Cloud Encryption Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

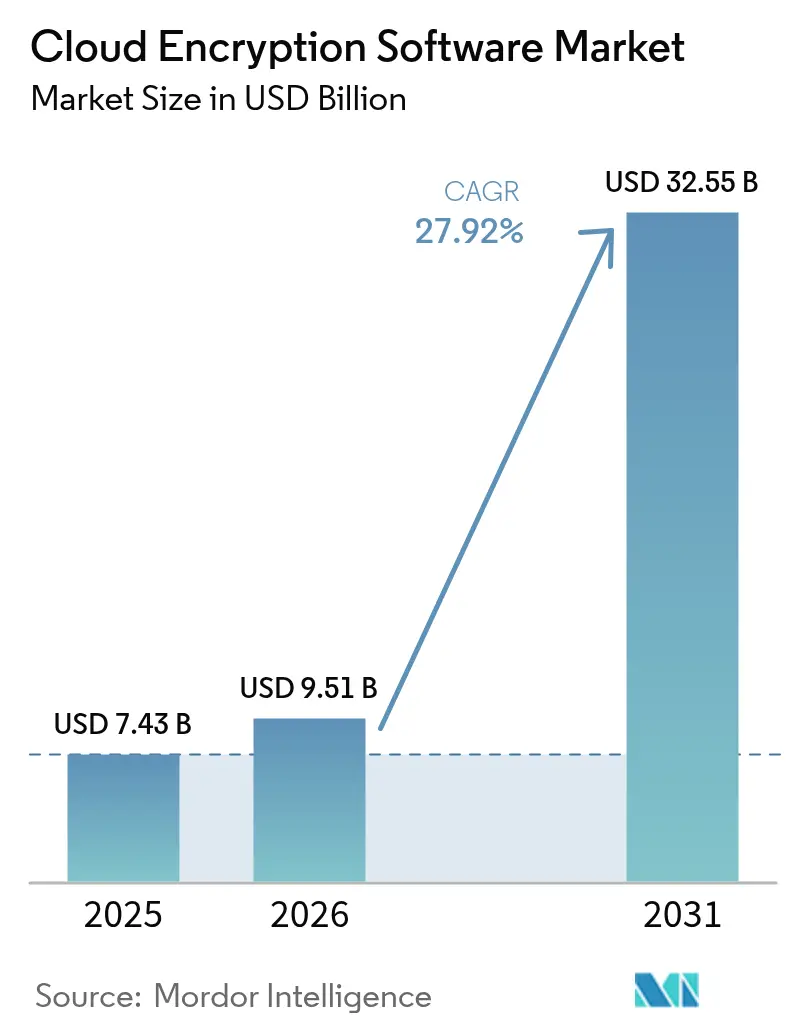

| Market Size (2026) | USD 9.51 Billion |

| Market Size (2031) | USD 32.55 Billion |

| Growth Rate (2026 - 2031) | 27.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Encryption Software Market Analysis by Mordor Intelligence

The cloud encryption software market size in 2026 is estimated at USD 9.51 billion, growing from 2025 value of USD 7.43 billion with 2031 projections showing USD 32.55 billion, growing at 27.92% CAGR over 2026-2031. The surge blends three powerful forces: unrelenting cyber-attacks, mounting regulatory pressure, and the operational shift toward multi-cloud computing. Post-quantum cryptography standards finalized by the National Institute of Standards and Technology (NIST) in August 2024 accelerated enterprise migration road maps as boards realized that harvest-now-decrypt-later risks have already materialized. At the same time, 98% of financial-services firms now operate workloads in public cloud, creating an urgent need for unified key management across heterogeneous platforms[1]Board of Governors of the Federal Reserve System, “Community Banking Connections: Cloud Adoption Survey,” federalreserve.gov. North America leads adoption, propelled by FedRAMP and Department of Defense mandates for quantum-safe algorithms, while sovereign-cloud policies push Asia-Pacific to the fastest regional CAGR. The encryption ecosystem is also shaped by performance-optimized symmetric tools, breakthrough fully homomorphic encryption, and hardware-assisted confidential-computing technologies that seal data during use.

Key Report Takeaways

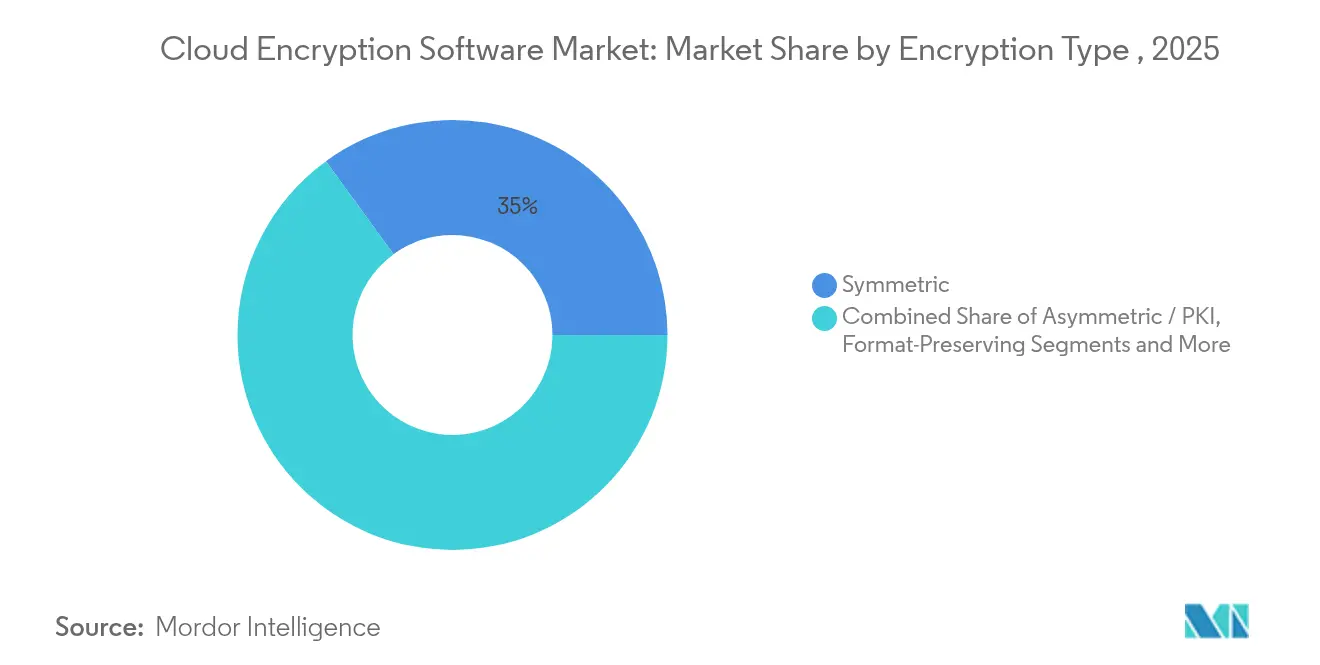

- By encryption type, symmetric algorithms led with 35.02% of cloud encryption software market share in 2025, while fully homomorphic encryption is projected to grow at a 28.57% CAGR through 2031.

- By application, data-at-rest protection accounted for a 36.10% share of the cloud encryption software market size in 2025; confidential-computing workloads will expand at a 29.11% CAGR to 2031.

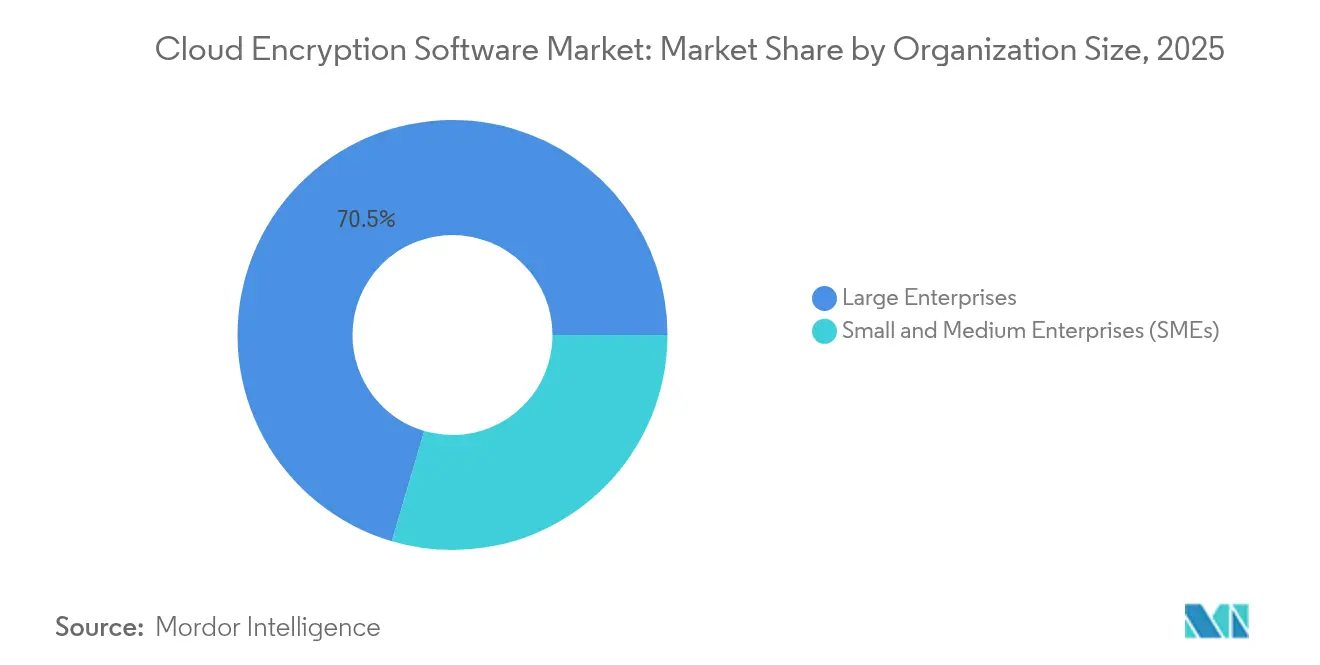

- By organization size, large enterprises held 70.45% of the cloud encryption software market share in 2025, whereas small and medium enterprises are poised for 29.52% CAGR over the forecast window.

- By industry vertical, IT and telecommunications commanded 33.12% revenue share in 2025; banking, financial services and insurance (BFSI) is forecast to advance at a 28.44% CAGR through 2031.

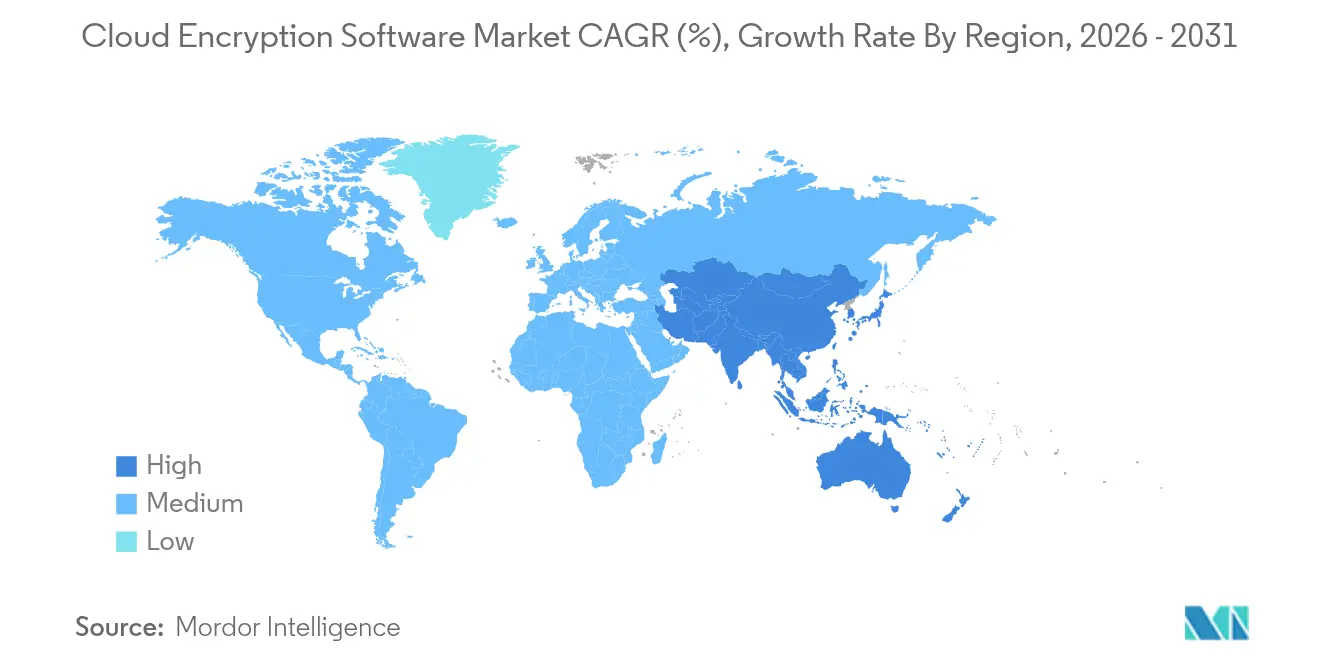

- By geography, North America represented 38.52% of the cloud encryption software market in 2025, while Asia-Pacific is set to climb with a 28.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Encryption Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening data-protection regulations | +4.2% | Global, with early gains in EU, North America | Medium term (2-4 years) |

| Surge in sophisticated cyber-attacks on cloud | +3.8% | Global | Short term (≤ 2 years) |

| Enterprise multi-cloud adoption | +3.1% | North America and EU, APAC core | Medium term (2-4 years) |

| Confidential-computing demand | +2.9% | Global, spill-over to emerging markets | Long term (≥ 4 years) |

| Post-quantum encryption urgency | +2.7% | North America and EU, expanding globally | Long term (≥ 4 years) |

| "Encryption-as-code" DevSecOps tools | +2.1% | Global, concentrated in tech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Data-Protection Regulations

Worldwide statutes are raising the security baseline. PCI DSS 4.0, effective March 2025, forces annual cryptographic reviews and multi-factor authentication across all card-holder environments. Europe’s Digital Operational Resilience Act and NIS 2 directive require quantum-resistant encryption by 2030 for banking and critical infrastructure. In the United States, the Quantum Computing Cybersecurity Preparedness Act compels federal agencies to pivot to NIST-approved post-quantum algorithms, setting a template the private sector is following. FedRAMP has already mandated FIPS 140-2 validated modules for all federal cloud services, turning compliance into a de facto market entry ticket. Even universities are hardening controls because the 2002 FERPA framework never anticipated cloud-stored student data, prompting encryption measures that exceed legal minima.

Surge in Sophisticated Cyber-Attacks on Cloud

Cloud workloads absorbed 31% of recorded cyber incidents in 2024, with ransomware costs in financial services averaging USD 5.37 million[2]Broadcom Inc., “2025 State of Ransomware Report,” broadcom.com. Advanced persistent-threat actors now harvest encrypted troves, betting on future quantum decryption. Real-time encryption monitoring and hybrid classical-plus-post-quantum key exchange are therefore gaining traction. Misconfigurations cause 44% of public-cloud breaches, so automated policy engines that wrap encryption around every object—independent of administrator skill—are becoming mandatory. Attackers increasingly target control-plane identities rather than endpoints, reinforcing the need for data-centric protection that stays effective even when perimeter controls fail.

Enterprise Multi-Cloud Adoption

Seventy percent of retail banks intend to run fully cloud-based operations by 2025, yet each hyperscaler ships its own key-management service, creating a patchwork of policies that teams struggle to reconcile. Bring-your-own-key and hold-your-own-key models are emerging to let firms keep cryptographic sovereignty, but performance and lock-in concerns still curb uptake. External key-management services promise centralized oversight across Amazon Web Services, Microsoft Azure and Google Cloud Platform, though integration overhead remains non-trivial. Zero-trust architecture—grounded in the assumption that breach is inevitable—now frames most multi-cloud encryption blueprints, driving demand for controls that travel with the data rather than the infrastructure.

Confidential-Computing Demand

Hardware-based trusted execution environments (TEEs) such as Intel SGX and AMD SEV encrypt data in use, closing the last exposure window. Banks deploy TEEs for fraud detection across shared datasets without revealing underlying records. Healthcare providers run AI diagnosis models on protected patient information, preserving HIPAA compliance. Since the launch of the Confidential Computing Consortium, cloud providers have worked to standardize enclaves, speeding commercial adoption. Current TEEs add 10-40% processing overhead, yet the security gain outweighs the cost for most analytic and AI pipelines. Side-channel-attack research continues, keeping vendor road-maps focused on microcode hardening and noise-injection techniques.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance overhead and latency | -2.8% | Global, particularly affecting real-time applications | Short term (≤ 2 years) |

| Key-management complexity | -2.3% | Global, concentrated in multi-cloud environments | Medium term (2-4 years) |

| Lack of interoperability in trusted-execution | -1.9% | Global, affecting enterprise adoption | Medium term (2-4 years) |

| Edge-cloud data-sovereignty dampening demand | -1.6% | APAC, EU with strict data localization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Overhead and Latency

Encrypting data adds compute cycles and I/O waits. Classical encryption-at-rest slows SQL queries by several hundred milliseconds in high-volume databases. Fully homomorphic encryption, while revolutionary for privacy, can inflate processing time by 1 000× unless hardware acceleration is employed. GPU-assisted frameworks cut that overhead by roughly 12% according to recent benchmark studies published in Computers, Materials and Continua. Edge-computing scenarios feel the penalty most because encryption delay compounds existing network latency, forcing architects to weigh real-time responsiveness against confidentiality. Post-quantum algorithms also raise computational tax because of larger key sizes, challenging performance budgeting in low-power devices.

Key-Management Complexity

Encryption is only as strong as its keys, yet few enterprises run unified key life-cycle platforms across multiple clouds. Distinct native services—AWS KMS, Azure Key Vault, Google Cloud KMS—offer scant interoperability, leaving teams to juggle rotation schedules and access controls manually. Two-thirds of organizations cite inadequate cryptographic expertise as their chief roadblock, a gap that frequently leads to misconfigured policies that silently weaken protection. PCI DSS 4.0 now demands automated key rotation, adding urgency. The forthcoming migration to post-quantum standards means most hardware security modules will need firmware or outright replacement, further straining budgets and skill sets. Centralized services help, but they introduce single points of failure—an architectural trade-off that large enterprises analyze closely.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Encryption Type: Quantum-Resistant Algorithms Drive Innovation

Symmetric methods dominate the cloud encryption software market with 35.02% share in 2025, favored for their speed and low CPU overhead. Fully homomorphic encryption, despite its infancy, is the fastest-rising technique, forecast to grow at 28.57% CAGR as confidential-computing use cases blossom. The August 2024 release of FIPS 203, FIPS 204, and FIPS 205 set the baseline for post-quantum key encapsulation, digital signatures, and stateless hash-based signatures, prompting vendors to embed these algorithms into product road maps.

Enterprises are deploying hybrid cryptography that blends classical elliptic-curve methods with post-quantum lattices, hedging against algorithmic failure. Format-preserving encryption is also expanding because it lets legacy applications store protected data without schema redesign. With NIST’s March 2025 selection of HQC as a fifth algorithm for additional diversity, crypto-agile tooling has become a board-level priority. As a result, the cloud encryption software market size for symmetric workloads is projected to climb steadily, while quantum-safe options capture a larger slice of new deployments.

By Application: Confidential Computing Transforms Data-in-Use Protection

Data-at-rest still tops the application stack with 36.10% share of the cloud encryption software market in 2025, reflecting mature backup and storage practices. Yet it is data-in-use encryption that makes headlines, surging at a 29.11% CAGR as TEEs remove the longstanding barrier of processing on plaintext. The cloud encryption software market size for confidential-computing workloads will therefore expand faster than any other segment.

Transport-layer protection remains indispensable for inter-cloud links, but performance tuning has shifted toward post-quantum handshake algorithms. SaaS collaboration tools are seeing wider client-side encryption rollouts so organizations retain control over cryptographic keys. Searchable symmetric encryption now appears in big-data environments, where latency overhead can be tolerated for high-value queries. Together these shifts advance the vision of persistent, state-agnostic protection across the entire data life cycle.

By Organization Size: SME Adoption Accelerates

Large enterprises held 70.45% of cloud encryption software market share in 2025 thanks to sprawling hybrid estates and bigger compliance budgets. They lead pilots in fully homomorphic encryption and confidential computing. In contrast, small and medium enterprises are adding encrypted SaaS and API-based key services at a 29.52% CAGR, the fastest trajectory in the market.

Pay-as-you-use pricing, managed key rotation and template-driven compliance reports are lowering barriers for firms without dedicated security staff. However, 51.3% of small businesses still cite implementation complexity as their top impediment. As vendor UX improves and marketplace integrations mature, the cloud encryption software market size captured by SMEs is set to widen, gradually balancing segment concentration.

By Industry Vertical: BFSI Leads Quantum-Resistant Transition

IT and telecommunications captured 33.12% revenue share in 2025 because of early cloud migration and high bandwidth demands. Banking, financial services and insurance will be the fastest-growing vertical, sprinting at 28.44% CAGR to 2031 as regulators push quantum-safe standards and as fintech competition heightens risk.

Healthcare is ramping up confidential-computing pilots for AI-enabled diagnostics, protecting patient files that cost USD 10.93 million per breach—double the multi-industry average. Government agencies, under the Quantum Computing Cybersecurity Preparedness Act, serve as anchor customers for post-quantum modules. Retailers fine-tune tokenization to satisfy PCI DSS 4.0 without adding checkout latency. Across sectors, the cloud encryption software market provides a unifying shield against divergent, yet intensifying, data-security obligations.

Geography Analysis

North America held 38.52% of the cloud encryption software market in 2025, underpinned by FedRAMP mandates, Department of Defense directives and aggressive enterprise migration to post-quantum controls. Multi-cloud penetration is high, and vendors secure revenue through managed key services and crypto-agile orchestration. Large healthcare and finance clients also test confidential-computing frameworks at scale, accelerating innovation cycles.

Asia-Pacific is the fastest-growing region with a 28.96% CAGR through 2031. Sovereign-cloud blueprints in Australia, Japan, South Korea and India demand that encryption keys remain on domestic soil, spurring sales of external key-management gateways and hardware security modules that support national algorithms where required. The Asian Development Bank estimates improved cloud policy could lift regional GDP by up to 0.7% during 2024-2028, and encryption is cited as a pivotal enabler. Chinese and Southeast Asian hyperscalers are forming in-country alliances with chipmakers to deliver quantum-safe network encryption, keeping pace with Western rivals.

Europe maintains steady expansion driven by GDPR enforcement and the Digital Operational Resilience Act. Financial institutions must file resilience plans outlining migration to quantum-resistant algorithms, a move that is turning Europe into a laboratory for cross-border key-escrow interoperability. Privacy-preserving analytics—especially in health and mobility—stimulate demand for fully homomorphic encryption. Smaller markets in South America and the Middle East and Africa trail but present greenfield opportunities, particularly where 5G rollouts introduce edge-cloud architectures that require lightweight, low-latency encryption.

Regulatory Landscape

Cloud encryption software adoption is being shaped by converging security standards and procurement-driven requirements. In August 2024, NIST finalized its first three post-quantum cryptography standards (FIPS 203, FIPS 204, and FIPS 205), establishing a baseline for quantum-resistant implementations referenced across federal and regulated environments. In the United States, FedRAMP requirements for validated cryptographic modules (FIPS 140 validated) continue to function as a market-entry prerequisite for cloud services selling into government, while CNSA 2.0 sets a January 2027 procurement deadline for U.S. National Security Systems to transition to quantum-resistant encryption, pushing vendors toward crypto-agile roadmaps.

In Europe, compliance pressure expands beyond classic data protection into operational resilience and AI governance, which increasingly pulls encryption into auditability and workload-level controls. The EU AI Act transparency requirements (Article 50) take effect on August 2, 2026, reinforcing needs around labeling, disclosure, and associated logging and data-handling controls that intersect with encryption and key management in cloud deployments. Separately, NIST opened public comment in May 2026 (through July 13, 2026) on NIST IR 8320E covering hardware-enabled security and confidential computing for cloud workloads, signaling standards focus shifting toward encrypting data in use, not only at rest and in transit, particularly for AI datasets and regulated analytics.

Value Chain Analysis

The value chain spans cryptographic algorithm and library providers, encryption software and key-management developers, cloud platform providers, and hardware security suppliers that anchor trust. Hyperscalers (Amazon Web Services, Microsoft Azure, and Google Cloud Platform) provide native KMS and encryption primitives, while security vendors such as Thales, Broadcom (Symantec), Trend Micro, Palo Alto Networks, IBM, Check Point, Zscaler, Netskope, Fortanix, and Akeyless build differentiated layers around centralized key governance, policy automation, tokenization, and workload encryption. Hardware security module suppliers and confidential-computing silicon ecosystems, including TEEs used for data-in-use protection, remain critical upstream dependencies for regulated deployments and high-assurance key custody.

Downstream, systems integrators and managed security service providers operationalize encryption across multi-cloud estates through onboarding, migration, and continuous compliance reporting, with distribution increasingly occurring via cloud marketplaces and SaaS procurement channels. Standards and assurance mechanisms influence nearly every handoff, including NIST guidance for cloud-native data protection approaches, ISO/IEC 27018:2025 for protection of PII in public clouds, and financial-sector oversight practices tied to outsourcing and operational resilience. Key bottlenecks persist around interoperability across AWS KMS, Azure Key Vault, and Google Cloud KMS, alongside the operational complexity and performance trade-offs of data-in-use encryption in confidential-computing environments.

Competitive Landscape

The cloud encryption software market is moderately fragmented, yet consolidation accelerated in 2024 when Palo Alto Networks bought IBM’s QRadar cloud security assets and IBM announced a USD 35-per-share deal for HashiCorp. These moves highlight a pivot toward integrated platforms that blend posture management, key orchestration and policy analytics. Amazon Web Services, Microsoft Azure and Google Cloud Platform embed native quantum-safe options, challenging pure-play vendors but also broadening total demand.

Strategic partnerships are prolific. Thales deepened ties with Google Cloud to co-deliver quantum-safe key management across Anthos and Google Distributed Cloud. Broadcom unveiled the first quantum-resistant network encryption for Fibre Channel in January 2025, aligning with U.S. CNSA 2.0 and EU NIS 2 rules. Edge-oriented challengers target industrial IoT, where low-latency symmetric encryption and rugged hardware modules are still scarce.

Product road-maps center on three pillars: automated key life-cycle governance, crypto-agility for algorithm swaps and confidential-computing orchestration. Vendors able to combine those in a single pane of glass are expected to outgrow niche competitors. Open-source projects, many under the Confidential Computing Consortium, create community pressure for interoperability as buyers push back against lock-in. In sum, competitive intensity remains high, but market power is tilting toward full-stack suppliers with broad cloud-provider alliances and strong professional-services arms.

Cloud Encryption Software Industry Leaders

Google LLC

Symantec Corporation

Hewlett Packard Enterprise

Trend Micro Inc.

Hitachi Vantara

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity area is operationalizing post-quantum migration in cloud-native workflows where encryption and key management are delivered as policy. NIST's August 2024 FIPS 203, FIPS 204, and FIPS 205 standards, combined with visible platform implementations, are pushing buyers to demand crypto-agility (algorithm swap, hybrid key exchange, and centralized policy enforcement) as a product feature rather than a professional-services project. Evidence of this shift shows up in platform updates such as AWS Secrets Manager client support for hybrid post-quantum key exchange using ML-KEM for TLS (April 2026) and Cloudflare making post-quantum encryption generally available for IPsec with hybrid ML-KEM interoperability with Cisco and Fortinet hardware (April 2026). Together, these releases create whitespace for vendors that can unify certificate lifecycle, key rotation, and hybrid cryptography across application, network, and storage layers.

Another opportunity is independent key control and data-in-use protection for AI and regulated analytics, where sovereign-cloud and audit requirements extend beyond encryption-at-rest. Thales made CipherTrust Data Security Platform as a Service available on the Google Cloud Marketplace (July 2026), emphasizing hold-your-own-key patterns and marketplace-led deployment. At the same time, Google Cloud released open-source Prompt Encryption SDKs for protecting AI inference data (June 2026), providing a developer-driven route to embed encryption into AI pipelines. With marketplace distribution, developer SDKs, and confidential-computing attestation working together, the space opens for cross-cloud orchestration products that connect key custody, attestation, and policy-as-code into a single operating model for enterprises running multi-cloud and AI workloads.

Recent Industry Developments

- July 2026: AWS introduced declarative policies for VPC Encryption Controls, enabling centralized audit and enforcement of transit encryption across organizational units and accounts. The update moves encryption governance closer to a policy-as-code operating model, reducing reliance on per-resource configuration in large multi-account environments.

- April 2026: Cloudflare announced general availability of post-quantum encryption for IPsec, supporting hybrid ML-KEM interoperability with Cisco and Fortinet hardware. This expands quantum-safe options for site-to-site connectivity and managed network encryption where IPsec remains a core control plane.

- August 2024: NIST released the first three finalized post-quantum cryptography standards (FIPS 203, 204, and 205). Standardization accelerated vendor roadmaps and procurement checklists for quantum-resistant encryption in cloud security programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers software used to encrypt data in cloud environments, along with the related license or subscription value tied to securing data at rest, in transit, and in use, including key management features that enable encryption to be enforced.

Scope exclusions: We exclude general cloud security tools that do not perform encryption or do not manage encryption keys as part of the product.

Segmentation Overview

- By Encryption Type

- Symmetric

- Asymmetric / PKI

- Format-Preserving

- Fully Homomorphic

- Quantum-resistant Algorithms

- By Application

- Data-at-Rest (storage, backup)

- Data-in-Transit (TLS/VPN)

- Data-in-Use / Confidential Computing

- SaaS File and Collaboration Encryption

- Database / Big-data Encryption

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Industry Vertical

- BFSI

- Healthcare and Life Sciences

- Education

- Retail and e-Commerce

- IT and Telecom

- Government and Defense

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping demand drivers that are visible in public data, then narrowing those drivers to encryption software only, not broader security. Sources used include public standards and guidance (such as NIST publications), regulator and privacy material (such as FTC guidance and the EU GDPR text), cybersecurity incident reporting and advisories (such as CISA alerts), and cloud security references from trade associations and academic journals.

We also review supplier public disclosures such as annual reports, product documentation, and pricing pages where available, plus investor presentations, to understand packaging patterns for encryption, key management, and confidential computing use cases. To keep company-level inputs consistent, a paid subscription covering company financials and intelligence is used selectively, and patent databases are checked to understand the pace of encryption and key-management innovation. The desk sources listed here are illustrative, and many other public and paid references were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focuses on validating how cloud encryption software is bought and deployed across large enterprises and SMEs, and how adoption differs by industry verticals that handle sensitive data. We cover viewpoints from software providers, cloud security channel partners, and enterprise security leaders across APAC, EMEA, and the Americas. This helps close gaps around pricing logic, attach rates, and the timing of refresh cycles for encryption upgrades.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 44% |

| Mid tier: 60% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 15% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where cloud workload growth and security spend signals are translated into an encryption specific demand pool, followed by applying adoption and penetration assumptions for encryption across key use cases. The model is then cross-checked using selective bottom-up approximations, such as sampled vendor revenue ranges, channel feedback on typical deal sizes, and a price times volume sense-check for subscriptions tied to encrypted data footprints.

Inputs that materially move the model include the mix of data-at-rest versus data-in-transit use cases, adoption of confidential computing for data-in-use, the share of regulated workloads in BFSI and healthcare, and shifts to multi-cloud deployments that increase key-management complexity. We also incorporate expected price movement from bundling and longer contract terms. Where disclosure gaps exist, missing values are handled using peer-group proxies based on similar product packaging, then adjusted through interview feedback so the totals remain realistic by region and industry.

For forecasting, we rely on scenario analysis supported by a simple multivariate regression to connect growth to cloud migration pace, breach and compliance intensity, and the rollout of quantum-safe planning that triggers upgrade cycles. The final forecast stays interpretable so the drivers can be traced back to visible indicators and what experts report as practical buying behavior.

Data Validation & Update Cycle

Outputs are validated through multiple checks, starting with internal consistency tests across regions and use cases, and then comparing results with independent signals like cloud security budget direction, cloud workload growth, and the implied spend per protected workload. When a variance looks large, assumptions are revisited, and follow-up calls are triggered to confirm whether the gap is caused by scope, pricing changes, or a timing mismatch in contracts.

Before sign-off, the model and narrative go through a multi-step analyst review so any outliers are explained and corrected, and calculations remain reproducible. Reports are refreshed annually, and interim updates are made when material events occur that can move demand or pricing. Prior to delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Gobal Cloud Encryption Software Market Market Size Measured Against Other Published Estimates

Published values for cloud encryption software often do not match because each publisher draws the boundary of the market differently, and the timing of the base year and currency treatment also shifts the final number. Differences also come from how adjacent items are handled, especially when services, hardware, or broader cloud security categories are included.

Checks like application level split signals for data-at-rest, data-in-transit, and data-in-use, plus interview validation on key-management attach rates and subscription pricing bands, are what tie Mordor Intelligence to the 2026 market size in the table, rather than letting the number drift with broader cloud security spending.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.51 B (2026) | |

| Global Research House A | USD 7.73 B (2025) | This figure is anchored to 2025 and is presented with a broader component scope that can include services and, in some definitions, related hardware items, which changes what gets counted as software revenue. |

| Industry Publisher B | USD 5.94 B (2025) | The estimate uses a component split where services are explicitly part of the total, and the longer forecast window can lead to a more conservative near-term ramp for cloud encryption adoption compared with a tighter software-only focus. |

Seen together, the spread is mainly explained by year alignment and what sits inside the market boundary, especially services and any adjacent non-software items. By keeping the sizing anchored to clear application use cases and pricing logic that can be checked in interviews, the result stays traceable and repeatable for planning decisions.

Key Questions Answered in the Report

What is driving the sharp growth of the cloud encryption software market?

Heightened cyber-attacks, stricter global regulations and multi-cloud adoption are the primary catalysts, boosting demand for data-centric security across all cloud layers.

How large will the cloud encryption software market be in 2031?

The market is forecast to reach USD 32.55 billion by 2031, expanding from USD 9.51 billion in 2026 at a 27.92% CAGR.

Which encryption type is growing the fastest?

Fully homomorphic encryption is projected to rise at a 28.57% CAGR because it enables computation on encrypted data without decryption.

Why are SMEs adopting encryption faster than before?

Cloud-native, pay-as-you-use models have reduced cost and complexity, allowing SMEs to implement enterprise-grade encryption while avoiding hardware purchases.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest CAGR at 28.96%, driven by sovereign-cloud mandates and rapid digital transformation.

How soon must organizations migrate to post-quantum cryptography?

U.S. federal agencies and European financial institutions must start the transition now to meet mandates that take full effect by 2030, prompting near-term investment in crypto-agile architectures.

Page last updated on: