Autonomous IT Operations Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

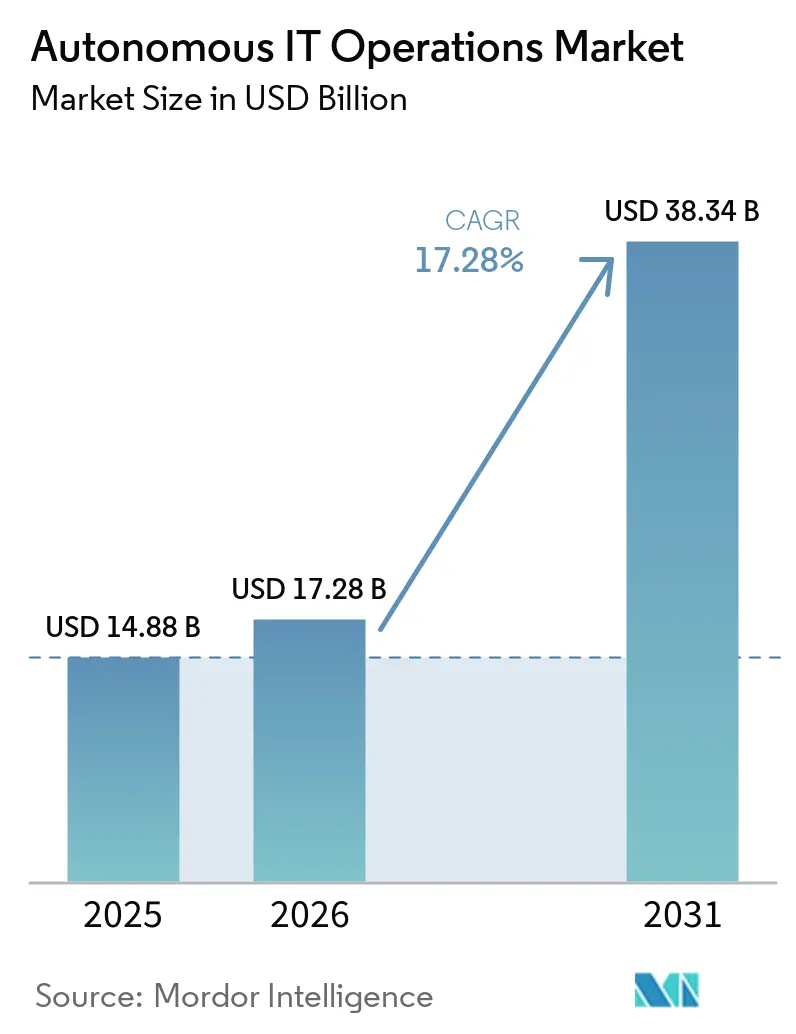

| Market Size (2026) | USD 17.28 Billion |

| Market Size (2031) | USD 38.34 Billion |

| Growth Rate (2026 - 2031) | 17.28% CAGR |

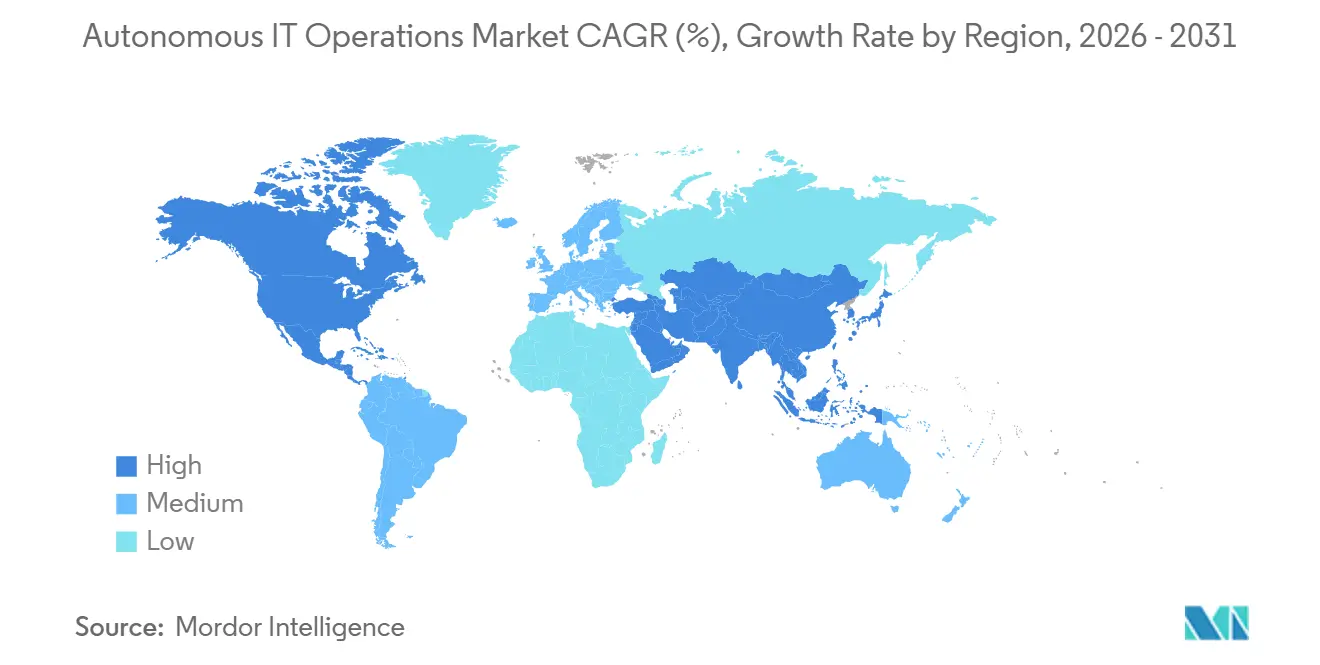

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous IT Operations Market Analysis by Mordor Intelligence

The autonomous IT operations market size is expected to grow from USD 14.88 billion in 2025 to USD 17.28 billion in 2026 and is forecast to reach USD 38.34 billion by 2031 at 17.28% CAGR over 2026-2031. Enterprises are replacing reactive ticket queues with predictive, self-healing workflows that shorten mean time to resolution, absorb soaring telemetry volumes, and cut downtime costs. Data-sovereignty mandates are fragmenting deployment topologies, pushing correlation engines to the edge in jurisdictions that restrict cross-border data flows. Generative AI copilots are lowering the skill threshold for observability, yet a shortage of professionals fluent in both legacy ITSM frameworks and cloud-native stacks continues to slow adoption. Platform consolidation remains a priority as organizations migrate from siloed point tools to unified engines that ingest logs, metrics, traces, and events, while vendor lock-in concerns are encouraging demand for OpenTelemetry compatibility.

Key Report Takeaways

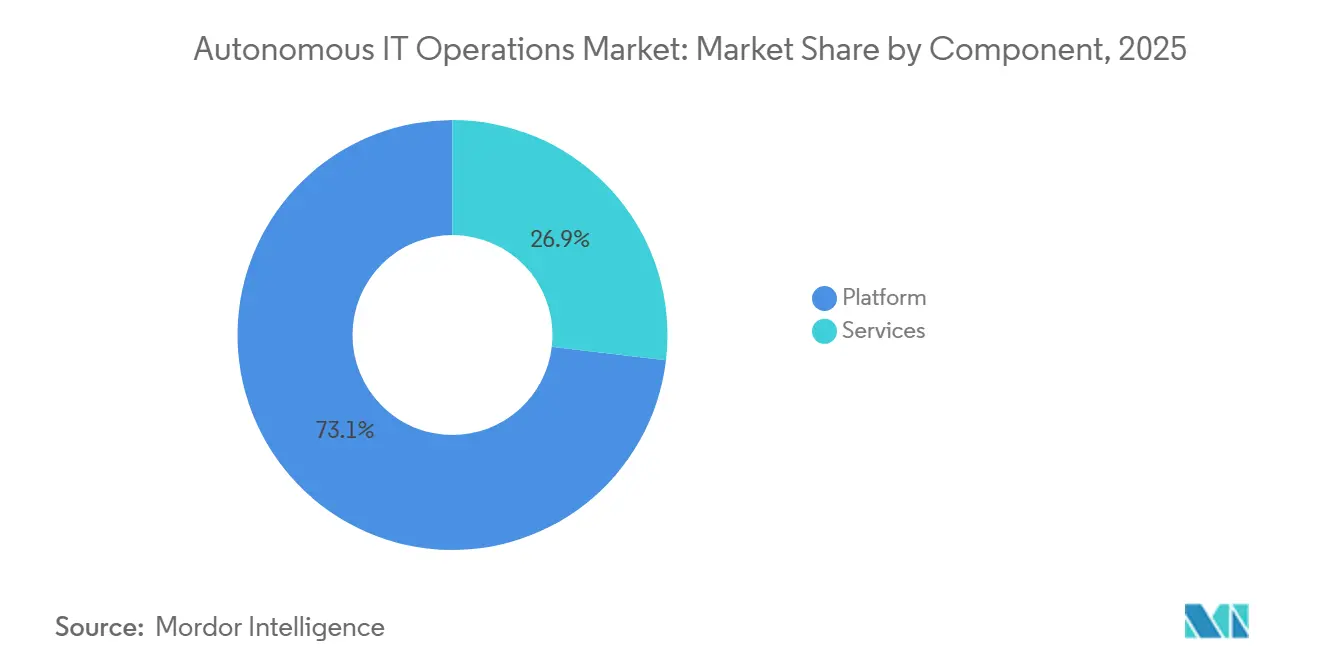

- By component, platforms captured 73.12% of the autonomous IT operations market share in 2025, while services are projected to expand at an 18.28% CAGR between 2026 and 2031.

- By deployment mode, on-premises installations accounted for 52.24% of the autonomous IT operations market in 2025, whereas cloud deployments are forecast to grow at a 17.88% CAGR through 2031.

- By organization size, large enterprises commanded 66.13% revenue share in 2025, while SMEs are advancing at a 17.68% CAGR from 2026 to 2031.

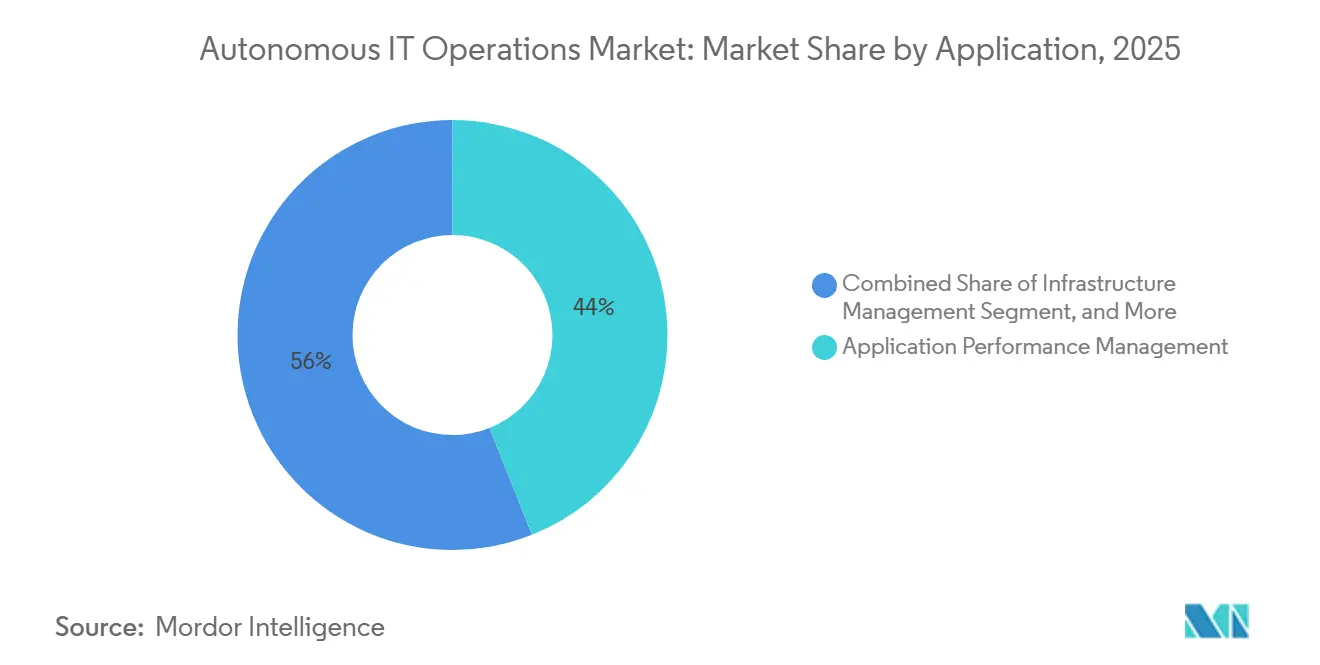

- By application, application performance management led with 43.98% of the autonomous IT operations market share in 2025; infrastructure management is the fastest mover, rising at an 18.42% CAGR to 2031.

- By industry vertical, IT and telecom accounted for 37.51% of revenue in 2025, whereas healthcare and life sciences are set to grow at an 18.68% CAGR over the forecast period.

- By geography, North America accounted for 32.78% of market revenue in 2025, yet Asia-Pacific is expected to register the highest regional CAGR at 19.21% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autonomous IT Operations Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of IT Telemetry Volumes Driving AI Correlation | +4.2% | Global, with peak intensity in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Adoption of Hybrid and Multi-Cloud Architectures | +3.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Need to Reduce Mean Time to Resolution and Downtime Costs | +3.5% | Global, acute in BFSI and healthcare verticals | Short term (≤ 2 years) |

| Generative AI Copilots Improving AIOps Usability | +3.1% | North America and Europe early, Asia-Pacific following | Medium term (2-4 years) |

| Data-Sovereignty Rules Fueling Autonomous Edge Operations | +1.9% | Europe, Middle East, select Asia-Pacific markets | Long term (≥ 4 years) |

| ESG-Linked Green Ops Mandates for Energy Optimisation | +1.2% | Europe and North America, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of IT Telemetry Volumes Driving AI Correlation

Cloud-native microservices generate thousands of events per transaction, creating petabyte-scale observability pipelines that overwhelm traditional rules-based monitoring systems. These pipelines produce an immense volume of data that is challenging to manage and analyze effectively using conventional methods. To address this, AI-driven correlation engines have emerged as a critical solution, capable of condensing this overwhelming data torrent into actionable root-cause insights within seconds. These advanced platforms are designed to process trillions of dependencies daily, ensuring rapid identification and resolution of issues. For instance, retail and e-commerce operators increasingly rely on these AI-powered engines to anticipate and mitigate latency spikes during high-demand periods, such as seasonal sales peaks.[1] Dynatrace Product Blog, “How Davis AI Correlates Trillions of Dependencies,” Dynatrace.com By transitioning from reactive alerting to predictive remediation, businesses can enhance operational efficiency, improve customer experiences, and maintain seamless service delivery during critical times.

Rising Adoption of Hybrid and Multi-Cloud Architectures

Workloads span on-premise data centers, public clouds, and edge locations, creating significant visibility gaps that manual runbooks and traditional monitoring tools cannot effectively bridge. These gaps arise from the complexity and diversity of modern IT environments, where workloads run across multiple platforms and infrastructures. Autonomous IT operations platforms address this challenge by federating telemetry across heterogeneous estates, enabling seamless, unified policy enforcement regardless of workload location. This capability ensures consistent management and compliance across all environments, whether on-premise, in the cloud, or at the edge. Additionally, sovereign-cloud initiatives in regions such as Europe and the Middle East are driving the adoption of autonomous edge operations.[2]European Commission, “Regulatory Framework on AI,” digital-strategy.ec.europa.eu These initiatives prioritize data sovereignty and security, encouraging the implementation of edge solutions that minimize data egress while maintaining operational efficiency and compliance with regional regulations.

Need to Reduce Mean Time to Resolution and Downtime Costs

Unplanned outages can result in significant financial losses, often costing thousands of dollars per minute for industries operating under strict regulations. Autonomous remediation systems address this challenge by executing pre-approved playbooks immediately after detecting anomalies. This approach eliminates the need for manual triage, significantly reducing downtime and ensuring faster recovery. For instance, public-sector pilot programs in the United States demonstrated the effectiveness of this technology by reducing resolution times for critical infrastructure incidents by 60%. These results highlight the cost-efficiency and operational benefits of adopting automated incident response solutions.

Generative AI Copilots Improving AIOps Usability

Early AIOps tools were constrained by the need for domain-specific query languages, limiting their usability to specialists with advanced technical expertise. However, the integration of large language models has significantly enhanced accessibility by enabling operators to ask natural-language questions and receive detailed causal graphs along with actionable remediation steps. Additionally, the introduction of low-code interfaces has further expanded the adoption of AIOps tools, particularly among small and medium-sized enterprises (SMEs) that often lack dedicated site-reliability engineering teams. These advancements have made AIOps solutions more user-friendly and accessible to a broader range of organizations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy IT Stacks | -2.1% | Global, acute in manufacturing and government sectors | Short term (≤ 2 years) |

| Shortage of AIOps-Skilled Professionals | -1.8% | Global, most severe in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| AI Model Auditability under Emerging Regulations | -1.3% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Vendor Lock-In from Proprietary Correlation Engines | -0.9% | Global, particularly impacting large enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy IT Stacks

Mainframes, proprietary databases, and custom middleware often lack modern instrumentation, which forces enterprises to deploy additional agents to enable monitoring and data collection. These agents, however, increase latency and add to maintenance costs, creating operational inefficiencies. In brownfield environments, where legacy systems dominate, adoption cycles for modern solutions can extend beyond a year. This delay occurs as teams work to retrofit telemetry connectors, integrate legacy systems, and normalize disparate data formats to ensure compatibility. Vendors offering hybrid discovery engines provide a solution to these challenges. These engines can map SNMP-based devices alongside Kubernetes clusters, streamlining the process by automating asset discovery and reducing manual effort during integration.

Shortage of AIOps-Skilled Professionals

The convergence of machine learning and distributed systems has created a significant demand for specialized expertise, which remains in short supply. Job postings for AIOps engineers, who are critical to managing and optimizing these advanced systems, tend to remain unfilled for much longer than for traditional IT roles. This talent gap has prompted vendors to introduce managed services and low-code playbooks, enabling organizations to adopt AIOps solutions without requiring extensive in-house expertise. In response to this growing demand, governments in countries such as India and Singapore have initiated training programs to expand the talent pool in this domain. However, despite these efforts, the demand for skilled professionals continues to exceed the available supply, creating ongoing challenges for the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Anchor Revenue, Services Accelerate

The platform segment accounted for 73.12% of the autonomous IT operations market share in 2025, as organizations consolidated point tools into unified engines capable of ingesting logs, metrics, traces, and events. The services segment is gaining momentum, driven by advisory, integration, and managed-operations packages that simplify complex deployments. During 2026-2031, services are projected to outpace platforms at 18.28% CAGR as enterprises seek faster time-to-value through external expertise. Vendors increasingly bundle platform licenses with managed services, shortening procurement cycles and smoothing consumption spikes.

The growing demand for continuous optimization is reshaping maintenance contracts into proactive engagements in which vendors retune correlation algorithms based on seasonal traffic patterns. Cross-selling opportunities have multiplied since large infrastructure providers integrated AIOps into existing estates, reinforcing platform stickiness while boosting services revenue. Consultant-led telemetry design has become pivotal for brownfield manufacturers and public agencies looking to modernize without disrupting mission-critical workloads.

By Deployment Mode: Cloud Gains as Hybrid Architectures Mature

On-premises installations accounted for the majority of the autonomous IT operations market share, at 52.24%, in 2025, due to strict data-residency and compliance requirements in healthcare and financial services. These industries prioritize on-premises solutions to ensure sensitive data remains within controlled environments and to adhere to stringent regulatory frameworks. Cloud deployments, however, are forecast to expand at a compound annual growth rate (CAGR) of 17.88% through 2031, as small and medium-sized enterprises (SMEs) increasingly adopt subscription-based models that eliminate the need for significant upfront capital expenditure. This shift allows SMEs to access advanced IT operations capabilities without the financial burden of maintaining physical infrastructure. Hybrid topologies are emerging as a preferred solution, enabling organizations to keep sensitive correlation workloads on-premises while leveraging the scalability and cost-efficiency of public cloud platforms for burst analytics.

Edge computing introduces an additional layer to this ecosystem by embedding lightweight correlation engines within operational environments such as factories and retail stores, where ultra-low latency, often measured in milliseconds, is critical for real-time decision-making. Recent platform updates that incorporate tiered storage solutions, storing hot data locally for immediate access and warm data in cloud object stores for cost efficiency, are helping organizations optimize both performance and expenses.[3]Elastic Technical Brief, “Tiered Storage for Edge Observability,” Elastic.co Furthermore, certification frameworks like ISO/IEC 27001 are increasingly expanding their coverage to encompass entire hybrid estates, encouraging businesses to adopt a unified security approach across on-premises, cloud, and edge environments. This holistic view ensures that organizations can maintain robust security standards while benefiting from the flexibility and scalability of hybrid and edge computing solutions.

By Organization Size: SMEs Embrace Consumption Models

Large enterprises accounted for 66.13% of the autonomous IT operations market in 2025, as their scale enables the amortization of multi-million-dollar platform investments. These organizations often have the resources to implement complex systems and integrate them into their existing IT infrastructure, ensuring seamless operations and compliance with industry standards. SMEs, constrained by limited capital and talent, prefer SaaS-native offerings with self-service onboarding and pay-as-you-grow tariffs. These solutions allow smaller businesses to access advanced IT operations capabilities without the need for significant upfront investments, making them an attractive option for cost-conscious organizations. They are projected to post a 17.68% CAGR from 2026-2031, narrowing the gap as vendor pricing aligns better with mid-market budgets and as SMEs increasingly recognize the value of automation in improving efficiency and reducing operational costs.

Investor interest confirms this shift is significant, as late-stage funding flowed to providers that streamline deployment for sub-100-employee customers. For SMEs, low-code workflow builders and pre-integrated connectors to popular developer tools shrink implementation from months to weeks, enabling faster time-to-value and reducing the burden on internal IT teams. Meanwhile, large organizations negotiate bespoke enterprise agreements that combine licenses, professional services, and governance features to satisfy audit requirements. These agreements often include tailored support and advanced security features, enabling large enterprises to maintain compliance and operational excellence while leveraging the full potential of autonomous IT operations platforms.

By Application: Infrastructure Management Gains Momentum

Application performance management maintained 43.98% of the autonomous IT operations market share in 2025, reflecting its early maturity in distributed tracing and user-experience monitoring. This segment has been a key driver of market growth, providing real-time insights into application behavior and end-user interactions to ensure optimal performance and customer satisfaction. However, infrastructure management is advancing at an 18.42% CAGR as operators increasingly extend autonomous remediation capabilities into compute, storage, and network fabrics. The autonomous IT operations market for infrastructure roles is expected to accelerate further as correlation engines evolve to integrate hypervisor, container, and bare-metal telemetry, enabling the prediction of resource contention before it cascades into larger issues.

Convergence with IT service management is significantly reshaping workflows. Generative AI now plays a pivotal role by drafting detailed root-cause reports and automatically closing incidents when self-healing scripts successfully resolve issues. This integration enhances operational efficiency and reduces manual intervention. Security and networking teams are also benefiting from these advancements, as zero-trust segmentation introduces granular flow data into systems, providing fresh and detailed context for root-cause isolation. Additionally, streaming analytics powered by technologies such as Apache Kafka and Flink has become a standard feature, enabling sub-second anomaly detection for mission-critical workloads.[4]Splunk Engineering Blog, “Streaming Analytics with Flink,” Splunk.com These innovations are driving the adoption of autonomous IT operations across industries, ensuring faster response times and improved system reliability.

By Industry Vertical: Healthcare Accelerates Amid Digital Transformation

IT and telecom organizations retained 37.51% revenue share in 2025, driven by their early adoption of DevOps practices and cloud-native architectures, which have enabled them to streamline operations and enhance scalability. The healthcare and life sciences sector is projected to grow at the fastest rate, with an 18.68% CAGR, as hospitals increasingly demand zero-downtime electronic health records, advanced clinical decision support systems, and reliable medical IoT uptime to ensure seamless patient care and operational efficiency. Banking and insurance industries are prioritizing millisecond-level reliability for payment rails to meet customer expectations and regulatory requirements, while the retail sector is leveraging predictive autoscaling to prepare for demand surges during holiday shopping peaks.

In the manufacturing sector, autonomous IT operations are being extended into operational technology, where correlating PLC telemetry with IT events enables predictive maintenance and reduces downtime. Public-sector agencies, often operating under tight budget constraints, are adopting autonomous workflows to optimize resource allocation, allowing staff to focus on strategic initiatives while maintaining uninterrupted citizen services. The expanding adoption across various verticals highlights how autonomous remediation is evolving beyond digitally native enterprises, becoming a critical component for organizations across diverse industries to enhance efficiency and resilience.

Geography Analysis

North America accounted for 32.78% of the autonomous IT operations market share in 2025, driven by the region's high concentration of hyperscalers and a robust DevOps talent pool. The United States leads the market with its advanced IT infrastructure and widespread adoption of automation technologies. Meanwhile, Canada’s focus on digital transformation and Mexico’s growing reliance on cloud platforms for operational efficiency further bolsters the region’s dominance. Despite this, the Asia-Pacific region is expected to be the fastest-growing region, with a projected CAGR of 19.21%. Countries like China, India, and those in Southeast Asia are bypassing legacy systems and adopting greenfield cloud builds. In China, stringent data-localization laws are pushing domestic vendors to develop solutions optimized for sovereign clouds, while India’s IT services giants are integrating AIOps into their managed services portfolios to enhance operational efficiency.

Europe’s growth in the autonomous IT operations market remains steady, supported by strict regulatory frameworks such as GDPR and the EU AI Act. These regulations require vendors to incorporate features such as model lineage and transparency, thereby ensuring compliance and fostering trust among enterprises. The Middle East is making significant investments in smart-city platforms, which rely heavily on autonomous IT operations to maintain stringent service-level objectives. Similarly, South America is witnessing modernization in its telecom networks, with AIOps being adopted to manage the complexities of 5G network slicing. These advancements are enabling the region to improve network efficiency and reduce operational costs.

Africa, while still in the early stages of adopting autonomous IT operations, has considerable growth potential. The region’s mobile operators are increasingly automating their extensive tower estates, which often span remote and underserved areas, to minimize the need for on-site staff. This shift toward automation is expected to address operational challenges and improve service delivery in the region. As global demand for autonomous IT operations continues to rise, regionssuch ase Africa are likely to play a more significant role in the market’s future growth.

Competitive Landscape

The autonomous IT operations market is moderately fragmented, with the top five vendors accounting for approximately 45% of the total revenue in 2025. This fragmentation leaves significant opportunities for niche specialists to establish themselves in the market. Established observability providers, such as IBM, Splunk, and Dynatrace, are leveraging their existing customer bases and market presence to cross-sell advanced remediation modules. At the same time, cloud hyperscalers are integrating AIOps capabilities into their core infrastructure services, creating competitive pressure on standalone vendors to differentiate their offerings. Horizontal expansion remains a key growth strategy for many players. For example, ServiceNow’s USD 7.75 billion acquisition of Armis in 2026 enabled the company to bundle IT operations with cyber-physical asset monitoring, positioning itself as a leader in managing converged IT-OT estates.

Generative AI integration has become a fundamental requirement in the autonomous IT operations market. Vendors embedding large language models into their user interfaces are democratizing complex correlation tasks, making them more accessible to a broader range of users beyond elite Site Reliability Engineers (SREs). OpenTelemetry compatibility has emerged as a critical factor in procurement decisions, as enterprises increasingly aim to avoid vendor lock-in. However, proprietary reasoning engines continue to play a crucial role in differentiating vendors by enhancing the speed and accuracy of incident remediation. These advancements are driving innovation and competition within the market, as vendors strive to meet the evolving needs of their customers.

Edge computing represents a significant untapped opportunity within the autonomous IT operations market. Lightweight, self-contained agents capable of operating within factories or retail locations are paving the way for challengers to focus on delivering ultra-low-latency autonomous solutions. These solutions are particularly valuable in environments where real-time decision-making and minimal latency are critical. As the demand for edge computing grows, vendors that can effectively address this need are likely to gain a competitive advantage. This emerging frontier offers new avenues for growth and innovation, further shaping the trajectory of the market in the coming years.

Autonomous IT Operations Industry Leaders

IBM Corporation

Cisco Systems, Inc.

Splunk, Inc.

Dynatrace, Inc.

ServiceNow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Aisera launched its Agentic Workflow Engine, providing fully autonomous Tier-1 incident resolution by learning from historical ticket patterns.

- January 2026: ServiceNow partnered with OpenAI to embed GPT-4 into Now Assist, enabling conversational incident analysis and automated remediation suggestions.

- January 2026: ServiceNow completed the USD 7.75 billion acquisition of Armis, integrating cyber-physical asset visibility with IT operations to support converged environments.

- April 2025: SolarWinds completed privatization in a USD 4.4 billion deal, freeing resources to accelerate autonomous network management.

Global Autonomous IT Operations Market Report Scope

The Autonomous IT Operations (AIOps) Market comprises advanced platforms and services that automate, monitor, and optimize IT operations across modern enterprise environments. These solutions leverage artificial intelligence (AI), machine learning (ML), and data analytics to detect, predict, and remediate issues in IT infrastructure, applications, and networks, enabling reduced downtime, faster incident resolution, and improved operational efficiency.

The Autonomous IT Operations Market Report is Segmented by Component (Platform, Services (Advisory Services, Integration and Implementation Services, and Support and Maintenance Services)), Deployment Mode (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Application Performance Management, Infrastructure Management, Network and Security Management, Real-Time Analytics, and IT Service Management), Industry Vertical (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and eCommerce, Manufacturing, Government, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform | |

| Services | Advisory Services |

| Integration and Implementation Services | |

| Support and Maintenance Services |

| On-Premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Application Performance Management |

| Infrastructure Management |

| Network and Security Management |

| Real-Time Analytics and Event Correlation |

| IT Service Management Automation |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| Manufacturing |

| Government and Public Sector |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Platform | ||

| Services | Advisory Services | ||

| Integration and Implementation Services | |||

| Support and Maintenance Services | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application | Application Performance Management | ||

| Infrastructure Management | |||

| Network and Security Management | |||

| Real-Time Analytics and Event Correlation | |||

| IT Service Management Automation | |||

| By Industry Vertical | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and eCommerce | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is spending on autonomous IT operations expected to grow through 2031?

Market revenue is projected to rise from USD 17.28 billion in 2026 to USD 38.34 billion by 2031, reflecting a 17.28% CAGR.

Which component captures the largest share of current spending?

Platform offerings held 73.12% of 2025 revenue as enterprises sought unified correlation engines.

Why are SMEs increasingly interested in autonomous IT operations?

SaaS-native platforms with pay-as-you-grow pricing and low-code workflow builders enable SMEs to adopt without heavy capital or specialist staff.

What is driving the rapid uptake of autonomous IT operations in healthcare?

Zero-downtime requirements for electronic health records and clinical decision support push hospitals toward self-healing infrastructure that guards patient safety.

How does the EU AI Act affect vendors in this space?

The Act mandates transparency and auditability for high-risk automated systems, favoring vendors that can document model lineage and decision logic.

Which region is forecast to be the fastest growing?

Asia-Pacific is set to advance at a 19.21% CAGR from 2026-2031, fueled by large-scale cloud investments in China, India, and Southeast Asia.

Page last updated on: