Japan Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

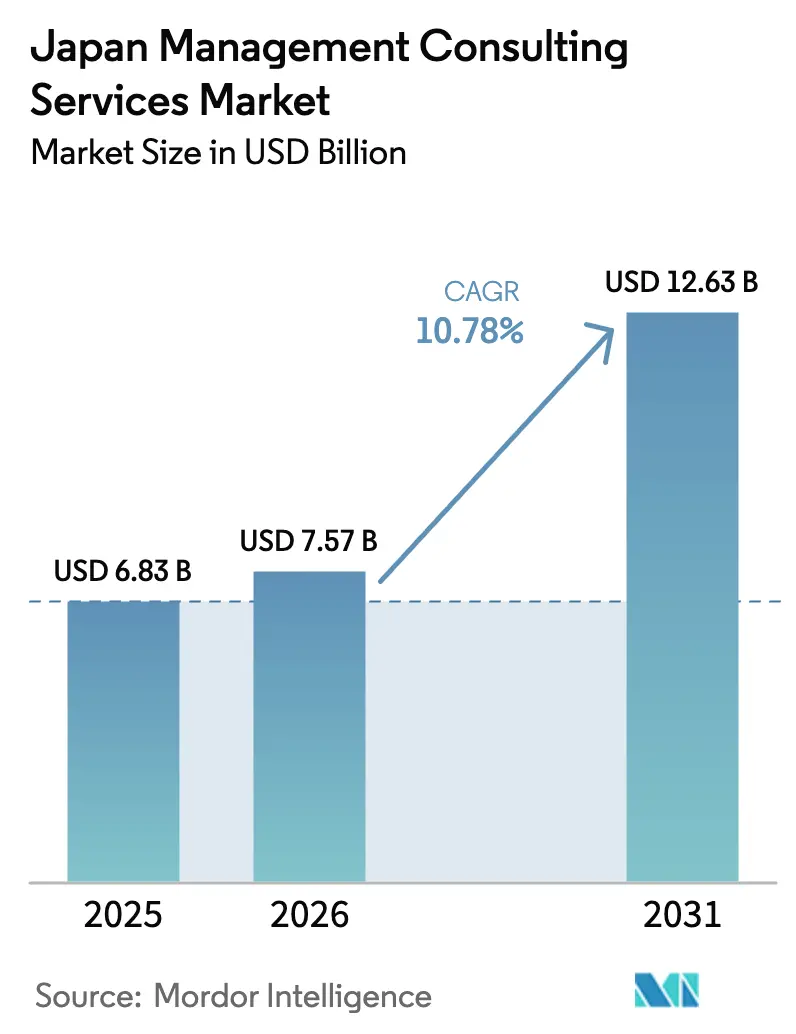

| Base Year Market Size (2025) | USD 6.83 Billion |

| Market Size (2026) | USD 7.57 Billion |

| Market Size (2031) | USD 12.63 Billion |

| Growth Rate (2026 - 2031) | 10.78% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Management Consulting Services Market Analysis by Mordor Intelligence

The Japan management consulting services market size is expected to grow from USD 6.83 billion in 2025 to USD 7.57 billion in 2026 and is forecast to reach USD 12.63 billion by 2031 at 10.78% CAGR over 2026-2031. The current market size reflects strong demand from both public and private sector transformation programs that combine digital-transformation (DX) targets with green-transformation (GX) mandates imposed by Tokyo. Heightened regulatory complexity, demographic pressures, and a nationwide pivot toward data-driven productivity have turned consulting engagements from advisory-only projects into execution-heavy partnerships that embed consultants inside client operating models. The coexistence of DX and GX obligations has created an unprecedented dual catalyst: enterprises must modernize IT systems while simultaneously aligning capital projects with net-zero pathways, an overlap that pushes boards to source outside expertise quickly. In parallel, rapid gains in generative-AI capability, widening subsidy frameworks, and record levels of corporate cash reserves continue to unlock discretionary budgets for large-scale change initiatives across financial services, manufacturing, healthcare, and energy verticals.[1]Information-technology Promotion Agency, “DX Trends 2024,” ipa.go.jp

Key Report Takeaways

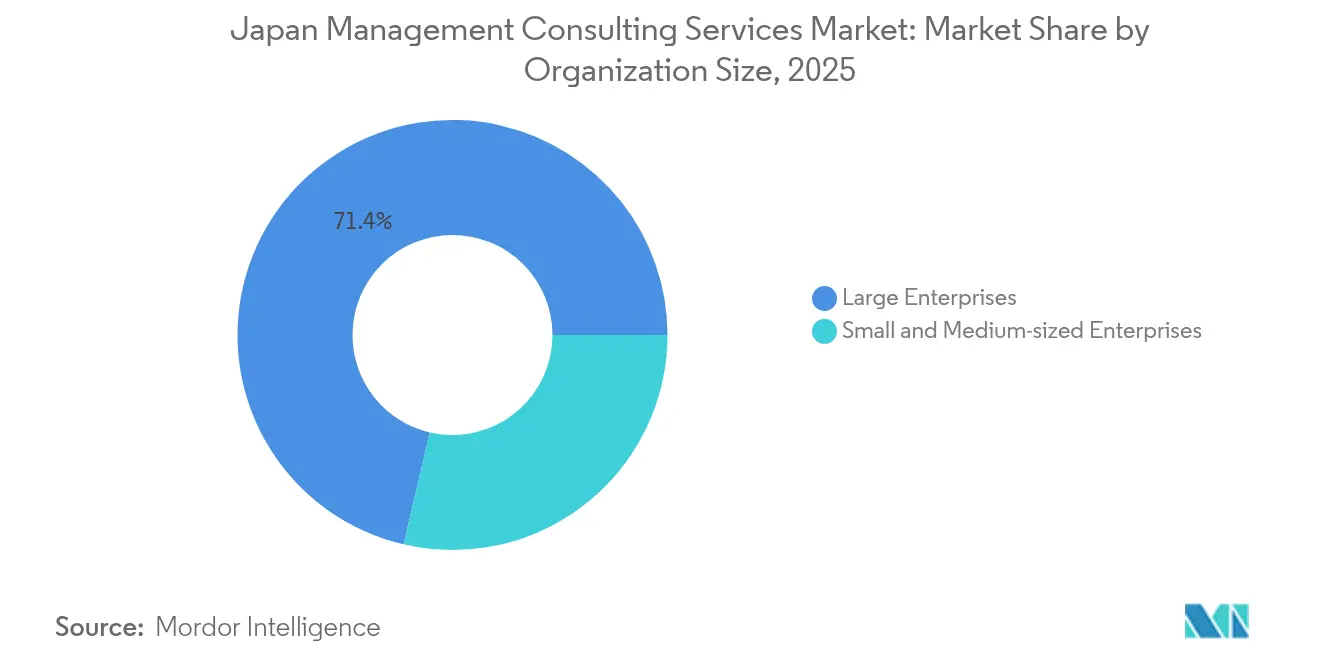

- By organization size, large enterprises held 71.35% of Japan management consulting services market share in 2025, whereas small and medium-sized enterprises are advancing at a 14.05% CAGR through 2031.

- By service type, operations consulting controlled 27.55% revenue in 2025, but technology consulting is expanding at a 13.25% CAGR on the back of generative-AI deployments.

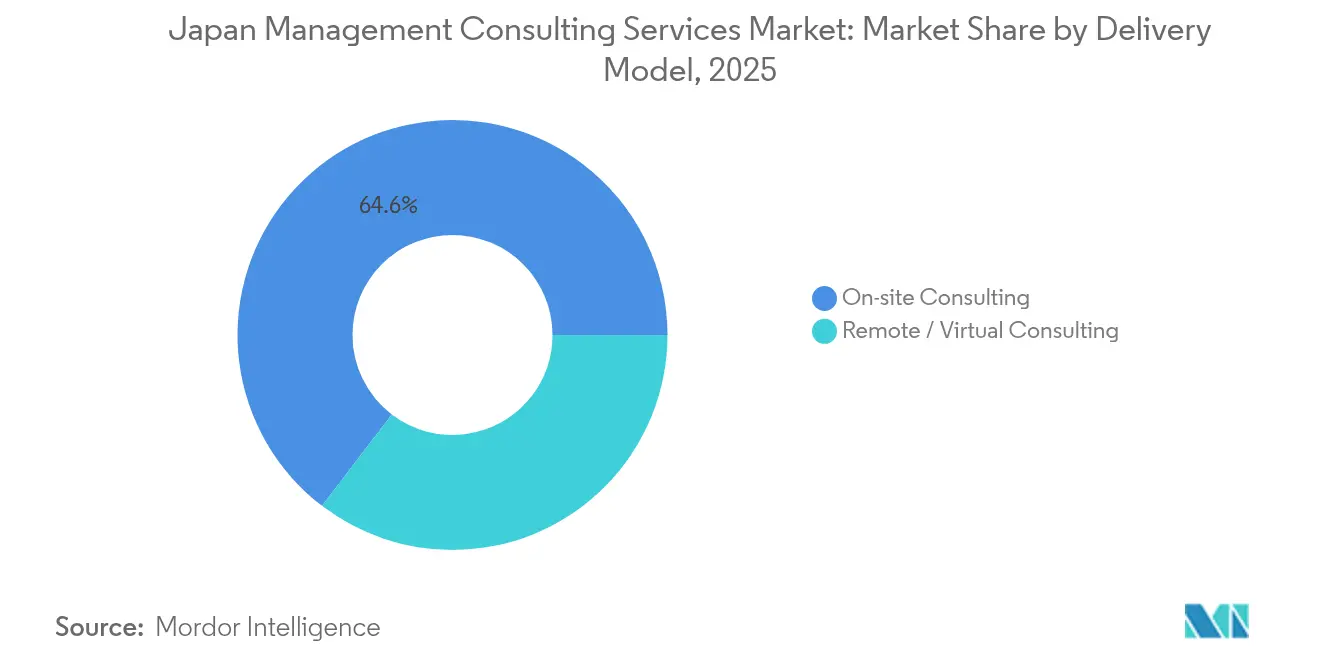

- By delivery model, on-site consulting retained 64.62% revenue in 2025, while remote and virtual engagements are rising at a 14.22% CAGR as regulatory barriers on data usage ease.

- By end-user industry, financial services commanded 27.12% of the Japan management consulting services market size in 2025, yet healthcare and life sciences represent the fastest trajectory with a 13.75% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating corporate digital-transformation (DX) spending | +2.80% | National, with concentration in Tokyo, Osaka, Nagoya metropolitan areas | Medium term (2-4 years) |

| Mandatory Green-Transformation (GX) subsidy compliance consulting surge | +2.10% | National, with early adoption in industrial regions | Short term (≤ 2 years) |

| Ageing-workforce productivity pressure on Japanese firms | +1.90% | National, with acute impact in rural manufacturing regions | Long term (≥ 4 years) |

| Post-pandemic hybrid / remote operating-model optimisation | +1.40% | National, with urban-rural hybrid adoption patterns | Medium term (2-4 years) |

| Reshoring of critical supply-chains under economic-security law | +1.60% | National, with priority in strategic industrial sectors | Medium term (2-4 years) |

| SME succession-planning boom amid record retirements | +1.80% | National, with concentration in traditional manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Corporate Digital-Transformation (DX) Spending

DX budgets have shifted from back-office automation to end-to-end business-model redesign. Government programs under the Digital Agency’s “Priority Plan for a Digital Society” call for seamless data interchange among municipalities, catalysing demand for consulting roadmaps that integrate legacy core systems with cloud-native stacks. Enterprise boards increasingly view DX as existential, committing multi-year funds to transform supply chains, customer experience, and cybersecurity layers. Consultants now deliver “AI-transformation” (AIX) offerings that bundle algorithm design, data-governance re-architecture, and workforce reskilling into single statements of work.[2]PR TIMES, “Launch of AIX Consulting Services,” prtimes.jp Market growth further benefits from Tokyo’s fast-tracking of open-API standards and public data lakes, which shortens pilot-to-scale timelines and raises client appetite for outcome-based fee models.

Mandatory Green-Transformation (GX) Subsidy Compliance Consulting Surge

The JPY 150 trillion GX roadmap relies on subsidy and tax-incentive instruments that obligate corporations to file voluminous technical documentation. Clients turn to consultancies for lifecycle carbon-accounting toolkits, technology due-diligence, and financial-model alignment needed to access Contracts-for-Difference support for clean-hydrogen, green-steel, and battery projects. Deep-tech startups vying for NEDO grants also request assistance in proposal drafting, commercialization strategies, and partner matchmaking. As a result, GX engagements often span regulatory interpretation, engineering economics, and supply-chain localization within multi-phase scopes lasting up to five years.

Ageing-Workforce Productivity Pressure on Japanese Firms

Japan will lose roughly 5.3 million workers by 2030, a demographic reality that forces even family-owned suppliers to automate assembly lines, redeploy retirees into knowledge-transfer roles, and recruit foreign language talent.[3]Carnegie Endowment, “Japan’s Aging Society as a Technological Opportunity,” carnegieendowment.org Consultants design lean-manufacturing frameworks, augmented-reality training modules, and robotic process automation sprints that reduce head-count dependency without sacrificing craftsmanship. Manufacturing clusters in Aichi and Shizuoka are piloting “Smart Manufacturing” blueprints that emphasize digital twins, predictive maintenance, and 5G-enabled quality analytics. The healthcare system mirrors these pressures, relying on advisory support to integrate AI-assisted diagnostics that offset nursing shortages in aging prefectures.

Post-Pandemic Hybrid Remote Operating-Model Optimisation

With clients now comfortable mixing physical workshops and online collaboration, firms package hybrid-delivery playbooks that standardize cadence, milestones, and cloud-whiteboard tooling. Proposed 2025 amendments to the Act on the Protection of Personal Information will let enterprises reuse anonymized data for AI-model training, materially expanding the scope of remote engagements. Freelance platforms signal market acceptance: roughly 70% of projects published in 2025 allow hybrid work structures, underscoring cultural normalization of video-first interactions. Consulting proposals increasingly bundle workplace culture change, security-by-design, and performance-management redesign.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price competition from freelance platforms | -1.20% | National, with concentration in Tokyo metropolitan area | Short term (≤ 2 years) |

| Consulting-talent attrition due to start-up ecosystem growth | -0.90% | National, with acute impact in Tokyo, Osaka innovation hubs | Medium term (2-4 years) |

| Rising client scrutiny over billable-hour models | -0.70% | National, with emphasis in cost-conscious SME segment | Medium term (2-4 years) |

| Data-privacy regulations restricting remote-delivery scope | -0.50% | National, with varying interpretation across industries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Competition from Freelance Platforms

Platforms such as Another works disclose median monthly consulting fees of JPY 1.2 million, roughly 30 to 40% below traditional firm rates, squeezing margins especially on standardized IT-implementation work. Transparency around rates encourages procurement teams to benchmark aggressively, prompting incumbent firms to adopt modular pricing or subscription-based support. Nevertheless, enterprises still lean on brand-name consultants for board-level credibility and regulatory assurance, which mitigates complete commoditization.

Consulting-Talent Attrition Due to Startup Ecosystem Growth

NEDO’s multibillion-yen deep-tech funds and corporate venture initiatives entice senior associates to swap fee income for equity upside. Firms counter by launching internal venture studios and fast-track-to-partner schemes, yet attrition persists, especially in AI and sustainability practices that overlap with active startup domains. Talent competition remains acute in Tokyo’s Marunouchi and Osaka’s Umeda districts, where venture accelerators cluster.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SME Transformation Accelerates

The small and medium-sized enterprise segment accounted for 28.65% of the Japan management consulting services market size in 2025 and is growing at 14.05% CAGR, markedly above the overall trajectory. Much of this velocity stems from supply-chain-transparency clauses inside the Economic Security Promotion Act that apply to vendors regardless of capitalization, compelling SMEs to seek external guidance on data-collection frameworks and cyber-resilience audits. Freelance marketplaces further democratize access by matching niche experts to project-based mandates at transparent price points, enabling owner managers to commission targeted deliverables instead of multi-year retainers. Consulting mandates often focus on hands-on ERP rollouts, subsidy paperwork, and successor-training programs aimed at mitigating founder-retirement risks.

Large enterprises still dominate project value, holding 71.35% of the Japan management consulting services market share in 2025. Budgets cover continent-spanning PMI programs and AI-factory conversions, such as Shiseido’s eleven-country FOCUS platform executed with a global consulting consortium. These blue-chip clients value integrated teams that blend strategy, design, and managed services within unified governance structures, securing long-term wallet share for tier-one firms.

By Service Type: Technology Consulting Dominates Growth

Operations consulting retained 27.55% revenue in 2025 as manufacturers rolled out kaizen-driven plant upgrades, yet technology consulting now posts the fastest 13.25% CAGR, capturing projects around generative-AI, zero-trust security, and cloud-native modernization. The Japan management consulting services market size for technology projects reached an estimated USD 2.30 billion in 2026 and is projected to exceed USD 4.28 billion by 2031. Consulting propositions combine large-language-model fine-tuning, data-fabric architecture, and ethical-AI guardrails to satisfy regulators and boards in tandem.

Strategy, HR, and other service lines continue to secure high-margin advisory roles but increasingly integrate analytics accelerators into core offerings. HR engagements, for instance, embed AI-driven skills taxonomies that feed into reskilling pathways for displaced employees, strengthening cross-practice synergies inside firms.

By Delivery Model: Remote Adoption Transforms Engagement

On-site engagements collected 64.62% of 2025 billings, rooted in Japan’s face-to-face business etiquette. Yet virtual delivery is compounding at 14.22% CAGR, supported by softened data-location rules and widespread deployment of secure video and digital-whiteboard suites. The Japan management consulting services market size captured through remote channels is forecast to double between 2026 and 2031 as multinationals pressure suppliers to cut travel emissions and CFOs shift toward outcome-aligned fee constructs. Hybrid models dominate RFP language, stipulating key-milestone workshops in person while allowing analysis streams to run offshore or near-shore, thus compressing cycle time without eroding rapport.

By End-user Industry: Healthcare Leads Transformation

Financial services generated 27.12% of total billings in 2025 thanks to Basel III finalization, core-bank modernization, and aggressive fintech competition. However, healthcare and life sciences now pace the field with a 13.75% CAGR to 2031, propelled by telemedicine platform scaling, hospital revenue-cycle digitization, and pharmaceutical R&D informatics. Regional hospitals engage consultancies to integrate AI-assisted imaging triage, a critical response to radiologist shortages in aging prefectures. Parallel momentum arises in manufacturing as Industry 4.0 pilots convert into plant-wide rollouts, creating synergies between operational and technology practices.

Geography Analysis

Greater Tokyo, Osaka Kyoto Kobe, and Nagoya continue to anchor project volume, yet rising adoption in regional economic blocs is reshaping the spatial distribution of the Japan management consulting services market. Metropolitan dominance still mirrors corporate head-office clustering, but government subsidies obligate plant-level compliance audits nationwide, redirecting consulting hours to Hokkaido dairy processors, Kyushu semiconductor fabs, and Tohoku renewable energy consortiums. Hybrid-delivery economics reduce travel friction, allowing Tokyo-based teams to serve Shikoku clientele without full-time deployment.

Regional governments under the Digital Garden City initiative award multi-year contracts for cloud migration of resident services, identity management, and subsidy-application portals. Such decentralized spending growth positions mid-tier consultancies and IT-services affiliates to capture work under local bidding thresholds. Moreover, prefectures specializing in energy-transition clusters draw GX advisory demand for feasibility studies and partner-ecosystem orchestration.

International expansion consulting emerges as a niche, with firms guiding mid-caps into Southeast Asia and Latin America trade zones amid yen devaluation. Tokyo-based QUNIE, for instance, launched a Latin America desk in 2025, reflecting how geographic diversification remains both a service line and a client imperative.

Competitive Landscape

Competition features a three-tier hierarchy. First, the Big Four and MBB maintain boardroom access and integrated global delivery centers. Deloitte Tohmatsu alone posted JPY 362.7 billion revenue in FY 2024, underpinned by 21,000 professionals across 30 cities. Second, Japanese pure plays such as Re-grit Partners and SIGMAXYZ differentiate through cultural fluency, flat hierarchies, and execution bias; Re-grit topped Financial Times high-growth rankings for three consecutive years. Third, platform-based freelance collectives aggregate thousands of independents, offering clients elastic capacity at 30 to 50% cost savings.

All tiers invest heavily in proprietary AI assets. Accenture’s 2025 purchase of digital studio Yumemi adds 400 designers and a 60-million-user platform, augmenting Accenture Song’s data-driven design bench. Itochu and Boston Consulting Group’s joint venture exemplifies cross-industry alliances that blend trading house balance sheets with strategy depth to attack AI solution white spaces. Competitive intensity is further amplified by Japanese conglomerates building in-house transformation arms to lock in knowledge and curtail consulting spend, pressuring external providers to prove measurable ROI.

Japan Management Consulting Services Industry Leaders

Accenture Japan Ltd.

Deloitte Tohmatsu Consulting LLC

McKinsey and Company Japan

PwC Consulting LLC (Japan)

Nomura Research Institute, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tohoku Electric Power and MBK Digital agreed to co-develop AI-driven analytics that improve energy-retail operations and offer DX services to local governments.

- July 2025: QUNIE introduced Latin America market-entry consulting backed by NTT DATA offices in seven countries.

- June 2025: TOKU Japan rolled out post-merger integration offerings led by ex-CxOs to raise M&A success rates.

- June 2025: Industry One partnered with Mitsubishi HC Capital to merge finance capacity with DX consulting know how.

Japan Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries |

Key Questions Answered in the Report

How big is the Japan management consulting services market in 2026?

It is valued at USD 7.57 billion in 2026, with a forecast 10.78% CAGR through 2031.

Which segment is growing fastest within consulting services?

Technology consulting shows the strongest pace at a 13.25% CAGR, propelled by generative-AI and cloud modernization.

Why are SMEs increasing their consulting spend?

Compliance obligations under the Economic Security Promotion Act and succession-planning needs are driving SMEs to hire external advisors.

What regions beyond Tokyo are seeing higher consulting demand?

Aichi, Shizuoka, and Tohoku prefectures are attracting projects in smart manufacturing, renewable energy, and public-sector digitalization.

How has hybrid delivery changed consulting engagements?

Hybrid models reduce travel costs, rely on secure collaboration tools, and now capture a growing share of project hours after privacy-law amendments.

Which industries will invest most in consulting by 2031?

Healthcare and life sciences are projected to outpace others, growing at 13.75% CAGR through wider tele-health and pharma-innovation programs.

Page last updated on: