Japan NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

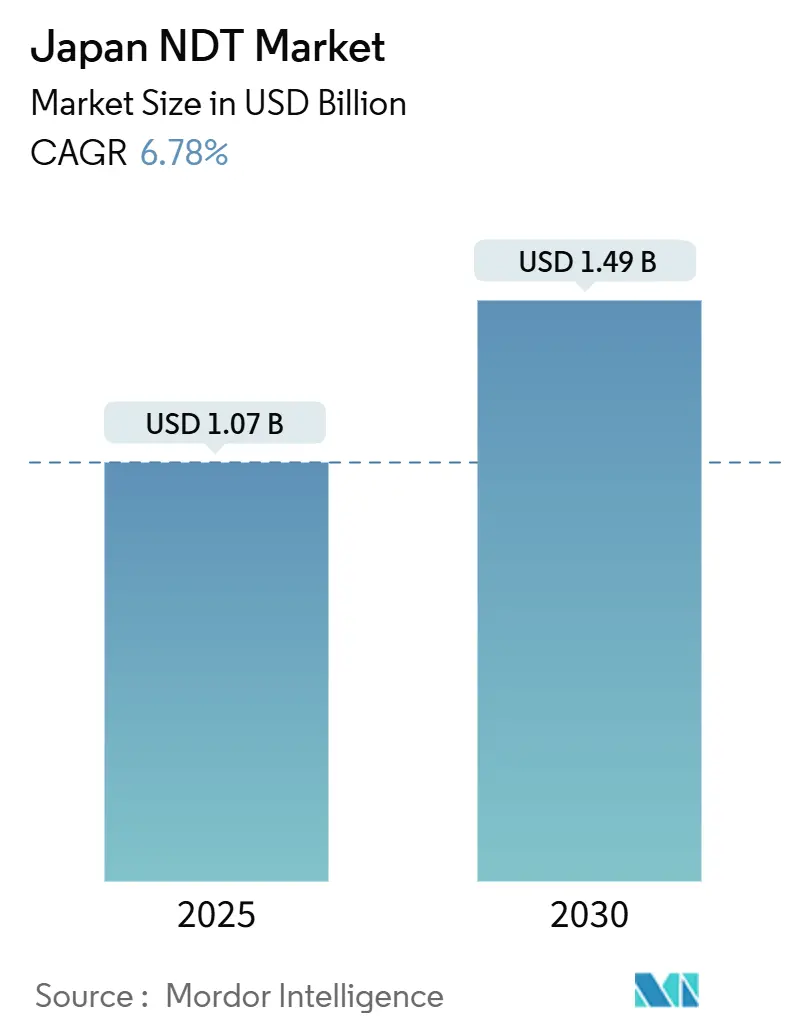

| Market Size (2025) | USD 1.07 Billion |

| Market Size (2030) | USD 1.49 Billion |

| Growth Rate (2025 - 2030) | 6.78% CAGR |

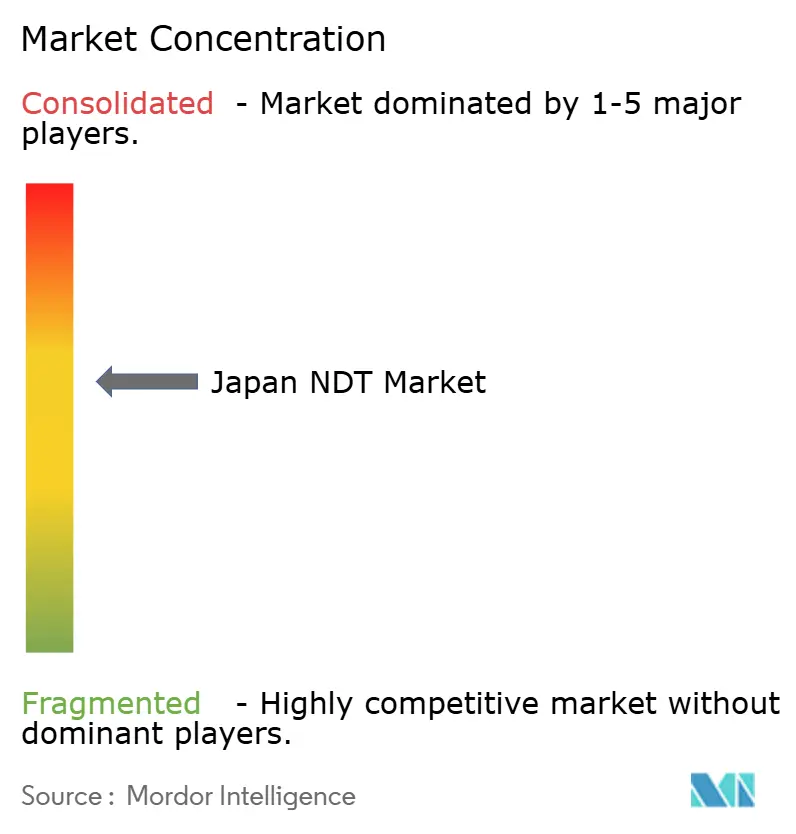

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan NDT Market Analysis by Mordor Intelligence

The Japan NDT market size is estimated at USD 1.07 billion in 2025 and is projected to reach USD 1.49 billion by 2030, representing a 6.78% CAGR over the forecast period. Robust capital spending on infrastructure rehabilitation, semiconductor capacity expansion, and aerospace maintenance drives steady demand, while government subsidies and digital factory incentives accelerate the adoption of data-centric inspection platforms. Clusters in Tokyo, Kyushu, and the Chūkyō industrial corridor drive growth by hosting aircraft MRO hangars, chip fabs, and high-precision automotive plants that require certified non-destructive testing. Rising investments in the hydrogen economy, stricter asset-life regulations, and Industry 4.0 programs are widening the addressable base for automated ultrasonic, eddy-current, and AI image-analysis equipment. At the same time, the limited availability of Level-III personnel and the high cost of phased-array systems encourage hybrid service models, cloud analytics, and remote diagnostics that reduce on-site person-hours while satisfying Japan’s strict quality standards.

Key Report Takeaways

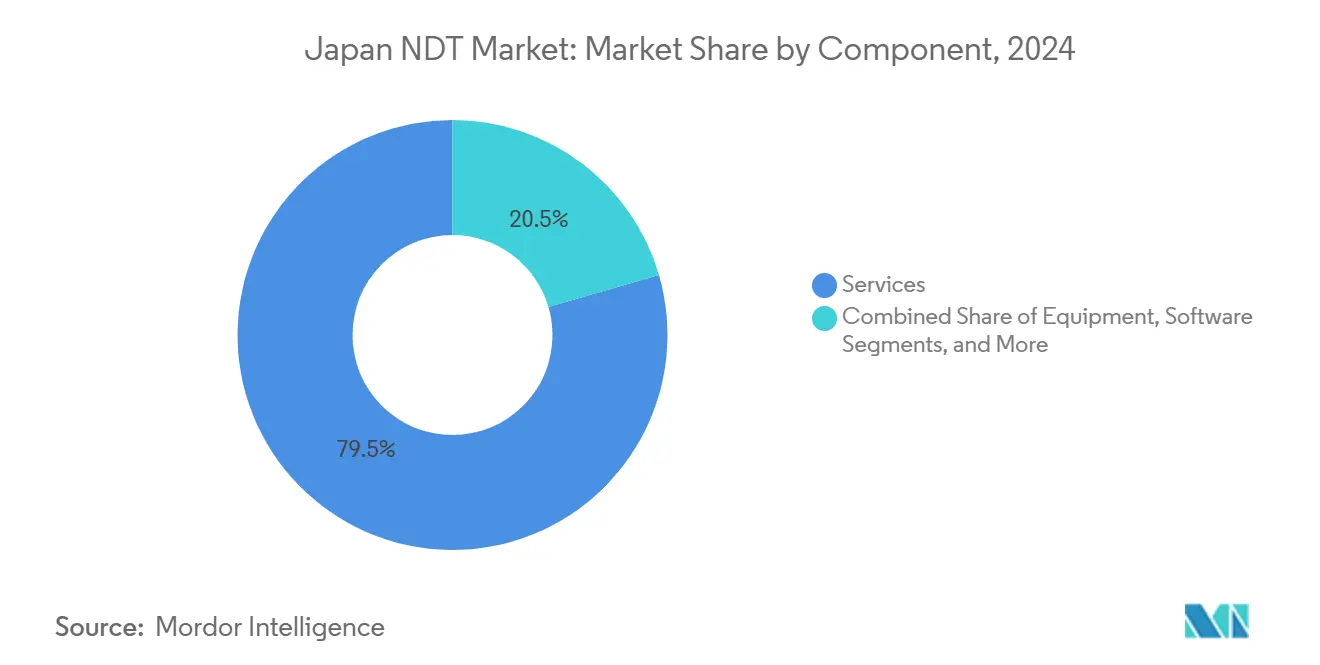

- By component, services captured 79.5% of the revenue in 2024; software exhibits an 11.6% CAGR through 2030.

- By testing method, ultrasonic testing led the Japan NDT market with a 28.2% share in 2024, while eddy-current testing is expected to advance at an 8.6% CAGR through 2030.

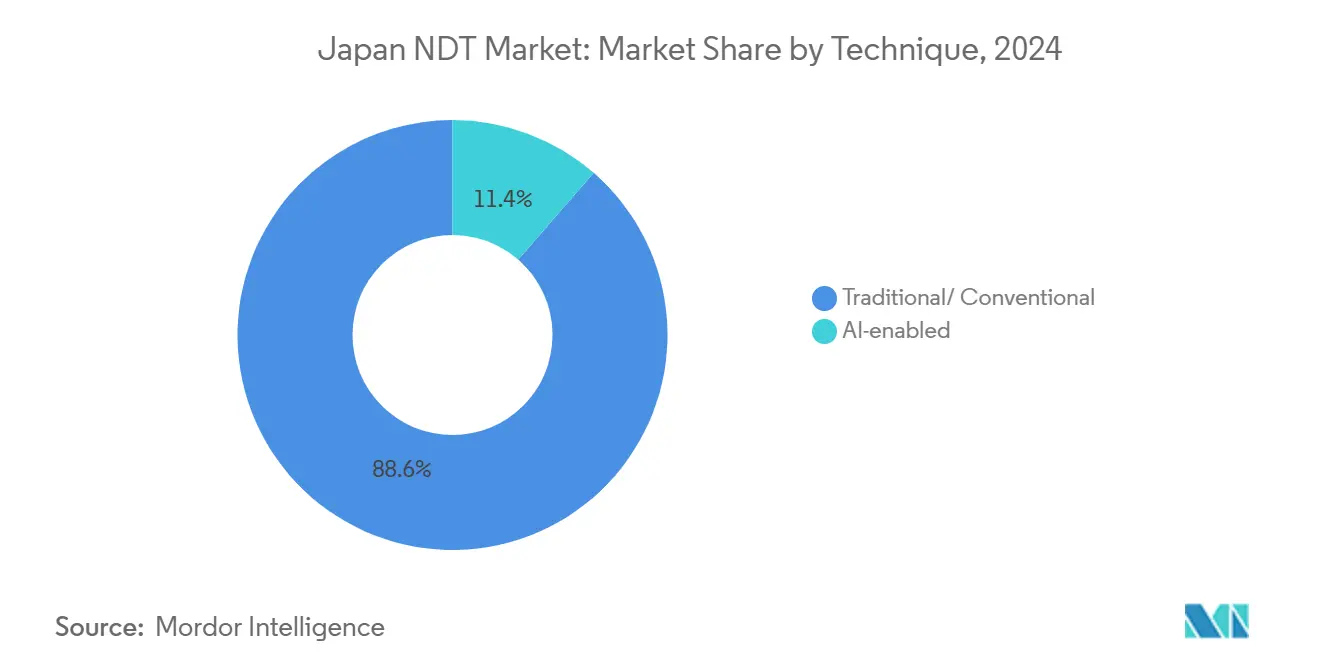

- By technique, conventional inspection accounted for an 88.6% share of the Japan NDT market size in 2024; AI-enabled approaches are expected to expand at a 14.7% CAGR to 2030.

- By end-user, oil and gas held a 25.7% share in 2024; automotive and transportation are forecast to grow the fastest at an 8.5% CAGR to 2030.

Japan NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing industrial infrastructure-driven inspection demand | +1.8% | National, with a concentration in the Tokyo Metropolitan area and industrial corridors. | Long term (≥ 4 years) |

| Emergence of a hydrogen economy requires new material inspections | +1.2% | National, with early deployment in Kyushu and industrial clusters | Medium term (2-4 years) |

| Government subsidies for smart factory adoption | +1.0% | National, prioritizing SME manufacturing regions | Short term (≤ 2 years) |

| Growing aircraft MRO activity at Haneda and Narita hubs | +0.8% | Tokyo Metropolitan area, extending to Osaka and the regional airports | Medium term (2-4 years) |

| Semiconductor fab capacity expansion in the Kumamoto cluster | +0.7% | Kyushu region, spillover to the national supply chain | Short term (≤ 2 years) |

| The rise of AI-based analytics is improving the probability of detection | +0.9% | Global adoption with Japanese technology leadership | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Industrial Infrastructure

Roughly 60% of road bridges and 40% of tunnels will exceed 50 years of service by 2033, forcing municipalities to outsource comprehensive NDT programs.[1]NewsonJapan Editors, “Aging infrastructure a major roadblock to Japan's future,” newsonjapan.com The central government earmarked JPY 15 trillion (USD 100 billion) for disaster-prevention projects that stipulate ultrasonic, infrared, and AI-vision inspections rather than visual checks alone. Urban-X Technologies’ smartphone-based crack-detection platform is already deployed by 54 local authorities, demonstrating a scalable model for cash-constrained cities. University of Tokyo engineers have validated a ground-penetrating radar that scans pavement at 80 km/h, promising to reduce lifetime repair costs by up to 30%. Together, fiscal urgency, aging assets, and proven cost savings create a multi-decade pipeline for service providers.

Hydrogen-Economy Material Requirements

Hydrogen-charged steel exhibits crack growth rates up to 10 times higher than uncharged metal, rendering conventional inspection methods inadequate. Japanese universities developed custom eddy-current coils and acoustic protocols that locate embrittlement sites without de-pressurizing pipelines, cutting outage time. Pilot electrolyzer arrays in Kyushu require monthly phased-array monitoring because of ammonia-related stress corrosion. Equipment makers now market probes calibrated for hydrogen partial pressures, opening a premium niche for the Japan NDT market. Government export goals for carbon-free ammonia spur early adoption and create experience advantages for local vendors over global rivals.

Smart-Factory Subsidies

The Monozukuri program reimburses 50-67% of qualified machinery spending up to JPY 30 million (USD 200,000) per project, widening access to inline X-ray, phased-array, and machine-vision systems. Additional tax credits cover cloud analytics and digital twins under JETRO’s digital-transformation incentives.[2]JETRO, “Government initiatives for manufacturing,” jetro.go.jp As factory labor shrinks by 40% by 2065, robots and AI analytics become vital for throughput, positioning software vendors for double-digit revenue growth. The grants also enable SMEs in regional clusters to lease rather than purchase high-cost scanners, thereby accelerating the nationwide diffusion.

Aircraft MRO Activity Expansion

JAL Engineering employs 4,600 technicians across Haneda, Narita, and Osaka, and is reshoring component repair from Southeast Asia to cut turnaround times. A partnership with Mitsubishi Heavy Industries targets regional aircraft checks, feeding demand for NAS 410-qualified inspectors and ultrasonic borescopes. NANDTB-Japan, administered by JSNDI, streamlines certification within the country, lifting barriers for new entrants. Steady 5% annual growth in global civil fleets underpins a resilient pipeline for local specialists well into the 2030s.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Level-III certified NDT inspectors | -1.5% | National, acute in the nuclear and aerospace sectors | Long term (≥ 4 years) |

| High capex of phased-array ultrasonic systems | -0.9% | National, affecting SME adoption rates | Medium term (2-4 years) |

| Stringent radiation regulations are slowing radiographic testing | -0.7% | National, concentrated in industrial and nuclear regions | Medium term (2-4 years) |

| OEM reluctance to share digital twin data with NDT vendors | -0.4% | National, primarily affecting the automotive and aerospace sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Level-III Inspectors

CRIEPI’s performance-demonstration data show a decline in new Level-III applicants since 2011, while the average inspector age continues to rise. Hyogo Prefecture’s aviation NDT school can train only five participants per session, underscoring capacity gaps. Employer-based NAS 410 schemes impose in-house qualification costs on companies, thereby delaying workforce replenishment. Consequently, service firms face scheduling bottlenecks and must deploy automated scanners or remote-analysis software to offset human scarcity.

High Capex of Phased-Array Systems

Basic operator training for an OmniScan X3 costs JPY 72,000 (USD 480), and full instruments retail above JPY 10 million, straining SME budgets.[3]Evidence Scientific Training Academy, “Japan Class 02 Course,” evidentscientific.com Complex 128-channel electronics and multi-axis scanners increase the capital load, despite throughput gains of 10-50 times that of single-probe setups. Some relief comes from 67% subsidy coverage under the Monozukuri scheme; yet, many firms still opt to outsource inspections, reinforcing service segment dominance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component – Services Dominate a Mature Landscape

Services accounted for 79.5% of the Japanese NDT market in 2024, indicating a preference for outsourced expertise and liability coverage across nuclear, aerospace, and automotive lines. Certified vendors manage compliance paperwork, deliver Level III personnel, and amortize capital-intensive scanners across multiple jobs. Software, though still a smaller slice, posts the fastest 11.6% CAGR as factories digitize inspection archives and deploy AI pattern recognition. These platforms combine phased-array waveforms with digital twins, enhancing maintenance scheduling and improving overall equipment effectiveness. Equipment sales remain steady because subsidies offset up-front pricing, while consumables grow in line with inspection volume.

By Testing Method – Ultrasonic Rules, Eddy-Current Accelerates

Ultrasonic testing led with 28.2% share in 2024, thanks to versatile phased-array and time-of-flight diffraction systems validated in nuclear and semiconductor fabs. Matrix arrays scan complex welds, turbine blades, and chip-etch chambers without disassembly, making them indispensable for these applications. Eddy-current techniques, expanding at 8.6% CAGR, detect hydrogen-induced flaws and surface micro-cracks in EV battery casings, fuel cells, and thin aerospace skins. Radiography faces regulatory friction due to 30-day notification rules for new X-ray units. Magnetic particle, liquid penetrant, and visual testing sustain niche roles in MRO hangars and forged-parts shops, often augmented by AI image analytics.

By Technique – AI-Enabled Tools Gain Traction

Conventional approaches still accounted for 88.6% of the testing volume in 2024, underpinned by conservative approval cycles in nuclear and aerospace regulation. Yet, AI-enabled modalities register a robust 14.7% CAGR, as printable photo-thermoelectric sensors, high-resolution IR cameras, and cloud algorithms enhance the probability of detection and reduce false positives. JSNDI working groups integrate ISO-23865 NDE 4.0 guidelines, allowing certified technicians to adopt AI classifiers without resetting qualification clocks. Hybrid workstations that combine automated robotic scans with real-time AI scoring bridge the skills gap and maintain legacy procedures during the transition period.

By End-User Industry – Electrification Reshapes Demand

Oil and gas facilities accounted for 25.7% of 2024 revenue as refinery towers, LNG tanks, and ammonia terminals undergo mid-life overhauls. Simultaneously, automotive and transportation spending grows at an 8.5% CAGR, driven by EV battery lines, lightweight aluminum welds, and hydrogen-ready drivetrains that require higher-frequency ultrasound and eddy-current probes. Kumamoto’s semiconductor cluster injects fresh demand for wafer-fab tool calibration and ultra-clean material certification, linked to TSMC’s USD 20 billion investment. Aerospace, defense, and power generation remain core workloads, each shaped by long-cycle maintenance mandates and public safety scrutiny.

Geography Analysis

The Tokyo metropolitan area hosts the densest concentration of certified labs because it combines Haneda and Narita airports, major petrochemical complexes in Chiba, and corporate headquarters that manage nationwide assets. Frequent heavy-check schedules for wide-body jets keep ultrasonic, radiographic, and magnetic particle inspection benches running near capacity, while proximity to regulator offices speeds up procedure approvals.

Kyushu follows as a high-growth zone. TSMC’s dual-fab project in Kumamoto, along with Fujifilm’s JPY 6 billion materials plant, fuels intensive inspections of cleanroom piping, CMP tools, and vacuum chambers.[4]Fujifilm Corporation, “Investment in Kumamoto site,” fujifilm.com Hydrogen pilot pipelines leverage the region’s petrochemical know-how, creating a sandbox for embrittlement-focused PAUT and eddy-current procedures.

Industrial arteries stretching from Osaka to Nagoya balance mature heavy-engineering fleets with fresh smart-factory retrofits backed by Monozukuri grants. Here, SMEs utilize cost-shared robots that integrate visual and ultrasonic tasks, while remote experts in Tokyo review datasets to mitigate inspector shortages. Coastal nuclear stations in Shikoku and Tōhoku maintain a steady baseline for certified ultrasonic crews under CRIEPI protocols, reinforcing nationwide skills distribution.

Competitive Landscape

Market concentration remains moderate, with Olympus-born Evident, Fujifilm, Nikon, and Hitachi offering broad product suites, while SGS Japan and Bureau Veritas dominate the service outsourcing sector. Bain Capital’s 2024 takeover of Evident supplies fresh R&D capital for automated scanners and AI analytics, raising the stakes for innovation. Fujifilm leverages imaging expertise to cross-sell computed radiography plates to semiconductor OEMs, and Nikon integrates metrology optics with X-ray CT for electric-vehicle battery packs.

Local distributors of high-channel phased-array units tap Monozukuri rebates to penetrate SME workshops, while JSNDI’s employer-based certification schema creates switching costs that lock in incumbent vendors. At the same time, university spin-offs commercialize lightweight IR sensors and AI software, often licensing to mid-tier service firms that address rural municipalities unable to hire full Level-III teams.

Strategic alliances flourish: Mitsubishi Heavy Industries collaborates with JAL Engineering on regional jet maintenance; Hitachi pairs with cloud integrators to stream ultrasonic data into plant digital twins; and semiconductor fabs co-develop cleanroom-qualified probes with tooling suppliers. This ecosystem rewards firms that combine hardware reliability, data interoperability, and training services, rather than focusing solely on the sale of pure-play equipment.

Japan NDT Industry Leaders

Olympus Corporation

Eddyfi Technologies Japan K.K.

Mistras Group K.K.

Zetec Japan Inc.

SGS Japan Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kumamoto’s second TSMC fab set to break ground in 2025, lifting local inspection demand for wafer-processing equipment.

- June 2025: METI issued JIS A 5016 and revised JIS A 4717, standardizing slag and impact tests that require accredited NDT protocols.

- May 2025: Japan Electron Materials opened its fourth probe-card component plant in Kikuchi City, forecasting a 30% production jump and new ultrasonic micro-weld inspections.

- April 2025: Shimadzu bought California X-ray Imaging Services to strengthen global service reach and grow medical-systems sales to JPY 82 billion by FY 2025.

Japan NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional/Conventional |

| AI-enabled |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and Semiconductor |

| Mining |

| Medical Devices |

| Others |

| By Component | Equipment |

| Software | |

| Services | |

| Consumables | |

| By Testing Method | Ultrasonic Testing |

| Radiographic Testing | |

| Magnetic Particle Testing | |

| Liquid Penetrant Testing | |

| Visual Inspection Testing | |

| Eddy-Current Testing | |

| Acoustic Emission Testing | |

| Thermography / Infrared Testing | |

| Computed Tomography Testing | |

| By Technique | Traditional/Conventional |

| AI-enabled | |

| By End-user Industry | Oil and Gas |

| Power Generation | |

| Aerospace | |

| Defense | |

| Automotive and Transportation | |

| Manufacturing and Heavy Engineering | |

| Construction and Infrastructure | |

| Chemical and Petrochemical | |

| Marine and Ship Building | |

| Electronics and Semiconductor | |

| Mining | |

| Medical Devices | |

| Others |

Key Questions Answered in the Report

What is the size of the Japan NDT market in 2025?

It stands at USD 1.07 billion and is forecast to grow at a 6.78% CAGR to reach USD 1.49 billion by 2030.

Which component dominates spending?

Services account for 79.5% of 2024 revenue, as they bundle Level-III talent, certification, and capital-intensive scanners.

What testing method is growing the fastest?

Eddy-current testing is projected to post an 8.6% CAGR through 2030, driven by hydrogen embrittlement and EV battery applications.

Why is Kyushu an emerging hotspot?

TSMC’s dual-fab build-out in Kumamoto and Fujifilm’s materials plant create a steady demand for inspection equipment in cleanrooms.

What subsidy supports NDT equipment purchases?

The Monozukuri program covers 50-67% of qualified machinery costs up to JPY 30 million, including phased-array and X-ray systems.

How severe is the inspector shortage?

Level-III applicant numbers have declined for a decade, reducing pipeline capacity and adding a 1.5% drag on market CAGR.

Page last updated on: