Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

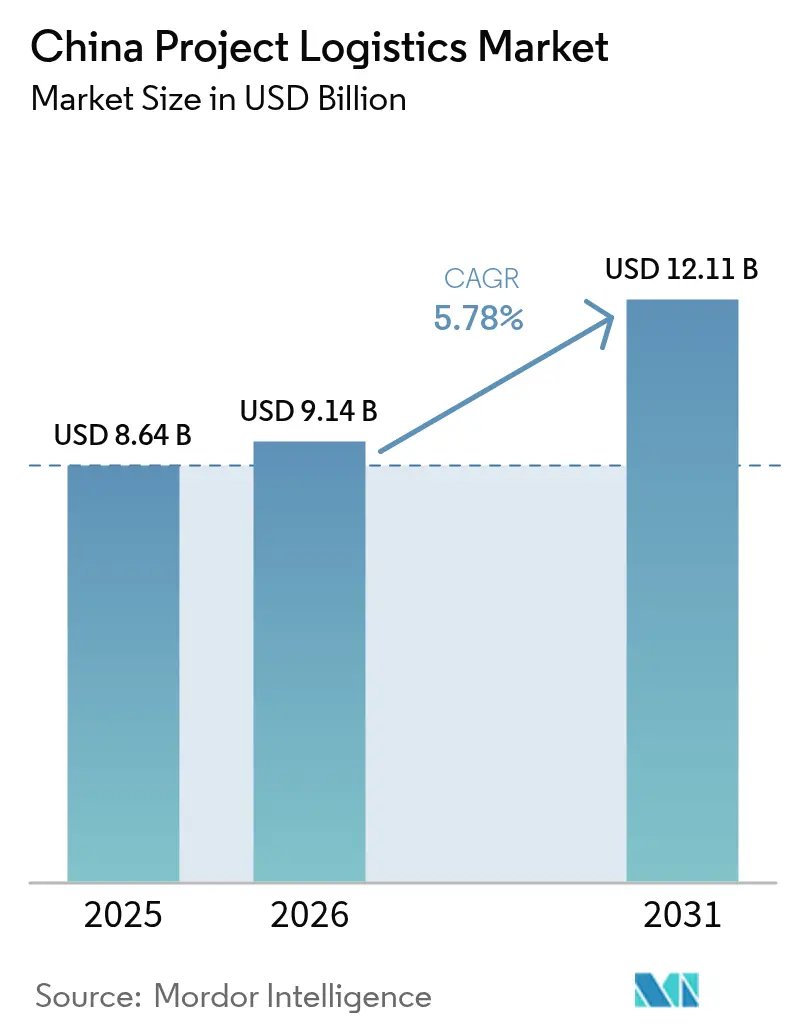

| Base Year Market Size (2025) | USD 8.64 Billion |

| Market Size (2026) | USD 9.14 Billion |

| Market Size (2031) | USD 12.11 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Project Logistics Market Analysis by Mordor Intelligence

The China Project Logistics Market size was valued at USD 8.64 billion in 2025 and estimated to grow from USD 9.14 billion in 2026 to reach USD 12.11 billion by 2031, at a CAGR of 5.78% during the forecast period (2026-2031).

The growth of the market reflects sustained infrastructure spending under the Belt & Road pipeline, aggressive renewable-energy roll-outs, and steady industrial modernization that together create multiple revenue streams and soften sector-specific slowdowns. Providers capture value by combining heavy-lift expertise with multimodal orchestration, enabling reliable movement of turbines, transformers, and prefabricated modules to remote sites. Integrated state-owned enterprises leverage their port assets and rail corridors to secure mega-project contracts, while global forwarders deepen local partnerships to tap demand from cross-border e-commerce fulfillment hubs. At the same time, green-freight regulations are hastening fleet upgrades to low-emission trucks and vessels, which raises near-term costs but promises longer-term operating efficiencies.

Key Report Takeaways

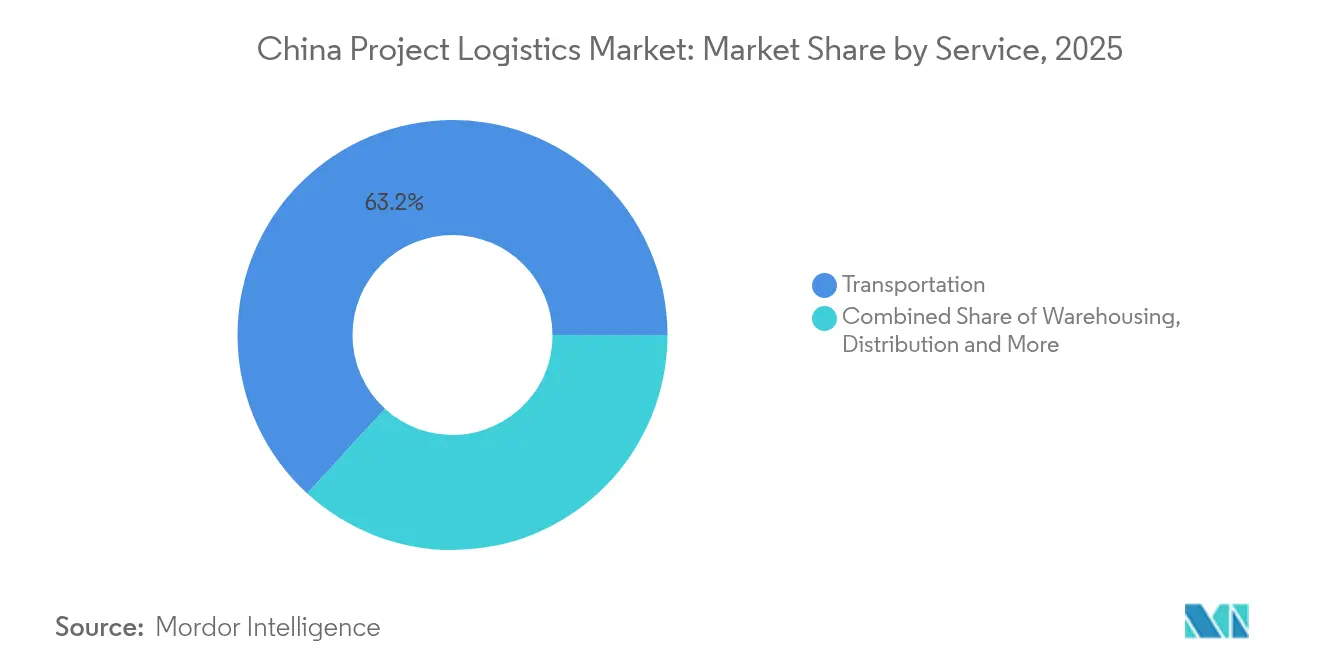

- By Service, Transportation services held a 63.20% China project logistics market share in 2025. Warehousing, Distribution & Inventory Management is projected to advance at a 4.47% CAGR through 2031.

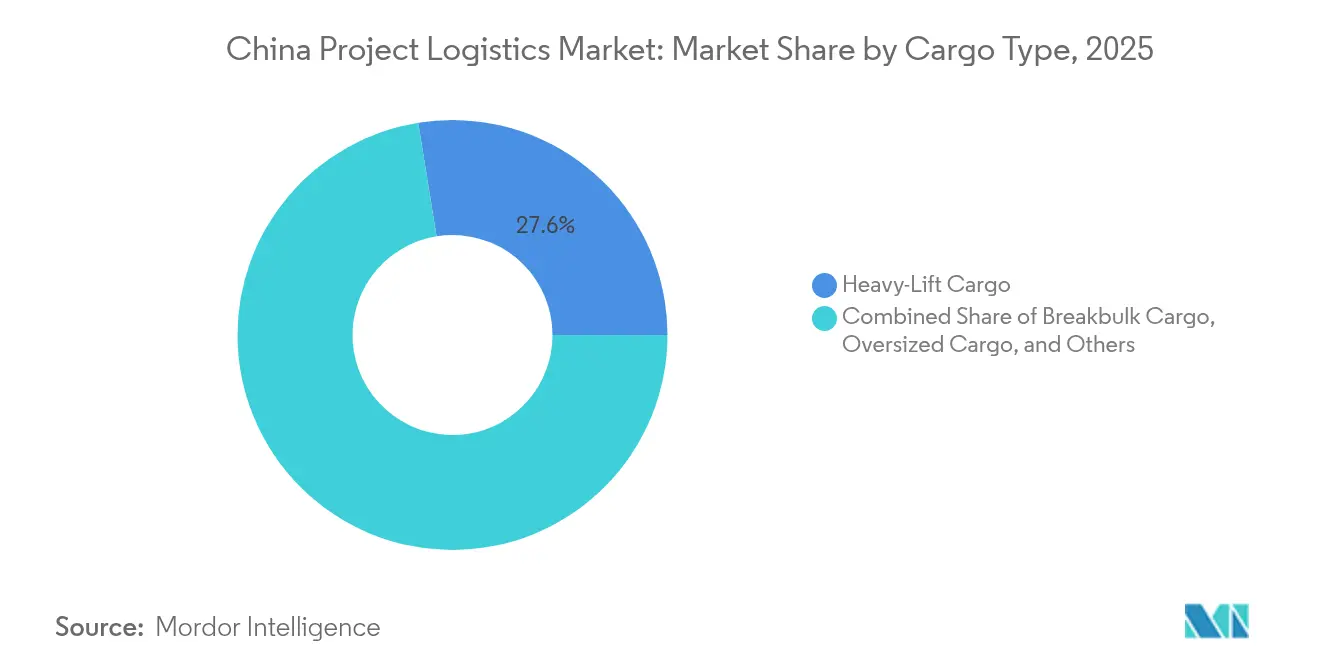

- By Cargo Type, Heavy-lift cargo accounted for 27.55% of the China project logistics market size in 2025. Oversized cargo is forecast to grow at a 4.98% CAGR to 2031.

- By End-User Industry, Energy Generation & Transmission captured 23.40% revenue share in 2025. Construction & Infrastructure is set to expand at a 5.32% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Project Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Belt & Road infrastructure pipeline | +1.0% | Central Asia, Southeast Asia, Western China | Long term (≥ 4 years) |

| Surge in domestic renewable-energy mega-projects | +0.8% | Coastal and inland provinces | Medium term (2-4 years) |

| Western China development and inland corridor build-out | +0.6% | Xinjiang, Tibet, Qinghai, Gansu | Long term (≥ 4 years) |

| Rapid scale-up of cross-border e-commerce fulfillment hubs | +0.4% | Shanghai, Shenzhen, Xinjiang | Short term (≤ 2 years) |

| Offshore and floating-wind boom along China’s coast | +0.3% | Jiangsu, Zhejiang, Guangdong, Fujian, Shandong | Medium term (2-4 years) |

| Rise of modular prefabricated high-rise construction logistics | +0.2% | Tier-1 and Tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Belt & Road Infrastructure Pipeline Accelerates Project Cargo Demand

Work on the 523-km China-Kyrgyzstan-Uzbekistan railway will require sustained volumes of heavy-lift equipment, specialized trailers, and synchronized multimodal transfers. Providers that can integrate rail, road, and air legs are positioned to command premium orchestration fees. The corridor also unlocks west-bound traffic that reduces exposure to coastal congestion. Demand continuity across planning, construction, and commissioning phases supports predictable earnings over several years[1]Belt and Road Portal, “Infrastructure Development Updates,” yidaiyilu.gov.cn.

Surge in Domestic Renewable-Energy Mega-Projects

Gigawatt-scale offshore wind farms now deploy 15-MW-plus turbines that weigh hundreds of tons, increasing the need for precision lifting vessels and engineered transport frames. Larger nacelles lower per-megawatt logistics cost, yet raise complexity and insurance requirements. Inland manufacturers must move blades and towers to coastal assembly yards, boosting long-haul road and rail volumes. Provincial subsidies for floating wind prototypes widen the addressable project pipeline and incentivize early investment in deep-water installation vessels[2]National Energy Administration, “Renewable Energy Development Statistics,” nea.gov.cn.

Western China Development and Inland Corridor Build-Out

Record freight throughput on the New International Land-Sea Trade Corridor validates western logistics routes that bypass crowded eastern ports. Xinjiang is expanding airport infrastructure to support out-of-gauge air charters, while Gansu is upgrading road links to connect remote mine sites. Providers able to stage specialized equipment in these regions gain a first-mover advantage and diversify away from coastal price competition.

Rapid Scale-Up of Cross-Border E-Commerce Fulfillment Hubs

China's cross-border e-commerce infrastructure reached unprecedented scale in 2024, with extensive overseas warehouse networks totaling significant storage capacity, while domestic cross-border e-commerce trade continued robust growth. This expansion creates demand for specialized project logistics services to establish and equip facilities with automated sorting systems, temperature-controlled storage, and customs processing equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and fuel cost inflation | -0.7% | Nationwide long-haul routes | Short term (≤ 2 years) |

| Shortage of project-logistics specialists | -0.5% | Western provinces, niche segments | Medium term (2-4 years) |

| Stricter green-freight road restrictions on oversize loads | -0.4% | Eastern provinces, urban corridors | Short term (≤ 2 years) |

| Congestion at secondary river and feeder ports | -0.3% | Yangtze and Pearl River Deltas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Fuel Cost Inflation

Fuel price volatility and capital cost inflation significantly impact project logistics margins, particularly for long-haul transportation and specialized equipment deployment. Global logistics companies have reported margin pressures from fuel cost increases, with road divisions experiencing profit declines despite revenue growth, demonstrating how fuel costs can rapidly erode profitability in asset-heavy logistics operations. Project logistics providers face additional capital cost pressures from specialized equipment purchases.

Shortage of Project-Logistics Specialists

Nationwide demand for rigging engineers and permit experts exceeds supply, with vacancy periods averaging six months. Western regions are hardest hit because qualified staff prefer coastal postings. Companies sponsor technical colleges and fast-track apprenticeships, yet upskilling cannot match project pace. Talent scarcity inflates wage bills and occasionally forces subcontracting to less-experienced teams, raising execution risk[3]China Association of Logistics & Purchasing, “Industry Analysis and Trends 2024,” cslp.org.cn.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Dominates Through Infrastructure Scale

Transportation captured 63.20% of China project logistics market share in 2025, reflecting the need for high-capacity trailers, rail wagons, and heavy-lift vessels to move turbines and tunnel-boring machines across 5,000-plus km corridors. The segment benefits from government investments in dedicated freight rail and expressways that shorten transit times and lower damage rates. Road remains essential for last-mile access to inland wind farms, while rail supports long-haul bulk moves to Central Asia. Sea transport handles oversize offshore wind parts and re-export cargo to ASEAN. Air remains niche but critical for emergent line-stop replacements.

Warehousing, Distribution & Inventory Management is the fastest-growing service, set to post a 4.47% CAGR (2026-2031), lifted by cross-border e-commerce facilities that require climate-controlled storage and automated retrieval systems. This rise aligns with just-in-time manufacturing goals that shift buffer inventory off-site to specialized hubs. Integrated providers bundle cargo insurance, trade compliance, and project management as value-added services, capturing higher margins and deepening client stickiness. The China project logistics industry also invests in RFID-enabled yard management to reduce dwell time and improve throughput visibility.

By Cargo Type: Heavy-Lift Expertise Drives Premium Pricing

Heavy-lift cargo comprised 27.55% of the China project logistics market size in 2025, anchored by transformer, reactor, and turbine moves for grid and refinery projects. Success demands engineered skids, modular hydraulic trailers, and synchronized bridge beam placements. Dual domestic and export flows reinforce volume stability. Oversized cargo is expanding at a 4.98% CAGR (2026-2031), powered by offshore wind blades exceeding 110 meters and high-rise modules that cannot be disassembled. Providers deploy 3-D route surveys and augmented-reality rigging plans to assure clearance under power lines and urban flyovers.

Breakbulk remains relevant for steel structures and machinery crates, though shippers increasingly seek pallet-wide unit loads that speed port handling. Niche cargo such as high-value electronics and temperature-controlled chemicals falls under Others, drawing specialized packaging and monitoring solutions. Tightening green-freight rules reinforces investment in low-emission tractors and reusable dunnage to minimize environmental footprints.

By End-User Industry: Energy Sector Leads Demand Transformation

Energy Generation & Transmission generated 23.40% of 2025 revenue, underpinned by carbon-neutrality mandates that accelerate wind-farm roll-outs and grid upgrades. Turbine nacelles, switchgear, and cable reels create steady high-value traffic. Construction & Infrastructure is the fastest-growing end-user at 5.32% CAGR (2026-2031), spurred by smart-city retrofits and mass transit expansions. Modular construction lifts demand for just-in-sequence delivery of façade panels, stair cores, and MEP units.

Oil & Gas, Mining & Quarrying maintains moderate flows, chiefly from maintenance-related rig moves and strategic natural-gas projects. Manufacturing & Industrial Plants sustain demand for turnkey line installations as firms automate production. Aerospace & Defense logistics remains a niche but commands premium pricing due to security and precision requirements. Emerging categories such as data center construction need specialized cooling equipment transport, adding future growth avenues.

Geography Analysis

Eastern coastal provinces hold the lion’s share of project cargo flows, thanks to mature ports, high-tech manufacturing clusters, and proximity to export customers. The Yangtze River Delta supports complex multimodal operations that connect containerized inputs at Shanghai with inland barge legs to Nanjing. The Pearl River Delta specializes in high-tech component moves bound for the ASEAN market, although feeder-port congestion occasionally forces schedule buffers.

Western China records the fastest expansion as Belt & Road corridors unlock Xinjiang, Gansu, and Tibet. The New International Land-Sea Trade Corridor trimmed the average Chongqing-to-Singapore transit to 13 days, winning cargo away from coastal gateways. Record freight at Urumqi and Alashankou has prompted investment in bonded logistics zones and heavy-lift crane yards. Providers that pre-position equipment and recruit local riggers can outrun competitors reliant on long repositioning hauls.

Competitive Landscape

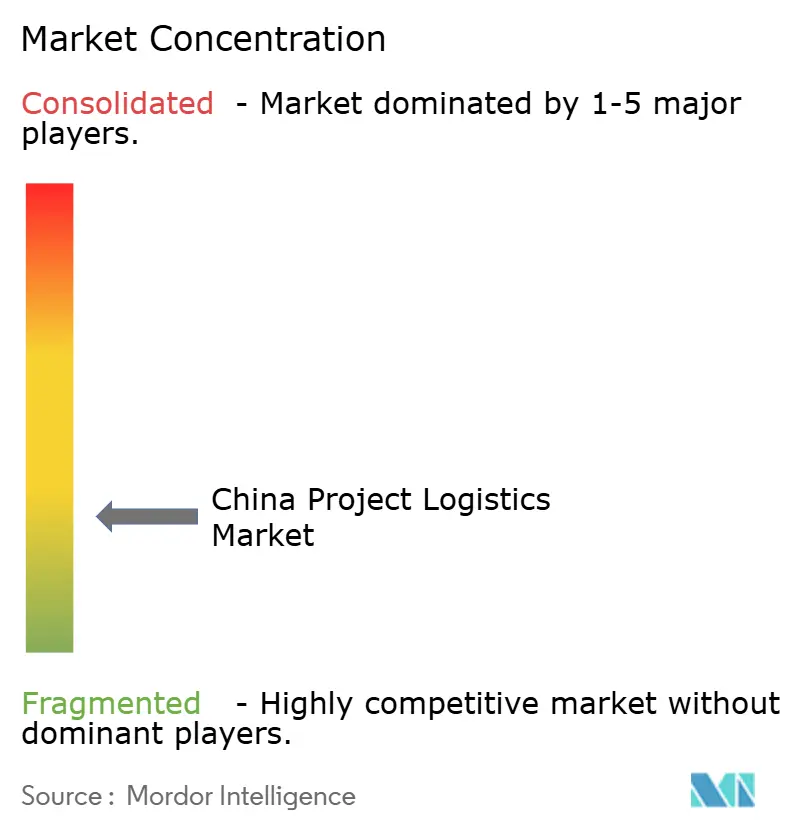

The China project logistics market features moderate fragmentation because capital intensity discourages frequent new entrants, yet diverse project needs prevent dominance by a few firms. State-owned COSCO Shipping Logistics and Sinotrans wield integrated port and rail assets along with preferential access to public-works tenders. International majors such as DSV and Kuehne + Nagel leverage global networks and digital platforms to win multinational EPC clients. Mid-tier specialists focus on west-bound routes or wind-turbine components, carving profitable niches.

Strategic themes center on digitalization and automation. Leading players deploy AI-driven route optimization that cuts empty mileage by up to 8%. Predictive maintenance on heavy-lift cranes limits unplanned downtime and secures project milestones. Blockchain pilot projects trace the chain-of-custody for high-value cargo, reducing insurance premiums. Industry consolidation accelerated in 2025 when DSV acquired DB Schenker, creating the world’s largest freight forwarder and reshaping tender dynamics.

White-space opportunities persist in inland corridor development, offshore wind logistics, and e-commerce fulfillment automation. Market entrants with low-carbon fleets gain advantage as green-freight rules tighten. Equipment manufacturers integrate transport services into turnkey offerings, introducing vertical competition that pressures pure-play forwarders. Overall, customer bargaining power remains balanced because specialized equipment and regulatory know-how limit easy switching among providers.

China Project Logistics Industry Leaders

COSCO Shipping Logistics Co., Ltd.

Sinotrans Ltd.

Kerry Logistics Network Ltd.

CJ Smart Cargo

InterMax Logistics Solution Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Kuehne + Nagel and MTU Maintenance Lease Services open an aero-engine parts hub in Zhuhai.

- July 2025: CEVA Logistics opens a 4,300 m² TIR center in Alashankou, including 1,000 m² for dangerous goods handling.

- June 2025: COSCO Shipping inaugurates its North China regional headquarters in Tianjin with an International Shipping Technology Center.

- April 2025: DSV completes its EUR 14.3 billion (USD 14.9 billion) acquisition of DB Schenker, creating the world’s largest freight forwarder.

China Project Logistics Market Report Scope

The project logistics market centers on managing and coordinating intricate logistics operations, particularly for transporting oversized and heavy equipment. Market size is determined by the revenue generated by logistics service providers through services like transportation, forwarding, warehousing, and other value-added offerings. The research includes a thorough background analysis of the China project logistics industry, a market overview, market size estimates for important segments, emerging trends by segments, and market dynamics.

The Project Logistics Market is segmented by service (transportation, forwarding, warehousing, and other value-added services) and by end users (oil and gas, petrochemical, mining and quarrying, energy and power, construction, manufacturing, and other end-users). The report offers market size and forecasts in value (USD) for all the above segments.

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing, Distribution & Inventory Management | |

| Value-added Services and Others |

By Cargo Type

| Oversized (Out-of-Gauge) Cargo |

| Heavy-Lift Cargo |

| Breakbulk Cargo |

| Others |

By End-User Industry

| Oil & Gas, Mining & Quarrying |

| Energy Generation & Transmission (Includes Renewable Energy) |

| Construction & Infrastructure |

| Manufacturing & Industrial Plants |

| Aerospace & Defense |

| Others (Maritime & Shipbuilding, Telecommunications, etc.) |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing, Distribution & Inventory Management | ||

| Value-added Services and Others | ||

| By Cargo Type | Oversized (Out-of-Gauge) Cargo | |

| Heavy-Lift Cargo | ||

| Breakbulk Cargo | ||

| Others | ||

| By End-User Industry | Oil & Gas, Mining & Quarrying | |

| Energy Generation & Transmission (Includes Renewable Energy) | ||

| Construction & Infrastructure | ||

| Manufacturing & Industrial Plants | ||

| Aerospace & Defense | ||

| Others (Maritime & Shipbuilding, Telecommunications, etc.) |

Key Questions Answered in the Report

How large is the China project logistics market in 2026?

It is valued at USD 9.14 billion, with a forecast to reach USD 12.11 billion by 2031.

What is the expected growth rate through 2031?

The market is projected to expand at a 5.78% CAGR during 2026-2031.

Which service segment holds the largest share?

Transportation services command 63.20% of 2025 revenue due to the capital-intensive nature of heavy-haul moves.

Which cargo type is growing fastest?

Oversized cargo is forecast to register a 4.98% CAGR, propelled by offshore wind and modular construction volumes.

Which end-user sector drives the most demand?

Energy Generation & Transmission leads with a 23.40% revenue share, while Construction & Infrastructure is the fastest-growing at 5.32% CAGR.

Which region offers the highest growth potential?

Western China corridors linked to Belt & Road projects are expanding the quickest as new rail and road links open.

Page last updated on: