China Diabetes Care Drugs And Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

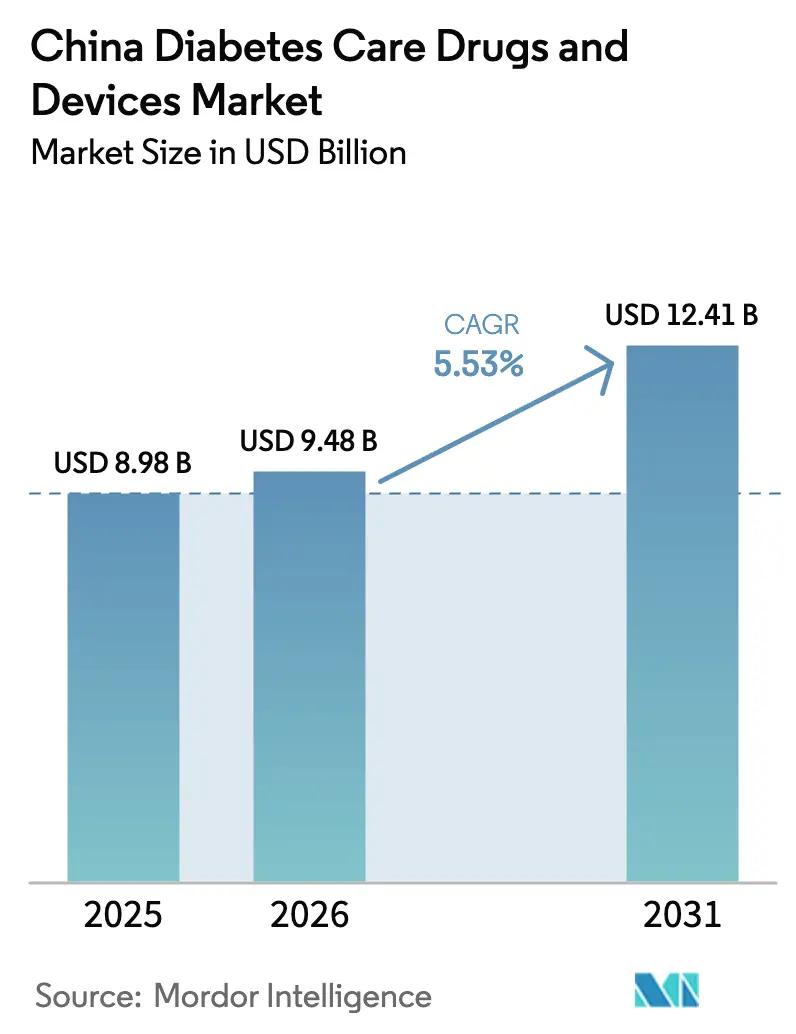

| Base Year Market Size (2025) | USD 8.98 Billion |

| Market Size (2026) | USD 9.48 Billion |

| Market Size (2031) | USD 12.41 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Diabetes Care Drugs And Devices Market Analysis by Mordor Intelligence

China diabetes care drugs and devices market size in 2026 is estimated at USD 9.48 billion, growing from 2025 value of USD 8.98 billion with 2031 projections showing USD 12.41 billion, growing at 5.53% CAGR over 2026-2031. Sustained growth reflects three structural forces: a diabetes population of 140-233 million people, a strong policy push for digital chronic-disease management, and rapid device innovation that augments traditional pharmacotherapy. National Volume-Based Procurement (NVBP) has lowered median insulin prices by 42.08%, unlocking USD 2.85 billion in cumulative savings and expanding access while compelling manufacturers to pursue cost-efficient, differentiated pipelines. Regulatory momentum is equally visible, with 228 novel diabetes filings cleared by the National Medical Products Administration in 2024, including the first ultra-long-acting oral hypoglycemic agent cofrogliptin. Geographic imbalances persist: tier-1 cities capture the earliest uptake of cutting-edge therapies, whereas pharmacy build-outs in tier-2/3 cities underpin the next demand wave.

Key Report Takeaways

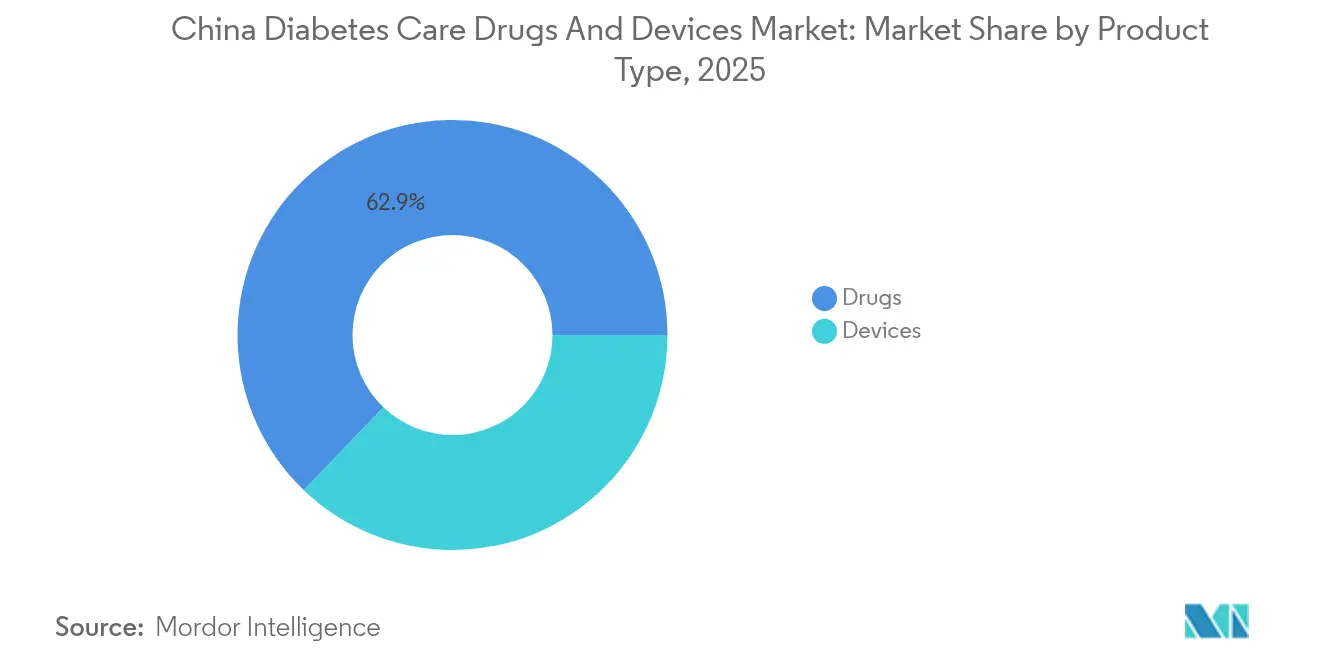

- By product type, drugs led with 62.85% revenue share in 2025; devices are set to grow the fastest at a 6.28% CAGR through 2031.

- By diabetes type, type 2 accounted for 90.55% of the China diabetes care drugs and devices market share in 2025, while type 1 is projected to advance at a 6.31% CAGR to 2031.

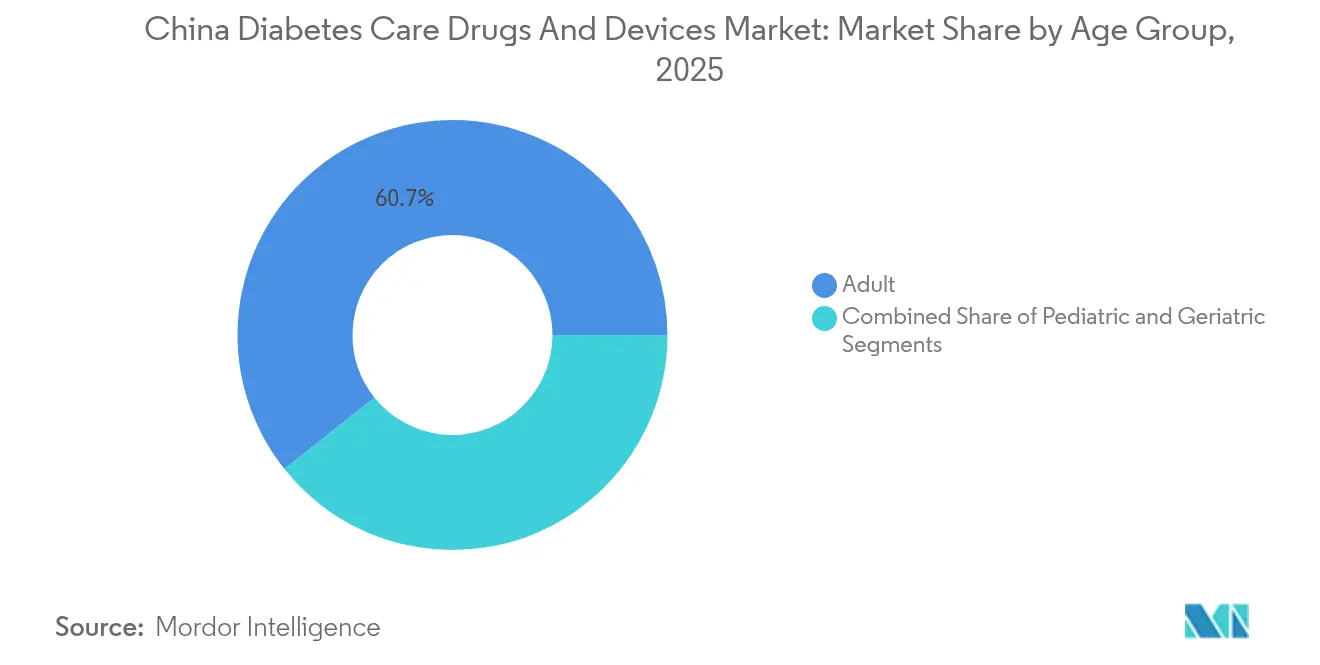

- By age group, adults held 60.72% of the China diabetes care drugs and devices market size in 2025; the geriatric segment shows the highest expansion pace at 6.18% CAGR until 2031.

- By distribution channel, offline outlets retained 71.65% share in 2025, yet online channels are forecast to register a 6.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Diabetes Care Drugs And Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing diabetes prevalence & ageing population | +1.8% | National, concentrated in tier-1 cities with spillover to tier-2/3 | Long term (≥ 4 years) |

| Government reimbursement expansion for innovative therapies | +1.2% | National, with early gains in Beijing, Shanghai, Guangzhou | Medium term (2-4 years) |

| Rising adoption of CGM & insulin pump technology | +0.9% | Urban centers, expanding to tier-2 cities | Medium term (2-4 years) |

| WeChat-based digital adherence platforms | +0.7% | National, higher penetration in tech-savvy demographics | Short term (≤ 2 years) |

| Domestic GLP-1 capacity surge & patent cliffs | +0.6% | National manufacturing hubs, export-oriented regions | Medium term (2-4 years) |

| Tier-2/3-city retail-pharmacy expansion | +0.5% | Secondary and tertiary cities, rural-urban transition zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Diabetes Prevalence & Ageing Population

China’s estimated 15.88% adult diabetes prevalence translates into 140-233 million patients, a figure that strains conventional care pathways. An ageing society compounds complexity: more than 200 million citizens are now ≥ 65 years old, a cohort that exhibits higher insulin resistance and poly-comorbidity [1]Yu-Chang Zhou, "The national and provincial prevalence and non-fatal burdens of diabetes in China from 2005 to 2023 with projections of prevalence to 2050," Military Medical Research, mmrjournal.biomedcentral.com. Elderly patients require assistive technologies and simplified regimens, spurring demand for connected monitoring devices that reduce clinic visits. Without systemic interventions, prevalence could hit 29.1% by 2050, but evidence suggests targeted digital solutions could halve that escalation. Rising expenditure—USD 165.3 billion in direct diabetes outlays—heightens urgency for scalable, tech-enabled models that the China diabetes care drugs and devices market is beginning to provide.

Government Reimbursement Expansion for Innovative Therapies

Annual National Reimbursement Drug List (NRDL) negotiations added 117 molecules in 2024, cutting prices by 61.7% yet safeguarding developer incentives via volume commitments. Inclusion of 15 orphan drugs in 2025 indicates broader coverage for complex diabetic complications. A dual-channel system now permits premium drugs outside hospital formularies, though navigation across basic and commercial insurance tiers remains intricate. Commercial health insurance, sized at RMB 900 billion, is emerging as a bridge for therapies still absent from NRDL coverage boundaries. NVBP insulin procurement trimmed daily insulin cost from 1.63 to 0.68 local daily wages, proving that affordability and quality need not be mutually exclusive [2]Jing Yuan, "National Volume-Based Procurement (NVBP) exclusively for insulin: towards affordable access in China and beyond," BMJ Global Health, gh.bmj.com.

Rising Adoption of CGM & Insulin Pump Technology

Continuous glucose monitoring (CGM) expanded from a RMB 150 million niche to a RMB 4 billion segment by 2025, pushed by young, wellness-oriented buyers and rising physician acceptance. Flash sensors improve time-in-range by 6.5% for premix-insulin users, while real-time CGM systems such as Glunovo achieve 8.89% mean absolute relative difference, surpassing older flash readers at 10.42% [3]Shenghui Ge, "Accuracy of a novel real-time continuous glucose monitoring system: a prospective self-controlled study in thirty hospitalized patients with type 2 diabetes," Frontiers in Endocrinology, frontiersin.org. Insulin pump uptake stands at 11.4% in type 1 patients; nonetheless, pump users reach HbA1c levels of 8.3% versus 9.2% for multiple injections, underscoring clinical value. Cross-company integrations—e.g., Abbott and Medtronic linking FreeStyle Libre with automated delivery algorithms—signal a shift to closed-loop paradigms.

WeChat-Based Digital Adherence Platforms

WeChat-centric care models show statistically significant reductions in fasting and post-prandial glucose as well as HbA1c for type 1 patients using combined flash monitoring. Mobile apps integrating intelligent glucometers helped 59% of participants reach HbA1c below 7.0% within 3 months, reflecting behavioral reinforcement that traditional clinics cannot match. The eKTANG framework uses continuous remote feedback to escalate drug titration or dietary advice promptly, elevating time-in-range metrics. Despite success, engagement divides between urban and rural users remain, making digital literacy a critical adoption hinge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NRDL price erosion for insulin & devices | -0.8% | National, particularly affecting premium product segments | Medium term (2-4 years) |

| Low insulin-pump penetration & education gaps | -0.6% | Rural areas and tier-3 cities with limited specialist access | Long term (≥ 4 years) |

| Data-privacy limits on cloud CGM data | -0.4% | National, affecting cloud-based analytics platforms | Short term (≤ 2 years) |

| Sensor-chip supply-chain volatility | -0.3% | Global supply chains affecting domestic device manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

NRDL Price Erosion for Insulin & Devices

Median insulin price cuts of 42.08% have democratized access but tightened margins, forcing multinationals to reconfigure China portfolios for lower price points yet uncompromised quality. Device makers now face similar procurement rounds, raising questions about capital recovery for R&D-heavy platforms such as patch pumps. Premium products can still enter via commercial insurance, but multi-tier reimbursement navigation delays uptake and complicates marketing. Companies are responding with China-specific SKUs and local manufacturing footprints to keep costs aligned with tender ceilings.

Low Insulin-Pump Penetration & Education Gaps

Pump therapy’s 11.4% penetration underscores systemic barriers beyond affordability, including limited specialist training and gaps in carbohydrate-count education. Rural providers seldom have standardized pump curriculums, resulting in fragmented after-sales support and suboptimal glycemic outcomes. Socio-economic gradients—higher uptake among better-educated, higher-income families—mirror broader digital divides. Hospital-centric care models restrict continuous mentorship, an essential element for pump success, thereby capping growth in the China diabetes care drugs and devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Devices Drive Innovation Despite Drug Dominance

The pharmaceutical segment captured 62.85% of 2025 revenue, confirming its primacy in the China diabetes care drugs and devices market. Yet device revenue is projected to rise faster at a 6.28% CAGR as patients and physicians converge on continuous glucose monitoring and automated delivery systems. CGM adoption has broadened from clinical users to wellness enthusiasts, while insulin pumps progress toward hybrid closed-loop integration.

Monitoring equipment maintains volume leadership; self-monitoring blood glucose meters dominate unit sales but face commodity pricing, whereas CGMs command premium price bands for real-time data feeds. Insulin innovations such as once-weekly Ico Insulin, cleared in 2024, illustrate convergence between long-acting drugs and device ecosystems. GLP-1 injectables, leveraging dual diabetes-obesity indications, are the fastest-growing non-insulin category, supported by strategic licensing moves worth over USD 2 billion each from Novo Nordisk and Merck. This cross-pollination indicates the China diabetes care drugs and devices market size for devices is escalating in tandem with next-generation pharmacotherapy.

By Diabetes Type: Type 1 Acceleration Amid Type 2 Dominance

Type 2 remains the volume anchor with 90.55% of 2025 revenue, driven by sedentary lifestyles and dietary transitions. Digital platforms now merge lifestyle coaching with medication adherence, expanding preventive care access across every tier-city cohort. Continuous remote coaching programs have improved HbA1c control, reinforcing device and drug adherence concurrently.

Type 1 revenue, though smaller, is forecast to grow 6.31% annually, lifted by better diagnostics and broader adult onset recognition. Clinical trials show pump therapy lowers HbA1c to 7.19% compared with 7.71% for multiple injections, underscoring superior glycemic stability. Premium per-patient spending means this cohort drives technological alpha for the China diabetes care drugs and devices market size, with spill-over benefits for type 2 care via shared CGM platforms.

By Age Group: Geriatric Surge Reshapes Care Models

Adults aged 18-64 generated 60.72% of 2025 sales, mirroring diabetes prevalence peaks; nonetheless, the ≥ 65 segment is expanding at 6.18% per year, reflecting population ageing. Cognitive decline and poly-pharmacy risks demand simplified regimens—once-weekly basal insulin and user-friendly CGMs—that fit geriatric limitations.

Guidelines published in 2024 call for personalized targets; digital interfaces now incorporate larger icons and voice prompts to enhance senior usability. Younger adults are the most tech-literate cohort, fueling early adoption of app-linked glucometers and remote consultations. Tailored product design across age strata is emerging as a competitive differentiator in the China diabetes care drugs and devices market.

By Distribution Channel: Digital Transformation Accelerates

Offline venues controlled 71.65% of 2025 turnover, yet online platforms are forecast to advance 6.42% per year as policy reforms permit e-pharmacy sale of prescription antidiabetics. Brick-and-mortar pharmacies remain indispensable in tier-3 cities, where personal counselling is valued and digital bandwidth can be limited.

E-commerce giants have invested in cold-chain and last-mile delivery that preserve insulin integrity; WeChat mini-programs link physician consultations, lab data, and doorstep fulfillment in a single workflow. Hybrid models integrating community pharmacists into digital ecosystems improve adherence monitoring, creating omnichannel synergies that propel growth of the China diabetes care drugs and devices market.

Geography Analysis

Regional performance diverges sharply. Tier-1 hubs—Beijing, Shanghai, Guangzhou—benefit from dense specialist clusters, premium insurance coverage, and early inclusion in NRDL pilots, forming the initial launchpad for novel drugs and sensors. Inter-city patient mobility within the Beijing-Tianjin-Hebei corridor eases some accessibility gaps, though intra-city transport still restricts clinic visits for low-income patients.

Tier-2 and tier-3 cities account for the highest incremental demand thanks to an expanding middle class and ongoing hospital and pharmacy expansions. The National Health Commission’s 2024 directive to broaden primary-care drug distribution targets these municipalities, with a 2027 deadline for chronic-disease coverage. Retail-pharmacy chains are also moving into suburban belts, supplying insulin and CGM consumables while offering diabetes educator services. Capitation pilots in rural counties have cut uncontrolled-diabetes rates and set templates for country-wide rollout.

Rural zones face specialist shortages and weaker digital infrastructure, compelling use of simplified, low-maintenance devices and SMS-based adherence tools. Government-sponsored telemedicine platforms bridge the gap by enabling county-level clinics to consult urban endocrinologists. Pending 5G network upgrades aim to support real-time CGM data streams, which would unlock latent demand and further balance regional inequities in the China diabetes care drugs and devices market.

Competitive Landscape

Foreign incumbents Abbott, Medtronic, and Novo Nordisk continue to command mind-share through breakthrough hardware and biologics portfolios. However, consistent NRDL deflation prompts margin realignment, encouraging joint ventures and technology transfers that localize production. Novo Nordisk’s USD 2 billion acquisition of United Laboratories’ obesity asset UBT251 exemplifies portfolio broadening into adjacent metabolic domains.

Domestic innovators are rapidly scaling. Sinocare’s exclusive European distribution pact for its third-generation CGM reflects international validation of Chinese engineering. Regulatory measures now prioritise local inventions within procurement, granting accelerated review to home-grown GLP-1 analogs and non-invasive glucometers. Hengrui’s USD 400 million licence-in of a US GLP-1 candidate further illustrates capital inflows to domestic R&D.

Competitive differentiation is shifting toward integrated ecosystems that combine drugs, devices, and data services into seamless user journeys. The Abbott-Medtronic linkage of FreeStyle Libre sensors with automated pumps underscores movement toward closed-loop platforms. Providers capturing rural expansion and geriatric service niches are likely to outpace rivals focused solely on urban hospital channels, setting the strategic trajectory for the China diabetes care drugs and devices market.

China Diabetes Care Drugs And Devices Industry Leaders

-

Medtronics

-

Roche

-

NovoNordisk

-

Sanofi

-

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: China’s NMPA approved Prusogliptin Tablets by Cspc Ouyi Pharmaceutical for adult type 2 diabetes management, marking another domestically developed oral agent.

- December 2024: Sanofi committed EUR 1 billion (USD 1.04 billion) to build a Beijing insulin manufacturing hub, its largest China investment to date.

- December 2024: A. Menarini Diagnostics and Sinocare signed an exclusive agreement to distribute Sinocare’s third-generation CGM across 20+ European markets.

- June 2024: The NMPA cleared Novo Nordisk’s once-weekly Ico Insulin for adult type 2 diabetes, reducing injection burden from daily to weekly.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the China diabetes care drugs and devices market as the combined annual revenue earned within the country from prescription anti-diabetic medicines and patient-use devices that monitor glucose or deliver insulin, expressed in constant 2024 dollars. According to Mordor Intelligence analysts, this includes oral and injectable therapies, self-monitoring blood glucose meters, continuous glucose monitors, insulin pens, pumps, syringes, and supporting consumables sold through hospitals, retail outlets, and online platforms.

Products used only for veterinary care and over-the-counter nutritional supplements that do not carry therapeutic diabetes claims stand outside the scope.

Segmentation Overview

-

By Product Type

-

Devices

-

Monitoring Devices

- Self-Monitoring Blood Glucose Meters

- Continuous Glucose Monitoring Systems

- Management Devices

-

Monitoring Devices

-

Drugs

- Oral Anti-Diabetic Drugs

- Insulin Drugs

- Non-Insulin Injectables

- Combination Drugs

-

Devices

-

By Diabetes Type

- Type 1 Diabetes

- Type 2 Diabetes

-

By Age Group

- Adult

- Geriatric

- Pediatric

-

By Distribution Channel

- Offline

- Online

Detailed Research Methodology and Data Validation

Primary Research

To balance published data, the team interviewed endocrinologists in tier-1 and tier-2 cities, procurement managers at hospital chains and device distributors, and surveyed insulin users across eastern, central, and western China. These voices tested prevalence assumptions, average selling prices, and channel shifts before numbers were finalized.

Desk Research

Public domain evidence underpins the initial model. Analysts assembled prevalence and treatment rates from sources such as the International Diabetes Federation atlas, the National Health Commission chronic disease bulletin, and the China Health Statistics Yearbook, and then checked trade flow shifts through General Administration of Customs data and patent filings accessed via Questel. Company financials from D&B Hoovers, drug price notices published in provincial reimbursement lists, and news captured by Dow Jones Factiva added price points and launch timings. Additional insight came from peer-reviewed journals outlining CGM adoption and volume-based procurement effects. The sources listed illustrate the mix only, and many other references informed validation and clarification.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build followed by expenditure per patient reconstruction produced the baseline, which is then cross-checked with bottom-up supplier revenue samples and channel checks to fine-tune totals. Key variables include adult diabetes prevalence, insured therapy coverage, average daily insulin dose, device replacement cycles, e-commerce penetration for test strips, and NVBP price erosion percentages. Multivariate regression projects each driver to 2030, after which scenario analysis examines reforms to reimbursement and domestic manufacturing capacity. Gaps in bottom-up samples are bridged by applying verified average selling prices to shipment volumes collected from customs and hospital tenders.

Data Validation & Update Cycle

Outputs pass a two-layer analyst review; variance against external benchmarks triggers re-work, and every model is refreshed annually with interim updates when policy or supply shocks occur. A final compliance check ensures clients receive the most current view.

Why Mordor's China Diabetes Drugs And Devices Baseline Earns Trust

Published estimates often diverge because firms choose different product baskets, convert currencies on assorted dates, and refresh models at varying speeds. By aligning both drugs and devices under one definition, fixing exchange rates to the People's Bank annual average, and updating the model every twelve months, our study reduces these moving parts.

Differences usually stem from excluding either drugs or devices, applying list rather than net prices, or treating self-monitoring consumables as separate. Mordor's analysts incorporate NVBP price outcomes, cross-verify unit volumes with customs ledgers, and introduce expert-endorsed dose intensity factors, which together temper extremes found elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.98 B (2025) | Mordor Intelligence | - |

| USD 7.85 B (2025) | Global Consultancy A | Covers drugs only and relies on unadjusted list prices |

| USD 3.20 B (2025) | Trade Journal B | Devices only, shipment scaling without net price normalization |

The comparison shows that values swing with scope and price treatment, yet the Mordor baseline sits mid-range and is built on transparent inputs that clients can trace and replicate, giving decision makers a dependable starting point.

Key Questions Answered in the Report

What is the current value of the China diabetes care drugs and devices market?

The market stands at USD 9.48 billion in 2026 and is forecast to reach USD 12.41 billion by 2031.

Which segment is expanding fastest within the product mix?

Devices, particularly continuous glucose monitoring and insulin pumps, are growing at a 6.28% CAGR through 2031.

How has government procurement affected insulin pricing?

National Volume-Based Procurement lowered median insulin prices by 42.08%, saving USD 2.85 billion across 32,000 medical facilities.

Why is type 1 diabetes expected to grow more quickly than type 2?

Improved diagnostics and higher per-patient technology spending are driving a 6.31% CAGR for the type 1 segment.

What role do online channels play in market distribution?

E-commerce and WeChat-based platforms are projected to expand at 6.42% per year, offering cold-chain delivery and digital adherence support, though offline pharmacies still hold the majority share.

How is the ageing population shaping product development?

More than 200 million citizens aged 65+ require simplified regimens such as once-weekly basal insulin and senior-friendly CGM interfaces, steering innovation toward usability and integrated chronic-condition management.

Page last updated on: