Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

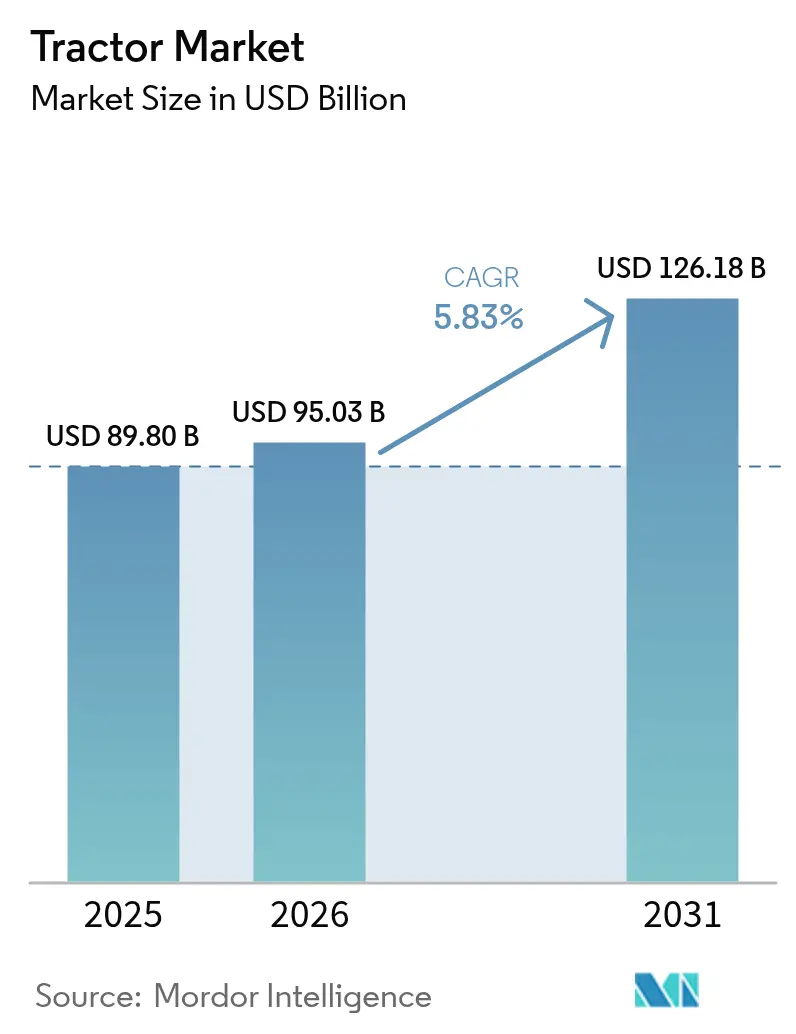

| Market Size (2026) | USD 95.03 Billion |

| Market Size (2031) | USD 126.18 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

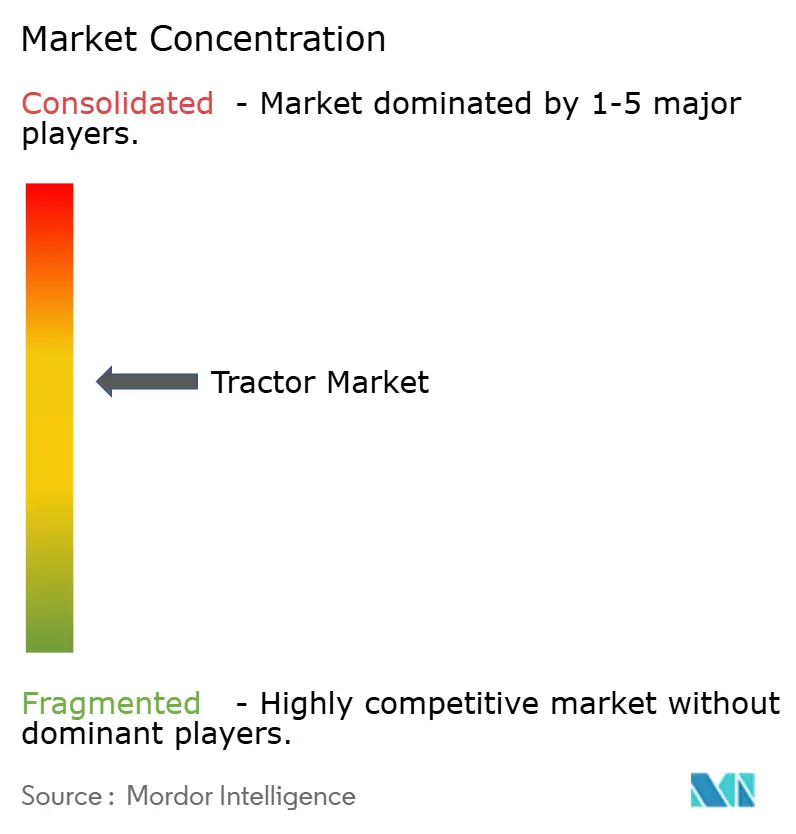

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tractor Market Analysis by Mordor Intelligence

Tractor market size in 2026 is estimated at USD 95.03 billion, growing from 2025 value of USD 89.8 billion with 2031 projections showing USD 126.18 billion, growing at 5.83% CAGR over 2026-2031. A confluence of mechanization demand in emerging economies, rapid precision-ag adoption, and expanding rental models underpins this steady rise. Asia-Pacific dominates volume, while South America records the fastest regional growth, reflecting divergent maturity curves. Power segmentation trends favor 40-100 HP for versatility, yet demand for above-100 HP machines accelerates as farms consolidate. Drive-type choices still lean toward cost-efficient 2WD, but 4WD gains ground where terrain dictates higher traction and data-driven practices require consistent wheel-slip control. Diesel propulsion remains the workhorse, although electric variants are scaling quickly as battery density improves and decarbonization rules tighten.

Key Report Takeaways

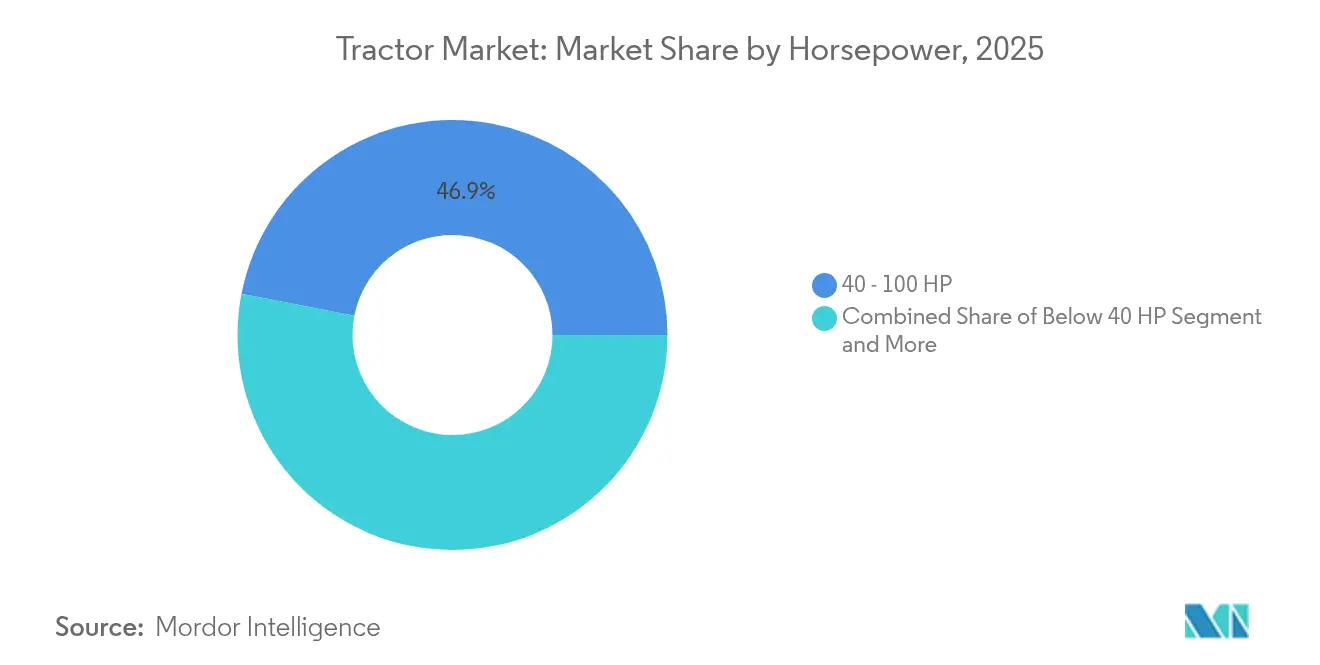

- By horsepower, the 40-100 HP class captured 46.93% of global tractor market share in 2025, while above-100 HP units are projected to expand at a 7.16% CAGR through 2031.

- By drive type, 2WD commanded 77.10% revenue share in 2025; 4WD is forecast to post the fastest growth at 7.69% CAGR to 2031.

- By propulsion, diesel engines represented 90.25% of the global tractor market size in 2025, whereas battery-electric platforms are advancing at a 9.05% CAGR during the forecast period (2026-2031).

- By application, agriculture accounted for 88.87% share in 2025, while construction demand is projected to rise at a 7.31% CAGR through 2031.

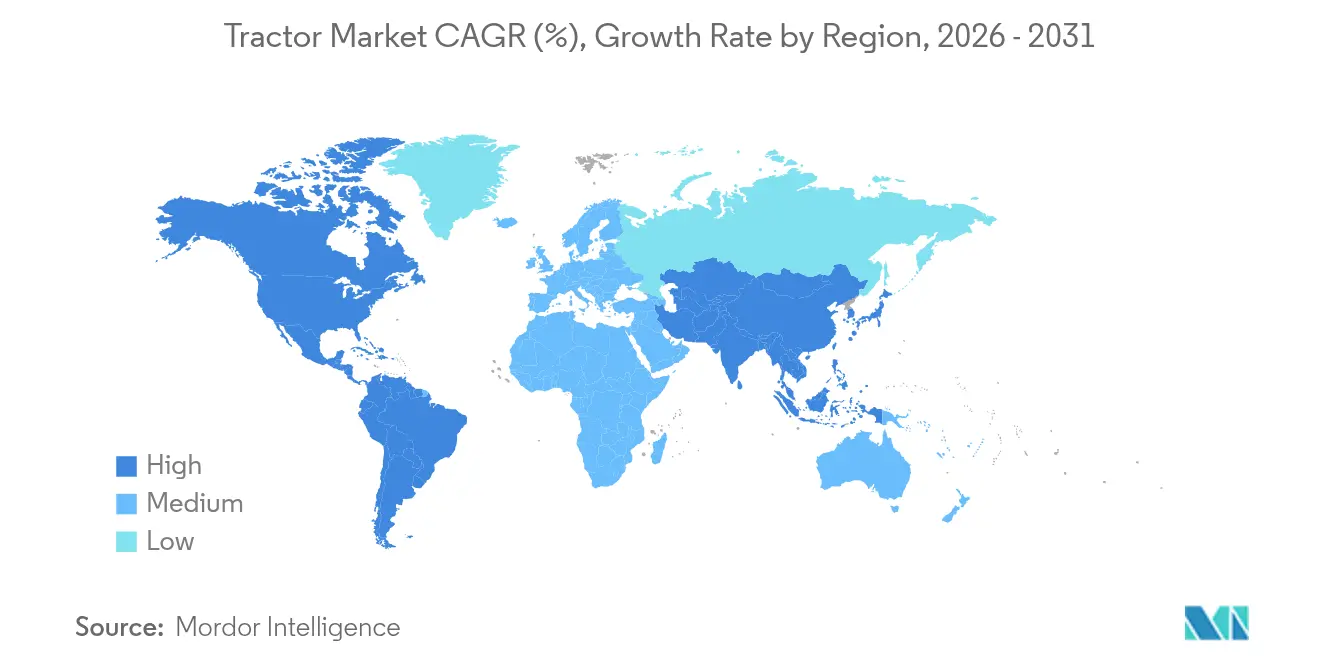

- By geography, Asia-Pacific held 55.35% of 2025 revenue; South America is set to expand at the highest regional pace, with a 6.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mechanization Demand | +1.8% | Asia-Pacific, Sub-Saharan Africa, South America | Medium term (2-4 yrs) |

| Subsidy and Ag-credit | +1.2% | Global hot spots (India, China, Brazil) | Short term (≤ 2 yrs) |

| Labor Shortages | +1.5% | North America, Europe, China, India | Long term (≥ 4 yrs) |

| Precision-Ag Uptake | +0.9% | North America, Europe, Australia | Medium term (2-4 yrs) |

| Electric Tractors | +0.7% | Europe, North America, select Asia-Pacific | Long term (≥ 4 yrs) |

| Rental Platforms | +0.4% | Global early adopters | Medium term (2-4 yrs) |

| Source: Mordor Intelligence | |||

Rising Mechanization Demand in Emerging Economies

Urban migration and shrinking rural labor pools make mechanization a strategic necessity across Asia and Africa. India’s 40-45% mechanization rate trails China’s 57% and the United States’ 95%, offering clear catch-up potential[1]“Agricultural Policy Monitoring and Evaluation 2024,”, Organisation for Economic Co-operation and Development, oecd.org. New subsidy schemes in China prioritize smart 4WD tractors, promoting a shift toward higher horsepower that lifts per-acre productivity. Cooperative ownership models and equipment-sharing apps further catalyze adoption by spreading costs, while precision-placement benefits such as optimized fertilizer use improve soil health. Collectively, these trends embed tractors as multifunctional assets rather than basic power units, reinforcing long-term demand for the global tractor market.

Escalating Farm-Labor Shortages in OECD and BRICS

United States farmers grapple with a significant labor shortage, leading to heightened wage costs and squeezed profit margins[2]“Farm Labor Markets in 2025,”, U.S. Department of Agriculture Economic Research Service, ers.usda.gov. Similar gaps exist in the European Union and China. Growers respond by accelerating machinery purchases, now adopting labor-saving technology ahead of wage hikes. Autonomous and remotely operated tractors are making significant strides in the realms of horticulture and specialty crop farming, particularly in areas where securing a reliable seasonal workforce has become an ongoing challenge. This persistent labor shortage creates a fundamental baseline for the demand in the global tractor market, underscoring a transformative shift in agricultural practices. As these advanced machines take to the fields, they are not just filling a gap; they are revolutionizing the way crops are cultivated and harvested, opening up new possibilities for efficiency and productivity in an industry in need of innovation.

Rapid Adoption of Precision-Ag and Telematics Platforms

70% of large United States farms use guidance autosteering, which delivers yield gains and input savings that justify higher equipment outlays[3]“Precision Agriculture Technologies,”, U.S. Government Accountability Office, gao.gov. Manufacturers embed 4G/5G modems and over-the-air software, turning tractors into data nodes that support variable-rate seeding, fleet optimization, and predictive maintenance. AGCO’s joint venture with Trimble targets USD 2 billion in precision revenue by 2028 [4]“AGCO and Trimble Form PTx Trimble,”, AGCO Corporation, agcocorp.com. The recent advancements in digital technology significantly enhance the appeal of new tractor models, driving a wave of fleet replacement and invigorating the global tractor market. As these innovations unfold, they not only elevate the overall value proposition but also entice operators to embrace the modern capabilities that promise greater efficiency and productivity in their farming practices.

Growth of Data-Driven Tractor-Rental Platforms

Managing lease fleets like MachineryLink empowers agricultural producers to harness the latest high-performance equipment without burdening their budgets. This approach allows them to allocate their capital more efficiently by distributing fixed costs across shorter usage periods. Through innovative cloud dashboards, growers can seamlessly align machine availability with the critical peaks of planting and harvesting seasons, significantly boosting fleet utilization.

As telematics technology delivers detailed insights into runtime and load factors, the concept of risk-based pricing becomes a viable option, paving the way for quicker adoption of these advanced models. This strategy not only widens the potential market for smallholder farmers but also enhances the cyclical resilience of the global tractor market, ensuring that it remains robust and responsive to varying demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Price and Commodity Swings | −1.4% | North America, Europe | Short term (≤ 2 yrs) |

| Seasonal Income Volatility | −0.8% | South Asia, Sub-Saharan Africa, Latin America | Medium term (2-4 yrs) |

| Chip Bottlenecks | −0.6% | Global manufacturing hubs | Short term (≤ 2 yrs) |

| Localization Rules | −0.4% | North America, Europe, Asia-Pacific | Medium term (2-4 yrs) |

| Source: Mordor Intelligence | |||

Electronics-Grade Chip Supply Bottlenecks

The ongoing semiconductor shortages are casting a long shadow over the production of power-train controllers and sensor modules. In early 2025, the lead times for 32-bit microcontrollers soared beyond a staggering 50 weeks, leading to frustrating line stoppages and protracted delivery timelines. While some automotive chip fabrication facilities are finally beginning to open their doors, the strain on capacity persists, limiting the immediate output crucial for the global tractor market. The ripple effects of this constraint are felt deeply, as manufacturers scramble to keep pace with demand amid an increasingly competitive landscape.

New Localization and Content-Origin Rules in Trade Pacts

The United States-Mexico-Canada Agreement (USMCA) content thresholds, along with stringent EU regulations, are forcing manufacturers to dramatically reshape their supply chains. This disruption not only leads to inflated tooling and validation expenses but also creates a ripple effect across the industry. The significant funds diverted towards compliance rob vital capital from crucial research and development efforts, stifling innovation and delaying the launch of new models. As a result, profit margins are squeezed, and the pace of advancements in the global tractor market grinds to a halt, leaving manufacturers grappling with the complexities of navigating an increasingly regulated landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Horsepower: Farm Consolidation Drives Power Demand

The 40-100 HP class supplied mainstream versatility and claimed 46.93% of the tractor market size in 2025, anchoring the global tractor market. Above-100 HP units are forecast to grow at a 7.16% CAGR during the forecast period, as larger farms seek acreage efficiency. This up-powering supports advanced hydraulic systems and greater implement widths, allowing integrated precision technologies. John Deere’s Iowa expansion to build 9RX machines underscores long-term confidence in significant iron demand.

Farm business models focusing on larger scales harness the power of telematics-driven fleet coordination, transforming horsepower into a catalyst for extraordinary productivity. While smaller tractors with less than 40 HP continue to carve out their niche in the specialized realm of horticulture, the gradual pace of mechanization in micro-plots casts a shadow over their prospects. Consequently, high-horsepower momentum lifts the premium end of the global tractor market size, propelling revenue faster than unit volume.

By Drive Type: Terrain Complexity Favors AWD

Cost-efficient 2WD platforms held a 77.10% share of the tractor market in 2025. Yet 4WD adoption benefits from added traction, distributing torque for tillage under wetter or sloped conditions. The 7.69% CAGR projected for 4WD through 2031 aligns with broader precision-ag uptake, where consistent wheel slip protects seed placement accuracy.

The unpredictable nature of climate variability is reshaping the landscape of agricultural practices, extending the fleeting windows of opportunity for fieldwork when soil moisture levels fall below ideal conditions. This shift underscores the value of Alternate Wetting and Drying (AWD) investments, forging a stronger connection between farmers and innovative solutions. As they strive for year-round cultivation, many are now viewing four-wheel drive (4WD) vehicles as a vital safeguard against the whims of the weather. This evolving mindset deepens the relationship between the adoption of 4WD and the quest for greater profitability, highlighting how essential these advancements have become in navigating the challenges of modern farming.

By Propulsion Type: Electric Transition Accelerates

Diesel remained dominant at 90.25% of the tractor market size in 2025; however, battery platforms expanded rapidly at 9.05% CAGR over the forecast period, as cell costs fell and charging solutions proliferated. Regulations in Europe set strict engine tier standards, redirecting R&D budgets into electric drivelines.

Fleet trials reveal a compelling transformation in the landscape of transportation, demonstrating fuel-cost parity at lower operating hours when electricity comes from renewable sources. As concerns about range anxiety diminish, the economic advantages of electric vehicles become increasingly evident over their entire lifecycle, greatly expanding their potential market. This pivotal shift is not just a minor adjustment; it steadily redirects the vast global tractor market toward innovative zero-emission solutions, while hybrid vehicles satisfy the transitional demand in this evolving ecosystem.

By Application: Construction Diversification Expands

In 2025, agriculture dominated the tractor market, commanding an impressive 88.87% share. However, the dynamic landscape of construction is increasingly steering tractors toward essential roles in grading, material handling, and site preparation. The projected 7.31% CAGR in the construction sector through 2031 is fueled by ambitious infrastructure initiatives in burgeoning economies like Brazil, India, and the United States, paving the way for a robust evolution in the utilization of these powerful machines.

Original equipment manufacturers (OEMs) skillfully tailor loader arms, backhoe attachments, and the ergonomic design of cabs to suit the rugged demands of off-farm environments. This customization not only elevates the functionality of their equipment but also unveils new revenue streams that help mitigate the impacts of fluctuating crop prices in the global tractor market.

Geography Analysis

Asia-Pacific contributed 55.35% of the tractor market size in 2025. China remains pivotal as it pivots toward high-horsepower and smart tractors. Southeast Asian governments channel concessional credit into machinery purchases, maintaining a solid growth runway for the global tractor market in the region.

South America delivers the fastest expansion at 6.89% CAGR, buoyed by Brazil’s soy and corn acreage gains and domestic credit lines that spur equipment upgrades. Massey Ferguson, Valtra, and New Holland have a significant share of Brazilian sales, illustrating the influence of localized assembly on customer preference. Chile and Colombia inject incremental demand through fruit-export diversification, reinforcing continental momentum.

North America and Europe showcase well-established markets characterized by a more measured pace of volume growth, yet they boast a higher value per unit. In 2024, European vehicle registrations plummeted to a decade low, reflecting the tightening grip of profitability challenges. Despite this, Europe stands at the forefront of pioneering electric vehicle trials and developing regulatory frameworks for autonomous technology.

Meanwhile, the Middle East and Africa, still in their early stages of market development, are becoming increasingly vital to the long-term expansion and diversity of the global tractor industry. Their strategic importance cannot be understated as they represent emerging opportunities in a landscape ripe for growth.

Mordor Intelligence provides coverage of the tractor market across other key regional markets. Detailed country-level analysis extends to Brazil incorporating local coverage and market participation, as required.

Competitive Landscape

The global tractor market is moderately concentrated: the major players account for a significant share of worldwide revenue, conferring procurement leverage yet leaving space for regional challengers. Deere, CNH Industrial, AGCO, Kubota, and Mahindra differentiate through proprietary precision stacks, autonomous roadmaps, and integrated finance arms. Technology partnerships are intensifying; AGCO’s USD 2 billion acquisition of Trimble’s ag unit vaults it into retrofit autonomy leadership. Deere’s USD 20 billion United States investment earmarks new 9RX capacity and battery R&D, fortifying its premium offering.

Regional specialists exploit localized after-sales networks and price competitiveness, defending share in Southeast Asia and Africa. Rental platforms add another layer of rivalry by decoupling equipment access from ownership, potentially diluting OEM brand loyalty. Component shortages and policy-driven localization raise operating complexity, rewarding vertically integrated players that can buffer supply disruptions. Overall, strategic focus has shifted from horsepower escalation toward software ecosystems and electrification, redefining success factors inside the global tractor industry.

Tractor Industry Leaders

Mahindra & Mahindra Ltd.

Deere & Company

CNH Industrial N.V.

Kubota Corporation

AGCO Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: John Deere has made a bold commitment of USD 20 billion to enhance its manufacturing capabilities in the United States, ushering in an era of growth and innovation. This significant investment will not only facilitate extensive factory expansions but also introduce the powerful new high-horsepower 9RX tractor lineup, setting a new standard in agricultural machinery.

- April 2025: Cathay Cargo Terminal has completed its first end-to-end trial of Autonomous Electric Tractor operations, enabling direct towing from within the terminal to the West Cargo Apron at Hong Kong International Airport.

- February 2025: John Deere rolled out its inaugural series of electric-powered agricultural tractors. The debut trio of E-Power models, tailored for vineyards, orchards, and dairies, is undergoing testing in three distinct sizes. These electric tractors, boasting around 130 horsepower, align closely with Deere's 5 Series and match the performance of their diesel-driven equivalents.

Global Tractor Market Report Scope

A tractor is a vehicle usually available with one or two small wheels in front and two large wheels at the back. It is used in agriculture, construction, and logistics applications to move attached implements such as rotavators, plowing, tilling, sowing, cultivation, and harvesting.

The tractors market is segmented by horsepower (below 40 HP, 40 HP - 100 HP, and above 100 HP), by drive type (two-wheel drive and four-wheel drive/all-wheel drive), and by geography (North America, Europe, Asia-Pacific, and the Rest of the World). For each segment, market sizing and forecast are given on the basis of value in USD billion.

| Below 40 HP |

| 40 - 100 HP |

| Above 100 HP |

| Two-Wheel Drive (2WD) |

| Four-/All-Wheel Drive (4WD/AWD) |

| Diesel |

| Battery-Electric |

| Hybrid (Diesel-Electric) |

| Agriculture |

| Construction |

| Forestry |

| Municipal & Grounds Maintenance |

| Haulage & Logistics |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Horsepower | Below 40 HP | |

| 40 - 100 HP | ||

| Above 100 HP | ||

| By Drive Type | Two-Wheel Drive (2WD) | |

| Four-/All-Wheel Drive (4WD/AWD) | ||

| By Propulsion Type | Diesel | |

| Battery-Electric | ||

| Hybrid (Diesel-Electric) | ||

| By Application | Agriculture | |

| Construction | ||

| Forestry | ||

| Municipal & Grounds Maintenance | ||

| Haulage & Logistics | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the global tractor market?

The global tractor market size reached USD 95.03 billion in 2026 and is forecast to top USD 126.18 billion by 2031.

Which segment is growing fastest by horsepower?

Tractors above 100 HP are projected to grow at 7.16% CAGR as farms consolidate and demand higher field capacity.

How quickly are electric tractors being adopted?

Battery-electric models are expanding at a 9.05% CAGR, the highest among all propulsion types, supported by emission regulations and lower operating costs.

Which segment is growing fastest by propulsion?

As cell costs declined and charging solutions became more widespread, battery platforms experienced a robust expansion, growing at a rate of 9.05% CAGR during the forecast period. This growth is attributed to battery technology advancements, increased electric vehicle adoption, and the rising demand for energy storage solutions across various industries.

Page last updated on: