Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

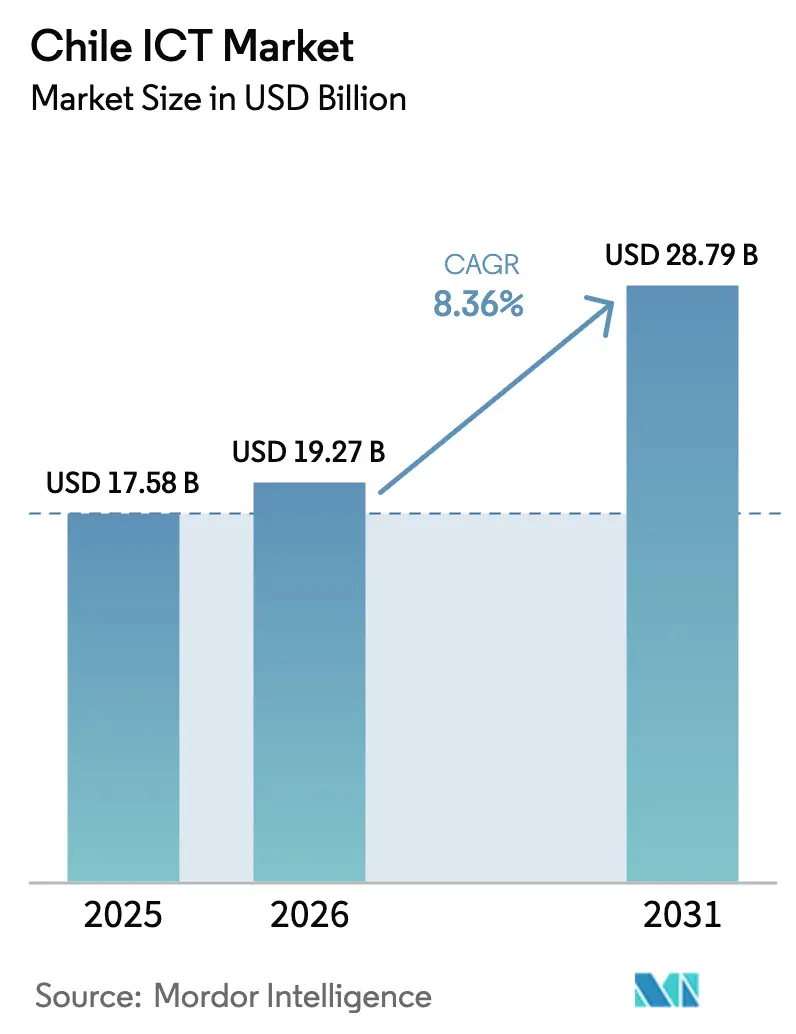

| Base Year Market Size (2025) | USD 17.58 Billion |

| Market Size (2026) | USD 19.27 Billion |

| Market Size (2031) | USD 28.79 Billion |

| Growth Rate (2026 - 2031) | 8.36% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile ICT Market Analysis by Mordor Intelligence

The Chile ICT Market size is expected to grow from USD 17.58 billion in 2025 to USD 19.27 billion in 2026 and is forecast to reach USD 28.79 billion by 2031 at 8.36% CAGR over 2026-2031. Fiber-dense fixed networks, hyperscale cloud commitments, and a cybersecurity law that took effect in 2024 are redirecting value away from legacy voice toward cloud-native and managed-service revenue streams. Amazon Web Services is investing USD 4 billion in a Santiago region scheduled to open by end-2026, while Microsoft launched the Chile Central Azure region in June 2025 with USD 3.3 billion allocated to 100% renewable-powered capacity. Together with Google’s Humboldt submarine cable, these new facilities lower latency for banking workloads and position Chile as Latin America’s most connected digital hub. Peso volatility and a skills gap in cloud architecture temper growth prospects, yet government voucher schemes for SMEs and compulsory digital-first public services under Law 21.180 keep domestic demand resilient. Competitive intensity centers on three telecom incumbents that control 72.6% of mobile subscriptions, but IT services remain fragmented, creating room for local integrators such as Sonda to scale recurring revenue through AI-led managed services.

Key Report Takeaways

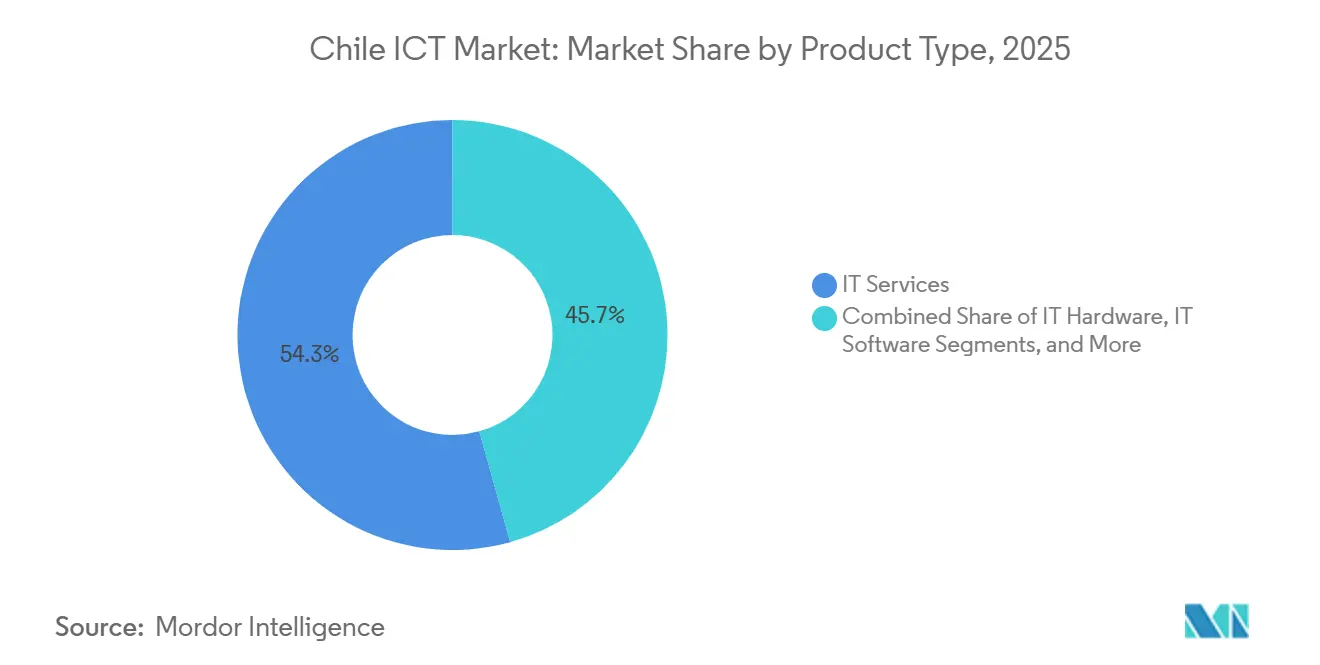

- By product type, IT services led with a 54.32% revenue share in 2025, while IT security and cybersecurity is forecast to expand at a 9.08% CAGR to 2031.

- By enterprise size, large enterprises accounted for 63.14% of 2025 spending, whereas small and medium-sized enterprises are advancing at a 9.82% CAGR through 2031.

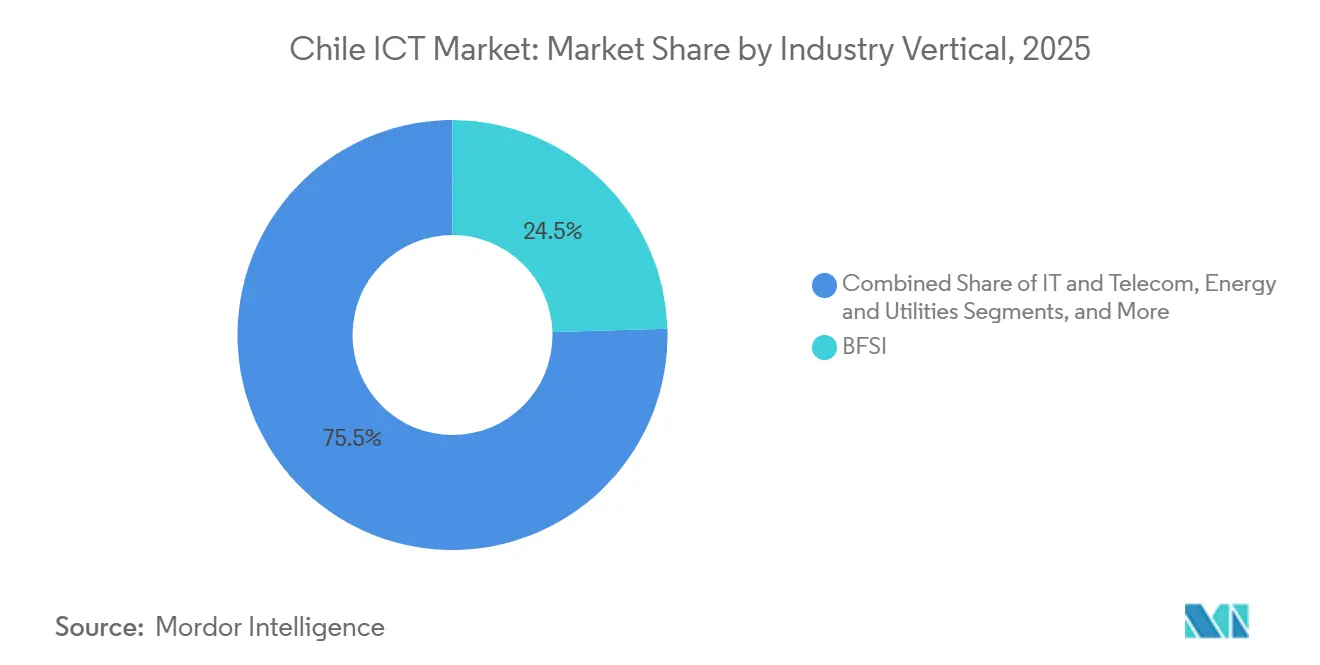

- By industry vertical, banking, financial services, and insurance captured 24.54% of 2025 revenue; healthcare and life sciences is projected to grow at a 10.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of fiber optic backbone infrastructure | +1.4% | National, highest density in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Rising cloud adoption among Chilean enterprises | +1.8% | National, concentrated in Santiago metropolitan area | Short term (≤ 2 years) |

| Government digital transformation programs | +1.2% | National, early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Growing demand for cybersecurity solutions | +1.5% | National, priority in BFSI and government sectors | Short term (≤ 2 years) |

| Submarine cable landings positioning Chile as digital hub | +0.9% | National, benefits Santiago and coastal cities | Long term (≥ 4 years) |

| Incentives for renewable-powered data centers in Patagonia | +0.7% | Southern Chile, Patagonia region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of Fiber Optic Backbone Infrastructure

Chile reached 4.72 million fixed-broadband connections by end-2025, with fiber-to-the-home accounting for 73.5% of lines, the region’s highest share.[1]Subsecretaría de Telecomunicaciones, “Estadísticas del Sector Telecomunicaciones,” subtel.gob.cl Competitive gigabit offers from Claro-VTR and Movistar nudge enterprises to swap MPLS circuits for SD-WAN, trimming WAN costs by up to 40%. Entel earmarked USD 431 million for 2025 capex focused on rural backhaul, and the National Fiber Plan targets 95% household coverage by 2030, although deployment in Aysén and Magallanes still lags because of rugged terrain. Dense last-mile fiber underpins cloud migration, hybrid work, and video-first collaboration, reinforcing bandwidth-heavy use cases across banking and education.

Rising Cloud Adoption Among Chilean Enterprises

AWS’s USD 4 billion Santiago region and Microsoft’s USD 3.3 billion Chile Central Azure region create in-country availability zones that satisfy data-residency clauses in the Personal Data Protection Law, cutting latency for e-commerce and financial apps by more than 30%. Cloud spending climbed to USD 1.9 billion in 2025 and is projected to grow at 20.3% CAGR through 2028, propelled by SaaS uptake in HR, CRM, and ERP workloads. Banks containerize core systems on Kubernetes for rapid feature releases, and manufacturers tap GPU instances for computer-vision quality control. Hybrid architectures persist in heavily regulated sectors, but the balance of new workloads now defaults to public cloud.

Government Digital Transformation Programs

The ChileAtiende platform handled 15 million online transactions in 2025, trimming in-person municipal visits by 40% and shrinking average service times from 12 to 3 days. ClaveÚnica counts 18 million registered users, delivering single sign-on across tax, health, and social-benefit portals. An AI investment fund of USD 20 million backs projects in agriculture and mining under the National AI Policy 2024-2030. Blockchain pilots for digital identity and open-source procurement policies push agencies toward interoperable, ISO/IEC 27001-aligned platforms, widening public-sector demand for middleware, analytics, and identity-management solutions.

Growing Demand For Cybersecurity Solutions

Law 21.663 obliges critical-infrastructure operators to report breaches within 24 hours, spurring double-digit budget increases across banking and energy firms. The workforce gap reached 28,000 specialists in 2025, pushing median salaries for senior roles above USD 80,000 and fueling demand for managed security services. Providers such as Sonda deploy SIEM and EDR platforms infused with machine learning to detect ransomware campaigns that targeted payment gateways in 2025. PCI DSS 4.0 compliance accelerated point-of-sale tokenization, and mid-tier retailers now outsource 24/7 threat monitoring to offset talent shortages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High concentration of market power in telecom operators | -1.1% | National, pronounced in mobile and fixed broadband | Medium term (2-4 years) |

| Skills shortage in advanced IT disciplines | -0.9% | National, acute in Santiago and tech hubs | Short term (≤ 2 years) |

| Macroeconomic volatility and peso depreciation | -0.8% | National, import-dependent hardware and software | Short term (≤ 2 years) |

| Limited edge data center footprint outside Santiago | -0.6% | Valparaíso, Concepción, northern mining zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Concentration Of Market Power In Telecom Operators

Entel, Movistar, and Claro together held 72.6% of mobile subscriptions and 66.2% of fixed-broadband lines in 2025, reinforcing price rigidity for enterprise circuits. The proposed Claro-Entel bid for Telefónica Chile triggered scrutiny from the Fiscalía Nacional Económica, which fears consolidation could stall rural 5G rollout. Asymmetric interconnection rates and local-loop unbundling exist in law but remain weakly enforced, limiting wholesale access for challengers such as WOM and Mundo Pacífico. Reduced competition keeps leased-line pricing above the Latin American average, squeezing margins for cloud-first SMEs.

Skills Shortage In Advanced IT Disciplines

Universities produced about 8,000 IT graduates in 2024, far short of demand for cloud architects, data engineers, and security analysts, forcing companies to recruit talent from neighboring countries. Median pay for senior cloud roles tops USD 80,000, a premium that squeezes SME budgets. Government vouchers cover consulting costs, and Microsoft pledged to train 180,000 workers by 2027, yet brain-drain persists as graduates relocate to higher-paying positions abroad.[2]Microsoft News Center, “Microsoft Opens Chile Central Azure Region,” news.microsoft.com Skills scarcity extends project timelines and inflates the total cost of ownership for AI and IoT deployments, capping adoption among resource-constrained firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services And Security Lead Diversification

IT services captured 54.32% of revenue in 2025 as multiyear ERP rollouts and managed operations contracts provided predictable cash flows less exposed to hardware cycles. Enterprises turned to S/4HANA migrations and AI-driven analytics to streamline supply chains, while outsourcing demand surged for business-process services in banking and mining. IT hardware spending lagged because peso depreciation lifted import costs by 12-15% and lengthened desktop refresh intervals to four years. Communication services posted single-digit growth as unlimited data plans compressed ARPU despite rising 5G penetration.

IT security and cybersecurity is the fastest-growing category, expanding at a 9.08% CAGR through 2031 as companies deploy zero-trust frameworks and endpoint detection tools to comply with Law 21.663. Managed security providers layer SIEM and XDR capabilities on Chile ICT market size agreements, helping mid-tier banks mitigate a workforce shortfall. Software-as-a-service adoption in HR and CRM remains brisk because subscription pricing shifts capex to opex, and hybrid cloud persists in regulated sectors where on-premises resources satisfy sovereignty rules. The shift away from hardware reselling toward value-added managed services widens margins across the Chile ICT market share for service-focused integrators.

By Enterprise Size: SME Digitalization Accelerates

Large enterprises accounted for 63.14% of 2025 outlays, led by mining majors and universal banks that integrate private clouds with hyperscale regions for burst capacity and disaster recovery. Dedicated teams from Accenture and IBM execute these complex migrations, layering predictive analytics over IoT sensor data in copper mines and retail chains. Edge computing pilots at autonomous haulage sites underscore demand for sub-10-millisecond latency in remote zones.

Small and medium-sized enterprises, however, are the fastest-growing cohort, with a 9.82% CAGR through 2031, as CORFO vouchers and fintech leasing cut up-front costs. E-commerce adoption among SMEs vaulted from 45% in 2020 to 78% by 2024, prompting the proliferation of Shopify plug-ins and Mercado Libre logistics. Yet 40% of SMEs cite talent gaps as a barrier to AI projects, leading them to turn to no-code automation platforms. As Chile's ICT market size spending shifts, integrators bundle cloud migration with bookkeeping and payroll SaaS, creating low-touch offerings that lower churn among cost-sensitive clients.

By Industry Vertical: BFSI Dominance And Healthcare Surge

Banking, financial services, and insurance led with 24.54% of 2025 revenue as open-banking regulations required account-data APIs and threat-intelligence investments to combat payment fraud. Santander reduced account opening to 15 minutes through digital onboarding, while Banco de Chile containerized payment processing on Kubernetes to absorb Black Friday peaks. Core-bank upgrades and real-time analytics ensure the vertical retains the highest Chile ICT market share in value terms.

Healthcare and life sciences is projected to grow at 10.19% CAGR to 2031, lifted by telemedicine platforms that handled 46% of consultations in 2024 and the Ministry of Health’s interoperability mandate for electronic records. Hospital Digital initiatives require cloud-hosted patient-record systems and secure data-exchange standards, driving fresh demand for integration middleware and cybersecurity. Retail, manufacturing, and energy segments trail but accelerate as AI-enabled inventory, digital twins, and smart meters mature, broadening the Chile ICT market size coverage across industrial use cases.

Geography Analysis

Santiago generated around 65% of Chile ICT market revenue in 2025, reflecting headquarter clustering of banks, ministries, and startups. Valparaíso contributed roughly 15% as port logistics digitalized and universities spun out SaaS ventures, whereas Concepción added 8% on the back of regional procurement and research activity. Northern mining hubs such as Antofagasta deploy industrial IoT at copper pits but still backhaul data 1,200 kilometers to Santiago because edge capacity is scarce, hampering real-time analytics.

Google’s Humboldt cable, live since 2024, delivers 15 Tbps between Valparaíso and California, slicing latency for cloud replication by 30%.[3]Google Cloud Blog, “Humboldt Submarine Cable Operational,” cloud.google.com The planned Southern Cross NEXT landing would further diversify pipes, complementing the National Data Center Plan that targets 300 MW of colocation by 2030 in power-rich Patagonia. Hyperscalers view Patagonia’s sub-USD 30 per MWh renewable tariffs as a magnet for GPU-dense AI clusters, anchoring long-haul fiber backbones to Santiago and Valparaíso corridors.

Ascenty opened its 16 MW SCL03 site in August 2025 and plans USD 1 billion for two more campuses exceeding 150 MW by 2028. TECfusions and Baeza Group intend to break ground on a 100 MW zero-water campus, easing drought pressure in the metropolitan region. Despite these builds, edge facilities outside Santiago lag, delaying low-latency retail analytics and telehealth offerings in secondary cities. Bridging that gap remains pivotal for balanced Chile ICT market growth.

Competitive Landscape

Telecom infrastructure is moderately concentrated. Entel holds 35.8% mobile share, Movistar 19.0%, and Claro 17.8%, together controlling over 72% of subscriptions. Their USD 2.3 billion collective 5G spend since 2022 produced 6.52 million 5G connections by end-2025, yet pricing remains rigid as unlimited data plans aim to curb churn. Claro’s 2024 merger with VTR established a quad-play bundle that pressures rivals to match content and convergence features.

IT services and software are far more fragmented, with no integrator exceeding 12% revenue share. Sonda’s USD 100 million alliance with IBM aligns watsonx analytics with 5,000 Latin American clients, highlighting a pivot from hardware resale to recurring managed services. Accenture bolstered SAP migration depth through local acquisitions, while AWS, Microsoft, and Google offer direct enterprise agreements that undercut reseller margins by up to 30%.

White-space opportunities concentrate in edge computing for autonomous mining, SaaS for SMEs, and managed detection and response for mid-tier companies that lack in-house security staff. Fintech lenders now finance equipment for SMEs at 12-15% annual rates, accelerating device refreshes. Competitive dynamics will hinge on continued spectrum allocations and the enforcement rigor of cybersecurity reporting mandates that raise compliance costs for smaller providers.

Chile ICT Industry Leaders

Entel Chile S.A.

Telefónica Chile S.A. (Movistar)

Claro Chile S.A.

Sonda S.A.

Adexus S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Sonda completed a Tier IV upgrade of its Kudos data center in Santiago and began seeking an external investor to fund regional expansion.

- November 2025: Movistar Chile unveiled a USD 140 million three-year 5G modernization plan covering 5,300 sites to boost urban and semi-rural reach.

- August 2025: Ascenty inaugurated its 16 MW SCL03 facility and announced USD 1 billion for SCL04-05 campuses totaling 150 MW by 2028.

- May 2025: TECfusions and Baeza Group signed a letter of intent to build a 100 MW zero-water data center campus in Santiago.

Chile ICT Market Report Scope

The Chile ICT Market Report is Segmented by Product Type (IT Hardware [Computer Hardware, Networking Equipment, and Peripherals]. IT Software (IT Services [IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, Managed Security Services, and Cloud and Platform Services] IT Infrastructure, IT Security/Cybersecurity, Communication Services), Enterprise Size (Small and Medium-sized Enterprises, and Large Enterprises), and Industry Vertical (Government and Public Administration, BFSI, IT and Telecom, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By Industry Vertical

| Government and Public Administration |

| BFSI |

| IT and Telecom |

| Energy and Utilities |

| Retail, E-commerce, and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas |

| Other Industry Verticals |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Government and Public Administration | |

| BFSI | ||

| IT and Telecom | ||

| Energy and Utilities | ||

| Retail, E-commerce, and Logistics | ||

| Manufacturing and Industry 4.0 | ||

| Healthcare and Life Sciences | ||

| Oil and Gas | ||

| Other Industry Verticals | ||

Key Questions Answered in the Report

How large will Chile ICT spending be in 2031?

The Chile ICT market is forecast to reach USD 28.79 billion by 2031, up from USD 19.27 billion in 2026.

What CAGR is expected for cloud services between 2026 and 2028?

Cloud spending is projected to rise at a 20.3% CAGR from 2026 to 2028 as new AWS and Azure regions come online.

Which product category is growing fastest?

IT security and cybersecurity leads with a projected 9.08% CAGR through 2031, driven by compliance with Law 21.663.

Which customer segment offers the highest growth potential?

Small and medium-sized enterprises are set to expand IT outlays at a 9.82% CAGR thanks to government vouchers and e-commerce momentum.

How concentrated is the telecom sector?

Entel, Movistar, and Claro held 72.6% of mobile subscriptions in 2025, giving the connectivity segment moderate concentration.

What regional factors make Chile attractive for data centers?

Abundant renewable energy in Patagonia, multiple submarine-cable landings, and supportive tax incentives lower operating costs for hyperscale facilities.

Page last updated on: