Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Micro-Tasking Market is Segmented by Task Type (Content Moderation, Data Entry and Processing, and More), by Application (AI Training and Data-Labeling, Market Research and Insights, and More), by End-User Industry (Retail and E-Commerce, Technology and Telecom, and More), by Platform Business Model (Open Marketplace, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

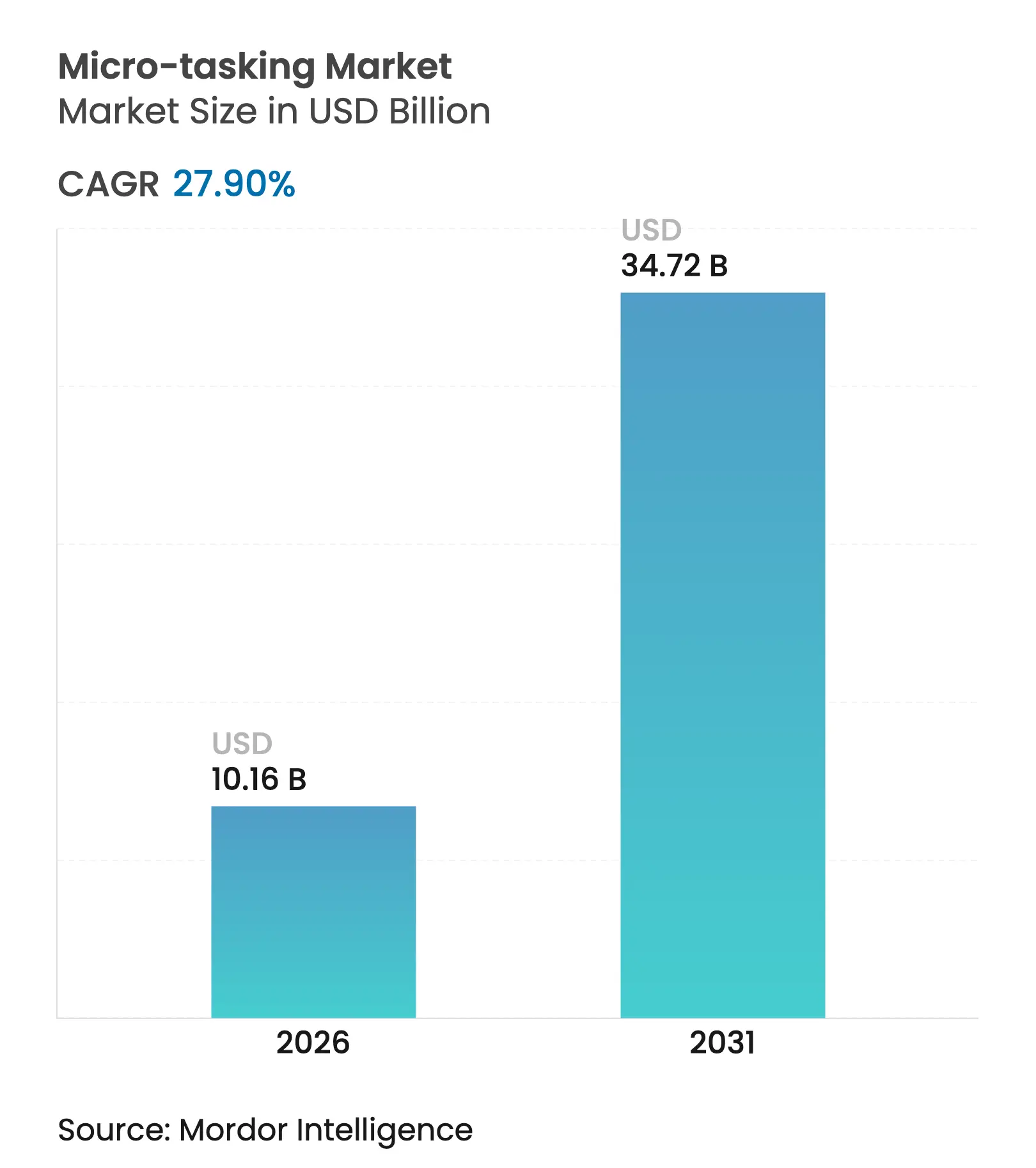

| Market Size (2026) | USD 10.16 Billion |

| Market Size (2031) | USD 34.72 Billion |

| Growth Rate (2026 - 2031) | 27.90 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The micro-tasking market size was valued at USD 7.9 billion in 2025 and estimated to grow from USD 10.16 billion in 2026 to reach USD 34.72 billion by 2031, at a CAGR of 27.90% during the forecast period (2026-2031). Early momentum stems from the steep rise in AI spending, the proliferation of large-language-model deployments, and a structurally larger remote workforce pool. Enterprises increasingly view human-in-the-loop workflows as a strategic lever to improve model fidelity, while managed service providers consolidate capacity to deliver multi-jurisdiction data governance at scale. Emerging regulatory frameworks now shape vendor selection criteria as much as cost, giving compliance-ready operators a measurable edge. At the same time, hybrid API-first platforms capture new demand from engineering teams that need rapid programmatic access to curated human judgment for continuous model updating.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expansion of data-labeling for Gen-AI Expansion of data-labeling for Gen-AI | +8.5% | Global, led by North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+8.5% | Geographic Relevance:Global, led by North America & Europe | Impact Timeline:Medium term (2-4 years) |

Proliferation of remote & flexible workforces Proliferation of remote & flexible workforces | +6.2% | Global | Short term (≤2 years) | |||

Rising digital-commerce SKU audits Rising digital-commerce SKU audits | +5.3% | North America, Europe, APAC | Medium term (2-4 years) | |||

Regulatory pressure for explainable AI Regulatory pressure for explainable AI | +4.7% | North America, Europe | Long term (≥4 years) | |||

Surge in short-form video safety checks Surge in short-form video safety checks | +3.2% | Global | Short term (≤2 years) | |||

Adoption of Web3 micro-incentive wallets Adoption of Web3 micro-incentive wallets | +2.6% | Tech-forward markets | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Expansion of data-labeling for Gen-AI

Labeled data volumes continue to multiply as generative models shift from research pilots to enterprise products. AI teams now commission multimodal preference and ranking tasks that cannot be automated reliably, reinforcing the centrality of the micro-tasking market. Superior training corpora increasingly dictate competitive advantage; operators with vertical-specific ontologies and quality-control pipelines command premium pricing. National AI strategies also highlight annotation capacity as a digital manufacturing asset, prompting policy support in several G-20 economies.

Proliferation of remote & flexible workforces

Permanent adoption of distributed work has unlocked a global talent reservoir, including part-time subject-matter experts who accept high-value annotation gigs around core professional schedules.[1]World Economic Forum, "The Future of Jobs Report 2025", weforum.org Platforms that authenticate credentials and tier compensation accordingly report lower task rejection rates and faster turnaround, moving market dynamics from worker-volume competition to worker-quality differentiation.

Regulatory pressure for “explainable AI” datasets

Mandates such as the EU AI Act force enterprises to document decision chains, spawning verification micro-tasks where annotators grade model outputs for fairness and traceability.[2]Federal Register, "Preventing Access to U.S. Sensitive Personal Data", federalregister.govCompliance budgets flow to providers capable of combining secure environments with expert reviewers.

Surge in short-form video safety checks

User-generated video below 30 seconds demands near-instant review cycles to uphold brand safety on social platforms. Annotators tag violence, hate speech, and policy breaches, while AI pre-filters accelerate throughput, sustaining high-volume micro-task streams.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Privacy & data-sovereignty laws Privacy & data-sovereignty laws | -5.2% | Europe, India | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-5.2% | Geographic Relevance:Europe, India | Impact Timeline:Medium term (2-4 years) |

Persistent low pay driving worker churn Persistent low pay driving worker churn | -4.1% | Global | Short term (≤2 years) | |||

Language quality concerns Language quality concerns | -2.8% | Non-English regions | Medium term (2-4 years) | |||

Rising carbon-audit costs Rising carbon-audit costs | -1.9% | Europe, North America | Long term (≥4 years) | |||

| Source: Mordor Intelligence | ||||||

Privacy & data-sovereignty laws (GDPR, DPDP-India)

Regional data-protection regimes fragment annotation pipelines, compelling providers to isolate data and labor pools by jurisdiction.[3]Federal Register, "Preventing Access to U.S. Sensitive Personal Data", federalregister.govCompliance redesign raises unit economics and favors managed service operators with federated cloud infrastructure.

Persistent low pay leading to worker churn

Below-minimum pay has intensified scrutiny of platform wage practices, with Human Rights Watch documenting gaps in basic protections.[4]Human Rights Watch, "The Gig Trap: Platform Work in the U.S.", hrw.org High churn jeopardizes output consistency, prompting premium platforms to pilot guaranteed-rate models and skill-ladder programs.

By Task Type: Visual Data Fuels AI’s Next Frontier

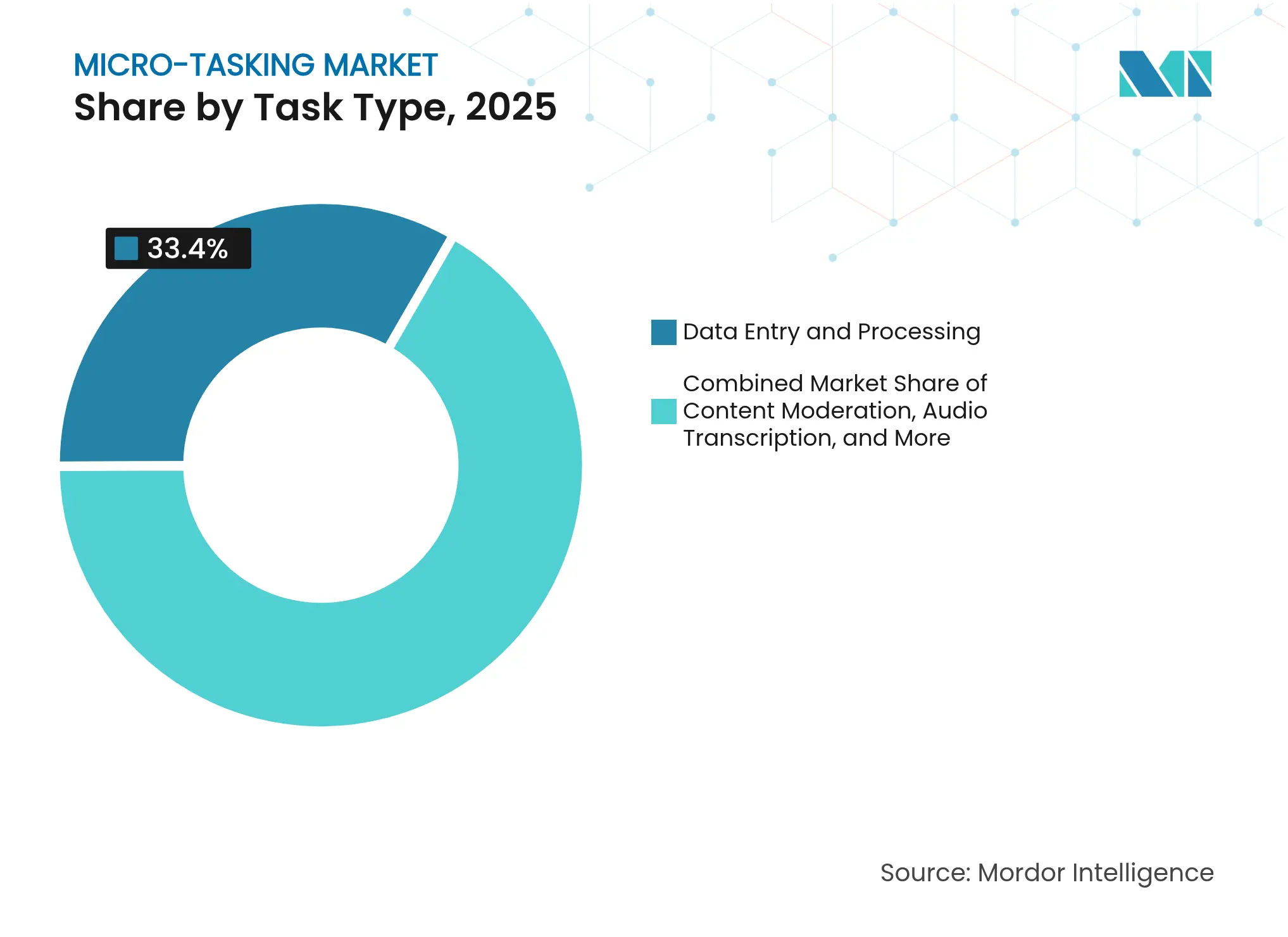

Data Entry & Processing currently holds the largest market share at 33.40% in 2025, serving as the foundation of the micro-tasking economy through its broad applicability across industries and relatively standardized workflows. Whereas, Image & Video Annotation will generate the fastest revenue growth, expanding at 43.20% CAGR to 2031 as demand soars for spatial labeling in autonomous driving, medical imaging, and retail analytics. Platforms embed ML-assisted annotation to cut per-frame costs, yet human validation remains indispensable for contextually rich bounding and segmentation tasks.

Continued toolchain innovation—auto-suggest, smart-polygon, active learning—raises throughput without eroding task volumes because enterprises now label finer-grained attributes. Content Moderation regulators tighten liability rules for social media. Audio Transcription benefits from rising multilingual voice-assistant roll-outs, while Surveys & Feedback evolves toward emotion-coding assignments, blending quantitative polling with qualitative sentiment capture. The micro-tasking industry thus shows a two-speed profile: commoditized text tasks plateau, whereas multimodal data-centric work accelerates.

Note: Segment shares of all individual segments available upon report purchase

By Application: AI Training Dominates Growth Trajectory

AI Training & Data-Labeling contributed 41.80% of 2025 revenue and is set to rise at 39.20% CAGR, underscoring its foundational role. Enterprises integrate continuous labeling loops into MLOps pipelines, driving demand for real-time judgment feeds exposed through RESTful APIs.

Trust & Safety/UGC Moderation, responds to regulatory risk and advertiser pressure; automated classifiers execute first-pass screening, yet edge cases still escalate to expert reviewers. Market Research & Insights leverages rapid panel formation for competitive intelligence, while Language & Localization capitalizes on brand pivots toward deeply localized digital experiences. Retail Shelf & Price Audits, though niche, gains strategic relevance as inflationary conditions push retailers to tighten price integrity governance. Collectively these trends reinforce the micro-tasking market as a critical middleware layer between unstructured data and production AI.

By End-user Industry: Healthcare & Life Sciences accelerate specialization

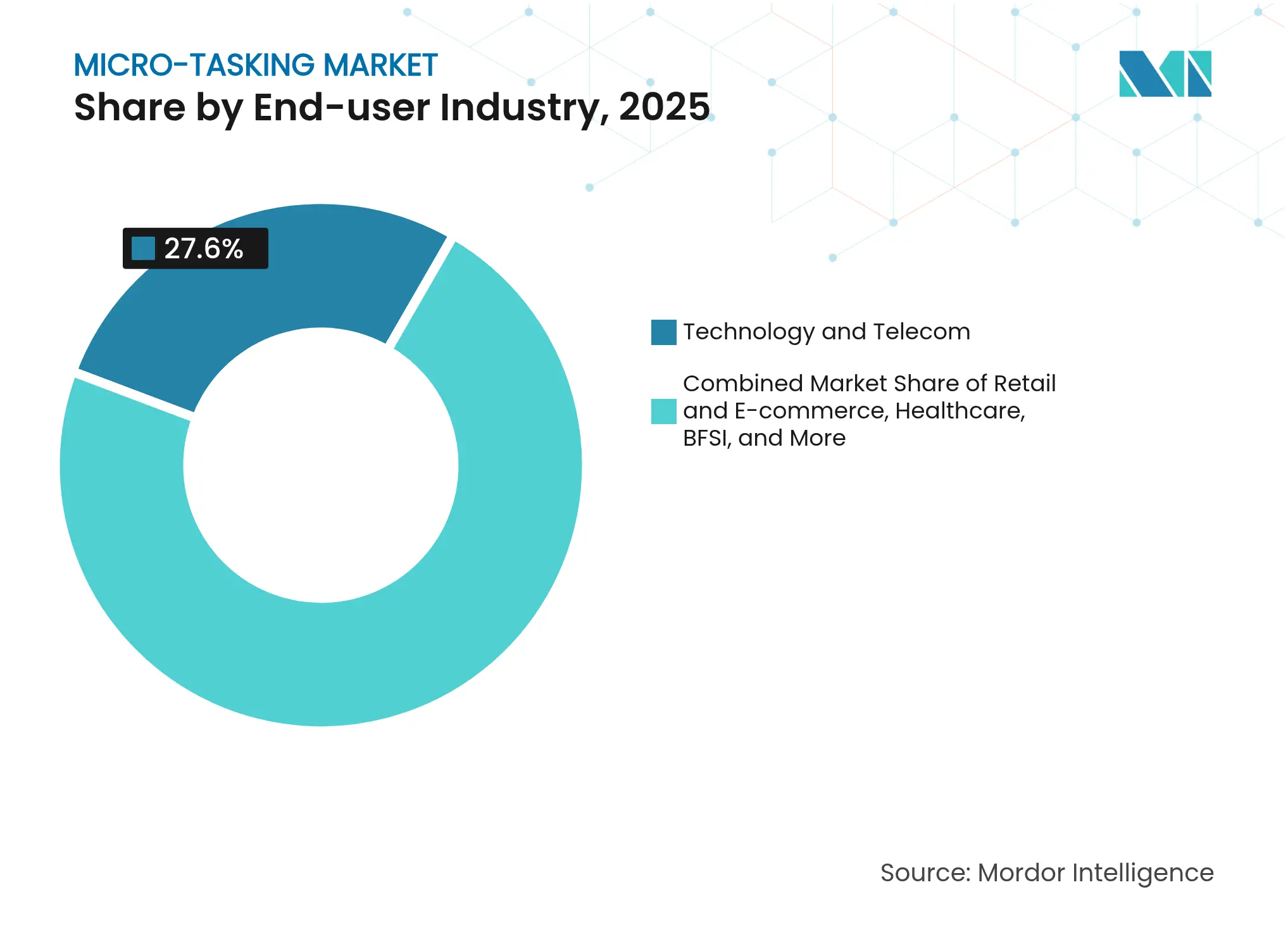

Technology & Telecom captured 27.60% of micro-tasking market share in 2025, yet Healthcare & Life Sciences is poised to outpace every vertical with a 29.90% CAGR through 2031. Hospitals, CROs and medical-device firms now outsource annotation for radiology scans, genomic sequences and clinical-trial notes, activities that require certified talent and HIPAA-grade security controls. NVIDIA’s 2024 launch of sector-specific generative-AI microservices reinforced demand for expert reviewers who can validate model outputs before clinical deployment.

Retail & E-commerce merchants blend automated shelf-recognition with spot-check micro-tasks to maintain price and product data integrity. Government & Public Sector, funds civic-data digitisation and document redaction initiatives, while Education shows a scaling assessment scoring and content localisation. Industries facing stringent regulation or specialised data formats increasingly prefer managed service providers capable of domain-specific ontologies, creating a premium tier within the micro-tasking market. As procurement criteria shift from lowest cost to validated expertise, vertical specialisation is becoming a durable differentiator for platform growth.

Note: Segment shares of all individual segments available upon report purchase

By Platform Business Model: Hybrid/API-first unlocks scalable quality

Managed Service Providers dominated 2025 with a 45.20% revenue share by bundling curated workforces, QA protocols and compliance dashboards into enterprise-grade SLAs. CRN’s 2025 channel survey shows 48% of solution integrators now attach AI consulting to these offerings, turning MSPs into strategic partners rather than simple capacity brokers. Their end-to-end control of data pipelines enables closed-loop quality improvement and jurisdiction-specific data residency—features that resonate with highly regulated customers. However, the approach can limit agility for engineering teams seeking rapid experimentation cycles.

Hybrid/API-first platforms are the fastest-growing model, scaling at 36.10% CAGR to 2031 by exposing human judgement through programmatic endpoints that integrate directly into MLOps workflows. A 2025 arXiv study comparing API and GUI agents highlighted efficiency gains that mirror enterprise preferences for low-code integration and continuous deployment. Open Marketplaces peers as quality variance and rising compliance costs erode price-led advantages. Oracle’s 2024 integration outlook notes the shift toward event-driven architectures; platforms that pair on-demand APIs with managed service layers position themselves to win incremental spend while meeting governance mandates. The competitive frontier therefore centres on combining developer-friendly interfaces with enterprise-class oversight, bridging the gap between speed and assurance in the micro-tasking market.

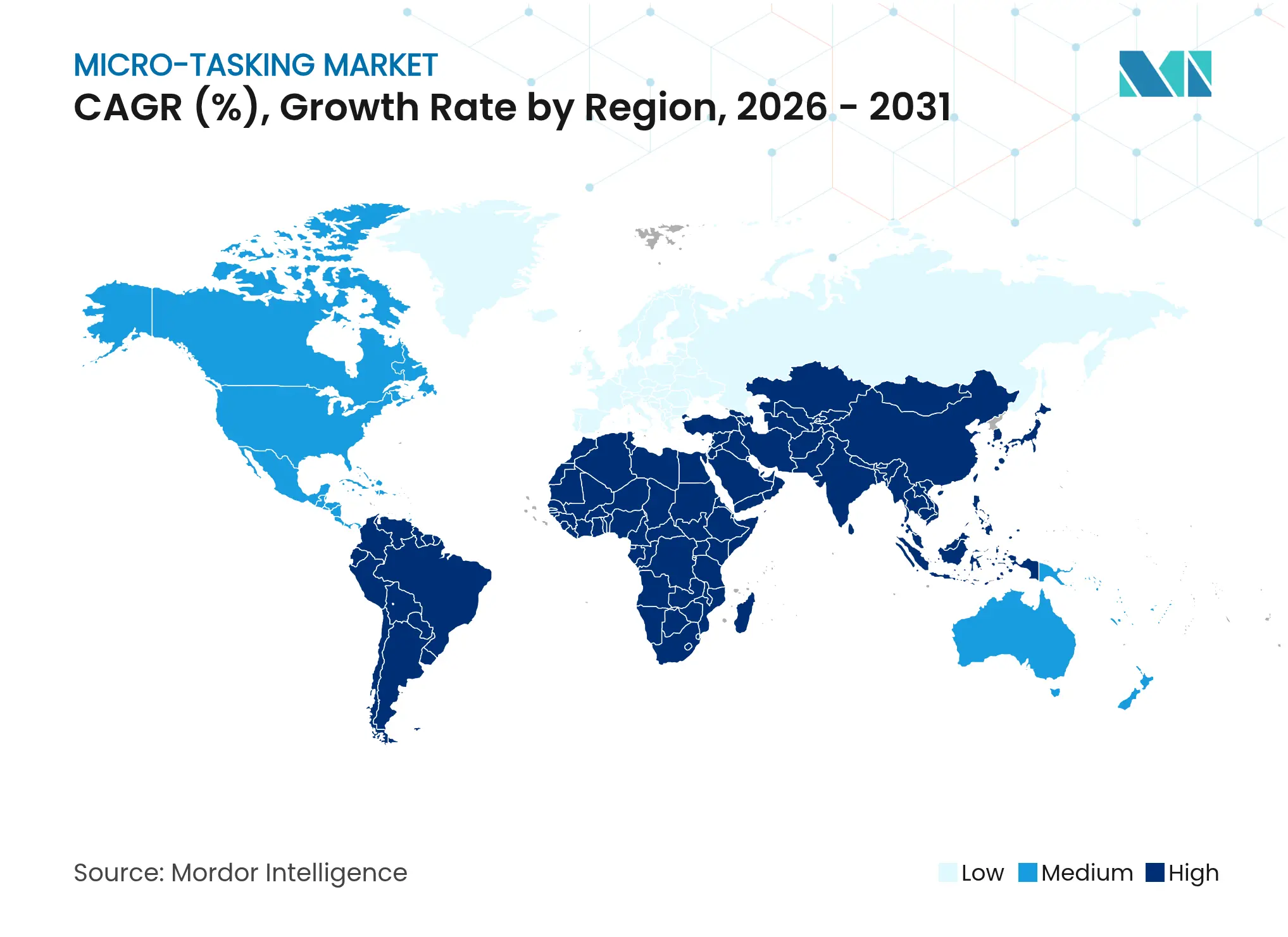

North America commands 37.70% 2025 revenue owing to deep AI capital expenditure—U.S. firms invested USD 109.1 billion in corporate AI projects in 2024.Demand is sustained by enterprise compliance requirements and a skilled freelance base. Growth moderates to 9.60% CAGR as automation of routine labeling expands, yet explainability and regulated-data tasks replenish volume. The micro-tasking market share leadership also reflects a concentration of hyperscale cloud and silicon vendors, whose foundation-model roadmaps depend on continuous human feedback.

APAC delivers the fastest expansion at 28.40% CAGR, propelled by digital-economy FDI surging to USD 230 billion across ASEAN in 2023. China scales multimodal foundation models, India leverages cost-competitive English-proficient labor, and Indonesia offers large mobile-first worker cohorts. Linguistic diversity, however, necessitates advanced quality-assurance frameworks.

Europe holds 21.10% share with 11.90% growth, balancing robust AI uptake against restrictive cross-border data mandates that stimulate in-region micro-task hubs. South America and the Middle East & Africa represent emerging demand pools with respective 18.90% and 23.20% CAGRs, anchored by youthful demographics adopting gig models for supplemental income.

Market Concentration

The sector is shifting from a volume-driven marketplace to a quality-led managed service paradigm. Top players integrate annotation tooling, workforce management, and compliance dashboards, enabling enterprise SLAs on accuracy, privacy, and turnaround. LXT’s 2025 acquisition of Clickworker aggregates a six-million-strong talent network, signaling scale-driven consolidation and a move up the value chain into healthcare and autonomous-vehicle datasets.[6]i-Payout, "LXT’s Acquisition of Clickworker" i-payout.comNVIDIA’s verticalized microservices illustrate how technology leaders cultivate specialized task ecosystems to complement proprietary AI stacks, locking in high-margin workflows.

Hybrid/API-first entrants differentiate through developer-centric integration and pay-as-you-go contracts, capturing incremental budgets from MLOps teams. Open marketplaces confront downward fee pressure and rising compliance costs, pushing them toward niche verticalization (e.g., medical imaging, legal discovery).

Strategic alliances emerge between cloud providers and annotation firms to embed labeling directly into data-warehouse environments, tightening vendor lock-in. Overall, bargaining power shifts toward platforms that can evidence worker fairness, carbon-accounting transparency, and geographically partitioned data flows.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Micro-Tasking Market Benchmark Remains the Trusted Reference

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 7.94 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 5.55 B (2025) | Global Consultancy A | Includes only annotation tasks; excludes survey micro-jobs | ||

USD 5.13 B (2025) | Industry Association B | Uses 2023 exchange rates and assumes flat commission fees | ||

USD 5.13 B (2025) | Regional Consultancy C | Counts offline gig errands yet omits platform take-rates |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.