Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

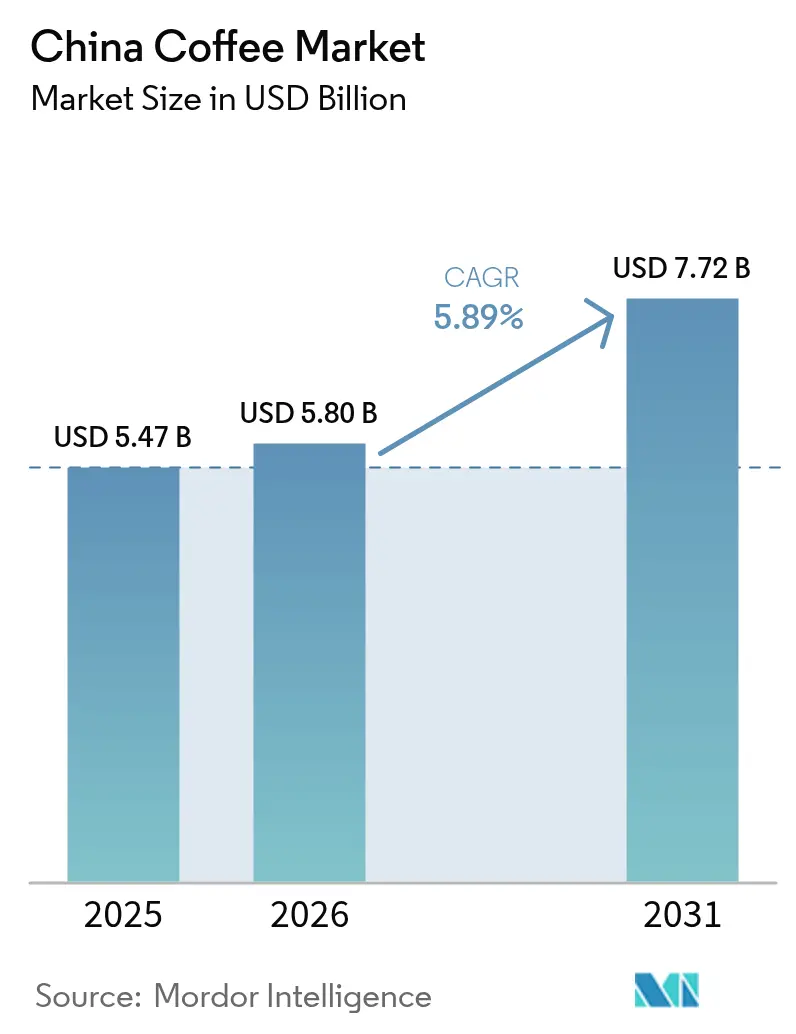

| Base Year Market Size (2025) | USD 5.47 Billion |

| Market Size (2026) | USD 5.80 Billion |

| Market Size (2031) | USD 7.72 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Coffee Market Analysis by Mordor Intelligence

The China coffee market size was valued at USD 5.47 billion in 2025 and is estimated to grow from USD 5.80 billion in 2026 to reach USD 7.72 billion by 2031, at a CAGR of 5.89% during the forecast period (2026-2031). Sustained urbanization, higher disposable incomes, and shifting lifestyle preferences continue to pull consumers toward coffee as a modern alternative to traditional tea. Besides, government trade-in programs that subsidize coffee machines, along with a 32.5% year-on-year surge in coffee imports in 2024 as per the USDA, underscore policy-led demand creation. In China's coffee market, domestic brands implement data analytics to identify growth opportunities in lower-tier cities, facilitating systematic store expansion and market penetration. The market demonstrates increased premiumization through specialty coffee products, single-origin selections, and specific brewing methods that meet consumer requirements. Multinational suppliers increase market competitiveness through investments in local research and development, modifying flavor profiles, packaging, and product formats according to Chinese consumer preferences. These operational strategies in expansion and product development transform the competitive environment and extend coffee consumption beyond major urban markets.

Key Report Takeaways

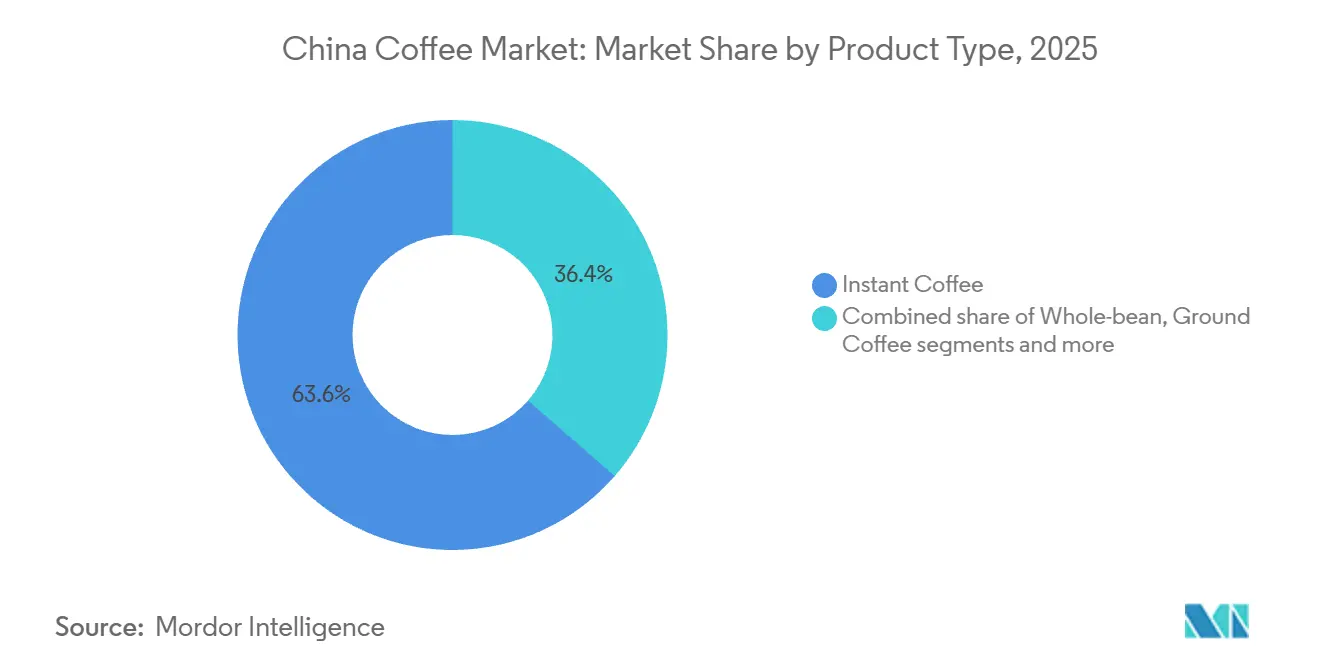

- By product type, instant coffee held 63.61% of the Chinese coffee market share in 2025, whereas coffee pods and capsules formats are projected to expand at a 9.89% CAGR through 2031.

- By flavor, plain variants commanded 59.94% revenue share in 2025; flavored coffee is set to grow at a 6.44% CAGR to 2031.

- By category type, conventional offerings accounted for 78.35% of the China coffee market size in 2025, while specialty (organic/single-origin) lines are advancing at a 6.97% CAGR.

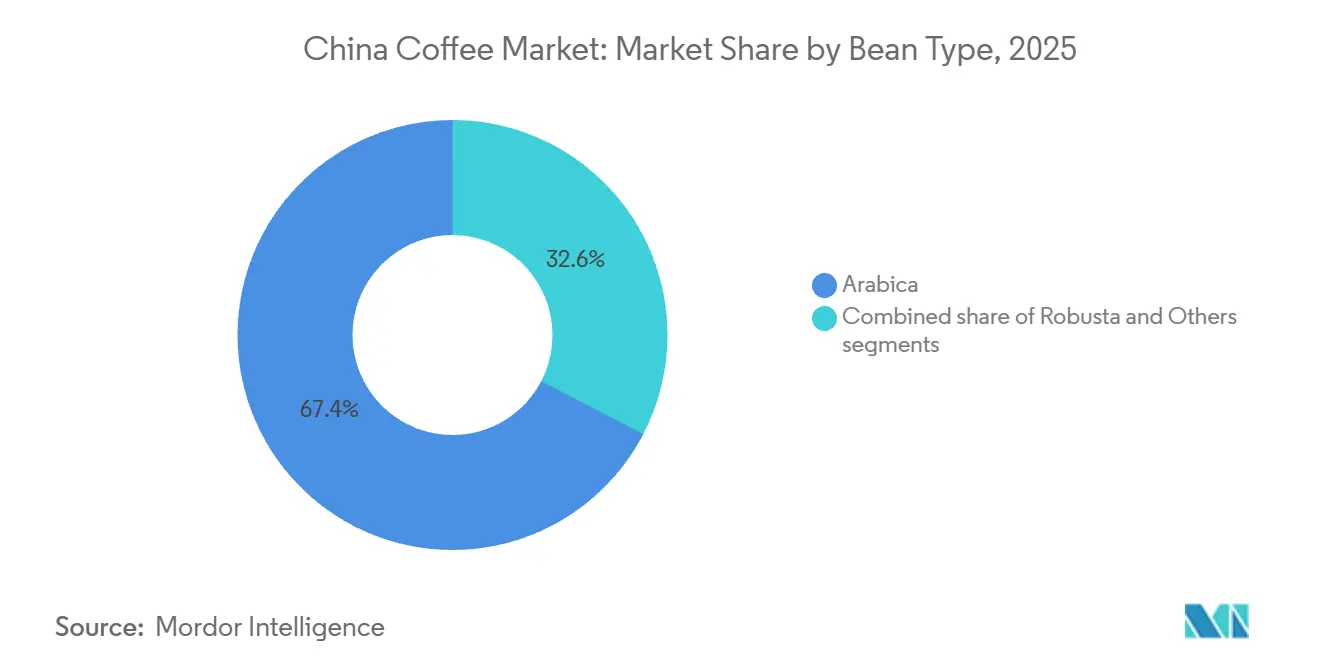

- By bean type, arabica beans led with 67.38% share in 2025; others usage is forecast to rise at a 5.99% CAGR thanks to cost-optimization in instant blends.

- By distribution channel, off-trade retail captured 83.00% of 2025 sales, whereas on-trade venues are growing at a 6.79% CAGR due to emerging café culture.

- By geography, Eastern China delivered 43.30% of the 2025 value, yet Northern China are on track for a 6.09% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising interest in specialty, gourmet, and artisanal coffee | +1.2% | Eastern and Southern China, with spillover to tier-2 cities | Medium term (2-4 years) |

| Expansion of café culture | +1.5% | National, with early gains in Shanghai, Beijing, Guangzhou | Long term (≥ 4 years) |

| Increasing popularity of homegrown brands | +0.9% | National, particularly strong in lower-tier cities | Short term (≤ 2 years) |

| Rising preference for convenience | +1.1% | Global, concentrated in urban centers | Medium term (2-4 years) |

| Government incentives for Yunnan coffee farming | +0.7% | National production, regional consumption benefits | Long term (≥ 4 years) |

| Growing health and wellness trends | +0.8% | Eastern China core, expanding to Southern regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising interest in specialty, gourmet, and artisanal coffee

The wave of premiumization is transforming the coffee market in China, as consumers increasingly demand specialty, gourmet, and artisanal coffee. This shift is driven by a strong preference for unique flavor profiles and compelling origin stories. Yunnan province leads this transformation, supported by government targets to achieve a 30% specialty coffee rate and an 80% deep processing rate by 2024, fostering higher quality and local innovation. Major international brands, such as Starbucks and Costa Coffee, have expanded their premium offerings, while domestic players like Luckin Coffee and Tim Hortons are innovating with regionally-inspired beverages, blending coffee with teas and fruits to align with Chinese preferences. Nestlé’s launch of six new products in April 2024, including the innovative “Guoran Light Coffee” fruit tea, demonstrates how established brands are adapting to local tastes while maintaining global standards. Premiumization is particularly evident in Eastern China’s tier-1 cities, where consumers are willing to pay a premium for experiences rooted in craftsmanship, storytelling, and quality sourcing. The café culture is thriving, with demand for artisanal brews, signature drinks, and environments that enhance social interactions. Local roasting capacity and research and development investments, particularly from brands like Soulmade Coffee in Shenzhen, are increasing to develop China-specific flavor profiles that combine international expertise with traditional tastes. This growth is fueling product diversification and advancing consumer education. The convergence of government support, brand innovation, and evolving urban consumer expectations is reshaping the coffee landscape into one of the most dynamic premium coffee markets globally.

Expansion of café culture

The rapid expansion of café culture in China has resulted in the establishment of nearly 12,000 new coffee shops over the past year, bringing the total number of outlets to approximately 67,000 by the end of 2024. This growth extends beyond major metropolitan areas to include emerging "new first-tier" cities, where younger and working-class consumers are driving demand for affordable and convenient coffee options. Local chains, such as Nowwa Coffee, are spearheading this expansion. Operating over 2,000 outlets with compact store formats in convenience stores and hotels, Nowwa targets office workers and service industry employees who previously relied on energy drinks. Government support for local coffee, particularly beans from Yunnan province, has further strengthened domestic coffee culture and encouraged its integration into daily life. However, the market faces increasing challenges, including saturation and intense price competition, which have driven a 14% decline in average coffee prices in 2024. To remain competitive, many coffee chains are diversifying their offerings by incorporating tea drinks, snacks, and culturally themed beverages, enhancing their social media presence and local relevance. This shift reflects broader changes in Chinese consumer behavior, where coffee is increasingly perceived as both a social and functional beverage. As a result, global and domestic brands are adapting their strategies to navigate a fast-growing yet highly competitive market. The evolving café culture is a critical driver of growth in China's coffee market and is reshaping consumption patterns across urban areas.

Increasing popularity of homegrown brands

Domestic coffee brands in China are rapidly strengthening their market position, driven by aggressive expansion strategies and localized product offerings that align with consumer preferences. Luckin Coffee, for example, operates over 22,000 stores across China as of 2024, utilizing an asset-light franchise model and quick innovation cycles to consistently introduce new beverages and maintain customer engagement [1]Source: Luckin Coffee Inc., "Luckin Coffee Announces Fourth Quarter and Fiscal Year 2024 Financial Results", luckincoffee.com . Cotti Coffee, which has surpassed Starbucks in store count, exemplifies the competitive intensity among local players. These brands excel in catering to Chinese tastes by offering larger serving sizes, incorporating traditional ingredients into innovative flavors, and implementing pricing strategies that make premium coffee more accessible to middle-income consumers. Their strategic focus on lower-tier cities, where global chains have limited penetration, enables them to establish early market dominance. This localized approach, combined with rapid store expansion and effective digital marketing, allows domestic brands to capture a diverse consumer base. The success of these companies reflects a broader trend in China’s coffee market, where strong domestic leadership complements rather than competes with international brands, reshaping consumption patterns nationwide. This trend aligns with government support for domestic industry growth and increasing consumer demand for culturally relevant coffee experiences. Such strategic positioning ensures the sustained growth of homegrown brands in China’s fast-expanding coffee market.

Government incentives for Yunnan coffee farming

Government support has established a robust foundation for sustainable growth in Yunnan's coffee industry, which accounted for over 98% of China's coffee cultivation and production as of 2023 [2]Source: State Council Information Office of China (SCIO), "SCIO briefing on taking solid steps to promote high-quality development in Yunnan", english.scio.gov.cn . Local policies prioritize modern agricultural practices and specialty coffee varieties, aligning with national objectives of food security and rural revitalization. Efforts such as identifying optimal coffee-growing zones and introducing high-quality coffee varieties have driven premium production rates. By 2024, the specialty coffee ratio is expected to reach 30%, with deep processing achieving 80%. Baoshan’s “Thousand, Hundred and Ten thousand Project” integrates coffee estates, shops, and farmers, strengthening the supply chain. These measures enhance coffee quality and market competitiveness while fostering technology transfer and advanced cultivation techniques. Partnerships, particularly with Brazilian exporters, ensure supply continuity amid global market fluctuations. Supported by training programs and research centers, Yunnan’s coffee sector is shifting from raw bean exports to value-added, premium products. This transformation positions China as a key player in the global coffee industry while driving rural economic growth and sustainability. A comprehensive policy framework is critical to establishing Yunnan’s coffee production as a high-quality, globally recognized brand within China’s growing coffee market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in global coffee bean prices | -0.8% | National, with higher impact on import-dependent regions | Short term (≤ 2 years) |

| Persistent health concerns over caffeine | -0.5% | National, stronger in rural and elderly demographics | Medium term (2-4 years) |

| Stringent food safety and regulatory compliance | -0.6% | National, particularly affecting importers and processors | Long term (≥ 4 years) |

| Strong cultural preference for tea in rural areas | -0.9% | Rural regions and smaller cities nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in global coffee bean prices

Fluctuations in global coffee bean prices present significant challenges for businesses operating in the Chinese coffee sector, exerting pressure on profit margins in an intensely competitive market. In 2023, China, the world's fifth-largest coffee importer, brought in coffee worth over 1.1 billion USD as per the China Food, Native Produce and Animal Products Import and Export Chamber of Commerce. This makes the nation's coffee sector especially susceptible to supply disruptions from leading coffee-producing countries. Adding to this vulnerability, the General Administration of Customs of China (GACC) mandates stringent registration for coffee beans, classifying them as medium to high-risk foods [3]Source: General Administration of Customs of China (GACC), "How Food Products Expot to China", china-gacc.agency. This classification requires importers to navigate rigorous documentation and testing, complicating and increasing their costs. Intense price competition among domestic brands has driven down the average price of a coffee cup. In response, companies like Luckin Coffee and local roasters are diversifying their sourcing strategies and forging direct ties with coffee-producing regions, aiming for stable supply chains. However, these strategic investments come with hefty capital demands and a long-term commitment, necessitating a balance between ensuring quality and managing costs. The persistent price volatility highlights the critical need for supply chain resilience and strategic procurement in China's burgeoning coffee market. As consumer demand surges and brands vie for relevance and profitability, these challenges act as a significant restraint on market expansion, urging innovative sourcing and operational management strategies.

Strong cultural preference for tea in rural areas

Traditional tea consumption in rural China remains a deeply entrenched cultural norm, creating a significant challenge for coffee adoption despite the rapid growth of coffee culture in urban areas. Rural consumers continue to favor tea due to longstanding cultural heritage and established consumption habits, with older generations particularly resistant to coffee as a daily beverage. This preference is further supported by the economic importance of tea production and consumption in these regions, where millions of tea consumers contribute to its role as a staple in daily life and social customs. Although urbanization and the migration of younger professionals to smaller cities are gradually introducing coffee culture to these untapped markets, tea continues to dominate rural beverage preferences. The emergence of rural cafés, however, is beginning to shift local perceptions, as younger demographics show increasing openness to coffee experiences. While the strong cultural preference for tea remains a key restraint on coffee market penetration, demographic shifts and exposure to new lifestyles suggest this resistance may diminish over time, creating opportunities for the gradual expansion of coffee consumption beyond urban hubs. Companies such as Luckin Coffee and local café initiatives are exploring these opportunities by adapting their offerings to align traditional preferences with the growing coffee trend. This evolving dynamic highlights the complex interplay of tradition and modernity, which is critical to the development of China’s coffee market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instant Coffee Dominance

In 2025, instant coffee accounts for a dominant 63.61% market share, driven by strong consumer demand for convenience and affordability. However, the coffee pods and capsules segment is witnessing rapid growth, with a projected CAGR of 9.89% through 2031. This growth is attributed to advancements in cold chain logistics and the increasing pace of urban lifestyles. Coffee pods and capsules represent a premium category with significant growth potential, as evidenced by Nespresso's success through localized product adaptations and larger serving sizes designed to meet consumer preferences. The shift from instant to fresh coffee formats underscores a broader trend toward premiumization, with fresh coffee's market share steadily increasing.

Millennials and Gen-Z in China are driving the instant coffee market by favoring trendy, modern beverages that align with their fast-paced and experiential lifestyles. These younger consumers are increasingly choosing convenient formats over traditional tea rituals. Data from the International Coffee Organization (ICO) supports this trend, showing rapid annual growth in China's coffee consumption over the past decade. As a result, China is the largest coffee consumer globally, based on import and derived figures, with younger demographics leading this growth in urban areas.

By Flavor: Plain Varieties Lead with Flavored Innovation Accelerating

Plain coffee variants hold a significant 59.94% market share in 2025, highlighting the strong consumer preference for traditional flavors and the continued dominance of instant coffee consumption. On the other hand, the flavored coffee segment is experiencing robust growth, with a projected CAGR of 6.44% through 2031. This growth is driven by the introduction of innovative products that cater to local taste preferences and incorporate seasonal ingredients. For instance, Nestlé's launch of "Guoran Light Coffee," China's first coffee fruit tea, along with citrus-infused variants in 2024, exemplifies how companies are strategically blending coffee with familiar flavors to enhance market penetration. The flavored coffee segment also benefits from the increasing willingness of younger consumers to experiment with new taste profiles, coupled with the influence of social media in promoting unique and engaging beverage experiences.

Local brands, such as Luckin Coffee, have effectively utilized flavor innovation as a competitive strategy, frequently introducing limited-time offerings that generate excitement among consumers and drive social media engagement. This trend toward flavor diversification aligns with broader shifts in Chinese food culture, where fusion concepts and international influences are becoming more widely accepted. Seasonal and festival-themed flavors have emerged as particularly effective in maintaining consumer interest, enabling brands to drive repeat purchases through limited-availability marketing campaigns that create a sense of urgency and exclusivity.

By Category Type: Conventional Dominance with Specialty Acceleration

Conventional coffee continues to dominate with an 78.35% market share in 2025, driven by the cost-conscious behavior of consumers and the widespread preference for instant coffee formats. In contrast, the specialty coffee segment, which includes organic and single-origin varieties, is experiencing robust growth, with a projected CAGR of 6.97% through 2031. This growth reflects a clear shift toward premiumization and evolving consumer preferences for higher-quality products. Government initiatives in Yunnan province, aimed at achieving a 30% specialty coffee production rate in 2024, are strengthening domestic supply chain capabilities to support the premium coffee segment. The specialty coffee market is further propelled by increasing health and environmental awareness among urban consumers, particularly in tier-1 cities where higher disposable incomes enable the adoption of premium-priced products.

Global coffee brands are intensifying their focus on the specialty segment by making substantial investments in research and development. Many companies are establishing local research and development centers to create premium offerings tailored to the Chinese market, combining global expertise with local flavor preferences. Additionally, the expansion of independent coffee shops and the growing influence of third-wave coffee culture, which emphasizes factors such as origin, processing techniques, and brewing methods, are driving the specialty coffee market. This trend offers significant opportunities for both domestic and international players to differentiate themselves through superior quality, sustainability initiatives, and unique flavor profiles, enabling them to command premium pricing in an increasingly competitive landscape.

By Bean Type: Arabica Leadership with Robusta Cost Optimization

Arabica beans hold a commanding 67.38% share of the market in 2025, driven by their superior flavor profiles, which make them the preferred choice in premium and specialty coffee segments. On the other hand, others varieties are projected to grow at a robust 5.99% CAGR through 2031. This growth is fueled by their cost-effectiveness and suitability for instant coffee production, aligning with cost optimization strategies adopted by industry players. In China's domestic coffee production, Yunnan province primarily focuses on Robusta beans for instant coffee applications, while high-altitude regions in the area produce high-quality Arabica varieties catering to specialty coffee markets. The segmentation of bean types reflects broader market dynamics, with arabica supporting premiumization trends and robusta driving price competitiveness.

Import diversification strategies are playing a pivotal role in strengthening supply chain resilience and enhancing price negotiation capabilities. The number of coffee import sources in China has increased significantly, rising from 31 in 1995 to 75 currently. Brazilian coffee exporters have capitalized on this trend, significantly increasing their shipments to the Chinese market. Additionally, the growing consumer awareness in China regarding coffee origins and processing methods has created opportunities for other bean varieties, including specialty cultivars and experimental types, to gain traction in the market.

By Distribution Channel: Off-Trade Dominance with On-Trade Expansion

Off-trade channels hold a dominant 83.00% market share in 2025, primarily driven by the strong presence of supermarkets, hypermarkets, and the growing influence of online retail platforms. On-trade venues are experiencing robust growth, with a projected CAGR of 6.79% through 2031. This growth is attributed to the expansion of café culture and the increasing establishment of coffee shops in non-traditional locations. E-commerce has emerged as a critical driver of market growth, with platforms such as Tmall witnessing significant expansion in the coffee category. However, while fresh coffee alternatives are gaining traction, the instant coffee segment is facing challenges. Specialty stores are capitalizing on premiumization trends, while convenience stores are diversifying their coffee offerings to cater to the rising demand for on-the-go consumption.

The distribution landscape is undergoing rapid transformation, driven by digital integration. According to World Coffee Portal, over 85% of consumers utilize mobile platforms like WeChat and Meituan for ordering and delivery, highlighting the increasing reliance on digital solutions. Luckin Coffee's strategic franchise expansion into high-traffic, non-traditional locations such as hospitals and gas stations exemplifies how brands are enhancing accessibility to capture consumer demand. Online retail channels are particularly significant for premium and specialty coffee products, where detailed product descriptions and customer reviews play a crucial role in influencing purchasing decisions. The integration of online and offline channels through omnichannel strategies has become a key competitive differentiator in the dynamic retail environment.

Geography Analysis

Eastern China is projected to account for a significant 43.30% share of the national coffee market in 2025, supported by high urbanization levels and a well-established coffee culture in key cities such as Shanghai and Beijing. This mature market is characterized by a strong presence of premium and specialty coffee segments, driving demand for both international brands and domestic companies catering to an affluent and discerning consumer base. Jiangsu province serves as a key coffee import and distribution hub, ensuring supply for the region's advanced coffee consumption trends.

Northern China represents the fastest-growing coffee market region, with a projected CAGR of 6.09% through 2031. The region remains a developing market with significant growth potential but exhibits growth rates below the national average due to persistent tea preferences and relatively lower urbanization levels in certain areas. Government initiatives aimed at promoting domestic consumption and improving infrastructure are expected to enhance market development by improving distribution and accessibility. While coastal cities have more readily adopted international coffee culture, inland and rural areas continue to favor traditional beverages. However, the emergence of rural cafés and the expansion of domestic brands into lower-tier cities are gradually increasing coffee's reach. This creates opportunities for both domestic and international players who can adapt their strategies to local tastes and consumption habits. As a result, regional variations in coffee consumption patterns require customized market approaches and distribution strategies. Domestic companies, such as Luckin Coffee, have expanded their presence across regions to address evolving consumer preferences and broaden their market reach. The growth of café culture beyond major cities and the success of local brands in smaller urban areas highlight the market's evolution, where a deep understanding of regional dynamics is crucial for sustained growth.

Southern China, spearheaded by Guangdong province, experiences growth driven by the province's economic development and its proximity to Hong Kong, a city with a strong international coffee culture that shapes local preferences. This dynamic market demonstrates a growing demand for varied coffee formats and experiences, supported by global flagship stores and innovative local brands addressing the changing tastes of consumers in this economically active region. Additionally, the region benefits from a robust supply chain and increasing investments in coffee-related infrastructure, further enhancing its position as a key market for coffee consumption and innovation.

Regulatory Landscape

China's coffee market operates under an increasingly formalized framework spanning import controls, food safety, and product and quality standards. On the import side, the General Administration of Customs of China (GACC) tightened compliance requirements for overseas food facilities through Decree No. 280, which entered into force in June 2026 and updated registration and administrative procedures for imported foods. This affects coffee bean and processed coffee suppliers shipping into China. In May 2026, GACC also moved to widen raw material sourcing optionality by announcing that, from July 20, 2026, eligible coffee beans from 53 African countries with diplomatic ties to China can access the market under streamlined quarantine and phytosanitary requirements.

On domestic standardization, 2025 saw multiple coffee-specific standards released that raise the bar on labeling, origin positioning, and processing practices. These include the Ministry of Agriculture and Rural Affairs industry standard NY/T 289-2025 (Green Food Coffee, effective May 2025), the national standard GB/T 45690-2025 (Geographical Indication Product Quality Requirements: Pu'er Coffee, effective September 2025), and group standards such as T/CFMA 05-2025 for coffee bean roasting production technical specifications (effective July 2025) and T/CSBX 0033-2025 for super instant coffee (effective September 2025). Taken together, these measures increase documentation, testing, and traceability expectations for both importers and domestic processors, shaping formulation, sourcing, and packaging decisions.

Value Chain Analysis

The China coffee value chain starts with upstream bean supply that blends imports with domestic cultivation, then moves through roasting and processing, packaging, distribution, and finally on-trade and off-trade sales. Imported beans remain important for scale and blend consistency, with Brazil a key origin in multi-year procurement strategies. Domestic production is concentrated in Yunnan (the core producing province), with smaller contributions from Hainan, supported by local programs that push higher quality grades and deeper processing. A clearer move toward long-term sourcing and scale procurement is evident in Luckin Coffee's agreements to purchase 120,000 tons from Brazil over two years (June 2024) and its subsequent memorandum with ApexBrasil for 240,000 tons over five years valued at 10 billion yuan (November 2024).

Midstream capabilities are expanding through regional roasting hubs and technology-led operations that improve throughput, consistency, and compliance, while downstream is shaped by omnichannel retail and delivery. Cold-chain and temperature-controlled storage remain key constraints for fresh and premium formats, and for maintaining ready-to-drink and chilled offerings, which increases last-mile fulfillment costs. At the same time, large chains are adding digital tools to manage sustainability and operational control across the chain, illustrated by Starbucks China's July 2026 collaboration with Envision Group to use the EnOS Ark digital carbon management platform across its supply chain. Standards such as NY/T 289-2025 also reinforce structured quality requirements at the farm and primary processing layer, influencing procurement specifications and supplier qualification.

Competitive Landscape

The competitive landscape of China's coffee industry is undergoing notable changes, influenced by shifting market dynamics and evolving consumer preferences. The market is moderately consolidated, with established international brands facing strong competition from emerging domestic players. Starbucks, previously a dominant player, has seen a decline in market share, while Luckin Coffee has become the market leader, operating over 22,000 stores nationwide as of 2024. Reflecting the challenging environment for global brands, Starbucks is reportedly considering selling a stake in its China business. Initial discussions have included over a dozen potential investors, such as Hillhouse Capital Group, FountainVest Partners, and Trustar Capital.

Technology adoption and digital integration have become critical success factors in this competitive market. Leading players are leveraging mobile platforms, advanced data analytics, and supply chain optimization to enhance operational efficiency and strengthen customer engagement. Luckin Coffee's dominance can be attributed to its digital-first strategy, which includes technology-driven store management and personalized engagement initiatives that resonate with younger Chinese consumers. Additionally, rural markets and lower-tier cities present significant growth opportunities. Coffee brands are increasingly adopting cooperative models and partnering with local entrepreneurs to expand café networks and stimulate tourism.

Emerging disruptors such as Cotti Coffee is aggressively pursuing store expansion and franchise growth, supported by recent funding rounds and reduced investment barriers for franchisees. Meanwhile, the regulatory environment continues to evolve, with updated food safety standards introduced by China’s National Health Commission and State Administration for Market Regulation (GB 7718-2025 for labeling and GB 2760-2024 for additives). Companies with strong compliance frameworks and traceability systems are better positioned to navigate these regulatory changes and capitalize on opportunities in premiumization and exports.

China Coffee Industry Leaders

-

Nestlé S.A.

-

Starbucks Corporation

-

Luckin Coffee Inc.

-

Saturnbird Coffee

-

illycaffè Shanghai Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Scale investments in processing infrastructure and shifts in operating models are creating room for suppliers of beans, ingredients, packaging, and technology that can support faster and more controlled supply chains. In April 2026, Luckin Coffee commissioned a RMB 3 billion smart roasting center in Qingdao, and it has positioned this facility as part of a broader network that lifts combined roasting capacity across multiple sites to over 155,000 tons. This strengthens domestic roasting and distribution efficiency for instant, RTD, and fresh coffee formats. In parallel, Starbucks finalized a joint venture with Boyu Capital on April 2, 2026 to move its China retail operations toward a licensed model across about 8,000 stores, highlighting continued format expansion and the need for localized product development, store-level equipment, and last-mile delivery integration.

On the supply side, regulatory changes are widening sourcing corridors and supporting diversification strategies for roasters and instant coffee manufacturers. GACC's May 2026 announcement that eligible coffee beans from 53 African countries gain full quarantine access from July 20, 2026 reduces friction for new-origin sourcing and supports blend innovation and risk management amid global price volatility. Meanwhile, the rollout of product and process standards in 2025, including GB/T 45690-2025 for Pu'er coffee (effective September 2025) and NY/T 289-2025 for Green Food Coffee (effective May 2025), supports premium origin positioning and higher specification procurement, benefiting specialty, single-origin, and quality-assured instant segments. These developments also raise demand for testing, traceability systems, and standardized roasting and processing practices across domestic and imported supply chains.

Recent Industry Developments

- April 2026: Starbucks finalized a joint venture with Boyu Capital on April 2, 2026 to move its China retail operations toward a licensed model across about 8,000 stores. The deal points to continued scale expansion and the need for localized product development, store-level equipment, and last-mile delivery integration.

- April 2026: Luckin Coffee commenced operations at its RMB 3 billion smart roasting center in Qingdao, Shandong Province, with an annual roasting capacity of more than 55,000 tons. The facility strengthens in-country roasting scale and automation, tightening control over quality and cost while supporting faster replenishment to both on-trade and off-trade channels.

- April 2024: Nestle Coffee expanded its portfolio in Pu'er, Yunnan, adding multiple products spanning refreshment, flavor combinations, and health-oriented propositions, including Guoran Light Coffee (coffee fruit tea) and plant-based ready-to-drink options. It also intensifies innovation cycles in flavored and functional adjacent offerings across retail and cafe channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the China coffee market is defined as the value of coffee products sold in the country across retail and foodservice routes, covering common forms such as whole bean, ground, instant, and pods or capsules.

Scope exclusions: This sizing does not count coffee shop equipment, vending machines, or non-coffee beverages such as tea, cocoa, and energy drinks.

Segmentation Overview

-

By Product Type

- Whole-bean

- Ground Coffee

- Instant Coffee

- Coffee Pods and Capsules

- Ready-to-Drink (RTD) Coffee

-

By Flavor

- Plain

- Flavored

-

By Category Type

- Conventional

- Speciality (Organic/Single-Origin)

-

By Bean Type

- Arabica

- Robusta

- Others

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Supermarkets/Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Region

- Eastern China

- Southern China

- Northern China

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the basic demand and supply context before any assumptions were locked into the model. We relied on public data points that can be checked, such as import and export statistics for coffee and extracts, published agriculture and production notes, and customs trade classifications that help separate green coffee from processed formats.

On the demand side, we reviewed sources such as China Customs trade statistics, UN Comtrade, FAOSTAT, and public releases from organizations like the International Coffee Organization, along with peer reviewed papers on consumption patterns and brewing formats. We also used company filings, investor presentations, association websites, and reputed business press to understand pricing movement, route-to-market shifts, and expansion plans. Where needed, a paid subscription database was used for company financials, and a shipment-level import and export view helped sanity check the direction and scale of trade flows. The sources listed here are illustrative only, and many other public sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating consumption growth, price ladders, and channel mix, because these variables can move the final value quickly in China coffee. We spoke with a mix of brand, distribution, foodservice, and supply-side roles, and we also used short surveys to cross-check assumptions on product form splits, retail pricing behavior, and the pace of specialty and online penetration across major city clusters.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | |

| Mid tier: 53% | Functional/Unit leaders: 40% | |

| Smaller Players: 14% | Managers: 47% |

Market-Sizing & Forecasting

Our core sizing is built using a top-down demand pool reconstruction, where population and urbanization signals are combined with coffee consumption frequency and conversion to product volumes by form, and then priced using observed retail and foodservice price bands. To keep totals realistic, we corroborated the outcome with selective bottom-up checks based on sampled brand and channel price points, format mix, and a limited roll-up of leading supplier and distributor revenue disclosures where available.

Key inputs in the model include coffee import volumes by category (green, roasted, extracts), the split between instant and roast and ground formats, the on-trade versus off-trade share, average selling prices by form and pack size, and the growth pace of online retail versus modern trade. When signals disagreed, we kept the assumption that matched multiple indicators, such as trade movement plus price direction plus channel commentary from interviews.

For forecasting, scenario analysis was used, with a base case anchored to expected outlet expansion, household penetration, and price inflation assumptions reviewed with industry respondents. Where bottom-up validation was weaker, we used conservative coverage ratios and then cross-checked back to the total market value implied by consumption and trade, before finalizing the year-by-year series.

Data Validation & Update Cycle

Validation is done in layers so a single noisy data point does not drive the result. We compare the modeled value and volume outputs against independent signals like coffee trade totals, visible retail pricing ranges, and reported channel growth patterns, and then the variances are reviewed by another analyst before sign-off.

If an input moves sharply, such as an FX shift, a tariff change, or a sudden channel disruption, we re-contact relevant experts to confirm whether the shift is temporary or structural. Reports are refreshed annually, and interim updates are made when material events can change demand or pricing. Before delivery, an analyst does a fresh pass through recent public releases so clients receive the latest updated view.

Mordor Intelligence's China Coffee Market Sizing Compared With Other Published Estimates

Published market sizes for China coffee often do not match because the boundaries are not set the same way, and because pricing and channel assumptions vary more here than in mature markets. Differences usually come from what gets counted as coffee, how out-of-home spending is treated, and whether the value is built from consumption signals or from broader beverage revenue buckets.

Key gap drivers are mostly scope and price logic. Some estimates fold in cafe beverage spending more broadly, including add-ons and non-coffee drinks, which can push the total up quickly when store counts are rising. Others start from retail sales only, or apply a single average price that does not reflect the spread between instant, pods, and specialty beans. Depending on the base year currency timing, this can pull the value down or flatten the trend.

After the scope is kept consistent, the remaining spread mostly comes from how each publisher treats out-of-home value and how fast they let average prices rise in the forecast model.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.47 B (2025) | |

| Industry Publisher A | USD 22.72 B (2025) | This figure appears to use a wider revenue boundary that can include a larger share of foodservice spending and broader end-use coverage, which lifts the total beyond packaged coffee value alone. |

| Data Platform B | USD 24.61 B (2024) | The estimate is anchored to a different base year and may rely on aggregated category definitions and a single value build that blends product forms and channels, which can overstate the priced volume when mix shifts are not separated. |

Import and export movements by coffee category, observed price ladders across instant, roast and ground, and channel-level growth checks are the evidence points that keep Mordor Intelligence tied to a defined coffee product scope instead of a broader cafe revenue view. After the scope is kept consistent, the remaining spread mostly comes from how each publisher treats out-of-home value and how fast they let average prices rise in the forecast model.

Key Questions Answered in the Report

What is the current value of the China coffee market?

The market is valued at USD 5.80 billion in 2026.

Which product segment is expanding the quickest?

Coffee pods and capsules coffee leads with a projected 9.89% CAGR to 2031.

Which region shows the highest growth momentum?

Eastern China is forecast to post a 5.73% CAGR, outpacing the national average.

How significant are domestic brands in shaping demand?

Homegrown chains such as Luckin Coffee leverage digital franchising and localized flavors, rapidly expanding into lower-tier cities and capturing share from multinationals.

Page last updated on: