Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

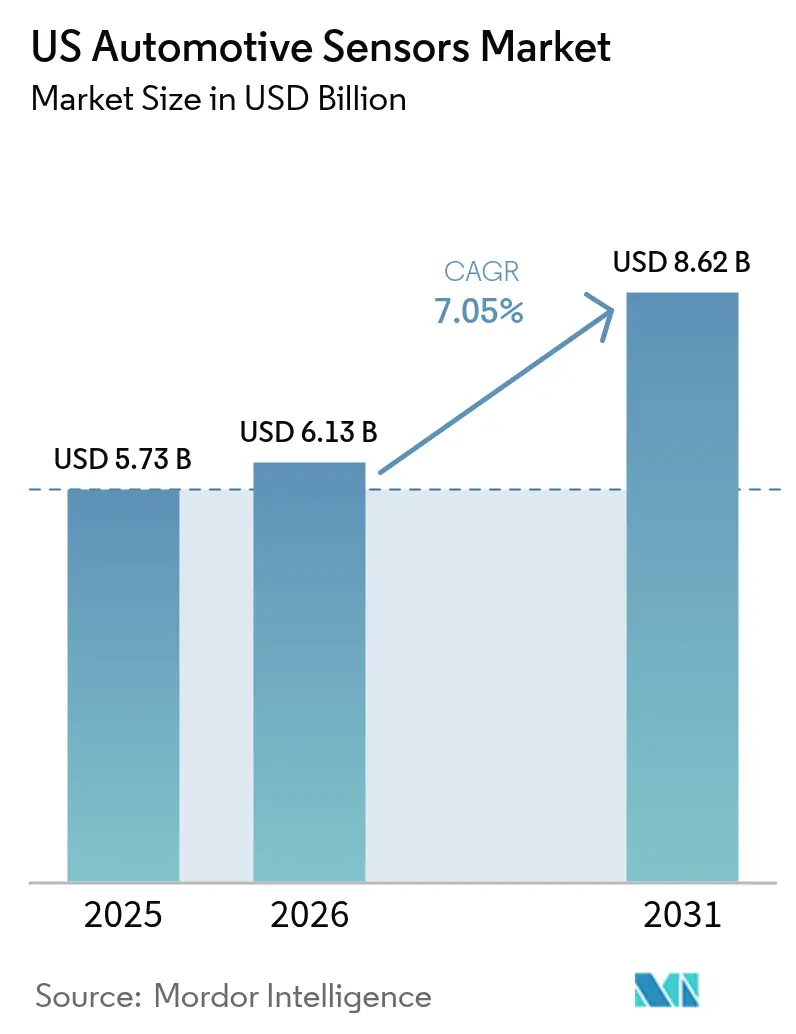

| Base Year Market Size (2025) | USD 5.73 Billion |

| Market Size (2026) | USD 6.13 Billion |

| Market Size (2031) | USD 8.62 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Automotive Sensors Market Analysis by Mordor Intelligence

The US Automotive Sensors Market size is expected to grow from USD 5.73 billion in 2025 to USD 6.13 billion in 2026 and is forecast to reach USD 8.62 billion by 2031 at 7.05% CAGR over 2026-2031. Automakers are embedding more sensors per vehicle to comply with tire-pressure, stability-control, and automated-braking mandates. At the same time, fleet operators adopt sensor-rich telematics to control insurance costs and emissions. Radar, lidar, and MEMS-based devices continue to achieve cost and performance breakthroughs, giving legacy suppliers and start-ups new avenues for differentiation in the United States automotive sensors market.

Key Report Takeaways

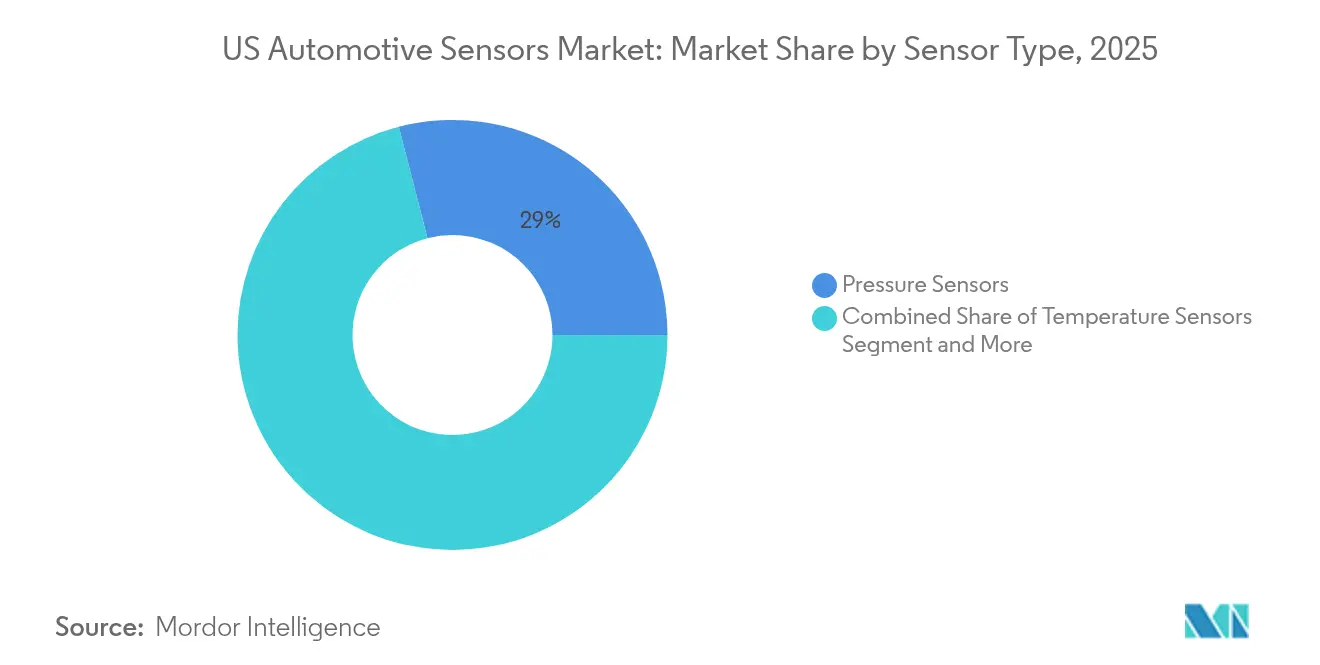

- By sensor type, pressure sensors led with 29.02% of the United States automotive sensors market share in 2025; radar sensors are forecast to expand at a 8.02% CAGR through 2031.

- By application, powertrain systems accounted for 35.98% of revenue in 2025, while ADAS is set to grow at an 8.36% CAGR to 2031.

- By vehicle type, passenger cars held 64.55% of the United States automotive sensors market size in 2025, and heavy commercial vehicles will post the quickest growth at an 8.62% CAGR.

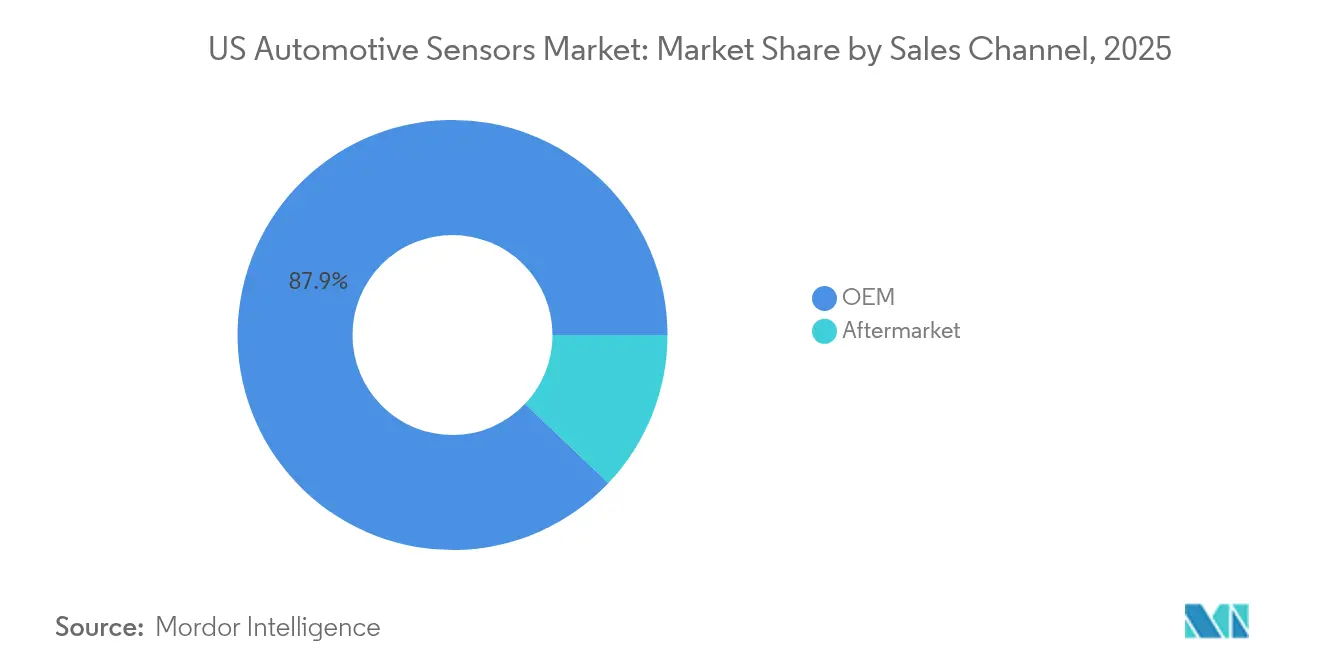

- By sales channel, OEM installations captured 87.92% share in 2025; the aftermarket segment is rising at a 8.99% CAGR as retrofits gain popularity.

- By propulsion, ICE powertrains kept 67.58% share during 2025; the Battery EV segment is rising at a 7.34% CAGR through 2031.

- By sensor technology, MEMS devices dominated with 73.44% share and are also the fastest-growing category at a 7.21% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Automotive Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Adoption Pushes Sensor Content per Vehicle | +2.4% | California, Washington, Northeast states | Long term (≥ 4 years) |

| Federal TPMS, ESC & NCAP Upgrades | +1.8% | Nationwide, with regulatory enforcement from Washington DC | Medium term (2-4 years) |

| Software-Defined Vehicle Architectures | +1.5% | Technology hubs: California, Michigan, Texas | Medium term (2-4 years) |

| CHIPS Act Incentivizes On-Shore MEMS Fabs | +1.2% | US nationwide, with concentration in Arizona, Texas, New York | Medium term (2-4 years) |

| Connected-Insurance Telematics Retrofits | +0.8% | Urban centers, initially in Northeast and West Coast | Short term (≤ 2 years) |

| Fleet Decarbonisation Targets | +0.6% | Corporate fleets nationwide, led by coastal states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CHIPS Act Incentivises On-Shore MEMS Fabs

New federal grants worth USD 39 billion are steering wafer-fab projects to Arizona, Texas and upstate New York, ensuring a local pipeline of MEMS pressure, inertial and magnetic sensors that underpin engine, battery and chassis controls. Rogue Valley Microdevices has already secured USD 6.7 million for a Florida plant that will nearly triple its automotive MEMS capacity, illustrating how smaller foundries can scale under the program. The added capacity reduces lead-times, cuts shipping risk and supports just-in-time delivery for Detroit and coastal assembly plants. Universities gain research grants that seed next-gen micromachining processes, further anchoring innovation inside the United States automotive sensors market. Combined, these actions lift resilience and pull future production back from overseas fabs.[1]“Rogue Valley Microdevices Receives USD 6.7 Million From CHIPS Act,” Plant Services, plantservices.com

EV Adoption Pushes Sensor Content per Vehicle

Electric models integrate two to three times more semiconductors than ICE cars, pushing sensor value toward a greater share by 2030. Battery-management systems alone require multiple temperature, current and voltage nodes to prevent thermal runaway. Position and magnetic sensors monitor e-motor speed, while high-voltage isolation devices maintain safety. Government tax credits and coast-to-coast charging grants accelerate delivery volumes, so suppliers are scaling SiC-based pressure and temperature dies to meet harsher under-hood environments. As a result, the United States automotive sensors market is benefiting from higher average selling prices even when overall vehicle production remains flat.

Connected-Insurance Telematics Retrofits

Usage-based insurance programs rely on accelerometers, gyroscopes and GNSS modules to track driving style and mileage. With connected cars projected to constitute more than four fifth of new US sales in 2025, retrofitting older models with plug-in telematics dongles is becoming common. Independent repair shops see new revenue in device installation and calibration, while insurers gain refined risk scoring that can slash claims costs increases. This aftermarket pull lifts unit volumes for MEMS inertial sensors and 4G/5G gateways across the United States automotive sensors market.

Software-Defined Vehicle Architectures

Central zonal controllers now aggregate data from hundreds of nodes and push updates over the air. Tesla proved that simplified wiring can cut cable length and weight, and mainstream OEMs are following suit. High-speed radar and lidar chips from Texas Instruments improve perception, and their software stacks are upgradable to future autonomy levels without hardware change.[2]“News Release 15 April 2025,” Texas Instruments, ti.com For suppliers, this means designing sensors with encrypted communication and deterministic latency to slot cleanly into the evolving backbone. The shift keeps the United States automotive sensors market aligned with cloud-native development cycles rather than traditional model-year updates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost & Price-Erosion Squeeze Tier-1 Margins | -1.2% | Michigan, Ohio, Indiana auto manufacturing belt | Medium term (2-4 years) |

| Silicon-Supply Water-Stress | -0.9% | Arizona, New Mexico, Texas | Long term (≥ 4 years) |

| Sensor-Level Cyber-Security | -0.8% | Nationwide, with regulatory focus in Washington DC | Medium term (2-4 years) |

| Harsh-Duty Reliability & Calibration | -0.6% | Extreme climate regions: Alaska, Desert Southwest, Upper Midwest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Silicon-Supply Water-Stress Constraints

Next-generation fabs in Arizona may each draw significant liters of water daily, straining aquifers already under drought pressure. Community opposition or permitting delays could cap local wafer output, tightening the flow of automotive pressure and inertial dies. To mitigate risk, manufacturers are installing closed-loop recycling that recovers more than 70% of process water, yet capital outlays lengthen payback. Prolonged shortages could temper growth for the United States automotive sensors market if additional sites are not approved.

Cost & Price-Erosion Squeeze Tier-1 Margins

OEMs are in-sourcing software and hardware road-maps, forcing traditional Tier-1s to slash prices and absorb design costs. Analysts expect average supplier margins to slip slightly within five years. Lower profitability limits R&D outlays for new sensing platforms, slowing mass-market deployment. Some US-based suppliers are pivoting to integration and over-the-air calibration services, yet widespread restructuring may still stifle innovation rates inside the United States automotive sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Pressure Sensors Hold the Lead, Radar Closes the Gap

Pressure devices delivered 29.02% of 2025 revenue, anchoring applications such as fuel injection, brake boost and mandated tire-pressure monitoring. The United States automotive sensors market size for pressure units is set to expand steadily in line with fuel-efficiency and emissions targets. Radar modules, although smaller today, will grow at a 8.02% CAGR through 2031 thanks to falling 77 GHz chipset prices and NCAP pressure to add blind-spot, front-collision and cross-traffic alerts. Tier-1s now bundle four-corner 4D radar into mainstream SUVs, signalling that sensor fusion is shifting from premium to volume segments.

Second-generation millimetre-wave architectures integrate digital beam-forming and AI-enhanced object classification on a single CMOS die. This reduces bill-of-materials and simplifies thermal design, helping radar to erode camera-only ADAS share. Suppliers that combine radar with inertial reference units promise high-accuracy odometry even when GPS is blocked, creating new value pools within the United States automotive sensors industry.

By Application: Powertrain Leads, ADAS Posts Break-Out Growth

Powertrain systems accounted for 35.98% of 2025 spend, covering air-flow, knock, coolant-temperature and battery pack sensors. Compliance with Tier 3 emissions rules keeps powertrain allocations high. At the same time, ADAS and autonomous functions will expand at an 8.36% CAGR to 2031, raising their portion of the United States automotive sensors market size considerably. Ultrasonic, camera, radar and lidar combinations enable Level-2+ functions, while NHTSA’s new automatic emergency-braking mandate locks in baseline volumes.

To meet redundancy targets, OEMs specify dual independent sensing paths for lateral and longitudinal control. This pushes total semiconductor count per vehicle past thousand mark by 2029, cementing ADAS as the fastest-growing budget line for sensors. Continuous over-the-air feature upgrades further stretch lifecycle revenue because dormant compute headroom can be monetised years after vehicle sale.

By Vehicle Type: Passenger Cars Dominate, Heavy Trucks Accelerate

Passenger cars absorbed 64.55% of shipments in 2025 given their much higher build numbers. Content per unit is rising in mid-sized crossover utility vehicles as well, broadening demand. Heavy commercial vehicles will post an 8.62% CAGR as federal regulators roll out automatic emergency braking and electronic stability rules for Class 8 trucks. Rising e-commerce volumes amplify the need for collision-warning and fatigue-monitoring sensors. Such mandates elevate the United States automotive sensors market share for heavy-duty applications despite slower build rates.

Light commercial vans benefit from last-mile delivery growth and electrification grants, which enable richer telematics packages. Integration complexities include sealing lidar housings against power-washer spray and managing electromagnetic interference from high-current traction inverters. These nuances spur specialised suppliers to co-design sensors with body builders, creating fresh revenue pockets inside the United States automotive sensors industry.

By Sales Channel: OEM Remains Dominant, Aftermarket Picks Up Pace

Factory-fit installations owned 87.92% of 2025 turnover, reflecting the complexity of integrating sensors into safety-critical networks. Automakers lock in multi-year supply agreements, offering volume visibility. Yet the aftermarket will rise at a 8.99% CAGR as insurers, fleet managers and tech firms retrofit data loggers and ADAS calibration kits into ageing vehicles. Growth favours plug-and-play MEMS hubs that pair cellular modems with GPS, accelerometers and CAN gateways.

Escalating calibration requirements pose hurdles for independent workshops because alignment rigs and software subscriptions raise entry costs. Consolidation among service chains may follow, gradually shifting bargaining power within the United States automotive sensors market toward equipment vendors that bundle hardware with training.

By Propulsion: ICE Still Largest, Battery EVs Surge

ICE powertrains kept 67.58% share during 2025, sustained by continued consumer preference for gasoline pickups and SUVs. Their sensor spend revolves around exhaust gas recirculation, particulate filtering and turbo boost control. Battery EV sensors will climb at a 7.34% CAGR, fuelled by federal tax credits and coast-to-coast charging network expansion. High-precision shunt, hall-effect and fibre-optic sensors supervise 800-V architectures, and silicon-carbide pressure dies monitor coolant flow in fast-charging loops.

Hybrid systems add duplicated sensing layers because both the internal combustion engine and electric motor require independent temperature and vibration monitoring. As cumulative hybrid volumes rise, suppliers can leverage shared pressure and position sensor platforms, smoothing ramp-up costs across the United States automotive sensors market.

By Sensor Technology: MEMS Commands Volume and Momentum

MEMS platforms supplied 73.44% of 2025 units and will grow at a 7.21% CAGR. Micro-machined capacitive and piezoresistive structures give unmatched size, cost and vibration resilience. Foundries are now releasing wafer-level packages that integrate ASIC signal-conditioning, slashing board space in power-dense inverters. Early adoption of MEMS micromirror lidar offers 120° field-of-view with sub-three-centimetre depth accuracy, crucial for urban automated-valet modes.

Non-MEMS sensors, such as bulk-wave ultrasonic transducers and macro-machined pressure capsules, retain niches where extreme pressures or fluid compatibility rule out silicon structures. Still, ongoing cost decreases within MEMS will gradually replace these legacy designs, cementing the dominant position of MEMS in the United States automotive sensors market.

Geography Analysis

Midwestern states such as Michigan and Ohio continue to assemble the majority of vehicles and therefore integrate the largest absolute number of engine, chassis and cabin sensors. Skilled labour pools and established Tier-1 clusters make these regions indispensable for validation and volume production. However, capital for greenfield fabs is drifting southwest toward Arizona and Texas, allowing a new semiconductor corridor to emerge under the CHIPS and Science Act. As those fabs reach volume, sensor wafers can ship directly to Midwest module lines, shrinking logistics risk and inventory buffers across the United States automotive sensors market.

California leads national electric-vehicle penetration, which in turn accelerates adoption of high-voltage current, temperature and isolation sensors. Silicon Valley software firms work hand-in-glove with semiconductor specialists to refine sensor fusion algorithms that underpin Level-2+ autopilot features. Regulatory open-roads permits further entice lidar and radar start-ups to pilot fleets in San Francisco and Los Angeles, reinforcing the coast’s innovation flywheel.

The Northeast and Mid-Atlantic present dense traffic and harsh winters. Demand therefore skews toward radar and all-weather camera modules capable of handling salt spray and sub-zero conditions. Insurance headquarters in Connecticut, New York and Pennsylvania promote telematics rollouts, spurring aftermarket dongle uptake. Meanwhile, Southeastern states like Tennessee and South Carolina host several new battery-plant and EV-assembly projects, expanding regional consumption of pack-level temperature and pressure sensors. Collectively, these geographic dynamics build a balanced regional footprint for suppliers serving the United States automotive sensors market.

Competitive Landscape

Five semiconductor majors—Infineon, NXP, STMicroelectronics, Texas Instruments and Renesas—collectively captured just over half of 2024 revenue, confirming a tight oligopoly. Continental, Bosch and Denso still lead module-level integration, yet their influence fades as OEMs negotiate directly with chip houses for next-gen radar and battery controllers. Texas Instruments recently introduced a 2.5-nanosecond response lidar driver that cuts system latency and a new 77 GHz radar transceiver that extends detection range past 500 metres.

Domestic capacity build-outs alter power balances further. Foundry start-ups supported by CHIPS grants can offer niche processes such as silicon-on-insulator MEMS to Tier-1s seeking dual sourcing. Strategic alliances pair fab-less radar designers with wafer fabs that specialise in high-resistivity substrates, ensuring volume scalability. Suppliers that master vertically integrated sensor-plus-software stacks stand to capture premium margins as vehicles morph into data platforms.

Tier-1s face margin compression yet retain integration expertise. Forward-looking firms reposition as system orchestrators that unify chips from multiple vendors, manage cyber-security keys and certify ISO 26262 safety. The value of such orchestration rises with every added ECU domain, allowing agile Tier-1s to defend relevance even while direct silicon revenue migrates upward in the United States automotive sensors market.

US Automotive Sensors Industry Leaders

Texas Instruments Incorporated

Robert Bosch GmbH

Continental AG

Denso Corporation

Infineon Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Texas Instruments unveiled the LMH13000 lidar laser driver and AWR2944P mmWave radar SoC for faster, longer-range perception.

- January 2024: Infineon introduced the Xensiv TLI5590-A6W magnetic position sensor, aimed at e-motor control in battery EVs.

- February 2023: Continental launched the eRPS rotational position sensor to heighten steering precision in electric power-assist systems.

US Automotive Sensors Market Report Scope

The United States automotive sensors market covers the current and upcoming trends with recent technological developments. The report will provide a detailed analysis of various market areas by type, application, and vehicle. The market share of automotive sensor manufacturing companies in the country will be provided in the report.

By Sensor Type

| Temperature Sensors |

| Pressure Sensors |

| Speed / Velocity Sensors |

| Level / Position Sensors |

| Magnetic Sensors |

| Gas / Chemical Sensors |

| Inertial Sensors (Accel/Gyro) |

| LiDAR Sensors |

| Radar Sensors |

| Ultrasonic Sensors |

| Image / Camera Sensors |

| Current Sensors |

By Application

| Powertrain |

| Body Electronics & Comfort |

| Vehicle Security & Safety |

| ADAS & Autonomous Systems |

| Telematics & Connectivity |

| Battery-Management (EV) |

By Vehicle Type

| Motorcycles |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

By Sales Channel

| OEM |

| Aftermarket |

By Propulsion

| Internal-Combustion Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Fuel-Cell Electric Vehicles |

By Sensor Technology

| MEMS |

| Non-MEMS / Macro Sensors |

| By Sensor Type | Temperature Sensors |

| Pressure Sensors | |

| Speed / Velocity Sensors | |

| Level / Position Sensors | |

| Magnetic Sensors | |

| Gas / Chemical Sensors | |

| Inertial Sensors (Accel/Gyro) | |

| LiDAR Sensors | |

| Radar Sensors | |

| Ultrasonic Sensors | |

| Image / Camera Sensors | |

| Current Sensors | |

| By Application | Powertrain |

| Body Electronics & Comfort | |

| Vehicle Security & Safety | |

| ADAS & Autonomous Systems | |

| Telematics & Connectivity | |

| Battery-Management (EV) | |

| By Vehicle Type | Motorcycles |

| Passenger Cars | |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| By Sales Channel | OEM |

| Aftermarket | |

| By Propulsion | Internal-Combustion Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| Fuel-Cell Electric Vehicles | |

| By Sensor Technology | MEMS |

| Non-MEMS / Macro Sensors |

Key Questions Answered in the Report

What is the current value of the United States automotive sensors market?

The market is valued at USD 6.13 billion in 2026 and is on track to expand at a 7.05% CAGR toward 2031.

Which sensor category holds the largest share today?

Pressure sensors lead with 29.02% of 2025 revenue due to mandatory tire-pressure monitoring and powertrain applications.

How quickly are radar sensors growing in the United States automotive sensors market?

Radar modules are projected to achieve a 8.02% CAGR between 2026-2031, making them the fastest-growing sensor type.

Why is the CHIPS Act significant for sensor suppliers?

Federal grants and tax credits worth USD 39 billion are financing new US fabs that shorten supply chains and expand MEMS production capacity, improving resilience.

Which vehicle segment offers the strongest growth opportunity?

Battery electric vehicles show the highest sensor CAGR at 7.34% through 2031 because they use two to three times more semiconductors than ICE models.

How are new safety rules influencing demand?

NHTSA mandates on seat-belt reminders and proposed automatic emergency braking require additional radar, camera and occupancy sensors, locking in baseline growth for suppliers.

Page last updated on: