Medical Coding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.15 Billion |

| Market Size (2031) | USD 42.43 Billion |

| Growth Rate (2026 - 2031) | 9.34% CAGR |

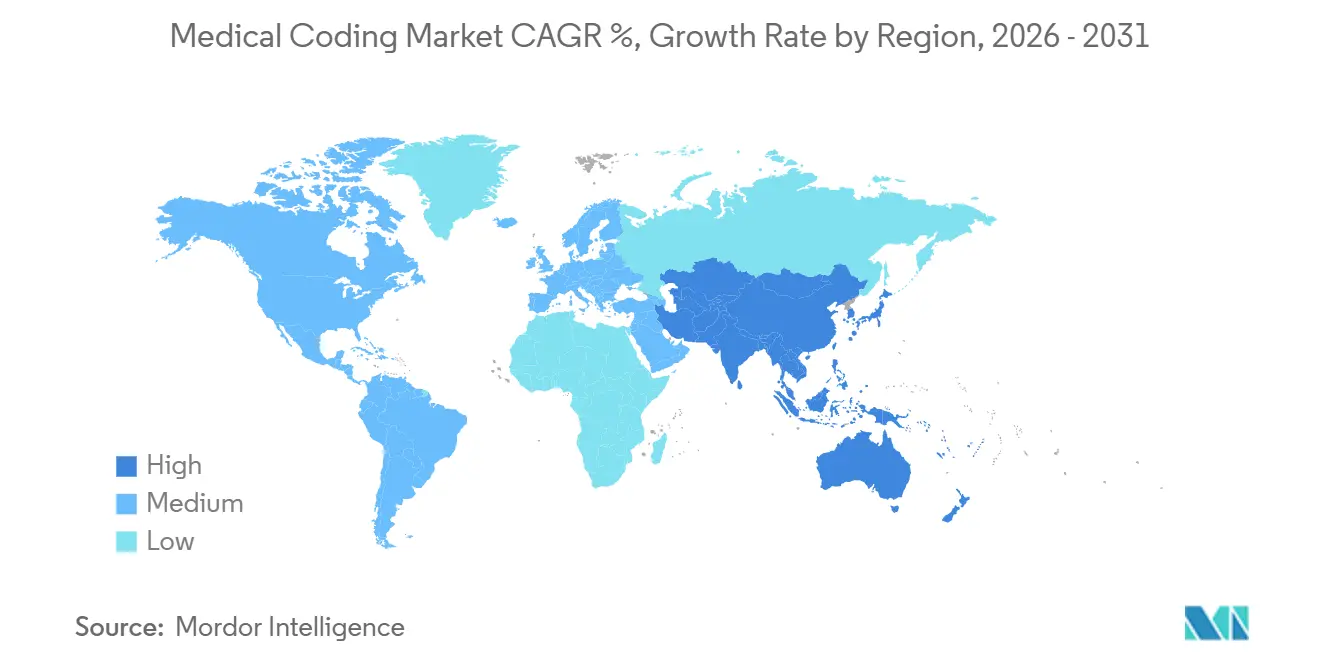

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

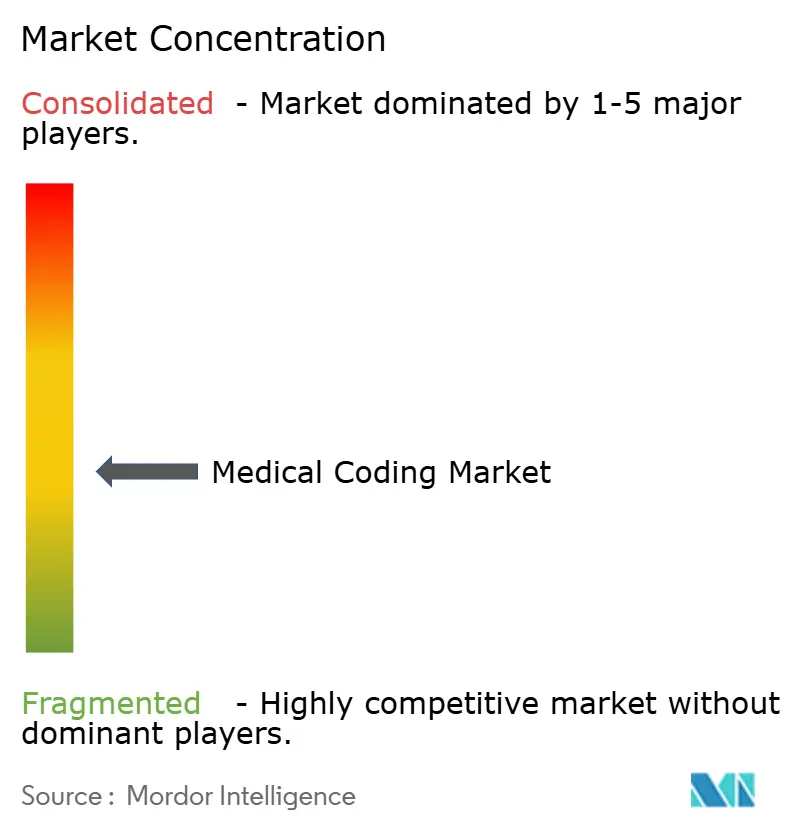

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Coding Market Analysis by Mordor Intelligence

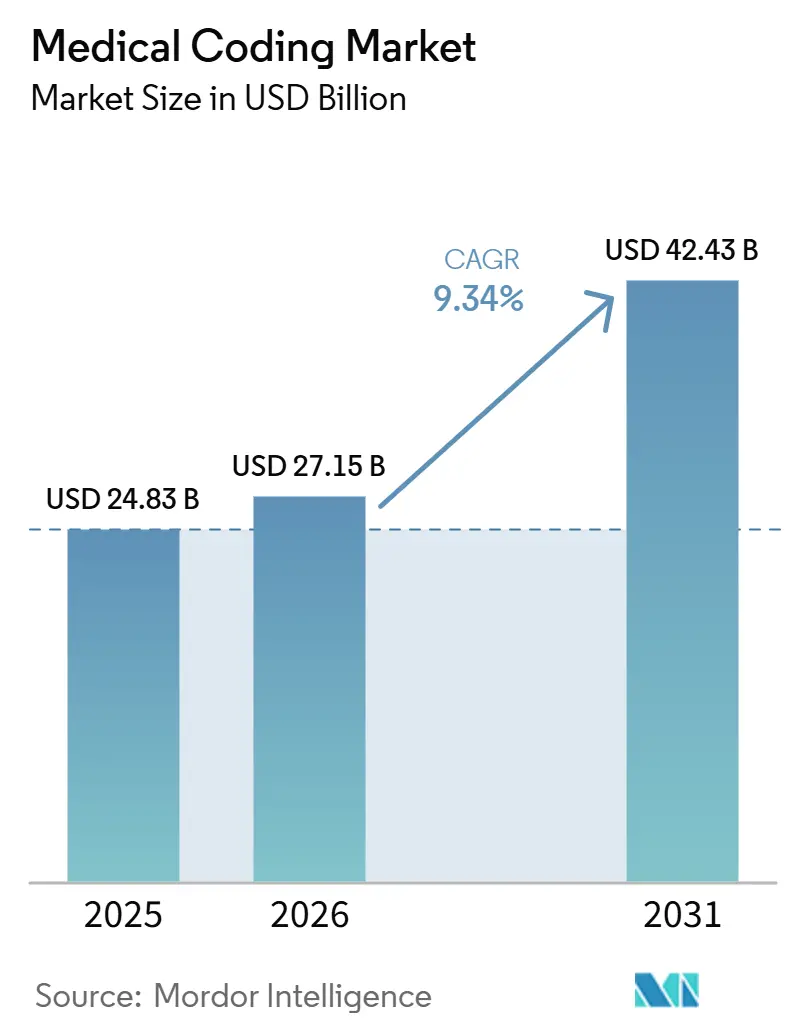

The Medical Coding Market size is expected to grow from USD 24.83 billion in 2025 to USD 27.15 billion in 2026 and is forecast to reach USD 42.43 billion by 2031 at 9.34% CAGR over 2026-2031.

Cloud-hosted platforms dominate because hospitals prefer scalable, subscription-based systems that integrate smoothly with electronic health records. Web access also enables remote teams, a necessity since healthcare providers still confront a 30% coder shortfall. The fast rollout of ICD-11, expansion of national insurance programs in emerging economies, and accelerating use of AI tools to cut charge lags all reinforce demand. Strategic acquisitions among service providers and software firms signal a race to build end-to-end solutions that link documentation, coding, and claims seamlessly across every care setting.

Key Report Takeaways

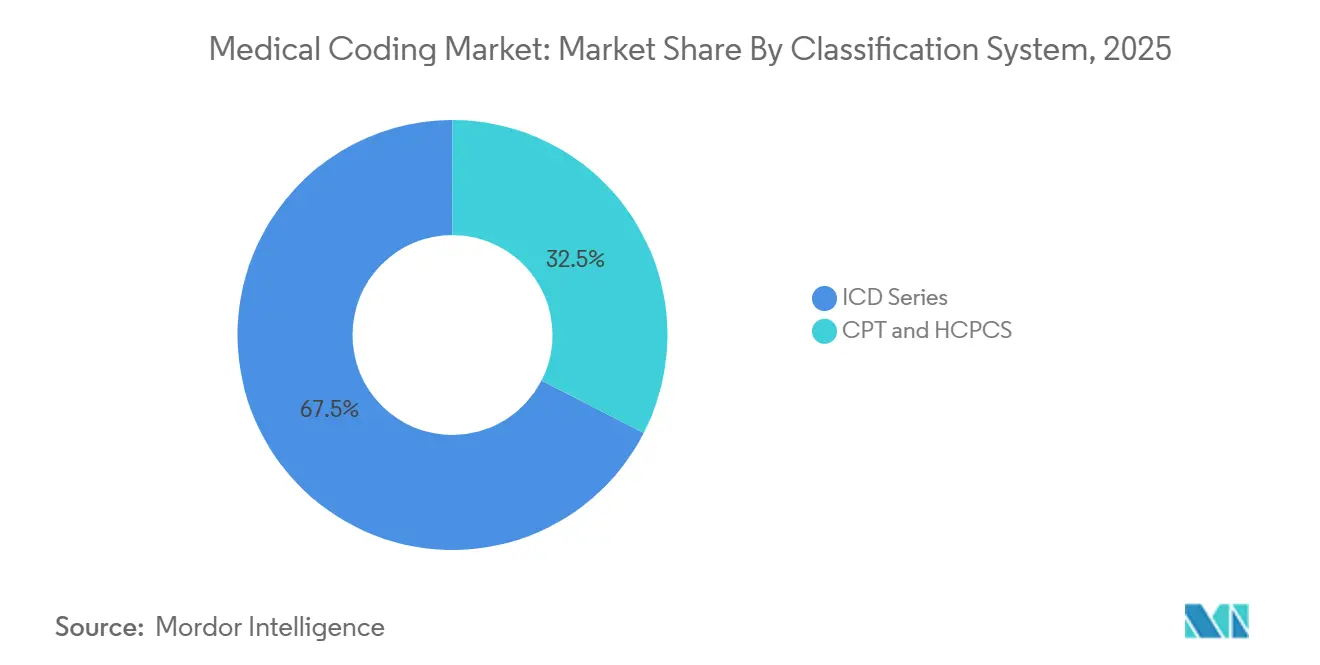

- By classification system, ICD series held 66.88% medical coding market share in 2025; it is projected to record a 9.88% CAGR to 2031.

- By component, outsourcing captured 59.71% of the medical coding market size in 2025 and is expanding at 10.41% CAGR through 2031.

- By delivery mode, web and cloud platforms accounted for 69.62% of the medical coding market in 2025; they are forecast to grow 11.08% a year to 2031.

- By end user, hospitals led with 40.12% revenue share in 2025, while insurance payers are advancing at an 10.76% CAGR through 2031.

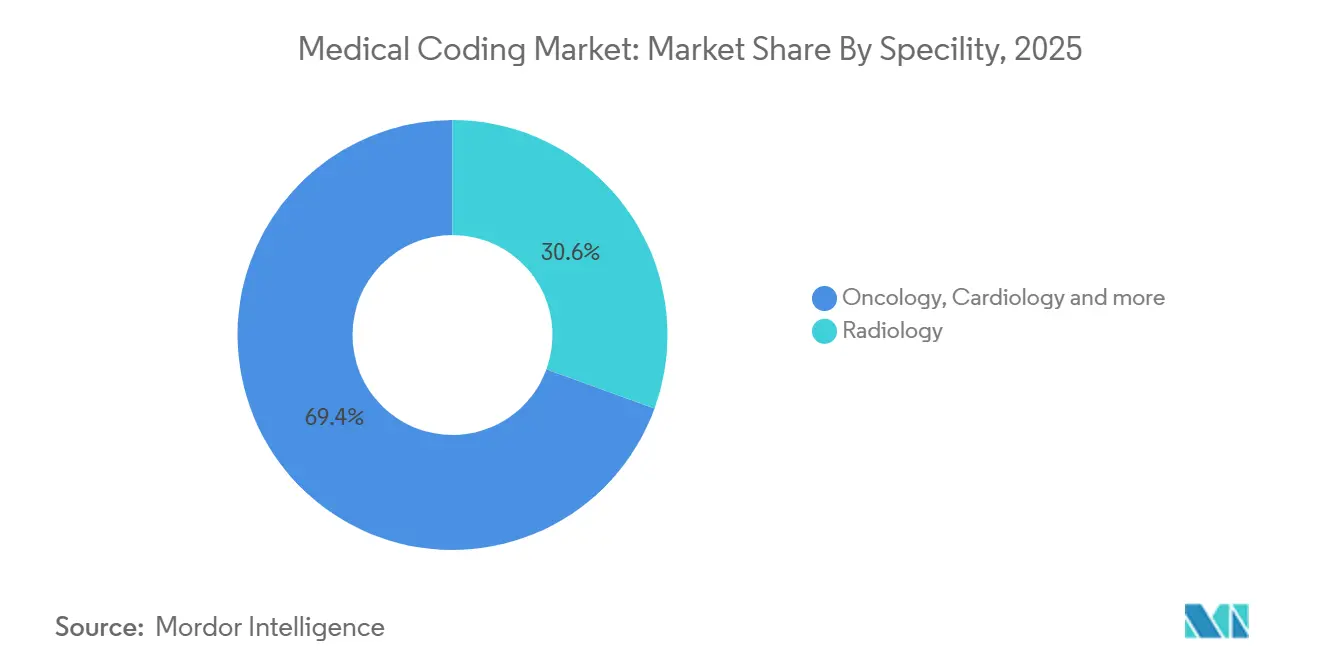

- By specialty, radiology held 29.35% of the medical coding market share in 2025; oncology is the fastest-growing specialty at 12.11% CAGR to 2031.

- By region, North America commanded 54.20% of the medical coding market in 2025; Asia-Pacific is rising the fastest at 11.04% CAGR between 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Coding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transition to ICD-11 and global standardization of healthcare coding | 2.30% | Global | Medium term (2-4 years) |

| Surge in healthcare claims volume amid aging populations | 1.80% | North America, APAC, Europe | Short term (≤2 years) |

| Accelerating adoption of AI-assisted auto-coding solutions in hospitals | 2.60% | Global | Long term (≥4 years) |

| Expansion of public health insurance schemes in emerging countries | 1.40% | Asia-Pacific, Latin America | Long term (≥4 years) |

| Regulatory push for accurate risk adjustment under value-based care programs | 1.20% | United States, selected OECD markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Transition to ICD-11 and global standardization

ICD-11 came into force on 1 January 2022 and now spans about 17,000 diagnostic categories and 130,000 clinical terms. The 2025 release adds multilingual support across 14 languages and introduces clustered codes that capture complex conditions more precisely. Fourteen European, eleven Asia-Pacific, six African, and four American nations already use the new system, prompting large-scale software upgrades and staff retraining. Vendors supplying automated map-ping tools and bundled training are gaining contracts because health systems must convert legacy ICD-10 libraries. The United States is expected to need a four-to-five-year migration window because its ICD-10-CM variant contains more than 70,000 codes, creating sustained business for transition consultants.

Surge in healthcare claims volume amid aging populations

Payers process unprecedented claim loads as seniors require multifaceted care; Humana alone adjudicates 480,000 claims. Electronic data interchange covers 96% of Medicaid submissions, and 99.1% clear within ten days, compressing revenue cycles. Faster payment targets obligate coders to match rising acuity with pinpoint documentation. Hospitals are therefore investing heavily in computer-assisted platforms that combine natural language processing with real-time edits to curb denials. Vendors able to scale processing power during seasonal spikes, such as influenza peaks, command premium contracts.

Accelerating adoption of AI-assisted auto-coding solutions in hospitals

Tampa General Hospital’s pilot uncovered USD 1 million that had been missed across 13,000 infusion cases, proving the revenue impact of machine learning engines . The U.S. Department of Veterans Affairs now runs the 3M RevCycle Health Services Platform on AWS GovCloud, showing that federal agencies also endorse cloud AI for coding efficiency. Leading suppliers aim for 70% autonomous coding coverage, a target enabled by models that continuously learn from clinician phrasing. As coder shortages persist, buyers treat AI as a strategic hedge against labor gaps and documentation errors.

Expansion of public health insurance schemes in emerging countries

Emerging nations launch universal coverage, prompting investments in robust claim-processing frameworks that tie directly to ICD-11. Asia-Pacific’s medical coding market grows at 11.30% CAGR because Indian and Philippine outsourcing hubs supply certified coders at competitive cost while domestic systems also digitize. Governments require antifraud analytics, so providers integrating rule-based flagging with coding platforms win tenders. Over time, authorities move from fee-for-service to value-based care, demanding even richer data capture and thus boosting demand for advanced coding modules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of certified coders | −1.9% | North America, Europe | Short term (≤2 years) |

| Continuous regulatory code-set updates causing operational disruptions | −1.5% | Global | Medium term (2-4 years) |

| Data security & HIPAA compliance concerns in offshore coding centers | −1.1% | United States, EU | Short term (≤2 years) |

| High training costs limiting adoption in small physician practices | −0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute shortage of certified coders

The United States posts a 30% coder vacancy rate, with many employees nearing retirement [1]Source: American Medical Association, “Addressing another health care shortage: medical coders,” ama-assn.org. Baptist Health Medical Group recently received 300 applicants for 20 internal training slots, illustrating training bottlenecks. Pay scales and signing bonuses are climbing, but smaller clinics struggle to compete. Outsourcing therefore grows 10.67% annually, and AI rollouts receive accelerated funding to offset staff deficits. High turnover also raises compliance risks because new hires often need six months of experience before coding autonomously, slowing productivity during onboarding.

Continuous regulatory code-set updates causing operational disruptions

CMS releases major CPT and HCPCS revisions each November for the following year [2]Source: Centers for Medicare & Medicaid Services, “List of CPT/HCPCS Codes,” cms.gov. The churn forces quarterly software patches and frequent staff retraining. The American Medical Association notes that unbundling and upcoding errors tied to rapid changes remain top audit findings. Providers therefore favor subscription platforms that push updates automatically while logging version histories for auditors. Yet even with automation, the change burden diverts clinical documentation improvement teams away from quality initiatives, dampening throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Medical Coding Market - Segmental Analysis

Classification System: ICD Series Dominates Amid Global Transition

The ICD family captured 67.46% medical coding market share in 2025 and is forecast to expand at a 10.07% CAGR, reflecting the World Health Organization’s stewardship and near-universal adoption. The medical coding market size tied specifically to ICD transition services is widening as hospitals license mapping tools, run dual-coding pilots, and train physicians in new cluster codes. Demand is especially strong among multinational health networks that must maintain cross-border data comparability.

The rollout of ICD-11’s 2025 edition brings natural language processing hooks and post-coordination logic, enabling vendors to package AI engines that parse narrative notes directly into compliant code sets. Consulting firms expect a multiyear wave of software refreshes, and government insurers are updating claim adjudication logic simultaneously. CPT and HCPCS remain critical in the United States for outpatient procedures, yet they complement rather than displace ICD.

By Component: Outsourcing scales amid workforce limitations

Outsourced services controlled 60.32% of the medical coding market in 2025, accelerating at 10.67% CAGR as hospitals convert fixed staffing costs to variable contracts. The medical coding market size assigned to third-party vendors is therefore expanding faster than in-house platforms. Health systems select partners that guarantee accuracy levels above 95%, especially for high-complexity specialties.

Consolidation continues; e4health’s acquisition of eCatalyst Healthcare Solutions adds audited coding and clinical documentation integrity under one banner. Many regional hospitals now run hybrid models where core inpatient charts stay in-house while specialized outpatient volumes shift offshore for overnight turnaround. Vendors offering teletraining to client staff and flexible staffing pools for peak volumes enjoy higher renewal rates.

By Delivery Mode: Cloud solutions unlock interoperability

Cloud and web platforms held 70% medical coding market share in 2025 and are forecast to climb at 11.35% CAGR. Hospitals prefer browser-based portals that merge seamlessly with revenue cycle suites and electronic health records. The medical coding market size attributable to cloud subscriptions benefits from OPEX budgeting and quicker deployment cycles compared to on-premises software.

The Department of Veterans Affairs choice of AWS GovCloud for its 3M RevCycle Health Services Platform underscores confidence in compliant public-cloud storage for protected health information. Automatic version control means ICD, CPT, and HCPCS updates roll out globally overnight, cutting downtime. Vendors bundle analytics dashboards that highlight denial trends and coder productivity, creating stickier client relationships.

By End User: Hospitals lead yet payers invest aggressively

Hospitals and clinics generated 40.71% of 2025 revenue, anchored by large inpatient case loads requiring multi-system coding. They rely on enriched AI engines for radiology, surgery, and cardiology, each with custom edits. Insurance payers, though smaller today, represent the medical coding market’s fastest-growing end-user group, with a 11.02% CAGR. They embed coding verification within pre-adjudication workflows to curb fraud and support value-based payment models.

Payers increasingly purchase the same natural language processing modules as providers but apply them post-submission to validate documentation. Some have started offering feedback loops to physicians that flag high-risk coding patterns, effectively turning oversight tools into provider education platforms. Alignment between payer and provider systems can reduce denial processing times and generate shared savings.

By Specialty Type: Radiology anchors volume while oncology accelerates

Radiology produced 30% of 2024 revenue, reflecting high procedure volume and mature digital imaging workflows. Coders navigate varied modality combinations, so AI decision support that links DICOM metadata with narrative reports sees rapid uptake. The medical coding industry segment for radiology retains strong margins because even incremental accuracy gains translate to substantial revenue across daily imaging volumes.

Oncology grows at 12.56% CAGR as precision medicine proliferates. Targeted therapies, genetic markers, and combination regimens require granular, sometimes novel codes. The American Heart Association’s guidance on cardio-oncology imaging further complicates documentation, propelling demand for multispecialty edits. Vendors releasing specialty-specific oncology modules, such as Optum360’s 2025 update, aim to automate capture of regimen cycles, biomarker results, and adverse events within a single coding pass.

Geography Analysis

North America held 55% of the medical coding market in 2025. CMS reimbursement policies drive exacting documentation standards, pushing hospitals toward AI-enabled platforms that curb denial risk. Ongoing coder shortages are driving outsourcing adoption, while regional consolidations, such as e4health’s purchase of eCatalyst, illustrate the value of scalable service footprints. Providers also accelerate internal coder upskilling through AAPC partnerships because the ICD-11 timeline remains undefined domestically.

Asia-Pacific is the fastest-growing region, with a 11.30% CAGR between 2026 and 2031. Eleven nations have already implemented ICD-11, and governments invest heavily in electronic health record platforms to extend insurance coverage. India and the Philippines export certified coders to global clients, capitalizing on English-language proficiency and robust vocational pipelines. Growing public insurance schemes and modernization in China and Japan drive continuous platform upgrades suited to high-volume claims.

Europe maintains steady growth underpinned by 14 countries that have fully adopted ICD-11. Coding primarily informs epidemiological tracking and resource planning across nationalized systems, yet value-based care pilots intensify demand for richer outcome codes. Strict GDPR rules elevate data-protection requirements, steering buyers toward cloud vendors with proven encryption and regional hosting. Cloud adoption also supports workforce mobility as many European coders now work remotely across borders.

Competitive Landscape

Competitive Landscape

Global competition is moderately fragmented. Technology leaders such as 3M, Optum360, and Microsoft-owned Nuance integrate natural language processing and analytics, while service firms focus on scalable coding, audit, and clinical documentation integrity offerings. Average valuation multiples span 12-30× EBITDA for tech-driven revenue cycle platforms, reflecting investor appetite for automated coding engines scoperesearch.co.

Acquirers prize companies with proprietary AI or strong offshore delivery centers. Private-equity funds often merge several mid-tier specialists to create national platforms capable of servicing multi-state health systems.

Product roadmaps focus on deeper specialty libraries, automated code-set updates, and tighter EHR integration that minimizes manual toggling. Vendors invest in explainable AI to satisfy auditor scrutiny and train clinicians to improve note specificity at the point of care. Partnerships with professional societies ensure that emerging therapy protocols translate quickly into coded terminology, shortening revenue realization cycles for providers adopting novel treatments.

Medical Coding Industry Leaders

3M Health Information Systems

Optum360 (UnitedHealth Group)

nThrive, Inc. (FinThrive)

Nuance Communications (Microsoft Corp.)

Aviacode, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Optum launched an AI-powered revenue-cycle platform designed to cut administrative burden by improving documentation and coding accuracy.

- February 2025: World Health Organization released the 2025 ICD-11 update featuring enhanced interoperability and multilingual support across 14 languages

- December 2024: e4health acquired Phoenix-based eCatalyst Healthcare Solutions, expanding outsourced coding and clinical-documentation-integrity services.

- October 2024: Centers for Medicare & Medicaid Services confirmed the 2025 CPT/HCPCS Code List publication date of 26 Nov 2024, signaling upcoming reimbursement changes.

- September 2024: EQT entered an agreement to acquire a controlling interest in GeBBS Healthcare Solutions, highlighting continued investor appetite for revenue-cycle assets.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the medical coding market as all software, tools, and service hours devoted to translating clinical encounters into ICD, CPT, or HCPCS codes across provider and payer settings worldwide, covering hospitals, ambulatory centers, insurance processors, and pure-play coding vendors. According to Mordor Intelligence, this scope captures value that flows directly through coding desks or embedded computer-assisted coding (CAC) modules, expressed in 2025 dollars.

Scope exclusion: Solutions offering only billing, claim clearing, or general revenue-cycle tasks without a coding engine are not counted.

Segmentation Overview

- By Classification System (Value, USD)

- ICD Series (ICD-10, ICD-11)

- CPT

- HCPCS

- By Component (Value, USD)

- In-house Coding

- Outsourced Coding

- By Delivery Mode (Value, USD)

- On-premise

- Web & Cloud-based

- By End User (Value, USD)

- Hospitals and clinics

- Insurance Payers

- Others

- By Specialty Type (Value, USD)

- Radiology

- Oncology

- Cardiology

- Pathology

- Other Specialties

- By Geography (Value, USD)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africe

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed coding managers at multispecialty hospitals, leaders of offshore business-process firms, health-IT product managers, and payer compliance officers across North America, Europe, Asia, and the Gulf. Conversations clarified typical code output per full-time coder, average selling price by specialty, and adoption hurdles for CAC, which sharpened our model assumptions.

Desk Research

We began with health system statistics from entities such as the Centers for Medicare & Medicaid Services, the World Health Organization's ICD-11 update library, and the Bureau of Labor Statistics for coder employment costs. Trade bodies like the American Hospital Association and the Medical Group Management Association provide patient-volume and claim-denial ratios, while export volumes of coding services were benchmarked through UN Comtrade. Paid intelligence from D&B Hoovers aided in triangulating revenue booked by large outsourcing firms. This list is illustrative; dozens of additional public and subscription sources underpinned the fact base.

Market-Sizing & Forecasting

A top-down reconstruction starts with inpatient and outpatient encounters, applies region-specific coding penetration and fee curves, then layers export revenues for third-party coding hubs. Select bottom-up checks, sampled coder head-count x productivity, CAC license roll-ups, and channel ASP snapshots validate totals. Key variables include:

1. Annual hospital discharges and ambulatory visits 2. Outsourcing penetration rates 3. Average codes generated per visit 4. Mean coding fee per claim 5. ICD-11 rollout tempo 6. Health-IT spending growth

Multivariate regression links these inputs to historical market value; scenario analysis molds the 2025-2030 outlook. Gaps in bottom-up estimates are bridged using coded-claim ratios from primary interviews.

Data Validation & Update Cycle

Outputs pass variance checks against historic coder wage indices and denial-rework rates, followed by a dual-analyst review. Reports refresh yearly, with mid-cycle revisions if regulatory or pricing shocks occur. Before release, an analyst re-verifies figures so clients receive the latest view.

Why Mordor's Medical Coding Baseline Commands Reliability

Published estimates often diverge because firms mix broader revenue-cycle services, apply divergent fee assumptions, or freeze exchange rates early. By isolating pure coding value and refreshing inputs annually, Mordor offers a balanced anchor for planning.

In sum, scope alignment, variable transparency, and a disciplined refresh cadence let Mordor deliver a dependable, easily traceable baseline for executives weighing investment, outsourcing, or product decisions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.83 B (2025) | Mordor Intelligence | - |

| USD 39.86 B (2024) | Global Consultancy A | Bundles wider RCM and audit services, inflating base |

| USD 30.34 B (2024) | Industry Analytics B | Uses uniform ASPs, ignores offshore price differentials |

| USD 32.45 B (2025) | Trade Journal C | Includes AI billing tools without human-coder revenue adjustment |

In sum, scope alignment, variable transparency, and a disciplined refresh cadence let Mordor deliver a dependable, easily traceable baseline for executives weighing investment, outsourcing, or product decisions.

Key Questions Answered in the Report

What is the size of the medical coding market?

The medical cosing market size stands at USD 27.15 billion in 2026.

How significant is the coder shortage in North America?

The United States currently faces a 30% shortage of certified coders, encouraging hospitals to outsource services and deploy AI platforms to maintain accuracy.

Why are cloud-based coding platforms preferred over on-premises software?

Cloud solutions offer secure, browser-based access, automatic code-set updates, easy integration with EHRs, and subscription pricing that reduces capital expense.

Which region is expanding fastest in the medical coding market?

Asia-Pacific is growing at 11.04% CAGR as nations adopt ICD-11, expand public insurance, and leverage large pools of trained coders.

What specialties require the most advanced coding tools today?

Radiology generates the highest volume, but oncology shows the fastest growth because complex precision therapies need highly granular codes.

How will AI change medical coding workflows by 2031?

Vendors aim to automate coding for at least 70% of cases, using natural language processing to extract data directly from clinician notes, which will reduce manual workload and error rates.

Page last updated on: