Chile Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

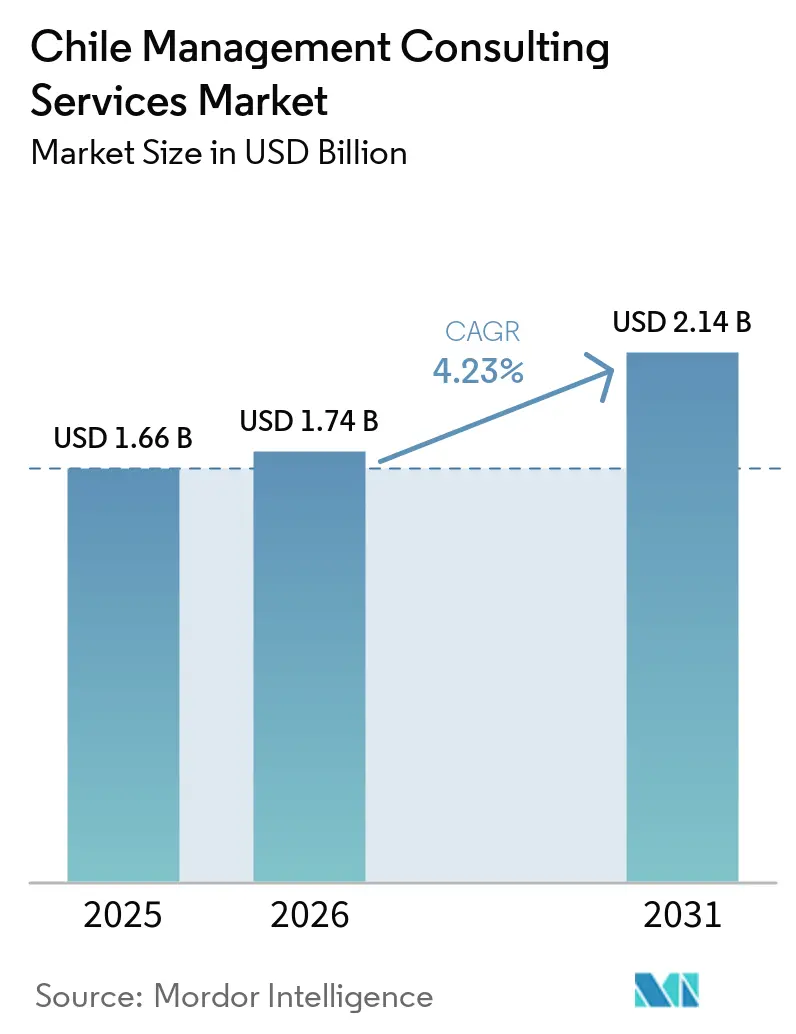

| Base Year Market Size (2025) | USD 1.66 Billion |

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.14 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

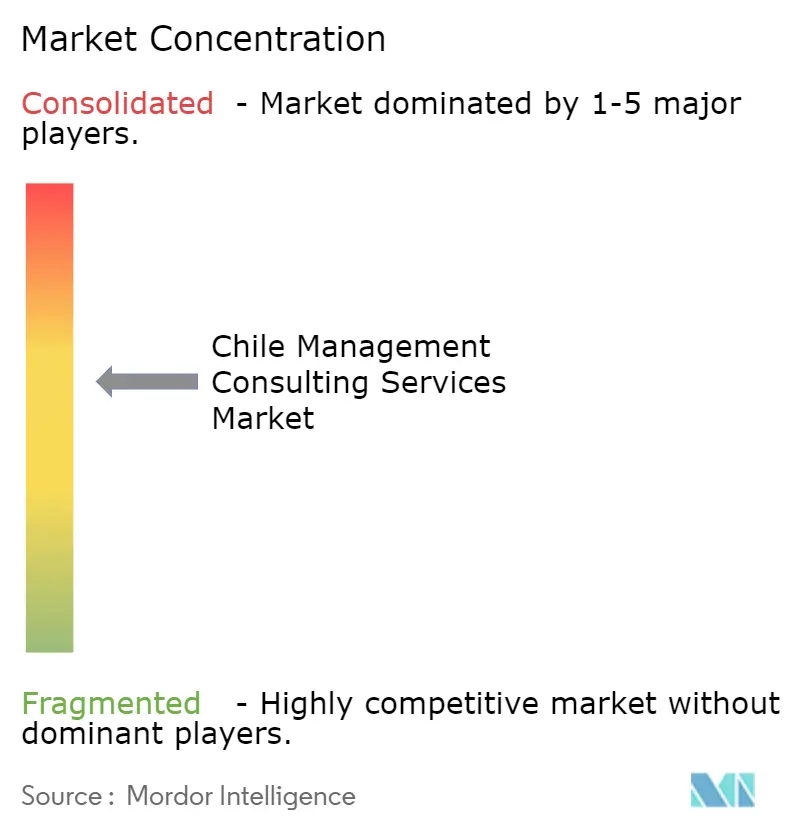

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Management Consulting Services Market Analysis by Mordor Intelligence

The Chile Management Consulting Services Market size is projected to be USD 1.66 billion in 2025, USD 1.74 billion in 2026, and reach USD 2.14 billion by 2031, growing at a CAGR of 4.23% from 2026 to 2031. Advisory demand is shifting from discretionary digital-transformation work toward mandatory governance programs as new criminal-liability, fintech, and anti-money-laundering rules reset compliance deadlines. Enterprises are also rebalancing delivery models, blending remote diagnostics with targeted on-site workshops to control travel spend without sacrificing executive facilitation. SMEs are entering the Chile management consulting services market more aggressively because government co-investment reduces project-failure risk, while the lithium value-chain expansion is opening white-space opportunities in sustainability and community-engagement consulting. Talent scarcity, especially of bilingual consultants, is inflating labor costs and reinforcing the appeal of hybrid engagement models that pool senior expertise across borders.

Key Report Takeaways

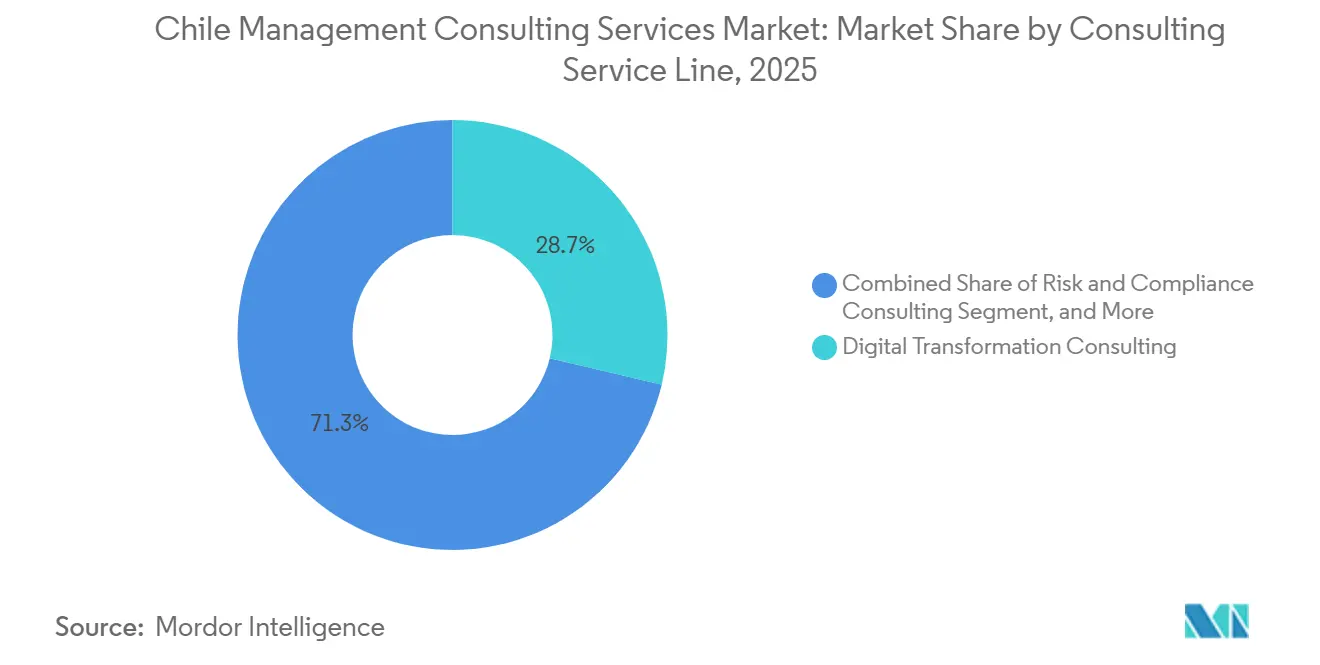

- By consulting service line, digital transformation consulting led with 28.72% revenue share in 2025, while risk and compliance consulting is poised to grow at a 4.53% CAGR through 2031.

- By organization size, large enterprises commanded 62.81% spending in 2025, whereas SMEs are forecast to expand at a 4.31% CAGR to 2031.

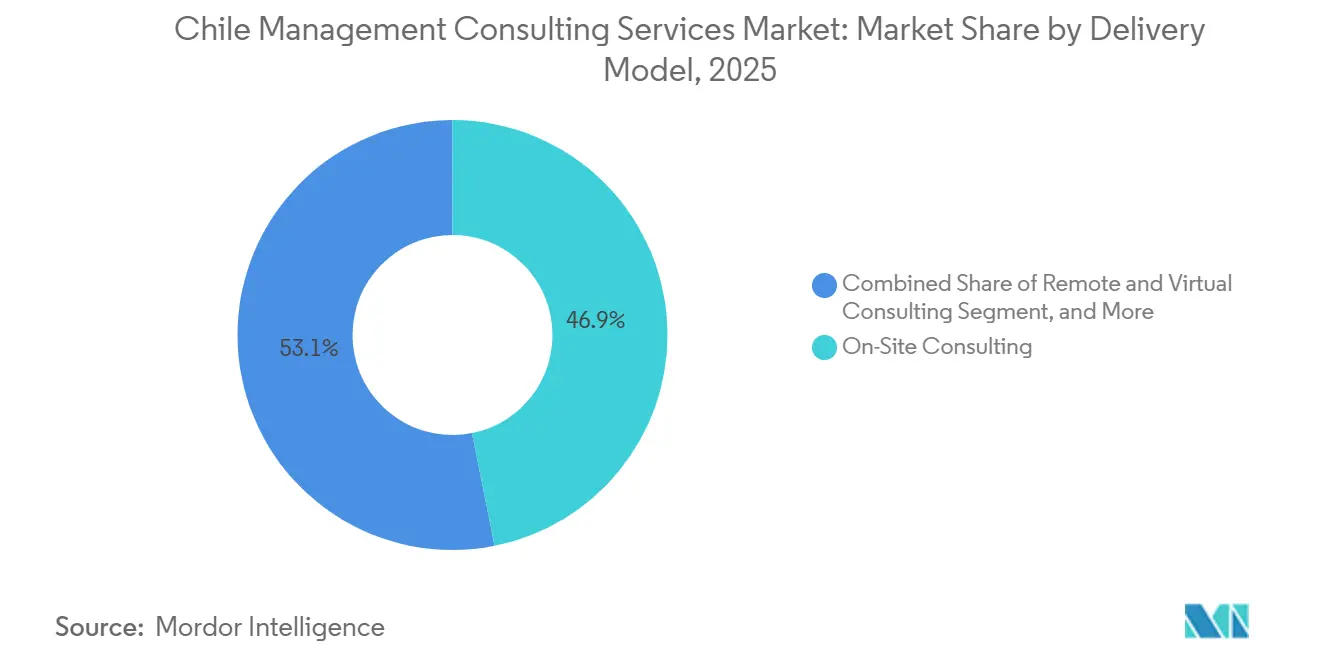

- By delivery model, on-site consulting contributed 46.87% of 2025 revenue, yet hybrid consulting will advance at a 4.64% CAGR during the outlook period.

- By end user industry, banking and insurance generated 19.48% of 2025 demand, while healthcare is projected to rise at a 4.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation Initiatives Among Chilean Enterprises | +0.9% | National, early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Growing Adoption of Cloud and Emerging Technologies | +0.7% | National, concentrated in Santiago Metropolitan Region | Medium term (2-4 years) |

| Chile's Upcoming Fintech Law Driving Regulatory Advisory Demand | +0.6% | National, concentrated in Santiago financial district | Short term (≤ 2 years) |

| Post-Pandemic Corporate Restructuring and Cost Optimization | +0.5% | National | Short term (≤ 2 years) |

| Lithium Industry Expansion Creating Sustainability Consulting Needs | +0.4% | Atacama, Antofagasta, spillover to Santiago | Long term (≥ 4 years) |

| Rise of Family-Owned SMEs Seeking Succession-Planning Expertise | +0.3% | National, nodes in Santiago, Viña del Mar, Concepción | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Initiatives Among Chilean Enterprises

Enterprises are accelerating end-to-end modernization to offset margin pressure and regulatory complexity. Codelco partnered with Schneider Electric in 2025 to introduce digital-twin analytics and predictive maintenance across mine sites, illustrating how operational imperatives translate into multi-year consulting roadmaps.[1]Codelco, “Codelco and Schneider Electric Partnership,” codelco.com Government programs such as Chequeo Digital are benchmarking agency maturity, channeling public budgets toward ministries that can demonstrate transformation readiness. UNESCO’s 2025 analysis of Chilean education adds that technology roll-outs must pair with organizational-change plans, expanding the advisory mandate beyond IT configuration. Forestry SMEs in southern regions adopted cloud supply-chain tools to satisfy European traceability rules, signaling that compliance pressure is pushing modernization even in resource sectors with limited internal IT capacity. Collectively, these factors turn digital execution skills into a baseline requirement across the Chile management consulting services market.

Growing Adoption of Cloud and Emerging Technologies

Chile leads South America in cloud-infrastructure readiness, yet Bain found a sizable execution gap in generative-AI deployments, creating advisory headroom to convert infrastructure availability into business value.[2]Bain and Company, “Chile Generative AI Implementation Study,” bain.com KPMG Chile’s Control AI fraud-detection suite exemplifies how firms are productizing analytics capabilities to win recurring revenues. Accenture research shows banks must integrate AI across credit, service, and risk workflows to counter digital-native challengers such as Tenpo. The 2024 cybersecurity law mandates incident-reporting and zero-trust architecture, driving risk-assessment engagements across regions. Early 5G rollout enables edge-analytics pilots in mining and logistics, but qualified consultants remain scarce outside Santiago, elevating fees for firms with verified use-case experience.

Chile's Upcoming Fintech Law Driving Regulatory Advisory Demand

The fintech bill, slated for mid-2026 enactment, formalizes licensing for digital lenders, payment platforms, and crypto exchanges. CMF’s Norma 559 in 2025 required regulated entities to harden cybersecurity and vendor-risk controls, sparking immediate gap-assessment contracts.[3]Comisión para el Mercado Financiero, “Norma de Carácter General 559,” cmfchile.cl EY forecasts that open-finance will obligate banks to redesign core systems and API gateways, blending compliance with architecture redesign. DLA Piper expanded its white-collar practice with a senior compliance partner, signaling legal-consulting convergence. The Financial Analysis Unit’s March 2025 rules compel diverse sectors to appoint compliance officers, compressing timelines for smaller players that now outsource program design. Vendors able to couple regulatory insight with technology execution will dominate engagements as the Chile management consulting services market pivots toward mandatory governance.

Post-Pandemic Corporate Restructuring and Cost Optimization

Margin compression and liquidity stress continue to propel restructuring engagements. EY advised clients on tax-neutral mergers under Chile’s reorganization framework, differentiating full-service advisories from boutiques. Mid-market specialist Reset Chile reported higher demand for debt renegotiation as copper volatility constrained cash flow, broadening the advisory mix beyond growth strategy. A Chambers guide recorded a fall in large-cap M&A but a rise in bolt-on deals that still need due-diligence and synergy-capture expertise.[4]Chambers and Partners, “Chile M&A Guide 2024,” chambers.com Pending labor-law reforms are prompting multinational subsidiaries to revisit workforce strategies, opening lanes for HR and change-management consulting. Firms that demonstrate measurable cost-savings and stakeholder-alignment frameworks preserve pricing power despite client budget vigilance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper-Price-Linked Economic Volatility Curbing Discretionary Spend | -0.6% | National, acute in mining and utilities | Short term (≤ 2 years) |

| Intensifying Competition From In-House Strategy Teams | -0.4% | National, centered in Santiago multinationals | Medium term (2-4 years) |

| Scarcity of Bilingual Consultants Limiting High-End Delivery | -0.3% | National, most severe in Santiago | Long term (≥ 4 years) |

| Public Scrutiny of Government Consulting Contracts | -0.2% | National, focused on central procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Copper-Price-Linked Economic Volatility Curbing Discretionary Spend

Copper generated roughly half of Chile’s export revenue in 2025, and prices swung between USD 8,000 and USD 10,000 per metric ton, squeezing investment budgets in mining, utilities, and public agencies. Lower ore grades and water scarcity further dampened production growth, prompting enterprises to defer transformation projects or re-scope engagements toward cost-reduction. Because fiscal policy is tied to structural balance adjusted for copper cycles, public-sector consulting outlays contract in tandem, heightening cyclicality. Political uncertainty surrounding constitutional reforms compounds hesitation, as boards delay big-ticket initiatives until regulatory clarity emerges. Firms diversified into counter-cyclical sectors such as healthcare and financial services mitigate volatility risk better than peers concentrated in extractives.

Intensifying Competition From In-House Strategy Teams

Large corporates are hiring former Big Four and strategy-firm alumni to lead continuous transformation, lowering reliance on external advisors for routine diagnostics. Banking, retail, and telecom players reserve external budgets for specialized compliance or vendor-selection mandates, which compresses scope and margins. Mid-tier consultancies respond with staff-augmentation models, but that approach blurs value differentiation and invites pricing pressure. The trend accelerates as experienced consultants pursue corporate roles offering equity and better work-life balance. Firms must counter by showcasing proprietary benchmarks, sector playbooks, and outcome-based contracts to preserve fee integrity within the Chile management consulting services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Compliance Overtakes Transformation as Regulatory Deadlines Loom

Risk and compliance consulting is forecast to post the fastest 4.53% CAGR, while digital transformation consulting still held 28.72% of the Chile management consulting services market share in 2025. The shift is driven by Law 21,595’s criminal-liability expansion and stricter anti-money-laundering rules that force enterprises to implement prevention models quickly. Strategy consulting remains a board-level staple but faces shorter engagement cycles as clients demand rapid insights. Operations consulting benefits from mining and manufacturing clients needing asset-utilization boosts, exemplified by SQM’s excellence program advised by McKinsey. HR advisory expands amid labor-reform uncertainty, with Deloitte deploying virtual innovation labs to accelerate workforce diagnostics. Firms that integrate compliance tooling, process redesign, and digital enablers into single workstreams secure longer retainers and a larger slice of the Chile management consulting services market.

The Chile management consulting services market size for risk and compliance assignments is set to grow consistently through 2031 as prevention-model design, audit readiness, and technology-enabled monitoring become recurring mandates. Digital transformation work will increasingly fold into broader regulatory or efficiency agendas, sustaining demand but diluting pure-play program size. Hybrid delivery lowers cost barriers, enabling mid-market companies to procure service-line bundles. Over the forecast horizon, consultancies that pair regulatory fluency with cloud or analytics accelerators will outpace traditional strategy shops confined to slide-ware deliverables.

By Organization Size: SMEs Unlock Growth as Public Programs De-Risk Advisory Spend

Large enterprises contributed 62.81% of 2025 spending, reflecting complex cross-border needs and sizable technology budgets. Yet SMEs are projected to expand at 4.31% annually, fueled by CORFO’s Fortalece Pyme grants that subsidize diagnostic and implementation phase.[5]Asociación de Emprendedores de Chile, “CORFO Fortalece Pyme Program,” asech.cl BancoEstado green-financing earmarks for small firms require technical advisory to validate carbon-reduction paybacks, stirring demand for environmental consultants. Roughly half of family-owned companies still lack documented succession plans, elevating governance advisory for directors seeking institutional longevity.

As hybrid models scale, consultancies can deliver template-based diagnostics remotely, lowering SME entry costs and broadening the Chile management consulting services market size at the lower end. Large enterprises, meanwhile, will continue to award multi-year digital-core modernization and compliance programs, sustaining absolute revenue leadership. Balanced portfolios that couple high-margin strategic accounts with scalable SME offerings will outperform single-segment plays.

By Delivery Model: Hybrid Consulting Captures Post-Pandemic Efficiency Gains

On-site work captured 46.87% revenue in 2025, anchored by executive workshops and go-live support. However, hybrid models are growing at 4.64% CAGR as clients favor remote data analysis, reserving travel for critical touchpoints. NobleProg demonstrates the model’s traction by marketing remote collaboration consulting with periodic in-person sprints. Scarcity of bilingual talent further encourages distributed staffing, allowing firms to deploy senior English-speaking experts from regional hubs while fielding local teams for stakeholder management.

Hybrid engagement unlocks margin by trimming per-diem spend and accelerates cycle time with always-on virtual collaboration. As video platforms and agile tooling mature, the Chile management consulting services market will treat hybrid capability as hygiene. Firms that invest in virtual-facilitation skills and security-certified collaboration stacks will command premium positioning.

By End User Industry: Healthcare Surges on Digital-Health Blueprint

Banking and insurance dominated 19.48% of 2025 demand, propelled by open-finance, fintech licensing, and cybersecurity compliance. Healthcare will register a 4.42% CAGR through 2031, driven by the proposed Servicio Nacional de Salud Digital and strengthened Superintendencia de Salud oversight, both demanding process re-engineering and change management that many providers lack internally. Energy, resources, and manufacturing sustain transformation pipelines tied to automation and sustainability, illustrated by Entel Digital’s 2026 IoT partnership with VOGT.

Public-sector digital programs, such as SONDA’s Software Factory contracts, underscore government appetite for modernization despite procurement scrutiny. Across industries, regulatory convergence, technology refresh cycles, and operational resilience imperatives intertwine, expanding cross-functional engagement scopes within the Chile management consulting services market.

Geography Analysis

Santiago Metropolitan Region retains the lion’s share of Chile management consulting services market demand, concentrating financial institutions, corporate headquarters, and ministries that anchor large transformation budgets. Valparaíso and Concepción form secondary nodes linked to port logistics, academia, and regional manufacturing, yet their combined market share remains modest relative to the capital. Northern regions Atacama and Antofagasta are emerging hotspots for sustainability and community-engagement consulting as lithium and copper projects scale, typified by the SQM-Codelco joint venture to produce 300,000 tons annually.

Chile’s first-in-region 5G network and robust cloud infrastructure position it as a South America sandbox for edge analytics and Industry 4.0 pilots, but Bain research notes a lag in generative-AI adoption, leaving room for advisory firms to translate infrastructure into value. Government programs such as Chequeo Digital channel budgets across regions by benchmarking agency readiness, so consultants with proven public-sector methodologies can diversify away from Santiago concentration. The 2024 cybersecurity law applies nationwide, pushing risk-assessment and zero-trust design engagements beyond the capital.

Nonetheless, talent availability and client decision-maker proximity keep most delivery capacity anchored in Santiago. Hybrid models mitigate travel overhead, yet mining and agriculture clients still prefer periodic on-site presence for community-relations or asset-critical stages. Consultancies balancing centralized expertise with regional field teams will capture share as the Chile management consulting services market deepens outside the capital.

Competitive Landscape

Global brands, McKinsey, Boston Consulting Group, Bain, Deloitte, PwC, EY, KPMG, Accenture, dominate board-level strategy and large public-sector mandates through brand equity and cross-border delivery capacity. Indigenous integrators such as SONDA, everis Chile, and Matrix Consulting leverage regulatory fluency, Spanish-first teams, and price flexibility to win implementation-heavy projects. SONDA ended 2025 with USD 1.59 billion revenue and a USD 6.4 billion pipeline, including Investigative Police and Internal Revenue Service digitalization contracts that highlight local players’ traction in mission-critical government work.

Strategic differentiation revolves around sector specialization and technology-enabled assets. KPMG markets a mining transformation practice, while Deloitte’s HR labs blend analytics with virtual collaboration. Legal-consulting hybrids, notably DLA Piper Chile and Anguita Osorio, are capturing compliance and cybersecurity advisory by bundling legal insight with process design. Emerging niches include sustainability for lithium extraction, succession planning for family SMEs, and fintech compliance tooling.

Bilingual-talent scarcity raises delivery costs, so firms deploy regional virtual hubs to pool expertise, reinforcing the rise of hybrid engagement. Vendors that codify proprietary methods into toolkits and secure technology-vendor alliances will sustain pricing power in the Chile management consulting services market despite client push to internalize routine strategy work.

Chile Management Consulting Services Industry Leaders

McKinsey and Company

Boston Consulting Group, Inc.

Bain and Company, Inc.

Deloitte Consulting LLP

PricewaterhouseCoopers Advisory Services LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SONDA flagged a USD 6.06 billion regional project pipeline, including Software Factory, health-network modernization, and mining-communications contracts, signaling robust demand for digital public-infrastructure projects.

- January 2026: ChileCompra’s Observatorio flagged 1,131 purchase orders worth CLP 3,452 million (USD 3.6 million) for potential conflicts, intensifying scrutiny on public-sector consulting awards.

- January 2026: Entel Digital partnered with VOGT to deliver IoT connectivity and analytics for industrial processes, bundling advisory with infrastructure services.

- January 2026: SONDA reported USD 1.59 billion 2025 revenue and early-2026 wins for FONASA’s MCC platform and Teleférico Bicentenario payment systems, underscoring momentum in government digitalization.

Chile Management Consulting Services Market Report Scope

The Chile Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Chile management consulting services market?

The Chile management consulting services market size was USD 1.66 billion in 2025 and is projected to reach USD 2.14 billion by 2031.

Which consulting service line is expanding the fastest?

Risk and compliance consulting is expected to deliver the highest 4.53% CAGR through 2031 as new laws intensify governance obligations.

How are SMEs influencing demand for advisory work?

Government-backed programs such as CORFO's Fortalece Pyme grants reduce project risk, allowing SMEs to increase consulting spend and record a 4.31% annual growth rate.

Why are hybrid consulting models gaining traction in Chile?

Clients are optimizing cost and speed by using remote diagnostics for data work and reserving on-site sessions for pivotal workshops, allowing hybrid engagements to post a 4.64% CAGR.

Which industries will drive new consulting opportunities beyond banking?

Healthcare, mining-linked sustainability, and public-sector digitalization are generating multi-year pipelines thanks to reform initiatives and strategic infrastructure projects.

How is copper price volatility affecting consulting budgets?

Fluctuating copper revenues lead mining and utilities clients to defer discretionary projects during downturns, shifting advisory focus toward cost optimization and resilience planning.

Page last updated on: