Pharmacovigilance And Drug Safety Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

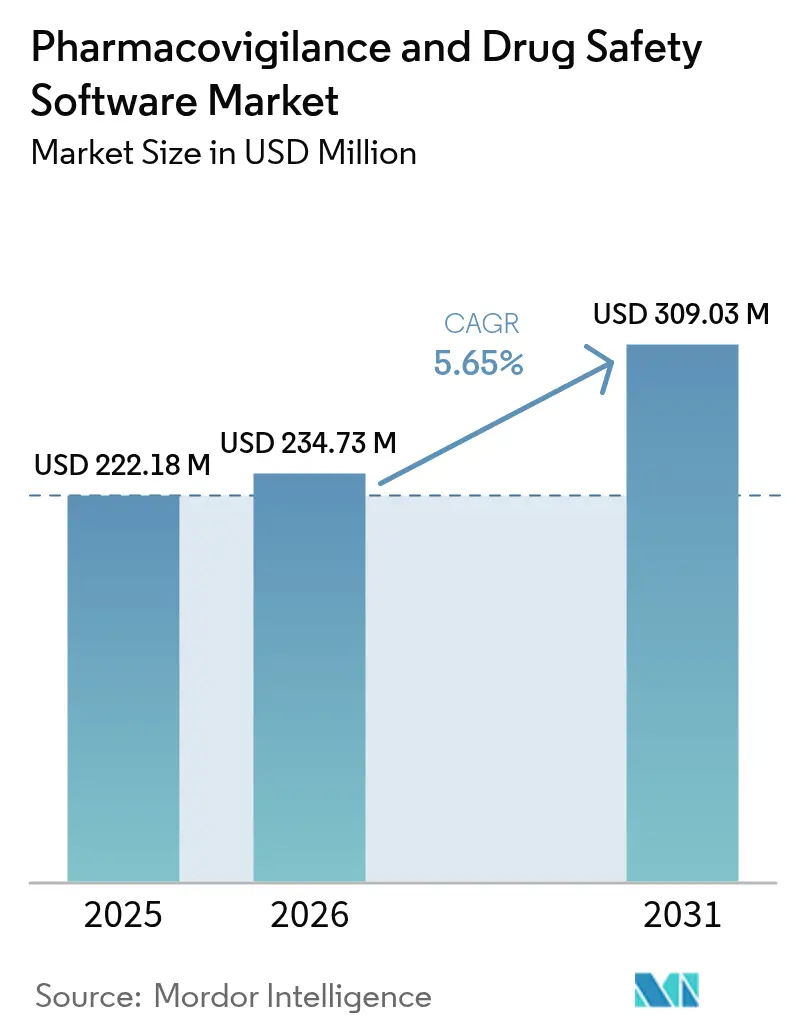

| Market Size (2026) | USD 234.73 Million |

| Market Size (2031) | USD 309.03 Million |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmacovigilance And Drug Safety Software Market Analysis by Mordor Intelligence

The pharmacovigilance software market size in 2026 is estimated at USD 234.73 million, growing from 2025 value of USD 222.18 million with 2031 projections showing USD 309.03 million, growing at 5.65% CAGR over 2026-2031. Growth pivots on the transition from basic compliance systems to AI-enabled safety intelligence platforms that help sponsors evaluate real-world evidence in near-real time. Intensifying harmonization of global reporting rules, spearheaded by the FDA’s E2B(R3) mandate and the European Health Data Space Regulation, converts regulatory deadlines into non-discretionary IT spending.[1]Food and Drug Administration, “Considerations for the Use of Artificial Intelligence To Support Regulatory Decision-Making for Drug and Biological Products,” fda.govCloud adoption crosses 80% penetration among life-science firms, creating a preferred deployment backbone for modern safety databases. Meanwhile, explainable-AI modules that automate case triage lower processing costs by as much as 50%, giving early adopters an economic edge. Geopolitical stability in Asia Pacific, coupled with streamlined ethics approvals, is relocating a rising share of clinical trials eastward and lifting regional demand for advanced surveillance tools.

Key Report Takeaways

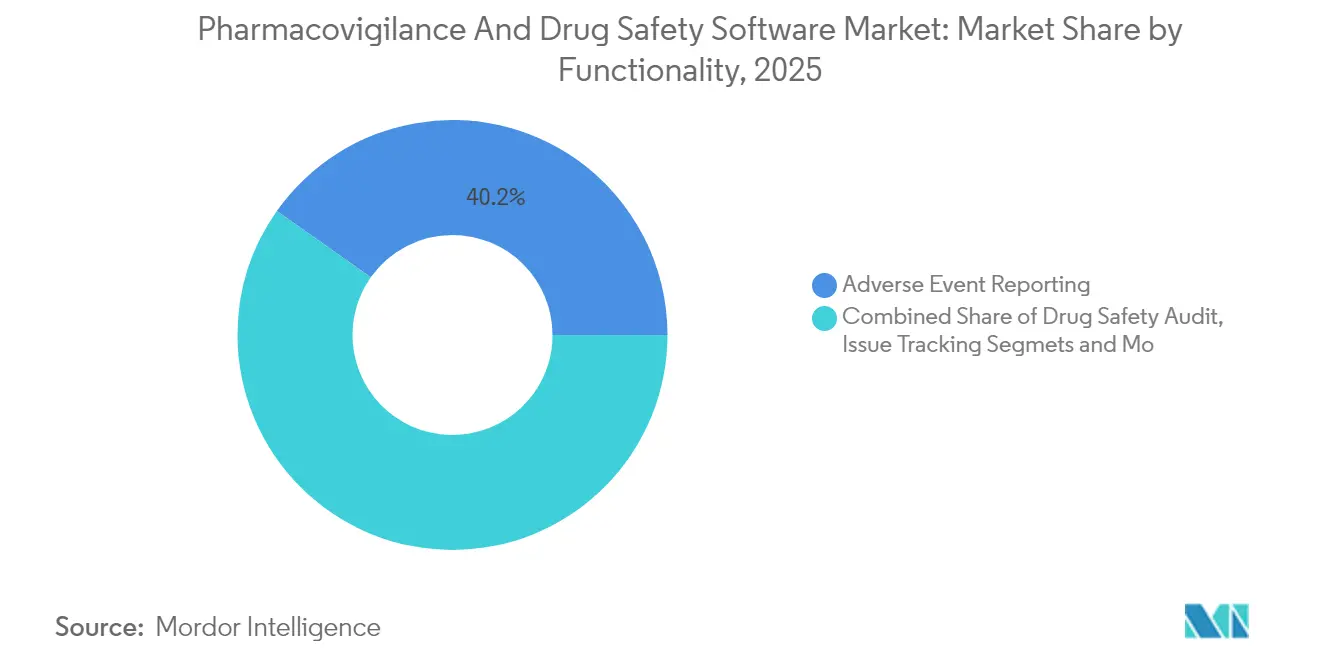

- By functionality, adverse event reporting led the pharmacovigilance software market with 40.22% of the share in 2025, while signal detection and risk management tools are poised to expand at an 17.5% CAGR through 2031.

- By mode of delivery, cloud and SaaS deployments captured 66.55% revenue share in 2025; the segment is growing at a 21.3% CAGR over the forecast period.

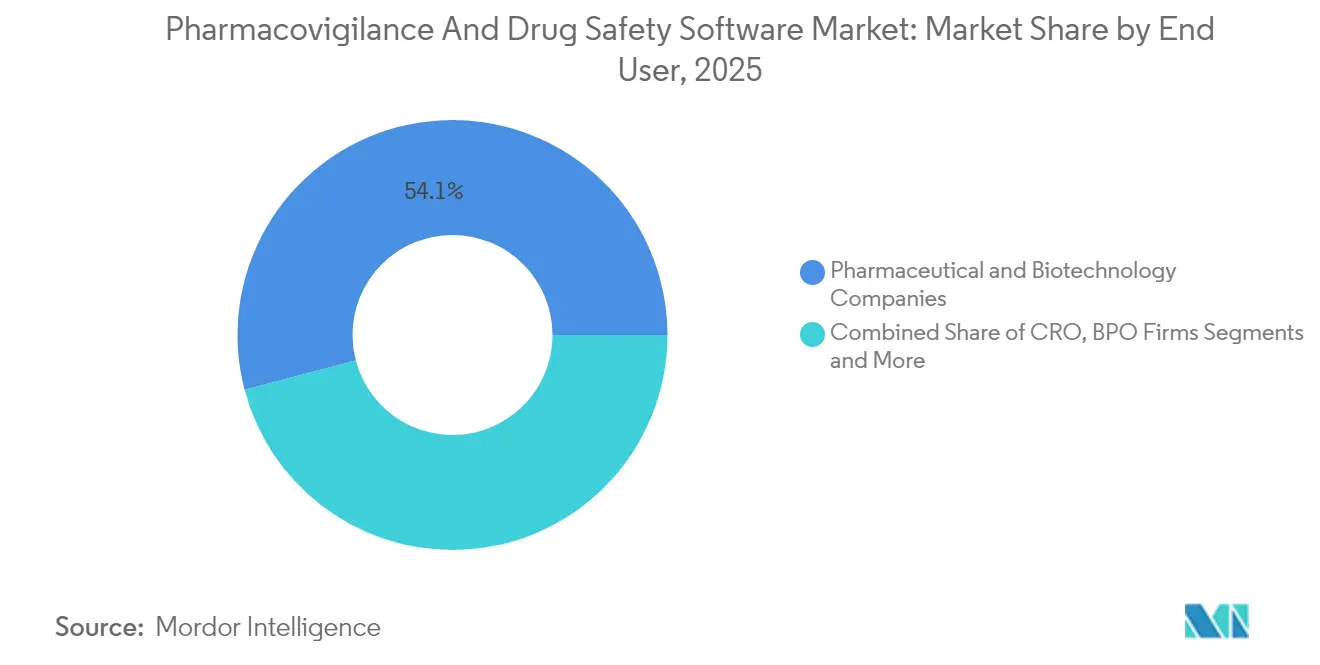

- By end user, pharmaceutical and biotechnology companies held 54.10% of the pharmacovigilance software market size in 2025, whereas business process outsourcing firms registered the fastest 17.2% CAGR.

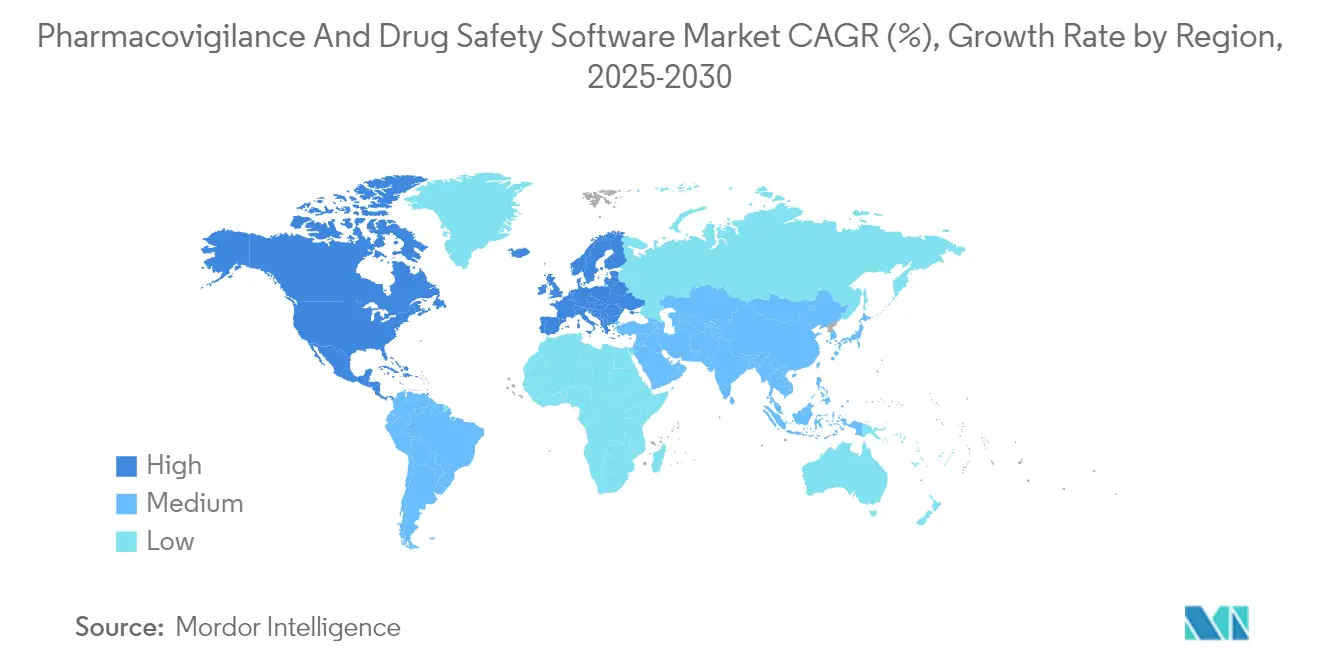

- By geography, North America commanded 35.55% revenue share in 2025; Asia Pacific is forecast to post a 13.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmacovigilance And Drug Safety Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Adverse Drug Reactions (ADRs) | +0.70% | Global, with higher impact in aging populations of North America & Europe | Medium term (2-4 years) |

| Stringent Global E2B(R3)/IDMP Compliance Deadlines | +1.10% | Global, with immediate impact in US & EU regulatory jurisdictions | Short term (≤ 2 years) |

| Cloud-First Migration Of Safety Databases | +0.90% | North America & EU leading, APAC following rapidly | Medium term (2-4 years) |

| Explainable-AI Modules Slash Case-Processing Costs | +0.50% | Developed markets initially, expanding to emerging markets | Long term (≥ 4 years) |

| Real-World-Evidence (RWE) Integration For Early Signals | +0.60% | North America & EU pioneering, APAC adoption accelerating | Medium term (2-4 years) |

| Low-Code Localisation For Emerging-Market Forms | +0.40% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Adverse Drug Reactions (ADRs)

Escalating ADR prevalence reshapes demand for advanced monitoring as new molecular entities enter wider use. Cureus Journal data show the 21-40 age group now reports the highest ADR frequencies, reflecting greater polypharmacy and increased hospital interactions. With the FDA approving 50 new molecular entities in 2024, sponsors must surveil diverse patient sub-populations for previously unseen safety signals.[2]Federal Register, “Emerging Drug Safety Technology Meetings; Establishment,” federalregister.gov Biologics and gene therapies add complexity because reactions can vary across genetic backgrounds. Accordingly, the pharmacovigilance software market shifts from static report repositories toward real-world evidence engines capable of analyzing heterogeneous longitudinal datasets. Vendors that embed AI-powered pattern recognition into reporting workflows gain relevance because manual methods cannot keep pace with volume and complexity.

Stringent Global E2B(R3)/IDMP Compliance Deadlines

April 2026 marks the FDA’s cut-off for E2B(R3) submissions, forcing sponsors to abandon legacy R2 formats and invest in upgraded platforms.[3]Food and Drug Administration, “Electronic Submission of Individual Case Safety Reports,” fda.gov Simultaneously, the European Medicines Agency’s IDMP roll-out tightens medicinal-product data requirements, compelling software to manage both event and product identifiers in one schema. Dual-system maintenance inflates risk and overhead, so firms accelerate migration ahead of statute. This regulatory synchrony turns spending on compliance upgrades into a certainty rather than a discretionary budget item, underpinning predictable growth for the pharmacovigilance software market.

Cloud-First Migration of Safety Databases

Eighty-three percent of pharmaceutical organizations now use cloud infrastructure for at least one critical workload, reflecting recognition that on-premises servers lack scalability for AI-heavy analytics. Pfizer’s AWS-backed case-processing engine and Moderna’s Google Cloud data lake show how cloud makes global collaboration routine while preserving audit trails. As GDPR and emerging digital-sovereignty laws push for local data residency, vendors respond with multi-region architectures that segment storage while unifying analytics layers. This hybrid evolution sustains double-digit growth for cloud sub-segments within the pharmacovigilance software market.

Explainable-AI Modules Slash Case-Processing Costs

Industry pilots confirm that machine learning trims expenses and accelerates throughput. IQVIA quantifies a 50% cost reduction from automated intake, with accuracy meeting or exceeding human benchmarks. TransPerfect Life Sciences reports 70% faster review times following AI-enabled triage. Regulatory openness is growing: the FDA’s Emerging Drug Safety Technology Meetings program lets sponsors pre-align AI validation plans with reviewers, shortening time to deployment. Explainability features that generate audit-ready reasoning logs quell historical concerns about “black-box” algorithms, unlocking broader uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Sovereignty & Cross-Border-Transfer Restrictions | -0.40% | EU leading with GDPR, expanding globally with digital sovereignty laws | Medium term (2-4 years) |

| Shortage Of PV Data-Science Talent | -0.30% | Global, with acute shortages in developed markets | Long term (≥ 4 years) |

| Algorithmic-Bias Scrutiny Delaying AI Approvals | -0.30% | North America & EU regulatory focus, expanding globally | Short term (≤ 2 years) |

| Escalating API Pricing From Dominant DB Vendors | -0.20% | Global, with higher impact on smaller pharmaceutical companies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty & Cross-Border-Transfer Restrictions

The European Health Data Space Regulation, effective May 2025, sets new standards for secondary health-data use and introduces consent layers that software must honor. GDPR already limits external processing, and similar frameworks are emerging in Asia and Latin America. Vendors must therefore design federated models that keep data in the country while sharing de-identified signals globally. This architecture raises costs and elongates deployment cycles, damping part of the pharmacovigilance software market’s expansion.

Shortage of PV Data-Science Talent

The industry needs an extra 5,000 professionals per year to execute AI-driven safety programs, yet few practitioners combine pharmacology, coding, and regulatory skills. Premium wages pull experts toward large multinationals, leaving small and mid-sized sponsors exposed. Automation helps, but AI still requires human oversight. Consequently, adoption of sophisticated modules may lag in organizations unable to recruit or retain specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: Predictive Analytics Surges Ahead

Adverse events reporting software retained a commanding 40.22% share of the pharmacovigilance software market in 2025, underscoring its status as a non-negotiable compliance pillar. Yet signal detection and risk-management modules are forecast to grow at an 17.5% CAGR, demonstrating the pivot toward preventive analytics that flag anomalies before regulators intervene. Many sponsors now favor unified platforms that merge intake, triage, analytics, and submission into one workflow. Oracle added AI-powered conditional touchless processing to Argus in 2024, illustrating how embedded intelligence elevates legacy solutions. Continuous rise in biological approvals coupled with diverse real-world data feeds widens the opportunity for platforms that draw correlations across ethnic, genomic, and social determinants of health datasets.

Integrated suites also reduce validation overhead because a single quality-management system covers multiple modules. As a result, vendors capable of harmonizing point solutions into end-to-end architecture are expanding their installed bases faster than niche competitors. Signal detection units may ultimately outpace event-reporting revenue, yet both modules remain symbiotic because regulatory filings still stem from source case data. The pharmacovigilance software market size attributable to advanced analytics is therefore set to climb more rapidly than the aggregate market, even as reporting retains foundational relevance.

By Mode of Delivery: Cloud-Native Platforms Set the Pace

Cloud deployments accounted for 66.55% of the pharmacovigilance software market in 2025 and are advancing at a 21.3% CAGR, accelerating digital transformation across sponsors of all sizes. Many firms embrace software-as-a-service because quarterly updates keep pace with shifting regulations without the downtime typical of on-premises patches. Hybrid models act as an interim bridge: sensitive identifiable data stay on local servers while anonymized datasets feed cloud-based AI models. Pfizer’s AWS architecture and Moderna’s Google Cloud approach validate the scalability and compliance of multi-tenant environments.

Security certifications such as ISO 27001 and SOC 2 have become table stakes for vendors, addressing lingering apprehension over confidential patient data. Nonetheless, data-sovereignty rules compel providers to offer regionally partitioned environments, adding complexity and incremental cost. As hyperscale cloud providers open additional life-science compliance zones in Europe and Asia, barriers recede, and the pharmacovigilance software market size under cloud deployment continues expanding at a rate far above on-premises installation.

By End User: Outsourcing Momentum Builds

Pharmaceutical and biotechnology firms controlled 54.10% of the pharmacovigilance software market in 2025 because they hold ultimate responsibility for product safety under global regulations. However, business-process outsourcing (BPO) providers are demonstrating a 17.2% CAGR as sponsors externalize case intake, triage, and submission. The strategy allows innovators to concentrate capital on core R&D while leveraging BPO scale for routine safety tasks. ProPharma Group’s acquisition of iSafety Systems in 2024 exemplifies how service providers extend reach to meet global sponsor demand.

Contract research organizations now incorporate post-marketing surveillance into traditional clinical-trial packages, offering end-to-end lifecycle support. This bundling increases appeal to biotechnology start-ups that lack in-house PV infrastructure. Medical-device manufacturers form a niche but growing cohort asthe convergence of drug and device vigilance rules boosts cross-sector platform demand. The pharmacovigilance software industry thus balances in-house stewardship with expanding managed-service ecosystems

Geography Analysis

North America led with 35.55% revenue share in 2025, anchored by stringent FDA oversight and a dense concentration of top 20 pharmaceutical companies. Many regional sponsors pioneered cloud-based safety systems before 2020; Pfizer's COVAES platform processed more than 1.5 million COVID-19 vaccine cases using automated triage and de-duplication. The FDA's 2025 creation of a chief AI officer underscores the regulator's readiness to evaluate algorithmic submissions, reinforcing regional appetite for AI-rich upgrades. Talent shortages remain a hurdle, inflating salaries for data-science specialists and pressuring smaller firms to outsource.

Asia Pacific records the fastest 13.9% CAGR on the back of clinical-trial migration to South Korea, Taiwan and Singapore, where shorter ethics-committee timelines accelerate recruitment. China's expanding contract research landscape, led by Wuxi AppTec, pulls in global clients that need local PV capacity aligned with National Medical Products Administration rules. Government investment programs, such as Japan's AMED grants for AI drug-safety research, further stimulate domestic software adoption. Despite diverse legal frameworks, many Asia-Pacific regulators now accept ICH E2B(R3) XML, reducing localization barriers.

Europe maintains significant scale because mature pharmacovigilance obligations and GDPR heightens the need for configurable, audit-ready platforms. The European Health Data Space Regulation formalizes secondary health-data use, prompting sponsors to adopt software capable of granular consent management. Germany's new Digital Act unlocks de-identified claims datasets for research, enabling safety algorithms to mine national repositories once off-limits. However, strict data-sovereignty clauses require EU-based hosting, spurring demand for region-specific cloud zones. Collectively, these dynamics keep Europe a premium market for feature-rich platforms even though growth trails Asia Pacific.

Competitive Landscape

The pharmacovigilance software market exhibits moderate concentration, with platform vendors favoring breadth of functionality and deep integration over discount pricing. Oracle, ArisGlobal, and Veeva Systems defend incumbency through continuous feature expansion. Oracle’s July 2024 Argus upgrade added conditional touchless processing that pushes automation rates toward 80%. ArisGlobal reported record new-logo growth in 2024 and widened its partnership with Sitero to span clinical and regulatory domains. Veeva, historically strong in quality and content, unveiled a unified safety suite with NLP support in April 2025.

Emerging challengers target specific pain points, such as literature mining, machine translation, or duplicate detection. Their specialized offerings integrate via open APIs into larger ecosystems, forcing majors to maintain aggressive R&D roadmaps. The FDA’s Emerging Drug Safety Technology Meetings program levels the playing field by giving smaller firms a formal pathway to validate novel AI models.

M&A continues as scale becomes a prerequisite for global regulatory support. Valsoft’s August 2024 purchase of Anju Software afforded the acquirer an immediate PV footprint, illustrating how consolidators seek synergies between life-science verticals. Meanwhile, service providers such as PrimeVigilance rebrand and reposition to capture outsourced processing demand, creating adjacent competition for pure software vendors. These dynamics keep pricing power balanced, with differentiation residing in automation depth, compliance agility and ecosystem partnerships.

Pharmacovigilance And Drug Safety Software Industry Leaders

Ennov Solutions Inc.

Extedo GmbH

United BioSource Corporation

Ab Cube

ArisGlobal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Veeva Systems announced AI enhancements across its pharmacovigilance platform portfolio, adding machine-learning-based adverse-event detection and NLP for regulatory document analysis.

- January 2025: Veeva Systems partnered with Zifo to accelerate quality-control modernization, integrating analytics with pharmacovigilance workflows.

- September 2024: ArisGlobal expanded its partnership with Sitero to deliver an integrated technology suite covering clinical and safety domains.

- September 2024: Veeva Systems introduced field-action and recall management capabilities in Vault QMS, extending into post-market surveillance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the pharmacovigilance and drug-safety software market as the global revenue generated from purpose-built platforms that capture, manage, and analyze adverse-event data across the product life-cycle, including compliance reporting modules and signal-detection dashboards. We tally license, subscription, and maintenance fees attributed to the software itself; ancillary services and broader safety outsourcing contracts stay outside this value.

Scope exclusion: Stand-alone call-center services, manual case-processing BPO contracts, and generic clinical trial EDC systems are not counted.

Segmentation Overview

- By Functionality

- Adverse Event Reporting Software

- Drug Safety Audit Software

- Issue Tracking Software

- Fully Integrated Safety Suites

- Signal Detection & Risk-Management Tools

- By Mode of Delivery

- On-premise

- Cloud / SaaS

- Hybrid Deployment

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Business-Process-Outsourcing (BPO) Firms

- Medical-Device Manufacturers

- Other PV Service Providers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed pharmacovigilance directors at pharmaceutical majors, CRO safety heads across North America, Europe, and Asia, and SaaS product managers. These discussions clarified live price bands, deployment mix shifts toward cloud, and regional regulatory pain points, plugging data gaps from desk work and validating preliminary ratios.

Desk Research

We began with public regulatory datasets, FDA FAERS download files, EMA EudraVigilance statistics, PMDA annual ADR digests, and WHO-UMC VigiBase summaries, to size the universe of reportable safety cases. Trade-association white papers from DIA and ISoP, academic journals such as Drug Safety, and IPO filings of key platform vendors then helped benchmark average software spend per processed case. We also leveraged Dow Jones Factiva for deal values and D&B Hoovers for vendor revenue splits. The sources cited illustrate, not exhaust, the secondary evidence pool that underpins our model.

A follow-up literature scan covered regional cloud adoption rates, patent filings from Questel signaling product innovation, and North America ICD-10 coding volume to capture growing real-world data feeds. These findings informed variable selection and boundary checks.

Market-Sizing & Forecasting

We reconstruct 2025 market value with a top-down "case-load x software spend" build, anchored to regulator-reported ADR volumes and adjusted for under-reporting. Select bottom-up roll-ups of leading vendor revenues tested and fine-tuned totals. Key drivers tracked include annual ADR case filings, proportion of cases processed with automated tools, average subscription price per seat, cloud migration pace, and emerging AI feature premiums. Forecasts to 2030 employ an ARIMA model blended with multivariate regression on those drivers, with scenario tweaks vetted by interviewees. Where vendor disclosures lacked regional splits, shares were prorated using import-export data and capacity notes from Volza.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance checks against historic growth corridors, and outlier resolution calls. Our numbers refresh each year, while material events, major regulation or a top-five vendor merger, trigger interim recalibration, ensuring clients always receive a current baseline.

Why Our Pharmacovigilance And Drug Safety Software Baseline Is Dependable

Published estimates frequently diverge because firms choose different inclusion rules, drivers, and refresh rhythms. By aligning scope strictly to software revenue tied to ADR management and by cross-checking both regulatory statistics and vendor books, Mordor delivers a balanced anchor for planning.

Key gap drivers versus other publishers include their mixing of service outsourcing, choice of older base years, limited geography coverage, or single-source invoice surveys without regulator triangulation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 222.18 million (2025) | Mordor Intelligence | |

| USD 2.09 billion (2025) | Global Consultancy A | Adds safety BPO revenue, bundled compliance services, and applies unverified FX conversions |

| USD 171.7 million (2022) | Industry Journal B | Uses earlier base year, omits cloud modules, straight-line CAGR without recent ADR surge checks |

| USD 198.15 million (2023) | Global Consultancy C | Relies on supplier invoice survey, narrow regional scope, no reconciliation with regulator case volumes |

These contrasts show that Mordor's disciplined variable selection and annual refresh cadence yield a transparent, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the pharmacovigilance software market?

The market stands at USD 234.73 million in 2026 and is projected to reach USD 309.03 million by 2031.

How fast is the pharmacovigilance software market expected to grow?

It is forecast to expand at a 5.65% CAGR over 2026-2031.

Which functionality segment holds the largest share?

Adverse event reporting software led with 40.22% revenue share in 2025.

What deployment model is growing the quickest?

Cloud and SaaS deployments are advancing at a 21.3% CAGR and already represent 66.55% of market revenue.

Which region is expanding the fastest?

Asia Pacific is forecast to register a 13.9% CAGR through 2031, benefiting from the eastward shift of clinical trials.

Page last updated on: