UAE NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

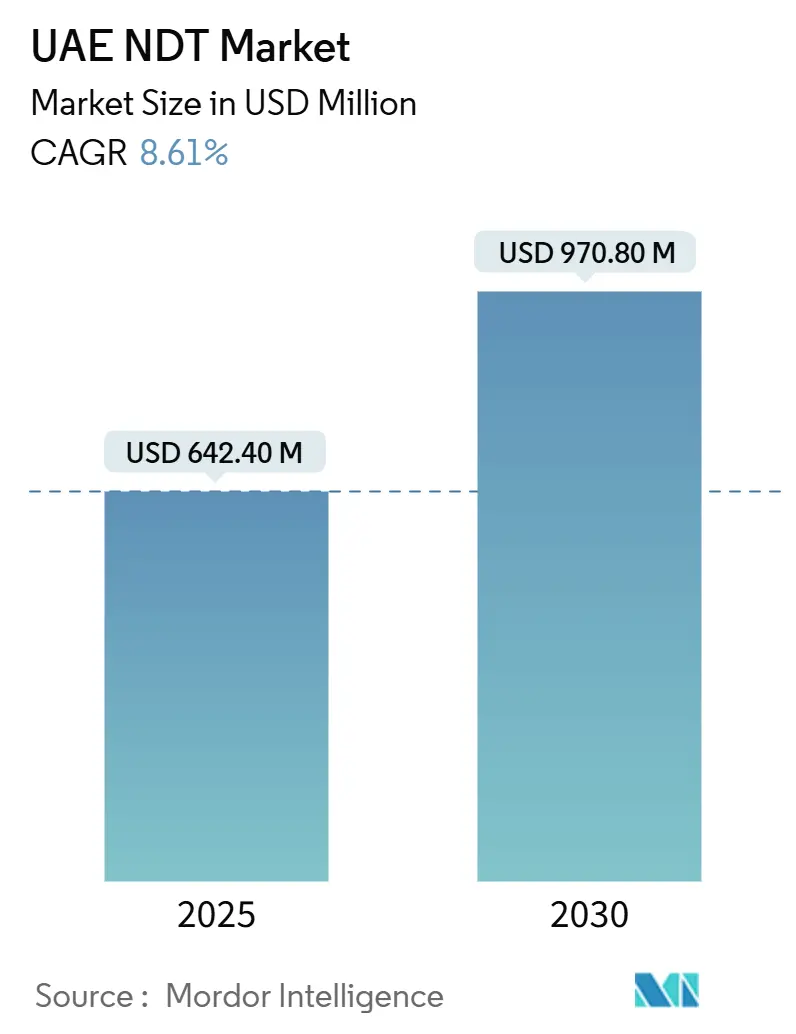

| Market Size (2025) | USD 642.40 Million |

| Market Size (2030) | USD 970.80 Million |

| Growth Rate (2025 - 2030) | 8.61% CAGR |

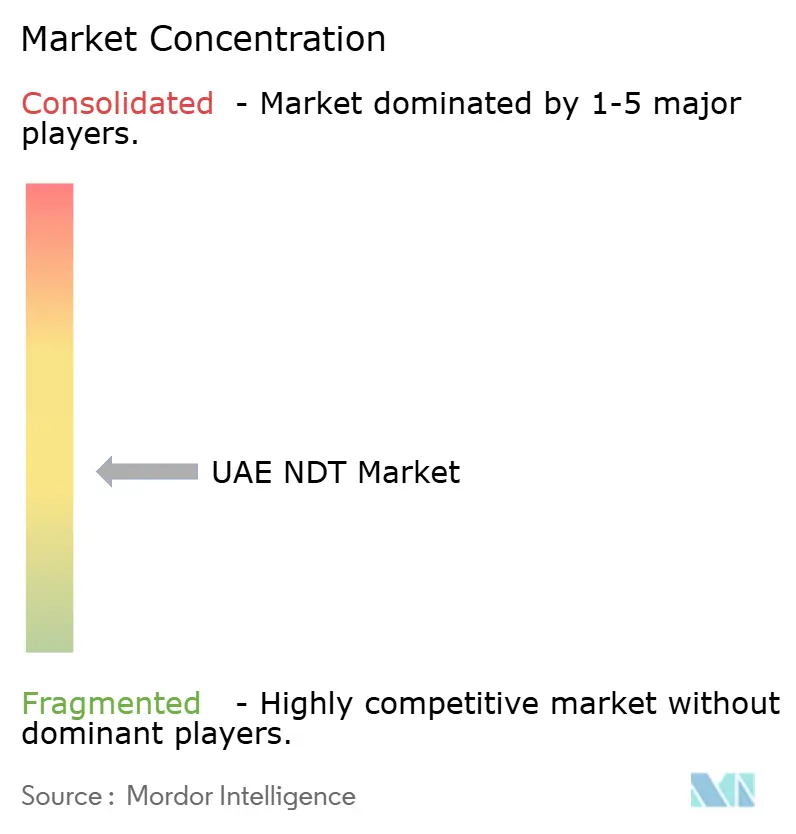

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE NDT Market Analysis by Mordor Intelligence

The UAE NDT market size was USD 642.4 million in 2025 and is projected to reach USD 970.8 million by 2030, representing an 8.61% CAGR from 2025 to 2030. Sustained investment in asset-integrity programs linked to ADNOC’s 2030 production agenda, the long-term inspection requirements of the Barakah Nuclear Power Plant, and wider smart-city infrastructure development form the core growth pillars of the UAE NDT market. Operators favor outsourced inspection over capital equipment purchases, a model reinforced by FANR and ENAS accreditation protocols that reward specialist service providers. The uptake of AI-enabled techniques is accelerating as end-users seek predictive maintenance tools that reduce unplanned shutdown risk and optimize inspection intervals. The regulatory emphasis on systematic integrity audits, growing insurance incentives for risk-based inspections, and technology-driven efficiency gains collectively create a robust outlook for demand.

Key Report Takeaways

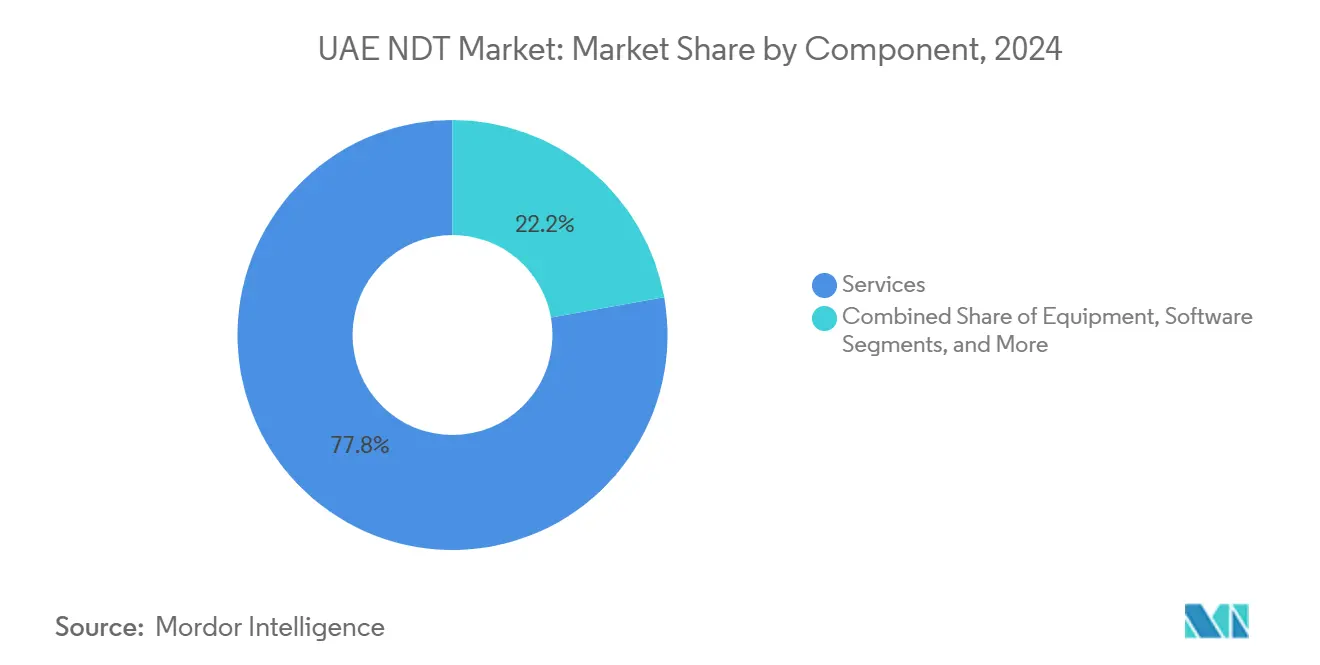

- By component, services held a 77.8% share of the UAE NDT market in 2024, while software is projected to record a 12.6% CAGR through 2030.

- By testing method, ultrasonic testing captured 26.5% of the UAE NDT market share in 2024; eddy-current testing is forecast to expand at a 9.6% CAGR to 2030.

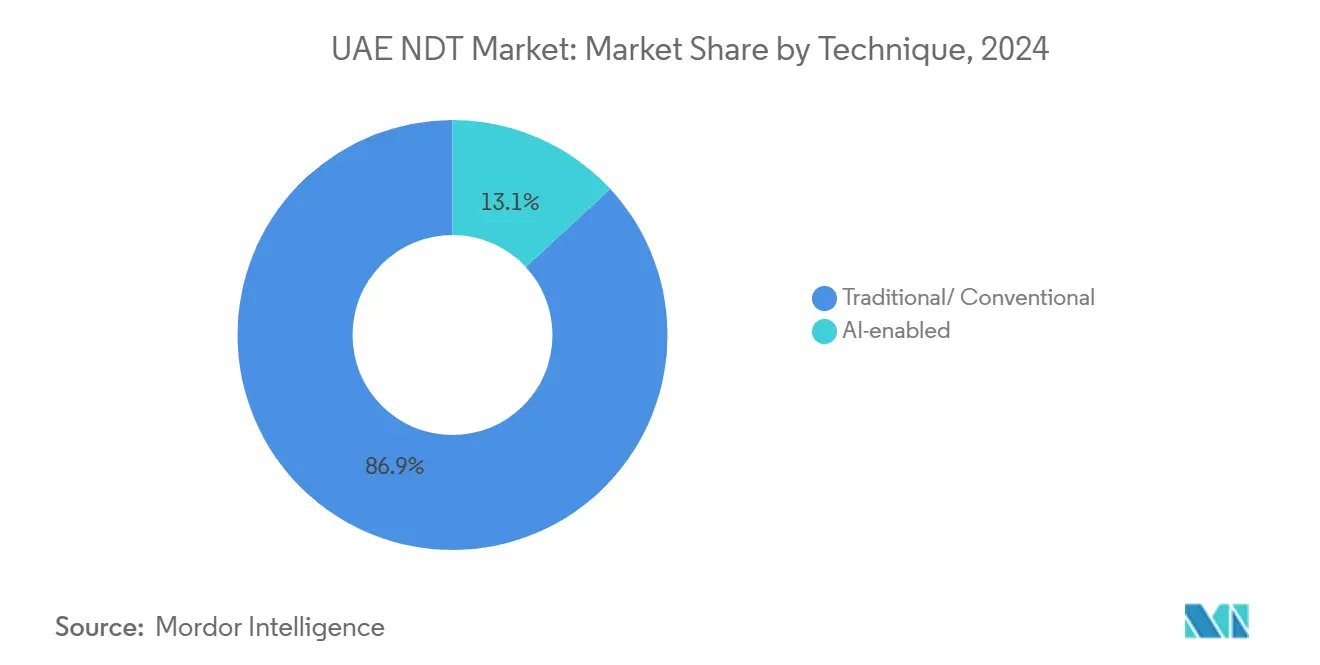

- By technique, conventional approaches accounted for 86.9% of the UAE NDT market size in 2024, while AI-enabled techniques are projected to advance at a 15.7% CAGR through 2030.

- By end-user industry, oil and gas led with 24.2% of the UAE NDT market share in 2024; automotive and transportation is projected to post the highest CAGR at 9.5% from 2025 to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid refinery upgrades to meet IMO-2020 sulphur limits | +1.2% | UAE national, with a concentration in Abu Dhabi refineries | Medium term (2-4 years) |

| Mandatory asset-integrity audits in ADNOC's 2030 strategy | +2.1% | UAE national, with primary impact in Abu Dhabi upstream operations | Long term (≥ 4 years) |

| Nuclear energy expansion at Barakah is driving advanced ISI demand | +1.8% | UAE national, concentrated in the Al Dhafra region | Long term (≥ 4 years) |

| Smart city megaprojects (e.g., Expo City, NEOM-adjacent supply chains) | +1.4% | UAE national, with spillover to the broader GCC region | Medium term (2-4 years) |

| Insurance-linked risk-based inspection premiums | +0.9% | UAE national, with early adoption in offshore operations | Short term (≤ 2 years) |

| Stranded onshore rigs re-purposed for geothermal – inspection uptick | +0.7% | UAE national, pilot projects in Abu Dhabi and Dubai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mandatory Asset-Integrity Audits Drive Systematic Inspection Protocols

ADNOC’s directive to raise crude production capacity to 5 million barrels per day by 2027 embeds comprehensive integrity audits across upstream assets, stimulating long-cycle demand for advanced services in the UAE NDT market.[1]ADNOC Drilling, “Strategy - Drilling,” ADNOC.DRILLING.AE Operators now combine risk-based inspection with AI platforms such as Neuron 5, which cut unplanned shutdowns by 50%, demonstrating tangible value in predictive workflows. Pre-commissioning checks for new facilities and fitness-for-service evaluations of mature assets run in parallel, expanding the breadth of services. Regulatory oversight by ENAS ensures data traceability, shaping procurement toward certified providers. Together, these factors place systematic inspection at the core of ADNOC’s asset integrity culture, reinforcing the momentum for outsourced services.

Nuclear Energy Expansion Establishes Advanced ISI Standards

With three Barakah units in commercial operation, FANR’s 220-plus inspections and the plant’s 60-year design life anchor a multi-decade inspection pipeline for the UAE NDT market. The Secondary Standards Dosimetry Laboratory’s 600 annual calibration certificates illustrate the instrumentation precision required for nuclear-grade work. Contractors certified for nuclear tasks leverage their credentials across petrochemical and power assets, cascading stringent quality benchmarks into adjacent sectors. The nuclear program, therefore, elevates national inspection standards, accelerates competency development, and stabilizes long-term service demand.

Smart-City Infrastructure Drives Digital Inspection Integration

Dubai’s ARIIS robotic rail system achieved a 75% reduction in inspection time and a 40% uplift in condition-assessment accuracy, validating AI-enabled inspection for urban assets. Drone-based tunnel surveillance, IoT-linked sensors, and real-time cloud analytics form a digital backbone that city planners now expect to have in place. These technologies align with broader UAE sustainability goals by minimizing service interruption and supporting data-driven maintenance. Consequently, smart-city programs serve as living laboratories for advanced inspection, driving rapid adoption curves and expanding use cases across the UAE NDT market.

Insurance-Linked Risk Assessment Reshapes Inspection Economics

Insurance underwriters now discount premiums when operators present certified inspection data, especially for offshore facilities where downtime can cost USD 30-40 million per day. Predictive corrosion-under-insulation monitoring by CorrosionRADAR, recognized by ADNOC, exemplifies how continuous data feeds enable dynamic risk pricing. The financial incentive accelerates the adoption of certified inspection platforms, embeds standardized reporting, and tightens the linkage between integrity management and insurance economics across the UAE NDT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited indigenous calibration labs are inflating turnaround times | -1.6% | UAE national, with a particular impact on specialized equipment | Medium term (2-4 years) |

| High import tariffs on isotopes and radiography sources | -0.8% | UAE national, affecting the radiographic testing segment | Short term (≤ 2 years) |

| Shortage of ASME-certified Level-III inspectors | -1.3% | UAE national, with spillover effects to the broader GCC region | Long term (≥ 4 years) |

| Cybersecurity concerns over cloud NDT data in sovereign facilities | -0.7% | UAE national, concentrated in critical infrastructure sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Calibration Infrastructure Constraints Limit Service Velocity

While FANR’s laboratory supports radiation equipment, most ultrasonic, eddy-current, and thermography instruments still require overseas calibration, which extends lead times and adds logistics costs for service firms.[2]World Energy, “FANR Built a Strong Nuclear and Radiological Regulatory Infrastructure in UAE for Protection of the Public and Environment,” WORLD-ENERGY.ORG Emerging ISO/IEC 17025 facilities from QTS Service and Westcal ease the burden, yet they remain insufficient to meet national demand. Delays complicate project timelines, elevate working-capital requirements, and erode price competitiveness, particularly for small and medium providers. Customers are increasingly factoring calibration turnaround time into their vendor selection, influencing competitive dynamics within the UAE NDT market.

Workforce Certification Gaps Constrain Advanced Inspection Capabilities

The demand for ASME and PCN Level-III personnel exceeds the local supply, as evidenced by the persistent job postings for advanced NDT inspectors.[3]ICM Careers, “Advanced NDT Inspector,” ICMPEOPLE.COM Nuclear and petrochemical projects require high-level certifications, necessitating a reliance on expatriate experts whose availability dictates scheduling flexibility. Training schemes are expanding, but Level-III pathways require years of practical exposure, meaning talent shortages will persist in the medium term. This bottleneck limits the scale-up of complex projects and reinforces premium wage structures across the UAE NDT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Preference Drives Outsourcing Efficiencies

Services accounted for 77.8% of the UAE NDT market size in 2024, underscoring operator preference for vendor-managed inspection programs over internal equipment ownership. Certified providers absorb capital expenditure, staff training, and calibration responsibilities, offering turnkey compliance in return for predictable operating fees. AI-enabled data analytics embedded in service contracts further reduce downtime, strengthening the business case for outsourcing.

Software is the fastest-growing component, rising at a 12.6% CAGR to 2030 as digital twins, predictive algorithms, and cloud dashboards become standard. Equipment and consumables remain essential yet grow more slowly, feeding the service ecosystem with specialized tools and materials. The interplay of these segments positions service firms at the center of value creation in the UAE NDT market, while customers focus capital on core operations rather than inspection assets.

By Testing Method: Ultrasonic Dominance and Eddy-Current Momentum

Ultrasonic testing captured a 26.5% UAE NDT market share in 2024, prized for versatility in thickness gauging, phased-array flaw detection, and weld inspection. Its compatibility with robotic crawlers and wall-climbing devices extends reach into high-risk environments, reinforcing its leadership.

Eddy-current testing is experiencing a 9.6% CAGR, benefiting from the rapid, contactless detection of surface and near-surface defects in heat exchangers and aircraft components. Automated probe arrays and AI-driven signal analysis reduce inspection cycles, facilitating widespread adoption across petrochemical and transportation assets. Radiography, magnetic particle, and liquid penetrant methods retain niche relevance, while thermography and computed tomography address specialized imaging needs. Collectively, method diversification offers operators a toolkit that spans real-time screening to in-depth characterization within the UAE NDT market.

By Technique: AI-Enabled Innovation Transforms Predictive Maintenance

Conventional techniques still accounted for 86.9% of the UAE NDT market size in 2024, driven by code compliance and established inspector skill sets. However, AI-enabled approaches are surging at 15.7% CAGR, propelled by pattern-recognition accuracy and automated defect classification that reduce manual review effort.

Hybrid workflows emerge as best practice: AI tools rapidly screen vast datasets, flagging anomalies for targeted conventional follow-up that satisfies regulatory documentation. Early adopters report measurable cost benefits, such as Dubai Municipality’s eight-minute material-testing turnaround, compared to the previous four days. As training datasets grow and cloud-security concerns abate, AI penetration will deepen, reshaping competitive differentiation within the UAE NDT market.

By End-User Industry: Oil and Gas Scale, Automotive Acceleration

Oil and gas held 24.2% of the UAE NDT market share in 2024, driven by complex upstream projects, downstream upgrades, and pipeline integrity mandates. Regular shutdown inspections, RBI programs, and new build commissioning together sustain high service intensity.

The automotive and transportation sectors are projected to grow at a 9.5% CAGR through 2030, driven by local vehicle assembly initiatives and the expansion of electric mobility infrastructure. Standards require extensive inspections of welds, castings, and composites, creating new opportunities for providers. Aerospace, defense, and power generation maintain steady demand, while electronics, marine, and medical devices add incremental volume. Diversified sectoral exposure mitigates cyclical risk and widens the opportunity pool for the UAE NDT industry.

Geography Analysis

The UAE NDT market concentrates in Abu Dhabi and Dubai, yet each emirate contributes distinct demand layers. Abu Dhabi anchors upstream oil, gas processing, and nuclear power assets, guaranteeing baseline inspection volumes over multiple decades. ADNOC’s headquarters and Barakah’s long-term ISI schedules require nuclear-qualified providers and sustain specialized calibration services. Dubai complements this with smart-city infrastructure, aviation hubs, and maritime logistics that emphasize AI-enhanced inspection and rapid turnaround.

Sharjah’s industrial zones add manufacturing and logistics requirements, while the Northern Emirates contribute utilities and infrastructure projects. Harmonized standards under FANR and ENAS allow providers to operate seamlessly across emirates, pooling talent and equipment. Free zones facilitate the importation of specialized tools, enabling foreign firms to establish regional bases. Consequently, the UAE serves as a springboard for GCC expansion, with providers leveraging domestic credentials to capture work in Saudi Arabia, Oman, and Qatar.

Digital infrastructure advantages, including 5G networks and government-backed cloud platforms, accelerate the adoption of predictive inspection. Combined with geopolitical stability and pro-business regulation, these factors cement the UAE’s role as a regional hub for advanced non-destructive testing services.

Competitive Landscape

Global TIC majors such as SGS Gulf Limited, Bureau Veritas, TÜV Rheinland, and Intertek hold sizable contract portfolios, leveraging worldwide expertise, method certifications, and integrated laboratories. Regional specialists, NDTCCS, Qualitas Material Testing Laboratories, and emerging tech firms, compete through rapid mobilization, localized pricing, and niche capabilities. Technology-centric newcomers, including Gecko Robotics and CorrosionRADAR, differentiate on AI and robotics, winning multi-million-dollar agreements with ADNOC and other operators.[4]Semafor, “Gecko Robotics plans to double UAE footprint,” SEMAFOR.COM

Strategic alliances underpin market success. Trendspek’s partnership with Applus+ yields AI-driven defect-recognition tools that feed into Applus+ field operations. FOERSTER Middle East’s collaboration with VisiConsult broadens advanced X-ray coverage. Such alliances accelerate technology transfer and bypass lengthy certification cycles.

Regulatory compliance remains a core differentiator. Providers with nuclear-grade qualifications, ISO/IEC 17025 laboratories, and rope-access safety certifications secure higher-value contracts. The convergence of digital innovation and stringent standards favors operators capable of integrating AI analytics with robust quality systems, shaping the next phase of competition in the UAE NDT market.

UAE NDT Industry Leaders

SGS Gulf Limited

Olympus Middle East FZE

MISTRAS Group Middle East

Zetec Inc - Middle East

Eddyfi Technologies FZE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NTS Group acquired Amega West Services, adding eight global facilities and expanding repair capabilities for MWD/LWD and drilling equipment.

- April 2025: The UAE Ministry of Economy signed an MoU with SGS Gulf Limited to enhance quality control for food and consumer products across seven emirates.

- March 2025: SGS Gulf Limited expanded electrical and electronic testing at its Dubai Center of Excellence, adding eight technical experts and advanced equipment.

- February 2025: Gecko Robotics announced plans to double its UAE robot fleet to 40-50 units under a USD 30 million ADNOC Gas contract.

UAE NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional/ Conventional |

| AI-enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| Consumables | |

| By Testing Method | Ultrasonic Testing |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional/ Conventional |

| AI-enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and Semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

What is the forecast value of the UAE NDT market by 2030?

The UAE NDT market is projected to reach USD 970.8 million by 2030.

Which segment currently leads by component?

Services dominate with a 77.8% share in 2024.

How fast are AI-enabled techniques growing?

AI-enabled inspection techniques are advancing at a 15.7% CAGR through 2030.

Which testing method is expected to grow the quickest?

Eddy-current testing is projected to post a 9.6% CAGR from 2025 to 2030.

Why are calibration facilities a restraint?

Limited local ISO/IEC 17025 labs result in longer equipment turnaround times, which increases project costs.

Which industry outside oil and gas shows the highest growth potential?

The automotive and transportation sector is forecast to expand at a 9.5% CAGR through 2030.

Page last updated on: