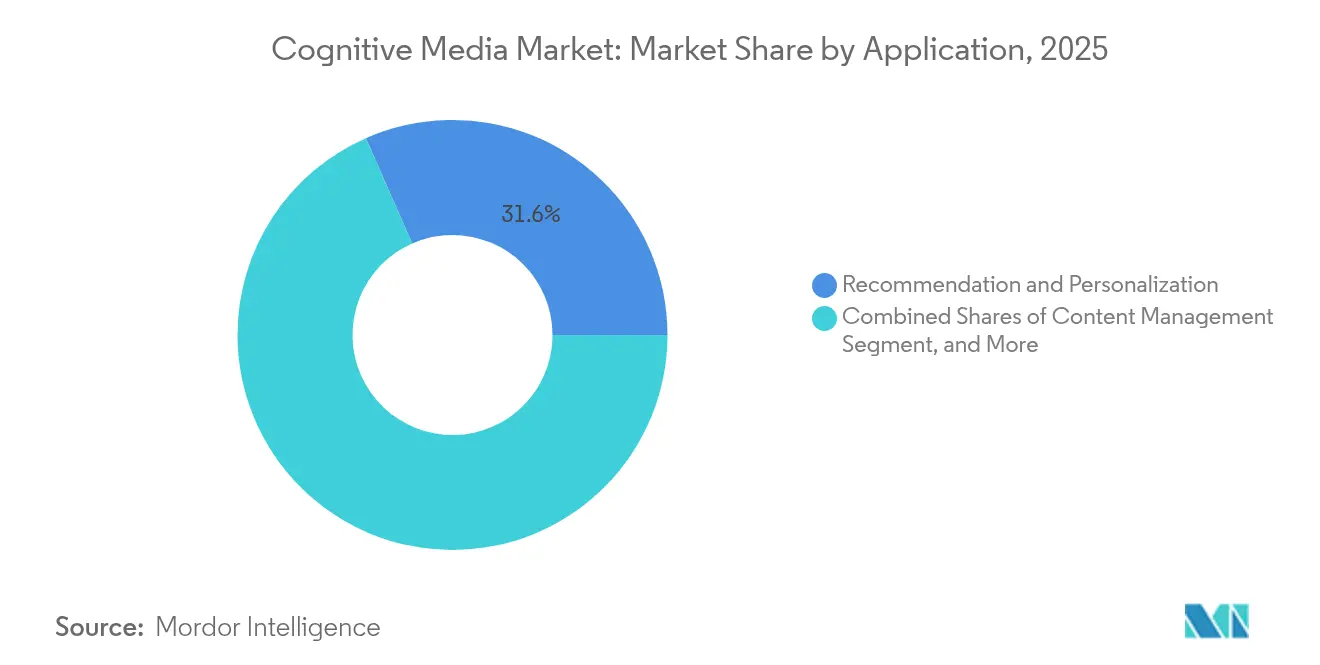

- By application, recommendation and personalization led with 31.60% revenue share in 2025 in the cognitive media market, while predictive analytics is advancing at a 26.80% CAGR through 2031.

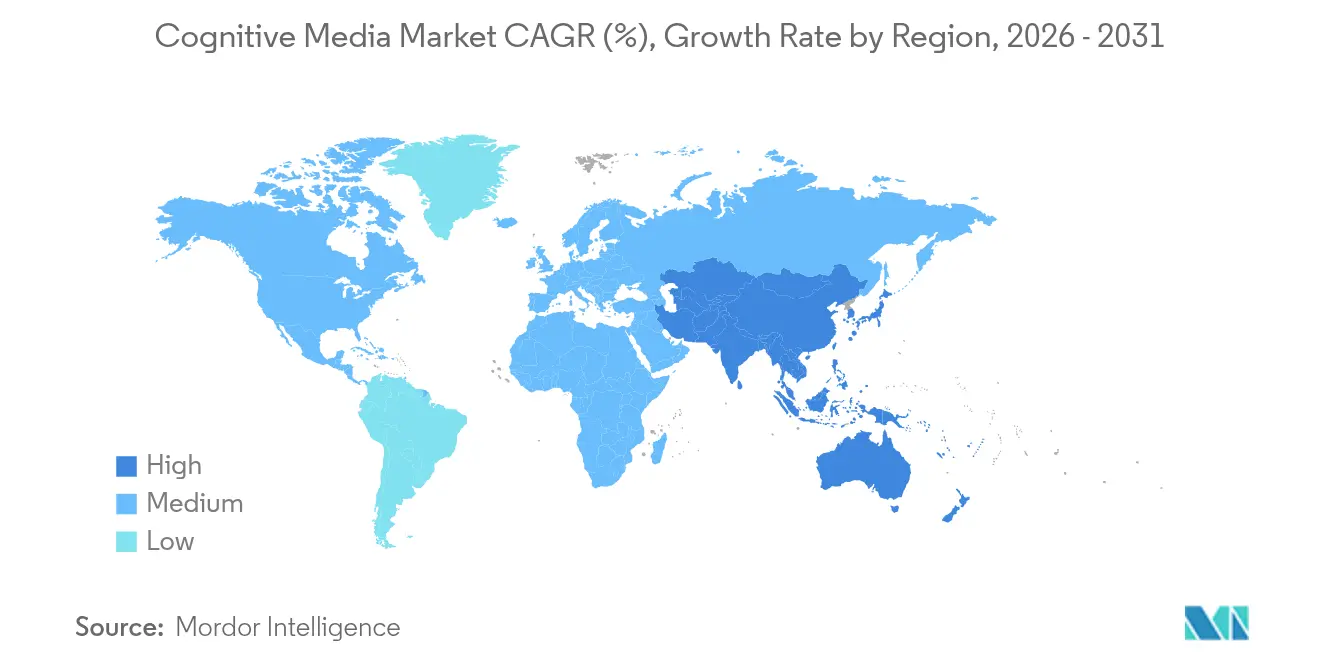

- By geography, North America captured 42.40% of the cognitive media market in 2025 in the cognitive media market; Asia-Pacific is set to post a 23.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cognitive Media Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workflow automation across multi-platform content supply chains | +4.20% | Global; early uptake in North America and EU | Medium term (2-4 years) |

| Hyper-personalized content as an ARPU lever | +3.80% | Global; strongest in Asia-Pacific streaming markets | Short term (≤ 2 years) |

| Cloud GPU cost curves falling faster than Moore’s Law | +3.10% | Global; concentrated in hyperscale regions | Long term (≥ 4 years) |

| AI-native advertising formats boosting CPM yields | +2.90% | North America and EU first; moving to Asia-Pacific | Medium term (2-4 years) |

| Generative-AI-ready creator tools democratizing production | +2.70% | Global; rapid takes in emerging economies | Short term (≤ 2 years) |

| Zero-party data strategies enhancing recommendation accuracy | +2.30% | Global; led by privacy-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Workflow Automation Across Multi-Platform Content Supply Chains

Media groups now automate up to 100% of ingest, edit, and caption tasks, pushing 4.2 percentage points of additional CAGR. Warner Bros. Discovery cut localization costs by 60% after integrating Google’s generative captioning suite. Broadcast schedulers such as Mediagenix simultaneously optimize linear and streaming grids, freeing staff to focus on premium content.[1]Mediagenix Editorial Team, “Unified Scheduling in a Multi-Platform Universe,” Mediagenix, mediagenix.tv Prime Focus Technologies reported a 30% fall in manual metadata work when AI agents preview, tag, and archive assets.

Hyper-Personalized Content as an ARPU Lever

Hyper-personalization adds 3.8 percentage points to growth by lifting engagement and subscriber spend. A healthcare retailer deploying AI recommenders logged a 33.49% ARPU jump and a 32.79% rise in average order value. The Financial Times uses an AI paywall that calibrates article access without depressing conversions, underscoring the delicate balance between personalization and revenue. Netflix analyzes more than 200 billion daily user events to steer script development toward segments most likely to binge entire seasons. Publishers collecting zero-party preference signals recorded 60% higher content clicks among self-declared interest cohorts.

Cloud GPU Cost Curves Falling Faster Than Moore’s Law

Spending efficiency gains contribute 3.1 percentage points to the cognitive media market. Akamai’s switch to NVIDIA RTX 4000 GPUs accelerated transcoding 25× and lowered live-stream cost bases by 70%. SoftBank’s Tokyo AI platform now runs 4,000 Hopper GPUs, illustrating how cloud economics beat most on-premise alternatives for model training at scale.[2]Mark Walsh, “SoftBank Expands Japan AI Compute,” softbank.jp These savings enable real-time automated moderation and dynamic ad insertion that were previously cost-prohibitive.

AI-Native Advertising Formats Boosting CPM Yields

New ad units account for a 2.9 percentage-point lift. Meta’s generative ad suite raised return-on-ad-spend by 22% for the 4 million advertisers already live on the tools. TikTok’s AI-powered virtual try-ons achieve engagement rates 40% higher than standard video placements. On the sell-side, Revenue Analytics’ Aida platform mines price-inventory vectors in real time to boost yield for streaming outlets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of licensed, culture-specific training data | -2.80% | Global; acute in non-English markets | Long term (≥ 4 years) |

| Escalating GPU power-consumption penalties | -2.10% | Global; hyperscale data-center hubs | Medium term (2-4 years) |

| Evolving copyright litigation on synthetic content | -1.80% | North America and Europe | Medium term (2-4 years) |

| Data-sovereignty constraints on cross-border AI workflows | -1.50% | Europe and parts of APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Licensed, Culture-Specific Training Data

Court rulings in 2024–2025 confirmed that unlicensed copyrighted inputs fall outside fair-use protections, trimming 2.8 percentage points off market expansion. Disney and NBCUniversal’s suit against Midjourney signaled aggressive enforcement by rights holders.[3]Bill Donahue, “Hollywood Studios Sue Midjourney Over AI Art,” NPR, npr.org News Corp’s USD 250 million licensing pact with OpenAI shows how compliant datasets now command premium fees. Smaller language markets face higher entry costs because culturally nuanced corpora remain scarce.

Escalating GPU Power-Consumption Penalties

Power draw erodes 2.1 percentage points of growth as data centers struggle with 120–140 kW racks. EPRI estimates AI workloads could reach 40% of new U.S. electricity demand by 2030. HPCwire projects AI accelerators will absorb 2,318 TWh between 2025 and 2029. Operators must invest in immersion cooling and renewable sourcing to keep large-model deployments financially viable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Drive Enterprise Adoption

Solutions contributed 67.20% of the cognitive media market in 2025 as studios prioritized turnkey AI systems over consulting-led roll-outs. IBM’s Watsonx alone booked contracts worth USD 5 billion by scaling language-model toolkits into existing broadcast asset management suites. Veritone’s Digital Media Hub and Ateliere Connect AI help rights-holders automatically surface long-tail clips for syndication, reducing dormant asset ratios by 45%. As a result, the solutions slice is forecast to maintain clear leadership through 2031.

The services sub-segment is expanding at a 23.30% CAGR because integration across legacy control rooms, playout chains, and OTT apps requires scarce engineering talent. Consulting practices now market rapid-deployment “factory models” to plug skills gaps within weeks. Where custom pipelines still prevail, newsrooms and multi-regional sports networks, specialists tune prompt-engineering, guardrails, and workflow orchestration on retainer models, adding annuity revenue to vendors.

By Deployment: Cloud Infrastructure Dominates

The cloud captured 81.30% of the cognitive media market share in 2025, the backbone for multi-petabyte training runs and large-scale inference tasks. Processing one 8K feature-length film already consumes tens of thousands of GPU hours; hyperscale clusters amortize this load across clients, keeping marginal compute affordable. SoftBank’s 4,000-unit Hopper cluster shows how country-level platforms can offer model-as-a-service while meeting data-residency rules.

On-premise remains essential for tier-one live news, where latency tolerance can be below 100 milliseconds. Hybrid builds therefore mix real-time encoding racks on-site with burst training in the cloud. Google Cloud and NVIDIA’s GB300 NVL72 system brings 30× faster memory bandwidth to these hybrids, making model fine-tuning feasible inside daily production windows.

By Application: Personalization Leads, Analytics Accelerates

Recommendation and personalization held a 31.60% share of the cognitive media market size in 2025, the direct beneficiary of zero-party data capture and real-time event feedback loops. Netflix uses pattern discovery on 200 billion daily touchpoints to green-light pilots that statistically align with high-completion cohorts. Publishers applying similar playbooks reduced churn by double-digits within one quarter.

Predictive analytics is advancing at a 26.80% CAGR through 2031 as networks model audience swings before locking program slates. Advanced churn-propensity models achieve accuracy above 85%, allowing pre-emptive retention incentives that raise subscription lifetime value. Content moderation and network optimization continue to mature, but the next uplift will arrive from AI-generated translation passes that compress localization timelines from weeks to days, expanding addressable audiences overnight.

Geography Analysis

North America accounted for 42.40% of 2025 revenue as platform majors assembled end-to-end AI stacks that blend proprietary data, silicon, and distribution. The region’s policy regime remains comparatively permissive; yet, a wave of copyright suits, with 25 active as of June 2025, has injected caution into generative deployment news.bloomberglaw.com. Nevertheless, combined USD 320 billion in 2025 AI capex from Meta, Amazon, Alphabet, and Microsoft keeps the cognitive media market primed for near-term innovations.

The Asia-Pacific region posts the fastest 23.10% CAGR through 2031, led by Japan’s Society 5.0 programs and SoftBank’s USD 960 million backbone expansion, which anchors local model training capacity. China’s conversational-AI revenue is projected to quintuple from USD 1.05 billion in 2023 to USD 5.19 billion by 2030, driven by policy incentives that leverage domestic datasets to fuel industry clouds. The first full-length AI-generated feature, “Pirate Queen: Zheng Yi Sao,” premiered in Malaysia in 2025, underscoring regional creative momentum.

Europe advances steadily, striking a balance between innovation and consumer protection under the 2025 AI Act, which mandates content watermarking by August 2025. Spain’s draft deepfake fines underscore rising enforcement appetite, but the bloc’s single digital market still offers scale advantages for vendors clearing compliance hurdles. Emerging Latin American and African markets, largely mobile-first, present white-space opportunities as telcos bundle AI-enabled streaming tiers with prepaid data packs, leapfrogging legacy pay-TV ecosystems.

Competitive Landscape

The cognitive media market remains moderately fragmented; yet share is consolidating as cloud titans bundle AI tooling with infrastructure. Meta hired four OpenAI veterans to spearhead an internal Superintelligence unit, dangling multimillion-dollar packages that intensified global talent scarcity. IBM secured enterprise mindshare by positioning Watsonx as a modular layer atop existing newsroom systems, landing multiyear deals across broadcast groups. Google and NVIDIA’s co-developed accelerators grant content studios turnkey performance leaps, prompting co-location partnerships with premiere post houses.

Start-ups still capture niche demand. Edge-focused vendors pipe context-aware recommendation engines directly into set-top boxes, eliminating round-trip latency. Others specialize in authenticity verification, embedding cryptographic watermarks at the frame level to deter deepfake misuse. Patent filings around energy-efficient inference soared during 2024, pointing to silicon-level differentiation as an emerging moat.

White-space persists in regional language datasets and real-time human-in-the-loop moderation. Vendors furnishing curated, licensed corpora or hybrid review teams can command premium service margins until regulatory clarity unlocks broader automated roll-out. As lawsuits drive up dataset costs, players with first-party IP libraries enjoy a defensible position.

Cognitive Media Industry Leaders

IBM Corporation

Google LLC

Amazon Web Services

Microsoft Corporation

Salesforce.com, inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Meta recruited four OpenAI researchers to form a Superintelligence team.

- June 2025: Disney and NBCUniversal sued Midjourney over alleged mass copyright infringement.

- June 2025: YouTube integrated Google’s Veo 3 model into Shorts for next-gen creation tools.

- May 2025: U.S. Congress passed the TAKE IT DOWN Act banning non-consensual intimate deepfakes.

Global Cognitive Media Market Report Scope

Media content providers across the globe are primarily using cognitive services in order to recommend and provide hyper-personalized content to all their viewers which are based on the data that is collected from the user's activity and behavior. Cognitive computing technologies primarily include a set of Artificial Intelligence (AI) technologies such as deep learning, machine learning among others.

| Solutions |

| Services |

| Cloud |

| On-premises |

| Content Management |

| Recommendation and Personalization |

| Predictive Analysis |

| Network Optimization |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Component | Solutions |

| Services | |

| By Deployment | Cloud |

| On-premises | |

| By Application | Content Management |

| Recommendation and Personalization | |

| Predictive Analysis | |

| Network Optimization | |

| Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the projected size of the cognitive media market by 2031?

The cognitive media market is expected to reach USD 45.48 billion by 2031, growing at a 19.4% CAGR from 2026.

Which component segment leads revenue today?

AI solutions led with 67.20% of 2025 revenue as media firms favored turnkey platforms over consulting-heavy builds.

Why is Asia-Pacific growing faster than other regions?

Large infrastructure investments by Japanese and Chinese conglomerates and supportive policy frameworks are driving a 23.1% CAGR in the region.

How are cloud GPUs influencing market economics?

A 25% annual drop in cloud-GPU pricing is lowering barriers for smaller studios and enabling real-time AI workflows once considered cost-prohibitive.

What is the main legal risk facing AI media companies?

A shortage of licensed, culture-specific datasets and a rising wave of copyright litigation threaten to raise development costs and delay model launches.

Which application area will grow the fastest through 2031?

Predictive analytics is set to expand at a 26.8% CAGR as studios use AI forecasting to guide content investment, ad inventory, and churn management strategies.

Page last updated on: