Osteoarthritis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

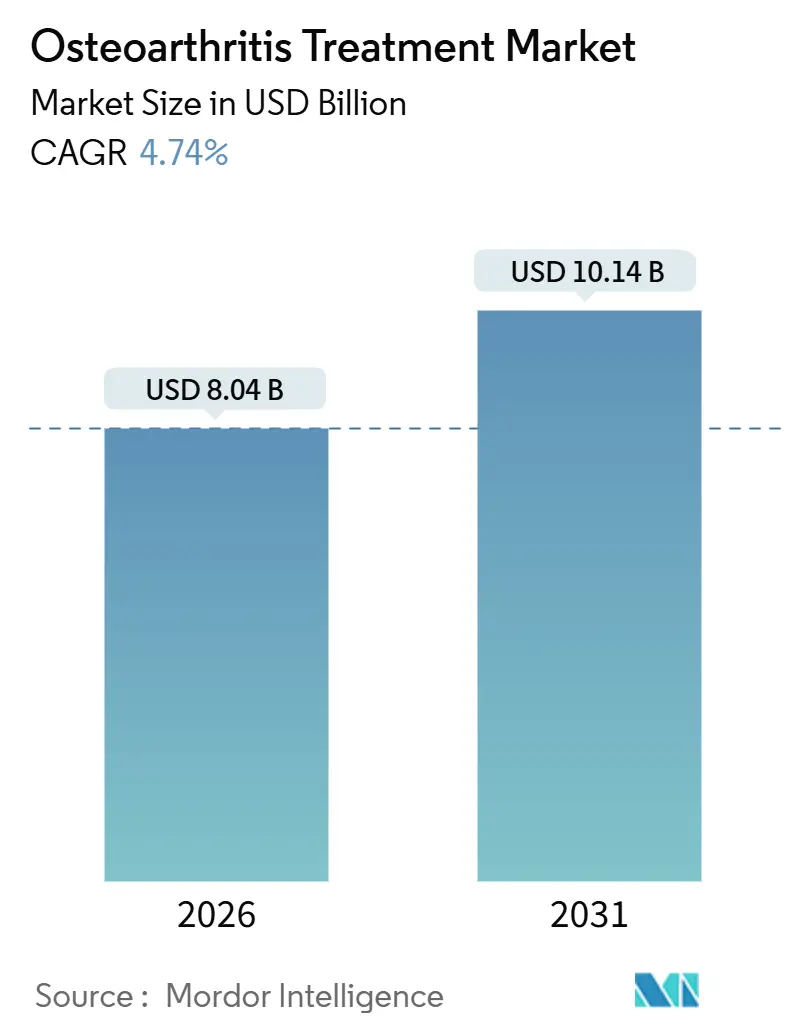

| Market Size (2026) | USD 8.04 Billion |

| Market Size (2031) | USD 10.14 Billion |

| Growth Rate (2026 - 2031) | 4.74% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Osteoarthritis Treatment Market Analysis by Mordor Intelligence

The Osteoarthritis Treatment Market size is estimated at USD 8.04 billion in 2026, and is expected to reach USD 10.14 billion by 2031, at a CAGR of 4.74% during the forecast period (2026-2031).

Demand is rising as aging and obese populations expand the addressable patient pool, yet reimbursement hurdles and evidence gaps slow uptake of disease-modifying therapies. Non-steroidal anti-inflammatory drugs (NSAIDs) remain first-line because they are inexpensive and widely available. Still, safety warnings are prompting clinicians to favor topical formulations and single-injection hyaluronic acid products. Hospital budgets favor minimally invasive injections that delay costly arthroplasty, encouraging manufacturers to innovate around extended-release corticosteroids and cross-linked viscosupplements. Competitive dynamics are intensifying as implant companies acquire regenerative assets to hedge against declining volumes of joint replacements.

Key Report Takeaways

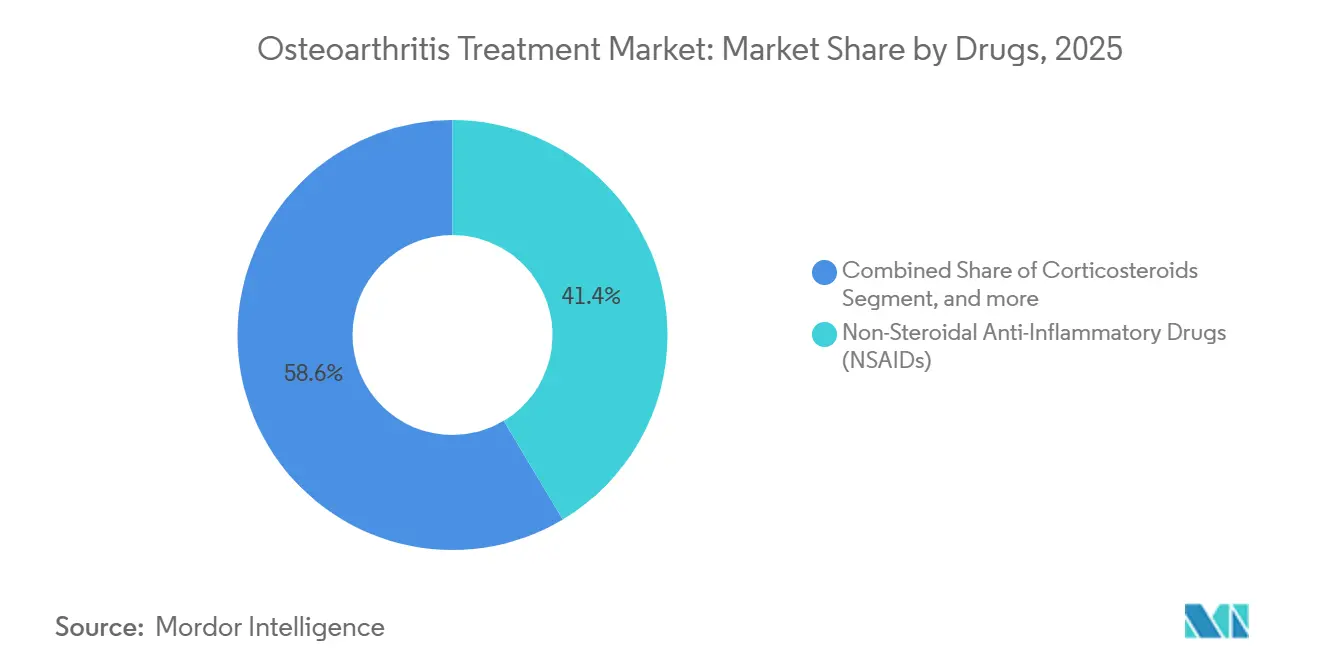

- By drug class, NSAIDs led with 41.43% of the osteoarthritis treatment market share in 2025, while single-injection hyaluronic acid is forecast to expand at a 6.54% CAGR to 2031.

- By anatomy, knee disease accounted for 46.76% of the osteoarthritis treatment market size in 2025, and shoulder cases are projected to advance at a 6.76% CAGR through 2031.

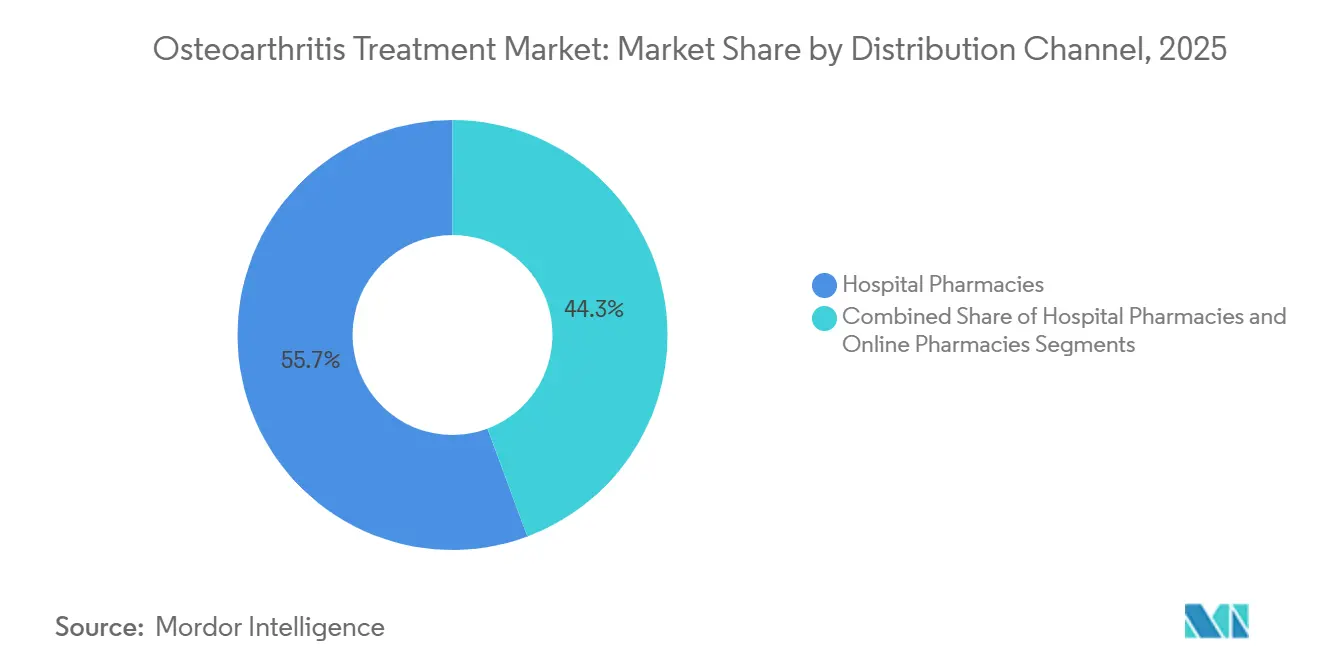

- By distribution channel, hospital pharmacies held a 55.67% revenue share in 2025, whereas online pharmacies are expected to grow at a 7.86% CAGR through 2031.

- By end user, hospitals captured 48.65% of the osteoarthritis treatment market size in 2025; however, orthopedic clinics are expected to expand at a 7.65% CAGR through 2031.

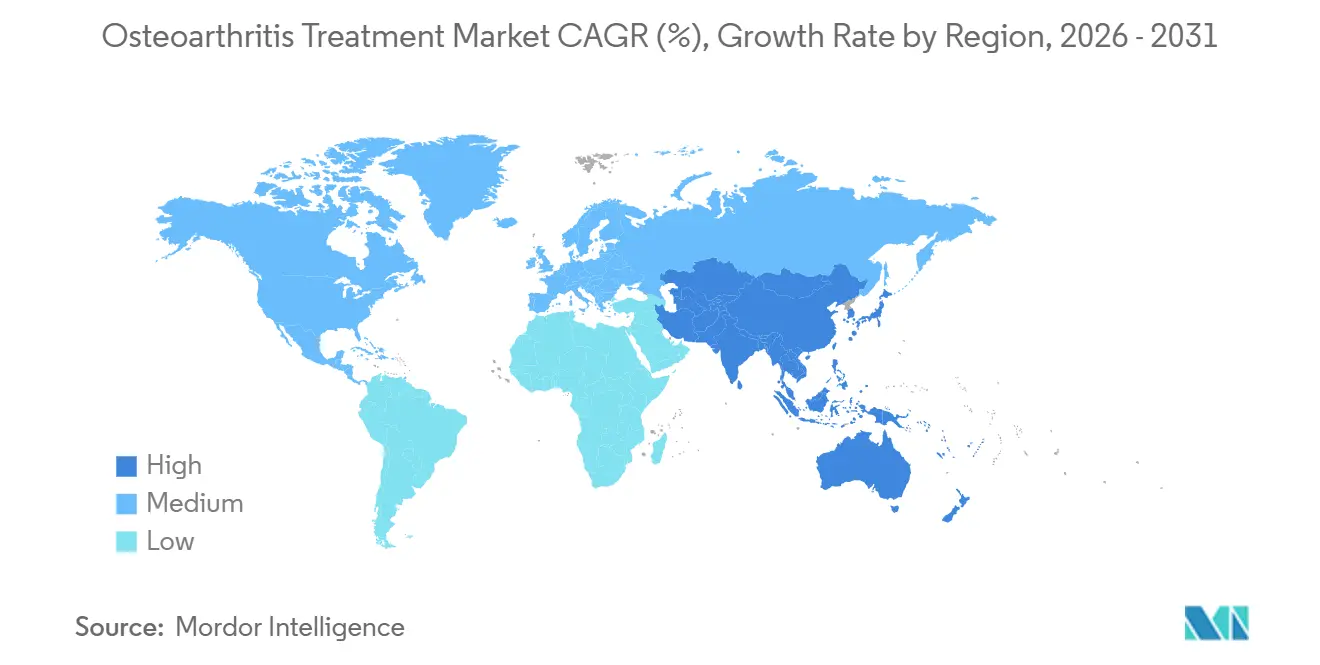

- By geography, North America retained a 42.65% revenue share in 2025, while the Asia-Pacific region is projected to grow at a 5.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Osteoarthritis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly aging global population and rising osteoarthritis prevalence | +1.2% | Global, with concentration in Japan, Western Europe, North America | Long term (≥ 4 years) |

| Rising obesity and sedentary lifestyles | +0.9% | North America, Middle East, Latin America | Medium term (2-4 years) |

| Growing adoption of minimally invasive intra-articular injections and single-injection viscosupplements | +0.8% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Expanding insurance coverage and reimbursement for non-surgical therapies in emerging markets | +0.5% | Asia-Pacific (China, India), Latin America, Middle East | Medium term (2-4 years) |

| Advances in regenerative medicine and disease-modifying therapies | +0.7% | North America, Western Europe | Long term (≥ 4 years) |

| AI-enabled early diagnostics and personalized treatment pathways | +0.4% | North America, Europe, select Asia-Pacific hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapidly Aging Global Population

United Nations projections indicate that 1.4 billion people will be aged 60 or older by 2030, up from 1 billion in 2020[1]United Nations, “World Population Ageing 2023,” un.org. Japan illustrates the impact, with 29% of residents already over 65 years. The prevalence of osteoarthritis is expected to reach 1 billion cases worldwide by 2050. China’s 280 million citizens aged 60 and above in 2024 are accelerating demand for cost-effective injections over surgery, according to. Pharmaceutical pipelines are adjusting; Novartis advanced its Wnt-pathway inhibitor LNA043 into Phase 2b during 2024.

Rising Obesity and Sedentary Lifestyles

The World Health Organization reported more than 1 billion obese individuals worldwide in 2022. Obesity raises the risk of knee osteoarthritis fivefold and quickens cartilage loss. Novo Nordisk’s STEP 9 trial demonstrated a 13.7% weight loss with semaglutide, reducing knee pain scores by 41.7 points in 2024. U.S. obesity-related medical costs exceed USD 170 billion annually. A 2024 Lancet study linked fewer than 5,000 daily steps to 22% faster cartilage thinning.

Growing Adoption of Single-Injection Viscosupplements

The FDA cleared HYMOVIS ONE in April 2025, reducing the number of clinic visits from three to one. ESCEO guidelines published in 2024 recommend single-injection hyaluronic acid for grade 2-3 knee disease. Ambulatory injections cost USD 800-1,200 per episode compared with USD 25,000-35,000 for knee replacement. Pacira and Johnson & Johnson began co-promoting ZILRETTA in July 2025 to extend corticosteroid relief to three months. Ultrasound guidance improves accuracy; a 2024 study in Arthritis & Rheumatology found 18% better pain reduction compared to the landmark technique.

AI-Enabled Early Diagnostics

The FDA cleared Lunit INSIGHT MSK in 2024, detecting early radiographic change with 92% sensitivity. A 2025 study in Nature Medicine predicted four-year progression to knee replacement with an AUC of 0.87, using MRI-based deep learning. IBM and the Osteoarthritis Research Society International launched a decision-support tool in 2024 that matches imaging, cytokine, and patient-reported data to recommended injections. A 2024 Health Affairs analysis estimated AI triage could save USD 1.2 billion per year in the U.S. by reducing unnecessary arthroscopies. The EMA issued draft guidance in 2025 to regulate such software.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced biologic therapies | -0.6% | Global, acute in emerging markets | Medium term (2-4 years) |

| Safety concerns and regulatory scrutiny around long-term NSAID and opioid use | -0.5% | North America, Europe | Short term (≤ 2 years) |

| Limited clinical evidence for novel regenerative treatments hindering physician adoption | -0.4% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Variability in reimbursement policies across regions | -0.3% | Europe, Canada, selected Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Biologic Therapies

Platelet-rich plasma costs USD 700-1,200 per injection and requires three sessions, yet Medicare offers no national coverage. Stem-cell injections priced at USD 3,000-7,000 showed no superiority to corticosteroids in a 2023 Nature Medicine trial. Amniotic suspension allografts, priced at USD 2,500-4,000, have faced repeated FDA warning letters for unsubstantiated claims. Pacira acquired GQ Bio in 2025 to develop PCRX-201 gene therapy that may debut at above USD 10,000 per dose. India’s Ayushman Bharat scheme reimburses only generic NSAIDs and corticosteroids, leaving viscosupplements as out-of-pocket purchases.

Safety Concerns and Regulatory Scrutiny Around Long-Term NSAID Use

The FDA boxed warning highlights elevated myocardial infarction and stroke risk from systemic NSAIDs. A 2024 Lancet meta-analysis reported diclofenac raised major vascular events by 40%[2]The Lancet, “Major vascular events with NSAIDs,” thelancet.com. A Cochrane review estimated that 1 in 1,200 annual NSAID users require hospitalization for upper-GI bleeding. The CDC’s 2024 guideline discourages opioids for chronic osteoarthritis pain. The UK MHRA will mandate cardiovascular risk checks for prescriptions longer than 30 days from 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drugs: Single-Injection Viscosupplements Reshape Protocols

Hyaluronic acid injections are forecast to rise at a 6.54% CAGR through 2031 as single-dose products remove adherence barriers. NSAIDs retained a 41.43% revenue share in 2025, yet topical diclofenac gels are gaining favor due to their lower systemic exposure. Corticosteroids, such as ZILRETTA, offer 12 weeks of relief, thereby limiting the need for repeat procedures. Biologics account for a small portion of spending but dominate R&D budgets. In 2024, GlaxoSmithKline partnered with Relation Therapeutics to identify genetic targets, with USD 200 million in milestones. The osteoarthritis treatment market share is likely to tip toward injectables if forthcoming disease-modifying candidates demonstrate structural benefit.

The FDA approval of HYMOVIS ONE in 2025 validated the one-shot approach, following a 600-patient trial that demonstrated six-month pain reduction equivalent to that of three-dose regimens. ESCEO’s 2024 guideline shift triggered European demand despite fragmented reimbursement. Opioid prescribing for osteoarthritis dropped 40% in the U.S. between 2020 and 2024 after CDC guideline updates. Pharmaceutical pipelines, therefore, prioritize structural agents that can postpone the need for replacement surgery and preserve pricing power in the face of generic NSAID competition.

By Anatomy: Shoulder Gains as Rotator-Cuff Sequelae Mount

Knee disease accounted for 46.76% of the osteoarthritis treatment market size in 2025, owing to its high biomechanical load and clear surgical pathways. Shoulder cases are projected to grow at 6.76% through 2031 as chronic rotator-cuff injuries progress to glenohumeral degeneration in aging workers and athletes. Hip disease follows a similar growth pattern but faces slower viscosupplement uptake because injections are technically complex[3]Arthritis Foundation, “Joint Specific Osteoarthritis Data,” arthritis.org. Ankle and small-joint disease together account for less than 10% of spending.

Smith & Nephew acquired CartiHeal for USD 180 million upfront in 2024, targeting focal defects that can precede knee replacement. Reverse total shoulder arthroplasty has expanded indications, leading to increased use of presurgical injections. The osteoarthritis treatment market share for shoulder interventions is expected to climb as implant survival improves and patients seek delay strategies before prosthesis.

By Distribution Channel: Online Gains as OTC NSAIDs Bypass Gatekeepers

Hospital pharmacies captured 55.67% revenue in 2025 because clinic-based injections require sterile compounding. Online pharmacies are forecast to grow 7.86% annually as direct-to-consumer NSAIDs and nutraceuticals gain traction. Retail chains still dominate prescription volume but face mail-order competition that compresses margins. The osteoarthritis treatment market size within e-commerce will expand if telemedicine waivers that allow virtual prescribing remain in force.

Amazon Pharmacy’s 2024 expansion into 20 U.S. states cut 90-day ibuprofen costs by 30% compared with brick-and-mortar outlets. Hims & Hers introduced a virtual musculoskeletal-pain service in 2025 pairing consults with home-delivered topical diclofenac. Specialty pharmacies now deliver ZILRETTA directly to orthopedic clinics under buy-and-bill models, eroding hospital control.

By End User: Orthopedic Clinics Capture Ambulatory Shift

Hospitals held 48.65% of osteoarthritis treatment market size in 2025 because joint replacement remains largely inpatient. Orthopedic clinics are growing 7.65% annually as ultrasound-guided injections migrate to office settings. Ambulatory surgical centers captured more unicompartmental knee cases after Medicare classified them as outpatient-eligible in 2024. Sports-medicine centers cater to younger patients seeking platelet-rich plasma or stem-cell injections that hospitals avoid due to uncertain reimbursement.

Pacira and Johnson & Johnson launched a bundled model for ZILRETTA that packages drug, supplies, and imaging in a single purchase order for clinics. Zimmer Biomet’s USD 177 million acquisition of Monogram Orthopaedics in 2025 equips high-volume centers with autonomous robotic planning that personalizes implant alignment. Digital therapeutics like Hinge Health reduced joint-replacement intent by 30% in a 2024 trial, hinting at further decentralization.

Geography Analysis

North America generated 42.65% of osteoarthritis treatment revenue in 2025, primarily driven by Medicare reimbursement for injections and surgeries. Local contractors tightened prior authorization, resulting in a 35% increase in denial rates for hyaluronic acid between 2023 and 2025. The FDA approval of HYMOVIS ONE and AI-based detection tools underscores the region’s leadership in innovation. Canada limits viscosupplement coverage, keeping penetration below 15% in Ontario.

The Asia-Pacific region is projected to expand at a rate of 5.64% through 2031, as Japan’s super-aged population and China’s 280 million seniors seek injections to defer surgery. Japan reimburses over 2 million viscosupplement injections annually. China added several hyaluronic acid brands to its national drug list in 2024, boosting domestic output. India’s public scheme excludes viscosupplements, but the rising income of the middle class is supporting a self-pay market. South Korea’s universal coverage and rapid aging underpin double-digit growth in Seoul and Busan.

Europe grows more slowly because cost-effectiveness thresholds vary. NICE confines hyaluronic acid use to salvage cases in the UK. Germany covers multi-injection regimens that boost volume but cap per-patient spend. ESCEO’s 2024 endorsement of single-injection products may harmonize reimbursement over time. In the Middle East, the UAE and Saudi Arabia are building orthopedic centers that attract medical tourists, whereas sub-Saharan Africa relies on low-cost NSAIDs. South American growth is concentrated in Brazil, where private insurance uptake is improving viscosupplement access despite currency volatility.

Competitive Landscape

The osteoarthritis treatment market is moderately fragmented, with branded NSAID leaders competing against specialty injection firms and regional manufacturers. Pfizer, Johnson & Johnson, and Sanofi remain strong in oral analgesics through pharmacy-benefit-manager contracts. Zimmer Biomet and Smith & Nephew are diversifying by acquiring regenerative assets; Zimmer bought Monogram Orthopaedics for USD 177 million in 2025 to leverage autonomous robotic planning. Smith & Nephew paid USD 180 million plus milestones for CartiHeal’s Agili-C scaffold in 2024.

Specialty players such as Anika Therapeutics and Bioventus focus on single-injection hyaluronates and extended-release corticosteroids distributed through specialty pharmacies. Relation Therapeutics entered a USD 200 million-per-target genomic collaboration with GlaxoSmithKline in 2024. Lunit’s FDA-cleared INSIGHT MSK AI tool is being integrated into hospital imaging systems to guide treatment pathways. Pacira’s GQ Bio acquisition brings gene therapy into its pipeline, potentially reducing repeat injection frequency if long-term expression proves durable. Market entry barriers include stringent FDA oversight for regenerative claims and growing payer scrutiny of high-cost biologics.

Osteoarthritis Treatment Industry Leaders

Sanofi SA

GlaxoSmithKline plc

Pfizer Inc

Bayer AG

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Biosplice Therapeutics, Inc. submitted a New Drug Application (NDA) to the FDA for Lorecivivint (LOR). The drug is intended for the treatment of knee osteoarthritis. This submission marks a significant step toward potential approval and availability of the treatment.

- December 2025: Helmholtz Munich, one of the leading German biomedical research centers, has announced its participation in the EU research initiative PROBE, aiming to revolutionize the diagnosis and treatment of osteoarthritis. The project is funded by Horizon Europe through the Innovative Health Initiative, with a total budget of approximately 26 million euros. Helmholtz Munich received over 1.4 million euros of this funding to support its research efforts.

- July 2025: Johnson & Johnson partnered with Pacira BioSciences, Inc. The collaboration aims to expand early intervention options for knee osteoarthritis. This move is expected to enhance treatment accessibility and innovation in the management of knee osteoarthritis.

Global Osteoarthritis Treatment Market Report Scope

As per the scope of the report, osteoarthritis treatment includes pain relievers like acetaminophen and NSAIDs to reduce pain and inflammation. Corticosteroid injections may be used for severe symptoms, while hyaluronic acid injections help improve joint lubrication. Additionally, certain supplements, such as glucosamine and chondroitin, may support joint health.

The Osteoarthritis Treatment Market is Segmented by Drugs (NSAIDs, Corticosteroids, Hyaluronic Acid Injections, Biologics & Disease-Modifying Therapies, and Other Drugs), Anatomy (Ankle, Hip, Knee, Shoulder, and Other Anatomies), Distribution Channel (Hospital, Retail, and Online Pharmacies), End User (Hospitals, Ambulatory Surgical Centers, Orthopedic & Rheumatology Clinics, Sports Medicine Centers, and Homecare Settings), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) |

| Corticosteroids |

| Hyaluronic Acid Injections |

| Biologics & Disease-Modifying Therapies |

| Other Drugs |

| Ankle Osteoarthritis |

| Hip Osteoarthritis |

| Knee Osteoarthritis |

| Shoulder Osteoarthritis |

| Other Anatomies |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Hospitals |

| Ambulatory Surgical Centers |

| Orthopedic & Rheumatology Clinics |

| Sports Medicine Centers |

| Homecare Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drugs | Non-Steroidal Anti-Inflammatory Drugs (NSAIDs) | |

| Corticosteroids | ||

| Hyaluronic Acid Injections | ||

| Biologics & Disease-Modifying Therapies | ||

| Other Drugs | ||

| By Anatomy | Ankle Osteoarthritis | |

| Hip Osteoarthritis | ||

| Knee Osteoarthritis | ||

| Shoulder Osteoarthritis | ||

| Other Anatomies | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Orthopedic & Rheumatology Clinics | ||

| Sports Medicine Centers | ||

| Homecare Settings | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the osteoarthritis treatment space in 2026, and what is its projected growth?

Spending totals USD 8.04 billion in 2026 and is projected to reach USD 10.14 billion by 2031, reflecting a 4.74% CAGR.

Which therapy class currently generates the highest revenue share?

Non-steroidal anti-inflammatory drugs account for 41.43% of 2025 revenue.

Which therapeutic approach is expanding most rapidly?

Single-injection hyaluronic acid injections are forecast to grow at a 6.54% CAGR through 2031.

Which anatomical site drives the greatest demand for treatment?

Knee disease held 46.76% of 2025 spending due to its load-bearing role and clear surgical pathway.

Which region is expected to post the fastest revenue growth?

Asia-Pacific is projected to advance at a 5.64% CAGR from 2026 to 2031.

What safety issues are shaping prescribing patterns?

FDA boxed warnings link systemic NSAIDs to elevated cardiovascular and gastrointestinal risk, while CDC guidance discourages long-term opioid use, pushing clinicians toward topical NSAIDs and injection therapies.

Page last updated on: