Blood Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

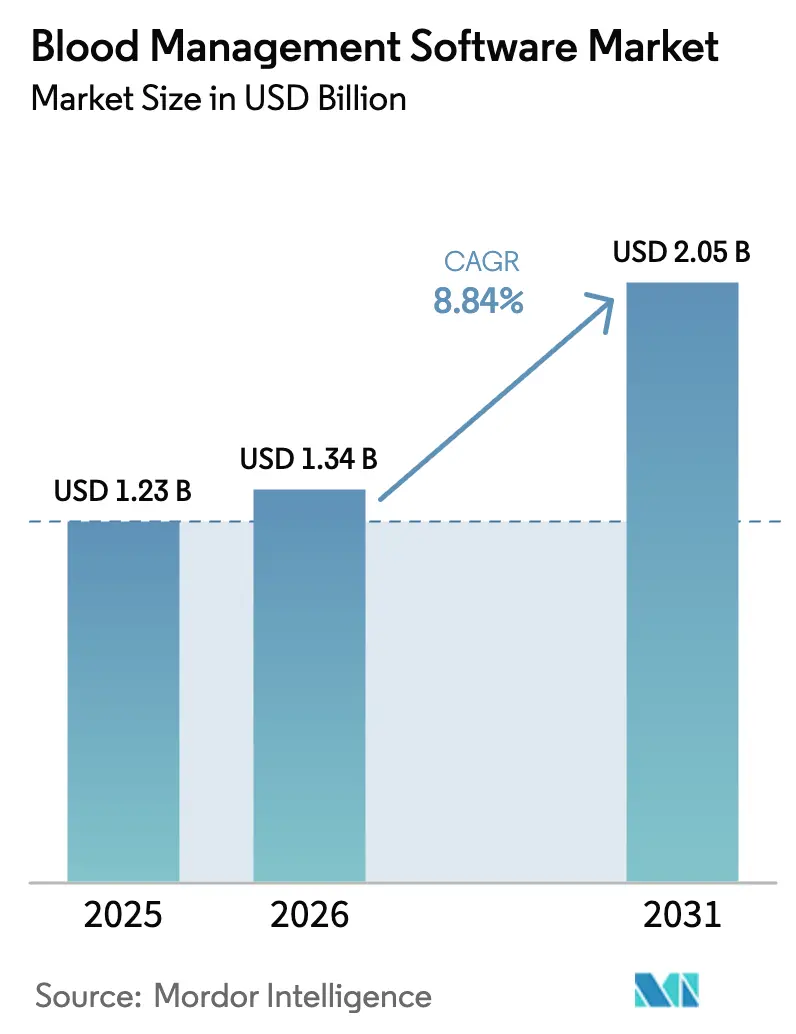

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 8.84% CAGR |

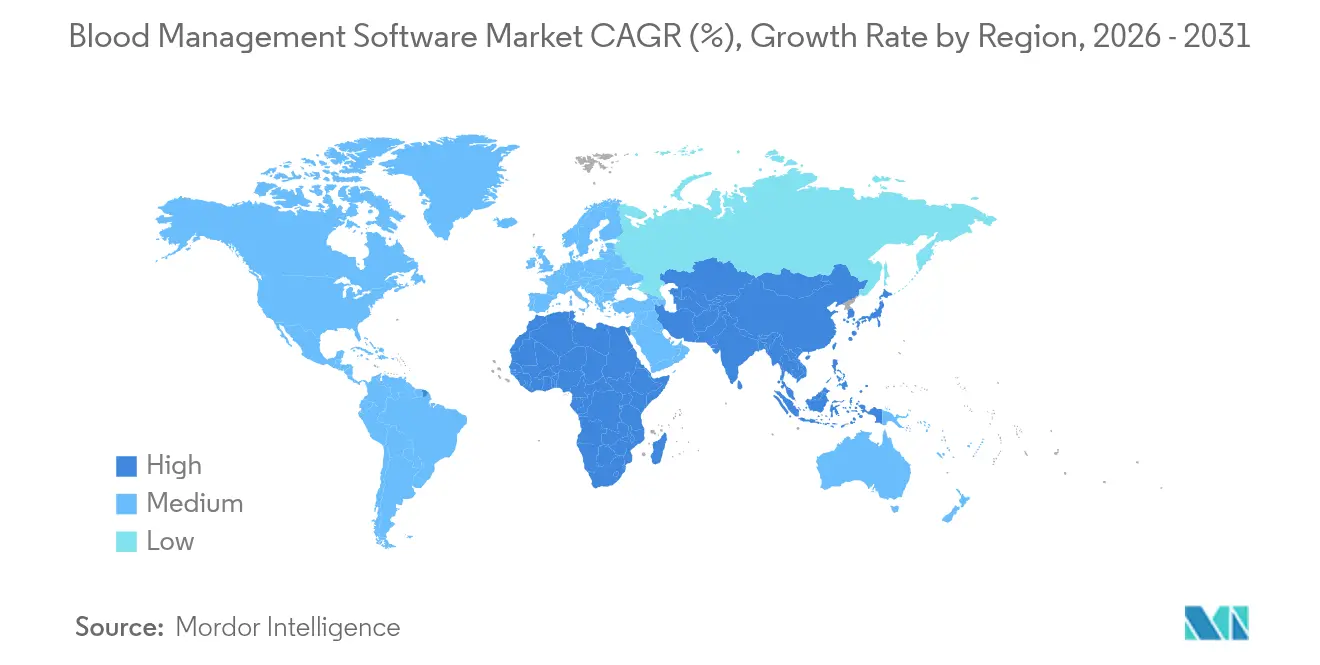

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Blood Management Software Market Analysis by Mordor Intelligence

The blood management software market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.34 billion in 2026 to reach USD 2.05 billion by 2031, at a CAGR of 8.84% during the forecast period (2026-2031). Steady replacement of paper files with unified digital platforms is improving traceability, regulatory compliance and patient safety while cutting manual workloads. Cloud deployments, now mainstream, let blood centers scale capacity on demand and avoid capital spending. Heightened haemovigilance rules—most notably the European Union’s forthcoming Substances of Human Origin (SoHO) Regulation—are pushing every establishment toward real-time, audit-ready data trails.[1]European Commission, “SoHO Regulation,” European Commission, health.ec.europa.euArtificial-intelligence modules that predict usage and flag shortages are also gaining traction, supported by Association for the Advancement of Blood & Biotherapies (AABB) evidence showing 40% lower red-cell inventories without supply risk.[2]Association for the Advancement of Blood & Biotherapies, “AI and Data Sciences in Blood Banking,” AABB News, aabb.org Consolidation among niche vendors and diagnostics giants is accelerating, illustrated by Thermo Fisher Scientific’s 2025 purchase of HistoTrac to deepen transplant-diagnostics data management .

Key Report Takeaways

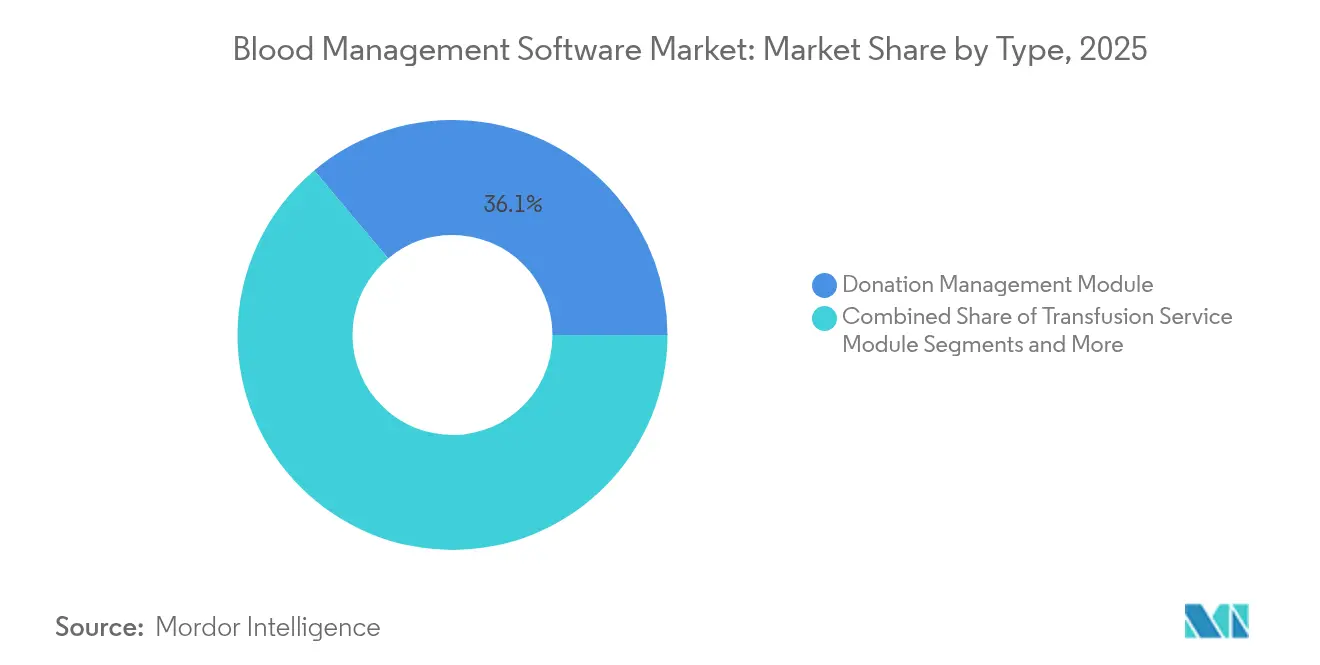

- By type, the Donation Management Module led with 36.12% of the blood management software market share in 2025, while Compliance & QA modules are forecast to expand at an 11.25% CAGR through 2031.

- By deployment, cloud/SaaS platforms accounted for 52.01% revenue and will post the fastest 11.92% CAGR to 2031.

- By end user, hospitals held 46.95% of 2025 revenues; public-health and Red-Cross agencies show a 10.35% CAGR to 2031.

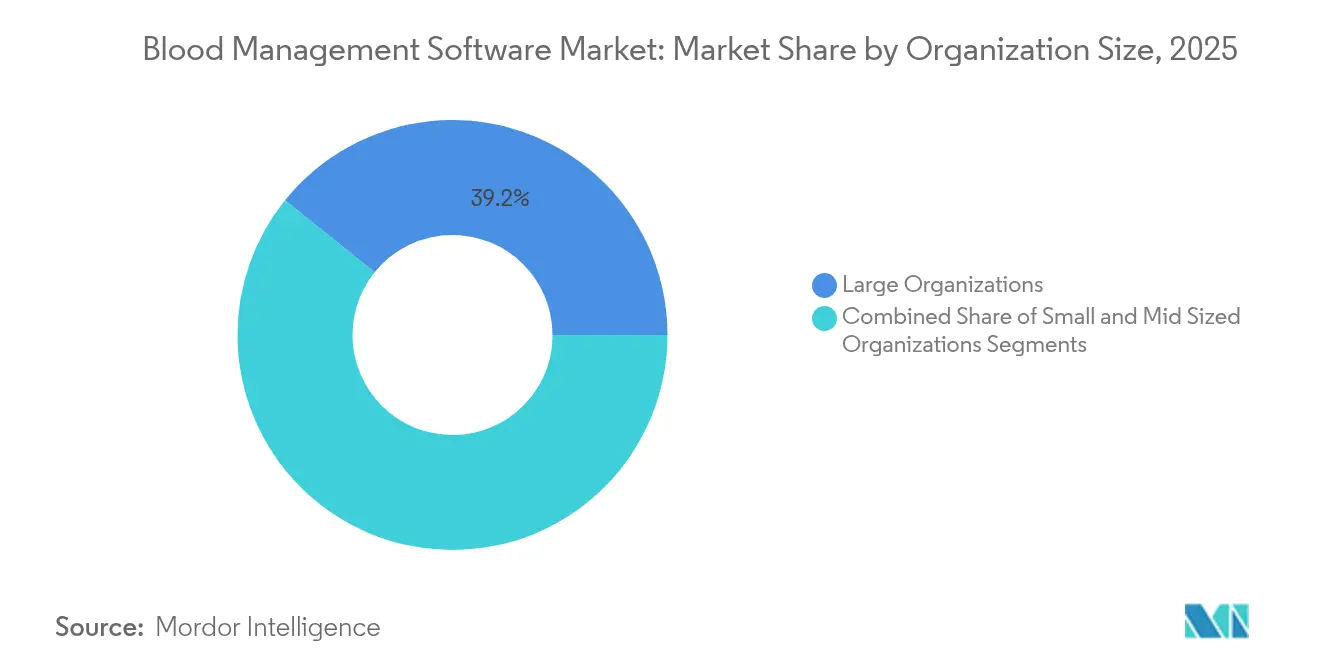

- By organization size, large institutions captured 39.22% of 2025 spend, whereas small centers (<200 beds) are growing at 10.62% CAGR.

- By interface, web solutions drove 46.78% of 2025 sales; mobile apps are accelerating at 11.31% CAGR.

- Regionally, North America commanded 38.10% of 2025 revenue; Asia-Pacific is advancing at an 10.95% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume Of Voluntary Blood Donations | +1.8% | Global, with stronger impact in APAC and MEA | Medium term (2-4 years) |

| Growing Prevalence Of Hematologic & Chronic Disorders | +2.1% | Global, concentrated in aging populations of North America and Europe | Long term (≥ 4 years) |

| Mandatory Haemovigilance & Traceability Regulations | +1.5% | Europe and North America, expanding to APAC | Short term (≤ 2 years) |

| Cloud-First & AI-Driven Product Innovations | +2.3% | North America and Europe leading, APAC following | Medium term (2-4 years) |

| Blockchain Pilots For Cold-Chain‐Verified Blood Provenance | +0.7% | North America and Europe pilot markets | Long term (≥ 4 years) |

| Mobile Donor-Engagement Apps Boosting Retention Rates | +1.2% | Global, with higher adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Voluntary Blood Donations

Blood establishments are modernizing donor-management workflows to handle larger volumes of altruistic donations. The European Commission counts 15 million donors supplying 22 million annual units, activity that demands end-to-end digital traceability. University Hospitals processed 4,300 more samples in 2024 than 2023, leading to 12,000 extra tests, a workload manageable only through automated recordkeeping. Cloud portals such as Degree37 allow real-time appointment scheduling, eligibility checks and retention analytics. FDA rules mandating 10-year donor-history storage increase the need for searchable electronic deferral logs. As voluntary programs replace replacement-donor models, scalable databases become mission-critical.

Growing Prevalence of Hematologic & Chronic Disorders

Ageing populations and chronic diseases are pushing demand for platelets, plasma and antigen-matched red cells. Teaching-hospital audits showed a 5% increase in Massive Transfusion Protocol activations during 2024, triggering stronger forecasting requirements. Advanced software integrates with electronic health records to automate compatibility checks across multiple blood-group systems, including rare phenotypes. Thermo Fisher’s BloodGenomiX array covers nearly 20,000 genomic markers; lab teams need robust platforms to store and interpret that file volume. Machine-learning routines fine-tune order sets, helping operators cut wastage without risking shortages—a capability proven during COVID-19 disruptions, according to AABB.

Mandatory Haemovigilance & Traceability Regulations

The EU SoHO Regulation taking full effect in 2027 requires digital audit trails and cross-border data exchange health.ec.europa.eu. Similar obligations appear in FDA and CDC guidance, compelling U.S. centers to adopt systems compatible with the National Healthcare Safety Network.[3]Centers for Disease Control and Prevention, “Blood Safety | NHSN,” Centers for Disease Control and Prevention, cdc.govThe Serious Hazards of Transfusion program in the U.K. attributes many errors to inadequate IT links, underscoring the software imperative. Integrating donor, laboratory and recipient data on a single platform lets managers run near-real-time recalls, lookbacks and adverse-event reports.

Cloud-First & AI-Driven Product Innovations

Cloud architecture now underpins more than half of all installations, offering instant scalability and smoother disaster recovery. Bloodbuy’s exchange links multiple centers and hospitals, trimming outdates through data-driven matching. AABB trials show 40% smaller inventories when AI predicts demand. Oracle’s coming AI-enabled EHR will use voice commands to surface transfusion data, hinting at a hands-free workflow. Peer-reviewed research confirms that AI applied to routine blood tests improves diagnostic yield. Cloud models also simplify upgrades, letting vendors push new compliance features without local downtime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of IT-Skilled Transfusion Staff | -1.4% | Global, more acute in developing markets | Medium term (2-4 years) |

| High Upfront Licence & Integration Costs | -1.8% | Global, particularly impacting smaller organizations | Short term (≤ 2 years) |

| Cyber-Security & PHI-Privacy Liabilities | -1.1% | Global, with higher impact in regulated markets | Short term (≤ 2 years) |

| Legacy LIS Interoperability Gaps | -0.9% | Primarily developed markets with established systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of IT-Skilled Transfusion Staff

Modern platforms demand teams fluent in both transfusion medicine and database configuration, a rare skill mix. AABB’s IT in Blood Banking certificate, priced below USD 600, aims to close that gap. Northern Ireland’s CoreLIMS project required months of training before go-live, illustrating the learning curve. Smaller centers often rely on vendors for daily support, inflating operating expenses and slowing innovation.

High Upfront Licence & Integration Costs

Total cost of ownership spans software, hardware refresh, data migration and process redesign. Springer research shows health-system migrations demand lengthy planning and dedicated budgets. University Hospitals had to digitize 30 years of antibody paperwork during its OnBase rollout, a sizeable archival task. Return-on-investment arguments become tougher when small organizations compare minimal legal compliance with cutting-edge analytics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Compliance Modules Drive Innovation

The compliance and quality-assurance segment is expanding at 11.25% CAGR, faster than any other module. Regulators are mandating tighter audit trails, prompting centers to embed deviation tracking, electronic lookbacks and real-time adverse-event dashboards. Donation-management software still delivers the largest revenue, holding 36.12% of 2025 revenues in the blood management software market. Demand for analytics and decision-support is also accelerating as centers seek AI-powered forecasting and genotype-matching engines. FDA clearance in 2025 for the Lookback Notification System v2.0 illustrates regulators’ support for integrated suites.

Growing adoption of these capabilities means the blood management software market size for compliance tools could outpace traditional donation features by 2031. Mid-cycle upgrades are leaning toward single-vendor ecosystems that fuse donor history, lab testing, labeling and transfusion outcomes into one auditable chain. Platforms able to harmonize these data silos position vendors for longer contracts and stickier revenue, especially in regions anticipating SoHO enforcement.

By Deployment Model: Cloud Dominance Accelerates

Cloud and SaaS deployments already account for 52.01% of 2025 spending within the blood management software market. Pay-as-you-go pricing and rapid provisioning appeal to both large hospital networks and community centers. Disaster-recovery designs mirror best practice across finance and retail, boosting confidence among risk officers. In contrast, on-premise solutions face slower feature release cycles and higher capital charges.

Between 2026 and 2031, cloud CAGR of 11.92% means more features—AI inventory predictions, blockchain-based cold-chain proof and voice-driven interfaces—will debut first in SaaS form. The blood management software market size attached to cloud subscriptions will therefore swell disproportionately. Vendors able to certify compliance with HIPAA, GDPR and EU SoHO will command premium pricing and reduce buyer hesitation.

By End User: Public-Health Agencies Emerge

Hospitals remain the primary buyers, representing 46.95% of 2025 sales, because blood supply sits at the junction of diagnostics, surgery and oncology. Integrated interfaces with electronic health records let clinicians order products and receive serology alerts without leaving their workflow. Public-health and Red-Cross agencies, however, are posting the quickest 10.35% CAGR. National digitization funds and large-scale outreach programs favor centralized systems that coordinate drives, track cold-chain logistics and broadcast shortage alerts on mobile apps.

As these agencies scale, the blood management software market share mix will shift: hospitals will still dominate dollar terms, yet NGOs and national services will drive unit growth. Successful suppliers offer multilingual portals, SMS integration and donor-engagement gamification to appeal to diverse populations.

By Organization Size: Small Centers Accelerate Adoption

Large, multi-hospital systems captured 39.22% of 2025 revenue, buying enterprise suites tightly linked to lab automation and enterprise resource planning. Smaller sites, once priced out, now adopt lean SaaS tiers that deliver core inventory, cross-match and donor modules without local servers. Annual growth of 10.62% reflects vendor focus on template workflows, in-app tutorials and 24/7 managed services.

Consequently, the blood management software market size generated by small institutions is narrowing the gap. Certification programs, including AABB’s IT certificate, lower onboarding friction and foster community best practice. Expect product roadmaps to maintain entry-level tiers even as advanced AI features roll out at the high end.

By Application Interface: Mobile Innovation Drives Growth

Web dashboards still account for 46.78% of 2025 demand, offering granular administration and integration with lab devices. Mobile interfaces, expanding at 11.31% CAGR, empower field collection teams and donor self-service. Features such as appointment booking, eligibility surveys and barcode scanning reduce queues and lift satisfaction. API-centric designs enable plug-and-play links to hospital and national registries, shrinking integration timelines.

As smartphones become the first point of contact for younger donors, mobile modules will capture an outsized portion of incremental spend within the blood management software market. Many providers ship mobile software development kits so hospitals can embed donation status into patient portals, tying community engagement to broader population-health goals.

Geography Analysis

North America held 38.10% of 2025 revenue thanks to mature health-IT ecosystems, early AI adoption and firm FDA oversight. January 2024 CLIA fee hikes and personnel-qualification updates raised compliance stakes, prompting software upgrades. High-profile ransomware incidents have also pushed executives to modern, cloud-secure platforms.

Asia-Pacific records the fastest 10.95% CAGR as governments invest in digitization and blood-science R&D. Japan’s hemoglobin-vesicle trials demonstrate the region’s scientific leadership and create new data-management demands for novel products. Mobile blood-collection drives in India show how donor apps can lift voluntary donations and feed real-time databases.

Europe, guided by harmonized SoHO rules, is steadily updating legacy systems for cross-border traceability. Northern Ireland’s CoreLIMS project illustrates large-scale transformation, with “vein-to-vein” tracking slated for 2026. Consistency across 27 EU members will ultimately favor vendors that certify modules for all languages and data-protection regimes.

Competitive Landscape

The market remains moderately fragmented. Diagnostics leaders such as Thermo Fisher are augmenting portfolios by acquiring specialized platforms like HistoTrac, signaling a pivot toward plug-in transplant and genomic modules. Cloud-native newcomers emphasize rapid updates, embedded analytics and consumption-based pricing, pressuring incumbents to streamline upgrade cycles.

Technology partnerships are proliferating. Oracle’s AI-driven EHR will surface transfusion data via conversational commands, while ELLKAY’s integration services help Babson Diagnostics feed micro-sample results into core records. Suppliers that can overlay blockchain provenance or gesture-driven mobile controls differentiate fast in tenders.

White-space opportunities persist in emerging markets and among small organizations where the blood management software industry historically lacked affordable tools. FDA device clearances for automated serology and electronic lookback further legitimize end-to-end suites and provide early-mover advantage to certified vendors.

Blood Management Software Industry Leaders

-

Veradigm LLC

-

WellSky

-

Haemonetics Corporation

-

Oracle

-

Epic Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Interswitch helped launch the Lagos State Blood Transfusion Committee’s Blood Inventory Management System, strengthening digital oversight in Nigeria.

- April 2025: Lytus Technologies finalized its purchase of Blod.in, an AI-powered platform for blood-component logistics.

- September 2024: Mexico unveiled the National Blood System to modernize donation and distribution across federal and state networks.

Global Blood Management Software Market Report Scope

Blood management software is a comprehensive solution tailored to streamline the storage, processing, retrieval, and analysis of data pivotal to the administrative, inventory, and clinical operations of blood banks.

The blood management software market is segmented into type, application type, end user, and geography. By type, the market is segmented into blood donor management module, blood bank transfusion service module, blood collection and processing module, and other types. The other types segment include inventory management, patient blood management, and others. By application type, the market is segmented into web-based and mobile-based. By end user, the market is segmented into hospitals, blood banks, and blood processing centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market size and forecast are provided in terms of value (USD).

| Donation Management Module |

| Transfusion Service Module |

| Blood Collection & Processing Module |

| Compliance & QA Module |

| Analytics / Decision-Support Module |

| On-premise |

| Cloud / SaaS |

| Hospitals |

| Stand-alone Blood Banks |

| Plasma & Apheresis Centers |

| Public Health & Red-Cross Agencies |

| Large (>500 beds / >100k annual units) |

| Mid-size (200-500 beds) |

| Small (<200 beds) |

| Web-based |

| Mobile-based |

| API-based Integration |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Donation Management Module | |

| Transfusion Service Module | ||

| Blood Collection & Processing Module | ||

| Compliance & QA Module | ||

| Analytics / Decision-Support Module | ||

| By Deployment Model | On-premise | |

| Cloud / SaaS | ||

| By End User | Hospitals | |

| Stand-alone Blood Banks | ||

| Plasma & Apheresis Centers | ||

| Public Health & Red-Cross Agencies | ||

| By Organization Size | Large (>500 beds / >100k annual units) | |

| Mid-size (200-500 beds) | ||

| Small (<200 beds) | ||

| By Application Interface | Web-based | |

| Mobile-based | ||

| API-based Integration | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the blood management software market?

The market is valued at USD 1.34 billion in 2026 and will reach USD 2.05 billion by 2031.

Which module segment is growing fastest?

Compliance and quality-assurance modules are expanding at an 11.25% CAGR driven by stricter haemovigilance rules.

Why are cloud deployments preferred?

Cloud models cut capital costs, provide elastic storage and enable rapid feature updates, supporting the market-leading 52.01% share in 2025.

Which region is the quickest to adopt these systems?

Asia-Pacific posts the fastest 10.95% CAGR, buoyed by government digitization programs and innovation in artificial blood.

How do AI tools benefit blood centers?

Machine-learning algorithms improve demand forecasts, reducing red-cell inventory by up to 40% without risking shortages.

Page last updated on: