Cloud Endpoint Protection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

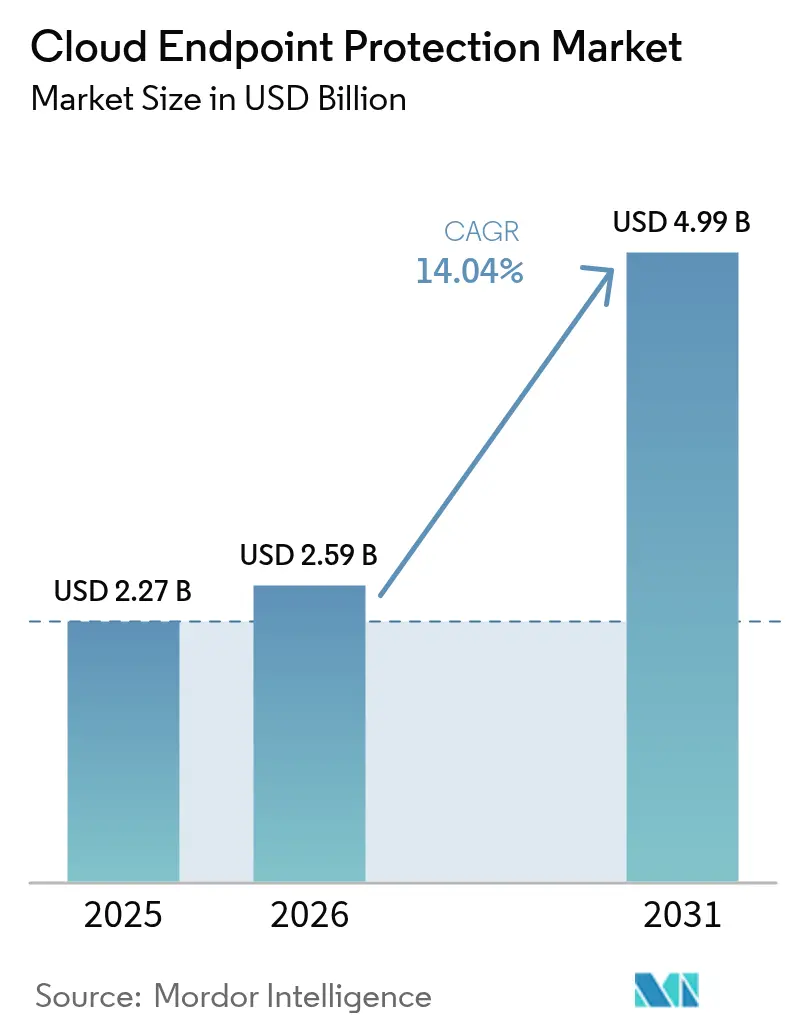

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 4.99 Billion |

| Growth Rate (2026 - 2031) | 14.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Endpoint Protection Market Analysis by Mordor Intelligence

cloud endpoint protection market size in 2026 is estimated at USD 2.59 billion, growing from 2025 value of USD 2.27 billion with 2031 projections showing USD 4.99 billion, growing at 14.04% CAGR over 2026-2031. The surge is explained by the rapid expansion of distributed workforces, cloud-native workloads, and the board-level push toward Zero Trust architecture. Large public-sector investments reinforce demand; for example, the U.S. Department of the Interior raised its FY 2025 cybersecurity allocation to USD 67.8 million, up USD 23.4 million solely for Zero Trust implementation [1]U.S. Department of the Interior, “FY 2025 Budget Justification and Performance Information,” doi.gov. Intensifying regulatory pressure such as the EU NIS2 Directive plus the HIPAA Security Rule proposals is sustaining double-digit adoption curves [2]Federal Register, “HIPAA Security Rule To Strengthen the Cybersecurity of Electronic Protected Health Information,” federalregister.gov. At the same time, AI-enhanced threats and the global cyber-talent shortage are accelerating managed detection and response outsourcing—especially across small and medium enterprises—thus broadening the addressable cloud endpoint protection market. Competitive dynamics tightened after CrowdStrike’s July 2024 outage, which triggered vendor diversification and catalyzed investment in AI-driven Extended Detection and Response (XDR) platforms.

Key Report Takeaways

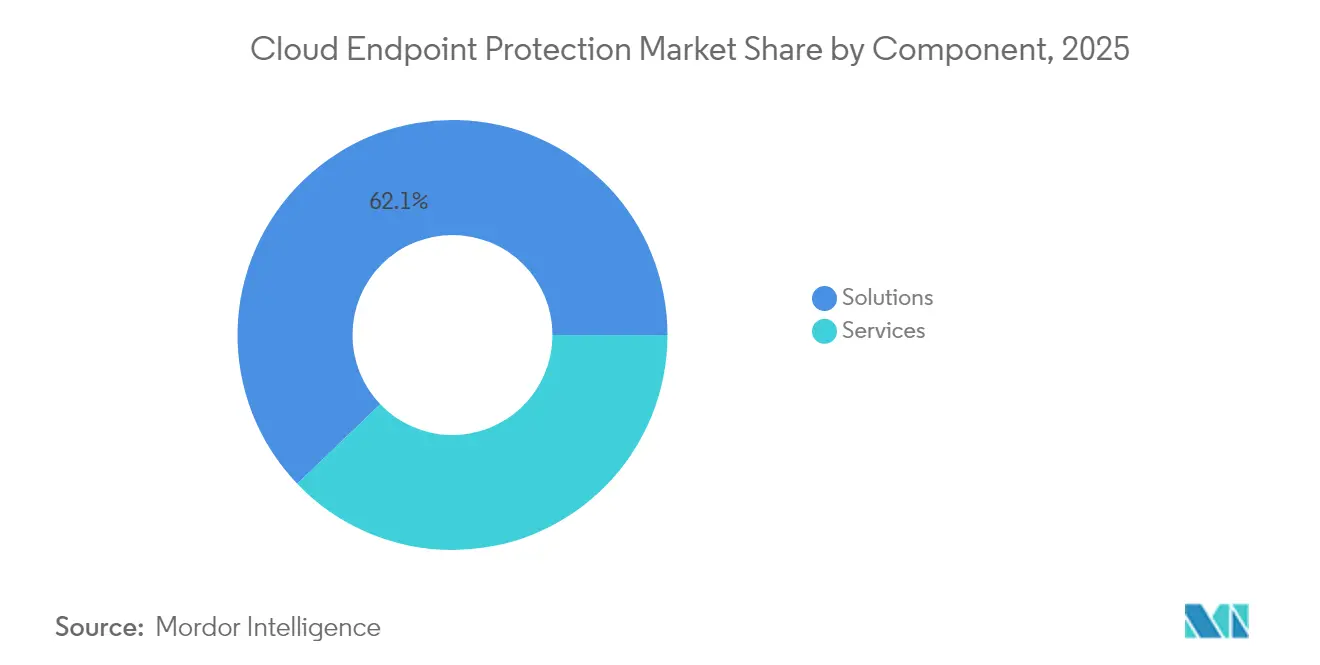

- By component, solutions held 62.15% of the cloud endpoint protection market share in 2025, whereas services are set to expand at a 14.72% CAGR to 2031.

- By enterprise size, large enterprises captured 57.45% of the cloud endpoint protection market share in 2025, while small and medium enterprises are forecast to grow at a 16.65% CAGR through 2031.

- By deployment model, public cloud led with 48.86% revenue share in 2025; hybrid cloud is projected to climb at an 17.35% CAGR through 2031.

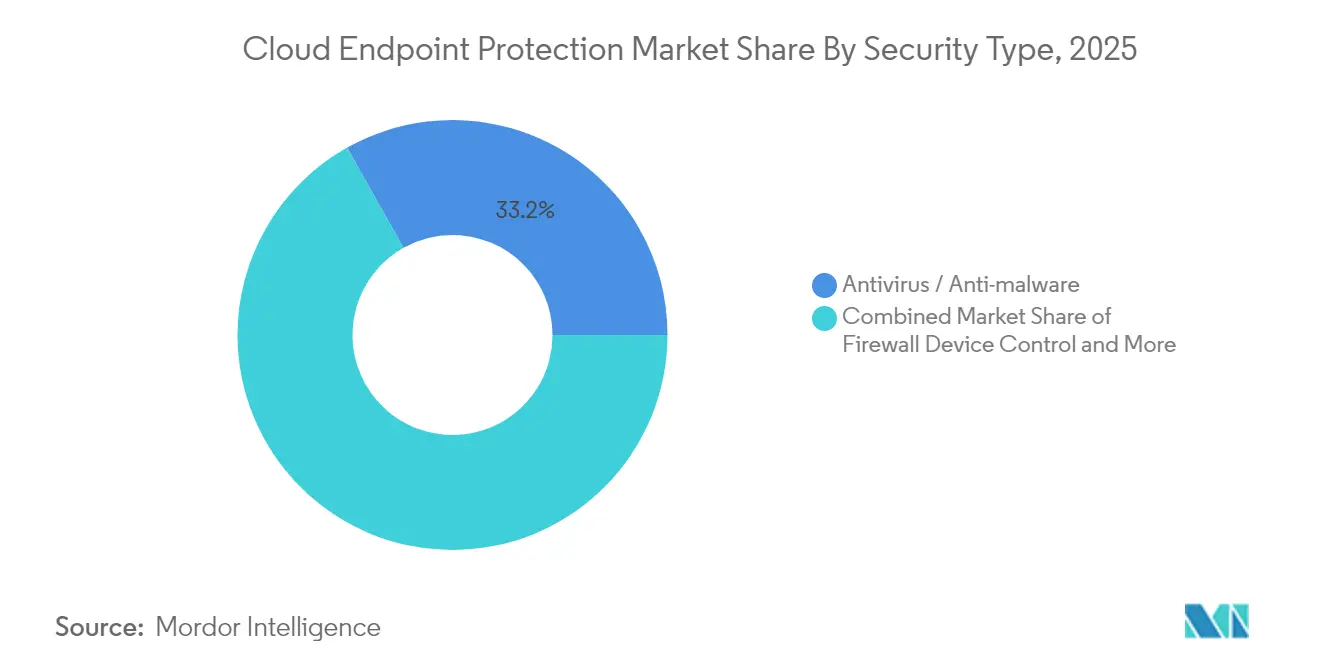

- By security type, antivirus and anti-malware still account for 33.15% of 2025 revenue, acting as baseline hygiene. However, EDR’s 20.95% CAGR signals a profound pivot to behavioral analytics and automated remediation. The cloud endpoint protection market size tied to EDR is projected to exceed USD 2.08 billion by 2031,

- By end-user industry, the BFSI sector accounted for a 24.95% slice of the cloud endpoint protection market size in 2025; healthcare is advancing at an 17.55% CAGR to 2031.

- By geography, North America delivered 40.35% of the cloud endpoint protection market size in 2025,

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Endpoint Protection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of remote work & BYOD | +2.8% | North America & Europe, global reach | Medium term (2-4 years) |

| Surge in sophisticated cyber-attacks & data breaches | +3.2% | APAC & North America | Short term (≤ 2 years) |

| Regulatory mandates for data protection & privacy | +2.1% | Europe & North America expanding to APAC | Long term (≥ 4 years) |

| Cost-saving scalability of SaaS security | +1.9% | SME-heavy regions worldwide | Medium term (2-4 years) |

| Integration of XDR & AI-driven automation | +2.4% | North America & Europe, emerging APAC | Medium term (2-4 years) |

| Zero Trust accelerates endpoint upgrades | +1.8% | Government & enterprise sectors worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of remote work & BYOD

The normalization of hybrid schedules has erased the traditional network perimeter, forcing security teams to protect devices that rarely touch the corporate LAN. Microsoft’s Secure Future Initiative demonstrates how hyperscalers embed protection across cloud assets to secure any endpoint, anywhere [3] Microsoft Corporation, “Microsoft 2024 Annual Report,” microsoft.com. Cisco’s Zero Trust Architecture Guide stresses device-level verification in Bring-Your-Own-Device environments. The outcome is a decisive shift toward unified platforms that merge endpoint protection, identity, and remote access functions, thereby enlarging the cloud endpoint protection market.

Surge in sophisticated cyber-attacks & data breaches

AI-enabled adversaries employ deep-fake lures, living-off-the-land payloads, and multistage ransomware. Proofpoint logged a 600% spike in deep-fake scam chatter in APAC during 2024. China-linked actors sustained five years of clandestine campaigns targeting unpatched edge devices. Vendors answer with AI-driven XDR that stitches telemetry across endpoints and cloud workloads to automate triage, cementing buyer preference for cloud-delivered endpoint security.

Regulatory mandates for data protection & privacy

The NIS2 Directive obliges European firms to institute “state-of-the-art” defenses or risk fines up to EUR 10 million (USD 11 million). In the United States, proposed HIPAA Security Rule changes impose first-year compliance costs of USD 9 billion, compelling health systems to upgrade endpoint defenses. Compliance deadlines therefore act as a predictable growth trigger for the cloud endpoint protection market.

Cost-saving scalability of SaaS-based security models

Subscription delivery lowers capital outlays and taps external expertise. LevelBlue’s partner program converts resellers into MSSPs offering 24×7 monitoring and response capabilities. SonicWall notes mounting SMB adoption of Managed Detection and Response as staffing constraints bite. SaaS scalability is therefore integral to the expansion of the cloud endpoint protection market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-talent shortage inflates service costs | -2.40% | Global; acute in North America & Europe | Short to medium term (1–3 yrs) |

| Deployment complexity in multi-cloud estates | -1.90% | Global | Medium term (2–4 yrs) |

| Price sensitivity among SMEs | -1.50% | Global; strongest in emerging markets | Medium term (2–4 yrs) |

| Scrutiny of telemetry-data privacy in security tools | -1.30% | Europe, regulated sectors globally | Short to medium term (1–3 yrs) |

| Source: Mordor Intelligence | |||

Cyber-talent shortage inflates service costs

The worldwide shortfall of qualified defenders raises billable rates for incident response and managed services, squeezing budgets even as threat volumes climb. Microsoft pledged to train 250,000 U.S. practitioners by 2025 to alleviate the pinch. Elevated labor pricing curbs spending elasticity, moderating near-term growth within the cloud endpoint protection market.

Deployment complexity in multi-cloud estates

Enterprises juggling AWS, Azure, and private clouds struggle to unify policy, visibility, and incident response. Cisco’s IT/OT convergence study highlights the operational friction when security tooling varies by environment.. Integration overhead prolongs rollouts and defers value realization, restraining a portion of the cloud endpoint protection market’s upside.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Surge Despite Solutions Dominance

Solutions generated the largest slice of the cloud endpoint protection market translating into 62.15% revenue share. Core detection, response, and anti-malware engines remain indispensable building blocks, yet buyers now evaluate them through an AI-first lens. Endpoint Detection and Response modules are evolving rapidly, with CrowdStrike patenting workflow automation that speeds analyst triage. Managed services, by contrast, posted the steepest 14.72% CAGR as organizations grapple with talent shortages and regulatory audits that demand 24×7 coverage.

The services boom is anchored by turnkey MDR, integration, and training offerings. LevelBlue’s MSSP transition blueprint exemplifies how channel partners monetize recurring revenue via remote SOC operations. Vendors are bundling advisory services—policy tuning, Zero Trust road-mapping, compliance reporting—to maximize lifetime value, thereby cementing services as a structural driver within the cloud endpoint protection market.

By Enterprise Size: SME Acceleration Challenges Large-Enterprise Dominance

Large enterprises contributed 57.45% of the cloud endpoint protection market share in 2025, underpinned by multi-million-dollar security budgets and appetites for early-stage innovation. Their pilots often shape vendor product-roadmaps, especially around AI-assisted threat hunting. Yet SMEs scored a 16.65% CAGR, proving that SaaS pricing and outsourced SOCs democratize sophisticated defenses. SonicWall confirms heightened SMB uptake of EDR capabilities once considered “big-bank only”.

Cost predictability and rapid onboarding make subscription models appealing to finance-constrained firms. Meanwhile, compliance automation embedded in cloud consoles eases audit anxiety. Hence the SME segment is reshaping go-to-market tactics across the cloud endpoint protection market, prompting vendors to launch one-click packages with usage-based billing and curated playbooks.

By Deployment Model: Hybrid Cloud Emerges as Strategic Bridge

Public cloud retained 48.86% revenue share, but hybrid architectures are accelerating at an 17.35% CAGR as boards demand workload portability and regulatory alignment. The cloud endpoint protection market size linked to hybrid deployments is estimated to climb from USD 1.01 billion in 2025 to USD 2.64 billion by 2031. Microsoft’s USD 20 billion-plus security revenue underscores the economic might of hyperscale platforms that embed endpoint defense deep inside their fabrics.

Yet sensitive datasets in finance, healthcare, and government remain anchored on-premises, driving demand for unified consoles that span legacy data centers and SaaS estates. Fortinet’s Security Fabric meshes firewall, endpoint, and network analytics across campus, cloud, and edge topologies. Consequently, hybrid solutions form the linchpin of multi-cloud security orchestration within the cloud endpoint protection market.

By Security Type: EDR Revolution Transforms Traditional Antivirus

Antivirus and anti-malware still account for 33.15% of 2025 revenue, acting as baseline hygiene. However, EDR’s 20.95% CAGR signals a profound pivot to behavioral analytics and automated remediation. The cloud endpoint protection market size tied to EDR is projected to exceed USD 2.08 billion by 2031, reflecting deep buyer confidence in AI techniques that surface zero-day threats. Palo Alto Networks frames AI as indispensable for eliminating manual triage delays.

Complementary technologies—device control, anti-phishing, and next-gen firewall—are converging into unified agents that share telemetry with XDR back-ends. Fortinet’s workspace security suite extends protection to browsers and collaboration apps, underscoring the broadening remit of endpoint platforms. Consolidation simplifies procurement and elevates cross-control efficacy inside the cloud endpoint protection market.

By End-User Industry: Healthcare Acceleration Challenges BFSI Leadership

BFSI held 24.95% share in 2025 due to strict governance and high-value digital assets. Yet healthcare’s 17.55% CAGR is outpacing all other verticals, propelled by HIPAA modernization that earmarks USD 9 billion in first-year security spend. Medical IoT devices introduce fresh attack vectors, turning endpoint controls into patient-safety imperatives.

Manufacturing, energy, and retail likewise expand deployments as IT/OT convergence and customer privacy mandates materialize. Government programs—from the U.S. Zero Trust memo to EU cyber-resilience acts—continue to establish baseline requirements that reinforce growth trajectories across every sector, bolstering the overall cloud endpoint protection market.

Geography Analysis

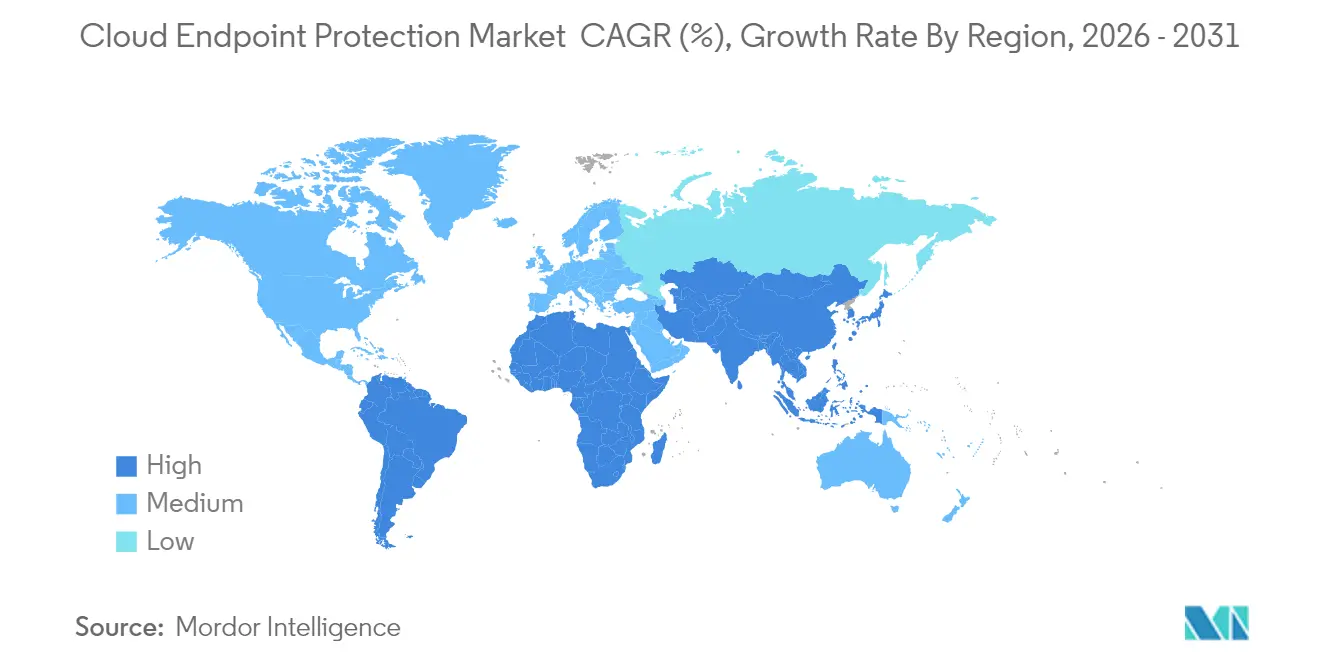

North America generated 40.35% of 2025 revenue owing to mature regulatory regimes and long-standing investments in cloud security. Federal Zero Trust blueprints and large-scale SaaS adoption keep refresh cycles brisk. The region’s enterprises adopted AI-driven XDR platforms early, shaping feature roadmaps and anchoring spend on next-generation endpoint suites. Venture capital funding and cybersecurity start-up density further fertilize innovation, strengthening North America’s position within the cloud endpoint protection market.

Asia-Pacific is the fastest-growing theatre, expanding at a 14.88% CAGR. The region benefits from hyperscaler capital flows such as Microsoft’s USD 2.2 billion Malaysian AI hub, Amazon’s USD 12.7 billion India build-out, and Google’s USD 6.7 billion Singapore expansion. A pronounced spike in ransomware and deep-fake scams compels enterprises to adopt advanced EDR and XDR capabilities, making APAC the next frontier for the cloud endpoint protection market.

Europe commands steady growth underpinned by the NIS2 Directive’s stringent penalties. Germany, the United Kingdom, and France spearhead adoption of AI-centric endpoint technologies to meet “state-of-the-art” compliance thresholds. Data-sovereignty sensitivities drive demand for vendors that can localize telemetry and sustain residency assurances, ensuring the region remains strategically salient in the cloud endpoint protection market.

Competitive Landscape

The market is moderately consolidated yet fiercely innovative. CrowdStrike’s 2024 platform outage exposed systemic concentration risk and prompted many enterprises to diversify endpoint suppliers. Palo Alto Networks quickly capitalized, acquiring Protect AI for USD 700 million to infuse AI security into its Cortex stack. Check Point’s Veriti buy extends exposure-management across multi-vendor estates, signaling a pivot toward consolidation of control planes.

Microsoft wields ecosystem reach, bundling Defender for Endpoint with Office 365, Azure, and Entra to deliver cross-stack synergies that small competitors struggle to match. Fortinet differentiates through ASIC performance and an integrated fabric that spans firewall, LAN, and endpoint. Up-and-coming players such as Arctic Wolf and Mind capitalise on data-loss prevention and workflow patents, injecting fresh IP into the cloud endpoint protection industry.

Vendor roadmaps converge around AI orchestration, open APIs, and vertically-tuned analytics. Healthcare, industrial, and public-sector blue-ocean spaces invite specialized modules—HIPAA reporting dashboards, SCADA protocol inspection, or CJIS compliance—to erect moats and expand total addressable share. M&A activity is anticipated to remain brisk as larger suites absorb niche innovators to shorten time-to-capability and protect gross margins.

Cloud Endpoint Protection Industry Leaders

Microsoft Corporation

CrowdStrike Holdings, Inc.

Cisco

Palo Alto Networks

Trend Micro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fortinet rolled out its AI-powered Workspace Security suite, adding browser and collaboration protection for hybrid workers

- May 2025: Check Point agreed to acquire Veriti Cybersecurity to harden Infinity with automated threat-exposure management

- May 2025: Fortinet debuted the FortiGate 700G hybrid mesh firewall featuring post-quantum cryptography readiness

- May 2025: IGEL purchased Stratodesk to enrich secure client OS and endpoint-management functions for cloud workspaces

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cloud endpoint protection market as subscription-based software and managed services that monitor, prevent, detect, and remediate threats on laptops, desktops, virtual machines, and mobile devices whenever the control plane is delivered from public, private, or hybrid cloud platforms. We count revenues that vendors book from cloud-hosted licences, SaaS seats, and related support in the invoicing year.

Scope Exclusions: Hardware appliances, pure on-premise endpoint security suites, and network-centric gateways are not included.

Segmentation Overview

- By Component

- Solutions

- Antivirus / Anti-malware

- Endpoint Detection and Response (EDR)

- Firewall

- Application / Device Control

- Services

- Managed Services

- Consulting and Integration

- Training and Support

- Solutions

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Security Type

- Antivirus / Anti-malware

- Endpoint Detection and Response

- Firewall

- Device Control

- Anti-phishing

- Application Control

- Others

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- Government

- Healthcare

- Energy and Power

- Retail and E-commerce

- IT and Telecom

- Manufacturing

- Education

- Media and Entertainment

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia

- China

- India

- Japan

- South Korea

- Southeast Asia

- Rest of Asia

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed CISOs, managed security service providers, and channel partners across North America, Europe, and Asia-Pacific to validate cloud seat penetration, blended pricing, and renewal ratios. Short web surveys with SME IT managers filled adoption and pricing gaps that seldom surface in public filings.

Desk Research

We began by extracting breach volumes, device stocks, and regulatory updates from ENISA, CISA, India-CERT, and NIST. Sector signals were obtained from the Cloud Security Alliance, the Financial Services ISAC, and the Health-ISAC. Company 10-Ks, investor decks, and earnings calls anchored vendor cloud annual recurring revenue, while Volza shipment logs and Questel patent analytics indicated supply momentum. Dow Jones Factiva news feeds and IEEE journals rounded out technology trend tracking. The sources listed are illustrative; numerous additional references supported data collection and cross-checks.

Market-Sizing & Forecasting

A top-down model converts active enterprise endpoint counts, derived from labor force and device penetration statistics, into a demand pool that is then multiplied by verified cloud adoption rates and blended average selling prices. Supplier revenue roll-ups and channel checks serve as bottom-up guardrails before totals are finalized. Key variables like remote work share, hybrid-cloud adoption, breach frequency, and regulatory rollout timelines feed a multivariate regression and scenario analysis engine. Residual gaps are smoothed through proportionate allocation using regional SaaS revenue mixes.

Data Validation & Update Cycle

Outputs pass anomaly tests, peer review, and management sign-off. Models refresh every year, and interim revisions follow material vendor restatements or major cyber incidents so clients receive the most up-to-date view.

Why Mordor's Cloud Endpoint Protection Baseline Earns Trust

Published estimates often diverge because providers apply different scopes, pricing bases, and refresh cadences.

By focusing strictly on cloud-delivered revenues and by recalibrating device counts annually, we keep our baseline aligned with market reality.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.27 B (2025) | Mordor Intelligence | - |

| USD 5.50 B (2024) | Regional Consultancy A | Includes on-premise EPP and bundled gateways |

| USD 16.36 B (2024) | Global Consultancy B | Uses device shipments instead of active seats and ignores churn |

| USD 27.46 B (2025) | Industry Journal C | Measures full endpoint security stack, not cloud-only |

These contrasts show that Mordor's focused scope, dual-pass validation, and live device metrics provide a balanced, transparent baseline that decision-makers can rely on.

Key Questions Answered in the Report

What impact did the 2024 CrowdStrike outage have on market dynamics?

The incident triggered vendor diversification, increased federal scrutiny, and accelerated investments in AI-driven XDR alternatives.

What is the projected size of the cloud endpoint protection market by 2031?

The cloud endpoint protection market size is forecast to reach USD 4.99 billion by 2031.

Which component is growing fastest within the cloud endpoint protection market?

Services, especially managed detection and response, are expanding at a 14.72% CAGR.

Why is healthcare the fastest-growing end-user segment?

New HIPAA Security Rule proposals require USD 9 billion in first-year cybersecurity investments, pushing 17.55% CAGR adoption.

How does hybrid cloud deployment influence endpoint security buying?

Hybrid environments demand unified consoles that span on-premises and public clouds, driving an 17.35% CAGR for hybrid solutions.

Page last updated on: