Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.74 Billion |

| Market Size (2026) | USD 9.98 Billion |

| Market Size (2031) | USD 11.27 Billion |

| Growth Rate (2026 - 2031) | 2.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hong Kong Facility Management Market Analysis by Mordor Intelligence

The Hong Kong facility management market size was valued at USD 9.74 billion in 2025 and estimated to grow from USD 9.98 billion in 2026 to reach USD 11.27 billion by 2031, at a CAGR of 2.47% during the forecast period (2026-2031). The expansion rate reflects a mature real-estate base where incremental value comes from service sophistication, technology integration, and strict regulatory compliance rather than new floor-area additions. Government megaprojects, a surging data-center footprint, and mandatory green-building standards are the leading demand catalysts, while workforce shortages and aggressive low-bid tenders constrain margin expansion. International and local providers, therefore, focus on integrated contracts, digital maintenance platforms, and ESG-oriented offerings to capture premium opportunities inside the Hong Kong facility management market.

Key Report Takeaways

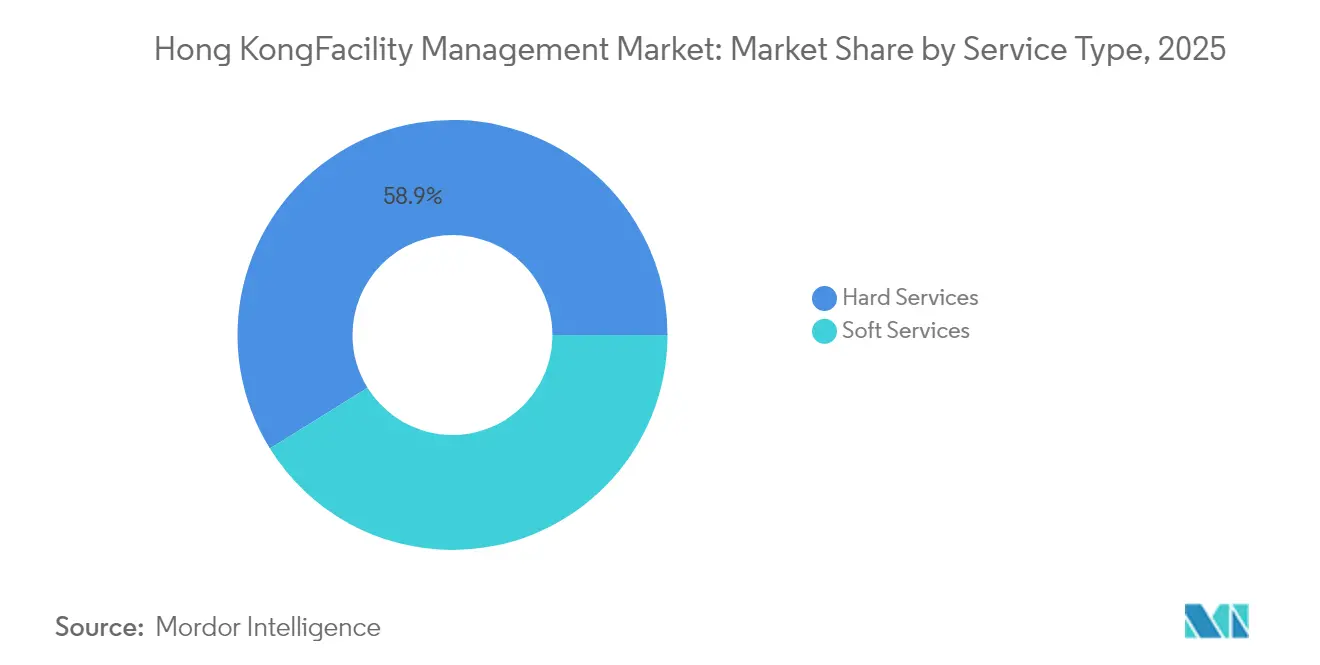

- By service type, Hard Services commanded 58.85% revenue share in 2025, whereas Soft Services is forecast to post a 3.63% CAGR to 2031 as wellness, security, and waste-management contracts scale up.

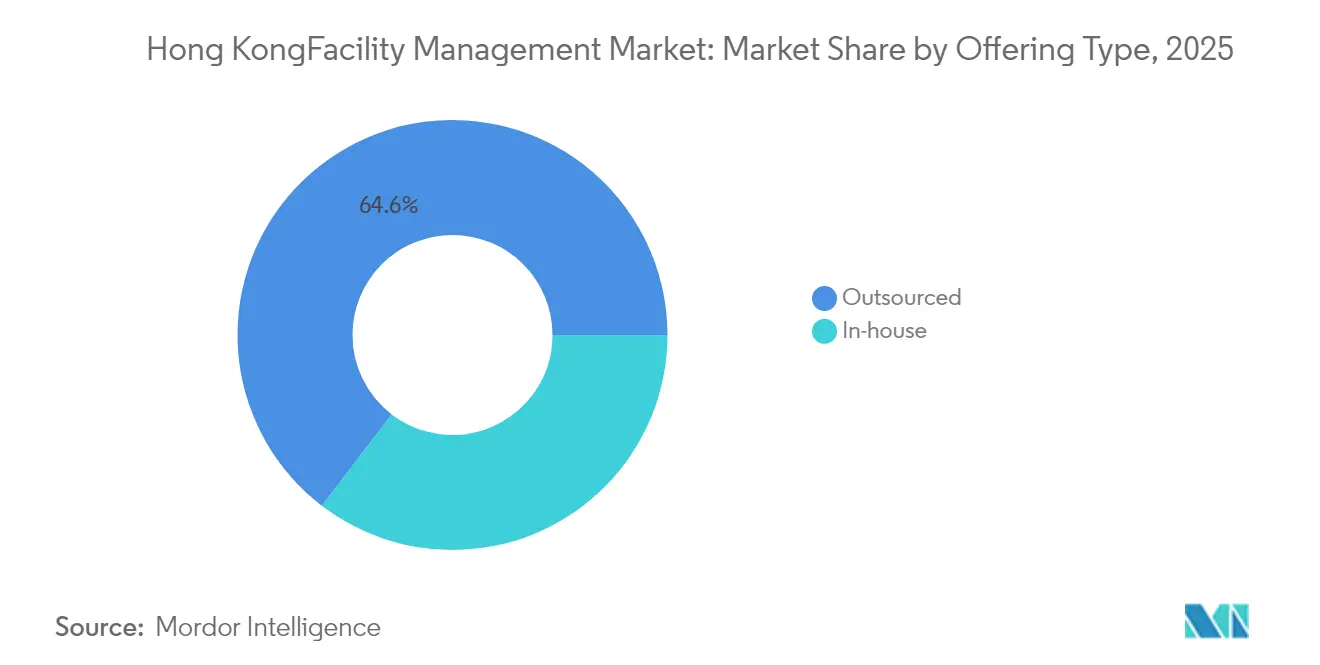

- By offering type, outsourced models accounted for 64.60% of the Hong Kong facility management market share in 2025, and the category is set to grow at 3.12% through 2031, driven by cost-flexibility needs and new procurement-transparency rules.

- By end-user industry, the Commercial segment held 37.05% of the Hong Kong facility management market size in 2025; Institutional and Public Infrastructure is projected to expand at 4.02% CAGR, supported by refurbishment budgets and transport links.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Hong Kong Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid recovery in Grade-A office occupancy post-pandemic | +0.8% | Hong Kong Island, Kowloon Central | Medium term (2-4 years) |

| Government-led infrastructure megaprojects boosting FM demand | +1.2% | New Territories, Lantau Island | Long term (≥ 4 years) |

| Corporate push for green buildings and ESG-certified facilities | +0.6% | Central, Admiralty, Tsim Sha Tsui | Medium term (2-4 years) |

| Cost-optimization drive toward outsourced Integrated FM models | +0.9% | Territory-wide | Short term (≤ 2 years) |

| Mandated BIM–AI convergence driving predictive maintenance services | +0.4% | New developments, data centers | Long term (≥ 4 years) |

| Expanding data-center footprint requiring specialised mission-critical FM | +0.7% | Tseung Kwan O, Tsuen Wan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-led Infrastructure Megaprojects Boosting FM Demand

The government’s capital works pipeline sustained the strongest pull on the Hong Kong facility management market before June 2025. The Kwu Tung North and Fanling North project, valued at HK$17.32 billion (USD 2.25 billion), covered 70 hectares of land formation and required asset-lifecycle FM contracts for MEP, fire safety, and compliance monitoring.[1]Civil Engineering and Development Department, “Advance Site Formation and Engineering Infrastructure Works at Kwu Tung North and Fanling North,” cedd.gov.hk Annual public works spending of HK$225–345 billion (USD 29.2–44.8 billion) further broadened the tender pool for technical service providers. Complex undertakings such as Route 6’s subsea tunnel needed BIM-enabled maintenance schemes that only integrated operators could supply. Providers that pair hard and soft capabilities, therefore, secured multi-year revenue visibility inside the Hong Kong facility management market.

Corporate Push for Green Building and ESG-Certified Facilities

BEAM Plus registrations climbed to 1,996 projects by April 2025, confirming that sustainability metrics became a central procurement filter for landlords and occupiers. Swire Properties reported that 98% of its wholly owned buildings held the highest BEAM Plus rating, raising the performance bar for FM vendors. The Hong Kong Green Label Scheme granted bonus BEAM credits for certified products, accelerating demand for transparent supply chains. Hang Lung’s tenant-focused “Changemakers” program wove green-service clauses into FM contracts, while ISS created a Group Head of ESG role to embed sustainability know-how. These shifts channelled incremental value toward operators with verified energy-optimisation and reporting capabilities, deepening the Hong Kong facility management market penetration within Grade-A portfolios.

Cost-Optimization Drive Toward Outsourced Integrated FM Models

Economic uncertainty and high interest rates spurred occupiers to swap fixed payrolls for variable-cost contracts. CBRE’s facility-management revenue rose 16% year-on-year in Q1 2025, led by technology and life-sciences clients seeking bundled solutions. Outsourcing already held a 65.1% share of the Hong Kong facility management market in 2024, and the Building Management Amendment Ordinance 2024 mandated tender transparency that favoured licensed integrated providers. Clients realised savings of up to 12% versus fragmented sourcing, reinforcing the pull toward single-invoice models. As a result, outsourced Integrated FM is set to outgrow the overall Hong Kong facility management market through 2030.

Expanding Data-Centre Footprint Requiring Mission-Critical FM

Cloud and AI workloads sparked a data-centre construction spree across Tseung Kwan O and Tsuen Wan. Equinix committed USD 124 million to the HK6 site, featuring 3,550 high-density cabinets with liquid cooling that demands 24/7 thermal analytics and redundancy management. SUNeVision launched plans for the 470,000 square-foot Mega Plus campus, necessitating predictive power-usage assessments and Tier-4 security protocols. Mission-critical FM contracts typically price at a 40–60% premium over standard commercial assets, making the segment the most profitable slice of the Hong Kong facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged real-estate price volatility dampens new contracts | -0.4% | Central, Admiralty, Causeway Bay | Short term (≤ 2 years) |

| Escalating labour costs amid a skilled technician shortage | -0.6% | Territory-wide | Medium term (2-4 years) |

| Tightening foreign-worker visa quotas restricts the FM workforce supply | -0.3% | Territory-wide | Long term (≥ 4 years) |

| Margin squeeze from aggressive low-bid tendering culture | -0.2% | Government contracts, SME sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Labour Costs Amid Skilled-Technician Shortage

The Labour and Welfare Bureau projected a territory-wide deficit of 180,000 workers by 2028, with construction and city operations trades hardest hit. Certified HVAC technicians commanded wage increases of 8–10% during 2024, eroding contract margins for FM providers. The Construction Industry Council promoted Modular Integrated Construction, which delivered 30% faster build times and 70% labour savings on pilot projects, but up-front technology investment weighed on service providers. Firms responded by cross-training staff and adopting sensor-based fault detection to maintain service standards inside the Hong Kong facility management market despite the talent squeeze.

Tightening Foreign-Worker Visa Quotas Restricting Workforce Supply

Policy changes narrowed visa pathways for blue-collar roles in 2024, forcing FM operators to rely more on local recruitment and automation. Although the Top Talent Scheme attracted managerial applicants, it did little for cleaning and security shortages. Providers installed IoT networks—such as Milesight’s estate-wide rollout—to replace manual patrols and reduce headcount needs by 40%. Over time, firms with robust training pipelines and digital-twin capabilities will remain resilient in the Hong Kong facility management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering Type: Outsourcing Commands Two-Thirds of Spend

Outsourced contracts held 64.60 of % Hong Kong facility management market share in 2025 and are projected to rise to 66.20% by 2031. Integrated FM combines engineering, cleaning, and catering in one invoice, creating 10–12% total-cost savings versus fragmented sourcing. The Building Management Amendment Ordinance 2024 required greater tender transparency and favoured licensed operators, accelerating the move toward professional providers. In-house teams persisted in hospitals, universities, and statutory bodies that value security and direct control, yet even these entities adopted outsourced consultancy for energy audits, adding incremental revenue to the Hong Kong facility management market.

By End-User Industry: Commercial Stock Dominates, Public Infrastructure Accelerates

Commercial assets generated 37.05% of the Hong Kong facility management market size in 2025. Grade-A vacancies peaked at 12.9% in January 2024, but landlords upgraded tenant-experience amenities to protect rental yields, fuelling demand for smart-office support. Logistics facilities such as Goodman’s 112,549 square-meter Gateway complex required 24/7 systems monitoring, broadening the service scope.

Institutional and Public Infrastructure is poised for the fastest growth at 4.02% CAGR. The Architectural Services Department allocated HK$1–30 million (USD 0.13–3.9 million) per refurbishment across parks, sports centres, and correctional buildings in its 2024-25 program. Healthcare facilities adopted AI-driven waste-segregation and predictive maintenance to meet infection-control standards, adding high-margin work orders to the Hong Kong facility management market.

By Service Type: Hard Services Anchor Revenue, Soft Services Lead Growth

Hard Services accounted for 58.85% of 2025 revenue, highlighting how regulatory inspections on electrical, plumbing, and fire-safety systems underpin the Hong Kong facility management market. Five-year electrical recertifications and monthly potable-water checks kept contractor backlogs high. Record summer temperatures, averaging 29.7 °C in August 2023, further increased HVAC optimisation demand. Consequently, Hard Services retained the largest share of the Hong Kong facility management market in 2025.

Soft Services will grow fastest at 3.63% CAGR through 2031. Housing Society pilots showed that pay-as-you-throw schemes cut refuse by 10% and lifted recycling by 23%, triggering higher demand for specialised cleaning and waste-audit contracts. Security, front-of-house, and catering vendors extended offerings around wellness and digital-badge access. Therefore, Soft Services will expand its slice of the Hong Kong facility management market even though Hard Services continues to anchor absolute revenue.

Geography Analysis

Hong Kong Island delivered the highest per-square-foot FM spend because Central and Admiralty housed the bulk of Grade-A offices. Even amid elevated vacancies, landlords retained premium maintenance contracts to uphold ESG credentials. Kowloon’s mixed commercial-industrial profile demanded both heavy-duty mechanical services and retail-oriented soft services, creating a balanced revenue mix for the Hong Kong facility management market.

The New Territories emerged as the principal growth engine. Government plans for a Northern Metropolis and Route 6 tunnel opened demand for compliance-focused FM, while Tseung Kwan O’s data-centre cluster added mission-critical requirements at premium rates. Modular Integrated Construction pilots in Fanling demonstrated cost and speed gains that later translated into lower life-cycle FM expenses but higher digital-service intensity.

Across all districts, rising climate volatility raised cooling loads. Observatory forecasts indicated 2025 would again challenge heat records, pushing asset owners toward AI-based chiller optimisation in an effort to curb energy bills and maintain indoor comfort within the Hong Kong facility management market.

Competitive Landscape

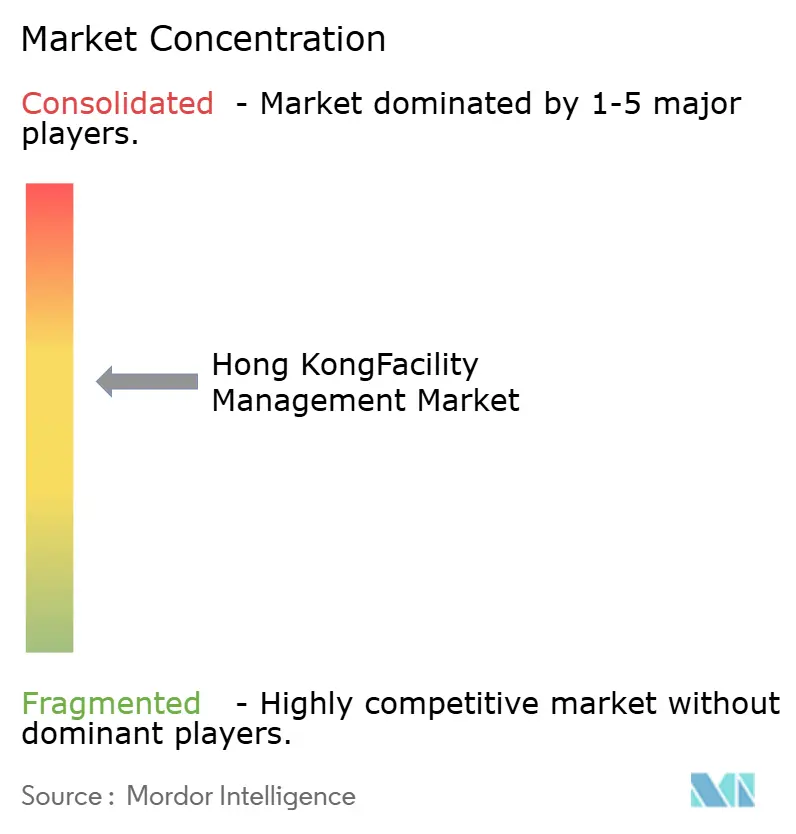

The market remained moderately fragmented in 2024-25. Multinationals ISS, CBRE, Sodexo, JLL leveraged global platforms to secure cross-border contracts. Regional specialists like Savills Hong Kong, Knight Frank, and Colliers combined brokerage insight with local compliance expertise to upsell FM mandates. Domestic operators, including Sino Property Services, Hang Yick, and Urban Group, retained stronghold positions in residential estates due to community ties and licensing familiarity.

Technology adoption defines competitive advantage. Milesight’s sensor suite cut manual patrol hours and provided real-time alerts, improving response times by 30%.[4]Milesight, “Smart Building Solution Deployment,” milesight.com CBRE integrated AI-driven energy analytics for life-sciences clients, while ISS formalised an ESG governance framework to satisfy green-procurement audits. The Construction Industry Council’s CITF subsidies for BIM, laser scanners, and safety systems lowered capital barriers for prop-tech entrants, intensifying rivalry within the Hong Kong facility management market.

Regulation also shaped positioning. The Building Management Amendment Ordinance 2024 enforced licensed-provider requirements for major property functions, a shift that is expected to nudge smaller, non-compliant firms toward merger or exit. Collectively, the top five suppliers controlled about 40% of 2024 revenue, leaving ample room for consolidation.

Hong Kong Facility Management Industry Leaders

Savills Hong Kong Limited

Knight Frank Hong Kong Limited EAA

G4S Facility Services Hong Kong Limited

Urban Group

Dusservice Hong Kong

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BDx secured financing to expand its hyperscale data centre in Hong Kong, reinforcing mission-critical FM demand.

- April 2025: CBRE posted a 16% rise in facility-management revenue for Q1 2025 as technology and healthcare clients scaled integrated contracts.

- March 2025: – ISS announced a DKK 2.5 billion share buyback after exceeding cash-flow targets, signalling financial strength for further ESG and tech investment.

- February 2025: Equinix confirmed a USD 124 million investment in the HK6 data centre, slated for Q1 2026 commissioning.

Hong Kong Facility Management Market Report Scope

Facility management (FM) is a profession that incorporates many disciplines to ensure functionality, safety, comfort, and efficiency of the built environment by integrating people, process, place, and technology.

The Hong Kong facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

Key Questions Answered in the Report

What is the current size of the Hong Kong facility management market?

The Hong Kong facility management market size reached USD 9.98 billion in 2026 and is expected to hit USD 11.27 billion by 2031 at a 2.47% CAGR during 2026-2031.

Which segment is expanding fastest?

Soft Services is projected to grow at 3.63% CAGR through 2031, outpacing Hard Services as corporations prioritise wellness, security, and waste-audit solutions.

Why is outsourcing dominant in Hong Kong?

Outsourced contracts capture more than 64.60% share because integrated providers deliver 10–12% cost savings and meet new procurement-transparency rules, making them attractive amid economic uncertainty.

How do government megaprojects affect demand?

Projects worth HK$225–345 billion (USD 29.2–44.8 billion) annually require comprehensive FM support from design through operations, adding long-term revenue streams for integrated providers.

What are the main challenges for service providers?

Labour shortages and rising technician wages inflate operating costs, while tighter visa quotas limit foreign-worker inflow, compelling firms to invest in automation and training.

How important is ESG in facility management contracts?

BEAM Plus and Green Label criteria now influence vendor selection, pushing FM companies to offer energy optimisation, transparent sourcing, and real-time sustainability reporting.

Page last updated on: