Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

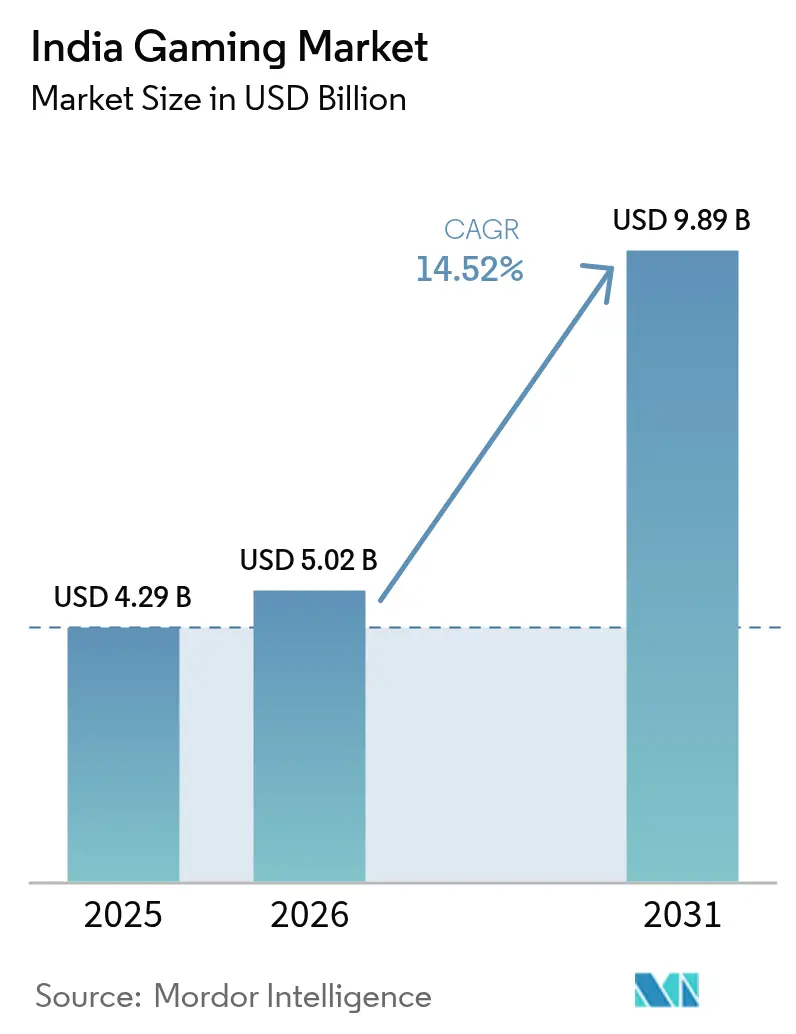

| Base Year Market Size (2025) | USD 4.29 Billion |

| Market Size (2026) | USD 5.02 Billion |

| Market Size (2031) | USD 9.89 Billion |

| Growth Rate (2026 - 2031) | 14.52% CAGR |

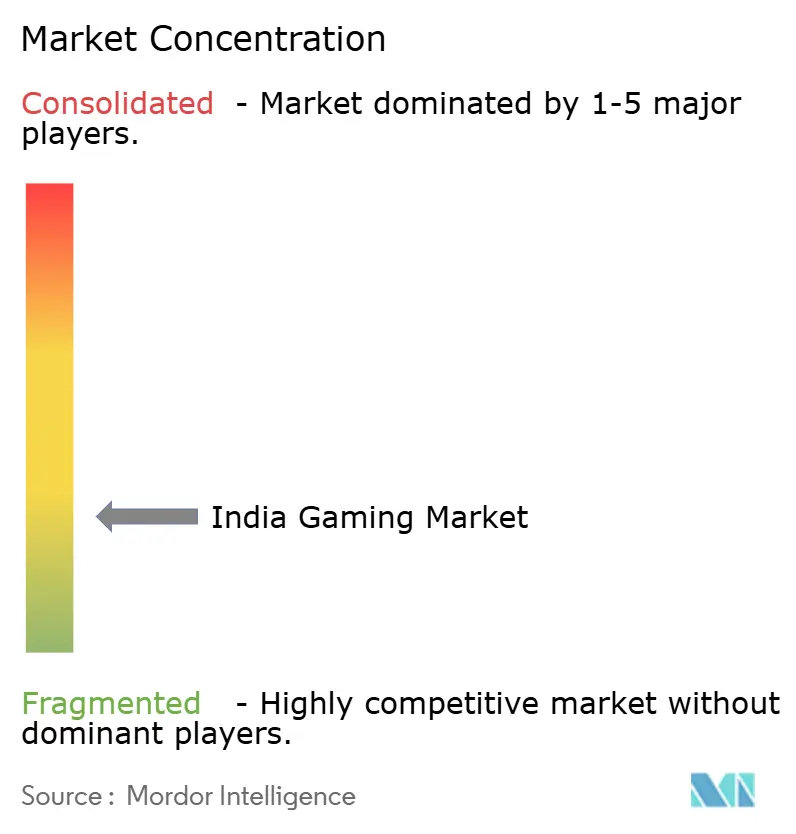

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Gaming Market Analysis by Mordor Intelligence

The India gaming market size is expected to increase from USD 5.02 billion in 2026 to reach USD 9.89 billion by 2031, growing at a CAGR of 14.52% over 2026-2031. User adoption is widening on the back of affordable 5G smartphones, a dense 5G radio network, and one-click UPI payments. Newly issued national rules under the Public Regulation of Online Gaming Act 2025 have reduced licensing friction and encouraged both domestic and foreign investment. Telecom operators and hyperscalers are co-locating edge servers, allowing cloud-streamed AAA titles to bypass handset storage limits. Publishers are also leaning into vernacular content that embeds local culture, which is extending engagement beyond metro areas into Tier-2 and Tier-3 cities.

Key Report Takeaways

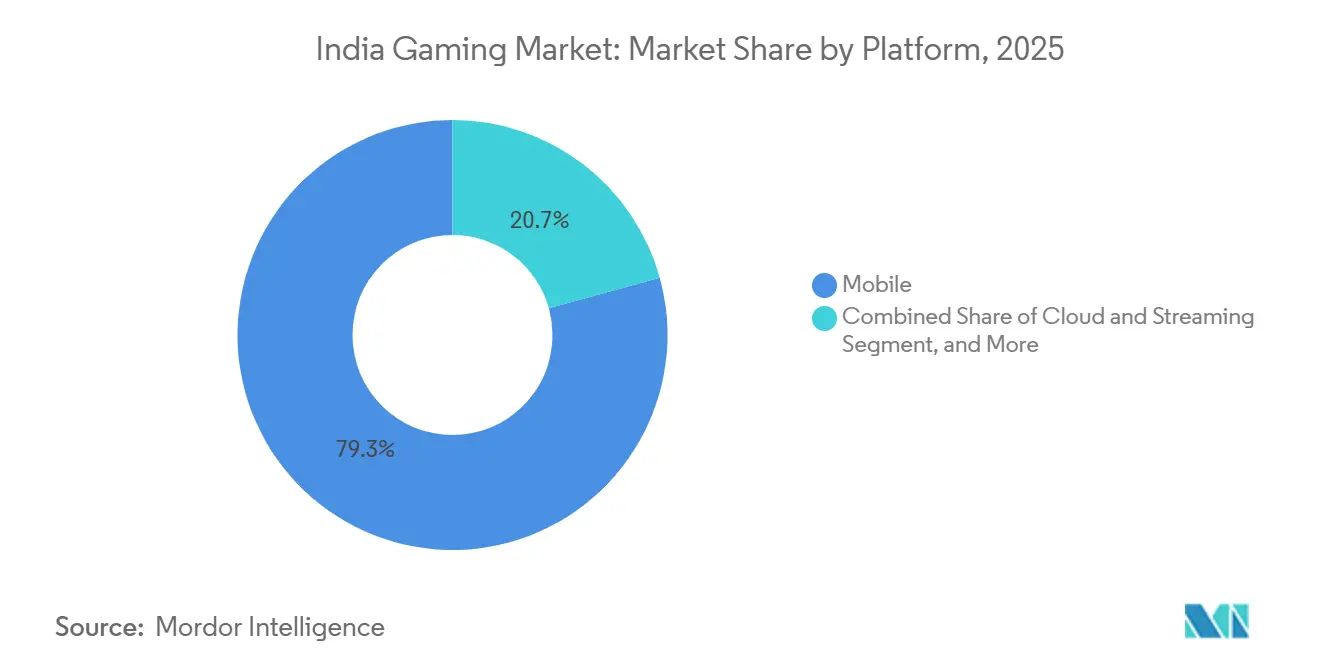

- By platform, mobile commanded 79.29% of India gaming market share in 2025, while cloud and streaming is projected to expand at a 14.89% CAGR to 2031.

- By revenue model, advertising-supported formats held 46.18% of 2025 revenue, whereas subscription passes are advancing at a 14.95% CAGR through 2031.

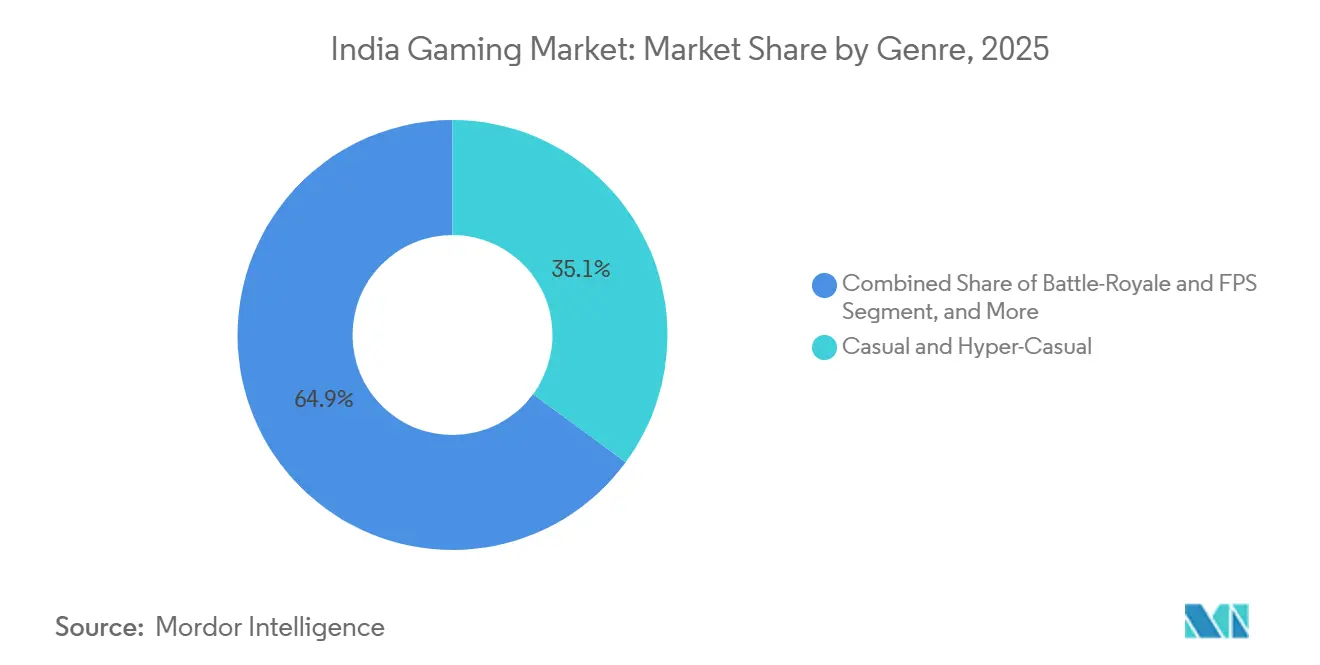

- By genre, casual and hyper-casual led with 35.08% of 2025 revenue; battle-royale and FPS titles are the fastest growing at a 15.12% CAGR.

- By age cohort, gamers aged 15-24 years accounted for 41.36% of 2025 spending; the 25-34 years segment is projected to grow at a 15.33% CAGR.

- By gender, female participation rose to 28% of WinZO’s user base in 2025, reflecting rising engagement in puzzle and simulation games.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Gaming Market Trends and Insights

Drivers Impact Analysis Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming Smartphone Shipments and Low-Cost Data Plans | +3.20% | Pan-India, with accelerated uptake in Uttar Pradesh, Bihar, Madhya Pradesh | Short term (≤ 2 years) |

| Roll-Out of 5G Enabling Low-Latency Cloud Gaming | +2.80% | Urban centers and Tier-1 cities, expanding to Tier-2 by 2027 | Medium term (2-4 years) |

| Surge in Vernacular Content and Locally Themed Titles | +2.40% | Regional strongholds in Tamil Nadu, West Bengal, Maharashtra, Karnataka | Medium term (2-4 years) |

| Government's ONDC and Digital India Initiatives | +1.90% | National, with early gains in Kerala, Rajasthan, Odisha | Long term (≥ 4 years) |

| Growth of UPI-Based Micro-Transactions | +2.10% | Pan-India, particularly Tier-2 and Tier-3 cities | Short term (≤ 2 years) |

| Corporate E-Sports Leagues Driving Engagement | +1.40% | Metropolitan hubs in Mumbai, Bengaluru, Hyderabad, Delhi NCR | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Smartphone Shipments And Low-Cost Data Plans

Smartphone shipments hit 32 million units in Q1 2025, 88% of which carried 5G radios, while the average selling price fell to USD 274. Reliance Jio’s two-gigabyte-per-day package at below USD 3 per month slashed the marginal cost of streaming heavy games, letting semi-urban users adopt console-grade titles. The Production-Linked Incentive scheme drew USD 1.5 billion in handset-component investment during 2025, anchoring local supply chains and sustaining price compression.[1]Ministry of Electronics and Information Technology, “Production-Linked Incentive Scheme Updates 2025,” MEITY.GOV.IN

Roll-Out Of 5G Enabling Low-Latency Cloud Gaming

The Telecom Regulatory Authority of India logged 518,854 live 5G radio sites covering 99.9% of districts by December 2025. Latency for cloud sessions fell under 30 milliseconds in major metros, allowing real-time shooters to render on edge servers. Microsoft Azure and Amazon Web Services placed GPU stacks inside Airtel and Vodafone Idea facilities in early 2025, cutting hop counts for players.[2]Telecom Regulatory Authority of India, “5G Network Coverage and Subscriber Data – December 2025,” TRAI.GOV.IN

Surge In Vernacular Content And Locally Themed Titles

Downloads for regional-language games more than doubled in 2025. WinZO reported 40% longer play times and 25% higher in-app purchase conversion among non-English users. The Ministry of Information and Broadcasting committed INR 500 crore (USD 60 million) to regional game studios, spurring titles that weave festivals, mythology, and Bollywood IP into core loops.[3]Ministry of Information and Broadcasting, “AVGC Sector Task Force Report 2025,” MIB.GOV.IN

Government Digital Commerce and Connectivity Initiatives

The Open Network for Digital Commerce processed 141.8 million orders across 1,100 cities by late 2025. BharatNet had connected 214,000 village councils to fiber, broadening multiplayer access in rural areas. The central Online Gaming Authority now issues skill-based certificates, trimming state-wise legal ambiguity and attracting USD 800 million in gaming startup funding during 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patchwork State-Level Real-Money Gaming Bans | -2.60% | Tamil Nadu, Andhra Pradesh, Sikkim; spillover risk in Kerala, Assam | Short term (≤ 2 years) |

| Rising Cyber-Fraud and AML Compliance Cost | -1.80% | National, with acute pressure on platforms exceeding 10 million users | Medium term (2-4 years) |

| Talent Crunch in AAA Game Development | -1.30% | Bengaluru, Pune, Hyderabad development hubs | Long term (≥ 4 years) |

| Stricter Age-Rating and Loot-Box Regulations Ahead | -0.90% | National, with phased enforcement starting 2027 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patchwork State-Level Real-Money Gaming Bans

Tamil Nadu and Sikkim continue to outlaw stake-based rummy and poker. Operators must deploy geo-fencing and run duplicate user pools, which lifted compliance outlays above USD 15 million each for major fantasy and card platforms in 2025. Biometric KYC now applies to transactions over INR 10,000 (USD 120), adding friction for high-value users.[4]Financial Intelligence Unit – India, “Enhanced KYC Requirements for Online Gaming Platforms,” FIUINDIA.GOV.IN

Rising Cyber-Fraud and AML Compliance Cost

CERT-In recorded a 35% surge in credential-phishing incidents targeting gamers during 2025. Platforms processing upward of one million monthly transactions must undergo quarterly security audits under Reserve Bank of India rules, an expense that small studios struggle to meet. Larger companies such as WinZO have spent more than USD 10 million on real-time fraud-detection models, though false positives still hover near 8%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Dominance, Cloud Momentum

Mobile accounted for 79.29% of India gaming market revenue in 2025, a share supported by Android devices priced below USD 300 and 5G radios that stream 60-frame graphics without thermal throttling. Console gaming remains niche because import duties lift PlayStation 5 Pro pricing to INR 59,990 (USD 720). PC rigs anchor the esports ecosystem but face components inflation. The India gaming market size for cloud and streaming platforms is forecast to rise at a 14.89% CAGR, helped by 518,854 live 5G towers and edge nodes that keep round-trip latency under 30 milliseconds. Studios are cutting QA budgets by targeting a standardized cloud runtime rather than dozens of handset SKUs.

The growth of cloud delivery is changing publisher economics. Subscription bundles such as Xbox Game Pass Ultimate priced at INR 499 (USD 6) per month have raised the ceiling for premium spend outside metro cities. Telecom bundles that zero-rate game traffic are nudging casual players toward heavier genres, and device makers preload cloud-gaming shortcuts to showcase 5G speeds. As a result, the India gaming market is set to witness deeper engagement time among first-time gamers who skipped the console era altogether.

By Revenue Model: Ads Hold Sway, Subscriptions Accelerate

Advertising-supported games captured 46.18% of 2025 revenue because UPI micropayments unlock free-to-play loops while brands chase the 15-34 years cohort. Rewarded video remains the dominant unit, with completion rates above 90%. In-app purchases rank second as the National Payments Corporation of India reported 21.7 billion UPI swipes in January 2026 alone. Subscription passes, though only a sliver today, are the fastest mover at a 14.95% CAGR, and are now exempt from the 28% goods-and-services tax levied on real-money stakes.

A richer pipeline of day-one launches is critical for subscription stickiness. Sony’s PlayStation Plus regional tier debuted in 2025 with a 200-title library at INR 699 (USD 8.40) per month, forcing rivals to court Indian studios for exclusive vernacular content. The India gaming market size for subscription models is expected to climb steadily as publishers favour predictable cash flows over volatile launch cycles. Premium pay-to-download titles, once the standard, continue to shrink in share because piracy and free trials reset consumer expectations.

By Genre: Casual Leads, Battle-Royale Gains

Casual and hyper-casual titles retained 35.08% of 2025 revenue thanks to snackable five-minute sessions and ad-first monetization. However, battle-royale and FPS games are pacing at a 15.12% CAGR through 2031, energized by Krafton’s Battlegrounds Mobile India comeback and Call of Duty Mobile’s 2026 esports roadmap. Vernacular myths, Bollywood cameos, and festival skins extend dwell time in strategy and card games, while the sports vertical monetizes official Indian Premier League and Formula 1 licenses.

Real-money formats remain compliance-heavy yet lucrative. Dream11 crossed 220 million users in 2024 and now cross-sells casual puzzle games during cricket off-seasons. Meanwhile, nostalgia remasters such as retro 1990s arcade shooters are courting the 35-plus bracket. Genre diversity is therefore widening, ensuring that the India gaming market continues to cater to both hyper-casual tappers and core-gamer clans alike.

By Gamer Demographics: Youth Core, Professionals Rising

The 15-24 years bracket provided 41.36% of 2025 spend, logging 90-minute average sessions in shooters and racing sims. Working professionals aged 25-34 are on track for the quickest 15.33% CAGR, buoyed by disposable income and preference for ranked, seasonal content. Under-14 users form a smaller slice, with monetization caps likely once draft loot-box rules go live in 2027.

Female gamers are closing the gap, now 28% of WinZO’s base, and show above-average retention in puzzle and life-simulation titles. Rural women logging in via BharatNet fiber are a newly addressable cohort. Studios are adding AI voice filters and women-only lobbies to counter harassment, a move that is raising session duration. Altogether, demographic breadth is pushing the India gaming market toward steady, inclusive growth that balances hardcore competition with casual discovery.

Competitive Landscape

The field is moderately fragmented, with local champions Nazara Technologies, Dream Sports, and WinZO battling Krafton, Garena, Microsoft, Sony, and Nintendo. Nazara logged INR 306.9 crore (USD 36.8 million) revenue in Q2 FY2025, thanks to Nodwin Gaming’s 50-event esports calendar and the Kiddopia edutainment buyout. Dream Sports uses its 220 million-strong fantasy-cricket funnels to cross-sell strategy titles, cutting acquisition cost per user by roughly one-third. Krafton has earmarked USD 20 million for a Bengaluru studio building an India-themed battle-royale map, diversifying away from a single flagship IP.

New entrants include nCORE Games with the nationalist FAU-G franchise and SuperGaming, which secured USD 10 million to develop Indus Battle Royale featuring motion-capture and local voice acting.

Pocket Aces’ Loco livestreaming service hosts influencer-led tournaments for 50 million spectators, giving publishers an alternative to YouTube Gaming. Differentiation hinges on AI voice moderation, blockchain asset ownership, and ad-personalization algorithms. Altogether, competition is intense but still allows white-space plays in cloud-exclusive AAA libraries, regional narratives, and UPI-first monetization designs that fit India gaming market user behaviour.

India Gaming Industry Leaders

Nazara Technologies Ltd.

Dream Sports (Dream11 Gaming Pvt Ltd.)

Games24x7 Pvt Ltd.

MPL Gaming Pvt Ltd.

JetSynthesys Pvt Ltd.

- *Disclaimer: Major Players sorted in no particular order

Geography Analysis

West India generated 24.84% of 2025 gaming revenue, led by Maharashtra’s corporate esports leagues and Gujarat’s real-money clusters. Mumbai and Pune attract venture capital and animation talent, letting studios upscale production values without offshore outsourcing. South India is poised for the fastest 14.98% CAGR as Karnataka reversed its 2024 ban on skill-based titles and Telangana’s Hyderabad hub houses 60% of national game-dev staff. Krafton and Garena have opened local headquarters in Bengaluru, embedding with telcos for handset preload deals.

North India benefits from dense 5G coverage and ubiquitous UPI, yet lower per-capita income bends monetization toward rewarded ads. East India remains under-penetrated but is catching up via Bengali-language libraries that drove 120% download growth in 2025. The India gaming market size for Tier-2 and Tier-3 cities is climbing as the Open Network for Digital Commerce lowers app-store tolls and extends discovery to towns where credit cards serve fewer than 5% of adults.

Regulatory divergence still shapes strategy. Karnataka offers licensing clarity, while Tamil Nadu continues to restrict real-money stakes, pushing operators to rely on geo-locks. National harmonization under the new Online Gaming Authority is underway but uneven by state. Despite the patchwork, edge infrastructure and localized content are helping every region find its own growth lane, keeping the India gaming market’s geographic footprint on an expansion trajectory.

Recent Industry Developments

- August 2025: Enforcement Directorate froze INR 284.5 crore assets of Probo Media Technologies in an illegal betting probe, highlighting stricter financial scrutiny.

- August 2025: Torrent Group acquired 67% of the Gujarat Titans IPL franchise, underscoring the convergence between traditional sports and gaming.

- August 2025: GameRamp secured USD 5.4 million for AI-based in-game economies, reflecting demand for revenue optimization tech.

- July 2025: Mayhem Studios, an MPL unit, raised USD 20 million Series A to develop AAA titles and deepen technology stacks.

- June 2025: Jio launched a Blacknut-powered cloud service offering 50 premium titles on 4G/5G networks, marking an infrastructure milestone.

- May 2025: Dream Sports invested USD 50 million in Cricbuzz and Willow TV to broaden its media footprint.

India Gaming Market Report Scope

The India Gaming Market Report is Segmented by Platform (Mobile with Android and iOS, Console with Hand-Held and Home Console, PC, Cloud and Streaming), Revenue Model (In-App Purchase, Advertising-Supported, Subscription Pass, Premium Pay-To-Download), Genre (Casual and Hyper-Casual, Action and Adventure, Battle-Royale and FPS, Sports and Racing, Real-Money Gaming, Strategy and Card), Gamer Demographics (Age Group with ≤14 Years, 15-24 Years, 25-34 Years, ≥35 Years, and Gender with Male and Female), and Geography (West India, South India, North India, East India). The Market Forecasts are Provided in Terms of Value (USD).

By Platform

| Mobile | Android |

| iOS | |

| Console | Hand-Held |

| Home Console | |

| PC | |

| Cloud, Streaming |

By Revenue Model

| In-App Purchase (IAP) |

| Advertising-Supported |

| Subscription Pass |

| Premium, Pay-To-Download |

By Genre

| Casual and Hyper-Casual |

| Action, Adventure |

| Battle-Royale and FPS |

| Sports and Racing |

| Real-Money Gaming (RMG) |

| Strategy and Card |

By Gamer Demographics

| Age Group | ≤14 Years |

| 15-24 Years | |

| 25-34 Years | |

| ≥35 Years | |

| Gender | Male |

| Female |

| By Platform | Mobile | Android |

| iOS | ||

| Console | Hand-Held | |

| Home Console | ||

| PC | ||

| Cloud, Streaming | ||

| By Revenue Model | In-App Purchase (IAP) | |

| Advertising-Supported | ||

| Subscription Pass | ||

| Premium, Pay-To-Download | ||

| By Genre | Casual and Hyper-Casual | |

| Action, Adventure | ||

| Battle-Royale and FPS | ||

| Sports and Racing | ||

| Real-Money Gaming (RMG) | ||

| Strategy and Card | ||

| By Gamer Demographics | Age Group | ≤14 Years |

| 15-24 Years | ||

| 25-34 Years | ||

| ≥35 Years | ||

| Gender | Male | |

| Female | ||

Key Questions Answered in the Report

What is the projected value of the India gaming market in 2031?

It is forecast to reach USD 9.89 billion by 2031 at a 14.52% CAGR.

Which platform dominates gamer spending in India?

Mobile platforms led with 79.29% of 2025 revenue, reflecting the smartphone-first nature of Indian consumers.

How fast is the cloud and streaming segment expected to grow?

Cloud and streaming platforms are projected to post a 14.89% CAGR between 2026 and 2031.

Why are subscription game passes gaining traction?

Tax exemptions, affordable monthly pricing, and day-one access to marquee titles are accelerating subscription adoption.

Which region in India is set for the quickest gaming revenue growth?

South India is expected to expand at a 14.98% CAGR through 2031, bolstered by policy clarity and a deep talent pool.

How are regulatory changes affecting real-money gaming?

A new central authority streamlines certification, but state-level bans and enhanced KYC still add compliance costs.

Page last updated on: