Cloud-Based Database Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

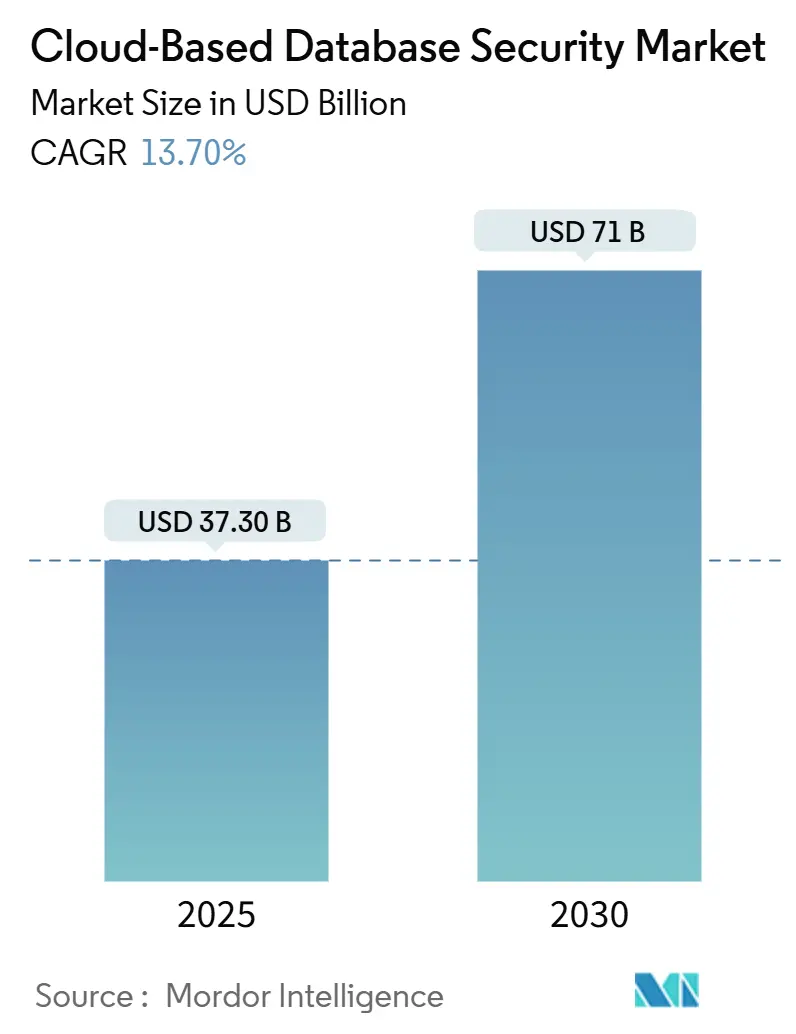

| Market Size (2025) | USD 37.30 Billion |

| Market Size (2030) | USD 71 Billion |

| Growth Rate (2025 - 2030) | 13.70% CAGR |

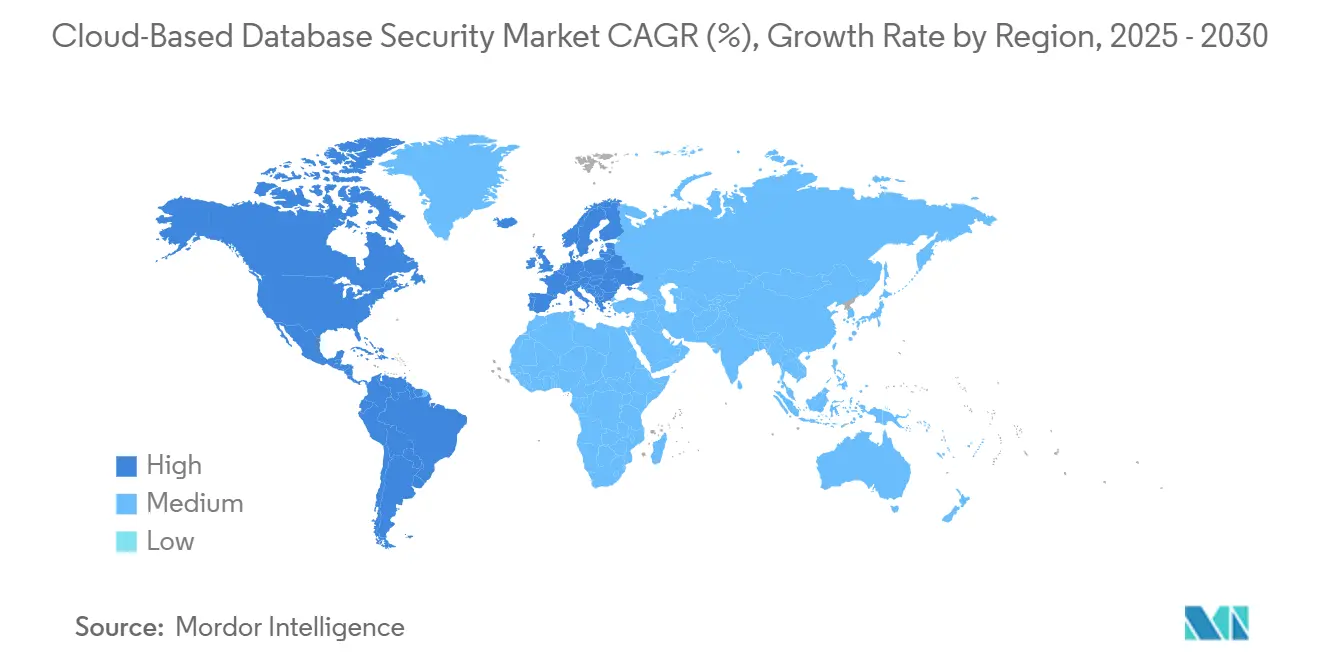

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud-Based Database Security Market Analysis by Mordor Intelligence

The cloud-based database security market size is estimated at USD 37.3 billion in 2025 and is forecast to reach USD 71.02 billion by 2030, advancing at a 13.7% CAGR. Rising migration of mission-critical workloads to public, private, and hybrid clouds is stretching traditional perimeter defenses, compelling enterprises to implement data-centric controls inside the database layer. Mandatory encryption of electronic protected health information under the tightened HIPAA rule, effective in 2025, and stronger multi-factor authentication mandated by PCI-DSS 4.0 are accelerating procurement cycles in highly regulated industries. Financial institutions continue to modernize cybersecurity stacks in step with digital banking expansion, while healthcare providers confront breach costs that averaged USD 10.9 million per incident in 2024. Rapid adoption of NoSQL and multi-model databases, post-quantum cryptography standards finalized by NIST in 2024, and AI-driven anomaly-detection features embedded in modern database activity monitoring platforms together underpin a robust long-term demand outlook.[1]National Institute of Standards and Technology, “NIST Releases First 3 Finalized Post-Quantum Encryption Standards,” nist.gov

Key Report Takeaways

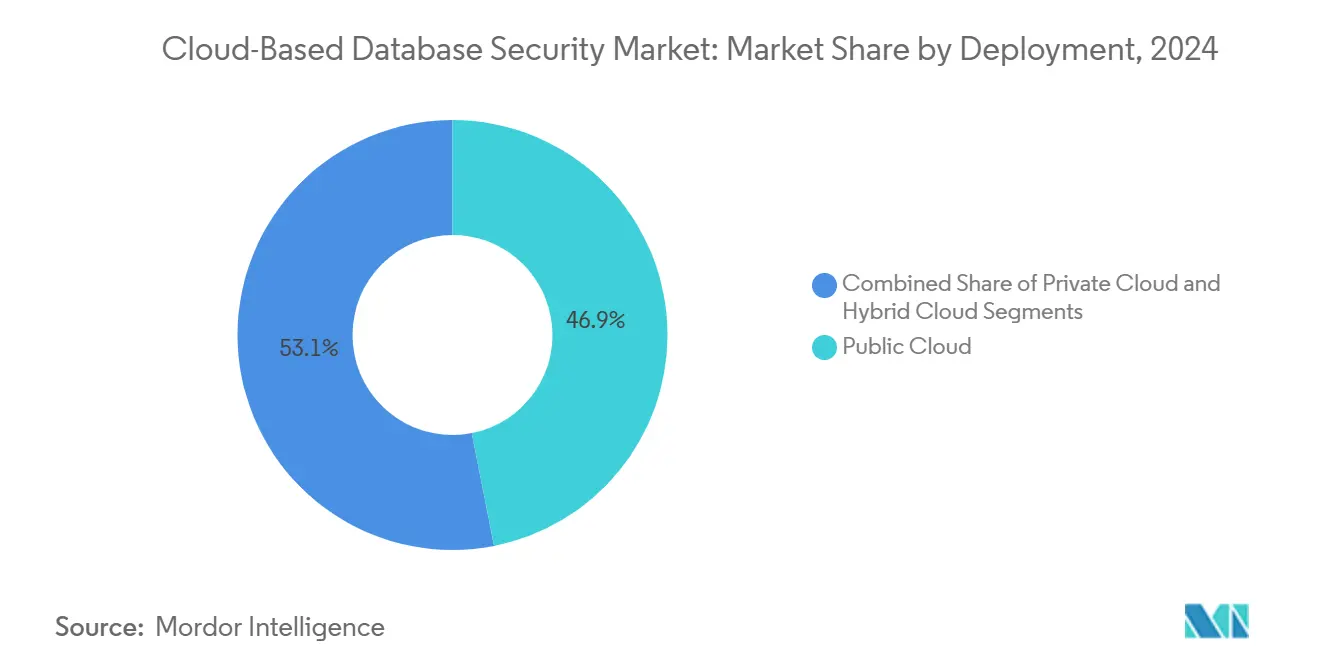

- By deployment, public cloud held 46.9% of the 2024 revenue; hybrid architectures are set to grow at the fastest rate, with a 15.4% CAGR to 2030.

- By end-user industry, the BFSI segment led with a 28.0% share of the cloud-based database security market in 2024, whereas the healthcare segment is projected to expand at a 17.7% CAGR through 2030.

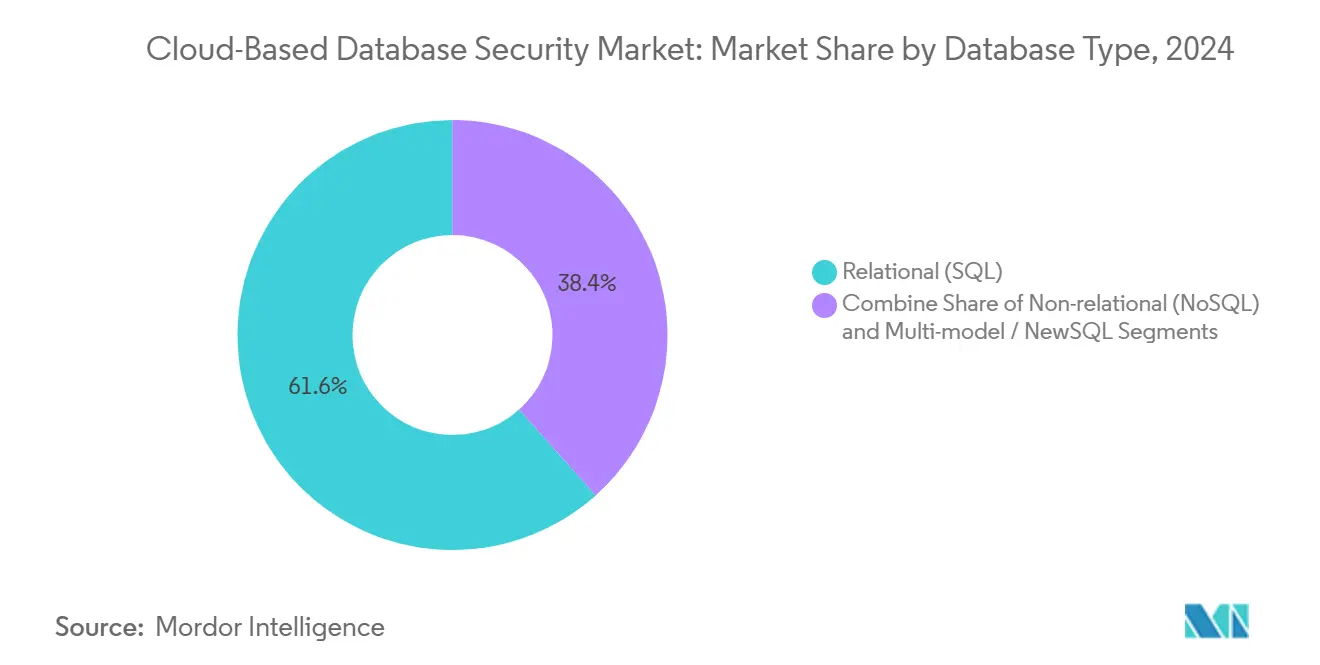

- By database type, relational platforms accounted for 61.6% of the revenue in 2024, while NoSQL implementations are expected to increase at a 22.5% CAGR through 2030.

- By security service function, access-control and identity-management services captured 32.9% of the 2024 revenue; encryption and tokenization services are expected to rise at an 18.8% CAGR during the forecast period.

- By geography, North America commanded 34.5% of the revenue in 2024; the Asia-Pacific region is advancing at the highest 16.6% CAGR through 2030.

Global Cloud-Based Database Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating volumes of mission-critical data in cloud workloads | +2.8% | North America, APAC | Medium term (2-4 years) |

| Heightened regulatory compliance requirements | +3.2% | Europe, North America | Short term (≤ 2 years) |

| BFSI sector cloud-first refresh cycles | +1.9% | North America, Europe | Medium term (2-4 years) |

| Hybrid and multi-cloud complexity | +2.1% | APAC, North America | Long term (≥ 4 years) |

| NoSQL / multi-model database adoption | +1.6% | Tech-forward regions | Medium term (2-4 years) |

| AI-driven anomaly detection | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Volumes of Mission-Critical Data in Cloud Workloads

Enterprises report that three-quarters of their cloud-resident information now qualifies as sensitive, a sharp shift from the early cloud era when non-critical data dominated. Industrial-manufacturing leaders such as Siemens and Merck are funneling telemetry from IoT devices into cloud data stores for predictive-maintenance analytics, increasing exposure while improving plant uptime. The average breach cost climbed to USD 4.88 million in 2024, prompting boards to authorize preventive spending on cloud-native encryption, tokenization and continuous monitoring solutions. Modern platforms support granular key management and vaultless tokenization that preserve data formats, enabling analytics without decrypting raw values.

Heightened Regulatory Compliance (GDPR, PCI-DSS, CCPA, etc.)

European regulators imposed multimillion-euro fines in 2024 for cloud-database misconfigurations that exposed personal data, signaling stricter GDPR scrutiny.[2]U.S. Federal Register, “Preventing Access to U.S. Sensitive Personal Data by Countries of Concern,” federalregister.govPCI-DSS 4.0 expands multi-factor authentication coverage to all cardholder-data environment access paths, forcing payment processors to re-architect database gateways before Q1 2025. India’s forthcoming Data Protection and Privacy Act and Vietnam’s localization mandates illustrate the compliance patchwork that multinational firms must navigate. Many organizations now treat adherence not as a cost center but as a competitive trust signal that helps win privacy-conscious customers

BFSI Sector’s Cloud-First Cybersecurity Refresh Cycles

Banks and insurers are re-platforming core transaction systems, embedding behavioral analytics and fraud-detection models inside database activity monitoring layers. JPMorgan Chase’s AI-enabled engine cut false positives by 30% while reducing unauthorized data exposure by 93.7%. Regulators in several jurisdictions responded to incident-response findings by prescribing stronger identity controls and encryption at rest for all financial databases, reinforcing a steady upgrade cadence.

Hybrid and Multi-Cloud Complexity Fueling Unified Security Layers

Seventy-nine percent of enterprises now run workloads across two or more hyperscale providers, and 55% say controlling data across those environments is harder than on-premises operations. Microsoft’s Cloud-Native Application Protection Platform fuses posture-management, workload protection and runtime monitoring to deliver a single operating picture, reducing tool sprawl and administrative gaps. Manufacturing majors like Toyota apply similar integrated controls to secure data flowing between edge gateways and cloud datastores that power supply-chain optimization algorithms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and location-control concerns | -2.4% | Global, strongest in Europe and APAC | Medium term (2-4 years) |

| Global shortage of cloud-security skillsets | -1.8% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Real-time analytics latency from in-line encryption/authentication | -1.2% | Global, particularly affecting high-frequency trading and real-time systems | Short term (≤ 2 years) |

| Vendor lock-in tied to proprietary cloud-native security stacks | -0.9% | Global, most pronounced in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Location-Control Concerns

A January 2025 U.S. rule restricts foreign access to sensitive American personal data, adding new licensing hurdles for cross-border database replication.[3]European Data Protection Board, “EDPB News,” edpb.europa.eu European buyers insist on EU-based hosting and custodial key control to satisfy GDPR and Schrems II transfer limitations, while Vietnam enforces in-country data residency for critical operators. Maintaining equivalent security controls in parallel jurisdictions inflates operational overhead and can slow full-cloud migrations.

Global Shortage of Cloud-Security Skillsets

Organizations struggle to recruit professionals who can blend traditional database administration with zero-trust architecture, AI-based anomaly-detection tuning and multicloud policy orchestration. Research shows many healthcare workers still fail to report phishing attempts, underscoring the human-factor gap even when technical safeguards exist. Vendors respond with managed-service offerings, yet talent scarcity remains a drag on the adoption rate in smaller enterprises and emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Configurations Drive Innovation

Hybrid deployments are climbing at a 15.4% CAGR through 2030, even though public-cloud instances retained 46.9% revenue in 2024. This trajectory reflects how regulated firms combine on-premises data stores for sovereign workloads with cloud elasticity for analytics. The cloud-based database security market size for hybrid environments is projected to rise in parallel with manufacturing’s Industry 4.0 rollout, where latency-sensitive shop-floor equipment streams data into regional edge nodes before synchronizing with cloud warehouses. Vendors offer policy engines that auto-translate classification labels and encryption rules between Kubernetes clusters, private-cloud OpenStack pools, and hyperscale SQL PaaS services, reducing misconfiguration risk during workload migration.

Organizations value hybrid models for disaster-recovery resilience and granular compliance zoning. Toyota’s supply-chain modernization shows how DevSecOps pipelines can push microservice-based inventory apps to Azure while backend Oracle databases remain in private racks until encryption-in-use hardware reaches maturity. CData’s 2025 Arc release introduced native two-factor authentication and EU-tenant isolation capabilities designed expressly for hybrid environments where cloud and on-premises connectors share the same workflow engine. As encryption-in-flight becomes mandatory for healthcare workloads under updated HIPAA guidance, hybrid gateways that terminate TLS at the data-layer will capture additional share in the cloud-based database security market.

By End-User Industry: Healthcare Leads Growth Transformation

Healthcare’s 17.7% CAGR through 2030 outpaces every vertical because ransomware operators disproportionately target electronic health record systems and imaging repositories. The cloud-based database security market size for healthcare is forecast to expand as providers adopt mandatory encryption and zero-trust segmentation to comply with HIPAA’s elimination of “addressable” clauses. Advanced tokenization preserves clinical-workflow performance while shielding Personal Health Information fields from unauthorized analytics queries.

The BFSI segment still contributed the largest revenue slice at 28.0% in 2024, reflecting four decades of mainframe-grade access controls that are now being recreated in cloud-native formats. AI-enhanced transaction monitoring embedded at the database layer allows real-time interdiction of anomalous payment patterns. Government agencies focus on sovereign-cloud deployments, leveraging FedRAMP-consented services with hardened audit trails. Retailers and e-commerce marketplaces integrate database protection with fraud-scoring engines to defend against account takeovers that surged after the 2024 holiday season, motivating incremental investment in workload encryption and just-in-time access grants.

By Database Type: NoSQL Expansion Creates New Security Paradigms

NoSQL platforms are climbing at 22.5% CAGR, widening the threat surface because document and key-value stores traditionally rely on network segmentation rather than table-level access control. Most vulnerable misconfigurations stem from default-allow bindings in DevOps sandboxes that later progress to production without credential rotation. The cloud-based database security market share for relational engines remained dominant at 61.6% in 2024, yet modern key-management APIs increasingly treat both relational and NoSQL resources as first-class objects, enabling unified policy push.

Academic work from the University of Central Florida demonstrates how malicious insiders can exploit eventual-consistency replication lag to infer theoretically protected fields in Database-as-a-Service offerings. In response, vendors integrate probabilistic-risk scoring into database activity monitors, flagging out-of-cycle write bursts typical of algorithmic exfiltration attempts. Distributed-ledger anchoring of cloud logs ensures tamper-evident telemetry for forensic review, a design increasingly adopted in financial-services pilots that require proof of data integrity across geographies.

By Security Service Function: Encryption Technologies Lead Innovation

Access-control frameworks delivered 32.9% revenue in 2024, underscoring identity as the first guardrail for database traffic. However, encryption and tokenization services will post the fastest 18.8% CAGR because algorithm agility and quantum-safe modes have become board-level concerns. The cloud-based database security market size for encryption is set to swell as 68% of CISOs flag “harvest now, decrypt later” risk scenarios.

NIST’s FIPS 203 and 204 standards give vendors the clarity to embed lattice-based algorithms in Transparent Data Encryption modules, providing forward secrecy without radical application refactoring. Meanwhile, machine-learning classifiers process millions of historical query plans to detect lateral-movement patterns that elude signature-based detectors, elevating the role of AI in database activity monitoring.

Geography Analysis

Asia-Pacific is projected to log a 16.6% CAGR through 2030, fueled by nationwide cloud-first directives in India and Vietnam alongside heavy investment in hyperscale regions by U.S. and Chinese providers. Japan’s Information Security White Paper 2024 attributed a spike in ransomware hits on port-terminal systems to credential reuse across cloud-based management consoles, encouraging adoption of zero-trust database gateways. Australia’s Critical Infrastructure Act similarly drives encryption projects inside energy-sector data lakes.

North America retained 34.5% revenue in 2024 as early adopters extend shared-responsibility models to include encryption-in-use and confidential computing enclaves. The Department of Defense Cloud Security Playbook calls for synchronous auditing between application and database layers, effectively merging DevSecOps pipelines and data-protection controls. Large enterprises increasingly deploy policy-as-code frameworks that replicate identity graphs across AWS, Azure, and Google Cloud to satisfy tighter Sarbanes-Oxley audit demands.

European revenue expands at a modest pace because GDPR vigilance raises compliance costs but also stimulates uptake of privacy-enhancing technologies. The European Data Protection Board’s 2024 maneuvers placed cloud-database encryption posture among the top inspection themes, and France’s CNIL levied fines for marketing-database misconfigurations that left telemetry unencrypted at res. Providers respond with sovereign-cloud variants that enforce in-region key custody and e-delivery standards.

South America and the Middle East and Africa exhibit steady double-digit growth as telecom modernizers embrace 5G core clouds and governments digitize citizen services, though shortages of cloud-security specialists slow complex zero-trust rollouts. Managed-security-service providers bridge the talent gap by bundling database-protection modules with SOC-as-a-Service offerings, accelerating entry for mid-market adopters.

Competitive Landscape

Moderate fragmentation defines the cloud-based database security market as hyperscale platforms - AWS, Microsoft Azure, and Google Cloud - bundle native controls, while pure-play specialists focus on AI, tokenization, or sovereign-cloud niches. IBM reclassified data security revenue under its broader Data segment, signifying a shift toward treating protection as an intrinsic database capability rather than an external add-on.

Consolidation quickened in 2024-2025. IBM’s acquisition of HashiCorp aligned Terraform’s infrastructure-as-code templates with Guardium Insights, simplifying policy propagation in multi-cloud pipelines. MongoDB’s purchase of Voyage AI augments query-optimization engines with trustworthy AI routines that can distinguish benign from malicious query bursts at a millisecond scale.

Patent intensity remains high. Google secured claims on field-preserving encryption that allows tokenization without schema rewrites, lowering migration friction from legacy Oracle to cloud-native Postgres engines. Start-ups like Akamai’s zero-trust identity partner, P3M, court government deployments where chain-of-custody requirements prohibit offshore key handling.[4]Akamai Technologies, “Akamai and FPT partner to help customers build and support cloud-native applications,” akamai.com

White-space opportunities remain in securing time-series and vector databases that underlie generative-AI platforms, a segment where current toolsets provide only coarse-grained access control.

Cloud-Based Database Security Industry Leaders

IBM Corporation

Intel Security Group

Fortinet Technologies Inc.

McAfee, LLC

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Akamai and FPT partnered to help customers build cloud-native applications with embedded zero-trust identity controls

- March 2025: IBM completed its acquisition of HashiCorp, integrating advanced infrastructure-automation tooling with IBM’s cloud-database protection stack

- February 2025: MongoDB acquired Voyage AI to embed trustworthy-AI features into its database platform

- January 2025: The U.S. Department of Justice enforced Executive Order 14117 restricting foreign access to sensitive personal data, impacting cross-border database replication strategies

Global Cloud-Based Database Security Market Report Scope

The Cloud-Based Database Security Market Report Can Be Segmented by Deployment (Public Cloud, Private Cloud, and Hybrid Cloud), End-User Industry (BFSI, Retail and E-Commerce, Government and Public Sector, Healthcare and Life Sciences, IT and Telecom, Manufacturing, and Other Industries), Database Type (Relational (SQL), Non-Relational (NoSQL), and Multi-Model/NewSQL), Security Service Function (Access Control and IAM, Data Encryption and Tokenization, Database Activity Monitoring and Auditing, Backup/Recovery and Data Masking, and Other Functions Including Risk and Compliance and Consulting), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts Are Provided in Terms of Value (USD).

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| BFSI |

| Retail and e-Commerce |

| Government and Public Sector |

| Healthcare and Life Sciences |

| IT and Telecom |

| Manufacturing |

| Other Industries |

| Relational (SQL) |

| Non-relational (NoSQL) |

| Multi-model / NewSQL |

| Access Control and IAM |

| Data Encryption and Tokenization |

| Database Activity Monitoring and Auditing |

| Backup, Recovery and Data Masking |

| Others (Risk and Compliance, Consulting) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Deployment | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By End-user Industry | BFSI | |

| Retail and e-Commerce | ||

| Government and Public Sector | ||

| Healthcare and Life Sciences | ||

| IT and Telecom | ||

| Manufacturing | ||

| Other Industries | ||

| By Database Type | Relational (SQL) | |

| Non-relational (NoSQL) | ||

| Multi-model / NewSQL | ||

| By Security Service Function | Access Control and IAM | |

| Data Encryption and Tokenization | ||

| Database Activity Monitoring and Auditing | ||

| Backup, Recovery and Data Masking | ||

| Others (Risk and Compliance, Consulting) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the growth outlook for the cloud-based database security market through 2030?

The cloud-based database security market is projected to rise from USD 37.3 billion in 2025 to USD 71.02 billion by 2030, registering a 13.7% CAGR.

Which deployment model is expanding fastest?

Hybrid architectures lead growth at a 15.4% CAGR as enterprises balance data-sovereignty needs with cloud scalability.

Why is healthcare the most dynamic end-user segment?

Healthcare faces escalating ransomware threats and new HIPAA encryption mandates, driving a 17.7% CAGR for security spending.

How will post-quantum cryptography impact database protection?

NIST’s 2024 standards enable vendors to integrate lattice-based algorithms, future-proofing encrypted data against quantum-computer attacks.

What role does AI play in modern cloud-based database security?

AI powers anomaly-detection engines that learn query patterns and flag suspicious access in real time, cutting false positives and breach dwell time.

Page last updated on: