Chronic Lower Back Pain (CLBP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

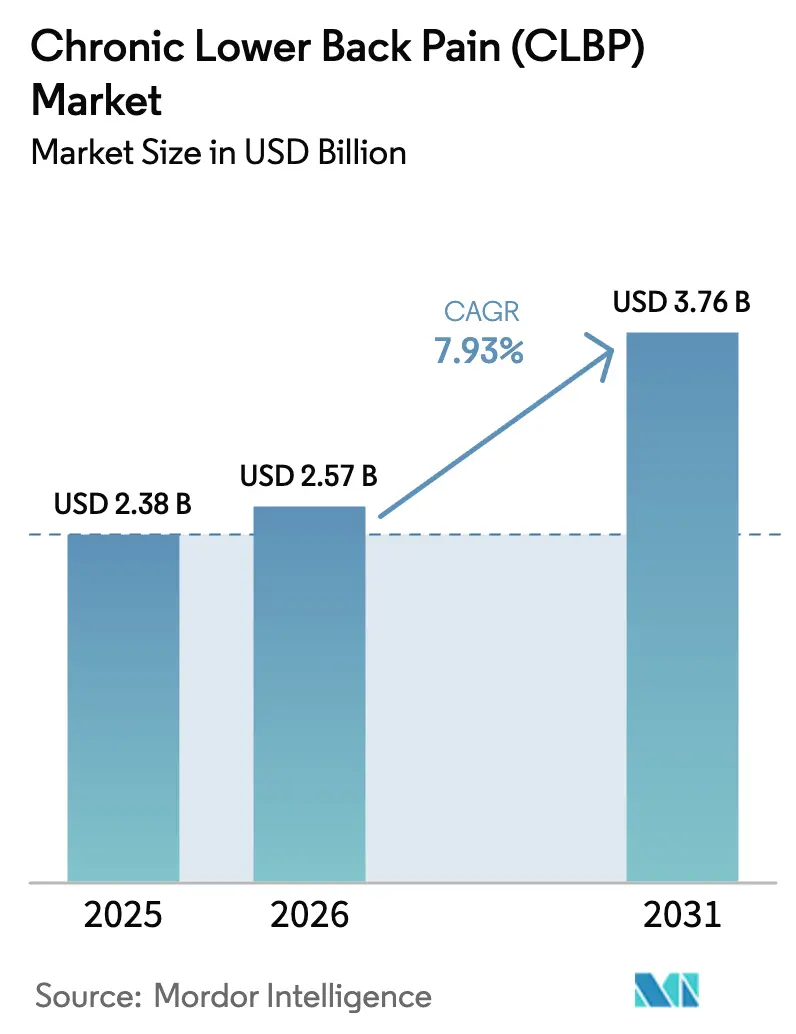

| Market Size (2026) | USD 2.57 Billion |

| Market Size (2031) | USD 3.76 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

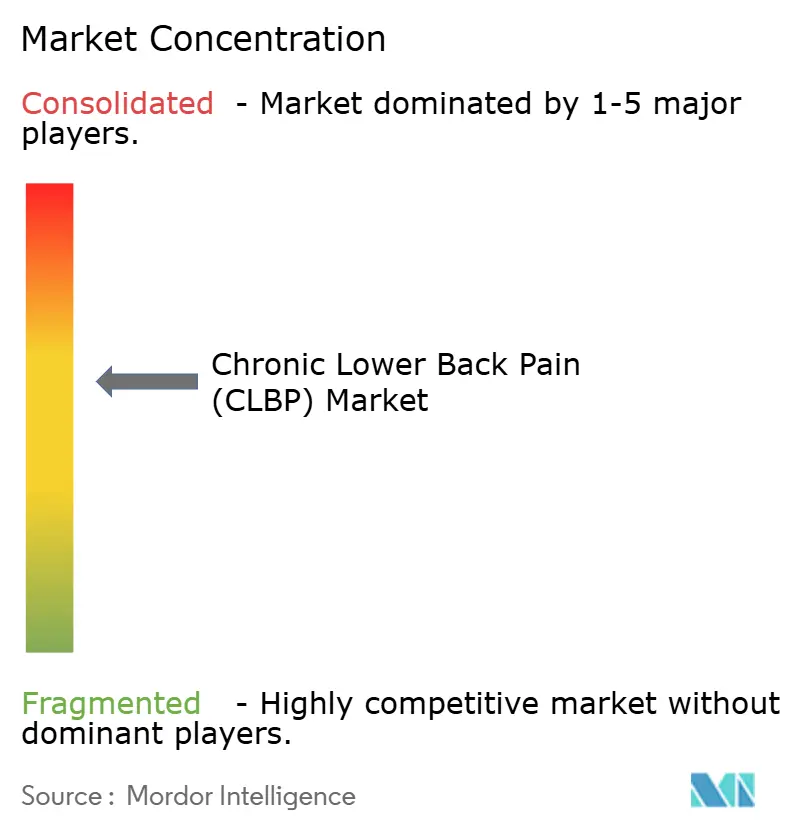

| Market Concentration | Medium |

Major Players_Market_CL.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chronic Lower Back Pain (CLBP) Market Analysis by Mordor Intelligence

The Chronic Lower Back Pain Market size in 2026 is estimated at USD 2.57 billion, growing from 2025 value of USD 2.38 billion with 2031 projections showing USD 3.76 billion, growing at 7.93% CAGR over 2026-2031.

Robust demand is being fueled by rapid acceptance of closed-loop spinal cord stimulators, the first new non-opioid drug class in more than two decades, and an aging global population that increasingly requires multidisciplinary pain management solutions. Hospitals remain the primary care setting, yet home-based digital therapeutics and remote monitoring are scaling quickly as payers shift toward value-based reimbursement. North America leads adoption because of sophisticated reimbursement pathways, while Asia Pacific is accelerating as healthcare infrastructure improves and populations gray. Competitive intensity is rising as device makers merge capabilities, drug developers push regenerative candidates through trials, and software firms embed artificial intelligence (AI) to tailor therapy in real time.

Key Report Takeaways

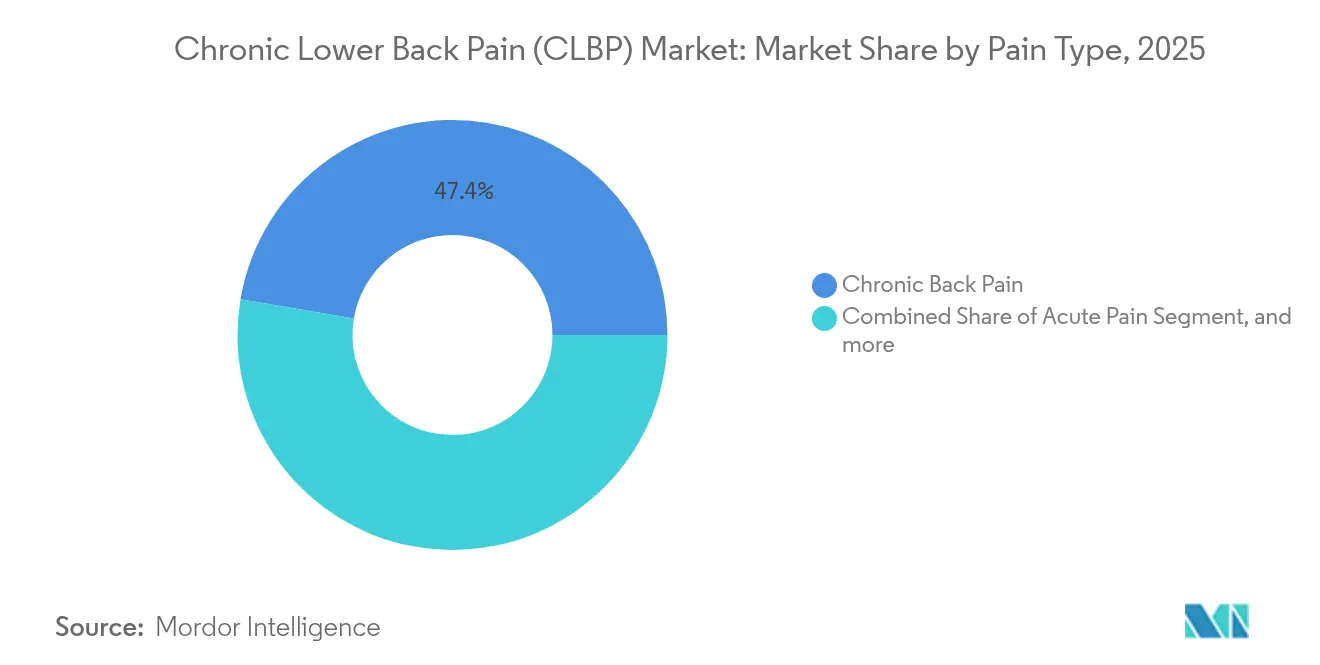

- By pain type, chronic pain accounted for 47.35% share of the chronic lower back pain market size in 2025 and acute pain is projected to grow 9.02% annually to 2031.

- By diagnosis technique, imaging guidelines secured 33.40% revenue in 2025; the segment is growing 8.3% per year through 2031.

- By therapy modality, pharmacologic products held 61.05% of the chronic lower back pain market share in 2025; regenerative medicine is forecast to expand at an 10.72% CAGR to 2031.

- By end user, hospitals controlled 56.85% of market revenue in 2025, whereas home-care settings are expanding at a 9.41% CAGR over the forecast period.

- By geography, North America contributed 39.70% revenue in 2025, while Asia Pacific is advancing at an 8.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chronic Lower Back Pain (CLBP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of Neuromodulation & SCS Implants | +1.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Rising Prevalence of Obesity & Sedentary Lifestyles | +1.2% | Global, with highest impact in North America & Gulf states | Long term (≥ 4 years) |

| Growing Geriatric Population Susceptible to CLBP | +1.5% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Expansion of Stem-Cell & Orthobiologic Trials | +0.9% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| AI-Driven Digital-Twin Models for Personalised Pain Therapy | +0.7% | North America & Europe, pilot programs in APAC | Short term (≤ 2 years) |

| Value-Based Reimbursement Favouring Non-Opioid Solutions | +1.1% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Neuromodulation & SCS Implants

Closed-loop spinal cord stimulation (SCS) has shifted the therapeutic paradigm by automatically adjusting signals in response to physiologic feedback, curbing overstimulation without clinician input.[1]Medtronic, “Inceptiv Closed-Loop SCS Clinical Results,” medtronic.com Medtronic’s Inceptiv system showed 82% of recipients experienced at least 50% pain reduction at 12 months. Nevro’s HFX AdaptivAI platform uses machine-learning algorithms to trim charging frequency while preserving efficacy. Together, these advances elevate long-term outcomes, improve health-related quality of life metrics, and reduce unplanned clinical visits. Reimbursement is increasingly tied to real-world evidence, and payers in the United States have begun adding supplemental payments for closed-loop stimulators that demonstrate opioid-sparing benefits. Manufacturers are also miniaturizing pulse generators, making same-day ambulatory implantation viable. Forward integration between device makers and telehealth platforms is creating an ecosystem where therapy parameters and patient-reported outcomes flow into cloud dashboards, enabling proactive adjustments by multidisciplinary teams.

Rising Prevalence of Obesity & Sedentary Lifestyles

Obesity induces biomechanical stress that accelerates intervertebral disc degeneration, heightening chronic lower back pain across demographics.[2]Centers for Disease Control and Prevention, “Obesity and Chronic Pain,” cdc.gov Remote work adoption since 2020 has deepened sedentary behavior, with musculoskeletal complaints ranking among the top reasons for physician visits. Economically, the United States registered USD 725 billion in chronic pain-related costs during 2024, hammered by health expenditures and lost productivity. Cellular gerontology studies now link adipose-driven inflammation to senescent “zombie” cells in spinal discs, and early-stage combination drugs that target these senescent cells have shown disc-height preservation in preclinical models.[3]Nature, “Senolytic Therapy for Disc Degeneration,” nature.com Such findings are steering investment toward regenerative pharmacology that intersects metabolic and orthopedic pathways.

Growing Geriatric Population Susceptible to CLBP

Individuals aged 65 years and older are projected to form 16% of the global populace by 2030, propelling demand for durable pain care. Research has highlighted SIRT6 as a genomic safeguard against disc degeneration; murine studies indicate that SIRT6 activation maintains disc hydration and mechanical properties, delaying the onset of chronic pain. For the geriatric cohort, minimally invasive options such as Boston Scientific’s Intracept intraosseous nerve ablation have demonstrated sustained efficacy, with 83% of treated patients reporting significant relief five years post-procedure. Multimodal geriatric programs combining exercise, nutrition, and mental-health counseling yield disability score improvements exceeding those of pharmacotherapy alone.

Expansion of Stem-Cell & Orthobiologic Trials

The RESPINE trial confirmed the safety of allogeneic mesenchymal stem cells (MSCs) injected intradiscally, building confidence in regenerative interventions despite missing primary efficacy end-points. Mayo Clinic’s ongoing trial targets facet joints with bone-marrow-derived MSCs, reflecting a shift toward localized, image-guided injections that limit systemic exposure. Beyond cells, platelet-rich plasma and recombinant growth factors are finding traction in military rehabilitation centers, where faster functional recovery is prized. Regulatory agencies are publishing draft frameworks to categorize orthobiologics under advanced-therapy medicinal product rules, clearing the runway for consistent commercialization pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Neurostimulators | -0.8% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Strict Opioid Prescribing & Reimbursement Clamp-Downs | -0.6% | North America & Europe | Short term (≤ 2 years) |

| Data-Privacy Risks in Cloud-Programmed Stimulators | -0.4% | Global, heightened in Europe due to GDPR | Medium term (2-4 years) |

| Semiconductor Shortages Delaying Closed-Loop SCs Launches | -0.3% | Global, supply chain dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Neurostimulators

Implantation of closed-loop SCS systems carries procedure costs between USD 35,000 and USD 70,000, posing reimbursement hurdles in low-resource settings. Revision surgeries occur in 9.82% of implanted patients, often for lead migration or inadequate pain control, compounding total lifetime expense. Cost-utility studies, however, prove rechargeable units deliver USD 104,000–168,833 in lifetime savings relative to non-rechargeable generators by minimizing battery replacements. Manufacturers are responding with simplified electrode arrays that shorten operating-room time and hospital stays, nudging health-economic equations in their favor.

Strict Opioid Prescribing & Reimbursement Clamp-Downs

The FDA’s 2025 mandate for strengthened opioid-risk language has made prescription renewals arduous, pushing clinicians toward device-based and regenerative modalities . Insurers now require documented failure of two non-opioid therapies before approving extended-release opioids, extending care pathways but redirecting spend to alternatives. While the policy suppresses opioid market volumes, it simultaneously expands the chronic lower back pain market for non-opioid solutions, albeit at the cost of elongated prior-authorization cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pain Type: Acute Pain Drives Growth Despite Chronic Dominance

Chronic manifestations held 47.35% of the chronic lower back pain market share in 2025, underscoring the need for long-term multidisciplinary care. Acute pain, though smaller, will expand at a 9.02% CAGR by 2031 as surgical volumes climb and hospitals standardize enhanced-recovery protocols. Acute management is benefiting from the FDA approval of suzetrigine, the first new non-opioid molecule in decades, enabling multimodal analgesia that limits narcotic use. Early, decisive pharmacologic and digital intervention forestalls transition to chronic states, lowering future care costs. Telerehabilitation applications integrating AI-guided exercise have cut postoperative readmissions by 18% in community hospital pilots.

In contrast, sub-acute back pain—often tied to workplace injury—presents a preventative opportunity for employers deploying ergonomics programs. Wearable posture sensors that feed into machine-learning dashboards alert users and human-resources departments about risky movement patterns, curbing incidence rates. Other pain categories, such as neuropathic and radicular pain, rely heavily on neuromodulation; insurers are beginning to approve dorsal-root ganglion stimulation when conventional SCS fails, widening the total addressable population.

By Diagnosis: Imaging Guidelines Dominate Assessment Protocols

Imaging captured 33.40% of 2025 revenue and is climbing 8.3% per year as protocols mandate objective verification before high-cost interventions. MRI remains the gold standard to detect disc herniation and Modic changes, while low-dose CT fills triage roles in trauma units. AI-aided post-processing improves diagnostic speed; NEC’s skeletal-pose engine raises detection accuracy for spondylolisthesis to 94%.

While clinical history and physical examination are entry points, payers increasingly demand imaging substantiation for reimbursement. Pain-score questionnaires, though essential for tracking, are now embedded in mobile apps, delivering real-time pain-intensity feeds to clinicians. Decision-support tools synthesize imaging and subjective metrics to flag candidates for minimally invasive ablation, trimming unnecessary surgical consults

By Therapy Modality: Regenerative Medicine Challenges Pharmacologic Dominance

Pharmacologic regimens commanded 61.05% of chronic lower back pain market revenue in 2025; nonetheless, they face escalating scrutiny amid duloxetine recalls and emerging gabapentinoid black-box warnings. Regenerative medicine’s 10.72% projected CAGR is underpinned by stem cell, platelet-rich plasma, and gene-editing approaches that repair tissue rather than mute symptoms. Gene-therapy nanocarriers restoring nucleus-pulposus integrity have achieved disc-height gains in rodent models, with first-in-human trials slated for 2026.

The chronic lower back pain market size attributed to neuromodulation continues to rise as AI-integrated devices document tangible opioid-sparing benefits. Minimally invasive ablation, particularly basivertebral nerve approaches, wins favor in ambulatory centers due to short procedure times and early ambulation. Payers are piloting outcome-based contracts where device makers absorb a portion of revision-surgery risk, accelerating switch-over from fixed-output systems.

By End User: Home-Care Settings Reshape Treatment Delivery

Hospitals generated 56.85% of 2025 revenue by orchestrating complex diagnostics, inpatient rehab, and surgical care. Still, home-care environments will register a 9.41% CAGR to 2031 as telemedicine parity laws in 38 U.S. states equalize reimbursement with on-site visits. Remote-programmed stimulators that leverage Bluetooth-to-smartphone bridges let clinicians tune parameters without in-person follow-up, lowering travel burden for mobility-impaired seniors.

Orthopedic and pain clinics act as procedural hubs for radiofrequency ablation and targeted drug injections, while ambulatory surgical centers capture patients needing same-day minimally invasive interventions. The chronic lower back pain market size flowing through these outpatient facilities is set to grow as insurers levy site-of-service differentials to shift care out of hospitals. AI-driven self-management apps have demonstrated 46% pain-score declines in German Rise-uP trials, equipping homebound patients with evidence-based exercise regimens and cognitive-behavioral prompts.

Geography Analysis

North America retained leadership with 39.70% of global revenue in 2025, helped by an installed base of more than 230,000 active spinal cord stimulators and favorable coding for closed-loop upgrades. FDA fast-track programs for breakthrough devices funnel innovations to market quickly, bolstering first-mover advantages for domestic manufacturers. Europe follows, aided by the Medical Device Regulation’s emphasis on clinical evidence, which accelerates uptake of technologies demonstrating opioid-sparing benefits.

The Asia Pacific chronic lower back pain market will grow 8.53% yearly through 2031 as Japan’s 22.5% adult pain prevalence forces systemic healthcare reforms. China’s inclusion of ion-channel modulators in the National Reimbursement Drug List widens access to novel pharmacology, while Australia’s early-adopter stance on neuromodulation guidelines positions it as a regional reference site. Investments in ambulatory surgery centers and physician training are lowering procedural backlogs across India and Southeast Asia.

South America and the Middle East & Africa collectively represent under 10% of current revenue but offer long-run upside given rising obesity rates and expanding private insurance coverage. Partnerships between Gulf-state hospitals and U.S. academic centers now include tele-mentoring for minimally invasive ablation, transferring skills without travel. Public-private initiatives in Brazil are piloting mobile MRI vans to deliver rural imaging services, showing early promise in shortening diagnostic delays.

Competitive Landscape

Moderate consolidation characterizes the field, with the top five companies accounting significant share of 2024 revenue. Globus Medical’s USD 250 million purchase of Nevro in April 2025 vertically integrates spine-surgery instrumentation and neuromodulation implants, unlocking cross-selling to 3,600 existing surgical accounts. Medtronic, Boston Scientific, and Abbott continue to anchor the device segment through closed-loop enhancements and cloud-based patient-management suites.

Drug developers such as Vertex are diversifying indications for suzetrigine into postoperative and neuropathic pain, chasing blockbuster forecasts that exceed USD 3 billion by 2032. Regenerative start-ups leverage fast-track FDA designations to rival incumbents, with Presidio Medical securing an Investigational Device Exemption for its ultra-low-energy field therapy in June 2025. Digital-health entrants partner with payers to wrap neuromodulation hardware into outcome-based service bundles, diluting the importance of device capital cost.

Competition increasingly hinges on data ownership; firms that aggregate longitudinal device telemetry and patient-reported outcomes generate predictive analytics that strengthen reimbursement dossiers. Cost-effectiveness modeling shows Evoke closed-loop systems become cost-dominant within five years, tilting buyer preference toward performance-linked procurement.

Chronic Lower Back Pain (CLBP) Industry Leaders

Medtronic

Mesoblast Limited

Johnson & Johnson (DePuy Synthes)

Pfizer Inc.

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Presidio Medical received Investigational New Drug approval for its neuromodulation platform designed to treat chronic lower back pain, enabling clinical trials to evaluate the safety and efficacy of its innovative approach . This approval expands the pipeline of next-generation neuromodulation technologies entering clinical development.

- May 2025: Stryker received FDA clearance for its OptaBlate BVN Basivertebral Nerve Ablation System, offering minimally invasive treatment for chronic vertebrogenic low back pain with rapid lesion creation and advanced microinfusion technology. Clinical studies demonstrate sustained pain and function benefits for up to five years.

- April 2025: Globus Medical completed its USD 250 million acquisition of Nevro Corporation, combining spine surgery expertise with advanced spinal cord stimulation technology to create comprehensive treatment solutions. The integration is expected to enhance market penetration and improve patient outcomes through coordinated care approaches.

- April 2025: Abbott launched a next-generation delivery system for its Proclaim DRG neurostimulation system, streamlining electrode placement during implantations for complex regional pain syndrome treatment. The improved system aims to increase physician adoption and patient access to specialized pain management technologies.

Global Chronic Lower Back Pain (CLBP) Market Report Scope

Chronic back pain is defined as pain that lasts for at least 12 weeks after an original injury or underlying cause of back pain has been treated. It is a common musculoskeletal problem with high prevalence among middle-aged and older adults.

The chronic lower Back Pain market is segmented by pain type (acute pain, subacute low back pain, chronic back pain, and other pain types (mechanical pain, radicular pain, and radiculitis)), by diagnosis (assessment of pain, clinical history, physical examination, and imaging guidelines), by end-user (hospital, orthopedic clinics, and other end-users) and geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD million) for the above segments.

| Acute Pain |

| Sub-acute Low Back Pain |

| Chronic Back Pain |

| Other Pain Types |

| Assessment of Pain Scores |

| Clinical History |

| Physical Examination |

| Imaging Guidelines |

| Pharmacologic |

| Neuromodulation |

| Regenerative |

| Minimally-Invasive Ablation |

| Hospitals |

| Orthopaedic & Pain Clinics |

| Ambulatory Surgical Centres |

| Home-care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pain Type | Acute Pain | |

| Sub-acute Low Back Pain | ||

| Chronic Back Pain | ||

| Other Pain Types | ||

| By Diagnosis | Assessment of Pain Scores | |

| Clinical History | ||

| Physical Examination | ||

| Imaging Guidelines | ||

| By Therapy Modality | Pharmacologic | |

| Neuromodulation | ||

| Regenerative | ||

| Minimally-Invasive Ablation | ||

| By End User | Hospitals | |

| Orthopaedic & Pain Clinics | ||

| Ambulatory Surgical Centres | ||

| Home-care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the chronic lower back pain market by 2031?

The market is forecast to reach USD 3.76 billion by 2031, reflecting an 7.93% CAGR over 2026-2031.

Which region is growing fastest for chronic lower back pain treatments?

Asia Pacific is the fastest-growing region, expanding at an 8.53% CAGR thanks to aging populations and improving healthcare infrastructure.

Why are closed-loop spinal cord stimulators gaining traction?

Closed-loop devices automatically adapt stimulation based on real-time feedback, deliver superior pain relief, and reduce opioid dependence, making them attractive to clinicians and payers.

How is regenerative medicine impacting back pain care?

Stem-cell and orthobiologic therapies aim to repair damaged discs and supporting tissues, driving an 10.72% CAGR in the regenerative segment through 2031.

What role do digital therapeutics play in managing lower back pain?

AI-guided apps provide remote exercise coaching and pain monitoring, cutting waiting lists and enabling home-based care that complements in-person treatment.

How are payers encouraging non-opioid chronic pain solutions?

Insurers are adopting value-based reimbursement models that favor neuromodulation, regenerative therapies, and digital interventions proven to lower opioid use and improve patient outcomes.

Page last updated on: