Nasal Drug Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

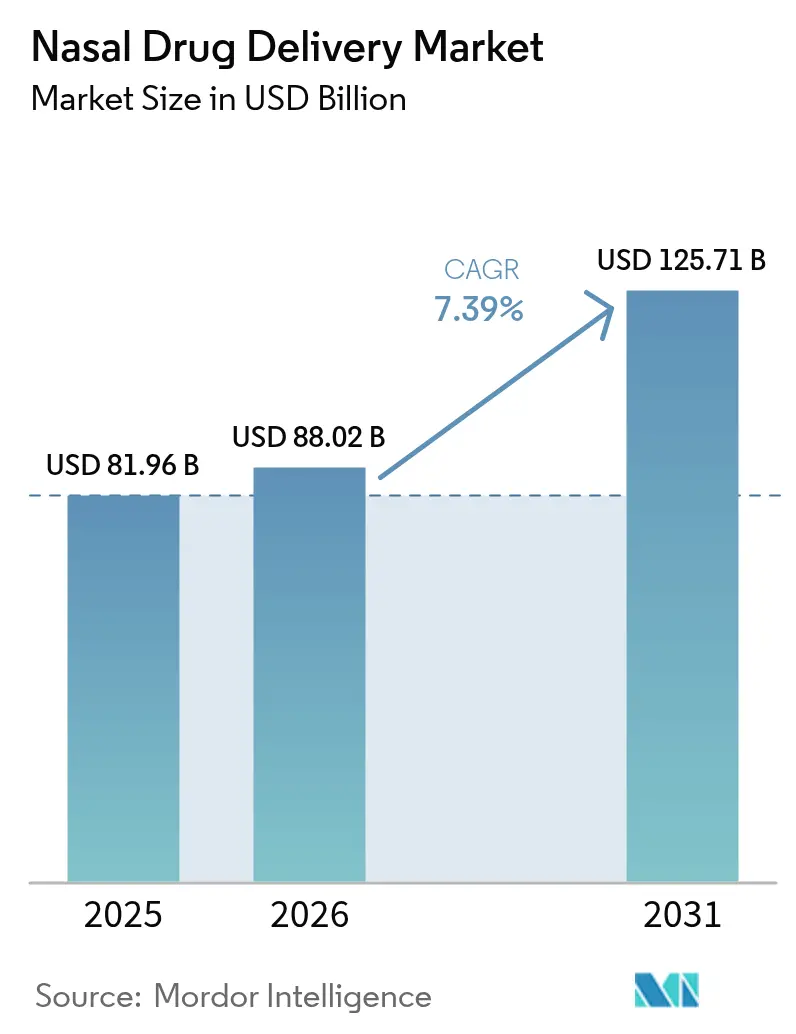

| Market Size (2026) | USD 88.02 Billion |

| Market Size (2031) | USD 125.71 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nasal Drug Delivery Market Analysis by Mordor Intelligence

The nasal drug delivery market size is expected to grow from USD 81.96 billion in 2025 to USD 88.02 billion in 2026 and is forecast to reach USD 125.71 billion by 2031 at 7.39% CAGR over 2026-2031. This solid growth reflects regulatory approvals that have shifted intranasal administration from niche use to a mainstream option for both small- and large-molecule therapeutics. Needle-free epinephrine, at-home influenza vaccination, and the first intranasal antidepressant in China illustrate the powerful pull of patient-centric innovation. Companies are matching the regulatory momentum with new device-drug combinations, especially where self-administration reduces the burden on overcrowded care settings. Dry-powder technologies, pressurized delivery systems, and smart-device integration together deepen the competitive moat for firms that can balance formulation science with engineering rigor. Across every region, the nasal drug delivery market benefits from patients seeking faster onset, less invasive routes, and freedom from cold-chain constraints.

Key Report Takeaways

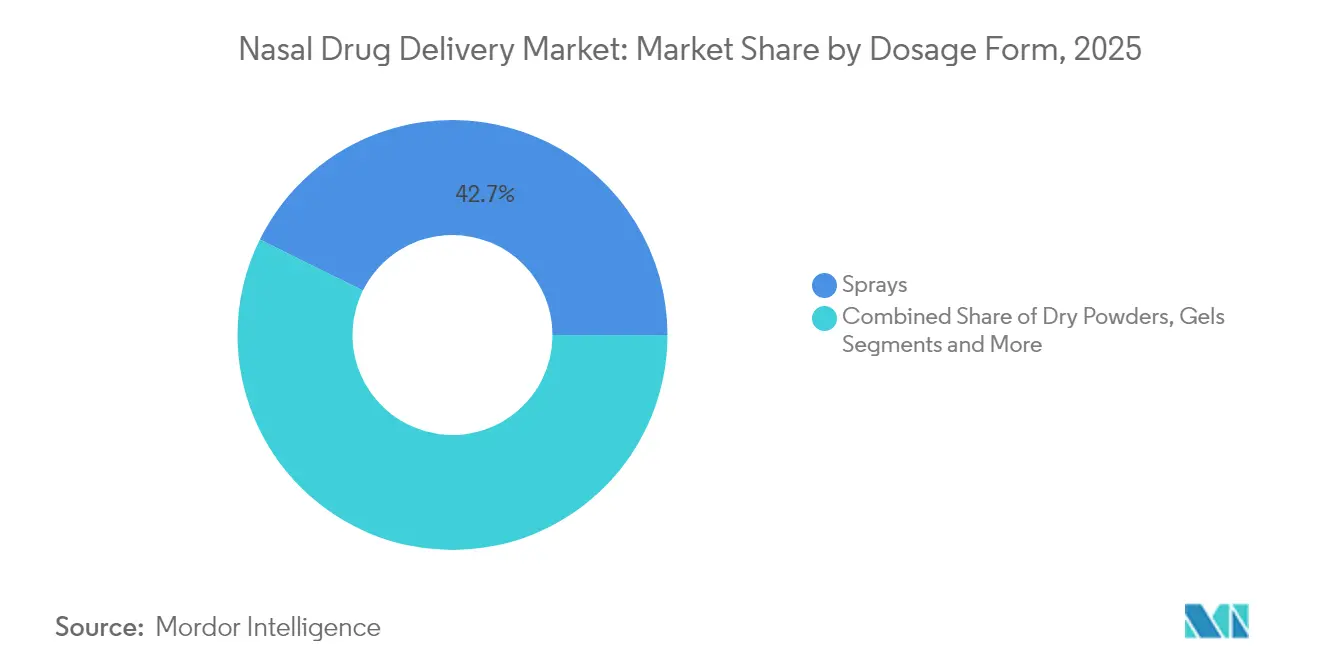

- By dosage form, sprays held 42.68% of the nasal drug delivery market share in 2025, while dry powders are projected to post a 10.24% CAGR through 2031.

- By container type, non-pressurized systems captured 61.63% revenue in 2025; pressurized containers are forecast to rise at a 9.55% CAGR to 2031.

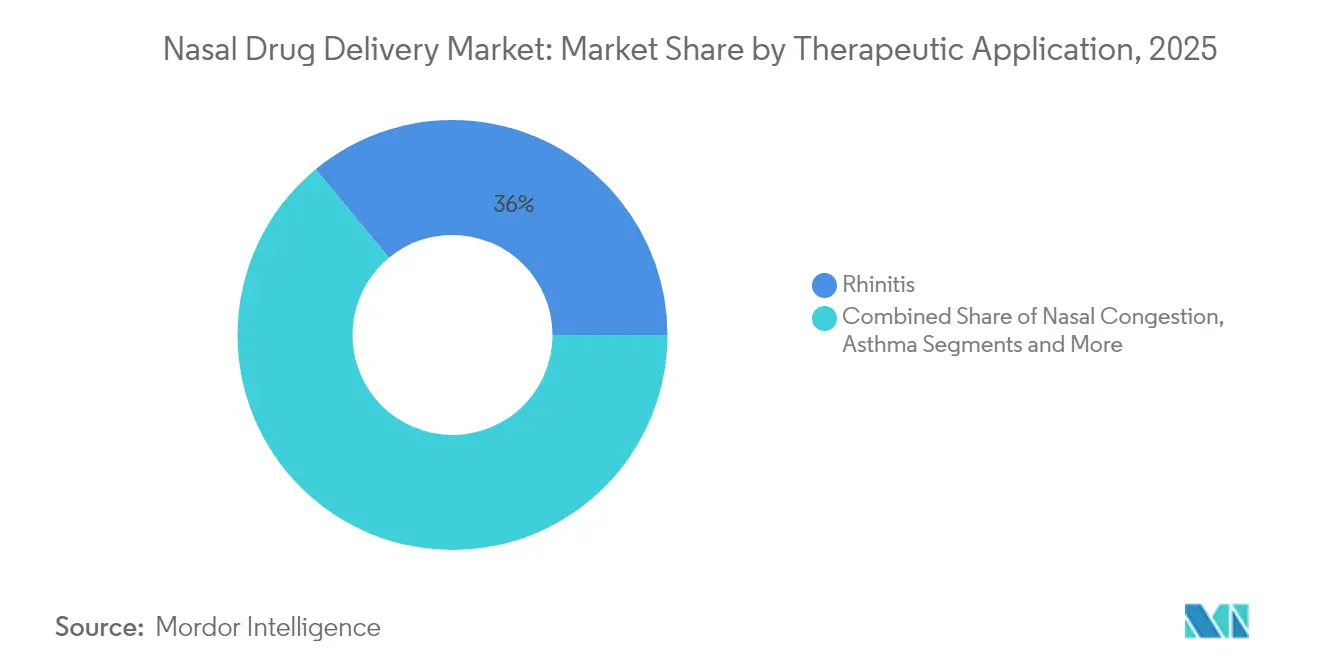

- By therapeutic application, rhinitis treatments commanded 35.98% of the nasal drug delivery market size in 2025, whereas pain management is set to expand at a 9.62% CAGR between 2026 and 2031.

- By end user, hospitals accounted for 46.89% of the nasal drug delivery market in 2025, while home healthcare is advancing at an 10.98% CAGR through 2031.

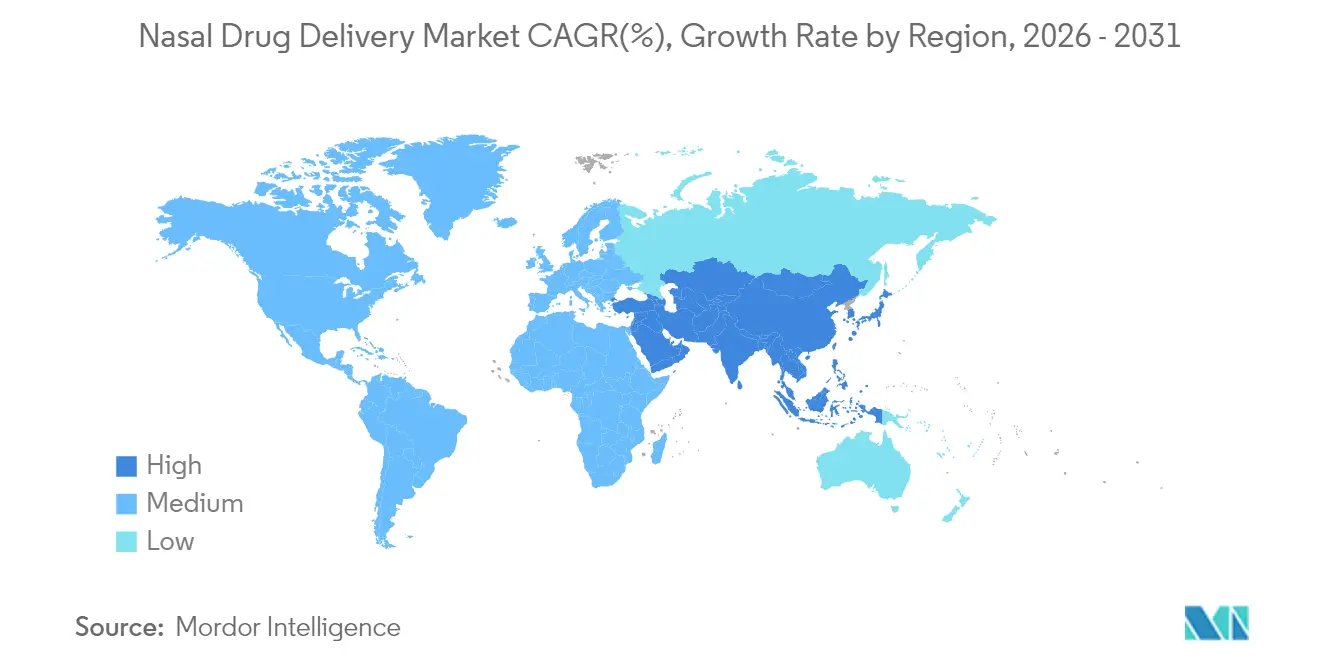

- By geography, North America led with 38.15% of nasal drug delivery market share in 2025; Asia Pacific is the fastest-growing region at a 9.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nasal Drug Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of allergic rhinitis & chronic sinusitis | +1.2% | Global, North America & Europe | Long term (≥ 4 years) |

| Growing adoption of self-administration practices | +1.8% | North America & Europe; Asia Pacific strengthening | Medium term (2-4 years) |

| Rising patient preference for needle-free routes | +1.5% | Global, strong in pediatric groups | Medium term (2-4 years) |

| Regulatory approvals of large-molecule biologics via intranasal route | +0.9% | North America & Europe leadership | Short term (≤ 2 years) |

| Pandemic-driven cold-chain cost-saving push | +0.7% | Global, emerging markets highlighted | Medium term (2-4 years) |

| Sensor-enabled smart nasal devices for adherence tracking | +0.4% | North America & Europe early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Allergic Rhinitis & Chronic Sinusitis

The rising burden of allergic rhinitis and chronic sinusitis sustains steady demand for intranasal therapies. The FDA cleared fluticasone propionate (XHANCE) for chronic rhinosinusitis without nasal polyps in March 2024, validating exhalation-delivery technology that targets inflamed nasal tissue. Phase 3 data show marked symptom relief and fewer exacerbations, broadening the addressable respiratory market. Pipeline programs extend to biologics such as stapokibart, an IL-4 receptor monoclonal antibody that improved nasal and ocular scores in late-stage trials, pointing to a new class of targeted intranasal immunotherapies.

Growing Adoption of Self-Administration Practices

Regulators now back patient-handled delivery. In September 2024 the FDA authorized FluMist for at-home use, the first vaccine approved for self-administration. Usability studies confirmed safe delivery across age brackets, removing both needle anxiety and clinic scheduling bottlenecks. Similar design principles guided neffy, which enables emergency epinephrine without medical supervision, a meaningful advance for people who avoid injectors. Education programs from hospital pharmacists reinforce correct technique, tightening the feedback loop between device innovation and real-world adherence.

Rising Patient Preference for Needle-Free Routes

Needle phobia affects up to one-quarter of patients who need epinephrine. Neffy directly tackles this barrier with a 30-month shelf-stable spray that resolved pediatric reactions in 16 minutes on median.[1]Anne K. Ellis, “Development of neffy, an Epinephrine Nasal Spray, for Severe Allergic Reactions,” Pharmaceutics, mdpi.com Companies see strategic value: ARS Pharmaceuticals has active filings in China, Japan, and Australia, aiming to leverage the global prevalence of injection avoidance. Beyond anaphylaxis, mucosal vaccines deliver broader immune coverage at the local infection site, illustrating how needle-free design can expand both market and clinical impact.

Regulatory Approvals of Large-Molecule Biologics Via Intranasal Route (2025+)

FDA draft guidance now details performance standards for nasal combination products, giving sponsors a clear path for complex biologics. Thin-film freeze-drying converts antibodies into stable powders that maintain activity when sprayed intranasally.[2]J.G. Barnard, “Intranasal Delivery of Thin-Film Freeze-Dried Monoclonal Antibodies Using a Powder Nasal Spray System,” ScienceDirect, sciencedirect.com Novel PLGA nanoparticles delivered trastuzumab nose-to-brain with nine-fold improved transport, underscoring intranasal feasibility for oncology and neurology.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Overuse complications causing rhinitis medicamentosa | -0.8% | Global, OTC markets | Medium term (2-4 years) |

| Patent cliff for leading allergic-rhinitis brands (2025-27) | -1.1% | North America & Europe | Short term (≤ 2 years) |

| Cold-chain integrity risk for temperature-sensitive biologics | -0.6% | Global, emerging markets | Long term (≥ 4 years) |

| Stringent regulations | -0.4% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Overuse Complications Causing Rhinitis Medicamentosa

Prolonged vasoconstrictor use can trigger rebound congestion. Surveys show 75% of Canadian otolaryngologists think current warning labels are insufficient, and nearly 30% of patients cannot stop over-the-counter sprays despite counseling. Severe cases call for surgical turbinate reduction, adding complexity and cost.

Patent Cliff For Leading Allergic-Rhinitis Brands (2025-27)

Key formulations such as oxymetazoline and fluticasone face impending exclusivity loss. Historical trends suggest 80-90% price erosion within 18 months post-expiry, compressing branded revenue and unsettling forecast baselines. Originator firms respond with combination products and device upgrades aimed at fresh patent life.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Dry Powders Drive Innovation

Sprays owned 42.68% of the nasal drug delivery market in 2025, reflecting decades of clinical familiarity. Dry powders, however, are projected to grow 10.24% annually as firms harness freeze-drying and spray-drying methods to stabilize antibodies and peptides. Thin-film freeze-dried monoclonal antibodies achieve effective aerosol performance without refrigeration. Breath-actuated insufflators, combined with mucoadhesive excipients, further lift residence time. Drops retain a role in pediatrics, while gels cater to chronic cases needing sustained mucosal contact. Each modality meets distinct clinical needs, yet powders capture the highest forward momentum by marrying stability with patient convenience.

The nasal drug delivery market size for dry powders is set to expand at the fastest clip, whereas sprays continue to anchor baseline revenue. Product design now centers on Quality by Design frameworks that link particle morphology to consistent dosing. Nanocarrier-loaded powders push the therapeutic frontier into vaccines, gene therapy, and brain-targeted oncology. This balanced portfolio lets manufacturers hedge mature volume against high-growth innovation streams.

By Container Type: Pressurized Systems Gain Momentum

Non-pressurized formats delivered 61.63% of 2025 sales due to low cost and simple design. Pressurized systems are on a 9.55% CAGR trajectory because biologics often need exact, repeatable doses. Aptar’s acquisition of SipNose technology signals confidence in soft-mist platforms that protect fragile proteins. Bespak’s customizable valves add another layer of precision. At the same time, unit-dose devices such as NasaDose improve sterility, making them attractive for emergency neurologic sprays.

As the nasal drug delivery market evolves, container choice increasingly follows molecule complexity. Large antibodies favor pressurized devices that guarantee plume geometry and minimal shear stress. Small molecules and decongestants stay in pump sprays for price sensitivity. The push-pull dynamic means suppliers must maintain dual manufacturing lines while upgrading quality control to meet combination-product regulations.

By Therapeutic Application: Pain Management Accelerates

Rhinitis therapies held a 35.98% share in 2025 thanks to high global prevalence. Pain management will outpace all others at 9.62% CAGR through 2031. Intranasal tapentadol reached faster pain reduction than intravenous tramadol in head-to-head trials, confirming the route’s value in post-operative care.Cardiovascular uses follow closely: intranasal etripamil offers rapid relief from supraventricular tachycardia without hospital IV access.

Vaccines represent a strategic frontier. FluMist’s self-administration approval built confidence for nasally delivered COVID-19 and dual RNA vaccines entering US phase 1. In palliative settings, one-third of hospice patients may benefit from nasal morphine sprays when oral or subcutaneous paths fail. This versatility keeps the nasal drug delivery market diversified against single-segment shocks.

By End User: Home Healthcare Transformation

Hospitals controlled 46.89% of 2025 demand, yet home healthcare is advancing 10.98% per year. FDA’s nod to at-home FluMist flipped the paradigm by proving that even live attenuated vaccines can be self-administered safely. Remote coaching apps and pharmacist-led tutorials ensure correct technique, directly addressing the misuse that historically undermined outcomes.

The nasal drug delivery market size for home healthcare will keep expanding as digital monitoring couples with user-friendly devices. Emergency products like neffy show parents can deliver lifesaving therapy without delay. Ambulatory surgery centers prefer nasal analgesics to speed discharge, and specialty clinics adopt intranasal biologics for targeted CNS delivery. Together, these settings dilute the hospital’s historic dominance.

Geography Analysis

North America retained 38.15% market share in 2025 on the back of a mature regulatory framework, early adopter payers, and high allergic-rhinitis prevalence. The region also acts as the first launch pad for large-molecule nasal biologics, reflecting strong FDA engagement. Europe follows with robust reimbursement structures, yet growth is more measured as generics temper price points. Stringent device guidelines, though, preserve premium space for engineered combination products.

Asia Pacific is the standout growth engine at a 9.87% CAGR. China’s June 2024 approval of esketamine nasal spray for depression validated the route for central-nervous-system biologics and unlocked a sizeable untreated segment. Japan positions itself as a fast follower: Aculys Pharma’s diazepam filing in 2024 signals future intranasal seizure-rescue launches. Australia mirrors these trends by fast-tracking needle-free epinephrine.

Middle East and Africa benefit from ongoing cold-chain upgrades that allow sensitive biologics to reach major urban centers. In South America, high respiratory-disease incidence and crowded outpatient clinics strengthen the appeal of self-administered sprays. As supply chains mature, the nasal drug delivery market will continue to widen its geographic footprint through localized manufacturing and regulatory harmonization.

Competitive Landscape

The landscape is moderately fragmented. Global pharmaceutical firms such as AstraZeneca, Janssen, and ARS Pharmaceuticals lean on device specialists like Aptar and Bespak to lock in differentiated delivery platforms. Aptar spent part of its USD 3.5 billion revenue on SipNose’s assets in October 2024, bolstering its pressurized portfolio. Such vertical integration raises barriers for single-capability entrants.

Generics loom large as patents lapse between 2025 and 2027, pressuring incumbents to innovate in combination sprays and smart-device tie-ins that are harder to copy. Meanwhile, AI-enabled adherence tools appear as a new battleground: firms that can integrate sensor feedback into therapeutic ecosystems may pull ahead on value-based-care contracts.

Third-tier innovators concentrate on nano-structured powders and CNS-targeted antibodies, often licensing device platforms to fast-track to clinic. Venture funding gravitates to programs that bridge formulation science, user-centered design, and regulatory clarity. As a result, the nasal drug delivery market remains contestable yet rewards cross-disciplinary execution.

Nasal Drug Delivery Industry Leaders

GlaxoSmithKline PLC

AstraZeneca PLC

Johnson & Johnson

Novartis AG

Pfizer Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Neurelis received FDA approval for VALTOCO diazepam nasal spray to treat seizure clusters, using INTRAVAIL absorption technology.

- March 2025: FDA cleared neffy 1 mg epinephrine nasal spray for children 4 years and older, marking the first innovation in pediatric epinephrine delivery in more than three decades.

- December 2024: ARS Pharmaceuticals filed for neffy approval in China, Japan, and Australia through regional partners.

- October 2024: Aptar Pharma acquired SipNose’s nasal delivery technology assets to strengthen its advanced intranasal platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the nasal drug delivery market as the worldwide value generated when finished pharmaceutical formulations are dispensed through the nasal cavity for local or systemic action, including sprays, drops, gels, powders, and related combination devices. According to Mordor Intelligence, this route's appeal stems from rapid absorption, improved bioavailability, and patient-friendly self-administration.

Explicit scope exclusion: We've excluded revenues from over-the-counter nasal dilators and purely diagnostic swabs, as these do not involve drug administration.

Segmentation Overview

- By Dosage Form

- Sprays

- Drops & Liquids

- Gels

- Dry Powders

- Others

- By Container Type

- Non-Pressurized Containers

- Pressurized Containers

- By Therapeutic Application

- Rhinitis

- Nasal Congestion

- Asthma

- Pain Management

- Vaccination

- Others

- By End User

- Hospitals

- Home Health Care

- Ambulatory Surgery Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interact with formulation chemists, device engineers, hospital pharmacists, and procurement heads across North America, Europe, and key Asian markets. These conversations test secondary assumptions around average selling prices (ASPs), in-hospital versus home-care preference shifts, and likely adoption timelines for single-use powder blisters.

Desk Research

We begin by mapping the regulatory, clinical, and trade landscape through freely available tier-1 sources such as the US FDA Orange Book, European Medicines Agency product lists, WHO ATC/DDD database, and United Nations Comtrade shipment filings. Industry associations like the Consumer Healthcare Products Association and the International Pharmaceutical Aerosol Consortium provide dosage-form adoption data, while academic articles in journals such as Drug Delivery and Translational Research clarify permeation kinetics. Mordor analysts then mine paid databases, D&B Hoovers for company revenue splits, Dow Jones Factiva for deal flow, and Questel for patent clusters to cross-check pipeline momentum and manufacturer concentration. The sources named here are illustrative; many other public and subscription inputs inform each step of desk validation.

Market-Sizing & Forecasting

A top-down construct starts with prescription and OTC volume estimates drawn from production and trade data, which are then multiplied by region-specific ASPs to yield baseline value. Results are corroborated through selective bottom-up checks, supplier roll-ups and channel interviews, to fine-tune totals. Key model inputs include chronic rhinitis prevalence, intranasal migraine therapy approvals, device unit-to-drug cartridge ratios, regional reimbursement ceilings, and e-pharmacy share of respiratory products. Multivariate regression guided by these variables and consensus from primary experts underpins the 2025-2030 forecast. Where bottom-up detail is patchy, variance bands flag uncertainty and prompt targeted follow-ups.

Data Validation & Update Cycle

Outputs pass multi-layered checks, anomaly flags, and senior reviews before sign-off. Reports refresh each year, and material events, such as a nasal vaccine approval, trigger interim recalculations so clients always receive the latest view.

Why Mordor's Nasal Drug Delivery Baseline Earns Decision-Maker Trust

Published estimates often diverge; scope breadth, base-year choice, and revenue attribution practices create visible gaps.

Key gap drivers here include whether device sales are bundled with drug revenues, the handling of compounded hospital preparations, refresh cadence, and currency conversion logic. Mordor's disciplined segmentation, yearly refresh, and explicit exclusion of non-drug nasal products keep our 2025 figure tightly aligned to the value chain that investors actually monetize.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 81.96 Billion (2025) | Mordor Intelligence | - |

| USD 69.93 Billion (2024) | Global Consultancy A | Narrow scope centers on branded sprays, omits hospital-compounded gels |

| USD 88.85 Billion (2025) | Research Publisher B | Bundles delivery-device hardware revenue with drug sales |

| USD 76.89 Billion (2023) | Industry Journal C | Older base year and inflation uplift, lacks recent OTC volume recalibration |

Taken together, the comparison shows that our balanced, transparent baseline is anchored in clearly defined variables, annually refreshed inputs, and repeatable steps that clients can readily trace back to source.

Key Questions Answered in the Report

What is the current value of the nasal drug delivery market?

The market stands at USD 88.02 billion in 2026 and is projected to grow to USD 125.71 billion by 2031.

Which region is expanding the fastest?

Asia Pacific is expected to register a 9.87% CAGR, the highest among all regions.

Why are dry-powder nasal formulations gaining traction?

They offer improved stability for biologics, longer shelf life without refrigeration, and a projected 10.24% CAGR through 2031.

How did the FDA’s approval of FluMist for self-administration impact the market?

It validated at-home vaccination, accelerated growth in the home-healthcare segment, and underscored patient demand for needle-free options.

What is driving the rise of pressurized nasal delivery systems?

Large-molecule therapeutics need precise, repeatable dosing, pushing pressurized containers to a 9.55% CAGR.

Page last updated on: