Cloud Security In Banking Industry Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

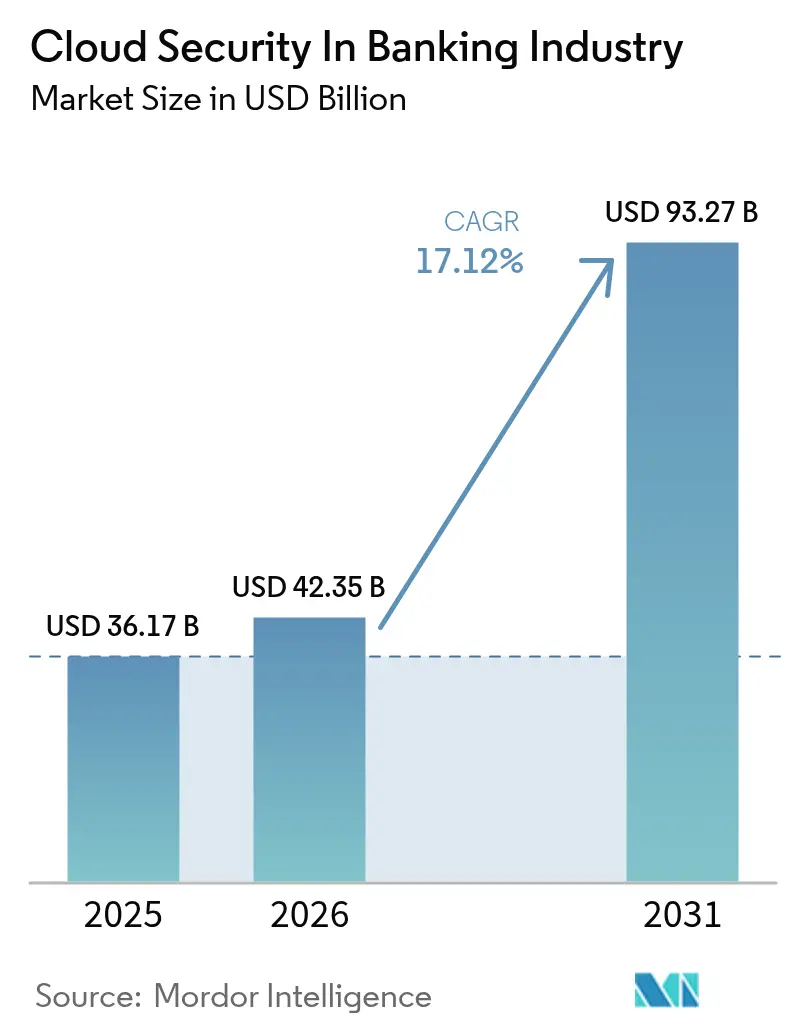

| Market Size (2026) | USD 42.35 Billion |

| Market Size (2031) | USD 93.27 Billion |

| Growth Rate (2026 - 2031) | 17.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Security In Banking Industry Analysis by Mordor Intelligence

The cloud security in banking industry was valued at USD 36.17 billion in 2025 and estimated to grow from USD 42.35 billion in 2026 to reach USD 93.27 billion by 2031, at a CAGR of 17.12% during the forecast period (2026-2031). This expansion mirrors banks’ pivot toward cloud-native architectures that cut operating costs, improve agility, and satisfy regulators demanding proven operational resilience. Demand is also rising because ransomware incidents targeting financial workloads climbed to 78% in 2024, pushing chief information security officers to accelerate zero-trust adoption and deeper third-party risk oversight. Consolidation among security vendors is giving banks access to broad platforms that combine API protection, identity governance, and AI-powered fraud analytics. In parallel, public cloud providers are embedding pre-configured compliance tooling that simplifies audits under measures such as the EU’s Digital Operational Resilience Act (DORA), which came into force in January 2025.[1]European Banking Authority, “Digital Operational Resilience Act,” europa.eu Although North America retained a 37.2% share in 2024, Asia-Pacific is advancing the fastest on the back of national data-localization rules and mobile-first consumer banking, contributing a 17.8% regional CAGR to 2030.

Key Report Takeaways

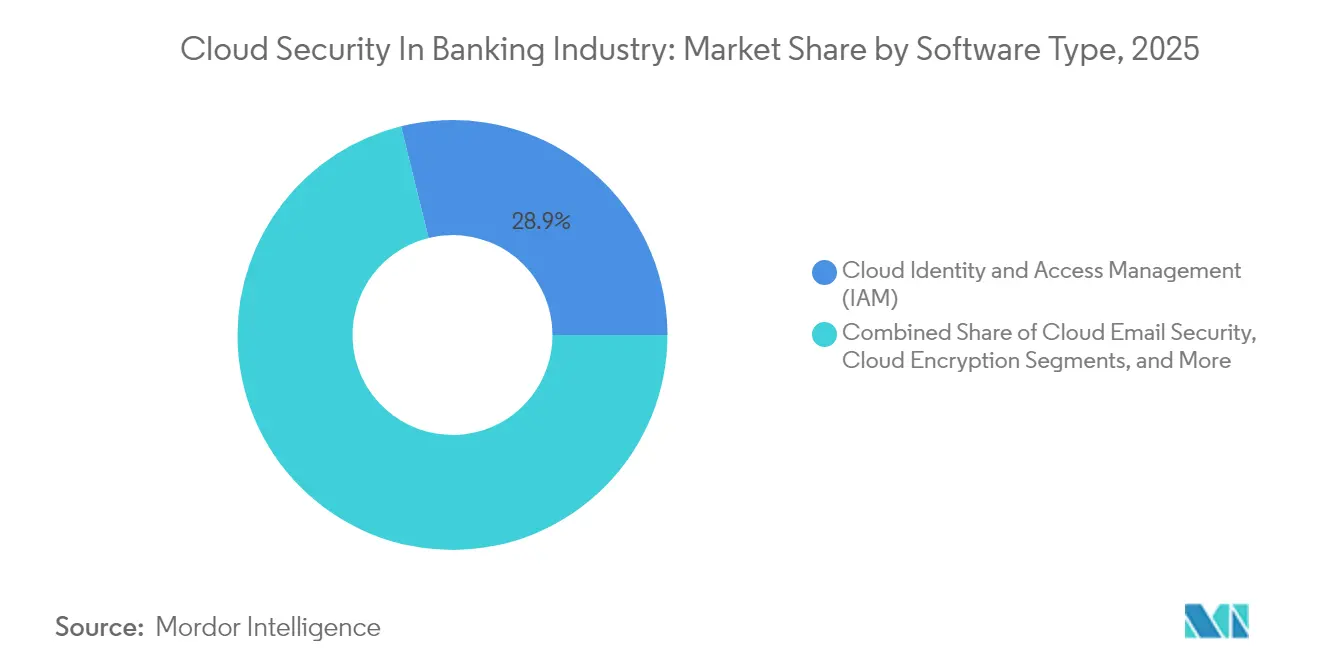

- By software type, Cloud Identity and Access Management led with 28.85% of the cloud security in banking industry share in 2025, while Cloud Encryption is projected to expand at an 17.75% CAGR through 2031.

- By deployment model, the public-cloud segment accounted for 61.55% of the cloud security in the banking industry size in 2025; hybrid cloud is set to grow the fastest at 19.45% CAGR to 2031.

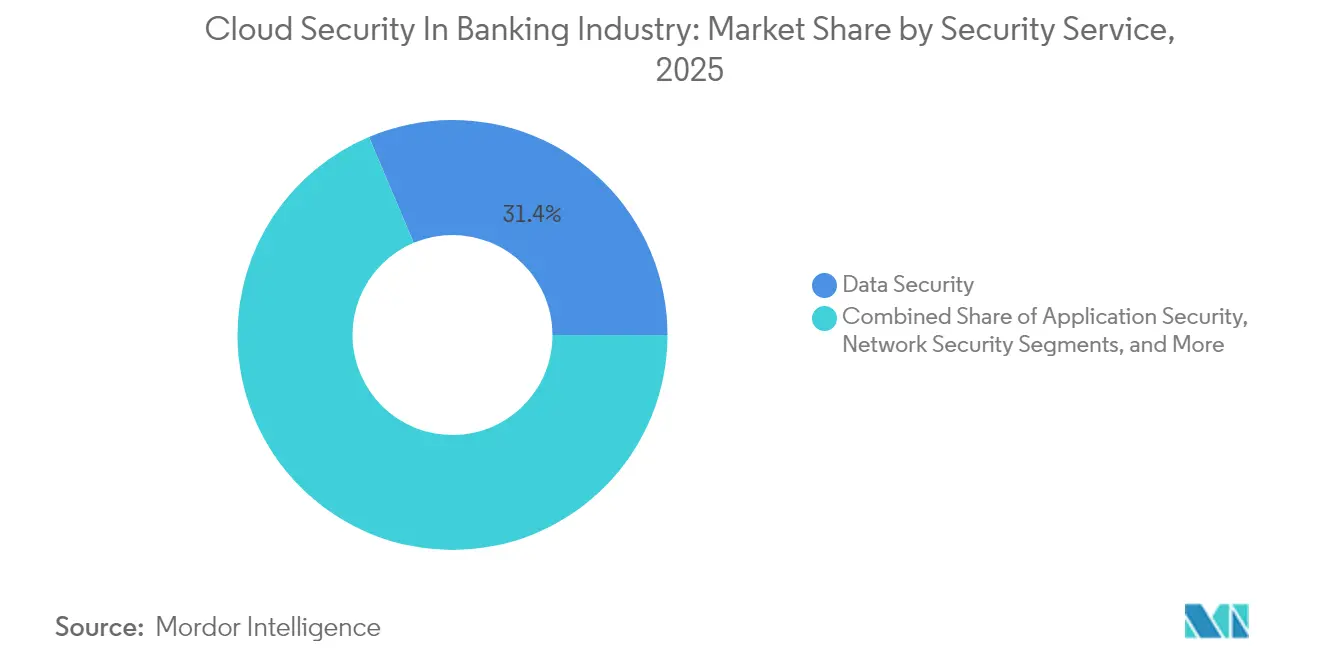

- By security service, data-security offerings represented 31.35% of cloud security in the banking industry size in 2025, whereas security monitoring & orchestration is forecast to post a 19.65% CAGR to 2031.

- By banking type, retail banking controlled 38.25% of the cloud security in the banking industry share in 2025; digital-only banks are expected to record a 19.05% CAGR between 2026 and 2031.

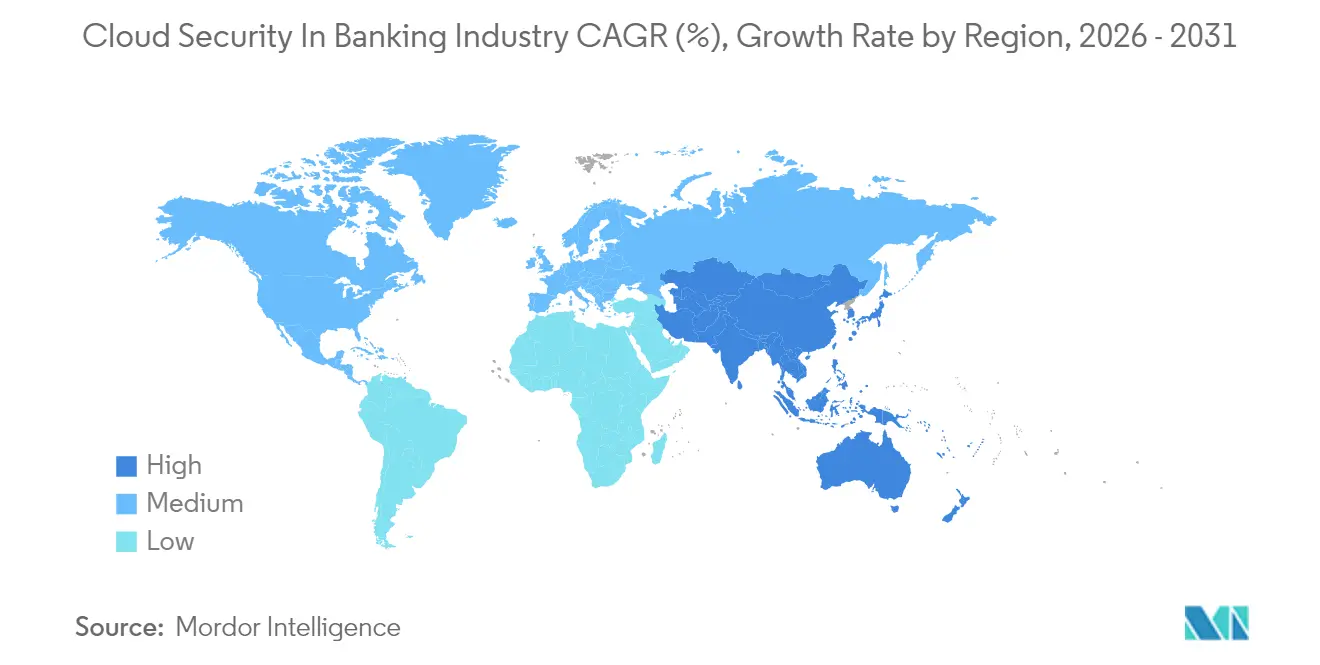

- By geography, North America dominated with a 36.85% revenue share in 2025; the Asia-Pacific region is on track for the fastest regional CAGR at 17.35% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Security In Banking Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising sophistication of cyber-attacks | +4.2% | Global | Short term (≤ 2 years) |

| Real-time compliance automation (Basel III, DORA) | +3.8% | EU primary, NA secondary | Medium term (2-4 years) |

| Serverless and container-native cost avoidance | +2.1% | North America, EU | Medium term (2-4 years) |

| Open-banking APIs accelerate zero-trust | +2.9% | EU primary, APAC secondary | Long term (≥ 4 years) |

| AI-powered fraud detection in security suites | +3.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Volume and Sophistication of Cyber-Attacks on Banking Workloads

Financial institutions faced 78% ransomware hit rates in 2024, double the prior year. Attackers are now exploiting API abuse, container misconfigurations, and third-party software flaws, in 1 incident, a cloud misconfiguration exposed nearly 500,000 JPMorgan Chase customers, underlining the new perimeter-free threat surface. Average breach costs reach USD 10 million per incident, prompting urgent migration to behavior analytics-driven zero-trust controls that verify every session and asset. Major banks are embedding continuous compliance scanning and threat hunting into DevSecOps pipelines to reduce exposure windows from days to hours. Global payments rail SWIFT is piloting federated learning models with Google Cloud that flag anomalous transactions without moving sensitive data, demonstrating how AI can detect fraud while protecting privacy. As organized crime monetizes access to stolen banking credentials on dark-net markets, proactive cloud segmentation and least-privilege IAM have become board-level priorities.

Real-Time Compliance Automation Requirements (Basel III, DORA, etc.)

The EU’s DORA obliges 22,000 financial entities to report severe cyber incidents within 24 hours and test exit plans for critical cloud suppliers, pushing banks to deploy automated evidence-collection engines that feed regulators in near real time. U.S. regulators are moving in the same direction: the Treasury’s 2025 cloud resilience report urges continuous control monitoring for systemic institutions.[2]U.S. Department of the Treasury, “Treasury Cloud Report,” home.treasury.gov Cloud vendors now bundle mapping templates for Basel III, PCI DSS, and GDPR into dashboards, cutting manual audit workloads by 40%. Banks with global footprints are standardizing on unified compliance fabrics so a single policy set satisfies overlapping jurisdictions—particularly valuable when customer data flows span the EU, the U.S., and Asia. Early adopters report faster product launches because embedded governance eliminates lengthy security-review cycles, turning compliance from a blocker into a revenue enabler.

Cost Avoidance Through Serverless and Container-Native Security Controls

Serverless models free banks from provisioning and patching hosts, trimming infrastructure bills by 35% while raising developer productivity by 25%. Container platforms deliver similar economies but stall if images lack baked-in controls; 67% of enterprises delayed shipments for security reasons, highlighting demand for integrated container scanning. One U.S. mid-tier bank shifted fraud-detection workloads to a serverless pipeline and saved USD 30 million annually, meeting GDPR encryption rules with minimal overhead. Isolation and immutable infrastructure shrink attack surfaces as functions spin up only when invoked, limiting lateral movement opportunities for attackers. With most banks targeting 80% cloud penetration by 2026, CFOs view serverless security as a hedge against margin pressure and ongoing capital-expenditure cuts.

Expansion of Open-Banking APIs Driving Zero-Trust Adoption

PSD2, PSD3, and similar regimes force banks to expose account data via APIs, inviting fintech partners, but also abuse. Europe now ranks third globally for API-layer attacks against financial services.[3]Akamai Technologies, “API Security in the Open Banking Ecosystem,” akamai.com Zero-trust architectures authenticate every call, apply micro-segmentation, and continuously inspect traffic using behavior baselines, offsetting the porous perimeter problem. At least 60% of large EU banks will have zero-trust frameworks in place by 2026 as they retrofit legacy authentication to FAPI and OAuth 2.0 profiles. The payoff is faster partner onboarding, reducing integration times from months to days, because granular policy engines mediate access without manual code review. Vendors that marry API gateways with adaptive MFA and real-time fraud scoring are gaining share, reflecting buyer demand for consolidated control planes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data residency conflicts with multi-tenant clouds | -2.8% | EU primary, Asia Pacific secondary | Long term (≥ 4 years) |

| Shortage of cloud-security-skilled talent | -3.1% | Global | Medium term (2-4 years) |

| Hidden dependencies in third-party fintech links | -1.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Residency Conflicts with Multi-Tenant Public Clouds

GDPR, China’s CSL, and India’s DPDP Act oblige banks to localize data, conflicting with global multi-tenant setups. Sovereign-cloud variants from hyperscalers promise metadata isolation and local key custody, yet still lack the granular placement controls some regulators demand. Smaller APAC markets often enforce data-center-in-country rules that erode economies of scale, nudging banks toward hybrid topologies where sensitive datasets stay on-prem or in local private regions. Resulting architectural complexity inflates cost and elevates configuration-error risk, adding drag to widespread cloud adoption plans. Policymakers are consulting with industry to refine residency stipulations so cyber resilience benefits outweigh jurisdictional concerns, but resolution is unlikely before the end of the decade.

Shortage of Cloud-Security-Skilled Talent in Banks’ SOC Teams

Seventy-six percent of financial institutions admit to a skills shortfall in cloud security, and only 14% feel fully staffed to address new threats. Traditional network-centric SOC playbooks do not translate neatly to container, serverless, and API ecosystems, leaving alert backlogs untriaged. Banks seek managed detection and response partners but must scrutinize external SOCs for regulatory alignment and data-handling safeguards. Automation is filling part of the gap: AI-driven event-correlation engines reduce alert volumes by 90%, freeing analysts for higher-value tasks. Large incumbents are also funding accelerated reskilling programs, covering certifications such as CCSP and Kubernetes security, yet the pipeline will lag demand into the medium term, according to workforce analysts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: IAM Dominance Amid Encryption Surge

Cloud Identity and Access Management accounted for 28.85% of the cloud security in banking industry share in 2025, reflecting banks’ shift from perimeter controls to identity-centric guardrails that authenticate users, services, and APIs at a millisecond scale. As distributed work models persist, IAM consolidates single sign-on, privileged access management, and device posture checks, forming the backbone of zero-trust programs. Vendors are now embedding continuous risk scoring and passwordless flows that trim login friction—a critical user-experience factor in consumer banking.

Cloud Encryption is the fastest segment, posting an 17.75% CAGR through 2031. Quantum threat awareness and stricter data protection statutes are prompting banks to implement hardware security modules and centralized key orchestration. The cloud security market size for encryption-focused products in the banking sector is forecast to rise alongside the implementation of quantum-safe algorithms across payment rails, positioning cryptography as both a compliance must-have and a competitive differentiator. Multi-party computation and format-preserving encryption are gaining traction, letting institutions analyze data without decrypting it, a breakthrough for cross-border fraud analytics and AI model training.

By Deployment Model: Hybrid Acceleration Challenges Public Dominance

Public-cloud implementations captured 61.55% of the cloud security market share in the banking industry in 2025, underscoring confidence in hyperscaler defenses, dedicated financial services regions, and shared-responsibility blueprints. Providers such as AWS and Microsoft report double-digit growth in bank workloads, aided by artifacts like PCI DSS on-demand audit packs that slice assessment times. However, the sovereign-cloud and regional-cloud variants illustrate that one model will not fit every jurisdiction, and exit-strategy testing, as demanded by U.K. supervisors, underscores residual concentration risk.

Hybrid-cloud installations are expanding at a 19.45% CAGR because they let banks meet data residency mandates while still bursting to public fabric for analytics surges. Containers and service meshes deliver workload portability, enabling stress-exit drills that shift traffic off a compromised provider within hours. As regulators scrutinize single-vendor dependencies, multi-cloud toolchains are becoming a broad metric for operational resilience, accelerating the procurement of abstraction layers that secure and orchestrate across providers.

By Security Service: Data Protection Leads Orchestration Growth

Data-security services held 31.35% of revenue in 2025, a natural outcome of regulations equating data mishandling with systemic risk. Tokenization, field-level encryption, and bring-your-own-key schemes are now standard for account data, cardholder information, and high-value payment messages. This priority is unlikely to wane as ransomware gangs pivot to double-extortion tactics that publicize stolen data.

Security monitoring and orchestration offerings are demonstrating a 19.65% CAGR because the cloud attack surface generates telemetry at a scale that human analysts cannot parse. Modern SIEM/SOAR stacks ingest logs from SaaS, PaaS, and IaaS layers, correlate events with threat intel, and launch automated containment playbooks. Banks deploying these stacks report cutting mean-time-to-detect from eight hours to thirty minutes while halving alert backlogs. With AI copilots now automatically packaging forensic context, orchestration is poised to surpass legacy log management in spending.

By Banking Type: Neobank Agility Drives Digital Transformation

Retail banking represented 38.25% of revenue in 2025 as mobile apps, instant payments, and card rails expose vast consumer attack surfaces. Phishing, credential stuffing, and account-takeover attacks grow in lockstep with digital volumes, keeping data-protection and anti-fraud at the top of spend lists. Established banks run parallel modernization tracks, replacing monolithic cores with microservices that assume pervasive encryption and identity federation.

Digital-only banks show a 19.05% CAGR, benefiting from greenfield technology stacks absent of mainframes. Their entire business rides on elastic compute and managed security services, making them early adopters of serverless WAFs, inline API discovery, and runtime container defense. Lessons learned cascade into the wider ecosystem as incumbents partner with or acquire fintech challengers to refresh legacy offerings, spreading cloud-native security patterns across the market.

Geography Analysis

North America dominated the cloud security market in banking industry, with a 36.85% share in 2025. A long-standing regulator-vendor dialogue, mature private-public threat-sharing, and USD 17 billion in annual tech spending at JPMorgan Chase underscore the depth of local demand. The U.S. Treasury’s 2025 cloud-resilience study formally encourages critical institutions to adopt a multi-cloud approach while implementing real-time monitoring pipelines, thereby accelerating orders for unified security stacks that can span multiple providers. Canadian regulators now explicitly reference zero-trust and secure-API norms in their open-banking guidance, signaling further momentum in investment.

The Asia-Pacific region is expected to deliver the fastest CAGR of 17.35% from 2026 to 2031, as regulators balance data localization with innovation. Japan’s consortium of regional banks adopted a shared hybrid platform running on IBM and Kyndryl infrastructure, illustrating collaborative approaches to cost-effective yet compliant security. Singapore’s national digital ID roll-out and Malaysia’s RMiT standard also drive the adoption of IAM and real-time monitoring, respectively. China’s multi-level protection scheme (MLPS 2.0) compels encryption, continuous monitoring, and onshore key custody, prompting providers to launch local-only regions with hardware attestation.

Europe is accelerating due to DORA and PSD2/PSD3. Italian bank Credem Banca migrated to a specialist security cloud that embeds encryption and real-time incident notification, achieving 20% faster regulatory reporting. The Thales 2024 study notes that 65% of European firms rank cloud security as their second-largest cybersecurity priority, indicating a board-level focus. Multi-cloud resilience drills and sovereign-cloud pilots are now contractual requirements, spurring demand for orchestration layers that enforce policies across Amazon, Microsoft, and Google environments without manual rule duplication.

Regulatory Landscape

Bank cloud-security programs are increasingly framed around operational resilience and third-party ICT risk mandates. In the EU, the Digital Operational Resilience Act (DORA) has applied since 17 January 2025, reinforcing requirements for ICT risk management, severe incident reporting, and governance over critical ICT third-party providers, with concrete controls around encryption and cryptographic key protections based on risk assessment and data classification.

Implementation detail is also tightening through supporting measures and supervisory guidance. Commission Implementing Regulation (EU) 2024/2956 (adopted 29 November 2024) sets standard templates for the register of information on contractual arrangements with ICT third-party providers, and the EBA ICT and security risk management guidelines (EBA/GL/2025/02) include a supervisor notification milestone by 20 May 2025. In parallel, the EBA Guidelines on Outsourcing Arrangements (EBA/GL/2019/02) continue to anchor expectations around documented and tested exit strategies for outsourced cloud functions, which raises demand for continuous compliance evidence, workload portability, and auditable third-party oversight.

Value Chain Analysis

The value chain begins with hyperscale infrastructure and platform providers (AWS, Google Cloud, Microsoft Azure, IBM, Oracle) supplying compute, storage, networking, and cloud-native security primitives (IAM, key management, logging, confidential computing) that underpin banking workloads. Security software and managed-service layers sit above this infrastructure, including CNAPP, CASB/SSE, SIEM/SOAR, encryption and key orchestration, API security, and fraud-analytics tooling, delivered by security vendors directly or via cloud marketplaces. System integrators and consultants (for example, Accenture) contribute to architecture design, migration, policy-as-code implementation, and run operations, while banks stay accountable for governance, risk, and compliance under shared-responsibility models.

Across the chain, regulation and concentration risk management increasingly shape where value is created and captured. The ECB has formalized supervisory expectations on cloud outsourcing and finalized its Guide on outsourcing cloud services (July 2025), pushing banks and suppliers toward more transparent subcontracting chains, measurable resilience controls, and tested exit plans. In the UK, the designation and direct oversight of Critical Third Parties covering major cloud providers from July 2026 adds a new control point that affects provider assurance artifacts, audit cooperation, and operational-resilience testing, with knock-on effects for banks procurement, vendor-management workflows, and security telemetry integration across multi-cloud estates.

Competitive Landscape

The cloud security in banking industry is moderately consolidated. Mega-vendors combine organically built capabilities with acquisitions such as Google Cloud’s purchase of Wiz, adding real-time risk scoring and sector-specific compliance dashboards. Palo Alto Networks’ buyout of IBM’s QRadar SaaS tightens the link between XDR and SIEM, enabling breach-detection cycles to shrink from days to hours. Banks favor these suites over point products because licensing simplicity and shared data lakes cut the integration burden.

Hyperscalers are embedding advanced controls natively, confidential computing, workload identity federation, and post-quantum encryption toolkits, using their infrastructure scale to undercut niche vendors. Traditional security providers respond by layering policy-as-code, real-time attack-path mapping, and AI copilots onto their existing portfolios. Identity specialists like Ping Identity and Okta deepen their ties with FIDO Alliance members to push passwordless flows, which are critical for the retail-bank user experience.

Innovative start-ups still find white-space in API security, developer-first SBOM validation, and quantum-resistant key management. However, exit valuations now factor in banking-specific compliance libraries, third-party assessment portals, and proven reference wins with tier-1 institutions. Vendors lacking these artifacts face tougher RFP slates as banks consolidate suppliers to manage third-party exposure and trim vendor-management overhead.

Cloud Security In Banking Market Leaders

AWS (Amazon.com, Inc.)

Google Cloud Platform (Alphabet Inc.)

Microsoft Azure (Microsoft Corporation)

IBM Cloud Security (IBM Corporation)

Oracle Cloud (Oracle Corporation)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Operational resilience regimes are creating whitespace for automated compliance, third-party risk visibility, and cross-cloud control enforcement. DORA obligations (in force since January 2025) and related EU technical standards that standardize third-party registers and supplier risk data are pushing banks to industrialize evidence collection, encryption and key governance, and audit-ready reporting across hybrid and multi-cloud footprints. The UK Critical Third Parties regime initiated in July 2026 extends scrutiny directly to major cloud providers, increasing demand for interoperable monitoring, exit-readiness tooling, and standardized assurance packages that banks can reuse across suppliers and jurisdictions.

Security capability is also being pulled forward by large-scale banking migrations and AI adoption programs that expand the cloud attack surface (APIs, containers, and AI pipelines), raising the need for continuous controls. In 2026, U.S. Bank expanded its collaboration with AWS to migrate hundreds of mission-critical applications under a secure and compliant foundation, and HSBC announced a multi-year partnership with Google Cloud centered on AI-enabled capabilities across operations. These initiatives support opportunities for integrated stacks combining IAM, data security (tokenization, encryption, BYOK/HSM), API protection, and SIEM/SOAR with AI-driven detection, alongside managed services that address the documented skills gap in bank SOC teams.

Recent Industry Developments

- June 2026: HSBC announced a multi-year partnership with Google Cloud to deploy AI across its global operations, positioning AI tooling alongside security and control requirements for regulated banking workflows. The program broadens the scope of cloud security demand to include governance of AI use cases, data protection, and operational controls embedded into cloud platforms.

- May 2026: Migration of hundreds of mission-critical applications to AWS expanded as part of U.S. Bank's broader cloud modernization, including payments and wealth management platforms. The expansion elevates requirements for cloud-native security controls, continuous compliance, and resilient operations at scale as more sensitive banking workloads shift onto public-cloud foundations.

- June 2025: OneSpan acquired Nok Nok Labs to expand passwordless authentication capabilities aligned with FIDO standards for banking customers. The acquisition strengthens identity-centric security programs in banks by consolidating authentication technology and accelerating adoption of phishing-resistant, passwordless access models within zero-trust architectures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market counts spending by banks on cloud security tools and security services that protect data, identities, and workloads running on public, private, or hybrid cloud environments.

Scope exclusions: It does not include stand-alone on-premise security appliances, and it does not include non-banking financial services security budgets that are not tied to banking cloud workloads.

Segmentation Overview

- By Software Type

- Cloud Identity and Access Management (IAM)

- Cloud Email Security

- Cloud Intrusion Detection and Prevention (IDPS)

- Cloud Encryption

- Cloud Network Security

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Security Service

- Data Security

- Application Security

- Network Security

- Security Monitoring and Orchestration (SIEM/SOAR)

- Identity, Authentication and Fraud Analytics

- By Banking Type

- Retail/Consumer Banking

- Corporate and Investment Banking

- Card and Payment Service Providers

- Digital-Only/Neobanks

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start with public data that helps anchor the banking and cloud context, and then we map what portion is realistically attributable to cloud security. Useful inputs come from sources such as the Federal Financial Institutions Examination Council (FFIEC) guidance, NIST publications, the European Banking Authority (EBA) and ECB cloud outsourcing expectations, and BIS/FSB papers on operational resilience.

To keep definitions consistent, we also use bank annual reports, 10-K style filings, and security and cloud risk disclosures, plus earnings presentations that discuss cloud migration and security spending priorities. Where available, we check patents, peer-reviewed journals on cloud security controls, and public procurement or tender notices to understand adoption patterns and pricing direction. We also use paid subscriptions for company financials and intelligence, patent databases, and a shipment-level import export database when hardware-linked security components appear in bundled contracts. This list is not exhaustive, and many other public and paid sources were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Our model assumptions are validated through expert conversations and structured surveys with cloud security practitioners, banking technology leaders, and risk and compliance stakeholders, plus channel-side implementation teams. Because cloud adoption maturity differs across geography and bank size, inputs were cross-checked across APAC, EMEA, and the Americas before finalizing growth, pricing, and mix assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 18% | Managers: 55% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where banking cloud footprint indicators and security spend signals are reconstructed into a cloud-security demand pool, and then split by solution and service intensity. The totals are then corroborated with selective bottom-up approximations, such as sampled pricing for key cloud security controls (IAM, encryption, workload protection, cloud email security, and SIEM-related use) multiplied by adoption ranges, followed by channel checks to adjust outliers.

A few inputs that mattered most were the pace of cloud workload migration in banks, regulatory pressure on outsourcing and data protection, incident and breach disclosure trends, identity and access modernization cycles, and typical contract lengths for managed security services. Where spending is bundled in broader cyber programs, we handle gaps by allocating only the cloud-addressable part using interview-based split factors, and then stress-testing those splits against bank IT spending commentary.

For forecasting, we used scenario analysis supported by a light multivariate regression view, where cloud workload growth, security headcount constraints, and compliance timelines were the key explanatory variables. The final path reflects what practitioners expect on renewal uplifts, new module attach rates, and the gradual shift from point tools toward more integrated cloud security stacks.

Data Validation & Update Cycle

Numbers are validated through multiple checks, including variance scans against independent indicators such as banking cloud adoption signals, security budget guidance, and reported cloud risk priorities. When a segment grows faster than the surrounding inputs can support, the assumptions are revisited, and follow-up calls are triggered to confirm whether the change is real or driven by a definition mismatch.

Before sign-off, the model is reviewed in steps by another analyst to catch logic breaks, currency conversion issues, and double-counting between software and managed services. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory changes or sharp pricing resets. Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Banking Cloud Security Market Size Compared With Other Published Estimates

Published market values for cloud security in banking can look far apart because the boundaries and timing are not always aligned, even when the topic label looks similar. Differences usually come from what is counted as cloud security, which banking entities are included, and how currency and price changes are treated.

In our refresh-led workflow, assumptions like subscription price progression, contract renewal uplifts, and currency conversion timing are rechecked close to publication, which helps reduce drift in fast-moving security categories, a step that is applied consistently by Mordor Intelligence. Some other estimates use longer refresh gaps, treat bundled security and cloud spend as fully attributable, or keep flat average selling prices even when solution mix shifts toward higher-value controls.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 42.35 B (2026) | |

| Global Research House A | USD 14.22 B (2025) | Uses a different base year and a longer forecast window, and the scope appears to be narrower around selected cloud security solution categories, which can understate managed services and broader bank workload coverage. |

| Industry Publisher B | USD 42.80 B (2025) | Reports a higher current-year value with a nearby year, and the definition likely includes a wider set of banking cloud security spend buckets, where bundled security programs and cloud database security may be allocated more aggressively. |

The table shows that year selection and what gets allocated into cloud security budgets can move the headline number a lot. By keeping the scope tied to banking cloud workloads and rechecking pricing and currency assumptions during updates, we keep a practical estimate that can be traced back to clear drivers and verified through repeatable checks.

Key Questions Answered in the Report

What is driving rapid growth in the cloud security in banking industry?

Growth stems from stricter regulations such as DORA, rising ransomware attacks that hit 78% of banks in 2024, and cost savings of up to 35% achieved through serverless and container security controls.

Which software segment dominates cloud security spending by banks?

Cloud Identity & Access Management leads with 28.85% of 2025 revenue thanks to its role in zero-trust architectures and remote-work authentication.

Why are hybrid-cloud deployments accelerating in banking?

Hybrid layouts satisfy data-residency laws while letting banks burst to public clouds for analytics, driving a 19.45% CAGR through 2031.

How are talent shortages affecting bank security operations?

With only 14% of institutions fully staffed, banks adopt AI-driven orchestration and managed detection services to close expertise gaps.

Which region is expanding fastest for cloud security adoption in banking?

Asia-Pacific shows a 17.35% CAGR to 2031, spurred by mobile-first banking and new localization mandates across Japan, Singapore and China.

What role does AI play in future cloud security platforms for banks?

AI supports anomaly detection, fraud analytics and compliance automation, with vendors embedding generative-AI safeguards and machine learning that cut mean-time-to-detect to under 30 minutes.

Page last updated on: