Clinical Documentation Improvement Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

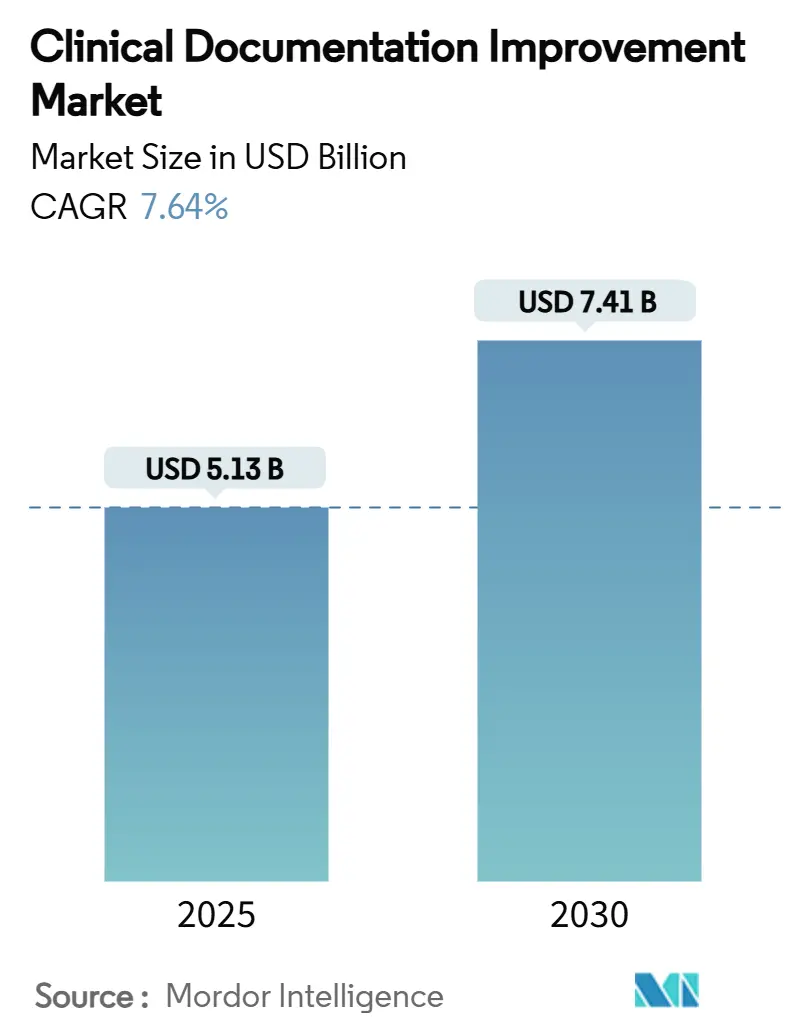

| Market Size (2025) | USD 5.13 Billion |

| Market Size (2030) | USD 7.41 Billion |

| Growth Rate (2025 - 2030) | 7.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Documentation Improvement Market Analysis by Mordor Intelligence

The Clinical Documentation Improvement market size reached USD 5.13 billion in 2025 and is projected to rise to USD 7.41 billion by 2030, advancing at a 7.64% CAGR. This growth reflects the sector’s pivot toward value-based reimbursement, the transition to ICD-11, and the rapid adoption of ambient artificial-intelligence scribes that ease physicians’ documentation load. Hospitals are increasing CDI investments to reduce claim denials and secure performance bonuses, while cloud deployments gain favor for their scalability and remote-access benefits. Meanwhile, post-acute and outpatient settings are becoming pivotal growth arenas as new payment models tighten documentation standards. Competitive dynamics remain moderate, with established health-IT vendors pursuing AI acquisitions to deliver unified CDI platforms.

Key Report Takeaways

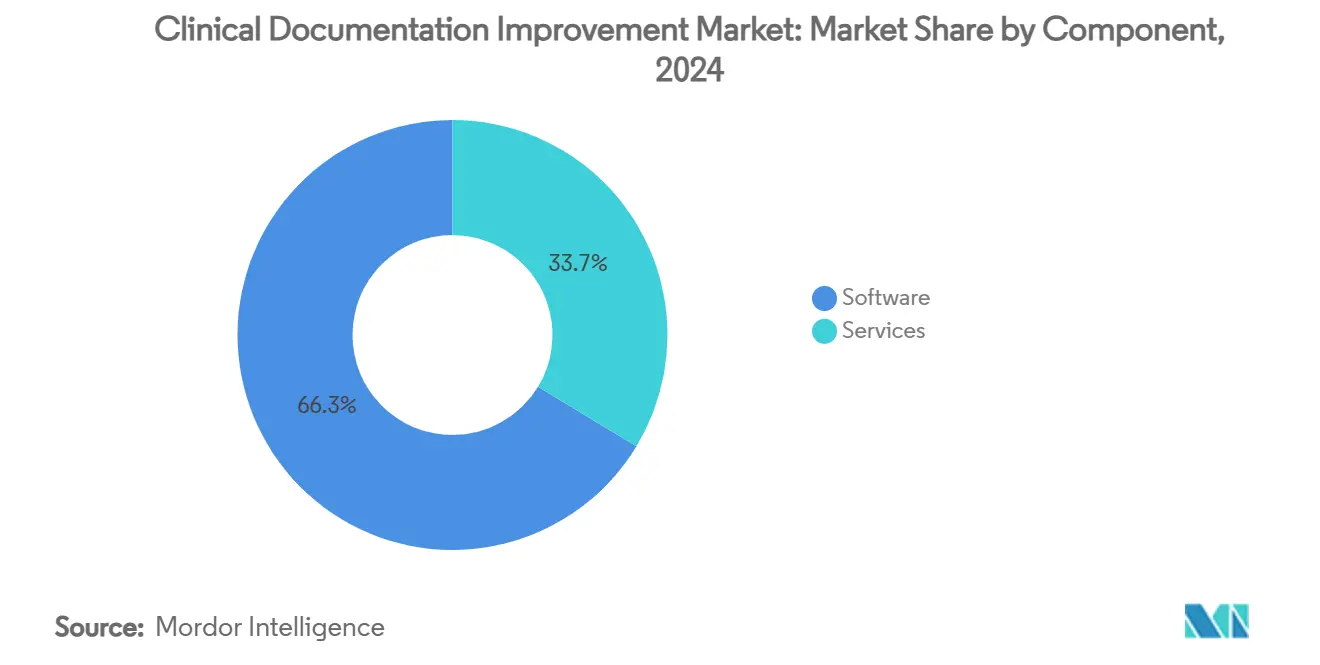

- By component, software commanded 66.34% revenue share in 2024 while services recorded the fastest 11.23% CAGR to 2030.

- By deployment mode, cloud solutions captured 54.56% of the Clinical Documentation Improvement market share in 2024 and are expanding at an 11.55% CAGR through 2030.

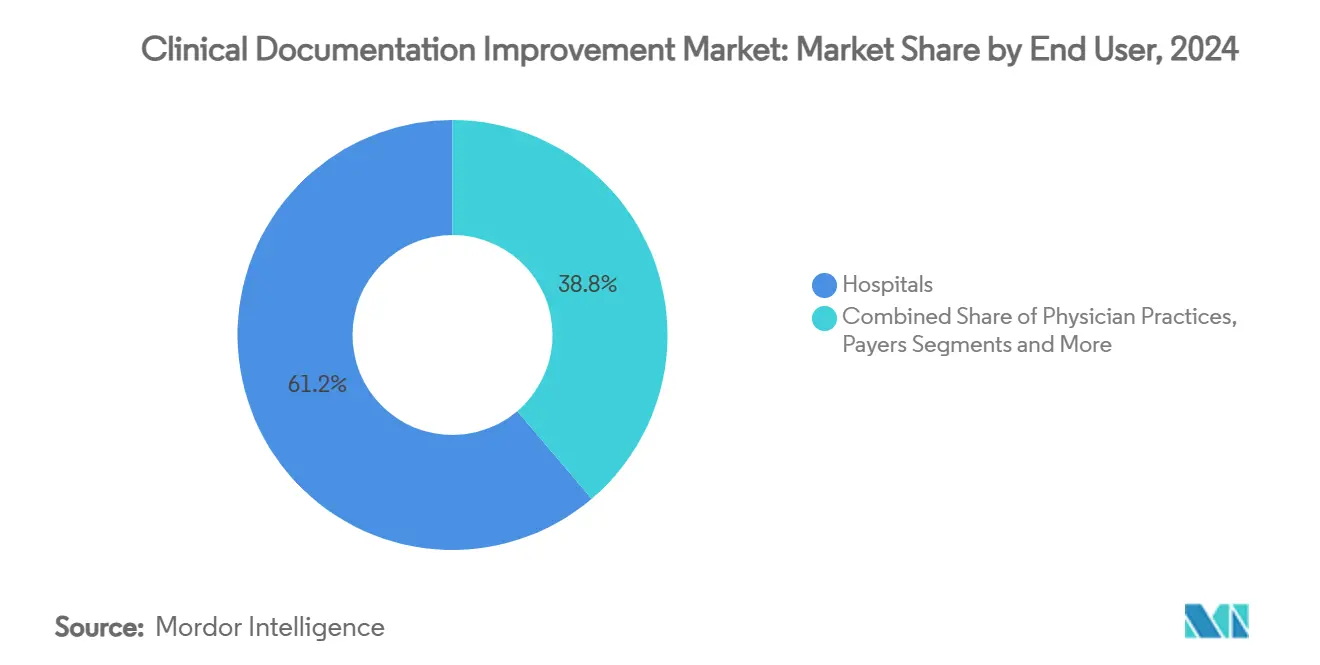

- By end user, post-acute and long-term care facilities achieved the highest 10.67% CAGR, whereas hospitals retained 61.22% revenue share in 2024.

- By application setting, inpatient programs held 62.34% of the Clinical Documentation Improvement market size in 2024, while outpatient CDI is forecast to climb at a 9.46% CAGR.

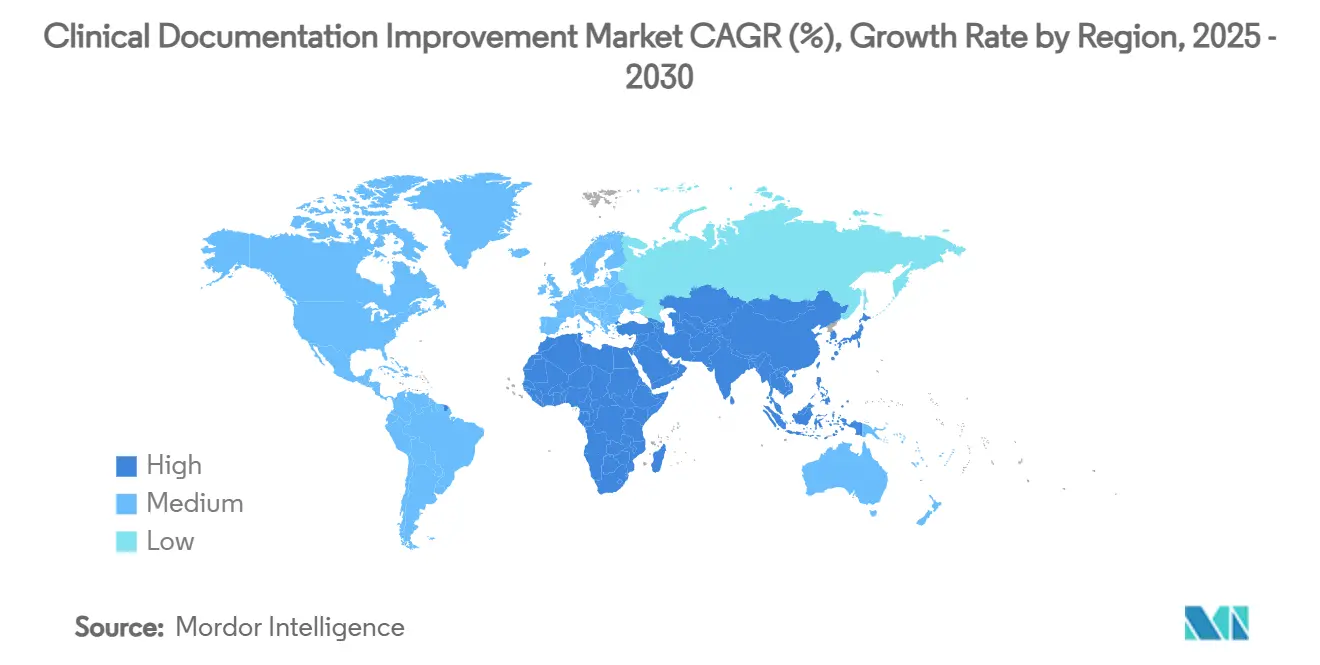

- By geography, North America led with 41.63% revenue share in 2024, whereas Asia-Pacific is advancing at a 9.33% CAGR to 2030.

Global Clinical Documentation Improvement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EHR proliferation & mandatory quality-based reimbursement | +1.8% | Global; strongest in North America & EU | Medium term (2-4 years) |

| Shift from fee-for-service to value-based care models | +1.5% | North America core; expanding to APAC & Europe | Long term (≥ 4 years) |

| ICD-11 transition accelerating documentation specificity | +1.2% | Global; phased by region | Short term (≤ 2 years) |

| Expansion of outpatient CDI programs | +1.0% | North America & Europe; emerging in APAC | Medium term (2-4 years) |

| Ambient AI scribes reducing clinician burnout | +0.9% | Global; early adoption in developed markets | Short term (≤ 2 years) |

| Hospital-at-home programs needing remote CDI workflows | +0.6% | North America & Europe; pilots in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EHR Proliferation & Mandatory Quality-Based Reimbursement

Saturation-level EHR adoption now coincides with quality-linked payment measures such as the 2025 Medicare Physician Fee Schedule, which ties reimbursement to documentation precision.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2025 Medicare Physician Fee Schedule Proposed Rule,” cms.gov Health systems that historically relied on volume now see revenue gains of up to 3% when CDI tools flag gaps inside the EHR workflow. Vendors respond by embedding AI-powered prompts at the point of care, easing clinician effort while satisfying rising regulator scrutiny. The result is a reinforcing loop: better tooling increases compliance, which in turn stimulates further CDI investment.

Shift From Fee-For-Service To Value-Based Care Models

CMS aims to place all Medicare lives in value-based contracts by 2030, driving demand for real-time CDI that captures risk-adjustment details across entire care episodes. Accountable Care Organizations depend on accurate notes for shared-savings tallies; even minor documentation lapses translate into seven-figure revenue losses. Providers are therefore layering predictive-analytics engines atop CDI systems to anticipate outcome gaps early, boosting both quality scores and financial performance.

ICD-11 Transition Accelerating Documentation Specificity

The 2025 ICD-11 release adds 17,000 diagnostic categories, requiring granular narrative capture that pushes conventional coding teams beyond capacity.[2]World Health Organization, “WHO Releases 2025 Update to the International Classification of Diseases (ICD-11),” who.int U.S. hospitals face an aggressive 2025–2027 rollout window, prompting rapid upgrades to AI coding assistants able to parse the new clustered code structure. Early adopters report fewer coder queries and higher first-pass accuracy once automated mapping tools replace manual look-ups.

Expansion Of Outpatient CDI Programs Amid Rising Complexity

Ambulatory surgical centers will see 21% procedure-volume growth over the next decade, and Medicare has already added 547 ASC-eligible codes, escalating denial risk without robust outpatient CDI.[3]ASC Focus, “Sg2 2024 Annual Report Projects High Growth in ASC Volume,” ascfocus.org Because reviews occur after brief encounters, providers implement retrospective analytics that scan multi-payer rule sets before claim submission. Investments are reinforced by the new G2211 add-on code, which requires detailed cognitive-load justifications, making comprehensive outpatient documentation indispensable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity concerns in cloud CDI | -0.8% | Global; stricter in EU & North America | Short term (≤ 2 years) |

| Shortage of certified CDI specialists | -1.2% | Global; most acute in North America & Europe | Long term (≥ 4 years) |

| Alert fatigue from over-zealous CAPD algorithms | -0.6% | Global; high-EHR regions | Medium term (2-4 years) |

| Payer-specific documentation rules causing re-work | -0.9% | North America core; emerging elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cybersecurity Concerns In Cloud CDI

Migration to cloud opens sensitive clinical narratives to new threat vectors, and forthcoming HIPAA revisions tighten breach-notification requirements. Multi-regional deployments raise data-sovereignty questions, particularly in Europe’s GDPR regime. Homomorphic encryption promises analytics on encrypted data yet still carries performance overheads that temper roll-outs. Hospitals therefore adopt hybrid models, keeping identifiers on-premise while outsourcing analytics to secured clouds.

Shortage Of Certified CDI Specialists

Two-thirds of HIM leaders cite staffing shortfalls that directly impact revenue integrity. Average specialist salaries climbed to USD 76,500 in 2025, stretching provider budgets and lengthening recruitment cycles. AI-driven chart reviewers partially bridge gaps, but complex cases still require human validation. Workforce constraints are most severe in outpatient and post-acute domains, where coding rules evolve rapidly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads While Services Surge

The software segment retained a 66.34% revenue share in 2024, underscoring providers’ preference for integrated, EHR-compatible platforms. This dominance is underpinned by enterprise scalability and standardized user experiences that smooth cross-facility roll-outs. Yet services are accelerating at an 11.23% CAGR, reflecting heightened regulatory complexity and talent shortages. Hybrid offerings such as Optum Integrity One pair AI engines with expert advisory teams, yielding 20% productivity gains for pilot customers.

Software vendors now bundle implementation road-maps, change-management support and ongoing education, blurring the line between product and consultative engagement. Hospitals realize that technology alone seldom resolves documentation bottlenecks; customized workflows and coder upskilling determine ROI. Consequently, the Clinical Documentation Improvement market increasingly prizes solution providers that combine robust platforms with deep clinical-coding expertise.

By Deployment Mode: Cloud Acceleration Transforms Access

Cloud options accounted for 54.56% of sector revenue in 2024 and are widening their lead with an 11.55% CAGR. Hospitals favor the model for continuous feature updates, reduced capital spending and seamless remote access—advantages proven invaluable during pandemic-related staffing disruptions. Scalable cloud architectures also support hospital-at-home initiatives, where remote teams require instant chart visibility.

Some institutions continue on-premise deployments due to legacy integrations or local security mandates, though these represent a diminishing share of new deals. Hybrid architectures, where sensitive identifiers reside on hospital servers while analytics run in the cloud, strike a pragmatic balance for privacy-constrained regions. Vendors now offer single code bases deployed across any environment, ensuring that functionality parity no longer dictates infrastructure choice.

By End User: Post-Acute Care Drives Unexpected Growth

Hospitals retained 61.22% of 2024 revenue, benefiting from years of CDI process refinement. However, post-acute and long-term care facilities will deliver the fastest 10.67% CAGR as PDPM links reimbursement directly to documentation fidelity. Skilled-nursing operators adopt CDI to avoid payment cuts stemming from coding inaccuracies, and cloud delivery removes the need for on-site IT teams.

Physician groups and ambulatory surgery centers are under similar pressure as Medicare expands its procedural list and introduces complex add-on codes. Cloud CDI tools offer these smaller entities enterprise-grade capabilities without heavy capital outlays. An emerging use case among payers shows insurers deploying CDI analytics to pre-empt claim denials and streamline appeals processing, further diversifying the end-user landscape.

By Application Setting: Outpatient CDI Gains Momentum

Inpatient programs still comprised 62.34% of 2024 spending, reflecting mature concurrent-review workflows refined over decades. Clinical Documentation Improvement market size for inpatient settings will nonetheless expand steadily as ICD-11 adds coding granularity. Outpatient CDI, meanwhile, is poised for 9.46% CAGR through 2030 as ASCs and physician clinics encounter rising denial rates.

Emergency departments illustrate CDI’s adaptation to high-velocity environments; AI scribes capture triage narratives in real time, cutting note-creation minutes and boosting accuracy. Hospital-at-home schemes merge inpatient complexity with outpatient logistics, giving rise to hybrid CDI approaches that rely heavily on cloud connectivity and mobile data capture.

Geography Analysis

North America led the Clinical Documentation Improvement market with 41.63% revenue in 2024, underpinned by mature EHR penetration, stringent CMS quality rules and early adoption of ambient AI. United States providers continue to refine CDI programs as hospital-at-home waivers extend remote-care documentation requirements, but market growth is moderating as penetration nears saturation. Canada follows similar patterns, though provincial interoperability projects are generating fresh demand for cloud-based CDI that spans regional health networks.

Asia-Pacific is the fastest-growing region at a 9.33% CAGR, buoyed by government digitization drives and impending ICD-11 implementation plans. Australia’s national mapping initiatives and staff-training grants accelerate technology purchases, while Japan’s aging population fuels post-acute CDI investments aimed at long-term-care reimbursement accuracy. In India and Southeast Asia, private hospitals view CDI as a competitive differentiator for medical tourism, prioritizing internationally recognized documentation standards.

Europe records steady growth as digital-health policies promote interoperability and data-quality improvements. General Data Protection Regulation requirements heighten the emphasis on privacy-preserving CDI deployments, spurring innovation in encryption and hybrid cloud architectures. Emerging Middle East and African markets adopt CDI mainly within high-acuity urban hospitals, though broader uptake is expected as regional coding standards mature and insurance coverage widens.

Competitive Landscape

The Clinical Documentation Improvement market features moderate concentration, with diversified health-IT giants contending against niche AI innovators. Microsoft-Nuance leverages DAX Copilot’s integration inside Epic to dominate ambient scribing, while Solventum positions its revenue-integrity suite as an end-to-end CDI backbone. Epic itself embeds more than 100 AI functions into its core EHR to streamline note completion and coding recommendations.

Merger activity underscores a platform-consolidation trend. R1 RCM’s USD 8.9 billion take-private deal and Commure’s USD 139 million Augmedix acquisition illustrate investor appetite for vertically integrated documentation engines. Smaller disruptors deploy large language models to attain autonomous CDI; AKASA’s GenAI optimizer analyzes entire chart populations, promising reduced query volume and higher capture of risk-adjustment factors.

White-space opportunities remain in post-acute care and non-U.S. markets where workforce shortages and regulatory transitions create unmet needs. Vendors differentiate on algorithm transparency, clinician-centric UX, and the ability to navigate payor-specific rules without generating alert fatigue. As generative AI matures, software suppliers emphasize responsible-AI frameworks to maintain trust and comply with evolving privacy laws.

Clinical Documentation Improvement Industry Leaders

Solventum

Microsoft (Nuance Communications)

UnitedHealthcare Corporation (Optum Inc)

Dolbey Systems Inc.

nThrive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Huma Therapeutics introduced Hi Scribe, a generative-AI tool that auto-creates clinical notes.

- March 2025: Microsoft launched Dragon Copilot, the first unified voice-AI assistant spanning clinical documentation and task automation.

- February 2025: IKS Health debuted Scribble Now, adding real-time documentation to its Scribble Suite during ViVE 2025.

- January 2025: ScribeAI exited stealth with technology that converts clinician–patient dialogue into SOAP notes, cutting doc time by 90%.

Global Clinical Documentation Improvement Market Report Scope

| Software |

| Services |

| On-premise |

| Cloud-based |

| Hybrid |

| Hospitals |

| Physician Practices |

| Ambulatory Surgical Centers |

| Post-Acute / Long-Term Care Facilities |

| Payers |

| Inpatient CDI |

| Outpatient CDI |

| Emergency Department |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | On-premise | |

| Cloud-based | ||

| Hybrid | ||

| By End User | Hospitals | |

| Physician Practices | ||

| Ambulatory Surgical Centers | ||

| Post-Acute / Long-Term Care Facilities | ||

| Payers | ||

| By Application Setting | Inpatient CDI | |

| Outpatient CDI | ||

| Emergency Department | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global Clinical Documentation Improvement market in 2025?

The Clinical Documentation Improvement market size stands at USD 5.13 billion in 2025 with a forecast 7.64% CAGR to 2030.

Which deployment model is growing fastest for CDI solutions?

Cloud platforms are expanding at 11.55% CAGR due to scalability, automatic updates and remote-access advantages.

Why are post-acute facilities investing in CDI programs?

Implementation of the Patient-Driven Payment Model links skilled-nursing reimbursement to precise documentation, spurring 10.67% CAGR among post-acute users.

How will ICD-11 affect CDI workflows?

ICD-11 introduces far more diagnostic codes, demanding granular clinician notes and driving the adoption of AI-assisted coding tools.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 9.33% CAGR thanks to accelerated digitization, government IT investment and upcoming ICD-11 adoption.

What technology trend most reduces clinician documentation burden?

Ambient AI scribes that transcribe and structure real-time conversations markedly cut note-taking time while improving data specificity.

Page last updated on: