Medical Terminology Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

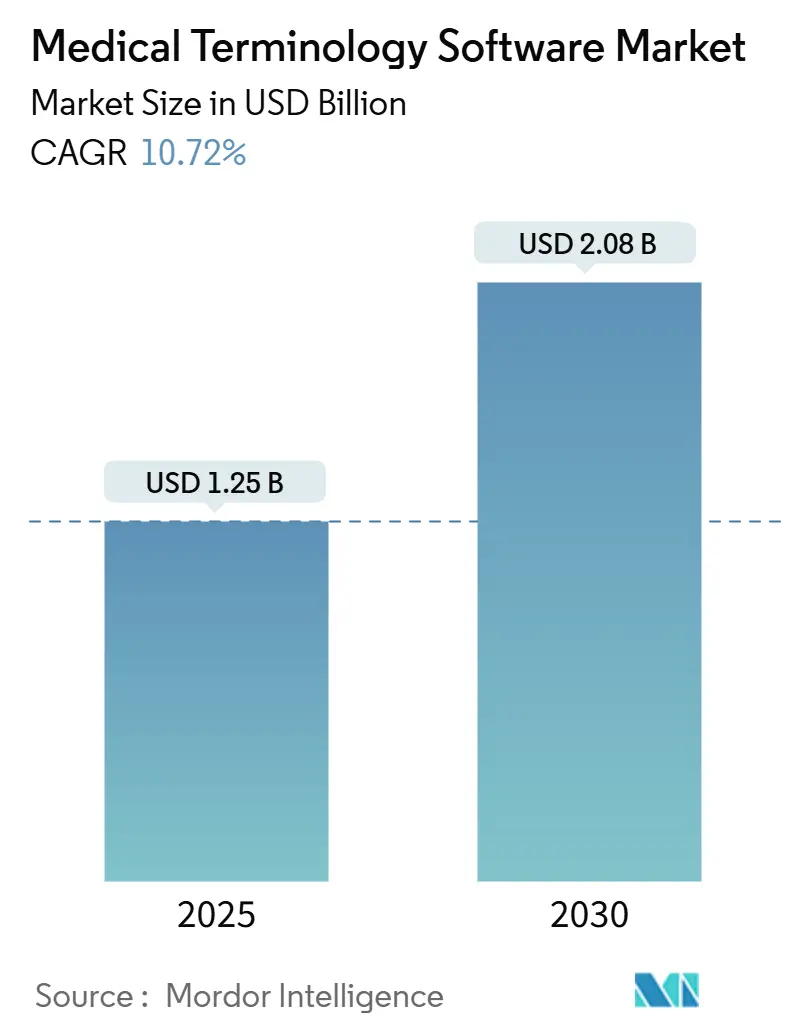

| Market Size (2025) | USD 1.25 Billion |

| Market Size (2030) | USD 2.08 Billion |

| Growth Rate (2025 - 2030) | 10.72% CAGR |

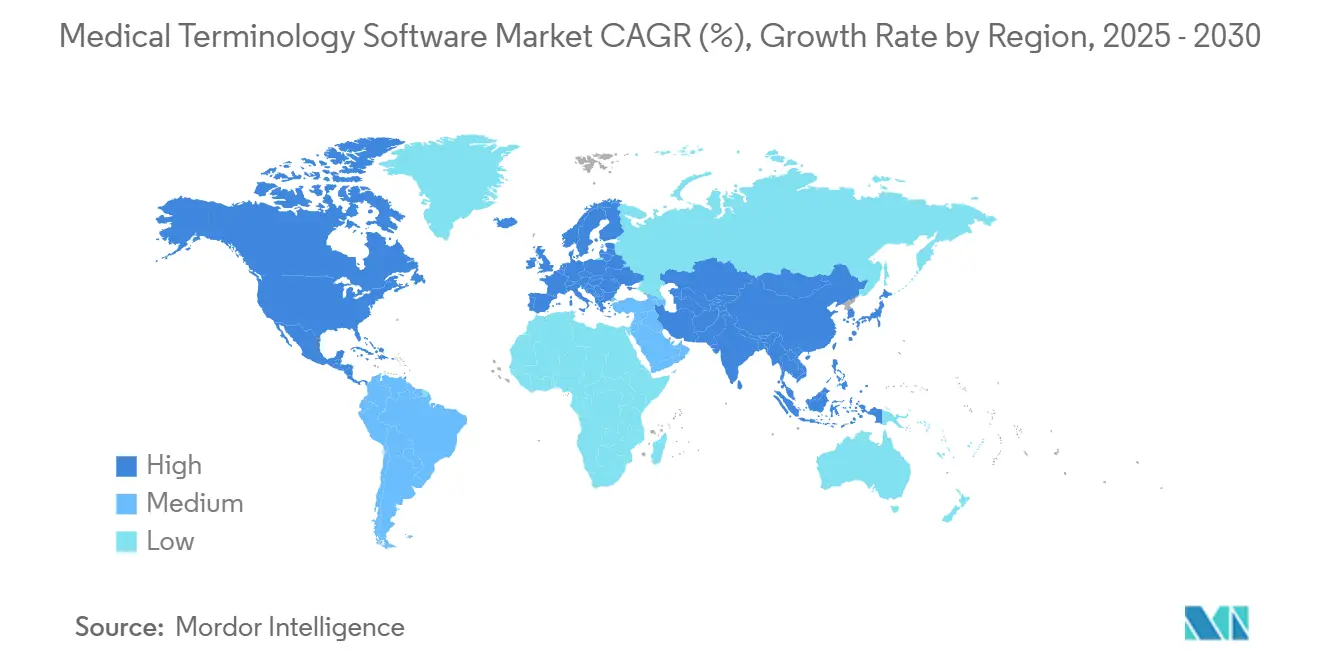

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Terminology Software Market Analysis by Mordor Intelligence

The Medical Terminology Software Market size is estimated at USD 1.25 billion in 2025, and is expected to reach USD 2.08 billion by 2030, at a CAGR of 10.72% during the forecast period (2025-2030).

The upward trajectory reflects the increasing regulatory pressure for interoperability, the surge in AI-enabled clinical decision support, and the healthcare sector’s shift toward value-based payment models. Stricter certification rules under the ONC HTI-1 framework, combined with financial incentives in the United States and Europe, are pushing hospitals to upgrade legacy HL7 V2 interfaces to FHIR-native, cloud-based terminology servers. Vendors that embed automated mapping, validation, and update services directly into electronic health record (EHR) workflows are capturing demand from organizations seeking to reduce documentation errors and accelerate quality reporting. North America continues to anchor global revenue given its mature EHR footprint, while Asia-Pacific’s public-sector digitization programs are expanding the potential user base for the medical terminology software market.

Key Report Takeaways

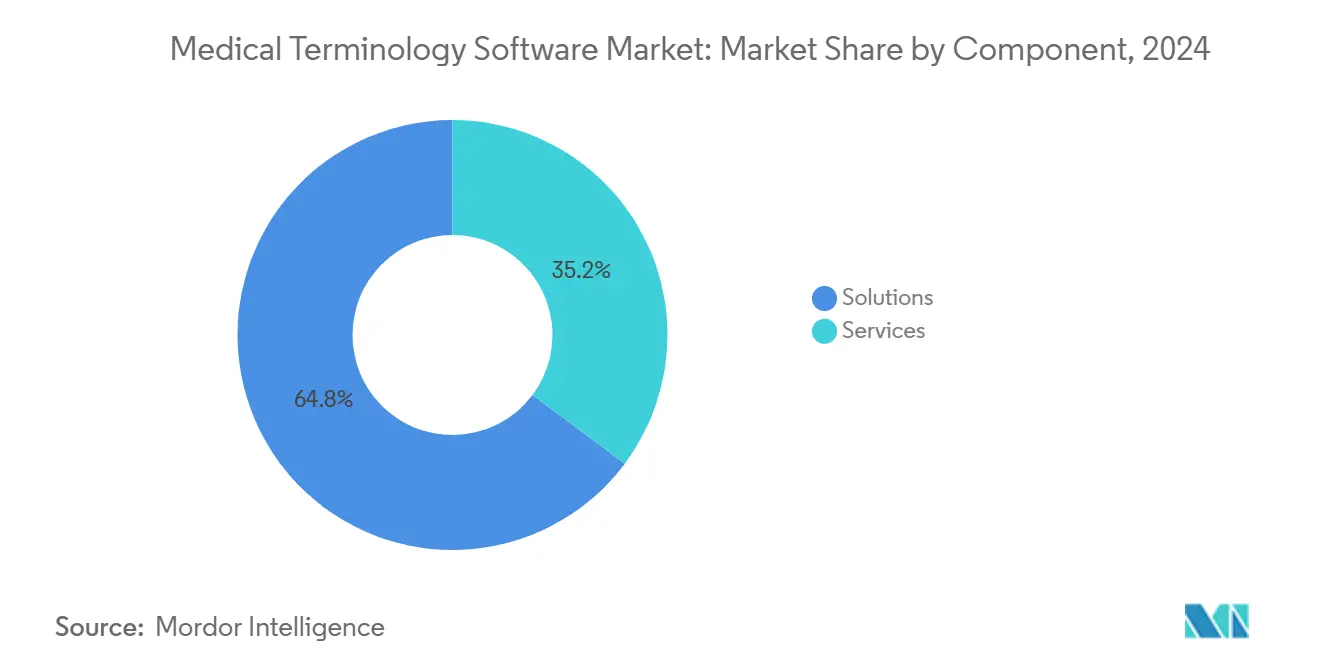

- By component, Solutions accounted for 64.78% of the medical terminology software market share in 2024; Services are forecast to expand at a 12.15% CAGR through 2030.

- By application, Quality & Outcomes Reporting led with a 23.01% revenue share in 2024; Clinical Trials & RWE is projected to grow at an 11.89% CAGR up to 2030.

- By deployment mode, Cloud-Based platforms captured 66.46% share of the medical terminology software market size in 2024 and will advance at an 11.23% CAGR to 2030.

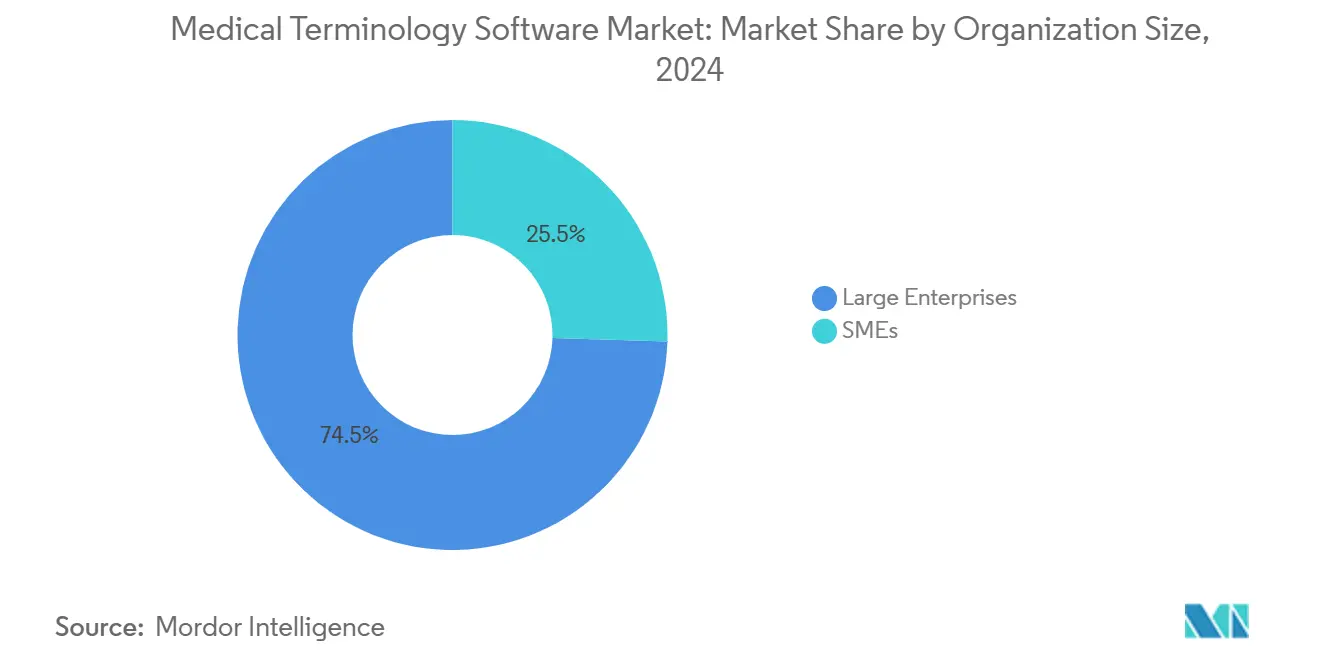

- By organization size, large enterprises retained 74.52% of the medical terminology software market in 2024, while SMEs posted the highest 11.74% CAGR.

- By end-user, healthcare providers controlled 63.39% of the medical terminology software market size in 2024, with both providers and payers growing by nearly 11.06% annually.

- By geography, North America held 40.35% of revenue in 2024; Asia-Pacific is the fastest-growing region, with a 12.05% CAGR through 2030.

Global Medical Terminology Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives & Mandates for HCIT Adoption | +2.8% | North America & EU primary, APAC emerging | Short term (≤ 2 years) |

| Need for Seamless Data Aggregation to Enable Value-Based Care Models | +2.3% | North America primary, EU secondary | Medium term (2-4 years) |

| Rising Focus on Minimizing Medical Errors | +2.1% | Global, with highest impact in North America & EU | Medium term (2-4 years) |

| ONC/EMA Interoperability Mandates & Evolving FHIR Standards | +1.9% | North America & EU | Short term (≤ 2 years) |

| Rise of RWE & AI Analytics Demanding High-Fidelity Terminologies | +1.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Monetization of Cloud-Native FHIR Terminology Servers | +1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives & Mandates for HCIT Adoption

Federal programs are accelerating purchases as providers must meet ONC HIT-1 requirements to maintain Medicare reimbursements. The rule compels migration to USCDI v3 by 2026 and USCDI v4 by 2028[1]Health and Human Services Department, “Health Data, Technology, and Interoperability: Trusted Exchange Framework and Common Agreement (TEFCA),” federalregister.gov, while the Trusted Exchange Framework and Common Agreement (TEFCA) sets uniform data-sharing terms. Hospitals unable to demonstrate semantic interoperability risk payment adjustments[2]Centers for Medicare & Medicaid Services, “Calendar Year 2024 Program Requirements,” cms.gov exceeding 4% of Medicare revenue. EU member states are imposing parallel mandates through the European Health Data Space, stimulating early procurement cycles across Germany, France, and the Nordics. The combined policy push lifts near-term demand for cloud-ready terminology servers that can validate data against national value sets and automatically create audit logs for regulators.

Need for Seamless Data Aggregation to Enable Value-Based Care Models

More than 40% of US payments now flow through risk-bearing contracts that demand precise hierarchical condition category capture and near real-time quality reporting. Providers are layering terminology engines on top of data lakes to normalize disparate codes and feed analytics tools, producing risk-adjusted cost metrics. An interoperability partnership between Innovaccer and Wolters Kluwer’s Health Language Platform estimates USD 1.5 billion in savings across 54 million lives by eliminating coding gaps that previously distorted risk scores. Payers are increasingly embedding terminology conformance into contracts, making software compliance a table stake for shared-savings eligibility. As FHIR-based electronic clinical quality measures mature, structured terminology validation becomes foundational for population-health dashboards.

Rising Focus on Minimizing Medical Errors

The US healthcare system loses an estimated USD 122 billion each year[3]Health Information and Management Systems Society, “AI-Driven Deep Learning Model for Medical Coding,” himss.org to preventable mistakes, with miscoded diagnoses and procedures driving denials and patient harm incidents. Hospitals that integrated real-time terminology validation into their EHR workflows recorded documentation error reductions of up to 25% within the first year, materially improving patient safety benchmarks. AI-assisted clinical decision support linked to curated vocabularies further reduces alert fatigue by suppressing irrelevant prompts and surfacing evidence-based suggestions that physicians can accept with a single click. Vendor case studies demonstrate how ambient documentation modules, paired with robust terminology engines, capture structured data directly from clinician-patient conversations, thereby increasing note completeness while reducing after-hours charting.

ONC/EMA Interoperability Mandates & Evolving FHIR Standards

Enforcement penalties of up to USD 1 million per information-blocking infraction are motivating provider organizations to deploy FHIR-native terminology endpoints[4]Office of the National Coordinator for Health Information Technology, “Health Data, Technology, and Interoperability Certification Program,” healthit.gov that satisfy both domestic and cross-border data-request obligations. The finalization of TEFCA in 2025 establishes a nationwide framework where query-on-demand exchanges must return records in standardized, coded formats. Parallel EU legislation on Identification of Medicinal Products (IDMP) compels life-science firms to adopt standard drug terminologies, increasing demand for specialized mappings that synchronize EHR, pharmacy, and regulatory systems. Vendors that provide dual-standard migration tools are well-positioned to win contracts as hospitals decommission HL7 V2 feeds, while still requiring backward compatibility during multi-year transitions.

IT-Infrastructure Constraints in Developing Regions

Bandwidth shortfalls, limited cloud availability zones, and a scarcity of informatics professionals impede widespread deployment in lower-middle-income countries. Healthcare IT budgets typically represent less than 2% of overall healthcare spending, compared with more than 4% in developed markets, which restricts funds for advanced terminology engines. To overcome the shortfall, public-private initiatives under programs such as India’s Ayushman Bharat Digital Mission subsidize secure hosting and shared terminology repositories. While these measures improve access, full impact will unfold over a longer horizon given the need for workforce training and stable connectivity.

Persistent Semantic Interoperability Gaps Between Legacy Systems

Nearly all US hospitals still exchange a sizable portion of messages via HL7 V2, forcing complex dual-stack environments during FHIR migrations. Large health systems allocate months to map thousands of custom vocabularies that have been built over decades. Integration projects can cost multi-millions of dollars, presenting a capital hurdle even when regulations push for modernization. Automated mapping accelerators and cloud-based validation APIs can reduce timelines. Still, they do not eliminate the need for staged testing, primarily when mission-critical decision support logic depends on exact code matches across downstream systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Dominate Through Platform Integration

Solutions claimed 64.78% of the medical terminology software market share in 2024 by bundling comprehensive mapping engines, vocabulary management dashboards, and automated update pipelines into unified platforms. The ability to integrate directly inside leading EHRs eliminates redundant interfaces, speeds clinician adoption, and satisfies ONC certification requirements in a single procurement cycle. Subscription license models, combined with high renewal rates, drive predictable revenue and encourage venture and private-equity backing for consolidators.

Services, growing at a 12.15% CAGR, address the continuous need for consulting, migration, and training as organizations upgrade to cloud-native infrastructure. Demand rises when providers move historical code sets and quality-measure logic from on-premise databases to managed FHIR stores. Vendors that package services with outcome-based milestones secure multi-year contracts, stabilizing cash flow while ensuring client success.

By Application: Quality Reporting Leads, RWE Analytics Accelerates

Quality & Outcomes Reporting held 23.01% of the medical terminology software market share in 2024 because CMS mandates tie Medicare reimbursement to accurate eCQM submissions each program year. Automated extraction of SNOMED CT, LOINC, and ICD-10 codes across inpatient and ambulatory encounters shortens submission cycles and lowers audit risk. The Medical Terminology Software market size allocated to Clinical Trials & RWE applications is projected to grow faster at an 11.89% CAGR as pharmaceutical sponsors reuse routine-care data for evidence packages.

Real-world evidence requires high-fidelity mappings to unify clinical, pharmacy, and device data, thereby satisfying regulatory traceability checks. Vendors that can align terminologies across longitudinal datasets gain an edge as life-science clients deploy decentralized trial models and pharmacovigilance analytics.

By Deployment Mode: Cloud Migration Accelerates Digital Transformation

Cloud-based platforms captured a 66.46% share of the medical terminology software market size in 2024 and remain the fastest-growing segment at a 11.23% CAGR. Hospitals are gravitating toward managed FHIR terminology endpoints that deliver 99.9% uptime, elastic scaling, and auto-refresh for new code releases, thereby removing the dependence on local IT for patching.

On-premise installations persist within integrated delivery networks that invested heavily in private data centers and maintain strict data-residency policies. Many adopt hybrid models, holding patient identifiers locally while calling cloud APIs for validation and translation. Over time, recurring OPEX savings and reduced hardware refresh cycles are expected to persuade even conservative buyers to adopt full SaaS.

By Organization Size: SMEs Embrace Cloud-Native Solutions

Large Enterprises, with a 74.52% market share in the medical terminology software market in 2024, purchase premium offerings that include configurable governance workflows, dual-language dictionaries, and advanced analytics for coding risk. Multi-hospital systems integrate terminology modules with revenue-cycle software to capture missed charges and monitor denial trends.

SMEs, posting the highest 11.74% CAGR, exploit pay-as-you-go SaaS tiers that require only a browser and RESTful API keys. The absence of capital expenditure and automatic updates allows small ambulatory groups to satisfy the Promoting Interoperability criteria without hiring full-time terminologists. Vendors target this cohort with starter bundles that cover common quality measures and standard value sets, expecting an upsell to broader vocabularies as regulatory complexity grows.

By End-User: Providers and Payers Converge on Interoperability

Healthcare Providers accounted for 63.39% of the Medical terminology software market size in 2024, reflecting their central role in data generation and regulatory reporting. Providers embed terminology engines within computer-assisted physician documentation tools to normalize free text in real-time. Payers closely follow as they automate prior authorization, risk adjustment, and fraud detection—each activity relying on precise code mapping.

The mutual dependence on standardized vocabularies is tightening integration between provider and payer systems. As FHIR Authorization Prior-Auth 2.0 pilots progress, both sides require synchronized terminologies to prevent mismatch denials and accelerate decision turnaround. The trend opens cross-selling prospects for vendors offering unified terminology management across clinical, financial, and administrative domains.

Geography Analysis

North America generated 40.35% of global revenue in 2024, driven by robust EHR adoption and clear financial penalties for non-compliance with information-blocking rules. The regional CAGR of 10.28% through 2030 stems from replacement demand as health systems transition from bespoke, on-premise dictionaries to cloud platforms that continuously align with USCDI updates. Canadian provinces are adopting comparable mandates, while Mexico’s public health networks are piloting FHIR-based exchanges, broadening addressable spend.

Europe holds the second position with a 10.67% CAGR, underwritten by the European Health Data Space regulation, which obliges cross-border providers to supply coded records to any EU citizen within hours of a request. The Medical terminology software market benefits from SNOMED International’s headquarters in London and the broad availability of open-source reference sets. However, GDPR introduces strict residency requirements that boost demand for local cloud zones. The implementation of IDMP drug identification rules creates a sizable niche within life-science workflows, prompting pharmaceutical clients to extend contracts for continuous dictionary maintenance.

The Asia-Pacific region records the fastest 12.05% CAGR, thanks to state-sponsored digitization drives in India, China, and emerging ASEAN economies. India’s national health stack integration plan requires multilingual code libraries to support more than 20 officially recognized languages, enlarging the scope for specialty vendors. Still, patchy broadband limits rural roll-outs, and varied privacy regimes compel market participants to tailor hosting strategies per jurisdiction. The Middle East & Africa, as well as South America, show parallel paths: governments fund new hospitals and national exchanges, yet workforce skills and capital drive the pace of complete cloud migration outlays. Vendors position themselves through channel partnerships with regional system integrators, aiming to capture an early share and scale as the infrastructure catches up.

Competitive Landscape

The Medical terminology software market displays moderate concentration with accelerating merger activity. Thomas H. Lee Partners’ 2024 buyout of Intelligent Medical Objects signaled private equity appetite for sticky subscription revenue tied to regulatory timeframes. InterSystems, Wolters Kluwer, and Oracle Health invest heavily in AI labs to infuse automated mapping and predictive maintenance into terminology products, building moats around data-quality IP.

Cloud hyperscalers deepen footholds through marketplace alliances; Amazon selected Clinical Architecture as a HealthLake partner for FHIR data normalization utilities, funneling enterprise traffic toward curated vocabularies embedded in AWS services. European vendors leverage GDPR-aligned hosting footprints to retain public-sector contracts as US competitors navigate cross-border transfer hurdles.

Competitive differentiation now centers on the speed and transparency of terminology updates. Providers insist new SNOMED CT releases propagate across environments within days, not weeks, to keep quality scores accurate. Vendors offering visual lineage tracking and rollback capabilities secure renewals by lowering audit risk. AI-powered ambient documentation has emerged as an adjacent battleground; companies that bundle terminology services with automated note generation create end-to-end value propositions difficult for point players to match.

The vendor landscape also witnesses specialization around life-science compliance. Firms with mature IDMP content and multilingual thesauri win contracts from global pharmaceutical companies seeking unified submissions across jurisdictions. Open-source community contributions continue, yet enterprise buyers gravitate to commercial distributions that wrap reference sets with indemnification, monitoring, and 24/7 support.

Medical Terminology Software Industry Leaders

Clinical Architecture, LLC

Intelligent Medical Objects, Inc.

InterSystems Corporation

Solventum Corporation

Wolters Kluwer N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ambience Healthcare unveiled an OpenAI-powered coding engine that raised coding accuracy by 27% across pilot sites and plans to expand to the Cleveland Clinic and UCSF Health in the summer of 2025.

- April 2025: Centauri Health Solutions acquired MedAllies to enhance secure messaging and patient record location capabilities.

- March 2025: InterSystems launched IntelliCare, an AI-enabled EHR with real-time encounter-note generation, at HIMSS25.

Global Medical Terminology Software Market Report Scope

As per the scope of the report, the language used to describe human body parts, medical operations, illnesses, disorders, and pharmaceuticals is known as medical terminology. The medical terminology software simplifies patient documentation and facilitates the capture of clinical information, such as reducing paperwork, tracking patient activity, and standalone software used for diagnostic or therapeutic purposes, as well as software embedded in medical devices. The medical terminology software market is segmented by Application (Data Aggregation, Reimbursement, Public Health Surveillance, Data Integration, Decision Support, Clinical Trials, Quality Reporting and Clinical Guidelines), Product & Service (Services and Platforms), End-User (Healthcare Providers, Healthcare Payers, and Healthcare IT Vendors), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Solutions | |

| Services | Consulting & Planning |

| Implementation & Training | |

| Maintenance |

| Data Aggregation |

| Reimbursement & Revenue Integrity |

| Clinical Decision Support |

| Clinical Trials & RWE |

| Quality & Outcomes Reporting |

| Other Applications |

| Cloud-Based |

| On-Premise |

| Large Enterprises |

| SMEs |

| Healthcare Providers |

| Healthcare Payers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Solutions | |

| Services | Consulting & Planning | |

| Implementation & Training | ||

| Maintenance | ||

| By Application | Data Aggregation | |

| Reimbursement & Revenue Integrity | ||

| Clinical Decision Support | ||

| Clinical Trials & RWE | ||

| Quality & Outcomes Reporting | ||

| Other Applications | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By End-User | Healthcare Providers | |

| Healthcare Payers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How are recent interoperability rules reshaping demand for medical terminology software?

New certification and information-sharing requirements compel healthcare organizations to upgrade legacy systems, so buyers now view advanced terminology engines as essential compliance tools rather than optional add-ons.

What role does artificial intelligence play in the next generation of medical terminology solutions?

AI accelerates code mapping, automates real-time validation, and powers ambient documentation, allowing clinicians to capture structured data with less manual effort while improving coding precision.

Why are cloud-native terminology servers gaining preference over on-premise deployments?

Managed SaaS platforms deliver instant vocabulary updates, high availability, and seamless API connectivity, reducing internal IT overhead and supporting modern FHIR-based data exchanges.

How is vendor consolidation affecting competitive dynamics in this market?

Strategic acquisitions are clustering specialized capabilities under larger platforms, enabling end-to-end offerings but also opening niches for innovators focused on life-science compliance or multilingual support.

What barriers inhibit adoption of medical terminology software in developing regions?

Limited broadband, scarce informatics talent, and fragmented regulatory frameworks slow large-scale rollouts, although public-private digitization initiatives are beginning to bridge these gaps.

How are payers and providers collaborating around terminology standards?

Shared needs for accurate risk adjustment, prior authorization automation, and quality reporting are prompting joint investments in unified terminology services that streamline data exchange across the care continuum.

Page last updated on: