South Korea Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

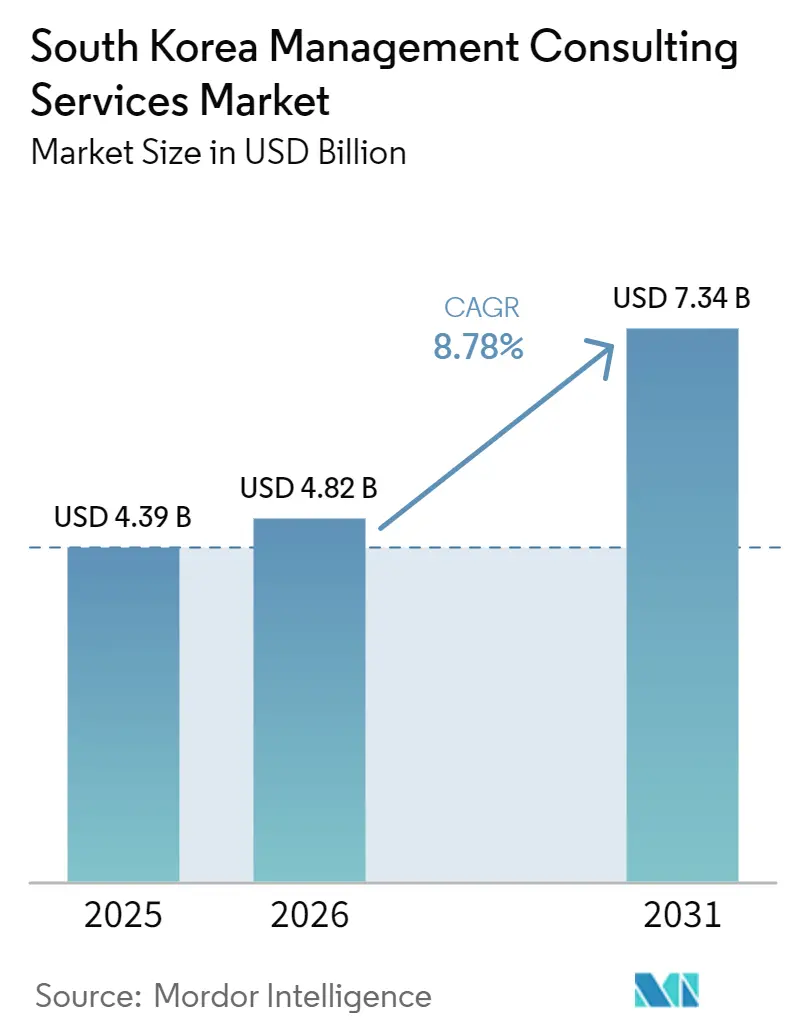

| Base Year Market Size (2025) | USD 4.39 Billion |

| Market Size (2026) | USD 4.82 Billion |

| Market Size (2031) | USD 7.34 Billion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

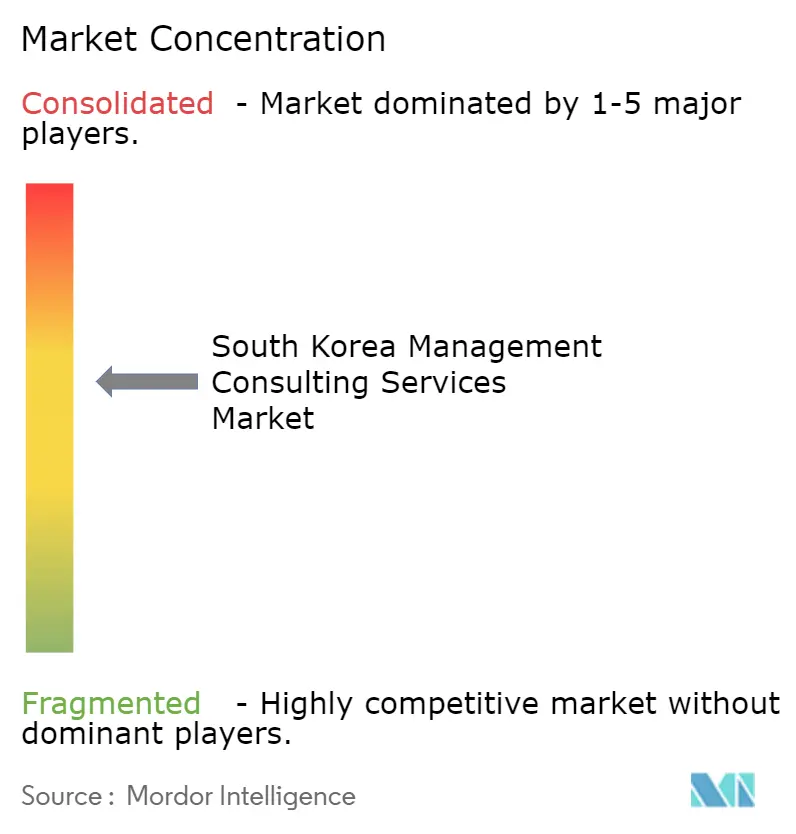

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Management Consulting Services Market Analysis by Mordor Intelligence

The South Korea management consulting services market size was valued at USD 4.39 billion in 2025 and estimated to grow from USD 4.82 billion in 2026 to reach USD 7.34 billion by 2031, at a CAGR of 8.78% during the forecast period (2026-2031). Structural drivers include chaebol-led digital-transformation megaprojects, KRW 5.4 trillion (USD 3.98 billion) of government subsidies for SME digitalization, and mandatory ESG disclosure rules that take effect in 2028. A concurrent AI productivity race in manufacturing and finance reinforces long-cycle advisory demand, while semiconductor-sovereignty and reshoring agendas elevate supply-chain strategy work. Heightened investment pledges from Samsung, Hyundai Motor Group, LG, and SK translate into sustained pipelines in strategy, operational redesign, and compliance architecture.

Key Report Takeaways

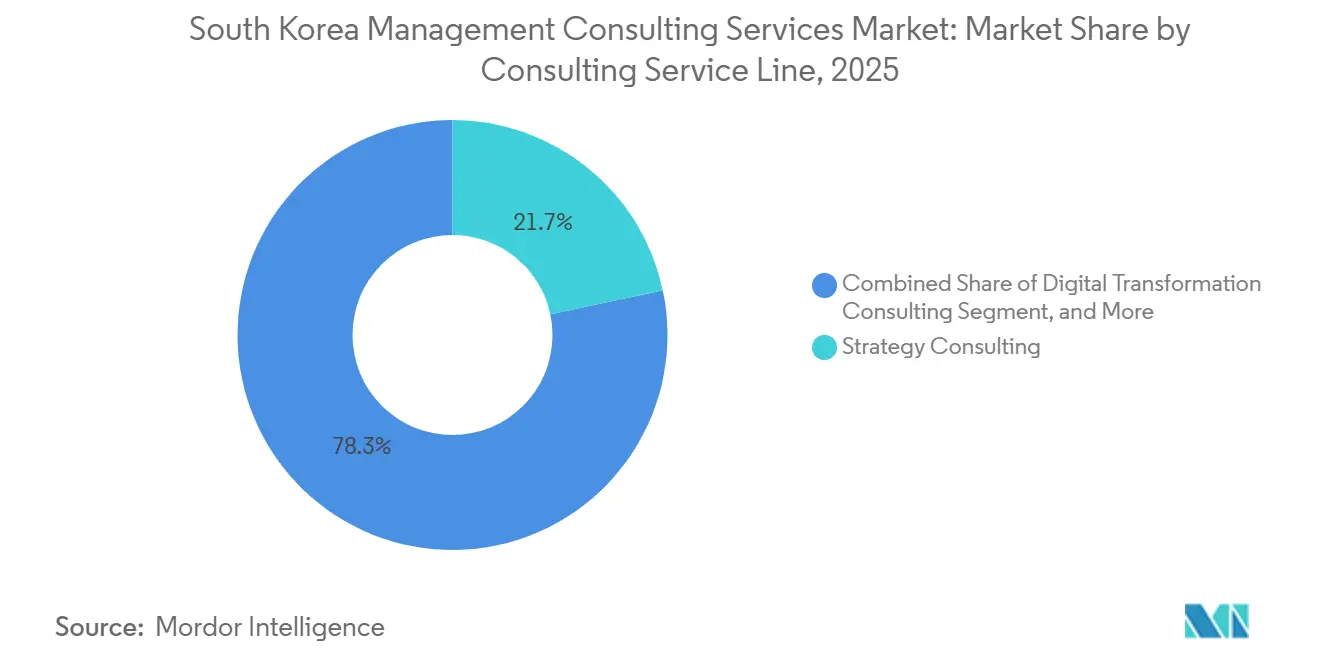

- By consulting service line, strategy consulting led with 21.68% of the South Korea management consulting services market share in 2025, whereas risk and compliance consulting is advancing at a 9.23% CAGR to 2031.

- By organization size, large enterprises held 62.84% of the South Korea management consulting services market size in 2025, while the SME segment is expanding at a 9.04% CAGR through 2031.

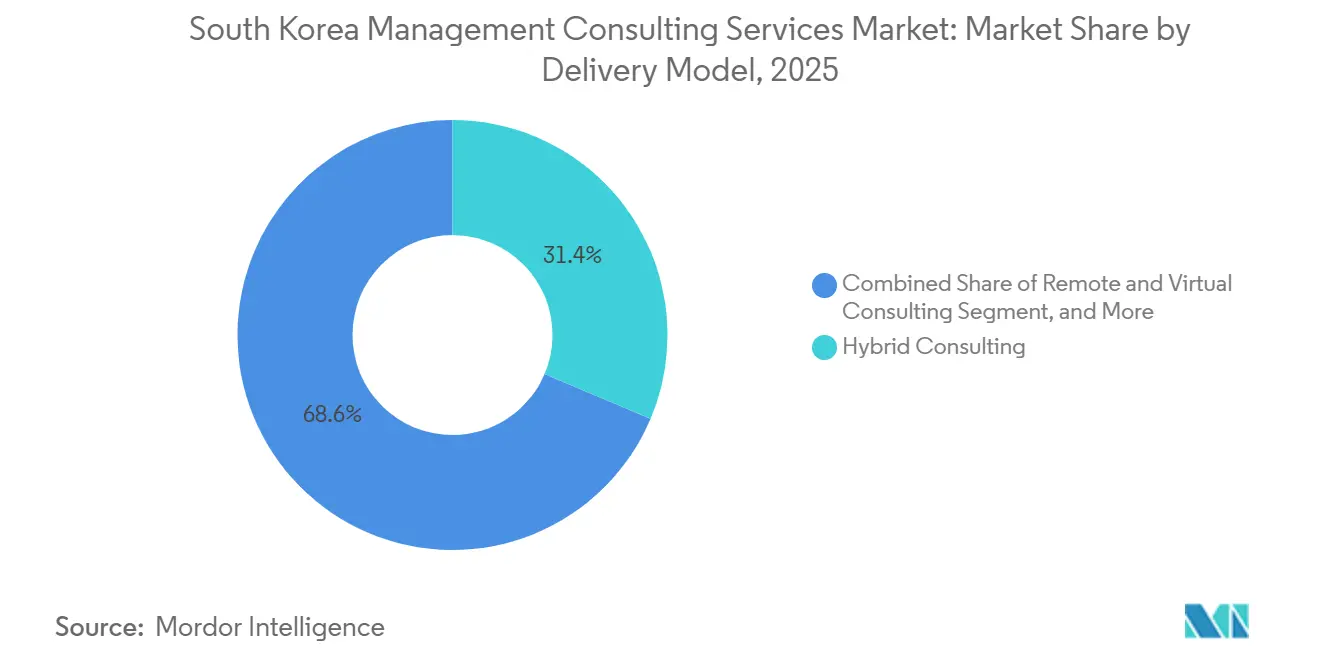

- By delivery model, hybrid consulting commanded 31.36% share of the South Korea management consulting services market in 2025, whereas remote consulting is projected to rise at an 8.96% CAGR between 2026-2031.

- By end-user industry, manufacturing contributed 20.41% revenue in 2025, and IT and telecommunications is forecast to register a 9.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Digital-Transformation Programs Across Chaebol Conglomerates | +2.1% | National, concentrated in Seoul metropolitan area and industrial hubs | Medium term (2-4 years) |

| Government Subsidies for SME Digitalization and Export Readiness | +1.8% | National, higher uptake in Gyeonggi, Busan, Daegu, Incheon | Short term (≤ 2 years) |

| Mandatory ESG and Carbon-Neutrality Disclosures Boosting Advisory Spend | +1.5% | National, all listed companies and large unlisted entities | Medium term (2-4 years) |

| AI-Driven Productivity Race in Manufacturing and Finance | +1.9% | National, manufacturing in Gyeongsang provinces, finance in Seoul | Short term (≤ 2 years) |

| Reshoring and Supply-Chain Diversification Imperatives | +1.2% | National, cross-border export sectors | Long term (≥ 4 years) |

| Semiconductor Value-Chain Sovereignty Investments | +1.0% | Gyeonggi and Chungcheong clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Digital-Transformation Programs Across Chaebol Conglomerates

The five largest chaebol groups have earmarked KRW 803 trillion (USD 591.6 billion) for investments through 2030, with sizable allocations for AI infrastructure, semiconductor capacity, and software-defined vehicles. These commitments translate into multi-year consulting engagements covering enterprise-architecture redesign, data-platform consolidation, and workforce reskilling. Samsung Electronics alone is spending KRW 300 trillion (USD 221.1 billion) on semiconductor capacity and AI-driven automation, necessitating embedded consultants on 12- to 24-month transformation sprints. The consortium approach of the M.AX Alliance further increases the coordination complexity that external advisors must manage.[1]Seoul Economic Daily, “Korean Banks Accelerate Digital Transformation with AI-Powered Loan Systems,” en.sedaily.com

Government Subsidies for SME Digitalization and Export Readiness

The Ministry of SMEs and Startups disbursed KRW 5.4 trillion (USD 3.98 billion) in 2025 to underwrite cloud-migration, AI pilot projects, and export-readiness consulting. Programs such as the Cloud Voucher and AI Voucher schemes subsidize up to 70% of eligible costs, expanding the South Korea management consulting services market beyond its traditional large-enterprise base. Consultancies are incorporating performance-based pricing tied to export revenue gains and productivity outcomes, aligning incentives with policy objectives and lowering adoption barriers.

Mandatory ESG and Carbon-Neutrality Disclosures Boosting Advisory Spend

The Korean Sustainability Standards Board’s rules, aligned with IFRS S1 and S2, trigger mandatory reporting on Scope 1 and 2 emissions in 2028 and Scope 3 after a grace period. Companies require governance structures, data-collection systems, and third-party assurance, all of which elevate demand for strategy, operational, and compliance consulting. Heavy-industry early movers are modeling carbon-pricing scenarios and evaluating carbon-capture solutions, creating high-value, multi-year pipelines for the South Korea management consulting services market.[2]Boston Consulting Group, “Jobs in Korea | Careers,” careers.bcg.com

AI-Driven Productivity Race in Manufacturing and Finance

The AX-Sprint program, funded at KRW 754 billion (USD 555.6 million), underwrites AI deployments across public and private sectors. Woori Bank’s plan to automate corporate-loan extensions exemplifies financial-services use cases, while the KAIROS smart-factory platform drives predictive maintenance and real-time quality control for manufacturers. Consulting engagements blend technical implementation with change management as firms confront legacy-system constraints and workforce resistance.[3]Seoul Economic Daily, “Korean Banks Accelerate Digital Transformation with AI-Powered Loan Systems,” en.sedaily.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Crunch for Bilingual Senior Consultants and Data Scientists | -0.9% | Seoul and Gyeonggi, spillovers in Busan and Daegu | Short term (≤ 2 years) |

| Fee Pressure From In-House Strategy Teams and SaaS Advisory Platforms | -0.6% | National, large enterprises and government agencies | Medium term (2-4 years) |

| Lengthy Procurement Cycles in Mid-Sized Domestic Firms | -0.4% | National, traditional manufacturing and regional firms | Medium term (2-4 years) |

| Conflict-of-Interest Regulations on Audit-Linked Advisory | -0.3% | National, Big Four consulting arms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Talent Crunch for Bilingual Senior Consultants and Data Scientists

The South Korea management consulting services market faces shortages of up to 52,000 qualified professionals in 2026. Job-to-applicant ratios above 8:1 for senior AI roles inflate salaries by 20-35%, squeezing consulting margins. Brain drain toward Singapore and the United States compounds scarcity, prompting firms to forge university partnerships, introduce accelerated promotion tracks, and shift routine analytics to offshore centers, yet bilingual, industry-savvy talent remains a binding constraint.

Fee Pressure From In-House Strategy Teams and SaaS Advisory Platforms

Chaebol groups such as Samsung have scaled internal advisory units, while subscription-based SaaS platforms commoditize benchmarking and analytics. The Financial Services Commission’s independence rules restrict audit-linked advisory, further limiting revenue pools. Consultancies respond by embedding proprietary analytics, emphasizing outcome-based pricing, and focusing on high-complexity mandates where internal teams lack capacity.[4]Management Consulted, “Samsung Global Strategy Group Firm Profile,” managementconsulted.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Risk and Compliance Consulting Gains Momentum

Risk and compliance consulting is expanding faster than any other service line at a 9.23% CAGR through 2031. Spending accelerates as the Financial Supervisory Service enforces virtual-asset regulations, stablecoin frameworks, and enhanced anti-money-laundering protocols. Korea Post Finance’s KRW 21.6 billion (USD 15.9 million) AI-driven fraud-detection program underscores rising investment. Strategy consulting, while still the largest at 21.68% of the South Korea management consulting services market share in 2025, now often integrates digital, ESG, and regulatory modules.

Operations, HR, and financial-advisory practices remain integral to smart-factory deployments, talent-reskilling, and cross-border M&A. Sustainability advisory overlaps heavily with compliance mandates, driving bundled engagements. As regulatory complexity rises, firms that combine deep domain expertise with advanced analytics capture larger slices of the South Korea management consulting services market size.

By Organization Size: SME Demand Accelerates Under Subsidy Tailwinds

Large enterprises delivered 62.84% of 2025 revenue, reflecting ongoing mega-programs that require multidisciplinary teams and global delivery networks. Engagements often exceed USD 5 million and span 12-24 months, reinforcing the dominance of global majors in high-stakes work.

SMEs, however, constitute the fastest-growing client base, expanding at a 9.04% CAGR. Voucher programs covering up to 70% of project costs stimulate cloud-migration planning, AI pilots, and export-readiness consulting. Domestic boutiques leverage cultural proximity and flexible pricing, while international firms experiment with productized offerings to profitably serve smaller clients within the South Korea management consulting services industry.

By Delivery Model: Hybrid Consulting Retains Primacy

Hybrid delivery, which mixes on-site workshops with remote analytics, held 31.36% share in 2025. Clients value the intimacy of face-to-face sessions for stakeholder alignment and the cost efficiency of virtual collaboration for iterative analysis.

Remote-only delivery, advancing at an 8.96% CAGR, gains acceptance in workflow normalization and public-sector budget constraints. Investment in digital workspaces, AI-assisted dashboards, and virtual-reality breakout rooms helps maintain engagement quality, yet complex engagements still favor hybrid approaches within the South Korea management consulting services market.

By End-User Industry: IT and Telecommunications to Outpace Manufacturing

Manufacturing accounted for 20.41% of 2025 spending, fueled by smart-factory rollouts co-funded by the government. Projects focus on predictive maintenance, carbon-neutrality roadmaps, and supply-chain resilience.

IT and telecommunications is projected to grow fastest at 9.47% CAGR, spurred by 6G network planning and sovereign-cloud initiatives. Banking, insurance, and healthcare also accelerate AI adoption, broadening the South Korea management consulting services market size through 2031.

Geography Analysis

Seoul and Gyeonggi anchor the South Korea management consulting services market, hosting the headquarters of chaebol conglomerates, financial institutions, and government ministries. Their dense innovation ecosystems translate into robust demand for strategy, digital transformation, and regulatory advisory.

Industrial belts in Ulsan, Pohang, and Gumi generate significant operations-consulting and sustainability work, as manufacturers pursue Industry 4.0 upgrades and carbon-neutrality. Busan’s port logistics landscape drives supply-chain optimization projects, while Incheon’s free-economic zones attract market-entry and FDI advisory.

Regional governments increasingly commission economic-development strategies, illustrated by EY Consulting’s March 2026 MOU with Gyeongsangbuk-do. Although balanced-development policies will disperse spending, Seoul and Gyeonggi are expected to maintain leadership within the South Korea management consulting services market.

Competitive Landscape

The market remains moderately fragmented. Global majors, McKinsey, Boston Consulting Group, Bain, Deloitte, Accenture, KPMG, PwC, and EY, compete with domestic leaders such as Korea Management Association Consulting, Human Consulting Group, and Samsung SDS Consulting. Big Four consulting arms collectively generated KRW 3.88 trillion (USD 2.86 billion) in 2025 revenue, underscoring demand for integrated services.

Strategic moves center on talent expansion and digital capability building. BCG Korea’s 30-partner roster, the largest among foreign firms, signals deeper local commitment. Samsung SDS launched a Virtual Asset IT Consulting Team and became a ChatGPT Enterprise reseller, leveraging blockchain and generative-AI growth niches.

Emerging disruptors include SaaS advisory platforms that provide subscription access to benchmarking tools, pressuring fees for routine analysis. Firms differentiate through proprietary analytics, sector specialization, and outcome-based pricing to defend margins in the South Korea management consulting services industry.

South Korea Management Consulting Services Industry Leaders

Deloitte Consulting

Accenture Plc

Bain & Company Inc.

Boston Consulting Group, Inc. (BCG)

McKinsey & Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Ministry of Health and Welfare launched the Medical AX program, allocating KRW 9 billion (USD 6.6 million) to chronic-disease AI pilots.

- March 2026: Korea Post Finance unveiled a KRW 21.6 billion (USD 15.9 million) AI road-map for underwriting, claims, and fraud detection.

- March 2026: EY Consulting signed an MOU with Gyeongsangbuk-do to support regional economic development.

- March 2026: Samsung SDS created a Virtual Asset IT Consulting Team addressing blockchain infrastructure and compliance.

- March 2026: Woori Bank announced an AI-based automated corporate-loan-extension system slated for year-end deployment.

South Korea Management Consulting Services Market Report Scope

The South Korea Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current South Korea management consulting services market size and its projected growth?

The market is valued at USD 4.82 billion in 2026 and is forecast to reach USD 7.34 billion by 2031, growing at an 8.78% CAGR.

Which consulting service line is growing the fastest?

Risk and compliance consulting is advancing at a 9.23% CAGR due to expanding virtual-asset and ESG regulations.

How are SMEs influencing demand for consulting in South Korea?

Government vouchers covering up to 70% of project costs are helping SMEs adopt cloud and AI solutions, making them the fastest-growing client segment.

What delivery model do clients prefer in 2026?

Hybrid consulting, which blends on-site interaction with remote analytics, holds the largest share, while remote-only delivery is expanding quickly.

Which industry will generate the highest consulting growth through 2031?

IT and telecommunications leads with a 9.47% CAGR, driven by 6G deployment plans and sovereign-cloud buildouts.

What is the main talent challenge facing consulting firms?

A shortage of bilingual senior consultants and data scientists, with job-to-applicant ratios above 8:1, is tightening labor supply and pushing up compensation.

Page last updated on: