China LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

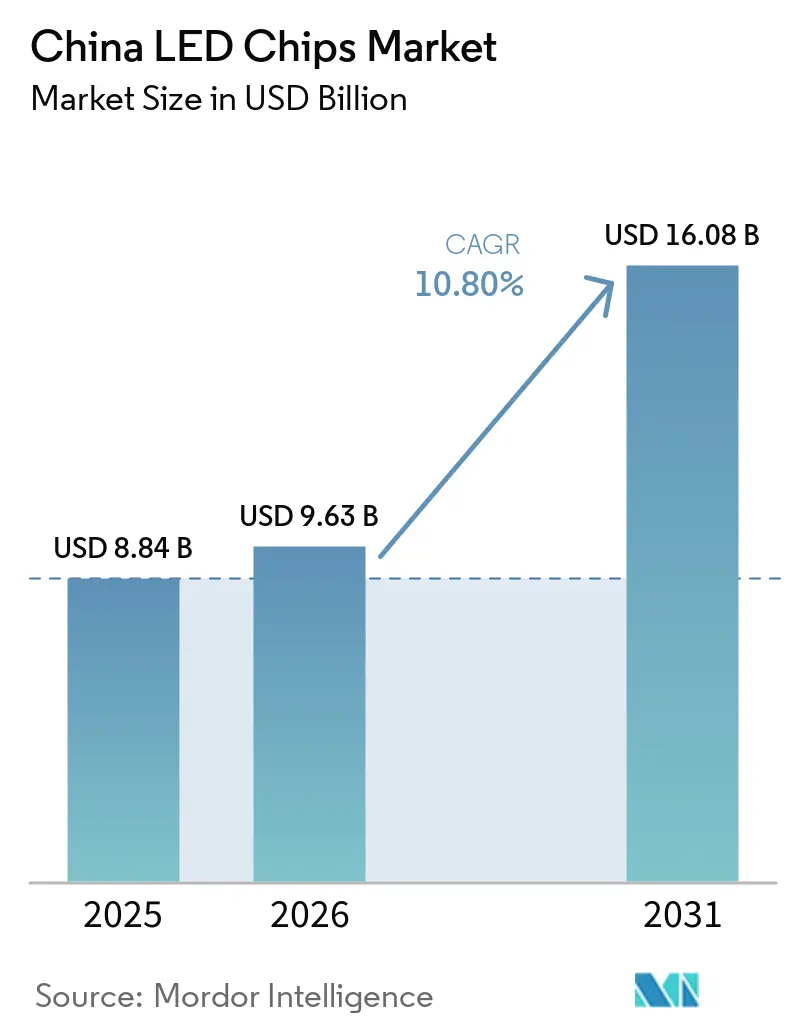

| Base Year Market Size (2025) | USD 8.84 Billion |

| Market Size (2026) | USD 9.63 Billion |

| Market Size (2031) | USD 16.08 Billion |

| Growth Rate (2026 - 2031) | 10.80% CAGR |

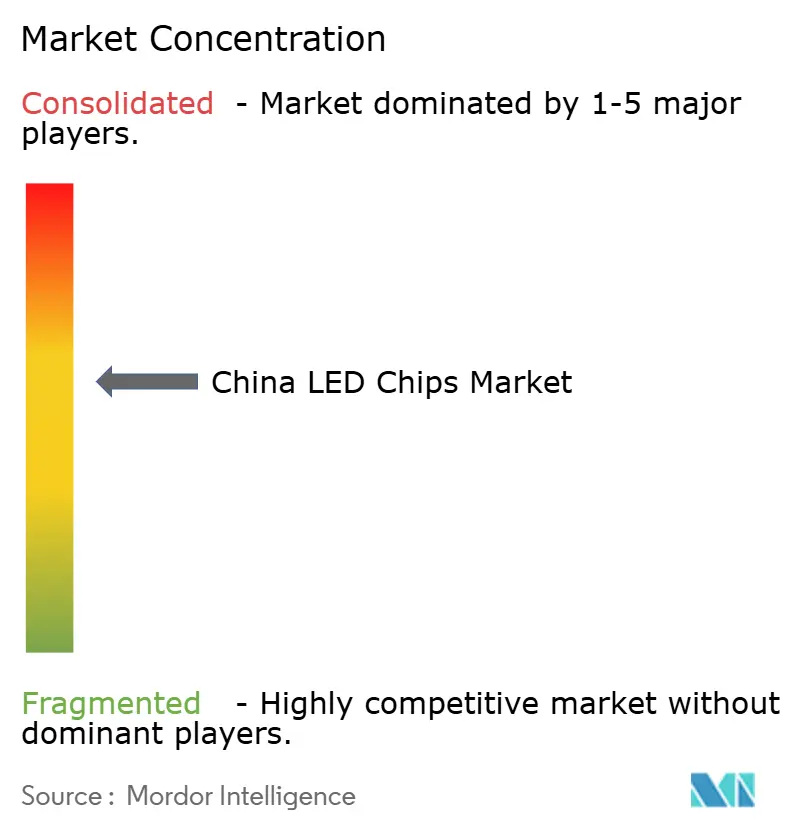

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China LED Chips Market Analysis by Mordor Intelligence

The China LED chips market size is projected to be USD 8.84 billion in 2025, USD 9.63 billion in 2026, and reach USD 16.08 billion by 2031, growing at a CAGR of 10.8% from 2026 to 2031. Policy-driven capacity expansion, rising mini-LED penetration in premium televisions, and the electrification of China’s vehicle fleet together underpin this robust trajectory. Domestic epitaxial producers now control more than 70% of installed capacity, yet foreign patent holders still command premium pricing in high-brightness and color-critical die, preserving a dual-track profit pool that rewards scale in conventional chips and innovation in micro-LED. Conventional LEDs, while facing margin pressure from an 8-12% price slide over 2024-2025, continue to anchor general lighting and legacy displays. Simultaneously, micro-LED prototypes for wearables and automotive head-up displays signal the next growth wave, even as mass-transfer economics lag. Substrate price swings and tighter subsidy milestones add operational risk for mid-tier players but also accelerate industry consolidation toward vertically integrated leaders.

Key Report Takeaways

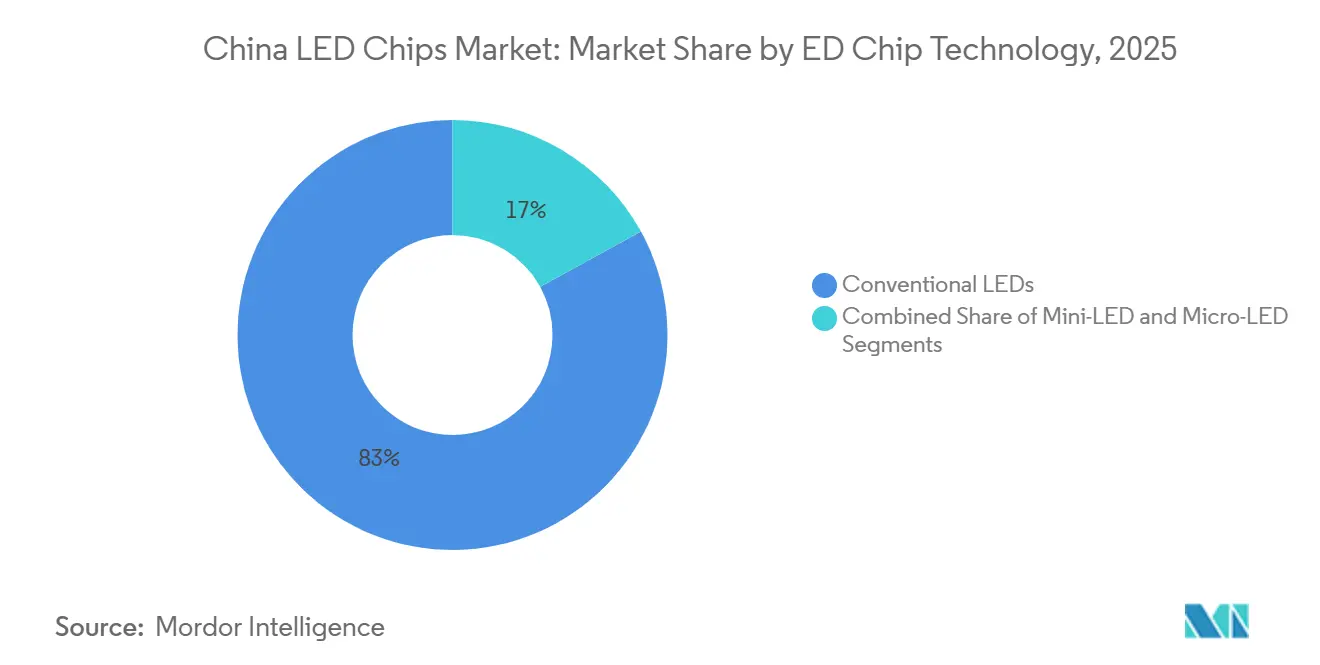

- By LED chip technology, conventional LEDs accounted for 83% of revenue share in 2025, while micro-LED is projected to advance at a 15.64% CAGR through 2031.

- By semiconductor material, GaN/InGaN held 82.2% of the China LED chips market share in 2025, whereas AlGaInP and other compounds are forecast to grow at a 16.23% CAGR to 2031.

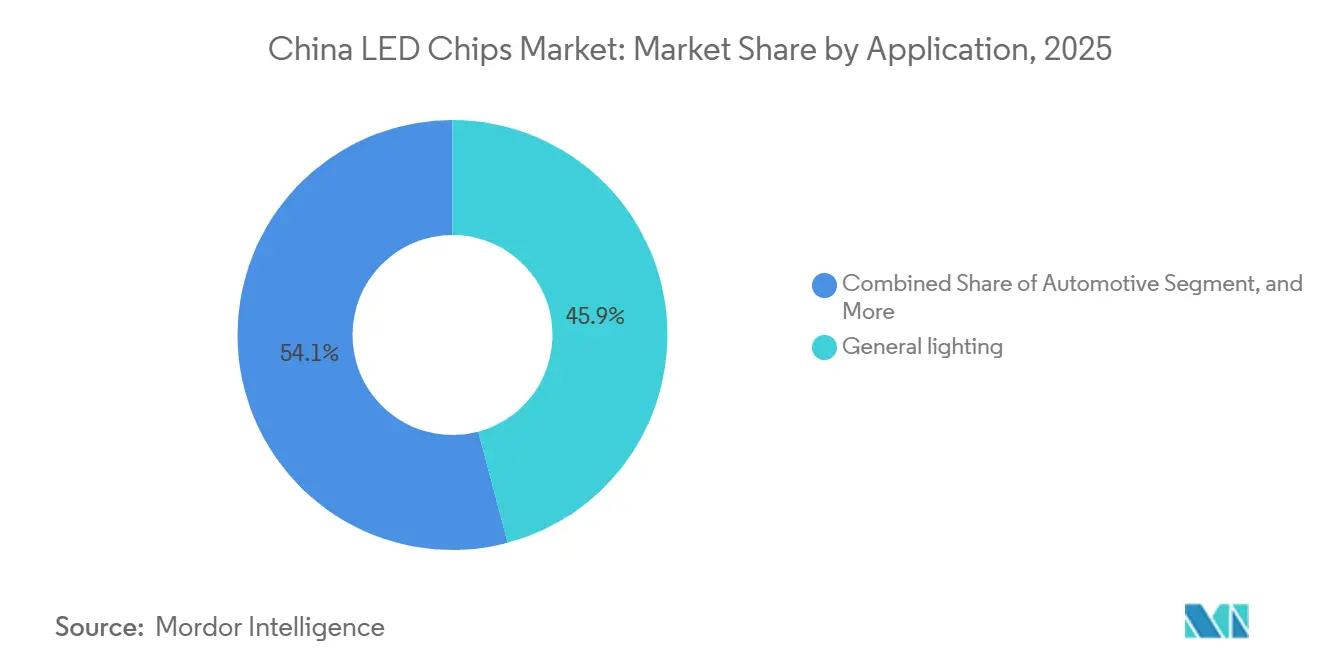

- By application, general lighting accounted for 45.87% of the 2025 value, and automotive chips are expanding at a 16.2% CAGR through 2031, driven by adaptive headlamp adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Demand for Mini-LED Backlighting in High-End TVs | +2.8% | Guangdong and Jiangsu manufacturing hubs | Medium term (2-4 years) |

| Government Subsidies for Domestic Semiconductor Manufacturing | +2.5% | Yangtze River and Pearl River Delta clusters | Short term (≤ 2 years) |

| Transition Toward High-Efficacy GaN-on-Si Epitaxy | +1.9% | Xiamen and Wuhu production bases | Long term (≥ 4 years) |

| Rapid Expansion of New-Energy Vehicle Headlamp Adoption | +2.3% | Shanghai, Shenzhen, Hefei automotive corridors | Medium term (2-4 years) |

| Localization Push Across Consumer Electronics Supply Chains | +1.2% | Chongqing and Chengdu electronics zones | Short term (≤ 2 years) |

| Integration of Micro-LED in Next-Gen Wearables | +0.9% | Beijing and Shenzhen R&D clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Domestic Semiconductor Manufacturing

Phase III of the National IC Fund earmarked USD 47 billion in 2024, with 18% directed to compound semiconductors, lowering MOCVD reactor costs by up to 50% for qualified LED fabs.[3]National IC Fund, “Phase III Allocation 2024,” ICFUND.GOV.CNProvincial co-funding adds a further USD 8.5 billion, translating into rapid capacity gains and safeguarding near-term capital access. Subsidy recipients, however, must hit 90% domestic equipment usage and 15% annual productivity metrics by 2027, requirements that favor entrenched scale players. Sanan reported government grants equal to 22% of 2024 net income, underscoring continuing dependence. While the cash support accelerates volume, the performance thresholds strengthen the competitive moat around leaders and cull weaker entrants, shaping the medium-term structure of the China LED chips market.

Transition Toward High-Efficacy GaN-on-Si Epitaxy

Sanan and HC SemiTek expanded their combined GaN-on-Si fleet from 31 to 47 reactors between Q1 2025 and Q1 2026, attracted by 30-40% lower substrate cost and the die density gains inherent to 8-inch wafers.[4]Applied Physics Letters, “High-Yield GaN-on-Si Epitaxy,” APPLIEDPHYSICSLETTERS.AIP.ORGBuffer-layer engineering breakthroughs published in 2025 pushed yields to 91%, closing much of the gap with sapphire platforms. Although high-brightness segments still prefer sapphire for thermal reasons, GaN-on-Si enables low-cost lamps and mid-power backlighting, broadening addressable demand. Producers that master wafer bow management and thermal mismatch will unlock margin relief while extending the lifespan of conventional lines, thereby sustaining the growth momentum of the China LED chips market.

Rapid Expansion of New-Energy Vehicle Headlamp Adoption

China built 9.4 million new-energy vehicles in 2025, and 28% of models priced above CNY 200,000 adopted matrix LED or adaptive driving beam systems. Each ADB headlamp integrates up to 120 addressable chips, creating a ten-fold rise in per-vehicle consumption versus halogen. C-NCAP’s bonus points for ADB accelerated OEM launch schedules, while domestic Tier 1s source 70% of dies from local vendors, cutting lead times by one-fifth. Foreign chipmakers still outperform on color consistency, but cross-licensing deals, such as OSRAM’s 2024 phosphor grant to Sanan, are narrowing the quality gap.[5]China Semiconductor Lighting Industry Alliance, “Q4 2025 Report,” CSLIA.ORG.CN The vehicle electrification wave, therefore, channels sustained, high-margin demand into the China LED chips market through 2031.

Rising Demand for Mini-LED Backlighting in High-End TVs

Mini-LED televisions shipped by Chinese panel makers climbed to 4.2 million units in 2025, up 68% from the prior year, owing to BOE and CSOT scaling capacity that now exceeds 55% of global supply. [1]BOE Technology Group, “2025 Investor Presentation,” BOE.COM Each 65-inch set integrates up to 25,000 chips, boosting die demand per unit by 50-100× compared with edge-lit LCDs. Yield improvement toward 90% narrows cost gaps with OLED, while the 2024 national standard GB/T 42937 increased OEM confidence by codifying luminance uniformity targets. [2]China Electronics Standardization Institute, “GB/T 42937-2024,” CESI.CN Chip vendors that can supply tight-bin lots win design-ins, and vertically integrated producers offset lower margins in legacy lighting by capturing this surge in volume. As local dimming zone counts climb beyond 2,000 per panel, incremental chip content directly lifts the China LED chips market.

Restraint Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Overcapacity in Conventional LED Chip Lines | −1.8% | Jiangxi and Hubei provinces | Short term (≤ 2 years) |

| High Capital Expenditure for Micro-LED Mass Transfer | −1.3% | Guangdong and Fujian R&D centers | Long term (≥ 4 years) |

| Patent Litigation Risks with Foreign IP Holders | −0.7% | Cross-border, EU and US markets | Medium term (2-4 years) |

| Volatility in Sapphire and Silicon Carbide Substrate Prices | −0.9% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Micro-LED Mass Transfer

State-of-the-art laser or electrostatic transfer tools cost USD 12-18 million each yet deliver only 20-40% of the throughput that consumer economics require, pushing a single micro-LED line’s capex above USD 50 million. Until tool speeds double and defect rates halve, mass-market wearables and TVs remain out of reach. For most domestic chipmakers, negative early-stage returns deter aggressive scaling, tempering the near-term uplift to the China LED chips market.

Overcapacity in Conventional LED Chip Lines

China operated about 3,200 MOCVD reactors in 2025, yet average utilization slipped to 70%, well below the 85% breakeven threshold, depressing average selling prices 10% over two years. Provincial incentives favored new fabs without coordinating downstream demand, creating 420 million wafer-equivalent units of surplus. Smaller producers that relied on 60% equipment subsidies now face cash strain; fourteen filed for restructuring by end-2025. Consolidation is expected to cut the participant base from more than 200 to fewer than 80 by 2028, reshaping competitiveness in the China LED chips market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Conventional Dominance Funds Micro-LED Bets

Conventional LEDs generated 83% of 2025 revenue, anchoring the China LED chips market size despite 8-12% price compression. Mature 4-inch and 6-inch lines still deliver positive cash flow, subsidizing R&D into mini-LED and micro-LED. Mini-LED backlighting shipments reached 4.2 million TV units, translating into a significant uplift in die volumes. Should OLED panels fall below USD 300 for a 65-inch size by 2027, mini-LED could retrench to outdoor signage and professional monitors. Yet today’s local dimming requirements and brightness advantages keep mini-LED on an expansion path that supports total unit growth in the China LED chips market.

Micro-LED, though contributing less than 2% of 2025 sales, is projected to grow at about 15.64% CAGR through 2031, the fastest among chip types. Wearable displays and automotive head-up units require the high brightness and extended lifetime that inorganic emitters provide. A 2025 Nature Photonics study validated efficiencies above 250 lm/W at sub-10 µm pitches, proving the physics while highlighting manufacturing hurdles. As mass-transfer improves, micro-LED could eventually shift revenue mix, but for the next three years, conventional LEDs will continue to bankroll technological migration across the China LED chips market.

By Semiconductor Material: GaN Incumbency Versus AlGaInP Specialization

GaN/InGaN platforms captured 82.2% of 2025 revenue; cost leadership and wide bandgap attributes explain the material’s ubiquity in blue and white devices. GaN-on-Si further lowers cost, reinforcing this grip on the China LED chips market share. AlGaInP and emerging gallium oxide variants, though starting from a small base, are set to grow 16.23% annually through 2031, propelled by red-rich automotive ambient lighting and horticulture installations.

Domestic capacity for red chips remains tight; automakers still import around 40% of AlGaInP dies. Xiamen Changelight’s addition of 24 reactors in late 2025 aims to carve out 25% domestic share by 2027. As phosphor-converted GaN bridges cost and efficiency gaps in yellow spectra, material selection grows more application-specific, amplifying the sophistication of procurement decisions across the China LED chips market.

By Application: Automotive Ascendancy Reshapes Demand Mix

General lighting comprised 45.87% of 2025 demand, buoyed by retrofit programs in municipal infrastructure. However, new-energy vehicles will raise automotive’s portion from 12% in 2025 to roughly 20% by 2031 on 16.2%CAGR volume growth, lifting the China LED chips market size linked to AEC-Q102-qualified supply. Each electric vehicle now embeds 150-250 chips across exterior and interior systems, double the count in combustion models.

Backlighting and displays formed roughly 28% of demand in 2025. Mini-LED captures premium televisions and gaming monitors, offsetting OLED erosion in phones. Industrial and specialty lighting applications, including UV-C sterilization and horticulture, represent a smaller but fast-growing slice, recording 12% CAGR as vertical farms and air-purification systems scale. The accelerating automotive pull, combined with specialty niches, diversifies end-use exposure and enhances resilience within the China LED chips market.

Geography Analysis

Installations cluster along the Yangtze and Pearl River Deltas, where 68% of MOCVD tools reside and where the China LED chips market size benefits from established supply chains. Guangdong hosts the largest concentration of mini-LED backlight assembly lines, ensuring short logistics loops between die fabs and panel makers. Anhui’s Wuhu city, historically an automotive hub, now hosts Sanan’s new GaN-on-Si complex, slated to reach 15 million wafers annually by 2027, positioning the province as an emerging capacity node.

Inland migration of electronics manufacturing to Chongqing and Chengdu stimulates local demand for die for smart devices, reducing dependence on coastal suppliers. Provincial incentives, however, have also created pockets of overcapacity in Jiangxi and Hubei, where utilization lags, and restructurings mount. Policy now ties subsidies to efficiency targets, steering incremental investment toward provinces that couple demand proximity with ecosystem depth.

Cross-border exposure remains limited; exports account for under 15% of output, mainly high-brightness chips shipped to Korea and the EU. Patent disputes temper wider overseas expansion, yet the domestic demand base is sufficiently large that capacity absorption through 2031 depends primarily on internal consumption trends rather than global cycles. Thus, regional policy harmonization and demand clustering will determine production footprints within the China LED chips market.

Competitive Landscape

The top five suppliers held roughly 60% revenue in 2025, indicating moderate concentration and reinforcing an oligopolistic dynamic in critical die categories. Vertical integration from substrate to package lets leaders buffer cost volatility and defend margins. Sanan’s March 2026 Wuhu fab underscores a scale play, targeting 30% automotive share by leveraging 8-inch GaN-on-Si economics. HC SemiTek’s joint venture with AIXTRON seeks process superiority, aiming for 95% wafer uniformity, which would tighten quality control and elevate competitive thresholds.

Foreign incumbents still dominate premium niches. OSRAM and Lumileds supply high-CRI museum lighting and ±50 K color-tolerance automotive whites, forcing Chinese challengers to license key phosphors or co-develop formulations. Consolidation accelerated as Hangzhou Silan acquired Lianchuang in 2025, adding both capacity and automotive-grade lines. Industry alliances forecast the player count falling below 80 by 2028, driven by stricter R&D spending mandates and automotive OEM demands for single-source contracts covering multiyear model cycles.

Strategic thrusts now center on UV-C efficacy improvements and tunable-spectrum horticulture solutions, valued at USD 320-380 million by 2030. Firms that master aluminum nitride growth or gallium oxide die may unlock premium margin pools. Given policy emphasis on domestic tool utilization, equipment localization partnerships, such as HC SemiTek’s AIXTRON project, could redefine cost curves, tilting long-term advantage toward innovators who close process gaps while scaling responsibly within the China LED chips market.

China LED Chips Industry Leaders

Sanan Optoelectronics Co., Ltd.

HC SemiTek Corporation

NationStar Optoelectronics Co., Ltd.

angzhou Silan Microelectronics Co., Ltd.

Xiamen Changelight Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sanan Optoelectronics commissioned a CNY 12 billion GaN-on-Si plant in Wuhu with 120 MOCVD reactors targeting 15 million wafers annually by Q2 2027.

- January 2026: HC SemiTek and AIXTRON launched a USD 85 million JV to co-develop 8-inch micro-LED MOCVD tools, with prototypes due Q4 2026.

- November 2025: Xiamen Changelight secured a USD 220 million credit line to expand AlGaInP red-chip capacity by 40%.

- September 2025: NationStar and BOE began co-developing 85-inch and 98-inch mini-LED backlights with 2,000+ dimming zones targeting 1.2 million panels annually by 2027.

China LED Chips Market Report Scope

The China LED Chip Market Report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, Micro-LED), Semiconductor Material (GaN/InGaN, AlGaInP, Other Semiconductor Materials), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, Industrial/Specialty Lighting). Market Forecasts are Provided in Terms of Value (USD Billion).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| By LED Chip Technology | Conventional LEDs |

| Mini-LED | |

| Micro-LED | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| Other Semiconductor Materials | |

| By Application | General Lighting |

| Automotive | |

| Backlighting / Displays | |

| Consumer Electronics | |

| Industrial / Specialty Lighting |

Key Questions Answered in the Report

What was the China LED chips market size in 2026?

It reached USD 9.63 billion in 2026, on its way to USD 16.08 billion by 2031.

Which application will expand fastest through 2031 in China’s LED chip space?

Automotive lighting, driven by matrix headlamps in new-energy vehicles, is set to grow 16.2% CAGR.

Who are the leading companies in China’s LED chip supply?

Sanan Optoelectronics, HC SemiTek, Xiamen Changelight, NationStar, and Hangzhou Silan together hold about 60% revenue.

Why is GaN-on-Si important to future competitiveness?

It cuts substrate cost by up to 40% and leverages 8-inch fabs, improving die economics for mid-power devices.

Page last updated on: