Chile Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

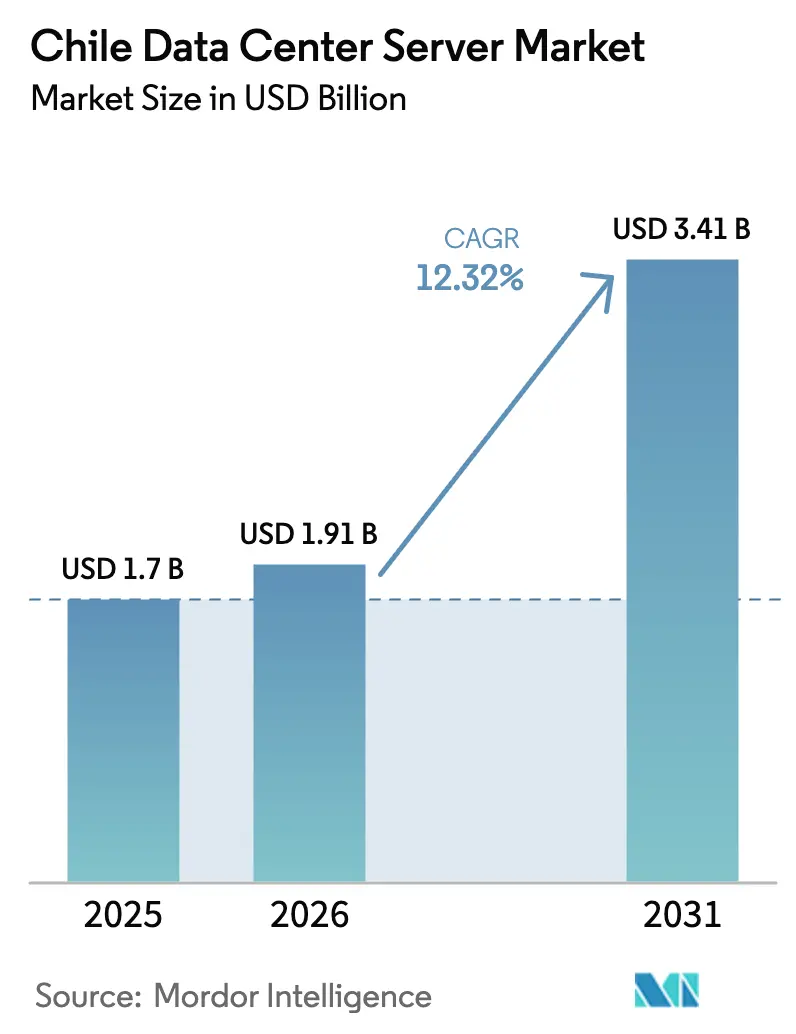

| Base Year Market Size (2025) | USD 1.70 Billion |

| Market Size (2026) | USD 1.91 Billion |

| Market Size (2031) | USD 3.41 Billion |

| Growth Rate (2026 - 2031) | 12.32% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chile Data Center Server Market Analysis by Mordor Intelligence

The Chile Data Center Server market size is expected to grow from USD 1.70 billion in 2025 to USD 1.91 billion in 2026 and is forecast to reach USD 3.41 billion by 2031 at 12.32% CAGR over 2026-2031. Heightened hyperscale spending, rapid enterprise cloud adoption, and a policy push for renewable-powered campuses keep demand on an upward trajectory. Santiago’s strategic role as a subsea cable nexus continues to lower latency, drawing spillover workloads from Brazil and strengthening the country’s regional interconnection profile. Capital-intensive AI and GPU refresh cycles are reshaping server specifications toward higher power densities, while pro-cloud tax incentives shave operating costs and improve return on invested capital. Competitive focus is shifting to cooling innovation because severe water restrictions and the peso’s volatility are testing traditional procurement and operating models.

Key Report Takeaways

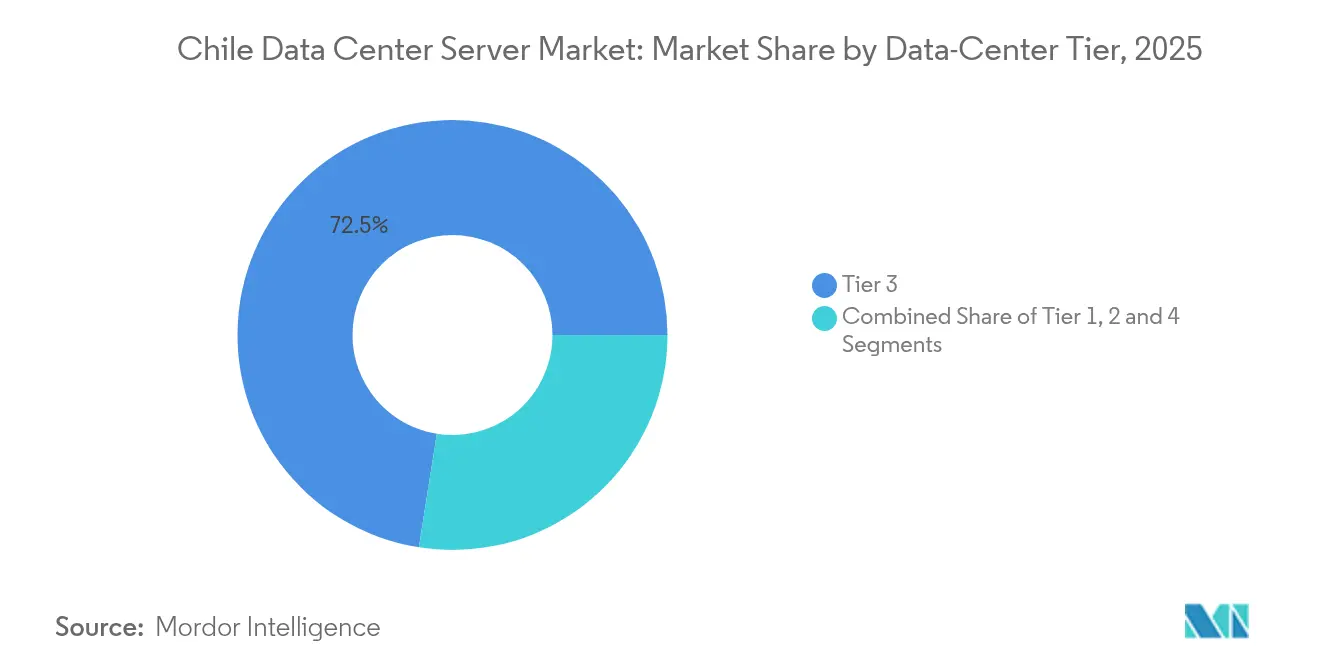

- By data-center tier, Tier 3 led with 72.50% revenue share in 2025; Tier 4 facilities are projected to expand at a 13.42% CAGR through 2031.

- By form factor, half-height blade servers held 61.30% share in 2025, whereas quarter-height and micro-blade configurations are expected to grow at a 13.12% CAGR to 2031.

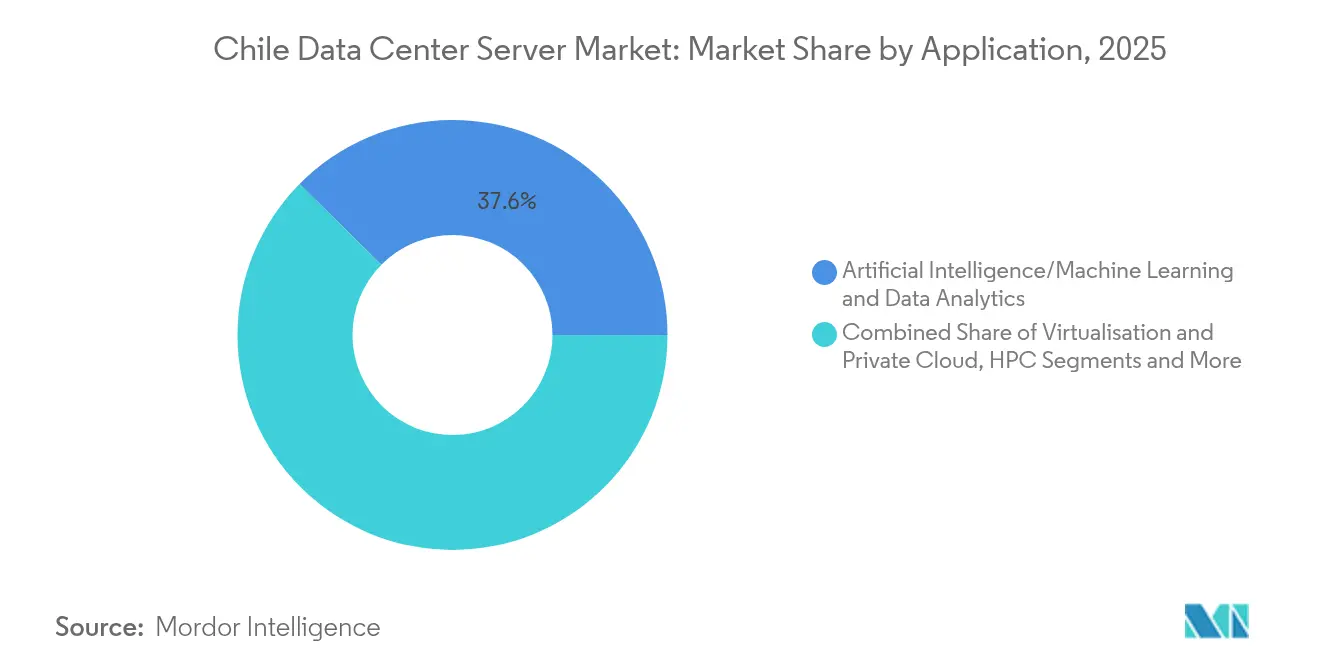

- By application, AI/ML workloads accounted for 37.60% of the Chile Data Center Server market size in 2025 and virtualization and private cloud are advancing at a 12.18% CAGR through 2031.

- By data-center type, colocation captured 54.60% of the Chile Data Center Server market share in 2025 while hyperscale deployments are set to grow at 14.23% CAGR through 2031.

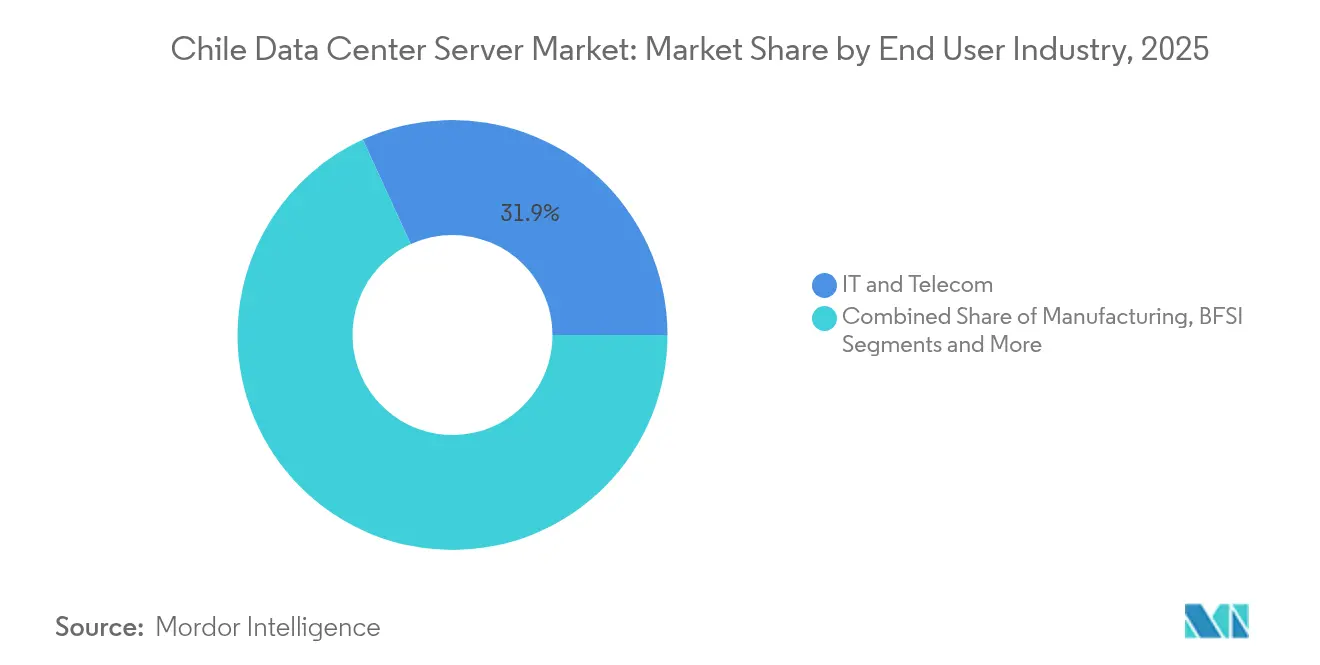

- By end-use industry, IT and telecom held 31.85% share of the Chile Data Center Server market size in 2025 and manufacturing and Industry 4.0 is projected to see 14.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Relative standing becomes clear only when country-level and regional contributions are evaluated alongside one another at a global level. Mordor Intelligence's data center server market share coverage captures this comparative structure.

Chile Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitisation of Chile's BFSI sector fuels hyperscale demand | +2.1% | National, with concentration in Santiago metropolitan area | Medium term (2-4 years) |

| Pro-cloud tax incentives & renewable-energy PPAs cut TCO | +1.8% | National, with early gains in Santiago, Valparaíso, Concepción | Long term (≥ 4 years) |

| Santiago's dense subsea-cable landing points lower latency | +1.5% | Santiago core, spill-over to Valparaíso region | Short term (≤ 2 years) |

| Rapid AI-workload adoption triggers GPU-rich server refresh | +2.3% | National, with enterprise concentration in Santiago | Short term (≤ 2 years) |

| Hyperscale self-build spill-over to local ODM & white-box supply | +1.2% | Santiago, with secondary impact in Concepción | Medium term (2-4 years) |

| Chile's sovereign-cloud mandate for public data residency | +1.4% | National, government sector focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digitization of Chile’s BFSI Sector Fuels Hyperscale Demand

Large banks are accelerating cloud migration and hybrid architectures. Banco de Crédito e Inversiones’ MACH platform now serves more than 3 million users and handles over 100,000 daily transactions using cloud-native back ends. Santander reports 90% of workloads in hybrid cloud, pushing steady demand for Tier 3 and Tier 4 server footprints that guarantee uptime and regulatory compliance. Real-time payment rails increase latency sensitivity and favor local server placement in Santiago. These trends underpin sustained capacity additions by hyperscale and colocation providers courting financial-sector tenants.

Pro-cloud Tax Incentives and Renewable-Energy PPAs Cut TCO

Renewables account for 65% of Chile’s installed generation and power purchase agreements tied to solar and wind unlock 15-20% lifetime cost savings for data-center operators. ENGIE Chile’s USD 650 million pipeline and Enel’s USD 1.8 billion grid upgrade plan bolster the reliability of clean energy inputs. [1]ENGIE."ENGIE Chile comunica al mercado inversiones por cerca de USD 650 millones en desarrollo de energía renovable," engie.clAmazon committed to sourcing 100% of its Chilean load from renewables, reinforcing the link between green policy and infrastructure build-out. These economics strengthen price competitiveness of the Chile Data Center Server market versus fossil-based peers.

Santiago’s Dense Subsea-Cable Landing Points Lower Latency

Multiple Pacific and Atlantic systems converge in Santiago, turning the capital into a gateway for regional and trans-Pacific traffic. Google’s cable projects anchor capacity, and fixed broadband averages 213.73 Mbps nationwide, enabling edge rollouts that require low-latency, high-throughput servers.[2]Google, "Quilicura, Chile - Google Data Center Location," datacenters. googleThe connectivity advantage trims international transit costs by up to 30% and attracts hyperscalers seeking geographic diversity away from saturated Brazilian clusters.

Rapid AI-workload Adoption Triggers GPU-rich Server Refresh

Chile ranks among Latin America’s top AI investment destinations. Enterprises are moving from CPU to GPU stacks that draw 40-140 kW per rack. The Guacolda-Leftraru supercomputer demonstrates local appetite for high-performance compute, processing 47 million DNA sequences for climate research. Limited global GPU supply prompts firms to secure in-country capacity, driving premium pricing for AI-optimized nodes and influencing data-center design toward higher rack densities and advanced cooling.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cyber-attacks push up security & compliance costs | -1.6% | National, with government and financial sectors most affected | Short term (≤ 2 years) |

| Severe water-use restrictions on cooling infrastructure | -2.1% | Santiago core, extending to Valparaíso region | Medium term (2-4 years) |

| Grid-congestion delays for >10 MW campuses in Santiago | -1.3% | Santiago metropolitan area | Medium term (2-4 years) |

| Persistent peso volatility inflates imported server CAPEX | -1.8% | National, affecting all import-dependent operations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-attacks Push Up Security and Compliance Costs

Law 21,663 established the National Cybersecurity Agency in 2025, mandating continuous security management and incident response for essential services.[3]United States Legislative Information,' Chile: Framework Law on Cybersecurity Comes into Force", loc.gov Compliance adds 15-20% to infrastructure budgets through hardware security modules, encrypted storage, and network segmentation. These heightened requirements slow procurement cycles and raise barriers for smaller entrants.

Severe Water-use Restrictions on Cooling Infrastructure

Persistent drought triggered legal scrutiny of water-intensive cooling. Google paused a second Chilean campus after courts questioned environmental assessments. Traditional systems consume nearly 6.8 million gallons per MW annually, pushing operators toward air and liquid cooling that can lift capital outlays by 25-30%. AWS pledged to rely on water for cooling only 4% of the year by employing air and evaporative solutions, signaling a shift to alternative thermal designs that influence server form factors and density ceilings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Tier: Balanced Tier 3 Dominance Meets Tier 4 Acceleration

Tier 3 facilities captured 72.50% of the Chile Data Center Server market in 2025 due to their cost-to-redundancy balance. Financial, government, and telecom tenants prefer 99.982% availability without the complexity of fully fault-tolerant designs. The Chile Data Center Server market size for Tier 3 deployments is projected to expand steadily alongside hybrid cloud adoption schedules.

Tier 4 is the fastest-growing slice at a 13.42% CAGR through 2031 as mandatory cybersecurity rules elevate uptime expectations for essential services. Newly tendered government workloads and AI-rich banking applications require multi-path power and cooling. These conditions position Tier 4 providers to command premium pricing, particularly in Santiago, where land scarcity favors vertically integrated, high-density footprints.

Chile’s cybersecurity framework accelerates Tier 4 conversions within banking and defense. Local lenders deploying real-time fraud detection cannot tolerate unplanned downtime, so they budget for dual active-active sites. Meanwhile, Tier 1 and Tier 2 sites serve as edge and backup locations in secondary cities where grid upgrades lag. The Chile Data Center Server industry therefore shows a clear two-tier investment pattern: cost-efficient regional nodes and capital-intensive primary hubs.

By Form Factor: Half-height Leadership Challenged by Micro-blade Innovation

Half-height blades maintained 61.30% share in 2025 as operators leveraged legacy procurement cycles and homogeneous fleet management. Density pressure is changing that equation. Quarter-height and micro-blade systems are growing at 13.12% CAGR as operators re-rack to fit more cores per square meter.

Blade shipments overall are declining worldwide, yet Chile’s land and water constraints inject renewed interest in ultra-compact, energy-efficient designs. Micro-blade platforms enable 40-50% higher compute density per rack, a critical metric in premium Santiago real estate. They also align with direct-to-chip liquid cooling retrofits that mitigate evaporative water use. The Chile Data Center Server market is therefore pivoting to modular blades that lower vendor lock-in and improve thermal performance.

By Application/Workload: AI/ML Surge Drives Infrastructure Evolution

AI/ML workloads accounted for 37.60% of the Chile Data Center Server market in 2025, a testament to surging GPU demand in mining, banking, and public-sector analytics. GPU clusters require up to 10 times the power envelope of legacy virtual machines and force operators to adopt higher rack densities and liquid cooling.

Virtualization and private cloud stacks are projected to grow at 12.18% CAGR as enterprises modernize legacy x86 estates to migrate toward container architectures. Edge analytics in mining and smart-grid rollouts drive new demand for hybrid nodes that handle both inference and training tasks. Consequently, the Chile Data Center Server market size tied to AI workloads is expected to widen its lead, but virtualization will supply a stable revenue floor.

By Data-Center Type: Colocation Strength Faces Hyperscale Expansion

Colocation facilities controlled 54.60% of the Chile Data Center Server market share in 2025, reflecting enterprises’ preference for physical control within professionally managed sites. Colocation partners provide compliance visibility and sovereign data assurances that remain important under new privacy statutes.

Hyperscale clouds, led by Amazon’s USD 4 billion region, represent the fastest growth at 14.23% CAGR. Their expansion introduces ready-made GPU capacity and offsets the capital burden for tenants migrating seasonal workloads. Hybrid architectures emerge as a de-facto standard, blending colocation resilience for sensitive data with hyperscale elasticity. This interplay deepens the Chile Data Center Server market’s service diversity and intensifies competition for network interconnect revenue.

By End-use Industry: IT/Telecom Leads, Manufacturing Accelerates

IT and telecom players held 31.85% of 2025 revenue, fueled by nationwide fiber rollouts, 5G densification, and content delivery caching. Their server demand centers on network function virtualization and customer experience analytics.

Manufacturing and Industry 4.0 workloads post the fastest 14.95% CAGR as copper-mining majors and process industries deploy machine-learning loops to boost yield and energy efficiency. Smart grid pilots in the utilities sector add edge computing demand, rounding out a broadening client base that underpins the Chile Data Center Server market’s resilience.

Geography Analysis

Santiago is supported by dense subsea cables, government presence, and the largest pool of skilled labor. The city’s renewable-ready grid underpins large campuses, yet water scarcity and grid congestion above 10 MW are emerging bottlenecks. Investors are responding with air-cooled and liquid-cooling retrofits designed for higher inlet temperatures.

Valparaíso and Concepción policymakers push to decentralize and reduce systemic risk concentrated in the capital. The National Data Centres Plan fast-tracks renewable hookups and simplifies permits in these regions. ENGIE Chile’s solar clusters supply competitive power that attracts midsized colocation builds targeting regional enterprises.

Northern zones around Antofagasta and the Atacama Desert offer vast solar capacity and lower land costs, appealing to future hyperscale AI and HPC farms able to tolerate higher latency. Early projects explore direct-to-chip liquid cooling married to on-site photovoltaic capacity. Southern provinces remain niche, serving disaster-recovery and content caching use cases where moderate climate lowers cooling costs.

Analysis of the data center server market by Mordor Intelligence spans multiple other regional evaluations across Americas, North America, and Europe, supported by country-level insights for United States, Brazil, Sweden, Norway, Philippines, and Singapore, wherein local market conditions keep varying from one country to another.

Competitive Landscape

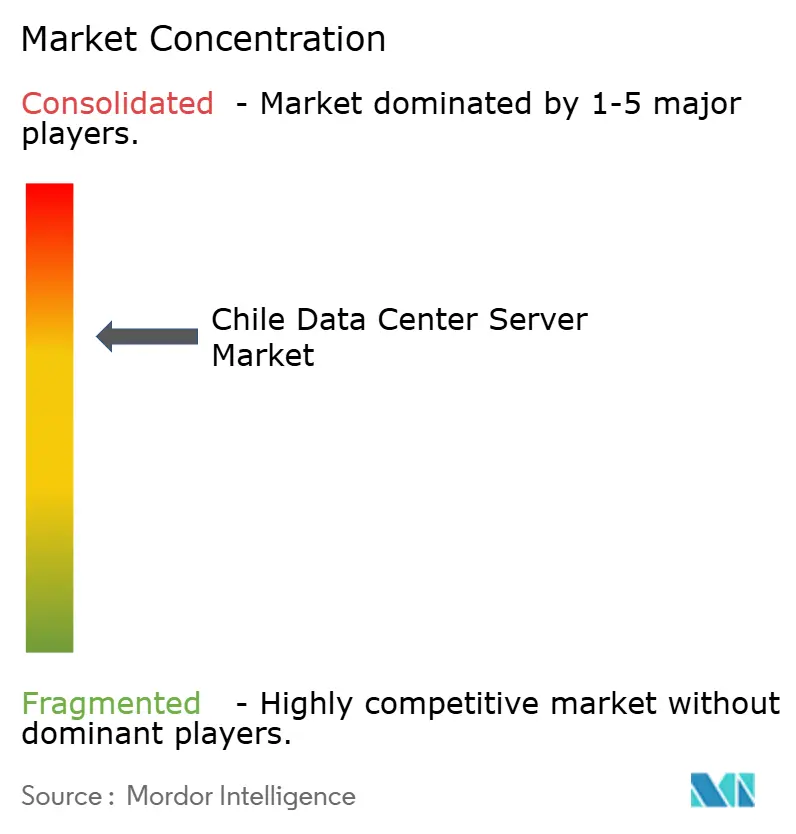

The Chile Data Center Server market shows moderate concentration. Global OEMs such as Dell Technologies, Hewlett-Packard Enterprise, and Lenovo control a large share through direct sales and channel partners that manage import logistics and peso hedging. Local value-added resellers specialize in compliance integration and post-deploy support, adding stickiness for domestic clients.

Competitive advantage now rests on energy and cooling efficiency as electricity represents more than 60% of lifetime TCO in GPU-rich racks. Vendors that certify hardware for direct liquid cooling and outer-shell immersion gain mindshare with operators contending with water quotas. AWS, Google, and Microsoft emphasize power-usage-effectiveness below 1.2 and 100% renewable guarantees, raising the standard for smaller rivals.

Edge opportunities in mining, smart grids, and remote manufacturing open space for modular micro-data-center suppliers and ODM white-box providers. Scala Data Centers and Cirion evaluate regional edge nodes that bring GPU capacity closer to industrial sites, further fracturing traditional supply chains and seeding next-generation sales channels for AI-ready servers.

Chile Data Center Server Industry Leaders

-

Dell Technologies

-

Hewlett Packard Enterprise

-

Lenovo Group

-

Cisco Systems

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amazon Web Services confirmed a USD 4 billion commitment to launch a multi-availability-zone region in Santiago, operational in the second half of 2026

- March 2025: Sonda outlined a USD 5.4 billion regional portfolio with Chile as a core growth pillar, targeting end-to-end digital transformation services

- January 2025: Cybersecurity Framework Law 21,663 took effect, creating the National Cybersecurity Agency and setting mandatory security baselines for data-center operators.

- December 2024: Chile aligned its privacy regime with GDPR by adopting a new Data Protection Law establishing the Personal Data Protection Agency, effective December 2026

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Chile data center server market as the annual US-dollar value of new rack, blade, micro-blade, and purpose-built AI servers installed in enterprise, colocation, and hyperscale facilities located within Chile. Values reflect vendor invoice price converted at the average interbank rate of each calendar year.

Scope Exclusion: Refurbished hardware, storage-only enclosures, and public-cloud managed services fall outside this scope.

Segmentation Overview

-

By Data-Center Tier

- Tier 1 and 2

- Tier 3

- Tier 4

-

By Form Factor

- Half-height Blades

- Full-height Blades

- Quarter-height / Micro-blades

-

By Application / Workload

- Virtualisation and Private Cloud

- High-Performance Computing (HPC)

- Artificial Intelligence/Machine Learning and Data Analytics

- Storage-centric

- Edge / IoT Gateways

-

By Data Center Type

- Hyperscalers/Cloud Service Provider

- Colocation Facilities

- Enterprise and Edge

-

By End-use Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Manufacturing and Industry 4.0

- Energy and Utilities

- Government and Defence

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews with operators in Santiago, Paine, and Antofagasta, plus surveys of regional server distributors, supplied utilization rates, refresh cadence, and GPU attach ratios that desk work could not capture. This allowed us to tighten assumptions and validate preliminary totals.

Desk Research

We combined public datasets such as Banco Central import statistics, Servicio Nacional de Aduanas HS 8471 shipment records, Ministry of Energy power-consumption bulletins, and Santiago stock-exchange filings to build an initial volume and price baseline.

We then mined international sources; for example, ITU broadband data, UN Comtrade trade flows, and peer-reviewed IEEE papers on liquid cooling, together with proprietary feeds from D&B Hoovers and Dow Jones Factiva, to cross-check shipment counts, average selling prices, and facility expansions.

The sources named illustrate only a part of the material consulted.

Market-Sizing & Forecasting

The 2025 base value is modeled with a top-down import reconstruct anchored on HS 8471 arrivals, adjusted for re-exports, and corroborated with selective bottom-up supplier roll-ups and channel checks.

Key variables include rack density (kW per rack), GPU share, peso-USD volatility, and national AI workload growth.

Forecasts apply multivariate regression on 2014-2024 series, blended with scenario weightings from primary experts. Gaps in bottom-up evidence are bridged through price-volume proxies from comparable Latin markets.

Data Validation & Update Cycle

Model outputs face variance scans against energy demand indicators and currency shocks before senior analyst sign-off.

Mordor reports refresh each year, with interim updates triggered by material events such as a double-digit peso shift or a major hyperscale build announcement.

Why Mordor's Chile Data Center Server Baseline Earns Confidence

Published estimates often diverge because firms choose different hardware sets, currency bases, and refresh cadences. Users therefore encounter noticeably different 2025 numbers.

Most gaps arise when other studies exclude AI accelerators, ignore hyperscale self-builds, or freeze average selling prices, whereas Mordor Intelligence folds each element into a quarterly reviewed framework.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.70 B (2025) | Mordor Intelligence | - |

| USD 1.53 B (2024) | Global Consultancy A | Omits GPU-rich edge nodes, counts vendor shipment revenue only |

| USD 1.51 B (2025) | Industry Association B | Uses constant peso basis, excludes hyperscale self-build volumes |

| USD 0.20 B (2025) | Regional Consultancy C | Survey limited to three data centers and short refresh window |

The comparison shows that once scope breadth, currency handling, and update frequency are normalized, Mordor's balanced, clearly documented approach delivers the most dependable baseline for decision makers.

Key Questions Answered in the Report

What is the current value of the Chile Data Center Server market?

The market stands at USD 1.91 billion in 2026 and is projected to reach USD 3.41 billion by 2031.

Which data-center tier dominates server demand in Chile?

Tier 3 facilities lead with 72.50% share in 2025, reflecting a balance of redundancy and cost efficiency.

How fast is hyperscale capacity growing in Chile?

Hyperscale deployments are forecast to expand at a 14.23% CAGR through 2031, driven by Amazon’s USD 4 billion region investment.

Why are AI workloads reshaping server purchases?

GPU-rich AI and ML applications already account for 37.60% of market revenue and require higher power densities and advanced cooling.

Page last updated on: