CMS Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

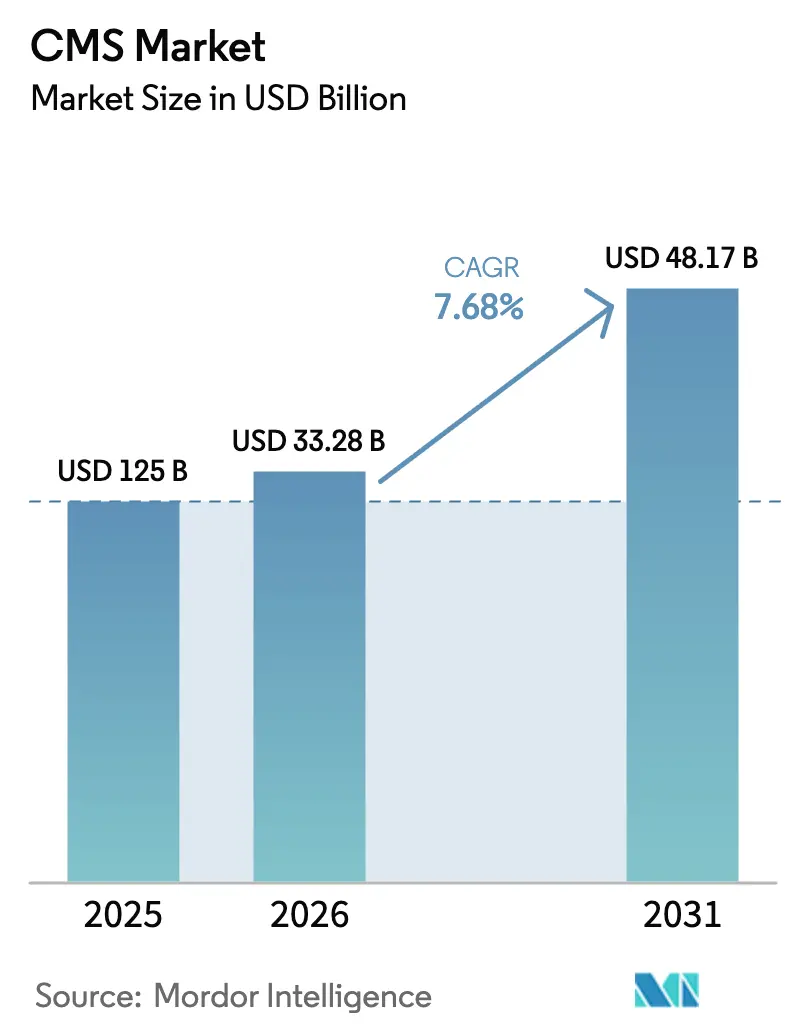

| Market Size (2026) | USD 33.28 Billion |

| Market Size (2031) | USD 48.17 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

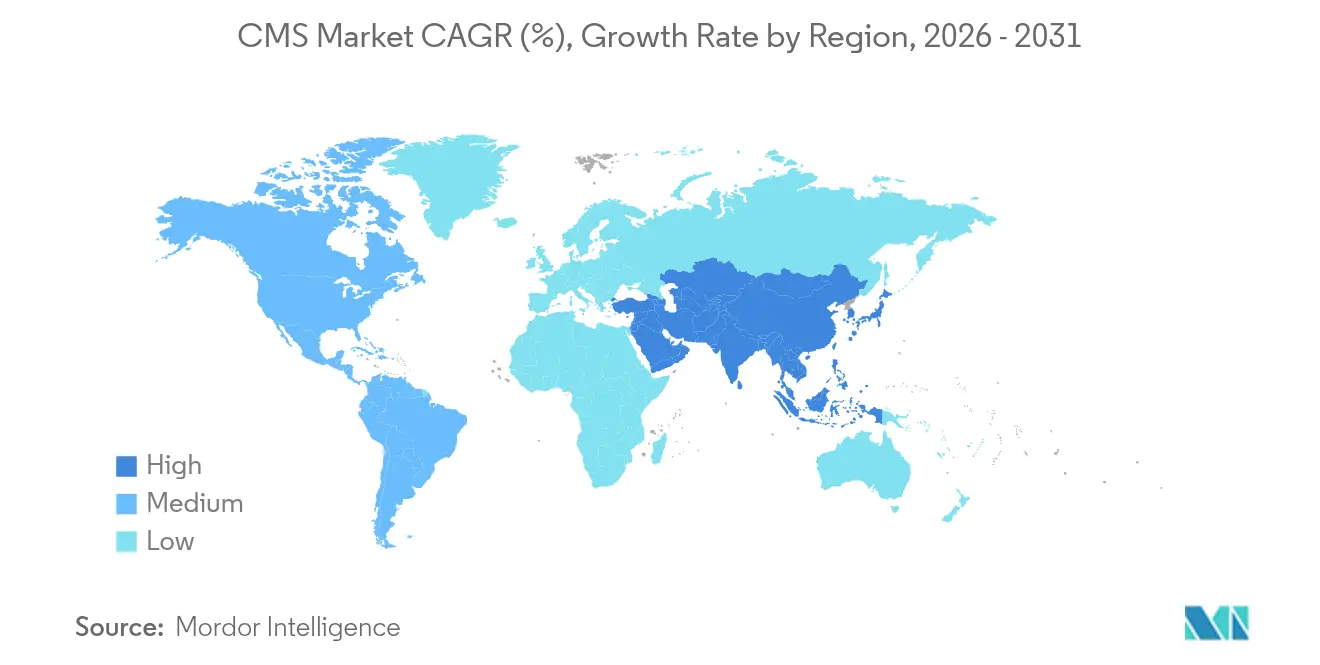

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

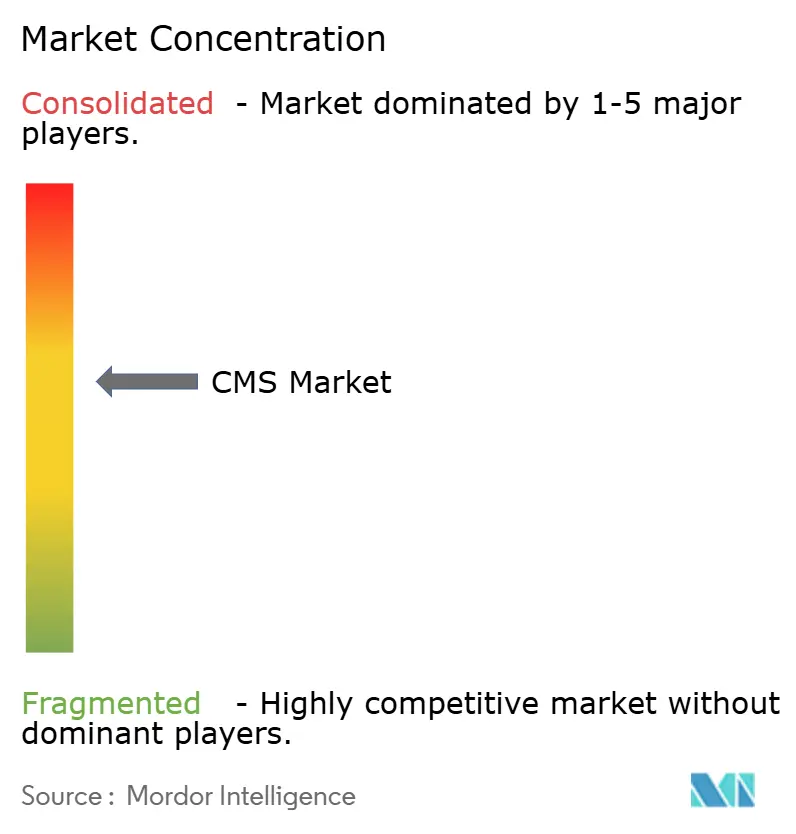

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CMS Market Analysis by Mordor Intelligence

The CMS market size was valued at USD 30.91 billion in 2025 and estimated to grow from USD 33.28 billion in 2026 to reach USD 48.17 billion by 2031, at a CAGR of 7.68% during the forecast period (2026-2031). Growth is propelled by enterprises replacing monolithic stacks with composable digital-experience platforms that decouple content from presentation for true omnichannel delivery. Generative AI modules are already proving commercial, with Adobe’s Experience Cloud adding USD 125 million in annualized recurring revenue in 2025. At the same time, cloud-native deployments shorten campaign launch cycles by 50% and help teams orchestrate content across more than 10 channels. North America retained a 36.2% share in 2024, while Asia-Pacific is expanding fastest at 15.1% CAGR as eCommerce surges. Software still controls 62.4% of revenue, yet services are climbing at 16.9% CAGR because enterprises need migration, integration and change-management expertise.

Key Report Takeways

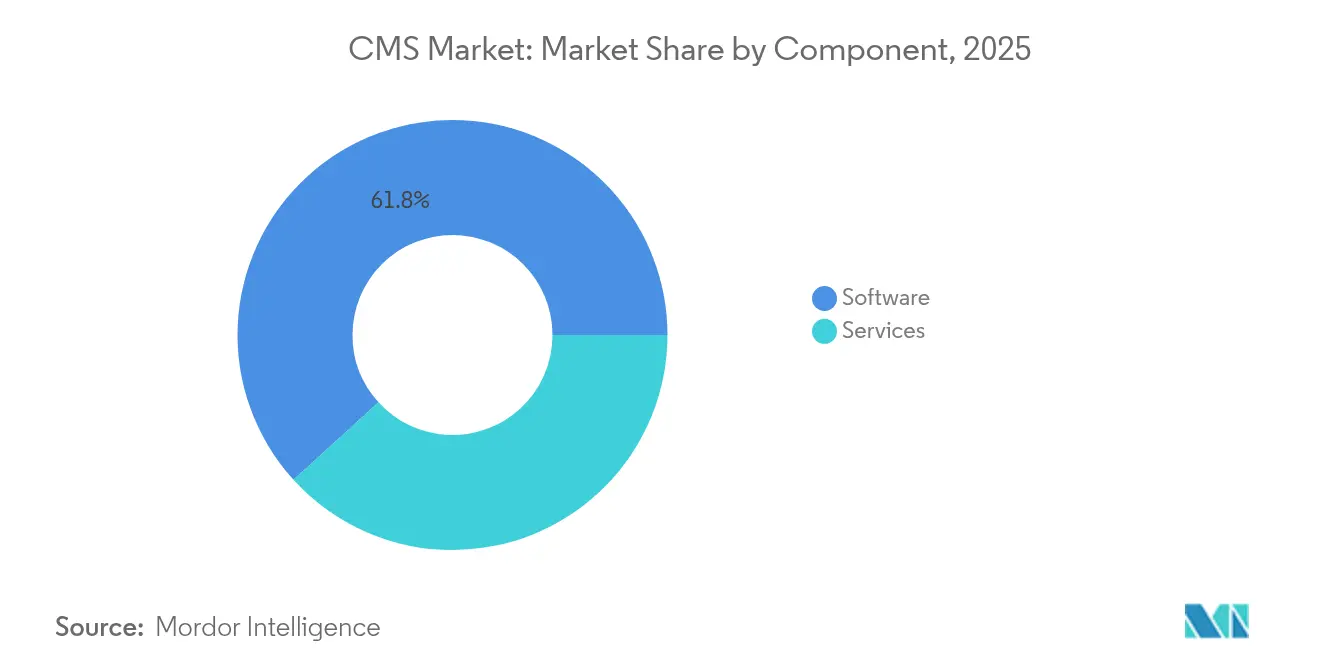

- By component, software led with 61.75% revenue share in 2025; services are forecast to expand at a 16.02% CAGR to 2031.

- By type, web content management accounted for 41.05% of CMS market share in 2025, while headless platforms are advancing at a 18.85% CAGR through 2031.

- By deployment mode, cloud captured 62.88% of the CMS market size in 2025 and is growing at a 19.1% CAGR through 2031.

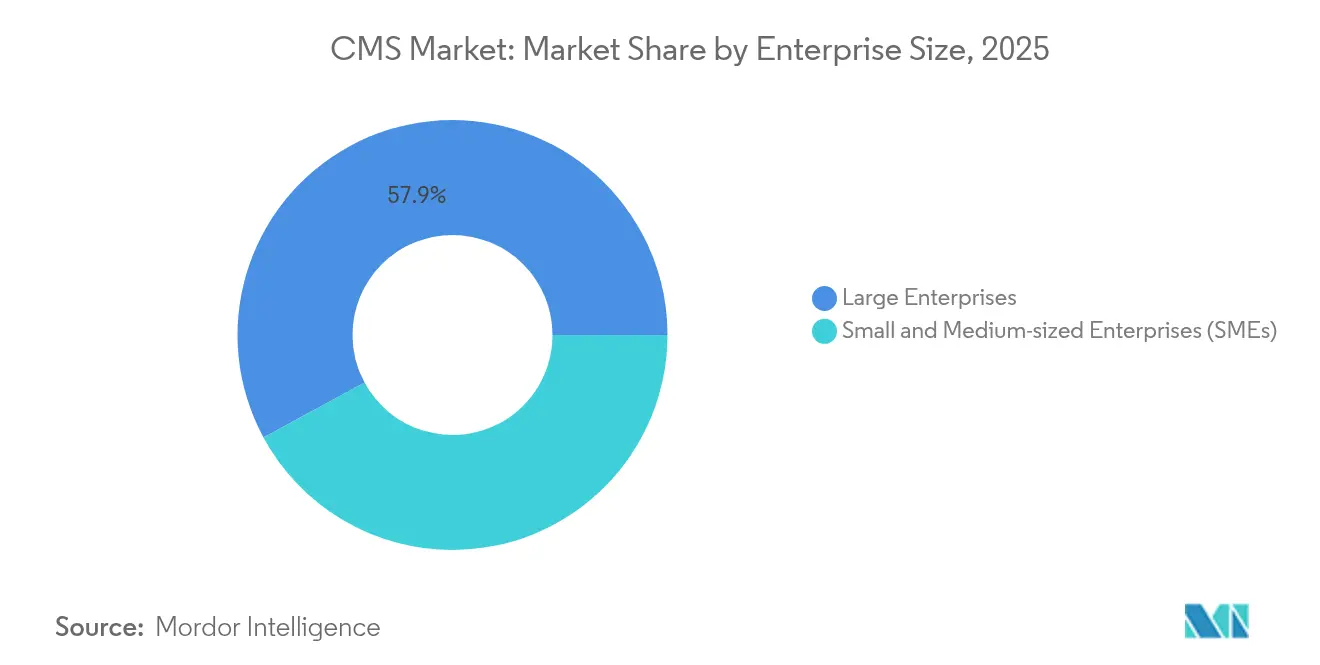

- By enterprise size, large enterprises held 57.90% share in 2025; SMEs are projected to post the highest 12.2% CAGR to 2031.

- By end-user industry, retail and eCommerce commanded 24.15% share of the CMS market size in 2025, whereas healthcare is projected to expand at 15.54% CAGR through 2031.

- By geography, North America led with 35.85% share in 2025, while Asia-Pacific registers the fastest 14.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global CMS Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of eCommerce and Omnichannel Retail Boom | +2.1% | Global, with Asia-Pacific leading growth | Medium term (2-4 years) |

| Cloud-native CMS Adoption for Composable Architecture | +1.8% | North America and EU early adoption, Asia-Pacific following | Short term (≤ 2 years) |

| Generative-AI Plug-ins Elevating Personalization | +1.4% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Rapid Localization Demand from Emerging-Market Brands | +0.9% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| API-first integrations with commerce engines | +0.7% | Global | Medium term (2-4 years) |

| Low-code CMS accelerators for SMEs | +0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise of eCommerce and Omnichannel Retail Boom

Retailers and B2B sellers now synchronize product data, pricing and promotions across web, mobile, social and in-store displays in real time. Advanced workflows support multi-stakeholder approvals and complex catalogs that legacy platforms struggle to manage. As more consumers adopt social commerce, real-time consistency drives customer trust, basket size and retention, making omnichannel capability an essential selection criterion in the CMS market.

Cloud-native CMS Adoption for Composable Architecture

Enterprises are prioritizing API-first systems that integrate best-of-breed tools while preserving governance. Sitecore’s XM Cloud doubled its revenue in 2024, underscoring demand for platforms that let marketers keep visual editors while giving developers flexible delivery APIs [1]Sitecore Newsroom, “XM Cloud Revenue Doubles Year on Year,” sitecore.com. Faster upgrades, auto-scaling and global CDNs also cut infrastructure costs, reinforcing cloud dominance.

Generative-AI Plug-ins Elevating Personalization

AI content engines draft copy, imagery and layout variants in seconds, then test and refine them based on engagement data. Adobe’s generative tools added USD 125 million in ARR during 2025, proving that AI modules create top-line value, not just cost savings. Automated personalization boosts conversion while freeing creative teams for strategy work.

Rapid Localization Demand from Emerging-Market Brands

Brands from Southeast Asia, Latin America and MEA require CMS integrations with translation management, cultural QA and regional compliance checks. Headless architectures connect seamlessly to these localization micro-services, enabling faster entry into new markets without ballooning internal resources.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front Migration Costs from Legacy Stacks | -1.2% | Global, particularly large enterprises | Short term (≤ 2 years) |

| Data-privacy and Sovereignty Compliance Burden | -0.8% | EU, North America, expanding globally | Medium term (2-4 years) |

| Shortage of Headless-CMS Skilled Developers | -0.6% | Global, acute in developed markets | Long term (≥ 4 years) |

| Escalating technical debt in unsupported legacy CMS versions | -0.50% | Global, especially mid-market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Up-front Migration Costs from Legacy Stacks

Enterprise re-platforming can exceed USD 420,000 and require dual-running old and new systems for up to 18 months. Delays amplify spend because content models, custom modules and staff skills must all be rebuilt or retrained, pushing ROI breakeven well beyond initial business cases [2]Valuebound, “Drupal 7 End-of-Life Costs and Migration Considerations,” valuebound.com.

Data-privacy and Sovereignty Compliance Burden

Twenty-one US states now enforce privacy statutes alongside GDPR and new AI-governance rules. Organizations often deploy multiple CMS instances or complex data localization workflows to stay compliant, elevating both capital and operating expenditures. Mid-sized firms, lacking dedicated legal staff, face disproportionate hurdles that slow CMS market adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Accelerates Digital Transformation

The CMS market size for software stood at 61.75% in 2025, but professional services are registering a 16.02% CAGR as firms need migration roadmaps, custom integrations and governance frameworks. Advisory and managed services help enterprises shift from on-premise to cloud, integrate content with commerce engines and retrain staff. Cloud migration engagements surged after retailers such as Clarks launched a 51-country commerce site within nine months by leveraging composable architecture and partner expertise.

Implementation specialists also capitalize on API-first adoption waves, designing headless blueprints that connect CMS with martech, CDP and DAM. As continuous optimization replaces one-time rollouts, outcome-based managed services grow, covering performance tuning, security patching and AI-based content testing. This recurring work anchors long-term vendor-client relationships and keeps the CMS market resilient during budget cycles.

By Type: Headless CMS Disrupts Traditional Web Content Management

Web content management maintained 41.05% share, yet headless platforms clock a 18.85% CAGR thanks to omnichannel imperatives. Decoupled models let marketers keep WYSIWYG authoring while developers serve content to web, mobile, IoT and kiosk endpoints. In retail and media, where latency and scalability affect conversion, businesses replace coupled stacks with API hubs that feed any front-end.

The headless wave boosts demand for complementary Digital Asset Management and micro-services. Vendors such as CoreMedia report clients managing millions of visual assets across social, marketplace and in-store screens through unified asset hubs. As composable commerce proliferates, headless CMS market solutions become default choices, pushing legacy platforms to retrofit APIs or risk churn.

By Deployment Mode: Cloud Dominance Accelerates Hybrid Adoption

Cloud claimed 62.88% of CMS market share in 2025 and is growing at 19.1% CAGR. Enterprises value instant scalability, built-in CDNs and managed security. AI features, real-time collaboration and edge rendering also tend to appear first in SaaS releases. Regulated sectors still keep sensitive data on-premise, but many now run hybrid patterns that store protected content locally while delivering public data through cloud CDNs.

Financial-services and healthcare firms rely on vendors like Hyland to route encrypted content between private and public nodes while staying compliant . Edge compute further narrows the performance gap against local servers, eliminating one of the last barriers to full cloud migration. Consequently, hybrid becomes a stepping stone rather than a permanent compromise, reinforcing cloud hegemony in the CMS market.

By Enterprise Size: SMEs Drive Adoption Through Simplified Solutions

Large organizations held 57.90% of revenue in 2025, supported by budgets for bespoke integrations and global rollouts. However, SMEs are expanding at 12.2% CAGR as cloud subscriptions eliminate hardware costs and low-code builders reduce dependence on in-house IT. Mono Solutions powers more than 250,000 SME websites by packaging templates, eCommerce and local-listing sync in one interface.

Affordable AI copy assistants, preset design blocks and pre-integrated payment gateways give small firms enterprise-grade experiences. Pay-as-you-grow pricing also aligns CMS spend with revenue, making advanced functionality accessible without capex. As vendors compete for this greenfield, the CMS industry witnesses shorter sales cycles and higher net-new logo counts.

By End-user Industry: Healthcare Leads Digital Transformation Adoption

Retail and eCommerce commanded 24.15% CMS market size in 2025, driven by real-time catalog, promotion and loyalty experiences. Yet healthcare shows the quickest 15.54% CAGR, propelled by telemedicine, patient portals and HIPAA-compliant content workflows. Providers like HealthHub boosted SEO traffic 75% and session duration 16% after a Sitecore deployment that unified patient education with appointment journeys.

Strict audit trails and consent records make general-purpose tools insufficient. Advanced CMS engines provide granular permissions, redaction tools and adaptive accessibility features. Media, telecom and education segments also grow steadily as they centralize multimedia libraries and multi-lingual documents, but healthcare’s regulatory urgency cements its status as the breakout vertical within the CMS market.

Geography Analysis

North America sustained leadership with 35.85% revenue in 2025. A mature vendor ecosystem and sizable IT budgets enable rapid upgrades to headless, AI-infused stacks. State-level privacy laws spark demand for consent and localization modules without the stringent cross-border constraints seen in Europe.

Asia-Pacific is the CMS market’s fastest riser at 14.52% CAGR, underpinned by double-digit eCommerce expansion in Indonesia, the Philippines and Vietnam. Enterprises need multi-language, multi-currency publishing backed by mobile-first templates, which accelerates headless CMS adoption across the region.

Europe remains sizeable though mature. GDPR and emerging AI Acts drive uptake of platforms with built-in governance and local hosting options. Latin America and the Middle East and Africa hold smaller shares but record growing investments in Arabic localization, Islamic finance content flows and government digitization, paving the way for future CMS market traction.

Competitive Landscape

The CMS market features established suites from Adobe, Microsoft, and Sitecore alongside headless specialists such as Contentful and Contentstack. Competition intensified after Sitecore posted USD 500 million ARR in 2024 by shifting to cloud-native, AI-enhanced services [4]Sitecore Newsroom, “Sitecore Reaches USD 500 Million ARR,” sitecore.com. Contentstack, meanwhile, reached USD 26 million in revenue by targeting API-first deployments.

Consolidation is underway. Contentstack bought Lytics for CDP capabilities, Netlify acquired Gatsby to bolster composable web frameworks and Acquia purchased Monsido for accessibility scans. Vendors seek end-to-end platforms that cover content, data, personalization and analytics out of the box, lowering integration burdens for buyers.

AI differentiation is now strategic. Platforms embed generative copy, image variations and predictive workflows to lift engagement and reduce manual effort. Industry-specific extensions for healthcare, finance and manufacturing add compliance features that horizontal tools lack, creating niches for emerging providers even as market concentration rises.

CMS Industry Leaders

Adobe Inc.

Automattic Inc.

Acquia Inc.

Optimizely Inc.

Sitecore Holding II A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sitecore announced more than 250 innovations for its intelligent DXP and CMS, including expanded Stream AI capabilities.

- January 2025: BizStream acquired Refactored to speed headless CMS implementations with Refactored’s Web Accelerator.

- January 2025: Drupal launched Drupal CMS, a marketer-centric open-source platform for enterprise digital experiences.

- October 2024: Sitecore introduced Sitecore Stream, an AI-powered DXP built on Microsoft Azure OpenAI Service with brand-aware content creation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the content management system (CMS) market as the revenues earned from licensed or subscription-based software, traditional coupled, decoupled, and headless architectures that let users create, store, deliver, and analyze digital content across web, mobile, and emerging touchpoints. We include related maintenance and support fees but exclude bespoke web-development services and stand-alone digital asset repositories. Our team clarifies that sales of open-source code forks offered without commercial support sit outside the scope.

Scope Exclusion: Pure-play document scanners, custom coding agencies, and generic cloud storage are not counted.

Segmentation Overview

- By Component

- Software

- Services

- By Type

- Web Content Management (WCM)

- Enterprise Content Management (ECM)

- Headless / API-First CMS

- Digital Asset Management (DAM)

- Document Management System (DMS)

- eCommerce CMS

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium-sized Enterprises (SMEs)

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Retail and eCommerce

- IT and Telecom

- Media and Entertainment

- Education

- Government and Public Sector

- Manufacturing

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with CMS product managers, cloud integrators, and mid-market web-agency leads across North America, Europe, and Asia Pacific. Their inputs verified average selling price ranges, typical migration timelines, and adoption hurdles, letting us tighten penetration assumptions that secondary data alone could not resolve.

Desk Research

We began by mapping the supply landscape through public company filings, W3Techs usage panels, United States Census digital trade releases, Eurostat ICT adoption dashboards, and industry association briefs such as the Content Management Professionals group. Commercial insights from approved paid datasets, D&B Hoovers for vendor revenues and Dow Jones Factiva for deal news, helped us benchmark share shifts. Open patents scraped via Questel highlighted the rise of API-first plug-ins, while World Bank broadband indicators anchored user-base growth. This listing is illustrative; many additional sources fed our evidence stack.

Market-Sizing & Forecasting

A top-down demand pool, built from active-website counts and CMS penetration ratios, provided the first read. Supplier roll-ups and sampled ASP × installation checks offered bottom-up validation, after which the two views were reconciled once. Key variables include global domain registrations, share of websites running a CMS, cloud migration rates, average subscription price shifts, regulatory privacy spend, and developer availability. We project forward with multivariate regression blended with scenario analysis, letting elasticity around cloud cost and AI feature uptake adjust outcomes. Gaps in granular spend were bridged by region-specific price bands gathered during interviews.

Data Validation & Update Cycle

Outputs pass three analyst reviews, anomaly scans against external trackers, and variance checks versus prior editions. Reports refresh every twelve months, and we issue interim pulses when material events, major vendor mergers or pricing pivots, occur. A final sense-check is completed the week before publication.

Why Our CMS Baseline Commands Reliability

Published CMS valuations often diverge because firms select different component mixes, pricing ladders, and refresh cadences.

Key gap drivers include some publishers reporting conservative on-premise only scopes, others extrapolating aggressive AI-premium prices, and still others rolling forward legacy estimates without adjusting currency. Mordor Intelligence applies consistent scope, triangulates hybrid pricing, and updates annually, which is why decision-makers rely on our baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 30.91 B | Mordor Intelligence | - |

| USD 34.94 B | Global Consultancy A | Includes custom web-dev services and counts freemium open-source forks |

| USD 35.16 B | Industry Association B | Uses vendor list prices, limited primary checks |

| USD 47.41 B | Regional Consultancy C | Blends ECM and WCM segments without removal of duplicative spend |

In closing, the comparison shows that our disciplined scope selection, mixed-method modeling, and annual refresh give buyers a balanced, transparent baseline rooted in verifiable variables.

Key Questions Answered in the Report

What is the current size of the CMS market in 2026?

The market stands at USD 33.28 billion, with an 7.68% CAGR projected through 2031.

Which region is growing fastest for CMS deployments?

Asia-Pacific is expanding at a 14.52% CAGR due to booming eCommerce and mobile-first consumers.

Why are services outpacing software growth in the CMS market?

Enterprises need specialized migration, integration and governance expertise as they transition to composable architectures, driving services at a 16.02% CAGR.

How is generative AI influencing CMS investments?

AI modules automate content creation and personalization, already delivering USD 125 million in new ARR for Adobe and boosting conversion for early adopters.

Which end-user industry shows the highest CMS adoption growth?

Healthcare leads with a 15.54% CAGR as providers digitize patient engagement while meeting strict compliance mandates.

What deployment model dominates the CMS market?

Cloud holds 62.88% share and is growing fastest at 19.1% CAGR thanks to scalability, built-in security and rapid feature releases.

Page last updated on: