Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

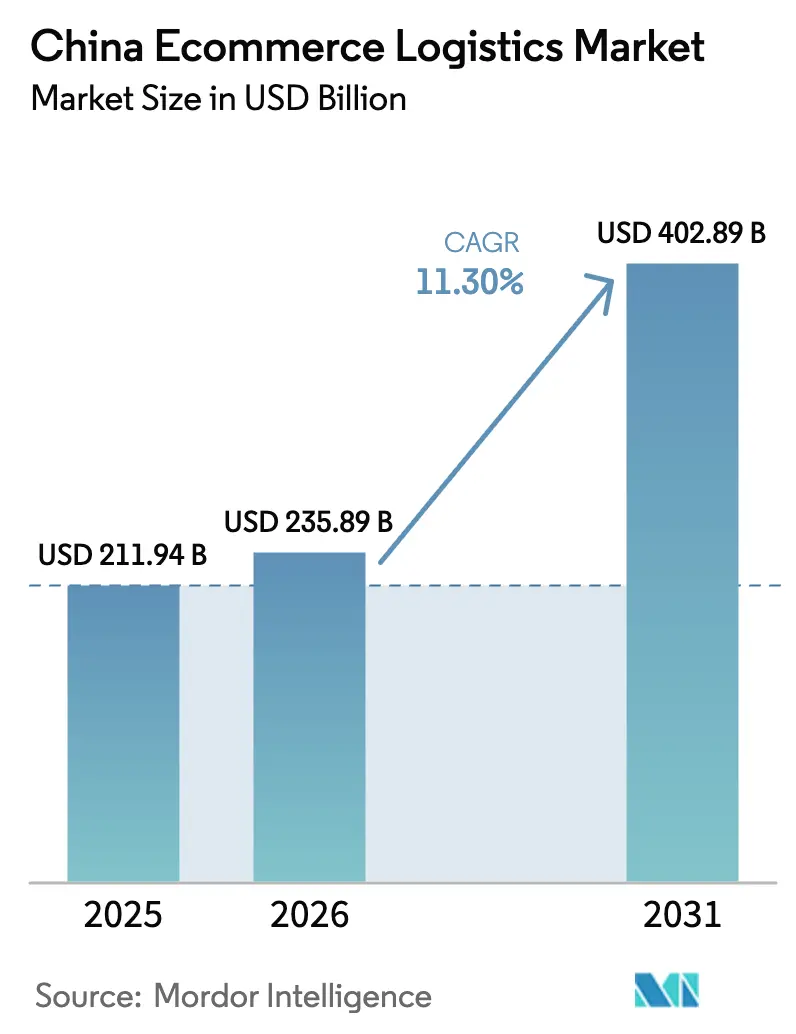

| Base Year Market Size (2025) | USD 211.94 Billion |

| Market Size (2026) | USD 235.89 Billion |

| Market Size (2031) | USD 402.89 Billion |

| Growth Rate (2026 - 2031) | 11.30% CAGR |

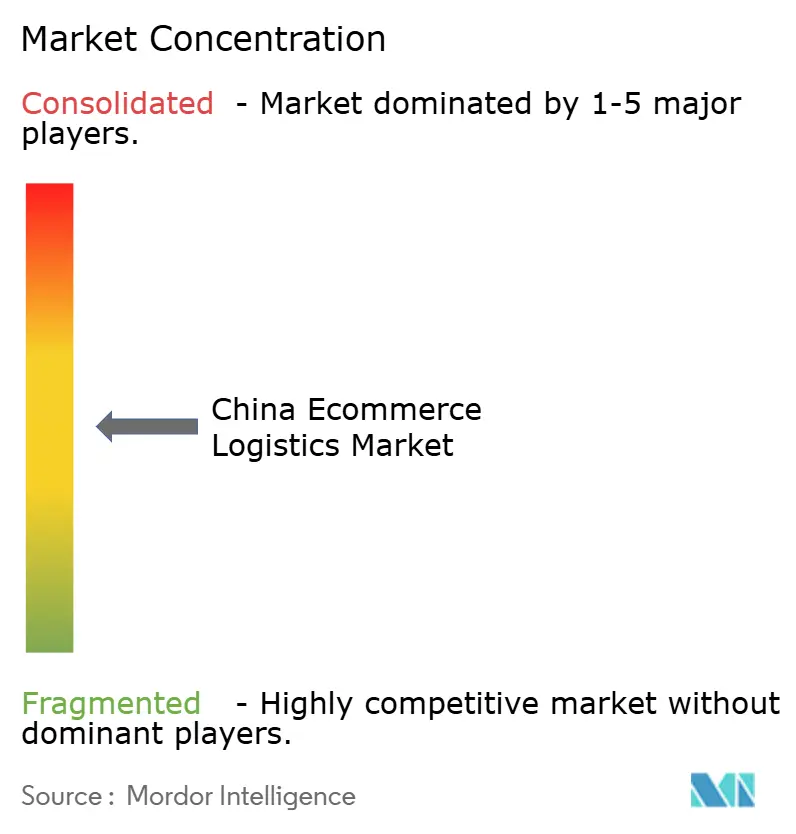

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Ecommerce Logistics Market Analysis by Mordor Intelligence

China E-commerce Logistics market size in 2026 is estimated at USD 235.89 billion, growing from 2025 value of USD 211.94 billion with 2031 projections showing USD 402.89 billion, growing at 11.30% CAGR over 2026-2031. Continuous digital-commerce penetration, government incentives that lower logistics costs, and rapid adoption of automation sustain this growth trajectory. Rising demand for ultra-fast fulfillment, expansion of cross-border pilot zones, and growing disposable incomes in lower-tier cities further amplify volumes. Technology deployments such as autonomous line-haul trucks and AI-driven routing support scale while value-added services create fresh revenue streams. Competitive intensity remains high, yet providers that integrate warehousing, data analytics, and micro-fulfillment hubs capture new margin opportunities within the expansive China e-commerce logistics market.

Key Report Takeaways

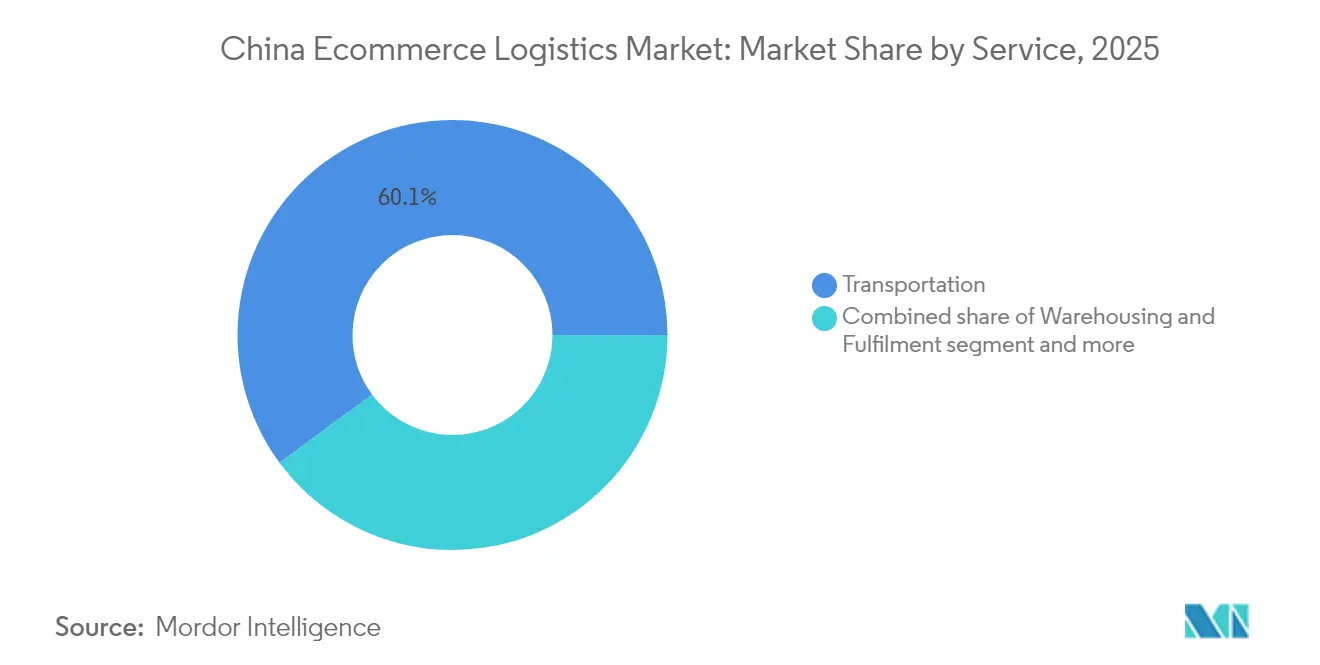

- By service, transportation led with 60.12% of the China e-commerce logistics market revenue share in 2025. The China e-commerce logistics market for value-added services is forecast to advance at a 13.86% CAGR between 2026-2031.

- By business model, the B2C segment held 71.86% of the China e-commerce logistics market share in 2025. The China e-commerce logistics market for C2C is projected to expand at a 13.12% CAGR between 2026-2031.

- By destination, domestic delivery commanded an 83.92% share of the China e-commerce logistics market size in 2025. The China e-commerce logistics market for cross-border outbound is poised for a 14.06% CAGR between 2026-2031.

- By delivery speed, next-day services captured 44.78% of the China e-commerce logistics market revenue in 2025. The China e-commerce logistics market for same-day delivery is set to post a 16.02% CAGR between 2026-2031.

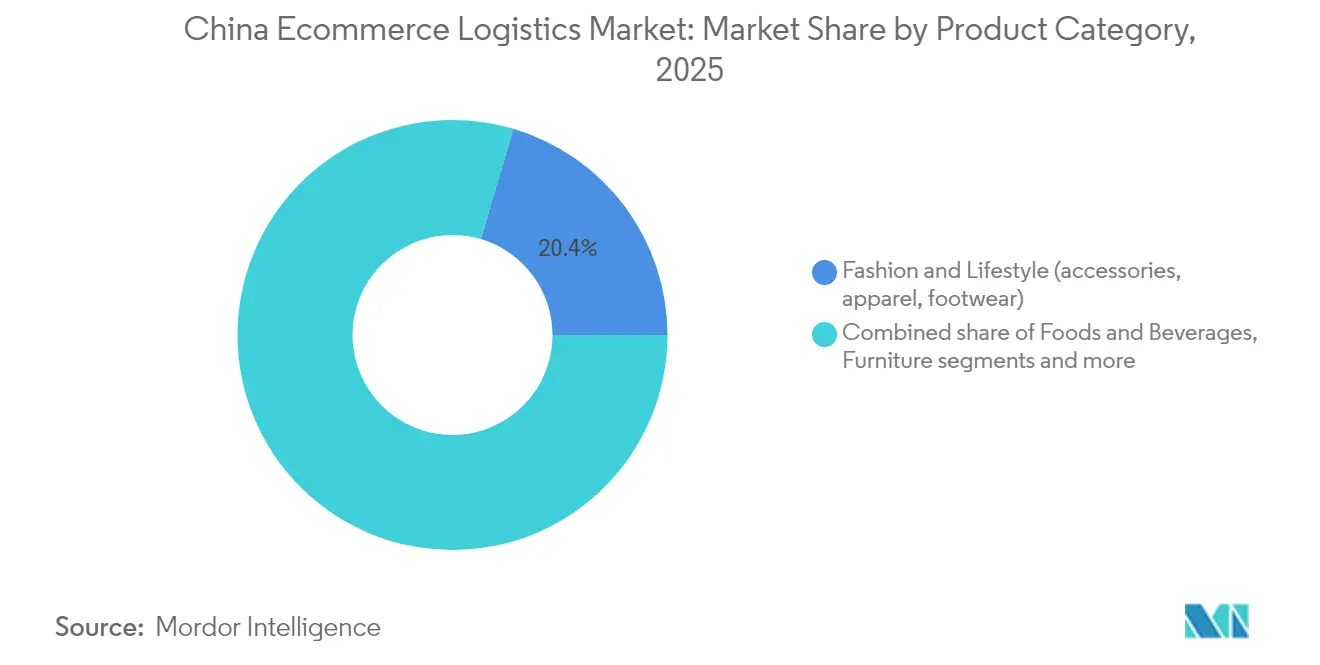

- By product category, fashion and lifestyle led with 20.43% of the China e-commerce logistics market size in 2025. The China e-commerce logistics market for foods and beverages will grow fastest at a 17.05% CAGR between 2026-2031.

- By city-tier, tier-2 cities accounted for a 45.05% share of the China e-commerce logistics market in 2025. The China e-commerce logistics market for tier-3 and below will expand at a 14.68% CAGR between 2026-2031.

- By geography, East China secured a 27.32% share of the China e-commerce logistics market in 2025. The China e-commerce logistics market for Southwest China is forecast to advance at a 13.14% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Ecommerce Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising tier-2 / tier-3 disposable incomes | +2.1% | Central and Southwest China | Medium term (2-4 years) |

| Livestream and short-video shopping boom | +1.8% | Tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Community group-buying adoption | +1.5% | East and South China | Medium term (2-4 years) |

| Silver-economy digital inclusion | +1.2% | National | Long term (≥ 4 years) |

| Duty-free cross-border pilot zones | +0.9% | Hainan and coastal FTZs | Medium term (2-4 years) |

| Thirty-minute micro-fulfillment roll-outs | +1.7% | Major urban cores | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising tier-2 / tier-3 disposable incomes shifting e-commerce GMV beyond tier-1 hubs

Secondary cities now deliver a larger share of national online retail value than premier metros, prompting network redesign and fresh distribution-center investments. Chongqing alone committed RMB 40 billion (USD 5.56 billion) to logistics projects that lowered local freight costs by 3.5%. Rural e-commerce participation, meanwhile, improved household financial resilience by 9.63%, highlighting the socioeconomic benefit of broader fulfillment coverage[1]Diego A. Vazquez-Brust, “E-Commerce Participation and Rural Household Resilience,” MDPI Agriculture, mdpi.com.

Livestream and short-video shopping are elevating impulse-buy conversion rates

Impulse purchases triggered by viral broadcasts generate demand spikes that stretch traditional inventory planning. Providers respond with predictive analytics and cloud-based control towers that redeploy safety stock to micro-fulfillment sites inside dense urban trade areas. Agility becomes a profit driver within the China e-commerce logistics market as retailers lean on one-hour delivery promises to lock in shoppers.

Community group-buying normalizes high-frequency online grocery purchases

Sales at leading platform Xingsheng Selected surged to CNY 30 billion (USD 4.6 billion) in 2024, proving that aggregated neighborhood orders can sustain daily fresh-food fulfillment at scale. Consolidated drop-off points shrink last-mile travel distance, while investment in temperature-controlled fleets positions carriers for long-term volume in the rapidly diversifying China e-commerce logistics market.

Silver-economy adoption of simplified apps is expanding the senior shopper base

The national silver-economy framework promotes age-friendly interfaces and subsidizes community delivery services for the nearly 300 million citizens aged 60-plus expected by mid-century[2]Xiaolan Zhang, “Silver Economy Development Plan 2024,” State Council of the People’s Republic of China, gov.cn. Senior consumers favor predictable time windows and value human interaction, pushing operators to retrain couriers and redesign packaging for ease of handling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating last-mile labor costs in tier-1 hubs | -1.4% | Beijing, Shanghai, Shenzhen | Short term (≤ 2 years) |

| Persistent rural address data-quality gaps | -0.8% | Western provinces | Medium term (2-4 years) |

| Regulatory complexity in cross-border data compliance | -0.6% | Nationwide | Short term (≤ 2 years) |

| Environmental targets raising fleet electrification costs | -0.4% | Coastal megacities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating last-mile labor costs in tier-1 hubs despite automation

Courier wages rise as operators compete for talent to execute doorstep delivery in densely populated towers. Even with driverless truck pilots and automated sorters, human couriers remain indispensable for high-service-level orders, limiting cost-down potential in the Chinese e-commerce logistics market.

Persistent rural address data-quality gaps are raising failed-delivery ratios

Village e-commerce coverage hit 86% by 2024, but inconsistent house-numbering and low GPS precision continue to produce higher redelivery costs. Hybrid truck-plus-drone programs and communal pick-up hubs mitigate inefficiencies, yet a national digital-address registry is still years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation leadership faces value-added disruption

Transportation dominated 60.12% of the China e-commerce logistics market in 2025, underpinned by a 169,000-km expressway grid that connects production zones with consumption hubs. Rail corridors along the Belt and Road funnel export parcels to Europe, while airfreight supports premium electronics. Value-added services are scaling at a 13.86% CAGR as merchants seek unique packaging, reverse-logistics handling, and compliance-ready labeling. SF Express’ “Fengzhiyun” platform shows how data analytics, inventory orchestration, and real-time visibility convert basic haulage contracts into integrated supply-chain partnerships.

Warehousing and micro-fulfillment networks multiply near consumers to enable same-day cut-off times. Robotics automates put-away and picking, trimming unit costs even as wage inflation persists. Air-cargo alliances such as the SF Express–Etihad Cargo joint venture extend reach into the Middle East. Maritime e-packet lanes, especially via Shenzhen and Ningbo, benefit cross-border sellers chasing tax-rebate programs. Competitive advantage now hinges on end-to-end orchestration across these service lines rather than isolated modal excellence, reshaping supplier criteria in the China e-commerce logistics market.

By Business Model: B2C supremacy challenged by C2C innovation

B2C held 71.86% of the China e-commerce logistics market share in 2025, anchored by platform ecosystems that aggregate merchant demand and standardize fulfillment practices. Brands outsource everything from inbound freight to doorstep returns, relying on carrier APIs to sync front-end ordering channels. The C2C segment, expanding at 13.12% CAGR, taps social-commerce momentum as Gen-Z consumers trade secondhand fashion and collectibles. Start-ups launch flat-rate parcel kits and smartphone apps that generate labels through mini-programs, simplifying sporadic shipping for individuals.

Cross-listing between B2C storefronts and C2C resale marketplaces blurs boundaries, with sellers shifting unsold inventory to peer-to-peer channels. That flow diversifies parcel origination points and pushes carriers to offer nationwide pick-up, thereby enlarging the China e-commerce logistics market. Meanwhile, B2B digital procurement platforms deploy bulk rate contracts that stabilize margins yet require multimodal coordination, encouraging carriers to maintain distinct pricing ladders for enterprise versus consumer traffic within the wider China e-commerce logistics industry.

By Destination: Domestic strength enables global expansion

Domestic routes captured 83.92% of 2025 volume, creating economies of density that fund investthe ments in export capacity. Government programs have led to more than 2,500 overseas warehouses totaling 30 million m², positioning Chinese sellers close to foreign buyers. The China e-commerce logistics market size tied to cross-border outbound parcels is on track for a 14.06% CAGR, buoyed by sellers embracing direct-to-consumer models in Europe and the Middle East. New data-transfer rules effective March 2024 require operators to localize systems or adopt secure gateways, lifting compliance costs but safeguarding consumer trust.

Inbound flows satisfy domestic demand for premium food, beauty, and luxury. Bonded fulfillment centers at airports in Guangzhou and Hangzhou speed customs clearance, shrinking delivery promises to under four days. Providers that integrate duty-paid and duty-unpaid inventory in shared facilities gain fill-rate flexibility, reinforcing network value in the evolving China e-commerce logistics market.

By Delivery Speed: Next-day stability versus same-day innovation

Next-day services retained 44.78% share in 2025 by balancing price and service expectations. Same-day parcels, however, will lead growth at 16.02% CAGR through 2031 as urban customers pay premiums for convenience. Instant-commerce programs integrate inventory from hypermarkets, pharmacies, and convenience stores into a single dispatch pool, with AI assigning tasks between couriers, automated lockers, and last-mile robots.

Ultra-fast models face profitability challenges, notably dead-heading on return legs and high rider churn. Operators offset these with dynamic zone routing and predictive batching that aggregates orders along common corridors. Three-to-five-day economy service remains relevant for rural and bulk orders, reminding carriers that speed stratification must coexist in the diverse China e-commerce logistics market.

By Product Category: Fashion leadership meets fresh-food challenge

Fashion and lifestyle retained a 20.43% share in 2025 thanks to liberal return policies and advances in size analytics. Foods and beverages, projected to grow 17.05% CAGR, rely on a quickly maturing cold chain. Providers expand multi-temperature sorting hubs and add smart sensors that transmit humidity and spoilage alerts in real time.

Electronics remain lucrative but face lengthening replacement cycles, intensifying margin pressure. Furniture logistics demand white-glove crews and appointment scheduling to navigate building regulations in large cities, adding complexity to the China e-commerce logistics market.

By City-Tier: Tier-2 dominance enables tier-3 penetration

Tier-2 cities held 45.05% of the China e-commerce logistics market in 2025, reflecting balanced cost and density advantages. Tier-3 and below will record a 14.68% CAGR as digital wallets, rural broadband, and government subsidies converge. Operators leverage tier-2 fulfillment nodes to stage inventory outward, trimming lead times without duplicating fixed assets in every micro-market.

Tier-1 hubs sustain pilot programs for autonomous vans and electronic proof-of-delivery, setting service benchmarks that cascade down the network. The spread of these innovations broadens expectations across the entire China e-commerce logistics market.

Geography Analysis

East China preserved a 27.32% share of the China e-commerce logistics market in 2025, anchored by mature ports, concentrated manufacturing clusters, and dense consumer populations. Consolidated networks around Shanghai and Hangzhou enable cost-effective next-day coverage for nearly 300 million residents. However, rising warehouse rents and labor costs are prompting network diversification toward inland hubs. Southwest China is the fastest-growing region at 13.14% CAGR to 2031, fueled by the New Western Land-Sea Corridor and aggressive infrastructure funds. Chongqing’s RMB 40 billion (USD 5.64 billion) logistics program cut regional supply-chain costs by 3.5% while improving highway connectivity.

South China, with its electronics export base, retains strategic value for cross-border flows into ASEAN markets. High-throughput border checkpoints at Shenzhen’s Huanggang Port accelerate parcel transit into Vietnam and Thailand. North China leverages proximity to resource basins and government institutions, but must modernize to match coastal automation levels. Environmental regulations restrict diesel truck entry in Beijing’s sixth ring road, nudging fleets toward electric vans.

Northeast China focuses on port-based development: Dalian handled 74.09 million tons of cargo in Q1 2024, up 6% year on year. Northwest provinces, with sparse populations, rely on rail and air gateways such as Xi’an to bridge long distances. Local governments invest in public cold-chain depots to attract agrifood sellers, gradually enlarging the China e-commerce logistics market footprint in previously underserved areas.

Competitive Landscape

The China e-commerce logistics market is moderately concentrated: the top five carriers account for about majority of the sector revenue, leaving room for niche entrants. SF Express recorded RMB 134.4 billion (USD 18.69 billion) in H1 2024 revenue and continues to target premium same-day niches. JD Logistics capitalizes on proprietary fulfillment assets that parallel its retail platform, reducing hand-offs and ensuring inventory accuracy. Cainiao integrates cross-border gateways with Alibaba data, while ZTO Express accelerates automation through driverless trucks now transporting up to 1,000 parcels per trip.

Technology rivalry focuses on AI-enhanced route planning, warehouse robotics, and digital twins that model capacity down to rack level. Strategic alliances dominate expansion strategy: SF Express teamed with Etihad Cargo to link Shenzhen and Abu Dhabi, combining Chinese volume with Middle East network access. Cold-chain specialists secure venture funding as fresh-food volumes soar, and community group-buying platforms forge exclusive delivery pacts to protect customer data. Mid-sized regional carriers either join platform ecosystems or risk margin erosion as scale economies deepen in the China e-commerce logistics market.

Service differentiation increasingly revolves around environmental credentials. Operators pilot solar-powered depots and deploy electric three-wheelers in low-emission zones, aligning with the amended Express Delivery Regulations effective June 2025 that mandate green packaging standards. Carriers that embed sustainability metrics into client dashboards win procurement points from multinational brands seeking low-carbon supply chains. Fragmented segments such as oversized freight and rural delivery remain open to consolidation, with private-equity funding supporting roll-up plays that could alter market share dynamics over the forecast horizon.

China Ecommerce Logistics Industry Leaders

SF Express

JD Logistics

Cainiao Network (Alibaba)

ZTO Express

YTO Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: JD.com introduced its first self-operated international express service, signaling overseas growth ambitions.

- April 2025: China Post and Cainiao launched automated “Village Mail Reach” services that boost rural coverage.

- April 2025: The State Council amended the Interim Regulations on Express Delivery, raising green-packaging requirements and formalizing e-commerce–carrier collaboration rules.

- January 2025: Cainiao opened a new warehouse in Rokitno, Poland, to support surging peak-season parcels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China e-commerce logistics market as all value earned inside mainland China from transportation, warehousing, fulfillment, returns handling, and other value-added services that directly support online retail orders across B2C, B2B, and C2C flows. Deliveries that serve only traditional store replenishment or bulk industrial freight are outside the scope.

Scope Exclusion: Instant meal-delivery platforms and pure freight forwarding unrelated to digital transactions are not included.

Segmentation Overview

- By Service

- Transportation

- Road

- Air

- Rail

- Maritime

- Warehousing and Fulfilment

- Value-Added (Labelling, Packaging, Kitting)

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Destination

- Domestic

- Cross-Border – Inbound

- Cross-Border – Outbound

- By Delivery Speed

- Same-day (less than 24 h)

- Next-day (24–48 h)

- Standard (3-5 days)

- Economy (more than 5 days)

- Others

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (accessories, apparel, footwear)

- Furniture

- Electronics and Household Appliances

- Other Products

- By City-Tier

- Tier 1

- Tier 2

- Tier 3 and Below

- By Geography

- East China

- South China

- North China

- Central China

- Northeast China

- Northwest China

- Southwest China

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with express operators, platform merchants, automation suppliers, and provincial transport officials across coastal, central, and western provinces. These discussions validated price bands, capacity utilization, and cross-border shares that were ambiguous in the public domain.

Desk Research

We began with authoritative public sources such as China State Post Bureau parcel data, General Administration of Customs cross-border trade tables, and Ministry of Transport freight cost indexes, which provided hard volume and lane metrics. Next, releases from the China Express Association, peer-reviewed papers in Transportation Research Part E, and press articles added unit-cost and technology adoption insights. Company filings, investor presentations, and paid feeds from D&B Hoovers and Dow Jones Factiva sharpened operator revenue splits and pricing curves. This list is illustrative; many other open and subscription materials guided data collection and verification.

Market-Sizing & Forecasting

According to Mordor Intelligence, a top-down build starts with 2024 parcel volume by speed tier, multiplies it by average revenue per parcel and warehousing value add, and then is cross-checked with selective bottom-up supplier roll-ups. Key model drivers include online GMV growth, parcels-per-order ratios, same-day penetration, cross-border shipment share, and average fulfillment cost per square meter. Multivariate regression, refreshed yearly, projects 2025-2030 values, while scenario analysis gauges macro shocks. Gaps in bottom-up inputs are bridged using price dispersion ranges collected during primary research.

Data Validation & Update Cycle

Outputs pass variance checks against independent metrics; any anomaly triggers re-contact with sources. This is where Mordor Intelligence differentiates, as analysts revisit currency, tariff, and cost assumptions before sign-off. Reports refresh annually, with interim updates when postal tariffs or major policy shifts occur.

Why Our China Ecommerce Logistics Baseline Commands Reliability

Published estimates often differ because firms choose distinct service mixes, fix exchange rates at different cut-off months, or ignore warehousing fees.

Key gap drivers include whether returns processing is counted, the aggressiveness of platform GMV forecasts, and refresh cadence variables Mordor revisits before every release.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 211.9 bn (2025) | Mordor Intelligence | - |

| USD 239.6 bn (2023) | Global Consultancy A | Excludes returns processing; holds 2023 FX rate constant |

| USD 450.0 bn (2024) | Industry Database B | Uses platform-reported parcel counts without adjusting duplicated legs |

| USD 62.5 bn (2025) | Trade Journal C | Counts only transportation revenue, omits warehousing and value-added fees |

The comparison shows that Mordor's disciplined scope, mixed top-down and bottom-up validation, and regularly refreshed driver set deliver a balanced baseline that decision-makers can track and replicate.

Key Questions Answered in the Report

What is the current size of the China ecommerce logistics market and how large will it become by 2031?

The market stands at USD 235.89 billion in 2026 and is forecast to climb to USD 402.89 billion by 2031, implying an 11.30% CAGR.

Which service segment is growing the fastest?

Value-added services—such as sustainable packaging, labeling, and kitting—are expanding at a 13.86% CAGR, outpacing the core transportation segment.

How quickly is the same-day delivery segment expanding?

Same-day delivery volume is projected to register a 16.02% CAGR through 2031 as urban shoppers increasingly pay premiums for immediacy.

Which geographic region offers the strongest growth outlook?

Southwest China is set to deliver the fastest regional expansion, with a 13.14% CAGR through 2031 on the back of New Western Land-Sea Corridor investments and rising consumer incomes.

What recent regulations are shaping industry strategy?

The revised Interim Regulations on Express Delivery that take effect in June 2025 mandate green packaging and tighter collaboration between carriers and ecommerce platforms, prompting new cost and innovation priorities.

Is the market concentrated or fragmented?

The sector scores 6 on a 1–10 concentration scale: the top five logistics providers control roughly half of total revenue, while numerous regional and specialist firms still compete for share.

Page last updated on: