Cognitive Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

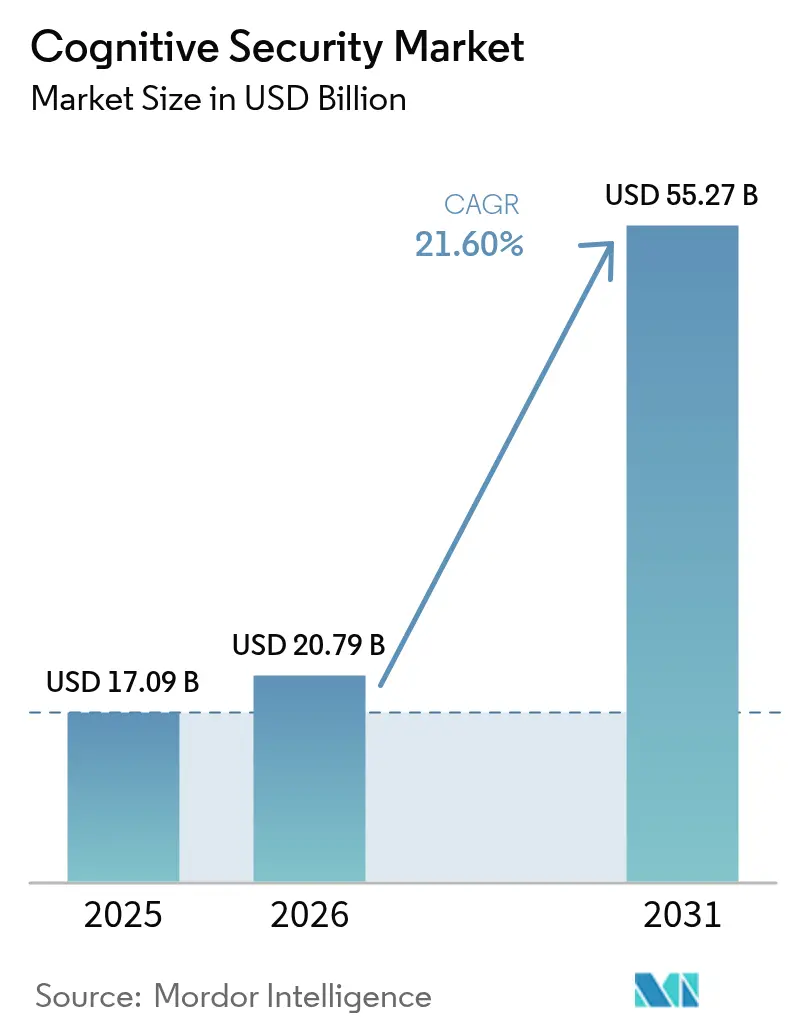

| Market Size (2026) | USD 20.79 Billion |

| Market Size (2031) | USD 55.27 Billion |

| Growth Rate (2026 - 2031) | 21.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Security Market Analysis by Mordor Intelligence

The cognitive security market size was valued at USD 17.09 billion in 2025 and estimated to grow from USD 20.79 billion in 2026 to reach USD 55.27 billion by 2031, at a CAGR of 21.6% during the forecast period (2026-2031). Persistent AI-enabled threats, expanding attack surfaces created by cloud adoption, and mounting regulatory scrutiny combine to fuel this growth. Enterprises invested heavily after discovering that conventional tools miss AI-specific vulnerabilities such as model poisoning, adversarial prompts, and synthetic data leakage, prompting an accelerated pivot toward advanced analytics and autonomous defense. Parallel advances in large-language-model deployments inside corporate workflows further sharpen demand, because every generative-AI rollout creates new entry points that must be continuously monitored and hardened. Vendors respond by embedding self-learning algorithms into incident-response playbooks, reducing mean time to detect and contain breaches from hours to minutes while simultaneously shrinking false-positive noise that overwhelms human analysts. These dynamics position the cognitive security market as one of the fastest-expanding segments within broader cybersecurity spending.

Key Report Takeaways

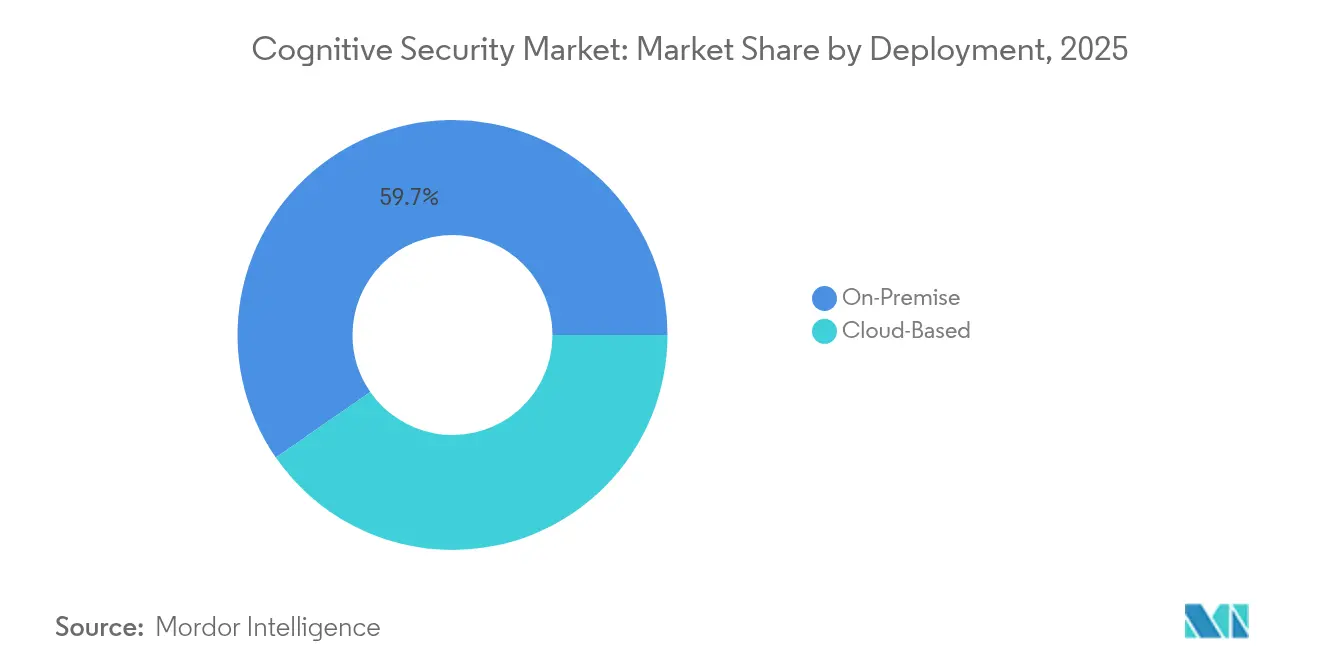

- By deployment, on-premises architectures held 59.65% of cognitive security market share in 2025, whereas cloud-based platforms are projected to expand at a 26.05% CAGR through 2031.

- By service type, professional services led with 59.85% revenue share in 2025, while managed services exhibit the highest anticipated CAGR at 27.8% through 2031.

- By application, automated compliance management accounted for a 44.65% share of the cognitive security market size in 2025 and is advancing at a 28.9% CAGR through 2031.

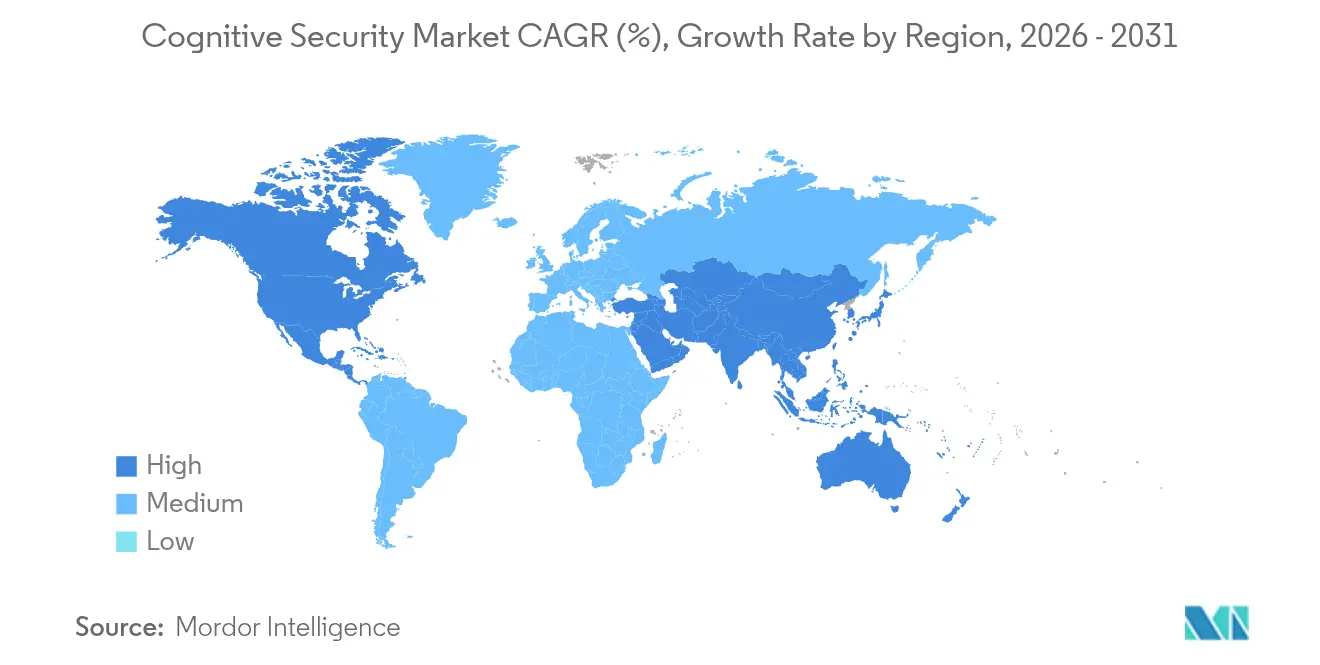

- By geography, North America commanded 35.25% of cognitive security market share in 2025, whereas Asia-Pacific posts the fastest regional expansion at a 24.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Cognitive Security Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exponential rise of unstructured enterprise data | +4.2% | Global, high intensity in North America and Asia-Pacific | Medium term (2-4 years) |

| Surge in IoT dark data | +3.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Cloud-native AI toolchains | +3.5% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Escalating threats on open-source and cloud stacks | +4.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Exponential Rise of Unstructured Enterprise Data

Massive growth in emails, collaboration files, sensor readings, and multimedia escalates both the visibility challenge and the attack surface. Cognitive engines ingest terabytes of raw logs to pinpoint deviations in user behavior, cutting false-positive alerts by 95% while surfacing stealthy lateral movements that bypass rule-based systems. However, attackers benefit from the same information richness, scraping content to craft context-aware spear-phishing campaigns. Security teams therefore integrate self-learning analytics directly into data-lakes to correlate identity, device, and network telemetry in near real time, turning previously dormant archives into actionable intelligence that enhances breach-detection accuracy. The net result is an elevated baseline for analytic depth that positions the cognitive security market for sustained expansion across all verticals.

Surge in IoT Dark Data

Industrial and consumer IoT deployments add billions of unmanaged endpoints, creating a torrent of operational telemetry that standard SIEM platforms cannot parse. Cognitive engines model baseline behavior for each device class and flag deviations such as anomalous firmware changes or unexpected east-west traffic. In energy grids and smart-factory floors, this functionality directly mitigates downtime risks while protecting life-safety systems. The security gap widens as OT networks converge with IT backbones, prompting manufacturing and utilities firms to invest in edge-resident AI analytics that operate under stringent latency constraints. Consequently, demand for scalable, device-agnostic platforms inside the cognitive security market continues to accelerate through 2030. [1]Frontiers in Computer Science, “AI Security in IoT Environments,” frontiersin.org

Cloud-Native AI Toolchains Democratizing Cognitive Security

Services like Amazon SageMaker, Azure Machine Learning, and Google Vertex AI simplify model deployment yet simultaneously enlarge exposure. Eighty-two percent of organizations leave notebook interfaces reachable without hardened authentication, enabling token theft and unauthorized model manipulation. Organizations embed shift-left security controls into CI/CD pipelines, scanning model weights for anomalies before promotion to production. The rapid feedback loop improves release velocity while hardening defense; however, continuous posture management becomes mandatory because code and model drift happen faster than manual reviews can track. These opposing forces propel rapid adoption of automated governance modules inside cognitive security platforms. [2]Trend Micro, “Cloud-Native AI Security Survey 2025,” trendmicro.com

Escalating Threats on Open-Source and Cloud Stacks

Attackers weaponize adversarial machine-learning techniques to plant poisoned samples into public model hubs and open-source code libraries. IBM’s X-Force observed a 71% rise in compromised credentials used to alter training data or hijack model endpoints, forcing defenders to verify dataset lineage and monitor runtime inference accuracy. Enterprises deploy ensemble detectors that fuse traditional network telemetry with model-integrity checks, spotting gradient manipulation or temperature skew in large language models before production impact occurs. The heightened sophistication locks in premium budgets for adaptive protection, cementing the uptick in the cognitive security market.

Restraints Impact Analysis of Cognitive Security Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of AI/ML cyber-analytics talent | –2.8% | Global, acute in North America and EU | Medium term (2-4 years) |

| Multi-jurisdictional data-governance complexity | –2.1% | EU primary, global secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of AI/ML Cyber-Analytics Talent

Demand for practitioners able to code reinforcement-learning defenses, tune prompt-shield models, and interpret threat telemetry vastly exceeds global supply. Organizations counter by outsourcing to managed-service specialists and by investing in low-code orchestration layers that let fewer engineers protect larger asset bases. Although automation handles level one triage, level two and level three escalations still require hybrid skill sets spanning mathematics, secure coding, and regulatory interpretation. The resulting wage inflation inflates project TCO, nudging some smaller firms toward consumption-based cloud subscription models instead of bespoke builds.

Multi-Jurisdictional Data Governance Complexity

The EU AI Act, China’s Cybersecurity Law, and evolving US federal guidance impose divergent obligations around audit logging, dataset provenance, and algorithmic transparency. Multinational firms must maintain region-specific model registries and segregated inference pipelines to comply with overlapping rules, raising compliance spend to as high as 15% of total deployment budgets. Vendors respond by embedding policy engines that automate retention, access, and explainability requirements in real time, yet smaller enterprises find the legal overhead daunting. Regional fragmentation therefore slows adoption in heavily regulated verticals even as the overall cognitive security market grows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Cognitive Security Market Segment Analysis

By Deployment:

Cloud Migration Accelerates Despite Security ConcernsOn-premises solutions retained 59.65% cognitive security market share in 2025 because defense agencies, financial institutions, and critical-infrastructure operators continue to mandate local data residency and air-gapped environments. However, cloud deployments are expanding at a 26.05% CAGR as hyperscalers integrate purpose-built telemetry collectors and model-integrity validation into their platforms, lowering entry cost. The cognitive security market size for cloud-based offerings is projected to rise steeply as subscription pricing and continuous threat-feed updates shorten procurement cycles and transfer capital expenditure into operating budgets.

Hybrid architectures now dominate new implementations, pairing edge inference nodes with central cloud analytics that feed global threat-intel graphs. Vendors pre-package reference blueprints that encrypt training data at rest while enabling secure compute enclaves for federated learning between on-prem and public-cloud zones. Security-operations centers benefit from unified dashboards that normalize detections across environments, closing visibility gaps that attackers exploit when workflows straddle multiple hosting models. These capabilities collectively position cloud variants as the principal expansion engine within the cognitive security market through 2031.

By Service:

Professional Services Lead Amid Skills ShortageConsulting and integration engagements captured 59.85% revenue share in 2025 because enterprises require customized data pipelines, model-validation frameworks, and regulatory mappings before cognitive controls deliver value. The cognitive security market size attributed to managed services is forecast to grow at a 27.8% CAGR as organizations outsource round-the-clock monitoring, model retraining, and adversarial-simulation exercises.

Specialist providers now bundle threat-hunting squads with MLOps engineers to maintain dynamic baselines tuned to each client’s evolving risk profile. Government contracts such as the USD 2 billion NSIN task order awarded to GovCIO illustrate how public agencies leverage external expertise to accelerate acquisition timelines while meeting classified accreditation requirements. Commercial buyers mirror this pattern, shifting budget from headcount to outcome-based subscriptions that guarantee detection-accuracy service-level agreements. The managed-services boom is therefore a structural, not temporary, phenomenon underpinning the growth trajectory of the cognitive security market.

By Application:

Automated Compliance Drives Market LeadershipAutomated compliance management retained 44.65% of the cognitive security market size in 2025 as ESG, privacy, and AI-safety mandates multiplied. Engines ingest operational logs, extract relevant events, and auto-populate regulatory reports, reducing manual audit prep times by 70% while lowering fines for late or inaccurate disclosures. Predictive maintenance in industrial sectors is the fastest-growing application, expanding at a 29.42% CAGR because machine-learning models detect impending equipment failures and pre-empt disruptions that would otherwise attract cyber-physical sabotage attempts.

Cross-investigation analytics gain traction in multinational corporations where attack campaigns span cloud tenants, SaaS apps, and operational technology. By correlating weak signals—such as anomalous inference latency or sudden prompt-format shifts—AI composes new hunting hypotheses that human analysts evaluate, accelerating root-cause analysis and incident containment. Vendors further embed explainable-AI modules to satisfy EU transparency provisions, reinforcing buyer trust and setting higher entry barriers for point-solution challengers. These developments sustain automated compliance as the revenue anchor while broadening adjacent use cases that propel the overall cognitive security market.

By End-User Industry:

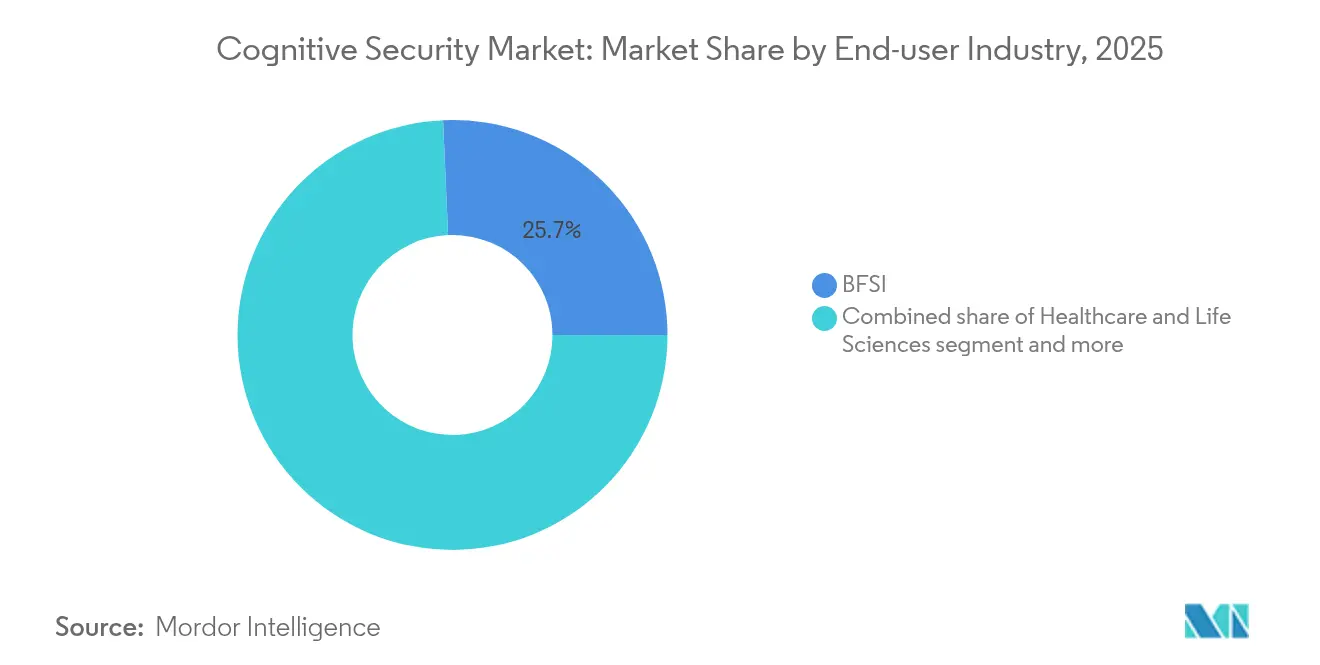

BFSI Leads Government Investment SurgeBanks, insurers, and capital-markets firms adopt advanced models to detect insider fraud, transaction anomalies, and rogue-trading patterns. Stringent regulatory capital and data-protection obligations make AI-driven controls mandatory rather than discretionary. Defense agencies follow closely, leveraging artificial intelligence to patrol open-source intelligence feeds, secure weapons-system software, and vet third-party suppliers.

Healthcare entities deploy privacy-preserving analytics that flag anomalous EHR access and validate AI-diagnostic suggestions against ground-truth labels, balancing innovation with strict patient-data protections. Manufacturing plants integrate model-based intrusion detection into programmable-logic controllers, shoring up operational resilience amid growing geopolitical cyber sabotage threats. Retailers and telecom operators harness cognitive engines to combat synthetic-identity fraud, automate KYC compliance, and secure 5G edge nodes at scale. Collectively, these industry-specific mandates ensure a diversified demand base that insulates the cognitive security market from single-vertical downturns.

By Component:

Solutions Dominate Integration ComplexityIntegrated platforms bundle dataset-sanitization, model-integrity checks, continuous attack-surface discovery, and security-orchestration playbooks. Buyers prefer these suites over stitching together disparate point tools that may not share ontology or support common policy schemas. The cognitive security market thus tilts toward vendors able to supply end-to-end pipelines, supported by plug-in ecosystems that extend into specialized niches like generative-AI watermark detection or synthetic-data governance.

Service components reinforce this dynamic by offering migration factories that port legacy detection rules into AI-native formats and by conducting continuous validation against evolving adversarial tactics. As acquisition activity accelerates, platform providers integrate recent purchases to broaden capability coverage, shrinking time-to-value for customers who face mounting compliance deadlines.

Geography Analysis

North America Cognitive Security Market

North America remains the largest regional cluster, holding 35.25% cognitive security market share in 2025. State and federal agencies allocate multibillion-dollar budgets to safeguard critical infrastructure, exemplified by the USD 2 billion Department of Defense NSIN task order and the USD 185 million F-35 cybersecurity support contract. Enterprises face an equally complex environment as AI-specific risk-management rules emerge alongside existing data-privacy statutes, raising compliance overhead yet simultaneously expanding addressable spend for platform vendors. Venture funding remains abundant, sustaining a pipeline of startups that commercialize niche capabilities such as prompt-injection testing and autonomous red-teaming. Nevertheless, growth rates moderate relative to emerging regions because many Fortune 1000 firms have already executed first-generation AI-security programs and now focus on incremental optimization rather than green-field rollouts.

APAC Cognitive Security Market

Asia-Pacific records the fastest trajectory at a 24.95% CAGR. Government programs in China, Singapore, and South Korea promote AI adoption while investing in national cybersecurity centers that procure local and international technology. Rapid digital-payment expansion and smart-city rollouts generate enormous telemetry volumes, providing fertile data for machine-learning-driven defenses but also luring cybercriminal syndicates that weaponize automated reconnaissance. Enterprises therefore prioritize AI-native security from the outset rather than layering it later, shortening sales cycles for full-stack platforms. Linguistic diversity and regulatory heterogeneity pose integration hurdles, yet hyperscalers’ growing regional footprints alleviate infrastructure constraints, reinforcing demand for scalable cognitive controls.

Europe Cognitive Security Market

Europe advances steadily as the EU AI Act transforms ambiguity into prescriptive obligations around transparency, robustness, and data governance. While compliance costs elevate project complexity, the legislative clarity encourages board-level approval for long-term investments in explainable-AI security. Vendors localize dashboards and audit trails to meet region-specific reporting schemas, and many offer sovereign-cloud options hosted in accredited data centers to respect cross-border transfer restrictions. Uptake is especially strong in Germany’s manufacturing heartland and France’s aerospace and defense sector, where cyber-physical risks intersect with intellectual-property protection imperatives. Together these factors ensure Europe remains a strategic revenue pillar for the cognitive security market, even if growth percentages trail Asia-Pacific’s breakneck pace.

Regulatory Landscape

Cognitive security procurement and design are increasingly shaped by AI-specific requirements layered onto broader cybersecurity and privacy regimes. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) tightens obligations for high-risk AI systems around accuracy, robustness, and cybersecurity, explicitly elevating controls that address data poisoning, model poisoning, and adversarial examples. This aligns closely with core cognitive security capabilities such as model-integrity monitoring and dataset lineage controls.

In the United States, federal standard-setting and consultation processes are also pushing cognitive security toward measurable lifecycle controls. In January 2026, the US Department of Commerce published an RFI on security considerations for AI agent systems (responses due March 9, 2026), reinforcing regulator focus on secure development and deployment for agentic workflows. Standards bodies such as ETSI (for example, EN 304 223) also influence common control baselines and conformity pathways by setting technical cybersecurity requirements for AI models and systems, which map into EU compliance expectations and support demand for auditable, policy-driven security automation.

Value Chain Analysis

The cognitive security value chain starts with upstream inputs that determine detection quality and compliance readiness, including security telemetry (identity, endpoint, network, cloud, OT), threat intelligence, and curated datasets used to train and validate ML models. Buyers also account for the compute stack (cloud and specialized hardware) that supports training, inference, and high-volume analytics. Model and platform providers then deliver core capabilities such as anomaly detection, adversarial ML defenses, prompt and agent monitoring, and automated compliance evidence generation, typically exposed through APIs and integrated into SIEM/SOAR and MLOps pipelines.

Downstream, systems integrators and professional services firms carry out data engineering, policy mapping, and model validation to operationalize cognitive security. Managed security service providers run continuous monitoring, tuning, and adversarial testing for buyers constrained by AI/ML cyber-analytics talent. A key bottleneck sits in third-party AI services and pre-trained components, where training infrastructure and runtime controls are abstracted, limiting visibility into dependencies and increasing Nth-party risk. This supports emerging practices such as AI dependency mapping (AIBOM-style inventories) and governance for non-human identities (service accounts, API keys) used in agentic workflows. Distribution is led by cloud marketplaces and enterprise security sales channels, with procurement increasingly tied to auditability, data residency, and demonstrable controls across the full AI lifecycle.

Competitive Landscape

The cognitive security industry features a mid-level concentration as legacy cybersecurity giants, cloud hyperscalers, and AI-native specialists jostle for share. No single vendor exceeds 15% of global revenue, reflecting the breadth of customer requirements and the nascency of standard architectures. Platform providers differentiate through proprietary model-integrity checks, unified data fabrics, and low-code policy authoring that lowers administrative burden.

Acquisition momentum is strong. Palo Alto Networks’ USD 650-700 million purchase of Protect AI represents the largest transaction since 2020 and signals a strategic pivot toward full-stack AI assurance. Cisco announced its intent to absorb Robust Intelligence, integrating model-validation pipelines into the Cisco Security Cloud. Tenable’s planned acquisition of Apex Security illustrates how vulnerability-management vendors extend into model-security as customers demand unified asset inventories spanning traditional servers and AI endpoints. These moves compress point-solution niches, pressuring startups to specialize further or seek early exit opportunities.

Strategic alliances complement MandA. Cloud providers bundle security copilot agents directly into developer toolchains, creating sticky ecosystems that funnel downstream demand for partner applications such as threat-intelligence enrichment or automated incident response. Meanwhile, open-source communities collaborate on model-watermark standards and adversarial-example corpora that vendors incorporate into commercial offerings, accelerating innovation diffusion. Pricing competition remains moderate because the complexity of implementation favours value-based negotiations over commoditized licensing. As buyers pivot from pilot projects to enterprise-wide rollouts, vendors able to prove ROI through metrics such as dwell-time reduction or audit-hours saved win multi-year expansions, reinforcing a virtuous cycle that sustains the cognitive security market.

Cognitive Security Industry Leaders

IBM Corporation

Microsoft (Azure Synapse / Fabric)

Amazon Web Services

SAP SE

Darktrace plc

- *Disclaimer: Major Players sorted in no particular order

Cognitive Security Market Companies Covered in this Report

- IBM Corporation

- Microsoft Corp. (Azure)

- Amazon Web Services Inc.

- SAP SE

- Cisco Systems Inc.

- Trend Micro Inc.

- Broadcom Inc. (Symantec)

- Darktrace plc

- McAfee LLC

- LogRhythm Inc.

- Fortinet Inc.

- SAS Institute Inc.

- Splunk Inc.

- Google LLC

- Oracle Corp.

- Micro Focus Intl.

- Dell Technologies (EMC)

- Palantir Technologies

- CrowdStrike Holdings

- SAS Institute Inc.

Market Opportunities and Future Outlook

Operational security for AI agents and autonomous workflows is a clear whitespace area. Buyers need in-line controls that can measure, enforce, and prove secure development and deployment practices for agent systems, rather than focusing only on monitoring conventional IT assets. Government attention adds urgency: in January 2026, the US Department of Commerce issued an RFI on security considerations for AI agent systems (responses due March 9, 2026). That signal points to stronger agent governance, non-human identity control, and auditable safety mechanisms across build and run phases within enterprise security programs.

National and hyperscaler initiatives are also catalyzing spend around machine-speed vulnerability handling and remediation. This supports demand for platforms that combine model assurance with exploit validation and automated patch workflows. In May 2026, GCHQ outlined the Cyber Shield blueprint for national-scale defense integrating agentic AI, and in May 2026 Google Cloud launched an autonomous AI Threat Defense platform positioned around prioritizing real-world risks and faster remediation. Separately, US activity around AI-enabled vulnerability coordination, including the July 2026 Gold Eagle initiative linked to an AI-security executive order, reinforces demand for vendor capabilities that integrate open-source dependency risk, supply chain remediation workflows, and continuous compliance reporting in regulated verticals.

Recent Industry Developments in Cognitive Security Market

- June 2026: IBM joined OpenAI's Daybreak Cyber Partner Program to bring frontier AI into cyber defense workflows and introduced an application security service focused on vulnerability validation. The initiative strengthens IBM's positioning in agentic security operations, where AI assists triage and remediation across large code and asset estates.

- May 2026: IBM expanded its AI-powered security portfolio and highlighted ongoing Project Glasswing work with Anthropic focused on defending critical software infrastructure. IBM also extended IBM Concert with AI-driven vulnerability management capabilities, deepening coverage for software supply chain risk and aligning cognitive security platforms with faster, evidence-driven vulnerability prioritization and response.

- July 2024: IBM Consulting and Microsoft announced collaboration to help clients modernize security operations and address cloud identity threats. The partnership supports integrated deployments across Microsoft-centric environments, reinforcing demand for cognitive analytics that correlate identity, cloud, and workload signals at enterprise scale.

Cognitive Security Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the cognitive security market covers software and related services that use AI and machine learning to detect, analyze, and respond to cyber threats, including automated investigation, threat intelligence enrichment, and anomaly detection across digital environments.

Scope exclusions: We exclude general IT outsourcing, basic perimeter hardware that is not AI driven, and non-security analytics tools that do not support security operations outcomes.

Segments Covered in This Report

- By Deployment

- On-Premise

- Cloud-Based

- By Service

- Professional Services

- Managed Services

- By Application

- Cognitive Threat Intelligence

- Predictive Maintenance

- Cross-Investigation Analytics

- Automated Compliance Management

- Other Applications

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Retail and eCommerce

- Government and Defense

- Telecom and IT

- Manufacturing

- By Component

- Solutions

- Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the basic boundaries of what is counted and to build a clean set of input indicators before any modeling was done. We reviewed public materials such as cybersecurity guidance and incident reporting updates from agencies like NIST and CISA, plus regulatory and privacy direction from sources such as ENISA and the European Commission, which helps interpret adoption timing.

To anchor the demand pool, we also referenced illustrative data series like IT and digital economy indicators from the World Bank and OECD, and security and telecom related statistics from ITU, followed by company filings, earnings call transcripts, investor decks, and reputable press coverage on security budgets and AI deployments. Where needed, paid subscriptions were used for company financials and news intelligence, and for patent databases to understand how fast cognitive techniques are being productized. These are representative sources only, and we also used additional public and paid references for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating which parts of spending are actually budgeted as cognitive or AI driven security, and how it is purchased across enterprises, government users, and service providers. We spoke with a mix of solution leaders, channel and implementation partners, and security operations practitioners across APAC, EMEA, and the Americas, so pricing, deployment mix, and adoption pacing assumptions could be stress tested against how buyers run SOC and incident response workflows.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 38% |

| Mid tier: 55% | Functional/Unit leaders: 36% | EMEA: 37% |

| Smaller Players: 20% | Managers: 49% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where the broader cybersecurity and security software spend is reconstructed by region, then filtered using adoption indicators for AI enabled security use cases, including automated investigation and anomaly detection. We adjust for deployment mix and industry uptake, and then corroborate totals with selective bottom-up approximations such as sampled vendor revenue splits from filings, channel checks on deal size, and ASP times volume checks for common license and subscription constructs.

Key inputs used in the model include the installed base of cloud workloads and enterprise application footprints, SOC staffing pressure and incident response cycle times, AI adoption in business workflows that creates new monitoring needs, the shift toward subscription billing, and the observed price progression for AI features bundled into security platforms. For forecasting, scenario analysis is used first to reflect different breach intensity and regulation enforcement paths, then the final curve is refined using exponential smoothing on historical adoption patterns, aligned with what primary respondents expect for budget cycles. Where a bottom-up view is sparse, gaps are handled by applying conservative penetration ranges and then revisiting them during validation rounds.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final numbers do not rely on a single assumption. We compare modeled spend against independent signals such as public cloud growth, reported security investment priorities, and observed changes in software pricing, and then review outliers before sign-off.

If a variance is material, respondents are re-contacted to confirm whether it is driven by scope, timing, or a real market shift. Reports are refreshed annually, with interim updates when major events occur, and a final pre-delivery review is done so clients receive the most current view available at the time of release.

Mordor Intelligence's Cognitive Security Market Size Compared With Other Published Estimates

Different published market sizes for cognitive security can look far apart because the boundary between AI enabled security, general security analytics, and broader cybersecurity platforms is not drawn the same way by every publisher. The year used for currency conversion, the treatment of subscription price changes, and how quickly estimates are refreshed after large policy or threat events can shift totals up or down.

In practice, the key gap drivers are whether managed services are bundled into the same number, whether adjacent categories like generic SIEM or data analytics are counted in full, and whether assumptions like ASP progression are updated with fresh deal feedback or left static. When currency timing is shifted by even one year, and when AI feature pricing is assumed to rise faster than adoption, the same demand story can produce a noticeably different market value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 20.79 B (2026) | |

| Global Consultancy A | USD 25.73 B (2026) | Uses a broader scope that can pull in more of the security analytics stack and related services, and it may apply higher early-cycle price uplift assumptions for AI features in enterprise security bundles. |

| Industry Publisher B | USD 8.03 B (2025) | Starts from a narrower 2025 base that appears to emphasize specific cognitive security solution types, and the longer forecast horizon can dilute near-term adoption signals if refreshes are less frequent. |

The spread across the three figures is mainly explained by scope boundaries and timing choices rather than a disagreement about how quickly the space is growing. By refreshing conversion timing and subscription ASP assumptions close to publication, and then re-checking them with field feedback, Mordor Intelligence keeps the 2026 value tied to what buyers and providers describe as cognitive security spend instead of adjacent analytics spend.

Key Questions Answered in the Report

What is the current value of the cognitive security market?

The market is valued at USD 20.79 billion in 2026 and is projected to reach USD 55.27 billion by 2031.

Which deployment model is expanding fastest?

Cloud-based cognitive security platforms are advancing at a 26.05% CAGR through 2031 due to scalability and ongoing threat-feed updates.

Why does automated compliance dominate application spending?

ESG, privacy, and AI-safety mandates drive organizations to automate evidence collection and reporting, giving automated compliance a 44.65% revenue share in 2025.

Which region will grow the most over the forecast period?

Asia-Pacific leads with a 24.95% CAGR, spurred by national AI programs and rapid digital-service adoption.

How are vendors addressing the AI/ML talent shortage?

Providers bundle managed services that supply 24/7 monitoring, model retraining, and adversarial simulation, enabling clients to offset internal staffing gaps.

Page last updated on: