Clinical Decision Support Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 4.94 Billion |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

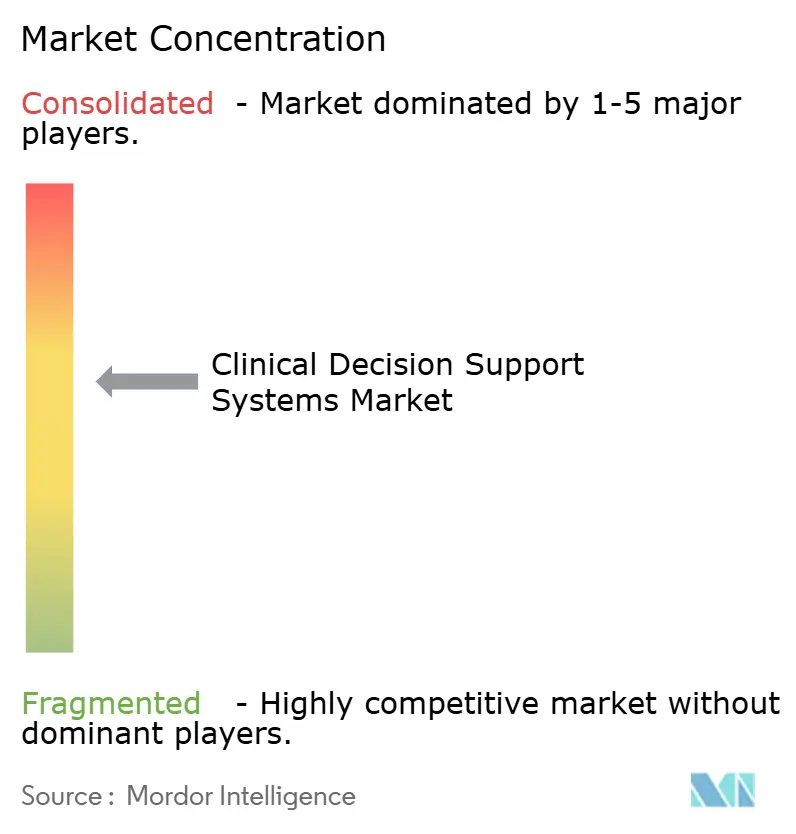

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Decision Support Systems Market Analysis by Mordor Intelligence

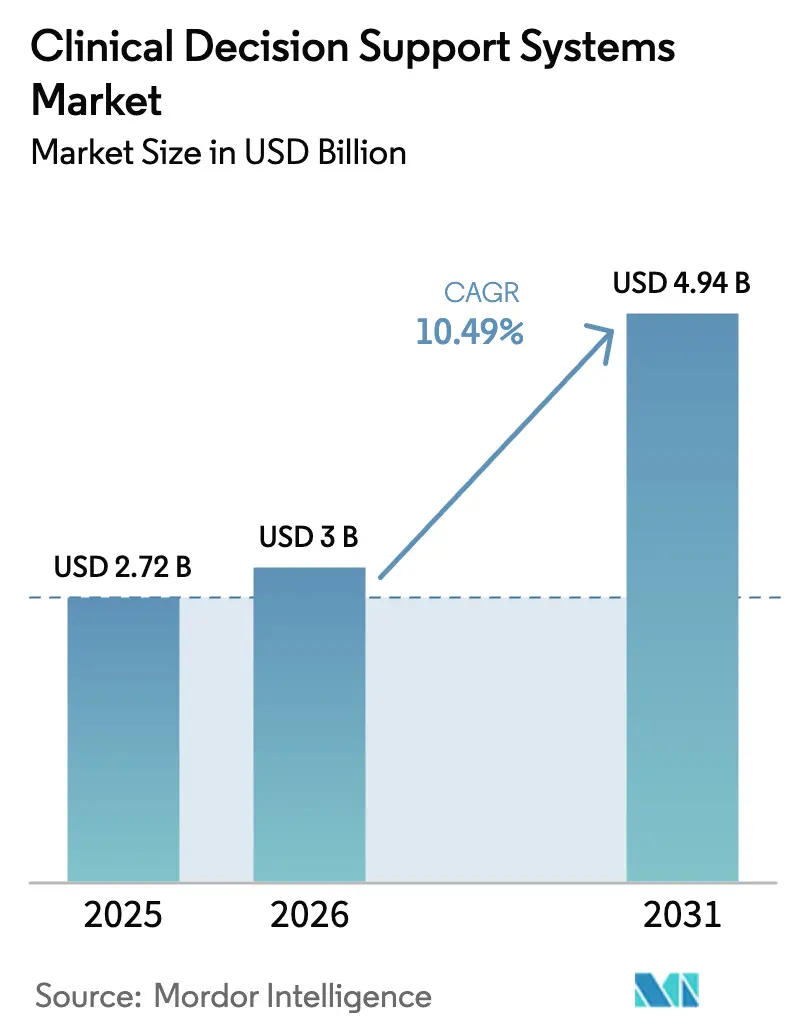

The Clinical Decision Support Systems Market size is projected to expand from USD 2.72 billion in 2025 and USD 3 billion in 2026 to USD 4.94 billion by 2031, registering a CAGR of 10.49% between 2026 to 2031.

The growth trajectory is fueled by near-universal electronic-health-record adoption, tighter value-based reimbursement rules, and expanding cloud capacity that makes large-scale AI model training financially viable. Mandatory U.S. interoperability standards and the European Union AI Act are forcing suppliers to expose application-programming interfaces and invest in explainability, respectively, which together accelerate product refresh cycles. Machine-learning CDSS outperforming rule engines in radiology and pathology, combined with elastic cloud pricing, is steering capital away from on-premise hardware toward subscription software bundles. At the same time, high-profile ransomware incidents are creating short-term headwinds that slow cloud migrations but, paradoxically, push vendors to harden security and differentiate on zero-trust architectures.

Key Report Takeaways

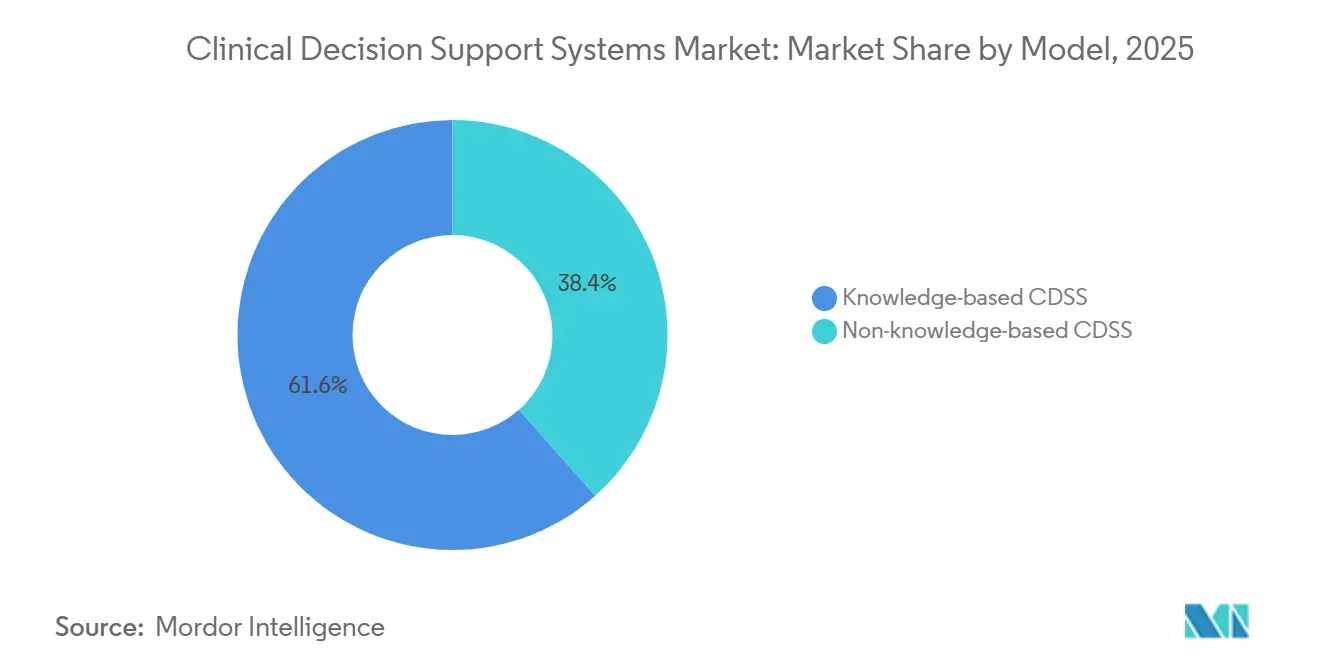

- By model architecture, knowledge-based CDSS led with 61.56% revenue share in 2025; non-knowledge-based platforms are projected to advance at a 14.25% CAGR to 2031.

- By delivery mode, on-premise deployments held 54.53% of the clinical decision support systems market share in 2025, while cloud delivery is expanding at a 16.85% CAGR through 2031.

- By component, services accounted for 43.63% share of the clinical decision support systems market size in 2025, whereas software subscriptions are growing at a 13.87% CAGR through 2031.

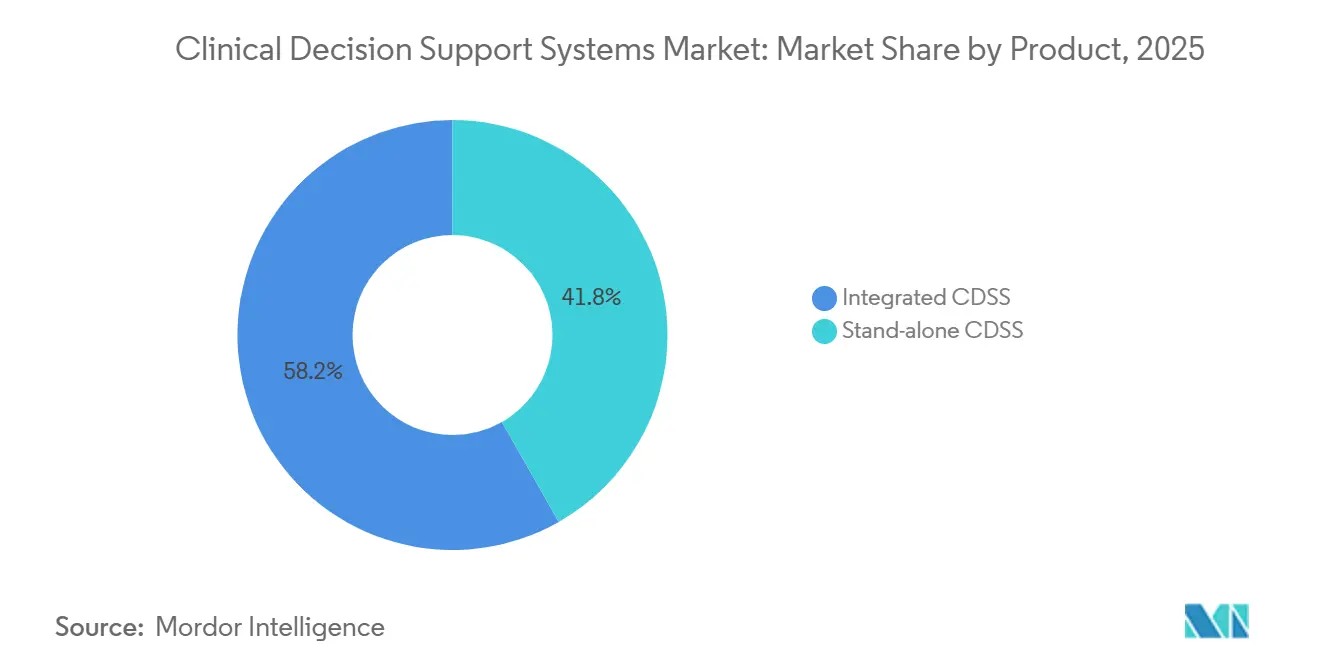

- By product, integrated CDSS captured 58.23% revenue share in 2025; stand-alone modules are forecast to post a 15.7% CAGR through 2031.

- By application, medical diagnosis tools held 31.3% of 2025 revenue, while information-retrieval platforms are advancing at an 18.81% CAGR to 2031.

- By geography, North America retained 46.53% share in 2025; Asia-Pacific is the fastest-growing region at a 12.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Clinical Decision Support Systems Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of EHR-integrated CDSS | +2.8% | North America, Europe, global spillovers | Medium term (2-4 years) |

| AI/ML-powered analytics enhancing precision | +3.1% | North America, Asia-Pacific, global | Long term (≥ 4 years) |

| Pressure to lower healthcare costs & errors | +2.4% | North America, Europe | Medium term (2-4 years) |

| Ambient voice-enabled CDSS easing burnout | +1.5% | North America, Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Regulation-driven demand for explainability | +1.2% | Europe, North America, Asia-Pacific spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of EHR-Integrated CDSS

Nearly all U.S. acute-care hospitals deployed certified EHRs by late 2024, creating an established data substrate for embedded decision engines. Epic’s 2025 release streamlined Cosmos-based machine-learning tools so that risk scores appear inside chart review screens without extra clicks, boosting workflow adherence. Oracle Health’s USD 1.50 billion codebase rebuild migrated CDSS logic to native cloud microservices that fire alerts only when contextual parameters are met, cutting duplicate pop-ups by 28% in pilot hospitals. Interoperability mandates lower integration barriers for third-party algorithms, yet they also deepen vendor lock-in because switching EHRs now means migrating thousands of custom CDS rules. Hospitals consequently prefer best-of-breed modules that can thrive inside major EHR ecosystems yet remain contractually portable if platform strategy shifts.

AI/ML-Powered Analytics Enhancing Decision Precision

The U.S. FDA cleared 171 AI-enabled medical devices in 2024, 42 of which were radiology algorithms calibrated on multi-site datasets[1]U.S. FDA, “Artificial Intelligence and Machine Learning in SaMD,” FDA.GOV. GE HealthCare’s AIR Recon DL halves MRI scan times while preserving image fidelity, cutting patient throughput bottlenecks in resource-constrained imaging suites. Philips’ Azurion platform automatically moderates radiation dose, helping hospitals comply with new IAEA dosage guidelines and avoid reimbursement penalties. Continuous-learning models retrain monthly in cloud sandboxes, incorporating fresh trial results faster than manual rule curation. Regulators now require post-market surveillance dashboards so that drift in algorithm performance across demographic cohorts triggers proactive updates rather than public-safety recalls.

Pressure to Lower Healthcare Costs & Medical Errors

Medicare’s Readmissions Reduction Program expanded penalties to eight conditions in 2024, putting USD 520 million of reimbursement at stake and pushing hospitals to embed risk-scoring CDSS that flag unstable patients before discharge. MEDITECH’s readmission score reduces 30-day bounce-backs by 11% in multi-hospital studies because care coordinators schedule follow-ups triggered by algorithmic risk tiers. Wolters Kluwer’s March 2024 pharmacogenomic alert expansion slashed warfarin adverse-event rates by 35% in early adopters. Such quantifiable returns underpin capital requests for CDSS despite margin pressure from nurse-staffing inflation.

Ambient Voice-Enabled CDSS Easing Clinician Burnout

JAMA Network Open reported that ambient AI scribes trim daily EHR time by 1.5 hours, allowing an extra 7.5 patient visits per week without lengthening shifts. Microsoft-Nuance’s Dragon Ambient eXperience streams conversations to Azure OpenAI, populating discrete EHR fields and simultaneously running context triggers so that chest-pain complaints prompt ACS checklists. Athenahealth’s February 2025 rollout bundled ambient documentation into platform fees, spurring a 3-point jump in customer-satisfaction surveys because providers perceive a fair exchange - PDMP queries and lab orders autopopulate without extra data entry.

Restraints Impact Analysis of Clinical Decision Support Systems Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy & cybersecurity concerns (cloud) | −1.8% | North America, Europe | Short term (≤ 2 years) |

| Shortage of informatics-skilled workforce | −1.3% | Asia-Pacific, rural North America | Medium term (2-4 years) |

| Alert-fatigue eroding clinician trust | −1.1% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy & Cybersecurity Concerns (Cloud)

Ransomware attacks on Change Healthcare and Ascension Health disabled billing and EHR systems for weeks, exposing gaps in multifactor authentication and network segmentation. The U.S. HHS responded with proposed rules mandating annual penetration tests, adding compliance costs that strain community hospitals contemplating cloud CDSS. Vendors counter by marketing confidential-computing enclaves that encrypt data during processing, yet CIOs remain wary of third-party access. Hybrid architectures are therefore rising: sensitive identifiers stay on-premise while de-identified training data moves to elastic cloud clusters.

Shortage of Informatics-Skilled Workforce

AMIA estimates the United States lacked 30,000 clinical informaticists in 2024, a gap poised to widen as AI upkeep demands continuous model tuning[2]AMIA, “Clinical Informatics Workforce Gap,” AMIA.ORG. Rural hospitals struggle to pay USD 120,000 salaries, so they outsource rule optimization to consultants, elongating go-live timelines. India’s national certification program aims to mint 10,000 informaticians by 2026 but faces faculty shortages, signaling that talent pipelines will lag CDSS rollout schedules for several years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Clinical Decision Support Systems Market Segment Analysis

By Model Architecture:

Machine Learning Overtakes Rule EnginesNon-knowledge-based CDSS are forecast to expand at a 14.25% CAGR, dwarfing the overall clinical decision support systems market growth. Knowledge-based engines still hold 61.56% revenue, yet their static rule trees require costly quarterly updates, especially as medical literature doubles every 73 days. Google Health’s diabetic-retinopathy algorithm, retrained on new images monthly, illustrates how ML systems assimilate latest evidence without manual curation. Knowledge-based platforms will persist in medication safety where deterministic logic remains sufficient, but radiology and pathology workflows now favor convolutional networks that surpass human accuracy in image interpretation.

Rule-engine stalwarts are adopting hybrid approaches, layering ML-derived probability scores under traditional rule triggers. Vendors that fail to pivot risk obsolescence, as Watson Health’s 2024 exit demonstrated. Over the forecast period, mature EHR providers will embed ML pipelines inside existing CDSS GUIs, blurring the boundary between rule-based and data-driven models. Hospitals will compare total-cost-of-ownership across both paradigms, and vendors offering automated retraining plus transparent version control stand to win replacement cycles.

By Mode of Delivery:

Cloud Elasticity Spurs MigrationCloud-delivered CDSS will compound at a 16.85% rate through 2031, despite heightened breach anxiety. The clinical decision support systems market size tied to on-premise architectures remains substantial, but CIOs increasingly allocate new budgets to SaaS licenses that include nightly security patches and GPU bursts for model re-training. Conflicts between latency requirements and data-sovereignty laws encourage hybrid topologies where sepsis and stroke alerts run on local edge servers while non-urgent analytics process in cloud clusters.

Ransomware events prompted temporary moratoriums on cloud transitions in 2024, yet those same incidents exposed under-invested on-premise defenses. Consequently, many health systems have negotiated “sovereign cloud” clauses that place patient identifiers in local regions while allowing de-identified pools to cross borders for research benchmarking. This arrangement satisfies regulators and delivers scale economics, positioning cloud consumption to outpace hardware refresh cycles by mid-decade.

By Component:

Subscriptions Eclipse Professional ServicesSoftware subscriptions are recording a 13.87% CAGR as vendors pivot from perpetual licenses to usage-based pricing that bundles upgrades, hosting, and support. Services still represent 43.63% revenue but are gradually cannibalized as low-code deployment templates shorten configuration windows from 12 months to 90 days. The outcome is margin compression for traditional systems integrators but wider adoption among small practices that could not previously afford six-figure implementation bills.

Hardware remains a niche segment anchored in imaging centers that deploy GPU appliances for on-premise inferencing to avoid network latency. Yet even here, vendors now embed Kubernetes clusters that can federate with cloud training nodes during off-peak hours. As model-update cadence accelerates, the value narrative shifts decisively to recurring software and data feeds rather than capital equipment.

By Product:

Integrated Dominance Challenged by Specialty ModulesIntegrated CDSS, embedded inside major EHR platforms, command 58.23% revenue because they eliminate context-switching and leverage single-sign-on. However, stand-alone modules growing at 15.7% CAGR now service specialties underserved by generic EHR tools. Dermatology, oncology pathology, and radiology prove particularly fertile niches where image-analysis algorithms deliver measurable diagnostic uplift.

Best-of-breed vendors capitalize on FHIR-based APIs to pull structured data without requiring EHR certification. The competitive dynamic is evolving toward “plug-in marketplaces” where hospitals assemble CDSS stacks à la carte, akin to smartphone app stores. EHR incumbents must demonstrate equal or superior performance in niche use cases or risk ceding margins to hyper-focused rivals.

By Application:

Evidence Synthesis Drives Information Retrieval BoomInformation-retrieval platforms clock the fastest growth at 18.81% CAGR because clinicians struggle to stay abreast of journal output. Generative-AI summarizers inside Elsevier ClinicalKey condense 20 pages of randomized-controlled-trial results into 200-word practice pearls, shaving literature review time to minutes. The clinical decision support systems market share for traditional diagnosis support tools remains large at 31.3%, yet liability worries temper aggressive rollouts in complex cases like oncology where false negatives carry high malpractice risk.

Prescription support is mature but evolving: pharmacogenomic alerts reduce adverse-drug-event litigation and thus keep payers engaged. Broader CDSS categories - population-health analytics, care-coordination alerts, and clinical-trial matching - are fragmenting as providers shift from episodic fee-for-service to longitudinal risk contracts.

Geography Analysis

North America Clinical Decision Support Systems Market

North America, holding 46.53% of 2025 revenue, leverages Medicare’s value-based purchasing penalties to justify CDSS investments that cut readmissions and hospital-acquired conditions. The 21st-Century Cures Act also criminalizes information blocking, giving third-party CDSS vendors API access to clinical data and accelerating plug-and-play adoption. Canada’s Connect Care platform embeds chronic-disease CDSS nationally but suffers provincial customization lags. Mexico’s diabetes CDSS pilot across 200 clinics demonstrates algorithm portability in low-bandwidth settings, yet national scaling depends on 5G rollouts.

APAC Clinical Decision Support Systems Market

Asia-Pacific records the fastest 12.21% CAGR. China’s EMR-maturity mandate requires Level 4 capabilities, directly embedding computerized-physician-order-entry and basic CDSS in 3,000 hospitals. India’s Ayushman Bharat Digital Mission assigns a unified health identifier, enabling tuberculosis screening algorithms to link radiographs with lab data for 95% sensitivity in trials. Japan subsidizes smaller hospitals to include polypharmacy CDSS, addressing medication adverse-event rates in its aging population. South Korea ties reimbursement to sepsis CDSS compliance metrics, making decision support financially non-negotiable. Australia’s My Health Record integrates cross-provider medication safety alerts, limiting duplication across its mixed private-public system.

Europe Clinical Decision Support Systems Market

Europe enforces strict AI governance. The AI Act imposes conformity assessments that extend product launches by up to 12 months, yet hospitals prefer CE-marked software because it certifies data-security and bias-mitigation practices. Germany reimburses 14 digital therapeutics, including diabetes CDSS, under its Digital Healthcare Act, offering vendors a template for payer engagement. The U.K. scaled an early-warning-score algorithm across 140 trusts but found 30% lacked informatics staff for local calibration, highlighting workforce bottlenecks. France’s Health Data Hub provides pseudonymized data from 67 million citizens to train cardiovascular-risk models, fostering public-private R&D partnerships.

LATAM and MEA Clinical Decision Support Systems Market

Latin America, the Middle East, and Africa represent smaller slices but register double-digit growth where national EHR programs exist. The UAE’s mandatory CDSS rollout across public hospitals by 2026 sets a regional benchmark. South Africa’s HIV-co-infection CDSS in 50 clinics lowered regimen-switch delays, while Brazil’s maternal-health CDSS shows promise but faces connectivity challenges in Amazon regions. These rollouts validate that CDSS delivers value even in resource-constrained environments when algorithms are tailored to local disease burdens.

Regulatory Landscape

In the United States, oversight of clinical decision support is tightening around transparency and interoperability. Under ASTP (formerly ONC) Health IT Certification Program updates, the legacy CDS criterion (45 CFR 170.315(a)(9)) sunset in January 2025, and developers had to meet the Decision Support Interventions (DSI) criterion (45 CFR 170.315(b)(11)) by December 2024 to stay aligned with Base EHR requirements. This has raised expectations around intervention design and disclosure for predictive outputs used in care workflows.

For AI-enabled CDSS, the U.S. FDA issued revised final guidance on Clinical Decision Support Software in January 2026. The guidance clarifies when CDS functionality may fall outside device regulation and emphasizes that clinicians must be able to independently review the basis for recommendations, backed by clear descriptions of logic, inputs, validation, and limitations. In Europe, the EU AI Act (Regulation (EU) 2024/1689) introduces additional obligations for high-risk AI, including governance, risk management, and documentation requirements that intersect with MDR/IVDR conformity activities. For CDSS suppliers serving EU health systems, these obligations can extend enterprise deployment timelines.

Competitive Landscape

The market remains moderately fragmented. Epic and Oracle Health collectively manage EHR platforms for a significant percentage of U.S. beds, granting them privileged data access to bundle CDSS. Stand-alone vendors counter by excelling in niche accuracy; VisualDx outperforms integrated dermatology modules in lesion classification, and Qure.ai’s chest X-ray tool rivals radiologist sensitivity in tuberculosis detection. IBM’s 2024 exit from Watson Health underscores that breadth without depth struggles against specialty-focused challengers.

Strategic partnerships shape differentiation. NextGen Healthcare now curates a marketplace of pre-certified stand-alone modules, lowering risk for community hospitals. Amazon’s AWS HealthLake collaborates with leading academic centers to co-develop cohort-level prediction models that run on serverless infrastructure, slashing compute procurement cycles. Meanwhile, cybersecurity maturity becomes a competitive lever - Microsoft’s confidential-computing enclaves encrypt data in use, a capability highlighted in RFPs post ransomware attacks.

White-space opportunities proliferate in post-acute care, where CDSS adoption lags acute care by half a decade. Vendors developing lightweight algorithms for skilled-nursing facilities or home-health agencies can gain first-mover advantages. Autonomous CDSS capable of rendering decisions without human oversight remain nascent but could disrupt triage and chronic-disease management once liability frameworks solidify.

Clinical Decision Support Systems Industry Leaders

Oracle (Cerner)

Epic Systems Corporation

Wolters Kluwer N.V.

Siemens Healthineers

Merative

- *Disclaimer: Major Players sorted in no particular order

Clinical Decision Support Systems Market Companies Covered in this Report

- Agfa-Gevaert

- Allscripts

- Athenahealth

- UnitedHealth Group (Change Healthcare)

- EBSCO Information Services

- Elsevier B.V.

- Epic Systems

- GE Healthcare

- Meditech

- Merative

- NextGen Healthcare

- Optum

- Oracle

- Koninklijke Philips

- Siemens Healthineers

- VisualDx

- Wolters Kluwer

- Zynx Health

Read Analysis of Clinical Decision Support Systems Companies

Market Opportunities and Future Outlook

Standardization and compliance-driven product refresh cycles are creating near-term whitespace for vendors that can operationalize transparency, monitoring, and workflow-safe user experience. The FDA's January 2026 revised final guidance on Clinical Decision Support Software pushes suppliers toward plain-language explainability, clear data-source disclosure, and explicit documentation of validation and limitations. That shift is increasing demand for packaged governance features, such as audit trails, model cards, and post-market performance monitoring, that can be rolled out across both integrated and stand-alone CDSS portfolios.

Interoperable, EHR-embedded decision layers are also moving up provider priority lists as organizations build modular stacks rather than rely on single monolithic tools. HL7 International's ongoing roadmap for CPG-on-FHIR STU3, along with continued use of CDS Hooks for remote, user-facing decision support, supports a practical integration path for third-party modules into dominant EHR workflows, including care pathways, order sets, and guideline-based reasoning services. This standards traction points to specific execution opportunities in specialty diagnostics and evidence retrieval, where best-of-breed vendors can connect through FHIR-based services while aligning with rising transparency and safety management requirements.

Recent Industry Developments in Clinical Decision Support Systems Market

- May 2026: Labcorp and Epic expanded their collaboration to integrate Labcorp's full diagnostic test menu into Epic Aura, strengthening end-to-end ordering and results workflows inside the EHR. Deeper diagnostic connectivity increases the addressable surface area for embedded decision support, including test selection guidance, reflex testing pathways, and result-specific interpretation prompts at the point of care.

- March 2026: Oracle Health made Clinical AI Agent note generation available in the United States for inpatient and emergency department settings. By placing a generative AI capability directly into high-acuity workflows, Oracle increased competitive pressure on CDSS vendors to deliver context-aware assistance that reduces documentation burden while maintaining clinician control and traceability.

- October 2024: Oracle Health introduced its Clinical AI Agent to support clinicians with AI-driven assistance within clinical workflows. The rollout shifted attention from traditional alerting to assistant-style decision support embedded in enterprise EHR environments, raising expectations for semantic understanding and workflow integration instead of standalone rule-based prompts.

Clinical Decision Support Systems Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers clinical decision support systems used by care teams to support medical decisions through software-led functions like alerts, reminders, guideline prompts, and diagnostic or medication support, across integrated and standalone deployments in healthcare settings.

Scope exclusions: We exclude general EHR functions that do not provide decision support logic and we also exclude non-clinical administrative IT tools.

Segments Covered in This Report

- By Model

- Knowledge-based CDSS

- Non-knowledge-based CDSS

- By Mode of Delivery

- Cloud-based

- On-premise

- By Component

- Hardware

- Software

- Services

- By Product

- Integrated CDSS

- Stand-alone CDSS

- By Application

- Medical Diagnosis

- Alerts & Reminders

- Prescription Decision Support

- Information Retrieval

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean fact base on healthcare digital adoption and clinical workflow needs, then using that to decide what should be counted as decision support versus adjacent IT. For this, we rely on public sources such as the US FDA digital health and SaMD guidance pages, CMS and ONC healthcare IT adoption materials, OECD health statistics, WHO digital health resources, and peer-reviewed clinical informatics journals.

Next, we use secondary documents such as annual reports, investor presentations, product brochures, and hospital procurement notes to understand how solutions are packaged (software, services, and supporting hardware) and how delivery models are shifting toward cloud. Where needed, we use paid subscriptions for company financials and news to sanity-check revenue direction and major contract announcements, and a patent database subscription to spot where decision-support functionality is actively being developed. The sources listed above are illustrative, and we also consult additional public and secondary references to fill gaps and validate assumptions.

Primary Interviews and Surveys

Primary interviews and surveys focus on confirming what buyers actually deploy and pay for, and on filtering out modules that are bundled but rarely activated in day-to-day clinical workflow. We speak with hospital IT leaders, clinical informatics staff, solution implementation partners, and product managers across major regions so assumptions like deployment mix, average contract sizes, and renewal behavior can be checked and adjusted.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | APAC: 53% |

| Mid tier: 42% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 20% | Managers: 52% | Americas: 18% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs the addressable spend pool by linking healthcare IT budgets and digital care adoption to the share typically allocated to decision support functions, then splitting the result by deployment mode, component, and care setting. Once that structure is in place, totals are cross-checked using selective bottom-up approximations, such as sampling supplier revenue disclosures where available, checking typical contract values by hospital size, and validating volumes using implementation counts and renewal cycles.

A few practical inputs that move the model are the installed base of EHR and CPOE-enabled sites, alert and medication safety module adoption, cloud migration pace for clinical software, average subscription and services mix, and the rate of guideline and drug database updates that drive ongoing spend. When some inputs are not visible for smaller markets, gaps are handled through proxy indicators like comparable country IT adoption levels and hospital bed capacity, and then corrected through interview feedback before totals are finalized.

Forecasting uses scenario analysis supported by trend lines on adoption and pricing, then a refinement step that applies exponential smoothing to near-term spending patterns so short-term volatility does not overstate long-run growth. The final trajectory is reviewed with experts to ensure assumptions like utilization, renewal timing, and the cloud shift are realistic for each region.

Data Validation & Update Cycle

Validation is done through multiple checks that compare model outputs to independent signals, such as reported healthcare IT spending trends, procurement momentum, and the pace of clinical workflow digitization. Outliers are flagged early, and drivers are rechecked by revisiting assumptions like deployment mix, contract duration, and service attachment before sign-off.

A second analyst review is completed before publication so the logic, math, and scope boundaries stay consistent across regions and segments. The report is refreshed annually, and interim updates are triggered when there are material events such as policy shifts, large platform changes, or sudden pricing moves. Before delivery, one more pass is done so clients receive an updated view that reflects the latest available information.

Mordor Intelligence's Clinical Decision Support Systems Market Size Measured Against Other Published Estimates

It is normal to see different market sizes for clinical decision support systems because publishers draw the boundary in different places and they also vary on what year they treat as the current reference point. Differences also come from how integrated modules are counted, whether services and supporting hardware are included, and how quickly assumptions are refreshed when cloud delivery accelerates.

By tracking deployed module activation, contract renewal patterns, and component-level splits, Mordor Intelligence keeps the estimate tied to decision-support usage in clinical workflow instead of counting broader clinical IT that sits next to CDSS. The spread in published values usually comes from whether integrated features inside EHR platforms are fully priced in, whether implementation and optimization services are included at the same rate, and whether currency timing and inflation adjustments are aligned to the same year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.00 B (2026) | |

| Global Consultancy A | USD 1.80 B (2024) | Uses a narrower revenue boundary that leans on standalone CDSS purchases and applies slower adoption assumptions for integrated decision-support modules inside clinical platforms. |

| Industry Publisher B | USD 6.36 B (2025) | Likely counts a wider bundle of clinical software functions as CDSS, and it appears to apply a higher pricing base without separating implementation services from ongoing subscriptions. |

The table shows that most of the variance can be explained by how integrated functionality is treated and how broadly the package of software and services is defined. Keeping scope rules explicit, then validating key inputs like deployment mix, service attachment, and pricing progression, gives a market value that is easier to reproduce and update over time.

Key Questions Answered in the Report

How fast is spending on clinical decision support growing worldwide?

Global outlays are rising at a 10.49% CAGR and are projected to reach USD 4.94 billion by 2031, led by machine-learning upgrades and cloud migrations.

Which delivery model is scaling quickest for CDSS?

Cloud-hosted platforms are advancing at a 16.85% CAGR as hospitals trade capital expenditure for elastic compute and bundled cybersecurity controls.

Where are regulation changes having the biggest market impact?

The European Union AI Act shapes product roadmaps by demanding conformity assessments and explainability, while U.S. interoperability rules foster third-party module uptake.

What segment currently commands the largest revenue share?

Knowledge-based CDSS still lead with 61.56% share, but their growth lags as machine-learning platforms outperform them in image-intensive specialties.

Why is alert fatigue a top concern for hospitals?

Studies show clinicians override up to 94% of duplicate-therapy alerts, eroding trust in decision support and forcing vendors to redesign rules for contextual relevance.

Which region is expected to post the highest future growth?

Asia-Pacific, expanding at a 12.21% CAGR, benefits from government-funded EHR mandates and subsidies for AI-enabled decision support in large public hospital networks.

Page last updated on: