China Integrated Circuit (IC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

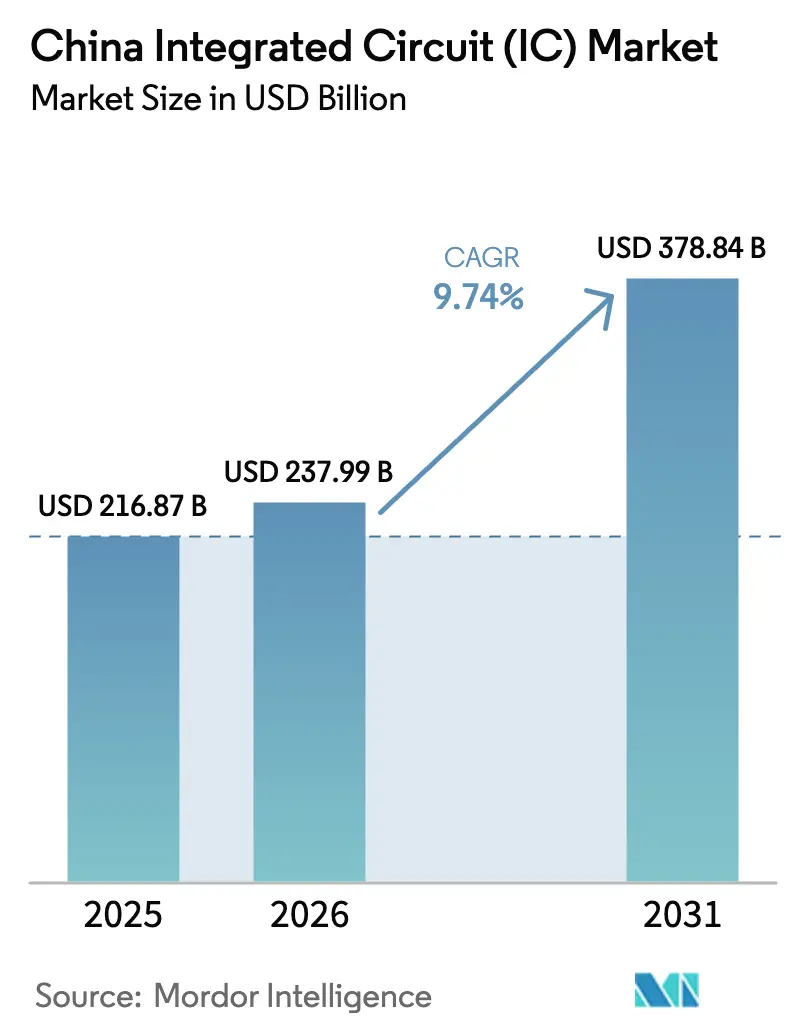

| Base Year Market Size (2025) | USD 216.87 Billion |

| Market Size (2026) | USD 237.99 Billion |

| Market Size (2031) | USD 378.84 Billion |

| Growth Rate (2026 - 2031) | 9.74% CAGR |

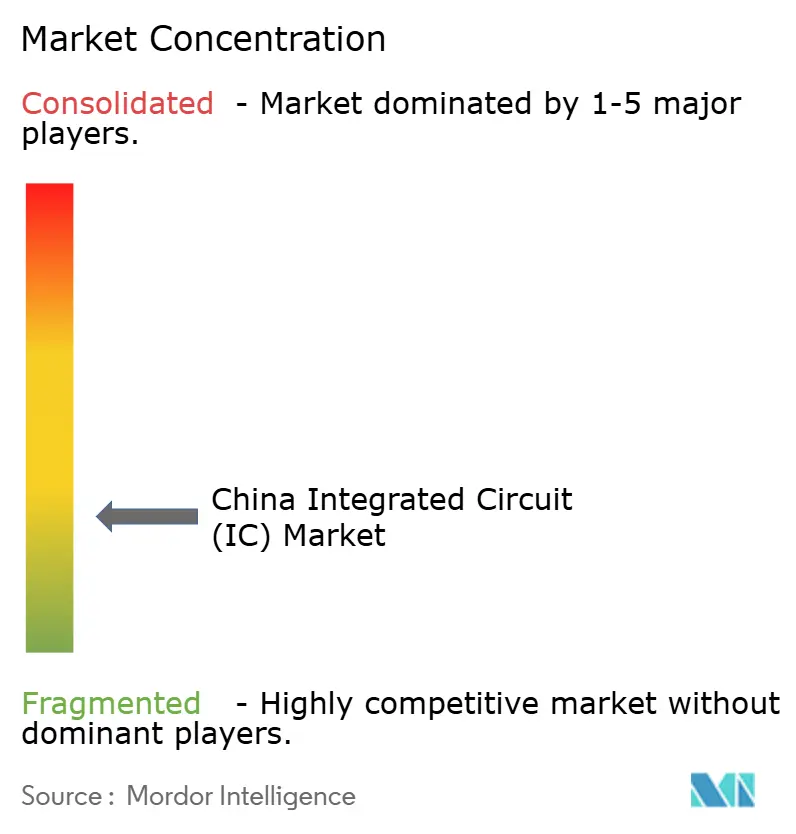

| Market Concentration | Low |

Major Players-Market-ML.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Integrated Circuit (IC) Market Analysis by Mordor Intelligence

The China integrated circuit market size is expected to grow from USD 216.87 billion in 2025 to USD 237.99 billion in 2026 and is forecast to reach USD 378.84 billion by 2031 at 9.74% CAGR over 2026-2031. This momentum stems from the government’s third-phase National Integrated Circuit Industry Investment Fund, a USD 47.5 billion vehicle that accelerates fab construction and advanced memory production. Memory devices retain a commanding foothold, while logic chips for AI and automotive electronics are rising fastest. Stricter export controls have intensified localization, pushing domestic foundries to refine mature-node capacity and explore alternative process techniques. Large-scale EV adoption, hyperscale data-center build-outs, and industrial IoT upgrades round out a demand profile that supports new entrants across materials, equipment, and chip design.

Key Report Takeaways

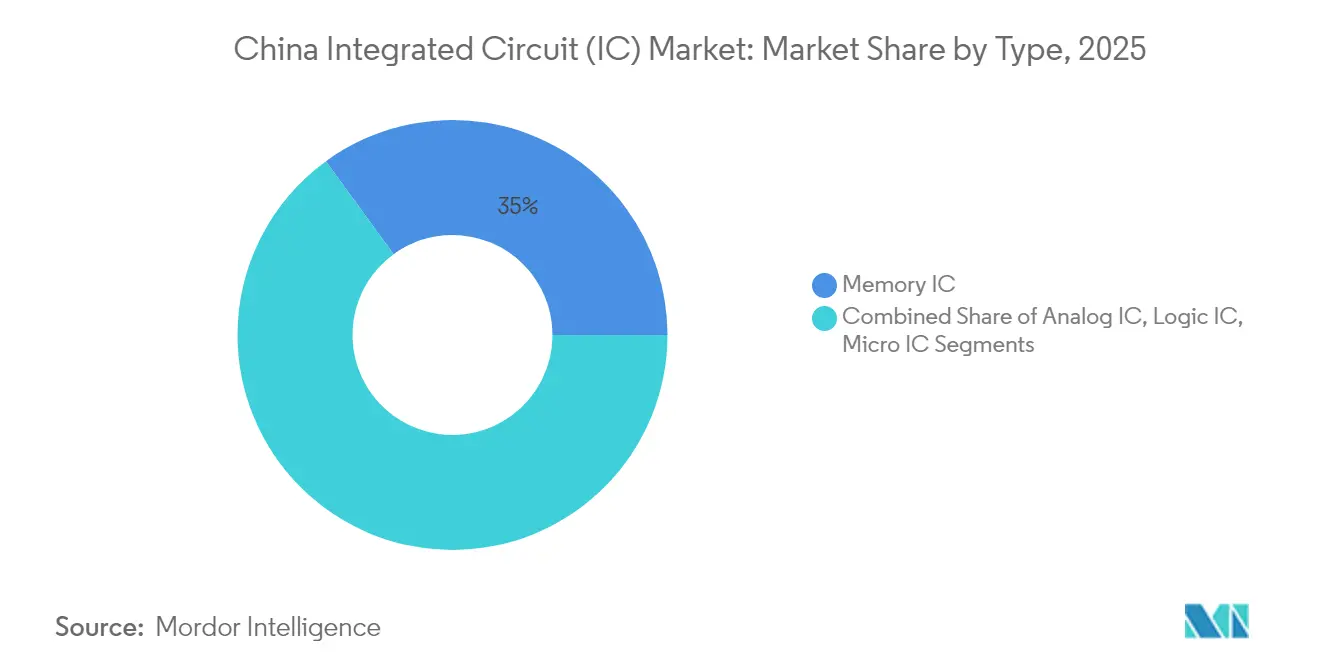

- By type, memory ICs captured 35.02% of the China integrated circuit market share in 2025; logic ICs are advancing at a 9.55% CAGR through 2031.

- By wafer size, 300 mm lines held 71.45% revenue share in 2025, whereas 450 mm pilot capacity is projected to expand at a 13.22% CAGR to 2031.

- By process node, ≤28 nm technology accounted for 62.50% of the China integrated circuit market size in 2025; the 16/14 nm tier is growing fastest at 11.78% CAGR.

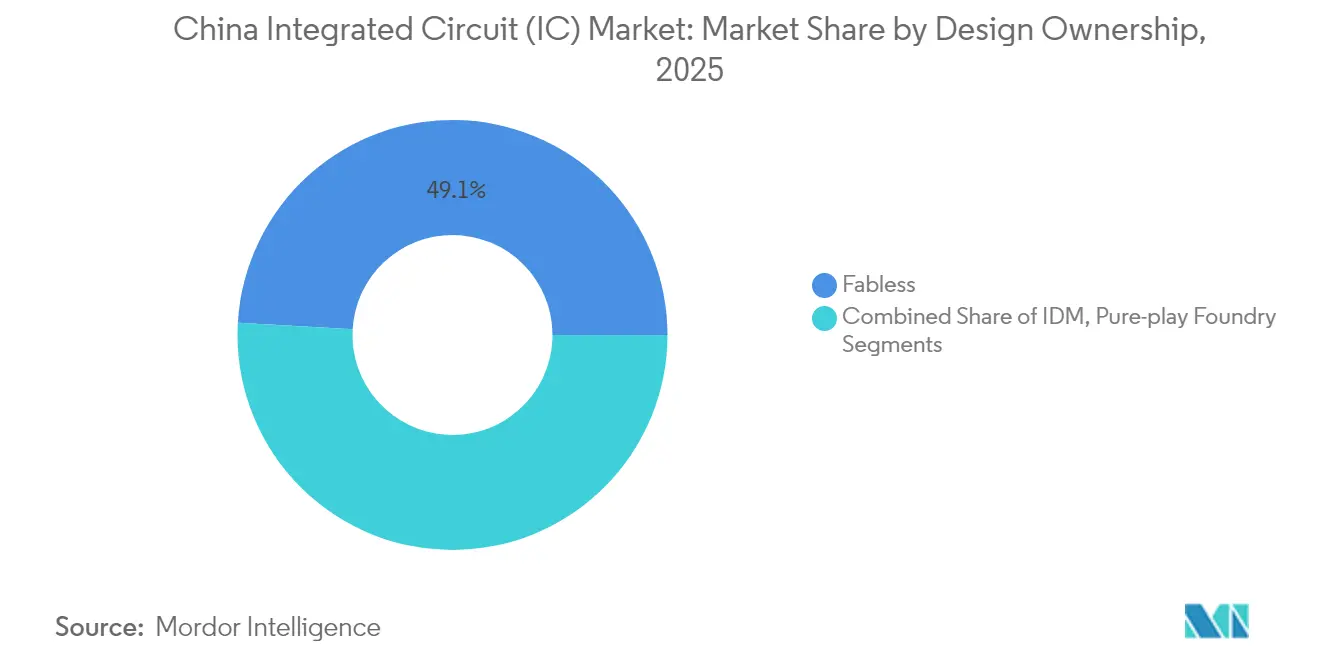

- By design ownership, fabless firms led with a 49.10% share in 2025, while pure-play foundries post the highest projected CAGR at 9.98% through 2031.

- By application, consumer electronics held 45.75% of China's integrated circuit market share in 2025, and automotive IC demand is set to rise at an 11.02% CAGR.

- By geography, East China generated more than 25% of national revenue in 2025, underscoring the region’s dense cluster of fabs and design centers.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Competitive positioning in China includes both locally based firms and those operating across multiple regions. The market landscape in the global integrated circuits industry research shows how these players are arranged internationally.

China Integrated Circuit (IC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Semiconductor Fund Phase III | +2.8% | East and South-Central China | Medium term (2-4 years) |

| EV and NEV Policy Push | +1.9% | National, strongest in East and South-Central | Medium term (2-4 years) |

| Hyperscale AI/Cloud Build-outs | +1.7% | Shanghai, Beijing, Guangdong | Short term (≤ 2 years) |

| Made-in-China IoT Deployments | +1.2% | Manufacturing provinces | Medium term (2-4 years) |

| Sanctions-Driven Localization | +1.6% | National | Long term (≥ 4 years) |

| Surge in 5G Base-Stations | +0.6% | Tier-1 and Tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

National Semiconductor Fund Phase III Driving Fab Capacity Expansion

The USD 47.5 billion third-phase Big Fund channels capital directly into high-bandwidth memory and advanced DRAM projects. With the Ministry of Finance holding 17.44%, close oversight ensures alignment with national technology goals. YMTC has already lifted output to 500,000 3D NAND wafers per month, fortifying China’s position in premium storage devices. Mature-node expansions that underpin automotive and industrial chips receive priority funding, bridging immediate shortfalls caused by import restrictions. The program’s structure ties milestone financing to capacity targets, narrowing gaps with leading overseas manufacturers and stimulating local toolmakers. Collectively, these initiatives quicken the scale-up of domestic fabs and firm long-term supply security across the China integrated circuit market.

EV and NEV Policy Push Boosting Demand for Automotive-grade ICs

China sold 11 million electric vehicles in 2024, equal to nearly half of national car sales.[1]International Energy Agency, “Global EV Outlook 2025,” iea.org Aggressive purchase subsidies and dual-credit mandates translate into surging orders for power management ICs, SiC modules, and automotive microcontrollers. BYD Semiconductor’s power module share hit 28.9% in 2023 as the company vertically integrated silicon carbide and IGBT lines into its EV stack. With the automotive IC pool forecast at USD 23 billion in 2025, local foundries are tailoring 28 nm and 16 nm processes for functional safety compliance. Partnerships between carmakers and chip designers deepen, accelerating qualification cycles and fostering an ecosystem that anchors future mobility electronics inside the China integrated circuit market.

Hyperscale AI/Cloud Build-outs Creating Custom Accelerator Demand

Cloud capital expenditure will climb 20-25% YoY in 2025 as Tencent, Alibaba, and Baidu deploy AI servers at scale. Export-control pressure is hastening domestic ASIC development, trimming the foreign GPU share of China’s AI compute purchases from 63% in 2024 to a projected 41.5% in 2025. Firms such as Huawei and Cambricon are taping out 7 nm and 5 nm AI cores, driving demand for high-density HBM stacks at YMTC and CXMT. Foundries gain additional revenue from packaging services optimized for large-die chiplets. The resulting feedback loop of in-country design and fabrication keeps more value inside the China integrated circuit market, sustaining a high-growth pocket even under geopolitical constraints.

Made-in-China IoT Deployments in “Digital Workshop” Manufacturing

Industrial modernization delivered 4.514 billion IC units in 2024, a 22.2% increase year-on-year.[2]National Bureau of Statistics of China, “Statistical Communiqué 2024,” stats.gov.cn The Ministry of Industry and Information Technology’s “Digital Workshop” framework equips factories with sensor-rich edge nodes that require ultra-reliable microcontrollers. Local vendors respond by ruggedizing 40 nm and 22 nm platforms for high-temperature, high-EMI settings common in steel and petrochemical plants. Demand cascades to analog front-end suppliers and protocol-stack IP providers, expanding the mid-tier of the China integrated circuit market. Scaled deployments are expected to grow most quickly in coastal manufacturing belts, but central provinces are also incorporating IoT tooling to ease labor-cost pressures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restricted Access to EUV Lithography Tools | -1.8% | East China | Long term (≥ 4 years) |

| Acute Shortage of Senior IC Engineers | -1.3% | National tech hubs | Medium term (2-4 years) |

| Price Erosion from 28 nm Over-capacity | -0.7% | National | Short term (≤ 2 years) |

| Persistent IP and Patent Litigation Risks | -0.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Restricted Access to EUV Lithography Tools

Export controls bar Chinese fabs from purchasing ASML’s EUV scanners, stalling mass-production economics below 7 nm. SMIC has replicated 7 nm logic using multi-patterned DUV, yet higher mask counts raise cost and reduce yield. Stricter Dutch and Japanese licensing rules, effective April 2025, deepen the bottleneck. This restraint pushes domestic R&D toward indigenous lithography but widens the cost gap with rivals leveraging full EUV. High-performance computing segments therefore, lean on advanced packaging and chiplet approaches to bridge performance shortfalls while policymakers negotiate for partial exemption

Acute Shortage of Senior IC Design and Process Engineers

Roughly 70,000 skilled positions remain unfilled, especially for FinFET process integration and high-bandwidth memory layout. Rising salary inflation inflates project budgets and lengthens time-to-market, eroding competitiveness. Firms establish satellite R&D offices in Singapore and Munich to access broader talent pools, while universities roll out fast-track semiconductor curricula. Though these initiatives broaden the funnel, hands-on expertise builds slowly, making this a medium-term drag on the China integrated circuit market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Memory IC Dominates Amid Logic Growth

Memory devices accounted for 35.02% of China integrated circuit market share in 2025 on the back of YMTC’s 3D NAND ramp-up and CXMT’s DDR5 debut. The China integrated circuit market size tied to memory is set to expand steadily as the Big Fund channels billions into high-bandwidth memory lines. Logic ICs, however, are poised for a 9.55% CAGR as AI inference, autonomous driving domains, and edge computing broaden demand for performance-dense SoCs.

The mixed-signal subset posts healthy gains because converged analog-digital architectures are critical for automotive sensors and industrial controls. Analog ICs remain indispensable in high-reliability sectors, giving local fabs with 180 nm and 90 nm assets enduring relevance. Micro IC demand accelerates alongside IoT proliferation, where domestic CPU players such as Loongson offer non-ARM alternatives that further localize the stack.

By Wafer Size: 450 mm Pilot Signals Future Scaling

The 300 mm format generated 71.45% of national revenue in 2025 as SMIC, Hua Hong, and several JV fabs maxed out capacity. These lines underpin most advanced logic, memory, and RF shipments and provide the cost base from which the China integrated circuit market scales. A nascent 450 mm pilot, projected to grow 13.22% CAGR, demonstrates China’s willingness to leapfrog international hesitation and secure long-term manufacturing edge.

Older ≤200 mm fabs sustain niche analog, power, and display-driver production. Government incentives permit selective modernization of 200 mm equipment to safeguard domestic supply of specialty nodes. This tiered wafer-size landscape creates flexibility, allowing manufacturers to balance capex risk while meeting differentiated product portfolios.

By Process Node: Legacy Dominance with Advanced-Node Momentum

Legacy ≤28 nm nodes represented 62.50% of the China integrated circuit market size in 2025, supplying cost-sensitive automotive and industrial segments. Subsidized tool procurement and plentiful engineering know-how make this space a bastion of self-reliance. Meanwhile, 16/14 nm runs at a brisk 11.78% CAGR, validating China’s incremental path toward finer geometries even without EUV.

The 10 nm and 7 nm echelons, implemented via advanced DUV multi-patterning, grant domestic smartphone and AI chipsets competitive performance, albeit at higher cost. This dual-track model positions foundries to monetize mature nodes today while investing in next-gen research that may mitigate EUV restrictions over the long haul.

By Design Ownership: Fabless Innovation Drives Ecosystem

Fabless companies captured 49.10% revenue in 2025, reflecting China’s edge in system-level insight and rapid design cycles. High-profile houses like HiSilicon and UNISOC iterate mobile and IoT designs attuned to domestic standards, keeping IP value local. Pure-play foundries, advancing at 9.98% CAGR, convert policy funding into new 28 nm and 14 nm modules, tightening supply chains inside the China integrated circuit market.

IDMs, highlighted by BYD Semiconductor, marry process ownership with dedicated end-use-EV traction inverters and onboard chargers. This integration builds yield learning into product design, boosting performance reliability for critical automotive electronics. The tripartite structure-fabless, foundry, IDM-now interacts in deeper co-development cycles that speed silicon bring-up and improve overall capital efficiency.

By Application: Automotive Segment Accelerates Amid Consumer Electronics Leadership

Consumer electronics led revenue with 45.75% China integrated circuit market share in 2025, powered by Guangdong’s manufacturing muscle. Smartphones, PCs, and wearables consume high volumes of memory, processors, and power management ICs, anchoring baseline fab-utilization rates. That said, automotive applications record an 11.02% CAGR, with EV content per unit climbing steeply as vehicles shift to zonal architectures and ADAS platforms.

Telecom infrastructure maintains steady demand for RF front-ends and switch matrices as 5G densification progresses. Industrial IoT deployments produce a secondary surge for rugged microcontrollers and sensor fusion ASICs. This diversification shelters the China integrated circuit market from single-segment volatility and seeds new specializations among design houses.

Geography Analysis

East China-including Shanghai, Jiangsu, and Zhejiang-generated more than a quarter of national semiconductor revenue in 2025. The Yangtze River Delta cluster, anchored by SMIC’s multiple fabs and a dense web of CAD software firms, benefits from proximity to tier-one universities and mature logistics infrastructure. Government subsidies offset land and utility costs, prompting fresh 300 mm and 200 mm expansions for memory and analog output. Regional co-operation agreements streamline permitting and accelerate time-to-fab, sustaining East China’s leadership within the China integrated circuit market.

South-Central provinces-especially Guangdong-hold the second-largest share, leveraging a USD 642 billion electronics industry that pulls through large ASIC and connectivity chip volumes. Shenzhen’s concentration of fabless start-ups fosters rapid tape-out cycles for AIoT devices, while local OSAT houses package chips destined for nearby smartphone plants. Hunan and Hubei add backend capacity and advanced materials, broadening the region’s capability stack.

Central and western corridors-Chongqing, Sichuan, Shaanxi-are gaining momentum as policy incentives entice fabs inland. Chongqing targets a trillion-yuan IC cluster, focusing on automotive-grade semiconductors to align with the city’s vehicle assembly base. Xi’an leverages historic defense microelectronics institutes to nurture memory and compound-semiconductor ventures. PwC’s 2024 survey shows 47% of multinationals considering these regions for production relocation, signaling a gradual rebalancing of the China integrated circuit market’s geographic footprint.

Mordor Intelligence tracks the integrated circuits market across other major regions such as Europe, with additional country-level coverage spanning South Korea, Taiwan, and United States, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

China’s semiconductor arena combines pockets of fragmented. SMIC, Hua Hong, YMTC, and CXMT command core manufacturing nodes, yet a long tail of more than 1,000 fabless firms populates consumer, industrial, and AI niches. Subsidized R&D budgets push companies beyond capacity chases toward proprietary IP in materials, lithography, and advanced packaging. Huawei’s cumulative CNY 215 billion (USD 30.00 billion) investment bankrolls internal chip programs and underwrites joint ventures that fill supply-chain gaps.

White-space remains in semiconductor tools and design-automation software. Naura and ACM Research have raised the domestic share of etch, deposition, and cleaning gear to one-third, yet EDA suites still depend heavily on U.S. vendors. Domestic start-ups are prototyping RISC-V cores and 2.5D interposers, creating disruptive wedges in server and edge-AI verticals. Geopolitical pressures further complicate strategy, with export-license constraints forcing JVs to engineer “clean rooms” entirely free of restricted technology.

Strategic moves highlight a pivot to value-added differentiation. SMIC’s 28 nm capacity build in Beijing, Huawei’s 7 nm Kirin 9000S reveal, and BYD Semiconductor’s funding expansion for SiC illustrate vertical integration designed to lock in captive demand. Collective learning curves spread quickly across the ecosystem, compressing time lag between international and domestic specifications and reinforcing the resilience of the China integrated circuit market.

China Integrated Circuit (IC) Industry Leaders

Semiconductor Manufacturing International Corporation (SMIC)

HiSilicon (Huawei Technologies Co., Ltd)

Yangtze Memory Technologies Co (YMTC)

UNISOC

Naura Technology Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Guangdong Tianyu Semiconductor disclosed plans to raise SiC epitaxial wafer output to 420,000 pieces per year, targeting 6-inch and 8-inch formats.

- April 2025: Guangdong Tianyu Semiconductor disclosed plans to raise SiC epitaxial wafer output to 420,000 pieces per year, targeting 6-inch and 8-inch formats.

- April 2025: ZTE filed more than 5,500 chip-sector patent applications, deepening its IP portfolio in AI and 5G semiconductors.

- February 2025: Huawei’s HiSilicon unveiled the Kirin 9000S processor on SMIC’s 7 nm line, marking progress in advanced node production despite EUV curbs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines China's integrated circuit market as the annual revenue generated from all newly fabricated monolithic semiconductor devices, including analog, logic, memory, and micro ICs, designed or produced within the nation and sold to domestic or export customers. Coverage spans wafers up to pilot-scale 450 mm lines and process nodes from legacy 65 nm through the latest 7 nm class.

Scope exclusion: We do not track discrete semiconductors, passive components, packaging substrates, or resale of imported finished ICs, keeping our scope tightly focused on true IC output.

Segmentation Overview

- By Type

- Analog IC

- General-purpose IC

- Application-specific IC

- Logic IC

- TTL

- CMOS

- Mixed-Signal IC

- Memory IC

- DRAM

- NAND/NOR Flash

- Other Memories (SRAM, EEPROM)

- Micro IC

- Microprocessors (MPU)

- Microcontrollers (MCU)

- Digital Signal Processors

- Analog IC

- By Wafer Size

- = 200 mm

- 300 mm

- 450 mm (Pilot)

- By Process Node

- = 65 nm (Legacy)

- 45/40 nm

- 28 nm

- 16/14 nm

- 10/7 nm

- By Design Ownership

- Fabless

- IDM

- Pure-play Foundry

- By Application

- Consumer Electronics

- Automotive

- IT and Telecommunications

- Industrial and Automation

- Other Applications

- By Geography

- East China (Shanghai, Jiangsu, Zhejiang)

- South-Central China (Guangdong, Hunan, Hubei)

- North China (Beijing, Tianjin, Hebei)

- Northeast China (Liaoning, Jilin, Heilongjiang)

- Southwest China (Sichuan, Chongqing, Yunnan)

- Northwest China (Shaanxi, Gansu, Xinjiang)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next interviewed foundry engineers, fabless design managers, equipment vendors, and large distributors across East, South-Central, and North China. Their inputs verified shipment splits, average selling prices, and ramp timelines that secondary data alone would miss.

Desk Research

We began by mapping authoritative public datasets, drawing on the National Bureau of Statistics of China, customs HS-level trade records, WSTS shipment tables, and MIIT capacity bulletins. Trade association yearbooks such as CSIA and SEMI, together with peer-reviewed papers indexed in IEEE Xplore, enriched supply-side unit insights.

To cross-check demand signals, our team reviewed OEM annual reports, 10-K filings, investor decks, and respected press coverage. Subscription resources that Mordor analysts access, including D&B Hoovers and Dow Jones Factiva, supplied hard financials and news flow. The sources noted illustrate our breadth, and many additional references informed gap closure.

Market-Sizing & Forecasting

A top-down build starts with domestic production plus net imports converted to value, followed by a demand-pool check that applies penetration rates in consumer electronics, automotive, and cloud infrastructure. Select bottom-up roll-ups of sampled supplier revenue and distributor billings reconcile remaining variances. Key variables include wafer start capacity, die-size trends, ASP erosion curves, localization incentives, and node-migration speed. Multivariate regression links those drivers with outlooks for EV production, smartphone output, and announced semiconductor capex, producing our 2025-2030 forecast.

Data Validation & Update Cycle

Every draft passes an analyst peer review where anomalies trigger source re-verification. Reports refresh each year, with interim updates for impactful policy shifts or fab incidents. Before dispatch, we have a final sanity check so clients receive the most current view.

Why Mordor's China Integrated Circuit Baseline Commands Reliability

Published estimates often diverge because firms choose different product baskets, discount factors, and currency bases. Our disciplined scope definition, fresh primary pricing checkpoints, and yearly refresh reduce that noise.

Key gap drivers emerge when others omit long-tail analog niches, assume static ASPs, or rely on outdated exchange rates. We incorporate node-specific learning curves, which strengthens confidence in our totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 216.9 B (2025) | Mordor Intelligence | |

| USD 178 B (2024) | Regional Consultancy A | Excludes micro-IC segment and 300 mm pilot output |

| USD 216.5 B (2024) | Industry Association B | Uses shipment value only without channel inventory adjustment |

These comparisons show that Mordor's balanced blend of verified capacity data, channel checks, and price trackers delivers a dependable baseline that decision-makers can trace and replicate.

Key Questions Answered in the Report

What is the current value of the China integrated circuit market?

The China integrated circuit market size is USD 237.99 billion in 2026 and is forecast to reach USD 378.84 billion by 2031.

Which segment holds the largest share of China’s IC revenue?

Memory ICs lead with 35.02% market share, reflecting substantial domestic capacity in 3D NAND and DRAM.

How fast is automotive semiconductor demand growing in China?

Automotive IC revenue is projected to grow at an 11.02% CAGR from 2026 to 2031, driven by record EV production.

Why is East China the primary semiconductor hub?

Shanghai, Jiangsu, and Zhejiang offer dense fab clusters, top-tier universities, and targeted subsidies, collectively providing more than 25% of national IC output in 2025.

What impact do export controls have on China’s advanced-node ambitions?

Restrictions on EUV tools slow sub-7 nm scaling, but domestic foundries are pursuing multi-patterned DUV techniques and chiplet architectures to partially offset the limitation.

How substantial is government funding for China’s semiconductor expansion?

The third-phase National IC Fund alone injects USD 47.5 billion, focusing on high-value memory and mature-node scaling to bolster self-sufficiency.

Page last updated on: