Cloud Workload Protection Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

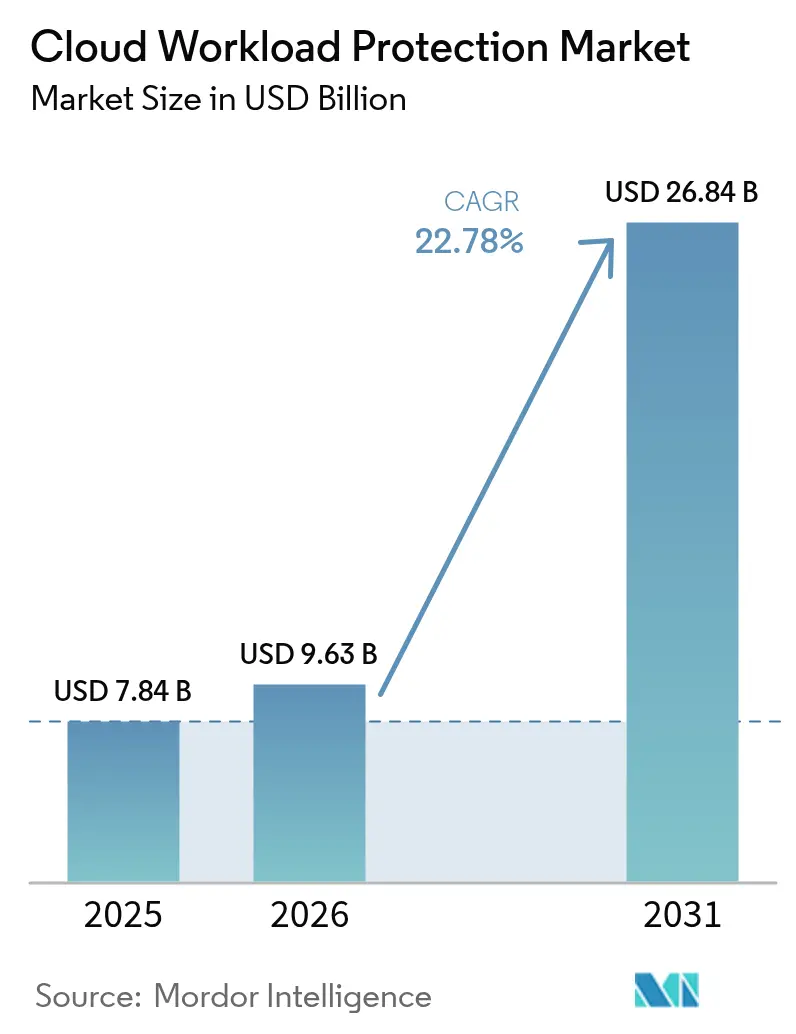

| Market Size (2026) | USD 9.63 Billion |

| Market Size (2031) | USD 26.84 Billion |

| Growth Rate (2026 - 2031) | 22.78% CAGR |

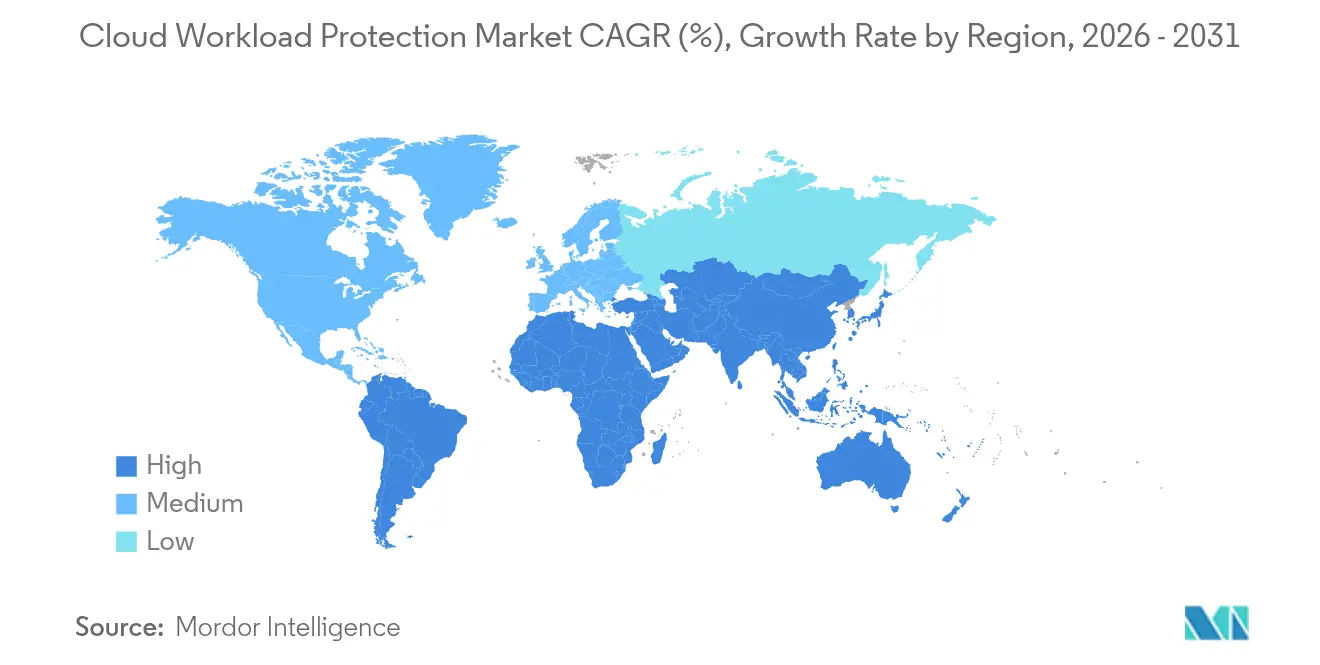

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

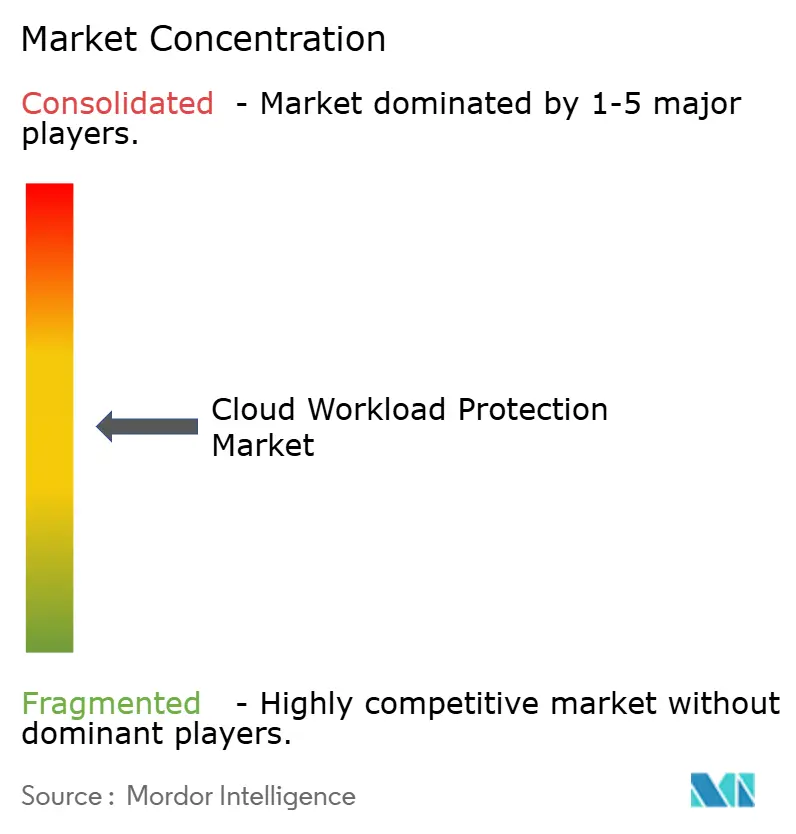

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Workload Protection Market Analysis by Mordor Intelligence

The Cloud Workload Protection market size is expected to grow from USD 7.84 billion in 2025 to USD 9.63 billion in 2026 and is forecast to reach USD 26.84 billion by 2031 at 22.78% CAGR over 2026-2031. Demand accelerates as enterprises replace perimeter-centric defenses with runtime controls that secure highly distributed workloads. Real-time telemetry from extended Berkeley Packet Filter (eBPF) technology, the rapid roll-out of cloud-native application protection platforms (CNAPP), and convergence with DevSecOps pipelines reshape competitive playbooks. Multi-cloud adoption, hybrid deployment flexibility, and compliance-driven purchasing in regulated verticals sustain double-digit expansion while kernel-level observability raises performance expectations. The cloud workload protection market now favors unified platforms that reduce tool sprawl, simplify agent management, and extend protection to containers, serverless functions, and AI workloads.

Key Report Takeaways

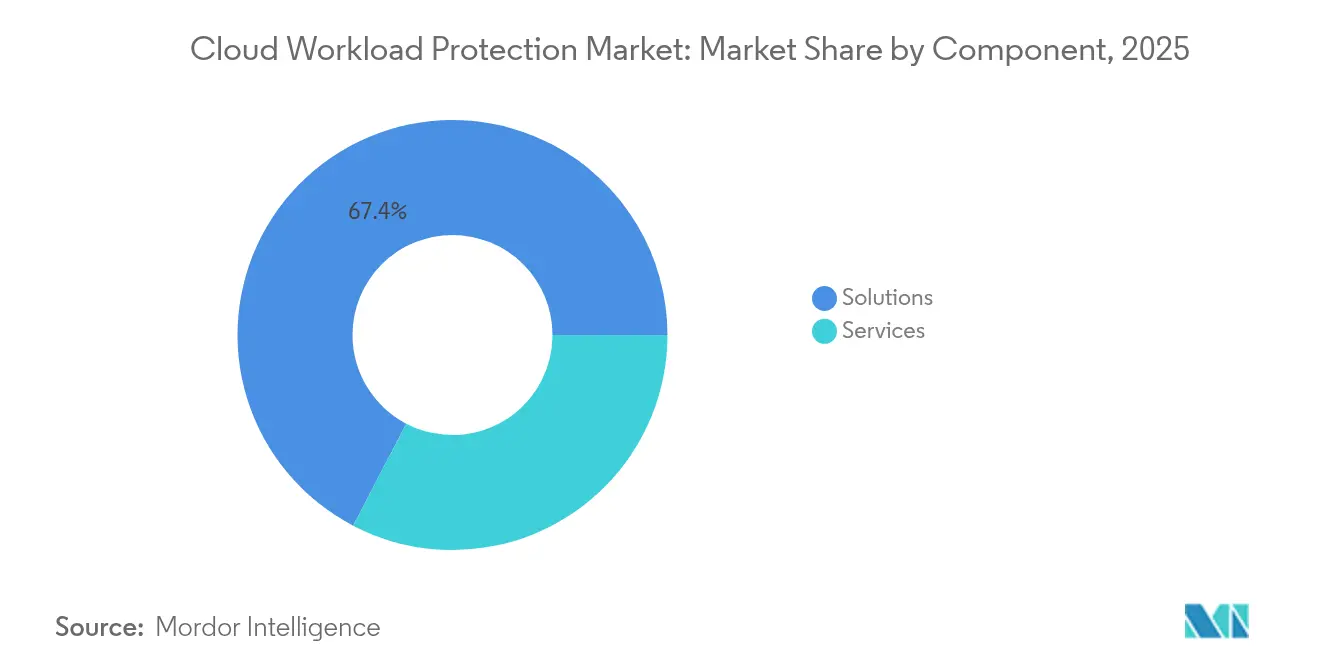

- By component, solutions held 67.35% of the cloud workload protection market share in 2025; threat detection and incident response is forecast to grow at 27.29% CAGR through 2031.

- By security architecture, agent-based deployments captured 63.25% of the cloud workload protection market share in 2025, while agentless models are expanding at 31.15% CAGR to 2031.

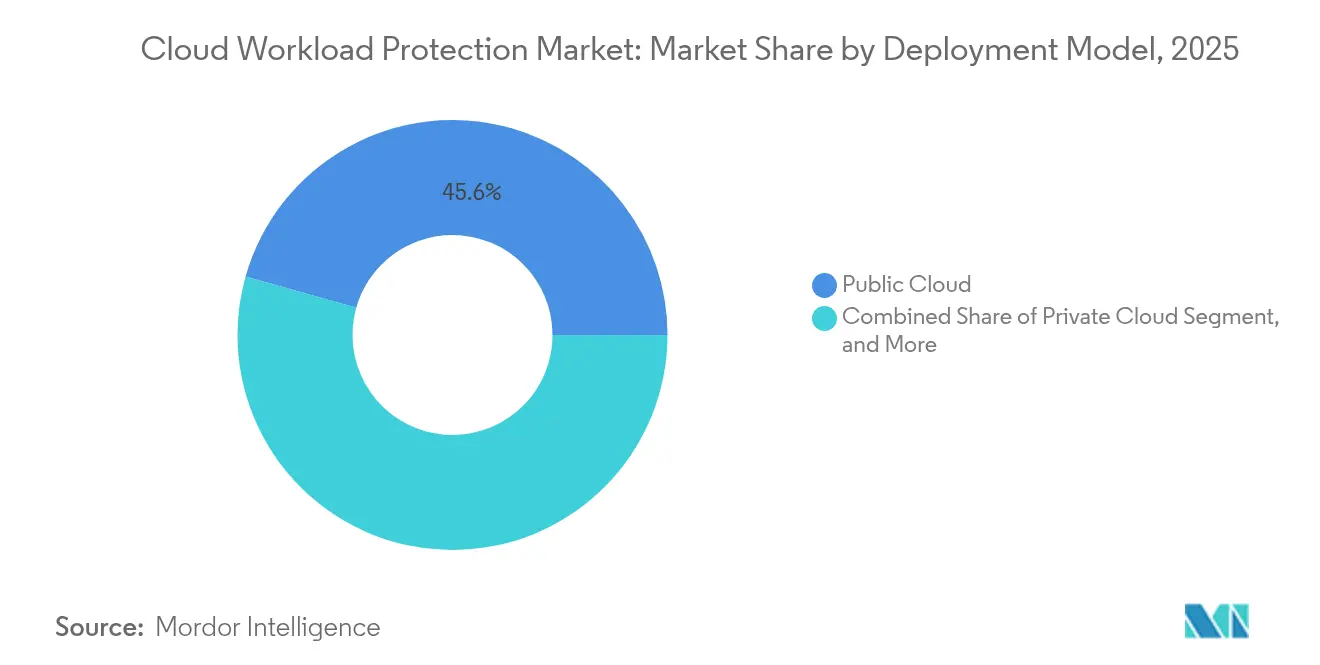

- By deployment model, public cloud commanded 45.62% of the cloud workload protection market share in 2025; hybrid cloud is projected to expand at 29.2% CAGR between 2026-2031.

- By workload type, virtual machines retained 40.55% of the cloud workload protection market share in 2025, whereas serverless functions are advancing at 33.2% CAGR through 2031.

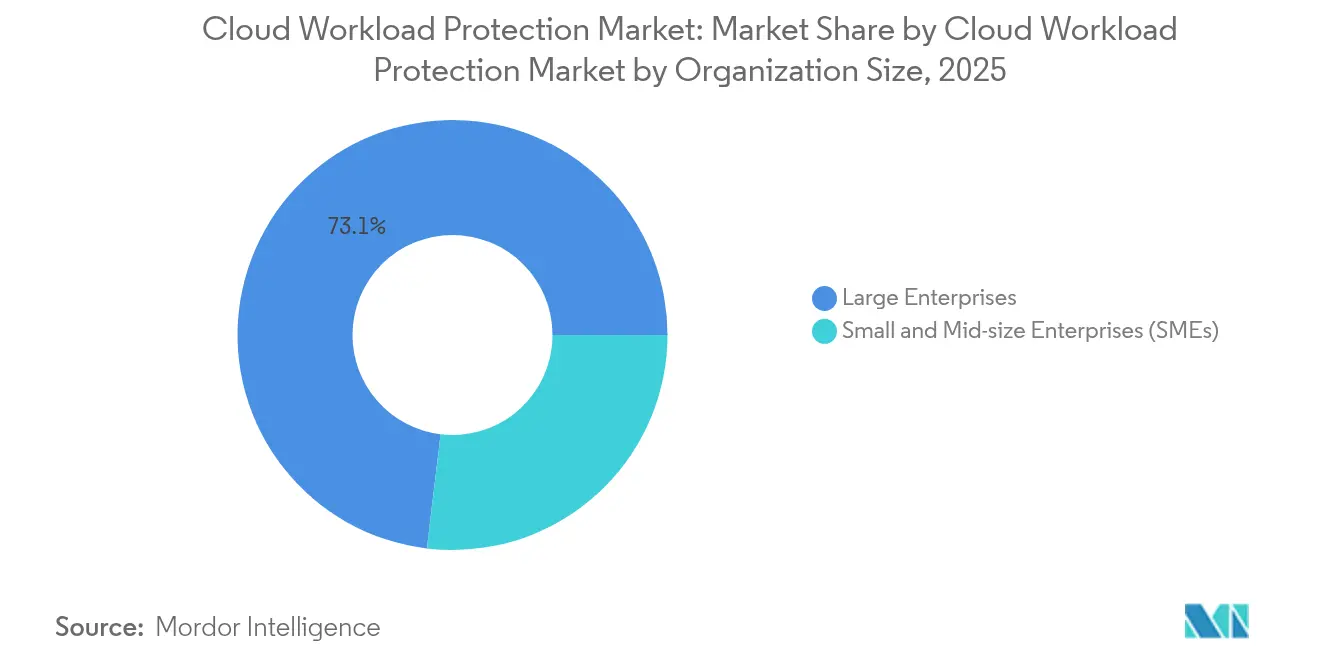

- By organization size, large enterprises led with 73.10% of the cloud workload protection market share in 2025; small and medium enterprises are growing at 25.9% CAGR.

- By end-user vertical, banking, financial services, and insurance (BFSI) accounted for 22.60% of the cloud workload protection market share in 2025, while healthcare and life sciences are poised to rise at 27.1% CAGR.

- By geography, North America held 37.70% of the cloud workload protection market share in 2025; Asia-Pacific is the fastest-growing region at 28.9% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Workload Protection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream multi-cloud adoption surge | +2.6% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Mainstream DevSecOps shift accelerating CNAPP roll-outs | +2.2% | Global DevSecOps hubs; US, UK, Israel, India | Short term (≤2 years) |

| Rising cloud-native ransomware & compliance fines | +2.0% | Global regulated industries (BFSI, healthcare, govt.) | Long term (≥4 years) |

| Operational-cost advantage vs. on-prem tooling | +1.4% | Global, especially SMB-heavy markets in APAC & LATAM | Medium term (2-4 years) |

| eBPF-powered deep telemetry unlocks runtime trust | +0.8% | North America and EU innovation clusters | Short term (≤2 years) |

| Cloud insurance underwriters mandating CWPP proof | +1.1% | North America, EU, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-cloud Adoption Surge

Enterprise strategies that distribute workloads across several hyperscalers reshape security architectures and elevate demand for agentless visibility. The Department of Defense Cloud Security Playbook advocates a unified security posture across heterogeneous environments, reinforcing platform-centric buying preferences.[1]Department of Defense CIO, Cloud Security Playbook Volume 1, U.S. DoD, dodcio.mil Financial institutions value multi-cloud for compliance across jurisdictions, ensuring operational resilience while avoiding vendor lock-in. CNAPP suites gain traction because they consolidate posture management, runtime protection, and incident response inside a single control plane. Vendor roadmaps increasingly emphasize API-based discovery that eliminates the administrative burden of deploying and updating agents across thousands of ephemeral assets.

DevSecOps Shift Accelerating CNAPP Roll-outs

Embedding security controls within continuous integration and deployment pipelines accelerates detection of vulnerabilities before workloads reach production. Microsoft’s guidance on cloud-native application protection illustrates how automated checks inside build processes shorten remediation cycles and align developers with security objectives.[2]Microsoft, Implementing a Cloud-Native Application Protection Platform, Microsoft, microsoft.com The approach boosts release velocity while sustaining governance requirements. Container orchestration platforms such as Kubernetes bring runtime complexity that traditional endpoint agents cannot easily monitor, spurring adoption of integrated scan-to-protect workflows. As DevSecOps culture matures, procurement pivots toward solutions that expose developer-friendly APIs, policy-as-code templates, and actionable feedback loops inside integrated development environments.

Rising Cloud-Native Ransomware and Compliance Fines

Threat actors exploit misconfigurations in containers and serverless functions, elevating operational risk for regulated industries. The European Data Protection Board notes mounting enforcement actions for cloud data mishandling, signaling that fines now outweigh the cost of preventive controls.[3]European Data Protection Board, EDPB Annual Report 2024, EDPB, edpb.europa.eu Runtime defenses capable of detecting lateral movement inside Kubernetes clusters become mandatory for financial and healthcare organizations. Zero-trust principles gain urgency because network perimeters do not protect workloads communicating across multiple clouds and regions. Vendors respond by integrating behavioral analytics, network micro-segmentation, and data-aware encryption into a single policy framework.

eBPF-Powered Deep-Telemetry Unlocks Runtime Trust

Extended Berkeley Packet Filter instrumentation offers kernel-level visibility without the performance overhead of legacy drivers. AccuKnox demonstrates how eBPF converts user-defined policies into bytecode that enforces process, file, and network controls in real time. The technique delivers granular telemetry for containers and virtual machines, supports policy-as-code workflows, and scales across multi-OS fleets. Adoption accelerates in Asia-Pacific where Linux dominance and open-source communities drive innovation, with subsequent uptake in North America and Europe as organizations seek deterministic runtime integrity and reduced agent footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex multi-regime data-residency mandates | -1.6% | EU, Middle East, APAC (India, Singapore), LATAM | Long term (≥4 years) |

| Tool sprawl & agent fatigue among SecOps teams | -1.3% | Global cloud-first enterprises | Short term (≤2 years) |

| Shortage of cloud-security skillsets | -1.5% | Global, especially emerging markets | Medium term (2-4 years) |

| Rising ARM-based server adoption breaking legacy agents | -0.9% | APAC hyperscalers, EU cloud sovereign initiatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Multi-regime Data-Residency Mandates

Divergent data-sovereignty rules force enterprises to maintain region-specific cloud instances and limit telemetry transfer, complicating unified threat detection. Impossible Cloud highlights how localization laws prompt fragmented security architectures and inflate operating costs. Financial firms must comply with GDPR, Basel III, and national banking statutes, requiring providers to offer in-country log processing, encryption key ownership, and locally certified data centers. Vendors allocate significant R&D resources to achieve compliance accreditations, which can slow feature innovation and increase barriers to entry for emerging players.

Tool Sprawl and Agent Fatigue Among SecOps Teams

Security operations centers deploy multiple point products that exhaust analysts with redundant alerts and overlapping dashboards. Academic research identifies alert fatigue as a root cause of burnout and missed incidents. Hybrid and multi-cloud estates compound the problem because distinct agents often lack parity on ARM-based servers or serverless runtimes. Enterprises therefore consolidate around platforms that merge posture management, runtime controls, and incident response, trimming license spend and administrative overhead. Vendor differentiation increasingly hinges on unified policy engines, normalized telemetry, and AI-assisted triage that shortens mean-time-to-detect.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate Through Integration

Solutions generated a 67.35% revenue contribution in 2025, reflecting the market’s preference for converged platforms that stretch from posture management to incident response. The cloud workload protection market size for solution offerings is poised to climb alongside a 27.29% CAGR in threat detection and response tooling as runtime analytics become table stakes. Comprehensive suites bundle vulnerability assessment, compliance reporting, and encryption, which drives platform stickiness and reduces total cost of ownership.

Services delivered the remaining 32.65% revenue, led by managed detection capabilities that offset talent shortages. Professional services support architectural design and migration, while managed offerings appeal to small and medium enterprises seeking operational expertise without hiring full-time staff. Tight integration between technology and services ensures faster time-to-value and creates up-sell pathways for advisory engagements, sustaining recurring revenue growth across the cloud workload protection market.

By Security Architecture: Agent-based Leads Despite Agentless Surge

Agent-based deployments accounted for 63.25% of the cloud workload protection market share in 2025 because kernel-resident modules provide deep packet visibility and process control. They remain indispensable for high-frequency trading and other latency-sensitive workloads that demand deterministic monitoring. However, the agentless cohort is scaling at 31.15% CAGR as hyperscaler APIs mature and customers gravitate toward lighter operational footprints.

The cloud workload protection market size attached to agentless models benefits from ARM server adoption and serverless expansion, both of which challenge legacy agents. Hybrid strategies that combine in-guest sensors for mission-critical assets with API telemetry for ephemeral workloads bridge capability gaps. Microsoft’s transition to Azure Monitor Agent exemplifies the industry’s pivot to consolidated collectors that minimize CPU overhead while expanding data granularity

By Deployment Model: Public Cloud Foundation Enables Hybrid Growth

Public cloud accounted for 45.62% of revenue in 2025, underpinned by built-in controls from hyperscalers and an expansive ecosystem of third-party integrations. Hybrid architectures, forecast to grow at 29.2% CAGR, resonate with organizations balancing regulatory control with elasticity. Private cloud persists at 30.7% share for industries requiring sovereign hosting or proximity to on-premises assets.

Unified platforms that abstract policy enforcement from physical location underpin the cloud workload protection market, ensuring consistent guardrails across Kubernetes clusters in data centers and serverless functions at the edge. The Department of Defense zero-trust overlays underscore the strategic value of deployment agnosticism, steering procurement criteria toward vendors that operate across cloud footprints without security blind spots

By Cloud Workload Type: Serverless Disrupts Virtual Machine Dominance

Virtual machines retained 40.55% revenue share in 2025, yet the serverless segment is advancing at 33.2% CAGR as event-driven architectures compress infrastructure overhead. Containers are expanding at 30.35% and represent the connective tissue between legacy monoliths and microservices. The cloud workload protection market size linked to serverless highlights the urgency for runtime controls that trigger in milliseconds and respect provider-defined sandboxes.

Aqua Security’s AI-workload protection underscores the importance of visibility inside GPUs and specialized accelerators powering machine-learning inference. eBPF instrumentation further levels the playing field by collecting granular telemetry across container-optimized operating systems without intrusive code changes.

By Organization Size: Enterprise Leadership Drives SME Adoption

Large companies generated 73.10% of 2025 revenue because of sheer workload volume and regulatory obligations. Integrated suites that dovetail with security information and event management (SIEM) pipelines reinforce renewal rates. Small and medium enterprises are expanding at 25.9% CAGR as SaaS-delivered protection lowers entry thresholds.

Agentless discovery, simplified dashboards, and consumption-based pricing allow SMEs to adopt controls that once required specialist teams, expanding the total addressable cloud workload protection market. SentinelOne’s FedRAMP authorization illustrates how single-tenant SaaS models can simultaneously serve sovereign agencies and mid-market firms through role-based access controls and modular feature tiers

By End-User Vertical: Healthcare Accelerates Beyond BFSI Leadership

BFSI maintained a 22.60% share in 2025 thanks to stringent audit mandates and high breach costs. Healthcare and life sciences will outpace other verticals with a 27.1% CAGR as ransomware targets patient data and connected medical devices. Telecommunications, energy, and government workloads also scale rapidly as 5G rollouts, smart-grid projects, and public-sector modernization push sensitive data into the cloud.

Vendors bundle compliance artefacts—such as HIPAA mappings and PCI DSS dashboards—directly into policy engines, shortening certification cycles. The cloud workload protection market size in regulated sectors grows alongside embedded frameworks, automated evidence collection, and AI-based anomaly detection that flags credential abuse inside critical systems.

Geography Analysis

North America held 37.70% share in 2025, anchored by mature cloud penetration, strong venture funding, and regulatory drivers such as FedRAMP. High-profile authorizations fuel adoption across civilian agencies and defense programs, reinforcing vendor legitimacy. Canada and Mexico mirror these trends, adapting U.S. frameworks to local privacy statutes and extending market reach.

Asia-Pacific is advancing at 28.9% CAGR, powered by digital-first banking in India, manufacturing digitization in China, and public-sector cloud mandates in Australia and Japan. Akamai recorded a 73% rise in web attacks across the region, with financial services absorbing more than 27 billion malicious requests in 2024. This threat landscape fosters rapid uptake of runtime protection, particularly in Singapore and South Korea, where regulators expect zero-trust adherence.

Europe maintained 27.95% revenue share in 2025, and GDPR remains the principal compliance engine. The European Data Protection Board stresses cross-border data controls, compelling multinationals to deploy region-specific telemetry pipelines. Vendors compete on localized data centers, encryption key ownership, and adherence to emerging AI Acts that govern model explainability and data retention. Eastern European and Nordic markets contribute incremental growth as cloud adoption extends into manufacturing and energy sectors.

Competitive Landscape

Market consolidation is moderate as established endpoint and network security vendors expand into workload protection through acquisitions and organic R&D. Cisco, Palo Alto Networks, and CrowdStrike integrate cloud security posture management, container runtime defenses, and threat intelligence feeds to offer full-stack visibility. Differentiation hinges on unified policy engines, eBPF-powered observability, and AI-assisted response.

Technology roadmaps emphasize agentless discovery for ease of deployment, supplemented by in-kernel guards where deterministic control is paramount. SEC filings from SentinelOne demonstrate growing cross-sell rates between XDR and CNAPP modules, validating the platform thesis. White-space opportunities remain in serverless, AI, and edge-computing workloads, prompting niche players to specialize in accelerated runtime inspection and data-aware micro-segmentation.

Partnerships also shape competition. Rubrik aligns with hyperscalers to integrate isolated recovery, while Accenture collaborates with CrowdStrike to modernize SIEM deployments. Such alliances strengthen solution stickiness, expand channel reach, and accelerate integration roadmaps, elevating switching costs for end-customers. Pricing models progressively favor consumption-based tiers that align spend with workload telemetry volume rather than static host counts.

Cloud Workload Protection Industry Leaders

Microsoft

Palo Alto Networks

CrowdStrike

Wiz

Trend Micro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rubrik reported 38% year-over-year subscription ARR growth to USD 1.18 billion and partnered with Google Cloud and Mandiant to launch isolated recovery solutions that harden cyber-resilience through air-gapped backups

- May 2025: Fortinet recorded USD 1.54 billion Q1 2025 revenue, citing 30% growth in Security Operations and 26% expansion of Unified SASE offerings that integrate workload and network protection

- May 2025: Zscaler posted USD 678 million Q3 FY 2025 revenue and introduced Asset Exposure Management to unify inventory and risk scoring across multi-cloud estates

- May 2025: Palo Alto Networks unveiled Prisma AIRS for Red Hat OpenShift, adding runtime segmentation to block lateral movement in containerized AI workloads

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cloud-workload protection market as all subscription and perpetual revenues that stem from software platforms purpose-built to secure virtual machines, containers, and serverless functions across public, private, and hybrid clouds. These platforms deliver real-time threat detection, vulnerability and posture assessment, micro-segmentation, and policy enforcement through agent-based or agentless sensors that integrate directly with cloud control planes.

Scope exclusion: Hardware firewalls, secure web gateways, and stand-alone endpoint security suites that never monitor cloud runtime telemetry are outside the study.

Segmentation Overview

- By Component

- Solutions

- Monitoring and Logging

- Policy and Compliance Management

- Vulnerability Assessment

- Threat Detection and Incident Response

- Encryption, Tokenisation and Key Management

- Services

- Managed Services

- Professional Services

- Solutions

- By Security Architecture

- Agent-based

- Agentless

- Hybrid

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Cloud Workload Type

- Virtual Machines (VMs)

- Containers

- Serverless / FaaS

- By Organization Size

- Large Enterprises

- Small and Mid-size Enterprises (SMEs)

- By End-User Vertical

- BFSI

- Healthcare and Life Sciences

- IT and Telecommunications

- Retail and Consumer Goods

- Media and Entertainment

- Energy and Utilities

- Government and Defense

- Other End-User Vertical

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia and New Zealand

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman)

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with CISOs, DevSecOps leads, and channel partners across North America, Europe, and Asia-Pacific clarified average selling prices, agentless adoption hurdles, and expected container-per-host ratios so our desk findings could be challenged, confirmed, and refined.

Desk Research

Our analysts began by mapping the global cloud-native stack through public sources such as NIST cloud guidelines, ENISA threat reports, Cloud Security Alliance controls, CNCF container surveys, and regional cyber-incident disclosure portals. This foundation was enriched with tariff data from UN Comtrade, workload migration statistics from Eurostat, and container density indexes published by the Linux Foundation, giving us early signals on workload volumes that drive security spend.

Corporate filings, investor decks, and earnings transcripts of 25 listed security vendors were then reviewed inside Dow Jones Factiva, while D&B Hoovers supplied historical revenue splits that help anchor vendor roll-ups. Select paid sources, Questel for patent momentum and MarkLines for sectoral container adoption, added technology and vertical fingerprints. The sources cited illustrate, not exhaust, the broader desk research library we referenced.

Market-Sizing & Forecasting

A top-down build, starting with global public-cloud IaaS and PaaS spend matched to workload penetration rates, establishes the 2025 revenue pool. Supplier roll-ups and channel checks supply bottom-up reasonableness tests before values are adjusted. Key variables like container density, average protected workload cost, multi-cloud adoption share, regulated-sector cloud uptake, and DevSecOps pipeline counts feed a multivariate regression that projects demand through 2030. Gaps in vendor disclosures are bridged by applying median margin yields from peers with comparable license mixes.

Data Validation & Update Cycle

Outputs pass three-layer reviews: automated anomaly scans, senior analyst variance checks, and a final reconciliation against fresh earnings releases. Reports refresh annually, and material cyber events trigger interim revisions so clients receive an up-to-date baseline.

Why Mordor's Cloud Workload Protection Baseline Commands Reliability

Published estimates vary because firms pick different service scopes, workload definitions, and refresh cadences. Our disciplined alignment to runtime-focused platforms, annual updates, and dual-track validation keeps Mordor's figure grounded and reproducible.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.84 B | Mordor Intelligence | - |

| USD 9.00 B | Global Consultancy A | Bundles managed services and training revenues, relies on top-down spend shares only |

| USD 8.32 B | Research Firm B | Extends scope to 2035 and allocates future CNAPP cross-sell back into 2025 base |

| USD 7.70 B | Data Publisher C | Uses vendor survey intentions rather than booked revenues for agentless products |

Differences trace mainly to what each study counts and how frequently figures are refreshed. By ring-fencing pure workload-centric software and corroborating totals with live vendor bookings, Mordor Intelligence delivers a balanced, transparent benchmark that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the cloud workload protection market?

The market is valued at USD 9.63 billion in 2026.

How fast is the cloud workload protection market expected to grow?

It is projected to advance at a 22.78% CAGR, reaching USD 26.84 billion by 2031.

Which security architecture is gaining the most momentum?

Agentless cloud workload protection is expanding at a 31.15% CAGR as organizations seek lighter deployment footprints.

Which workload type is growing the fastest?

Serverless functions are rising at a 33.2% CAGR as enterprises adopt event-driven computing models.

Why is Asia-Pacific the fastest-growing region?

Digital-first transformation initiatives and stricter data-protection rules propel a 28.9% CAGR across APAC markets.

Page last updated on: