Circular Economy Platform For The IT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

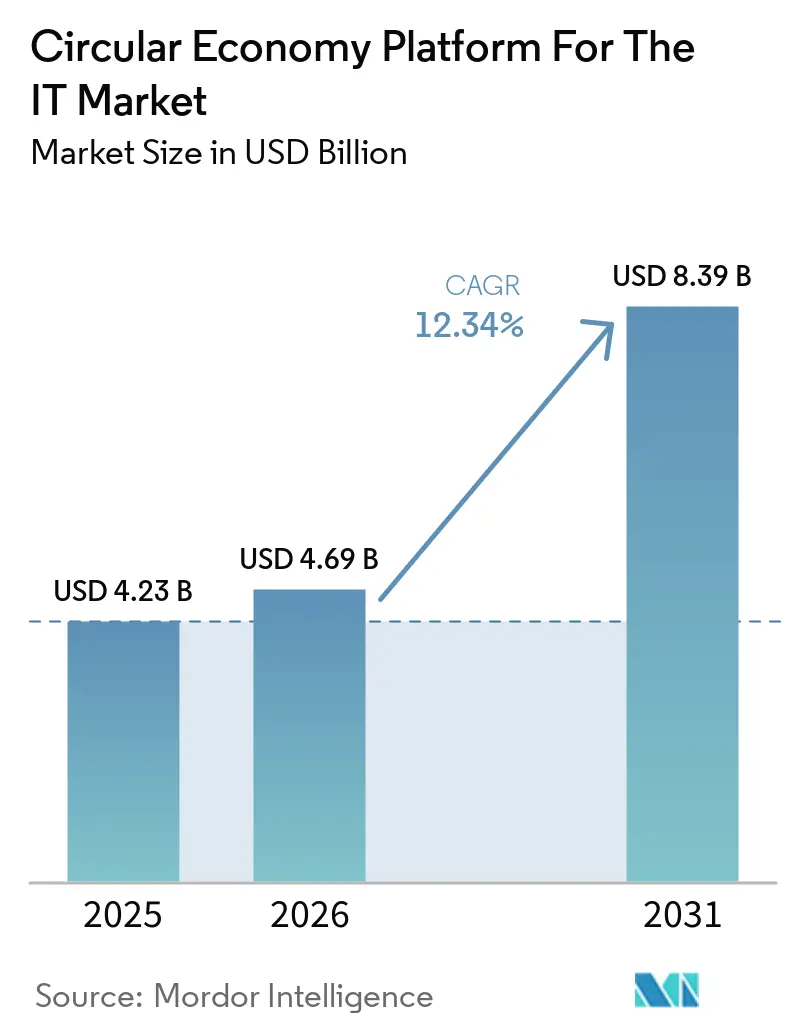

| Market Size (2026) | USD 4.69 Billion |

| Market Size (2031) | USD 8.39 Billion |

| Growth Rate (2026 - 2031) | 12.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Circular Economy Platform For The IT Market Analysis by Mordor Intelligence

The circular economy platform for the IT market is projected to reach USD 4.23 billion in 2025, USD 4.69 billion in 2026, and USD 8.39 billion by 2031, growing at a CAGR of 12.34% from 2026 to 2031. The circular economy platform for the IT market is expanding as enterprises replace hardware more frequently, e-waste rules become stricter, and finance teams recognize greater value in recovering proceeds from retired assets. AI-driven data center buildouts are also increasing the volume of servers, storage systems, and related components that require secure, compliant end-of-life handling. This is pushing the circular economy platform for the IT market toward tools that can track each asset, document data erasure, and support audit needs across multiple sites and countries. Competition is tightening as larger operators deepen hyperscaler relationships and add capabilities through acquisitions, while many regional providers still lack comparable automation, reporting depth, and cross-border coverage. Legacy asset records, uneven take-back standards, and friction with incumbent ITAD partners still slow adoption, but stronger AI-led grading tools and mandatory reporting rules continue to support long-term demand.

Key Report Takeaways

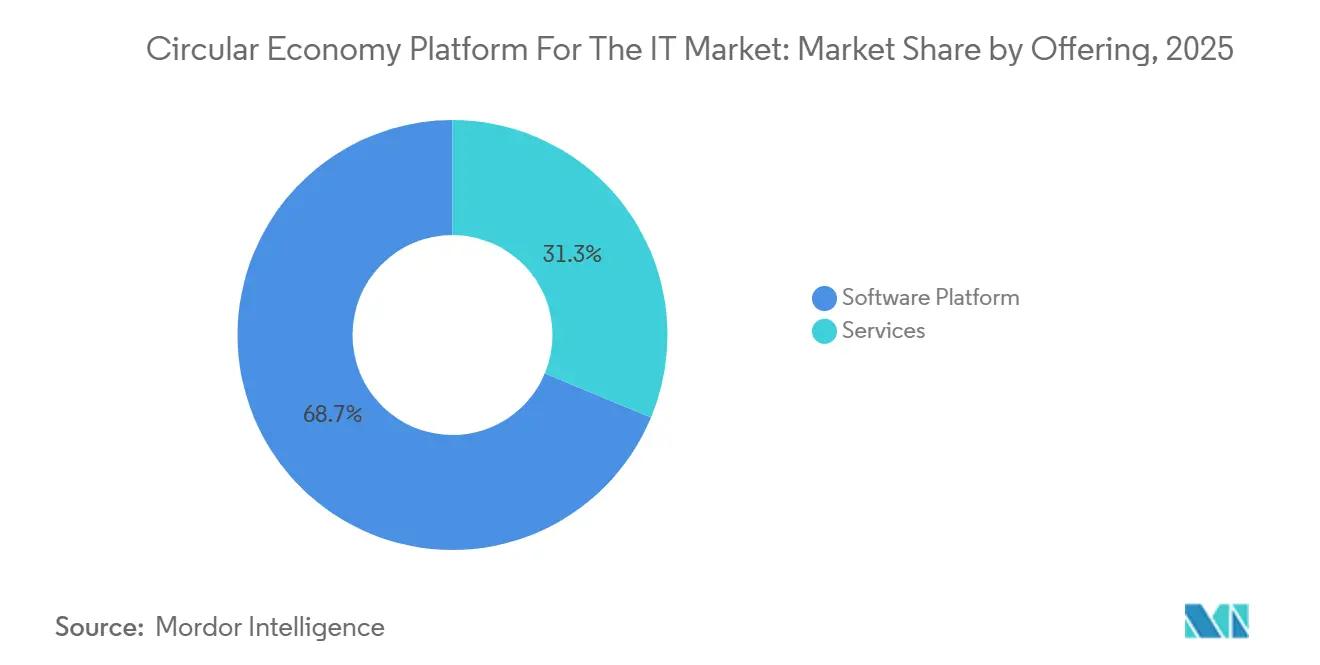

- By offering, software platforms held a 68.74% share of the circular economy platform for the IT market in 2025, while services are projected to expand at a 12.85% CAGR through 2031.

- By deployment model, cloud held 65.12% share in 2025, while hybrid is projected to advance at a 12.92% CAGR through 2031.

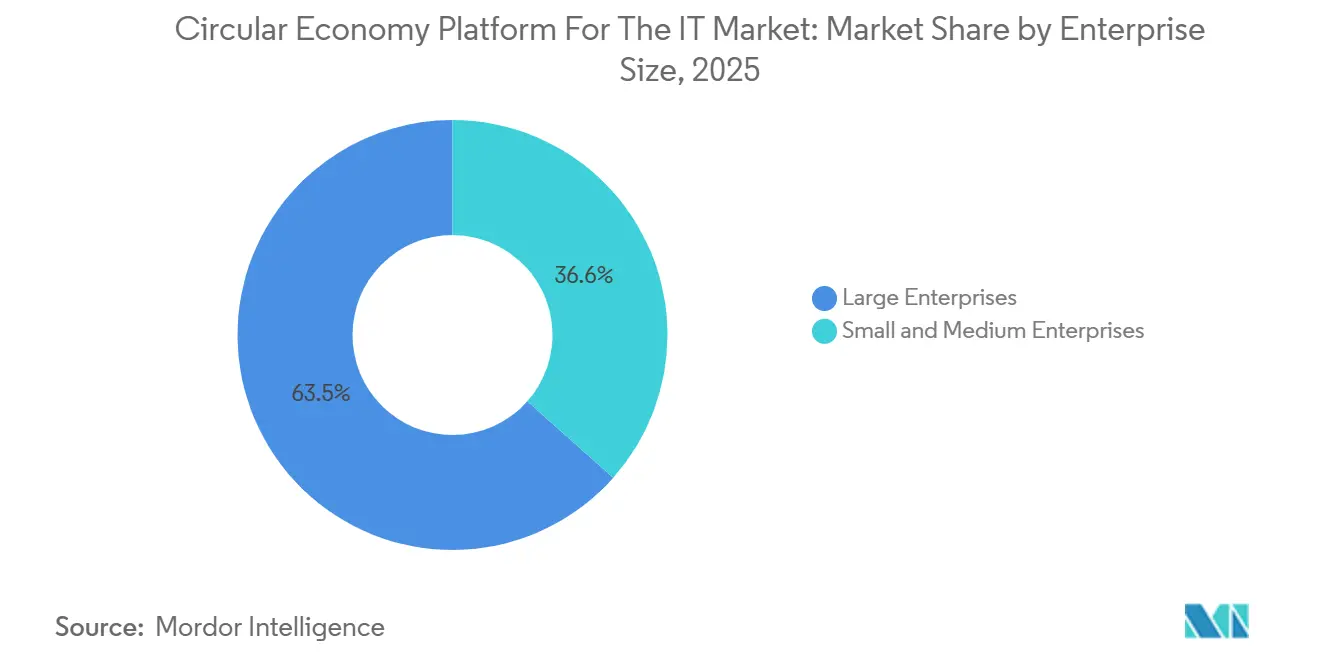

- By enterprise size, large enterprises held 63.45% share of the circular economy platform for the IT market in 2025, while SMEs are projected to expand at a 12.78% CAGR through 2031.

- In the circular economy, asset reuse and redeployment accounted for a 27.41% share in 2025, while ESG and compliance reporting are projected to grow at a 13.05% CAGR through 2031.

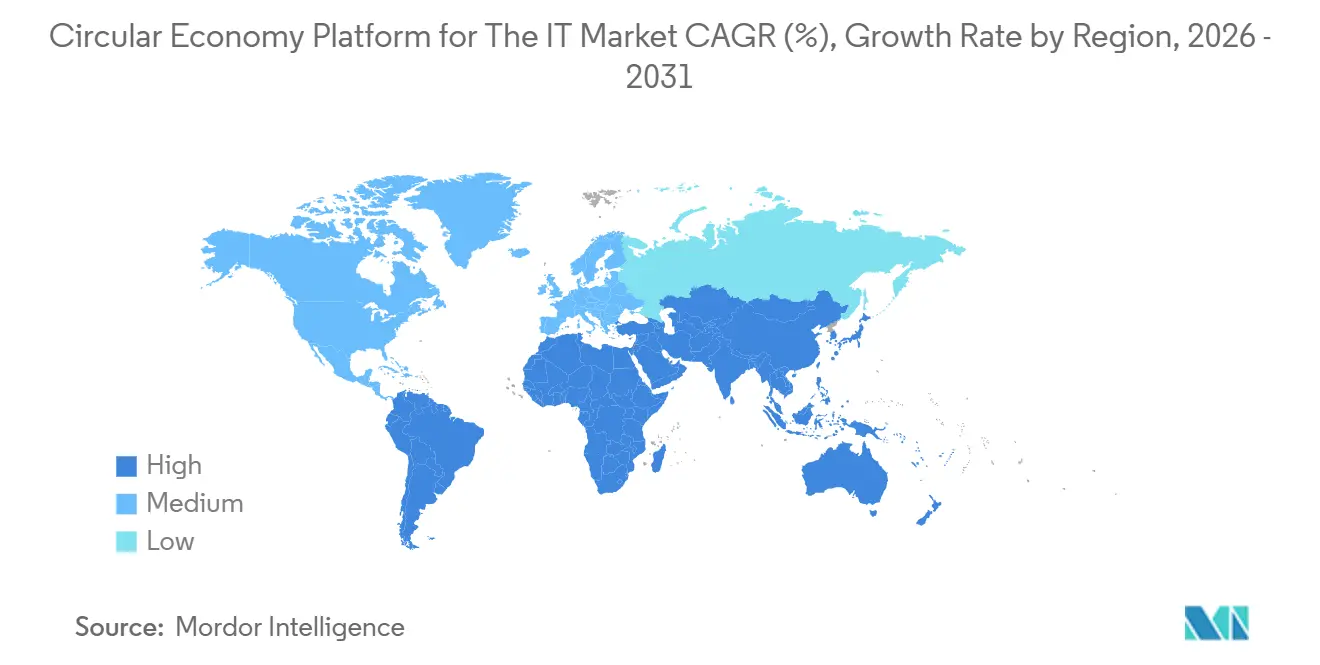

- By geography, Europe held 34.56% share in 2025, while Asia-Pacific is projected to expand at a 13.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Circular Economy Platform For The IT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Demand for IT Asset Traceability | +3.2% | Global | Medium term (2-4 years) |

| Regulatory Pressure on E-Waste Reporting and Audits | +2.8% | North America and EU, spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Expansion of Secure Data Sanitization Requirements | +2.1% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Corporate ESG Targets Driving Circular Procurement | +1.9% | North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| AI-Enabled Asset Grading and Refurbishment Workflows | +1.5% | North America and Asia-Pacific core | Medium term (2-4 years) |

| Multi-Vendor Fleet Complexity Increasing Platform Adoption | +1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Demand for IT Asset Traceability

The circular economy platform for the IT market is seeing its strongest push from the need to track assets from deployment through data erasure and final disposition. Large enterprises with multi-site and multi-vendor estates cannot demonstrate compliance, ESG performance, or Scope 3 accountability when records are scattered across spreadsheets and disconnected service providers. One provider reported repurposing 8.8 million IT assets in FY2025, a scale that underscores the importance of consistent traceability as decommissioning moves across regions and device classes. Another platform positioned serialized asset discovery and parent-child relationship mapping across servers and drives to automate visibility, reflecting how traceability has become a core product differentiator rather than a background feature. When that level of visibility is in place, enterprises can treat retired hardware as a measurable recovery stream rather than a disposal cost line, which changes how procurement teams value platform adoption.

Regulatory Pressure on E-Waste Reporting and Audits

The circular economy platform for the IT market is also moving higher because e-waste reporting and audit rules are becoming more detailed across major economies. In July 2025, it was reported that nearly half of WEEE generated in the EU remained uncollected, only 40% was recycled, and just 23% of recycling facilities applied high-quality treatment standards, which is increasing pressure for tighter oversight.[1]European Commission, “New Evaluation Looks at How to Improve WEEE Directive,” European Commission, environment.ec.europa.euItaly brought Directive (EU) 2024/884 into national law with effect from January 2026, which changed parts of the WEEE framework and financing responsibilities under extended producer responsibility. Germany’s system continues to require recurring producer reporting, and Regulation (EU) 2025/40 will apply from August 2026, meaning many enterprises now face overlapping documentation duties across jurisdictions. These layered timelines are increasing the demand for software and managed workflows that can keep reporting, registration, and audit records aligned without manual reconciliation.

Expansion of Secure Data Sanitization Requirements

The circular economy platform for the IT market is getting another boost from stricter rules on secure media sanitization. NIST issued SP 800-88 Rev. 2 in September 2025 as the first major update in more than a decade, adding clearer requirements for SSDs, NVMe drives, M.2 media, and virtual machine environments, and setting an 18-month federal transition window through March 2027.[2]National Institute of Standards and Technology, “Guidelines for Media Sanitization,” National Institute of Standards and Technology, nist.gov The update also shifted attention from device-level techniques to program-level controls and documentation, thereby increasing the compliance burden for organizations handling regulated end-of-life assets. GDPR Article 17 and PCI DSS v4.0.1 both reinforce the need for verifiable erasure in environments that process personal or payment data, which broadens the number of enterprises that need auditable sanitization records. ITU-T Recommendation L.1081 added a parallel reference point in July 2025 for end-of-life ICT device sanitization, further supporting platforms that can issue serialized destruction certificates and maintain defensible chain-of-custody records.

Corporate ESG Targets Driving Circular Procurement

The circular economy platform for the IT market is also benefiting from the fact that sustainability goals are now being applied to IT hardware programs with clearer operating targets. It was reported that 88.1% of operational waste was diverted and that 90.9% of servers and components were reused or recycled in FY2024, demonstrating that circular hardware practices are being measured as part of wider emissions accountability.[3]Microsoft, “Environmental Sustainability Report 2025,” Microsoft, microsoft.com In August 2025, a new subscription service was launched across 49 markets, combining carbon reporting, certified refurbished procurement, CO₂ offset services, and asset recovery into a single offering. Another provider processed 721,000 electronic devices for recycling and reuse in 2025, providing buyers with a visible benchmark for what scaled circular execution can look like in practice. As these programs mature, procurement teams are increasingly treating circular credentials as a supplier filter, as asset-level records now support both cost control and sustainability reporting in a single workflow.[4]Lenovo, “Lenovo Launches Modular DaaS for Sustainability to Manage Carbon, Reduce IT Costs, and Boost ROI,” Lenovo, lenovo.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Asset Data Across Legacy IT Environments | -1.8% | Global | Medium term (2-4 years) |

| Limited Standardization Across Global Take-Back Programs | -1.4% | Global | Long term (≥ 4 years) |

| Trust Gaps Around Data Destruction and Chain of Custody | -1.1% | Global | Medium term (2-4 years) |

| Channel Conflict With Incumbent ITAD and Resale Partners | -0.8% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Asset Data Across Legacy IT Environments

The circular economy platform for the IT market still faces a major operational barrier: many enterprises lack clean, unified records of their installed hardware base. Serial numbers, ownership history, location data, and end-of-life status often reside across different ERP, ITAM, and regional systems, which slows onboarding and increases its cost. The issue is most visible in large organizations that expanded through acquisitions or system migrations, because they often need a discovery project before disposition workflows can even start. One provider’s asset discovery layer was built to reconcile serial-level gaps between what is found in the field and what appears in client inventory systems, which shows how common this problem remains. Until upstream data quality improves, many buyers will continue to face an integration burden that delays value realization and limits platform usage after deployment

Limited Standardization Across Global Take-Back Programs

The circular economy platform for the IT market also slows when enterprises try to run a take-back model across multiple countries and meet very different compliance rules. Implementation and enforcement across WEEE schemes has remained fragmented, especially for online sellers and cross-border flows, and only Bulgaria, Latvia, and Slovakia met the 65% collection target in 2022. Outside Europe, enterprises still have to work across different certification and documentation expectations, including local regulatory approvals and recovery standards that do not align well with each other. This makes global programs harder to standardize, giving larger providers with local compliance expertise an advantage over smaller domestic operators. Even if rules become more aligned over time, the current patchwork will continue to slow rollout speed in emerging and frontier markets over the next few years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Anchor Revenue While Services Gain Momentum

Software platforms accounted for 68.74% of the circular economy platform share in the IT market in 2025, indicating that enterprises favored centralized systems that could tie together asset discovery, data erasure records, disposition routing, and ESG documentation. The market moved in this direction because manual processes and separate recycling engagements did not produce the serialized records required to meet current compliance expectations. As GDPR, WEEE, and related disclosure requirements demand clearer asset-level documentation, software-based control layers have become the simplest way to create a usable audit trail at scale. Buyers also value the ability to view device status, certificates, and recovery outcomes in one place, especially when hardware is spread across multiple business units and countries. This keeps software platforms at the center of the commercial model even when service delivery still happens through physical collection, repair, and remarketing operations.

Services are the fastest-growing offering type, and the circular economy platform for the IT market size for this segment is projected to expand at a 12.85% CAGR from 2026 to 2031. Enterprises are turning to managed service models when they lack internal ITAD expertise or when decommissioning cycles are becoming harder to manage due to AI server refresh activity. The installed base of AI servers has been identified as a major future ITAD challenge, underscoring the need for providers that can manage secure removal, grading, and recovery as an ongoing service. Service providers with recognized security and recycling credentials are also winning more enterprise tenders because buyers want a single accountable party for chain of custody, documentation, and jurisdiction-specific reporting.

By Deployment Model: Cloud Leads While Hybrid Adoption Builds In Regulated Environments

Cloud held a 65.12% share in 2025, reflecting the appeal of lower upfront infrastructure costs and faster rollouts across distributed locations. The circular economy platform for the IT market adopted a cloud-first approach because many organizations wanted real-time asset tracking, automated reporting, and multi-site visibility without expanding their internal IT stacks. These benefits were especially relevant for mid-sized companies and newer technology businesses that needed structure but did not want to run an on-premises platform. At the same time, a full public cloud deployment does not suit every workflow because asset records, sanitization proofs, and customer data often reside in regulated environments. This is why deployment choice is increasingly shaped by compliance and data-handling needs rather than by pure architectural preference.

Hybrid is the fastest-growing deployment model, and the circular-economy platform for the IT market in this segment is projected to expand at a 12.92% CAGR from 2026 to 2031. Updated standards reinforced the need for program-level documentation and stronger operational controls, making hybrid deployment more suitable for organizations that need local control over sensitive records while still using cloud layers for reporting and partner coordination. Europe adds another pull factor because cross-border compliance and data management rules remain stricter, and China has also moved toward tighter controls through its national standard on electronic product information clearance. As a result, hybrid design is becoming the practical default for enterprise buyers that operate across regulated sectors or multiple jurisdictions.

By Enterprise Size: Large Enterprises Lead While SMEs Open A Wider Adoption Base

Large enterprises accounted for a 63.45% share in 2025, reflecting their broader hardware estates, formal IT asset management structures, and stronger internal reporting requirements. The circular economy platform for the IT market was first developed around these buyers because they had sufficient device volume, geographic spread, and compliance exposure to justify structured platforms. It was reported that approximately 24 Fortune 1000 customers were added in Q1 2026, indicating that many large organizations are still early in their adoption path. This leaves room for deeper cross-sell as companies move from one-time decommissioning work to broader programs covering reuse, recovery, and reporting.

SMEs are the fastest-growing segment of enterprises, with a 12.78% CAGR projected through 2031. The circular economy platform for the IT market is becoming more accessible to smaller firms because as-a-service delivery removes much of the upfront capital commitment and reduces the minimum scale needed to access secure erasure, reporting, and recovery workflows. A subscription model was launched with no upfront capital requirement, which lowers the entry barrier for organizations that could not previously run formal circular IT programs. Smaller firms are also being pulled into adoption by customer expectations, as large buyers increasingly ask suppliers to document asset-disposal practices as part of wider sustainability and governance reviews. That indirect pressure means SME demand is not driven solely by regulation; supply chain relationships with larger enterprise customers also shape it.

By Circular Economy Application: Asset Reuse Leads While ESG Reporting Expands Fastest

Asset reuse and redeployment accounted for the largest application share at 27.41% in 2025, reflecting the direct financial benefit of extending the life of servers, laptops, and networking equipment before new procurement is approved. This use case has shaped the circular economy platform for the IT market because reuse produces both cost savings and lower disposal volumes, which makes the value case easier for finance and sustainability teams to support. Refurbishment, ITAD, and recycling continue to matter because each step supports compliant hardware handling, but reuse remains the most immediate lever for controlling spend and reducing waste. ESG and compliance reporting is the fastest-growing application area, with a 13.05% CAGR projected through 2031, as buyer expectations shift from summary estimates to asset-level evidence. Partnerships that enable material-level fingerprinting and critical mineral reporting are moving closer to operational workflows, which support the growth of platforms that connect disposition events with auditable sustainability records.

The circular economy platform for the IT market is also being influenced by stronger economics in parts recovery and secondary resale. DDR4 memory prices surged 461.9% year on year in H1 FY2026, making component recovery a much more meaningful earnings driver for ITAD activity tied to retired data center hardware. At the same time, evaluations of WEEE schemes identified missed opportunities for critical raw material recovery, suggesting that recycling and recovery requirements will receive greater attention in future rule updates. Providers that can document device condition, parts value, and material content in a single workflow will be better positioned as reporting and recovery obligations deepen.

Geography Analysis

Europe accounted for 34.56% of the circular economy platform for the IT market share in 2025, maintaining its position as the largest regional market. The circular economy platform for the IT market is strongest in Europe because the region combines WEEE, broader sustainability disclosure pressures, and tighter producer accountability within a single operating environment. A July 2025 evaluation found that collection and treatment results still fall short of policy goals, and that gap reinforces the case for tighter controls and better reporting systems. Italy’s January 2026 transposition of Directive (EU) 2024/884 and Germany’s reporting framework add country-level administrative pressure on top of the wider EU framework. This combination keeps Europe ahead because enterprises in the region have fewer practical ways to manage end-of-life IT assets without formal platform support.

North America remained the second-largest region, supported by federal procurement requirements, enterprise decommissioning demand, and stronger media sanitization expectations. The circular economy platform for the IT market in the United States is also being lifted by the updated NIST sanitization framework and by faster hardware turnover in hyperscale data centers. Asset lifecycle management revenue reached USD 232 million in Q1 2026, up 92% year on year, with organic data center decommissioning growth exceeding 100%, demonstrating how quickly enterprise and hyperscaler activity is scaling in the region. South America remains smaller and less standardized, but demand is growing as enterprises lean more heavily on refurbishment, redeployment, and controlled disposal to extend hardware value under tighter budgets.

Asia-Pacific is the fastest-growing region, and the circular economy platform for the IT market size there is projected to grow at a 13.12% CAGR through 2031. The market is expanding quickly across Asia-Pacific, but the drivers differ by country: Japan is building stronger commercial partnerships, China is tightening clearance and information-handling standards, and India is attracting new processing capacity. A mandatory national standard published in December 2025 for electronic product information clearance adds a clear compliance trigger for enterprise sanitization and disposal workflows in China. In Japan, a capital and business alliance signed in April 2026 is building a circular tech value chain spanning procurement, third-party maintenance, remarketing, and ITAD. India, Australia, and South Korea remain earlier in their adoption curves, while the Middle East and Africa are still nascent, with demand centered on smart-city, digital infrastructure, and data-center modernization programs in markets such as Saudi Arabia and the UAE.

Competitive Landscape

The circular economy platform for the IT market has a concentrated top tier, but the broader field remains fragmented across regional operators and specialist service firms. The market, therefore, remains open to consolidation because larger players can add compliance depth, logistics reach, and software capability more quickly through acquisitions than through greenfield expansion. One example is the completion of acquisitions in 2024, followed by continued tuck-in deals in 2026, showing how expansion models are being built around integration. That strategy matters because smaller operators often have strong local collections but limited ability to support multi-country audit, recovery, and reporting requirements. As enterprise buyers look for fewer vendors and more consistent controls, scaled platforms are better placed to win complex mandates.

The market is also separating leaders from followers based on technical capability, not just geographic reach. Advanced recovery capacity is being built, including new facilities with automation and robotics designed for DDR4 and DDR5 memory processing. That kind of infrastructure is important because AI-grade servers, dense memory systems, and newer data center hardware require more specialized grading and recovery than standard office devices. Providers that can recover more value from components are less exposed to pure price competition and can defend stronger margins over time.

The market is also being shaped by companies that bundle circular services into broader enterprise technology offers. Subscription models that combine refurbished procurement, carbon reporting, and asset recovery within one structure are easier for large organizations to adopt at scale. Compliance thresholds are also rising, and requirements linked to updated sanitization standards, WEEE reporting, and recognized recycling credentials are making it harder for under-certified operators to qualify for enterprise programs. This means competitive advantage is increasingly tied to trust, documentation, and operational consistency rather than to basic collection capacity alone.

Circular Economy Platform For The IT Industry Leaders

Sims Lifecycle Services, Inc.

Electronic Recyclers International, Inc.

Iron Mountain Incorporated

Apto Solutions, Inc.

TES-Amm (Singapore) Pte Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Iron Mountain reported Q1 2026 Asset Lifecycle Management revenue of USD 232 million, up 92% year-on-year (organic growth 77%), with data center decommissioning growing organically above 100%. The company raised its full-year 2026 ALM revenue guidance to USD 950 million and signed a new multi-year agreement naming it the sole ALM provider in more than 30 countries for a global advertising conglomerate, encompassing enterprise IT decommissioning and remarketing.

- April 2026: Get-IT Co., Ltd. (Japan) and Itochu Corporation signed a capital and business alliance to build a "Circular Tech Value Chain" integrating IT hardware procurement, third-party maintenance, remarketing, and ITAD. The partnership leverages Itochu's global network, including prior investments in Belong and Electronic Recyclers International, with Get-IT's 25 years of IT asset circular economy expertise.

- March 2026: Sims Lifecycle Services held an Investor Day announcing plans for a new 11,000 m² Ireland Circular Center, backed by a 10-year lease, with operations starting July 2026. The facility targets hyperscaler customers in Europe, projecting 4 million Memory GB sold capacity in FY27, with automation and robotics infrastructure designed to process both DDR4 and DDR5 memory.

- February 2026: Sims Limited reported H1 FY2026 results, ending December 31, 2025, Sims Lifecycle Services revenue rose 69.9% to AUD 327.4 million (USD 209 million at 2025 average exchange rates per IRS yearly average currency rates), and underlying EBIT grew 247.5% to AUD 49.0 million (USD 31 million). DDR4 memory prices surged 461.9% year-on-year, converting ITAD component recovery into a primary earnings driver.

Global Circular Economy Platform For The IT Market Report Scope

The Circular Economy Platform for the IT market refers to software platforms and services that enable organizations to manage IT assets through circular economy principles, focusing on reuse, refurbishment, recycling, and responsible disposal. These solutions provide functionalities such as asset reuse and redeployment planning, refurbishment tracking, IT asset disposition (ITAD), recycling and recovery management, and ESG compliance reporting. By embedding sustainability intelligence into IT asset lifecycle management, these platforms help enterprises reduce e-waste, extend asset lifespans, optimize resource utilization, and align IT operations with ESG and decarbonization goals.

The Circular Economy Platform for the IT market report is segmented by Offering (Software Platform, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Circular Economy Application (Asset Reuse and Redeployment, Refurbishment, ITAD, Recycling and Recovery, and ESG and Compliance Reporting), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Platform |

| Services |

| Cloud |

| On Premises |

| Hybrid |

| Large Enterprises |

| Small And Medium Enterprises |

| Asset Reuse and Redeployment |

| Refurbishment |

| ITAD |

| Recycling and Recovery |

| ESG and Compliance Reporting |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Software Platform | ||

| Services | |||

| By Deployment Model | Cloud | ||

| On Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium Enterprises | |||

| By Circular Economy Application | Asset Reuse and Redeployment | ||

| Refurbishment | |||

| ITAD | |||

| Recycling and Recovery | |||

| ESG and Compliance Reporting | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size outlook for the circular economy platform for the IT market?

The circular economy platform for IT market stood at USD 4.23 billion in 2025, is valued at USD 4.69 billion in 2026, and is forecast to reach USD 8.39 billion by 2031 at a 12.34% CAGR.

Which region leads global demand for circular IT platforms?

Europe led in 2025 with a 34.56% share, supported by stricter e-waste, reporting, and producer responsibility rules across the region.

Which offering type generates the most revenue?

Software platforms led the mix in 2025 with a 68.74% share because enterprises need centralized records for asset tracking, data sanitization, and reporting.

Why is hybrid deployment gaining traction?

Hybrid is projected to grow at a 12.92% CAGR through 2031 because regulated sectors often need local control over sensitive records while still using cloud-based reporting and partner coordination.

What application area is growing the fastest?

ESG and compliance reporting is projected to expand at a 13.05% CAGR through 2031 as enterprises move from broad sustainability estimates to asset-level documentation.

Which customer group is expanding fastest?

SMEs are projected to grow at a 12.78% CAGR through 2031 as subscription delivery models reduce upfront cost and make certified circular workflows easier to adopt.

Page last updated on: