Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 123.48 Billion |

| Market Size (2031) | USD 140.32 Billion |

| Growth Rate (2026 - 2031) | 2.59% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Spirits Market Analysis by Mordor Intelligence

The United States spirits market size reached USD 123.48 billion in 2026 and is forecast to climb to USD 140.32 billion by 2031, advancing at a 2.59% CAGR during the period. Premiumization is driving value growth as consumers reduce their drinking frequency yet willingly pay more for super-premium and ultra-premium tiers, allowing supplier revenue to rise even as total case volumes soften. Craft authenticity, once the growth engine, now competes with broader quality cues such as age statements, provenance, and sustainability claims that resonate with urban, high-income buyers. Federal excise incentives under the Craft Beverage Modernization Act continue to support small producers, but declining craft case sales indicate that tax relief alone cannot fully offset distribution frictions and shelf crowding. Channel diversification introduces another layer of change, as direct-to-consumer (DTC) shipping in 18 states opens up options for niche labels, but leaves producers in restrictive states bound to the traditional three-tier system.

Key Report Takeaways

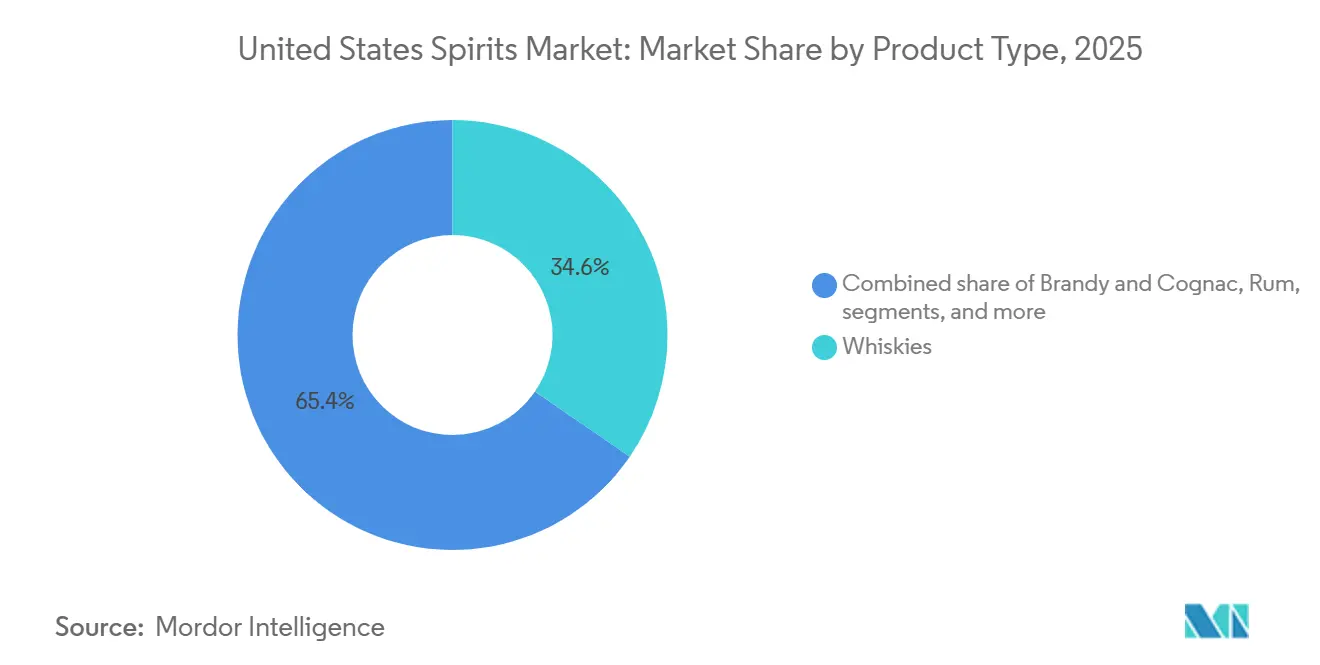

- By product type, whiskies led with 34.58% of the United States spirits market share in 2025, while white spirits are projected to post the quickest 3.03% CAGR through 2031.

- By end user, men commanded 74.61% share of the United States spirits market in 2025, and women represent the fastest-growing cohort at a 3.46% CAGR through 2031.

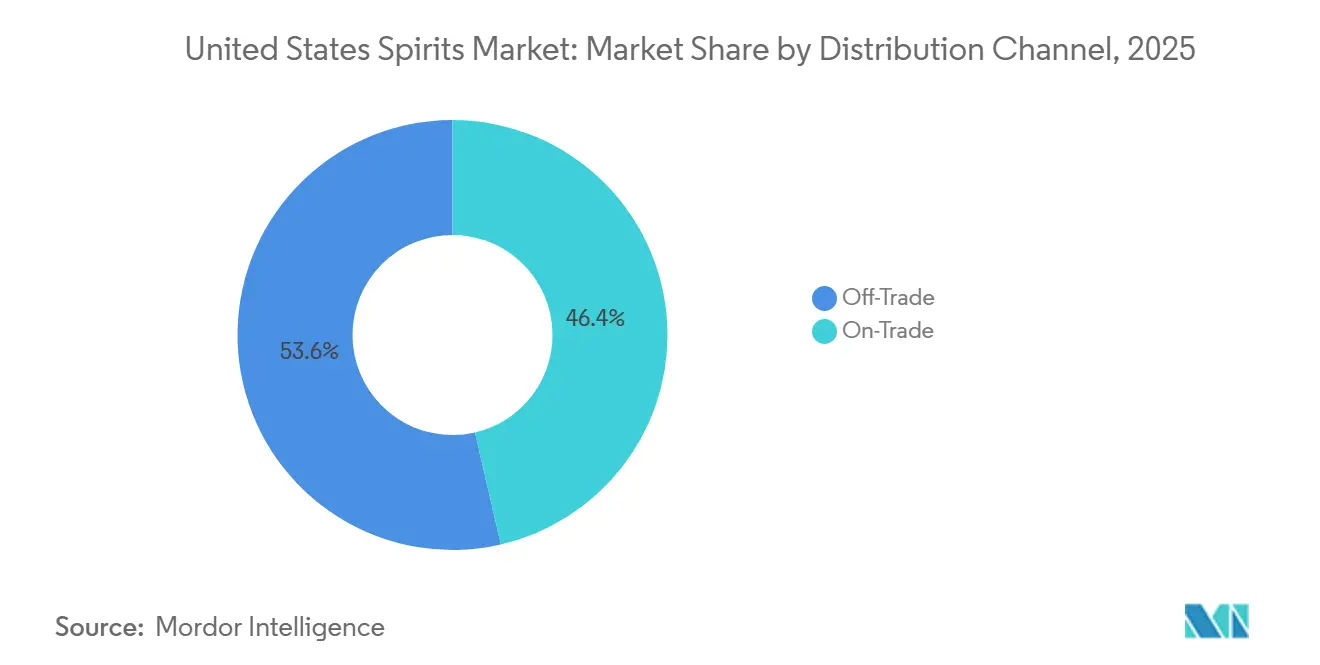

- By distribution channel, the off-trade segment held a 53.61% share of the United States spirits market in 2025; the on-trade channel is expected to expand at a 2.86% CAGR through 2031.

- By geography, the South captured a 34.59% share of the United States spirits market in 2025, whereas the West is forecast to grow the fastest at 3.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing tourism and hospitality sector | +0.80% | South, West, Northeast | Medium term (2-4 years) |

| Consumers' inclination towards craft spirits | +0.60% | National, with concentration in West and Northeast | Medium term (2-4 years) |

| Surge in demand for premium alcoholic products | +0.50% | National | Long term (≥ 4 years) |

| Product differentiation in terms of raw material and alcohol content | +0.40% | National | Medium term (2-4 years) |

| Sustainability and ethical sourcing | +0.30% | West, Northeast | Long term (≥ 4 years) |

| Strategic expansion by pubs and bars | +0.30% | South, West | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing tourism and hospitality sector

Tourism-driven spirits consumption is on the rise as both international arrivals and domestic leisure travel recover from pandemic-related lows. According to the U.S. Travel Association, domestic leisure travel spending in 2024 surpassed pre-2020 levels, with Nevada and Florida capturing a particularly large share of hospitality revenue[1]Source: U.S. Travel Association, “Travel and Tourism Overview 2024,” ustravel.org. Distillery tourism, especially in Kentucky, Tennessee, and California, generates additional income through tasting-room sales, which avoid traditional distribution markups. In California, craft distilleries welcomed over 1 million visitors in 2024, with average tasting-room purchases of USD 75 per visitor, a margin structure that allows smaller producers to thrive despite challenges in competing on wholesale pricing, according to the American Craft Spirits Association[2]Source: American Craft Spirits Association, “Craft Spirits Data Project 2024,” americancraftspirits.org. Hotels and resorts are increasingly curating spirits menus that highlight local products, a trend that boosts regional brands and creates geographic advantages around production hubs. This effect is most pronounced in the West and South, where tourism infrastructure and favorable tasting-room regulations converge.

Consumers inclination towards craft spirits

The U.S. craft distillery sector reached 2,282 producers in 2024, yet case sales dropped to 12.7 million from earlier peaks, signaling that growth in production has outpaced consumer demand, according to the American Craft Spirits Association. This imbalance is largely driven by oversupply in crowded categories, such as vodka and gin, where differentiation at retail is challenging. Leading craft brands are shifting focus to grain-to-glass narratives that showcase local sourcing, heritage mash bills, and transparent production methods. The Craft Beverage Modernization Act provides a cost advantage through reduced federal excise taxes for producers with annual production of less than 100,000 proof gallons, but distribution remains the key bottleneck. Craft spirits thrive in states with strong locavore cultures, such as Oregon, Colorado, and New York, where retailers prioritize regional brands on their shelves. Ultimately, the sector’s long-term success will depend on whether distillers can scale distribution without compromising the artisanal positioning that justifies premium pricing.

Surge in demand for premium alcoholic products

The United States spirits market is witnessing a notable shift toward premiumization, as consumers increasingly favor high-quality products despite economic challenges. According to Diageo's interim report for FY 2025, the premium and super-premium categories have grown significantly, now accounting for nearly 35% of the market value, compared to 26% a decade ago. This trend is particularly pronounced among consumers aged 18-34, with 54% actively choosing premium spirits. Even during economic downturns, consumers demonstrate a clear preference for premium products by reducing consumption frequency rather than compromising on quality. This behavior underscores the importance of brands effectively communicating their superior quality and authentic brand narratives to capture market share. The shift toward premium offerings, despite declining overall volumes, highlights a structural change in the spirits industry, transitioning from a volume-driven approach to a value-focused consumption model. Additionally, this trend aligns with broader consumer preferences for premiumization across other beverage categories, further reinforcing the long-term potential for growth in the premium spirits segment.

Product diffrentiation in terms of raw material and alcohol content

Distillers are exploring heritage grains, alternative aging vessels, and unique botanicals to stand out in crowded categories. Bourbon producers are offering single-barrel and cask-strength expressions that command prices exceeding USD 100, while gin makers are highlighting regional botanicals, such as California citrus or Pacific Northwest juniper, to convey a sense of terroir. Lower-ABV spirits, typically 20–30% alcohol by volume, are gaining popularity among health-conscious consumers seeking moderation without full abstinence. In 2024, Pernod Ricard’s Absolut Vodka introduced a 20% ABV line designed for occasions where standard-strength spirits may be perceived as too strong. Flavored whiskeys and spiced rums continue to draw entry-level consumers, though premiumization is steering innovation toward subtle, complex flavor profiles rather than overt sweetness. Compliance with Alcohol and Tobacco Tax and Trade Bureau (TTB) labeling standards ensures ingredient claims are verifiable, which discourages exaggerated marketing but can pose challenges for smaller producers lacking regulatory expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -0.30% | National, with particular impact in Control States | Long term (≥ 4 years) |

| Rising consumer inclination towards other alcoholic beverages | -0.20% | National | Medium term (2-4 years) |

| Health issues over excessive consumption | -0.10% | National | Long term (≥ 4 years) |

| Supply chain disruptions | -0.10% | National, with heightened impact in import-dependent categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations

The three-tier distribution system, required in most states, creates structural inefficiencies that limit market access for emerging brands. Producers must sell through wholesalers, who then supply retailers, with each tier taking a margin and controlling inventory flow. Direct-to-consumer shipping, legal in 18 states as of 2025, provides an alternative, but inconsistent regulations across jurisdictions complicate compliance, according to the Distilled Spirits Council[3]Source: Distilled Spirits Council, “Direct Shipping Laws 2025,” distilledspirits.org. The Alcohol and Tobacco Tax and Trade Bureau’s Certificate of Label Approval process mandates detailed ingredient disclosure and formula approval, ensuring product safety but delaying launches by 6–8 weeks. State-level taxes on spirits vary significantly: Washington imposes combined excise and sales taxes exceeding 35%, while Missouri applies minimal levies. These disparities distort pricing and competitive dynamics, placing producers in high-tax states at a disadvantage. Regulatory oversight from the TTB and state alcohol control boards will continue to create friction, especially as health advocacy groups push for stricter labeling and advertising rules.

Rising consumer inclination towards other alcoholic beverages

Rising health consciousness regarding alcohol consumption is significantly influencing consumer behavior and market dynamics. The US Surgeon General's Advisory on Alcohol and Cancer Risk identifies alcohol as a major preventable cause of cancer, resulting in approximately 100,000 cancer cases and 20,000 deaths annually in the US[4]U.S. Department of Health and Human Services, "Alcohol and Cancer Risk 2025", www.hhs.gov. The advisory emphasizes that cancer risk increases even with minimal alcohol consumption, fundamentally challenging long-held beliefs about the benefits of moderate drinking. According to the National Institute on Alcohol Abuse and Alcoholism, alcohol contributes to approximately 178,000 deaths annually and is linked to more than 200 distinct health conditions. With less than half of Americans currently understanding the connection between alcohol and cancer, intensifying public health awareness campaigns about these risks are accelerating consumer shifts toward lower-alcohol and non-alcoholic alternatives, potentially constraining growth in traditional spirits markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whiskies Lead Despite Supply Challenges

Whiskies accounted for 34.58% of the market in 2025, fueled by bourbon’s cultural cachet and the premiumization of Scotch and Irish imports. White spirits are projected to grow at a rate of 3.03% annually from 2026 to 2031, the fastest among categories, as vodka and gin drive the ready-to-drink cocktail market and appeal to consumers seeking lower-calorie options. Tequila and mezcal are seeing strong demand, supported by celebrity endorsements and the premiumization of reposado and añejo expressions. Rum faces headwinds due to declining traditional dark rum consumption, though spiced and flavored variants continue to attract younger drinkers. Brandy and cognac remain niche, concentrated in high-income segments and Asian-American communities where cognac carries cultural significance. Liqueurs remain stable, primarily serving as cocktail modifiers rather than standalone beverages.

Regulatory frameworks reinforce market dynamics. The Alcohol and Tobacco Tax and Trade Bureau (TTB) mandates that bourbon be produced in the United States and aged in new charred oak barrels, creating a protective moat for domestic producers. Tequila’s Denomination of Origin restricts production to select Mexican states, limiting supply flexibility and contributing to price volatility. The growth of white spirits is further driven by innovation in ready-to-drink formats, with Diageo, Pernod Ricard, and Bacardi launching canned vodka sodas and gin tonics to capture convenience-focused occasions. Whiskey’s market dominance reflects decades of brand equity and established distribution infrastructure, though its slower growth signals category maturation. Across the industry, traditional product boundaries are blurring as hybrid offerings, such as whiskey-based RTDs and flavored vodkas, fragment segmentation and redefine consumer choices.

By End User: Female Consumers Reshape Market Dynamics

Male consumers accounted for 74.61% of spirits demand in 2025, reflecting historical marketing and cultural associations that have positioned spirits as a masculine category. Female consumption, however, is growing at an annual rate of 3.46% through 2031, outpacing the overall market as brands develop products and messaging tailored to women. Flavored vodkas, botanical gins, and lower-ABV spirits resonate with female consumers who prioritize taste and moderation over alcohol strength. Ready-to-drink cocktails, especially those emphasizing convenience and portion control, are capturing share among women who view spirits as occasional indulgences rather than habitual purchases. The gender gap is narrowing most rapidly in urban areas and among younger cohorts, where traditional consumption norms are undergoing a shift.

Brands are adapting accordingly. Pernod Ricard’s Absolut Vodka and Diageo’s Tanqueray Gin have launched campaigns featuring female brand ambassadors and highlighting the versatility of cocktails, marking a strategic pivot from the spirit-forward messaging that has historically been aimed at men. End-user segmentation is increasingly nuanced, with non-binary and gender-fluid identities prompting some brands to adopt gender-neutral positioning. Male consumption remains concentrated in whiskey, rum, and tequila, while female preferences skew toward vodka, gin, and liqueurs. The 3.46% growth rate among female consumers indicates that closing the gender gap will be a multi-decade endeavor, dependent on sustained marketing efforts and product innovation aligned with female preferences.

By Distribution Channel: Experiential Retail Drives On-Trade Growth

Off-trade channels captured 53.61% of the market in 2025, reflecting the convenience and cost advantages of purchasing spirits for home consumption. On-trade channels are projected to grow at a rate of 2.86% annually from 2026 to 2031, as experiential dining and craft cocktail culture recover from pandemic disruptions. Specialty liquor stores within the off-trade segment provide curated selections and knowledgeable staff, serving as discovery points for premium and craft brands. Other off-trade outlets, including supermarkets and convenience stores, focus on high-velocity mainstream brands, limiting shelf space for emerging producers. Direct-to-consumer shipping, legal in 18 states, is expanding off-trade access for distillers who can bypass wholesaler margins, though regulatory complexity constrains widespread adoption.

Full-service restaurant beverage sales grew faster than food in 2024, according to the National Restaurant Association, signaling a recovery in on-premise spirits consumption[5]Source: National Restaurant Association, “Restaurant Industry Outlook 2024,” restaurant.org . Craft cocktail bars and upscale restaurants function as brand-building venues, with bartender recommendations driving trial and subsequent off-premise purchases. While on-trade channels support premium positioning through higher per-serving prices, volume is constrained by dining frequency. Off-trade growth is fueled by at-home entertaining and the proliferation of ready-to-drink cocktails that replicate bar-quality experiences. Distribution channel segmentation is evolving as e-commerce and direct-to-consumer models challenge the three-tier system’s dominance, though regulatory barriers remain significant in most states.

Geography Analysis

The South accounted for 34.59% of the U.S. spirits market in 2025, primarily driven by the large populations of Texas and Florida, as well as permissive alcohol regulations that facilitate broad retail availability. The West is projected to grow at 3.87% annually from 2026 to 2031, the fastest regional rate, driven by California’s distillery tourism infrastructure, Nevada’s hospitality sector, and the Pacific Northwest’s craft spirits culture. In California, 1 million distillery visitors in 2024 generated tasting-room revenues that support smaller producers, who are unable to compete on wholesale pricing, according to the American Craft Spirits Association. Nevada’s casino and resort sector is rebounding with international tourism, yielding some of the highest per-capita spirits consumption in the nation. Texas benefits from population growth and favorable tax policies, while Florida’s tourism economy and retiree population sustain steady demand.

The Northeast and Midwest exhibit slower growth, constrained by mature markets and restrictive distribution frameworks in states like Pennsylvania and Ohio, where state-controlled liquor stores limit retail competition. New York’s craft distillery scene is vibrant, yet complex licensing and distribution rules hinder scaling beyond local markets. In the Midwest, consumption is concentrated in urban centers such as Chicago and Minneapolis, with rural areas showing lower per-capita demand. Strict pricing and promotion rules enforced by state alcohol control boards in the Northeast reduce competitive intensity, limiting innovation compared to less-regulated regions.

Western growth is further supported by demographic trends, including migration from higher-cost Northeastern and Midwestern states to Western metros with expanding tech and service sectors. The region’s younger population aligns with premiumization and craft spirits trends, while environmental consciousness drives demand for sustainably produced brands. The South’s market dominance is structural, rooted in population size and cultural norms that favor spirits over wine. The Midwest and Northeast face headwinds from aging populations and economic stagnation in legacy industrial cities, though growth persists in college towns and revitalized urban cores. Overall, geographic performance is increasingly determined by local regulatory environments, distribution infrastructure, and demographic composition rather than regional identity alone.

Competitive Landscape

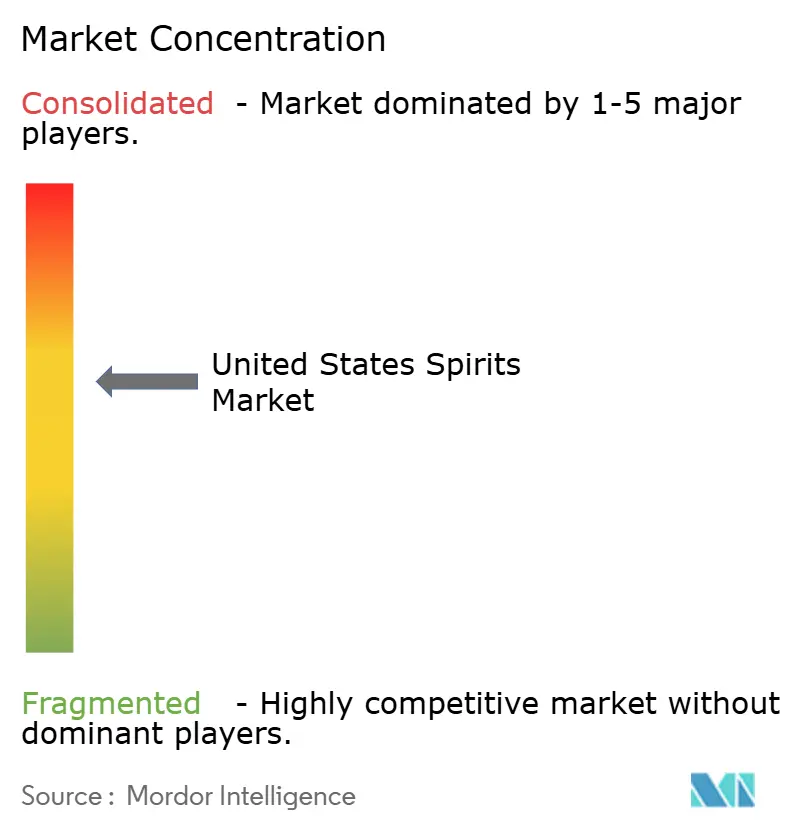

The U.S. spirits market exhibits moderate consolidation, with Diageo, Bacardi, Suntory, Sazerac, and Pernod Ricard dominating, alongside a fragmented segment comprising craft distillers and regional brands. These major players leverage decades of established distribution networks and strong relationships with wholesalers to secure shelf space and on-premise placements. Their strategies increasingly emphasize premiumization, with many divesting mainstream brands to focus on super-premium and ultra-premium tiers that deliver higher margins. Diageo’s fiscal 2025 results highlighted portfolio optimization toward premium and above segments, a strategy mirrored by Pernod Ricard and Bacardi.

White-space opportunities exist in ready-to-drink cocktails, low-ABV spirits, and sustainably produced brands, where consumer demand outpaces incumbent innovation. Emerging disruptors include celebrity-backed tequila brands and craft distillers utilizing direct-to-consumer models that bypass traditional distribution channels. Technology adoption is reshaping competitive dynamics. Suppliers are deploying data analytics to optimize pricing, promotions, and inventory allocation, with Diageo’s use of artificial intelligence for demand forecasting and personalized marketing creating a capability gap smaller producers cannot easily replicate.

Patent filings for novel distillation and aging techniques are rare, as trade secrets provide stronger protection than public disclosure. The Alcohol and Tobacco Tax and Trade Bureau’s formula approval process creates a regulatory moat favoring established players with compliance expertise, while also ensuring product safety and label accuracy. Competitive intensity is highest in the standard-tier segment, where price competition compresses margins, whereas premium tiers offer room for differentiation. The market’s fragmented tail of craft distillers faces consolidation pressure as distribution challenges and capital constraints drive exits or acquisitions.

United States Spirits Industry Leaders

-

Diageo plc

-

Bacardi Limited

-

Suntory Holdings Limited

-

Sazerac Company Inc.

-

Pernod Ricard SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Maker’s Mark launched Star Hill Farm Whisky, its first non-bourbon wheat whisky in over 70 years, made with estate-grown wheat, aged 7–8 years, bottled at cask strength, and certified under the University of Kentucky’s Estate Whiskey program.

- April 2025: Chinola launched its third liqueur, Chinola Pineapple, a handcrafted spirit made from 100% fresh MD2 pineapple and neutral cane spirit, showcasing the tropical flavors of the Dominican Republic.

- March 2025: Brugal unveiled Andrés Brugal Edition 02, the second ultra-premium rum in its limited Andrés Brugal Collection, with only 416 bottles released globally at a retail price of USD 3,000 each. According to the brand, it was presented in a bespoke travel-inspired case with a crystal decanter and exclusive glasses and launched worldwide through select retailers in the US and UK.

- February 2025: The Muff Liquor Company, an Irish spirits producer from Donegal, officially launched its premium range in the U.S. market through a partnership with Lucas Bols USA, introducing a potato-based Irish vodka and gin, both distilled six times, and a distinctive peated Irish whiskey, all crafted to honor Irish heritage and craftsmanship.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States spirits market as total annual sales value generated inside the country from distilled beverages, whiskies, brandy & cognac, rum, white spirits, tequila & mezcal, liqueurs, and other minor spirit types sold through both on-trade and off-trade channels, measured at consumer spend levels before taxes and discounts are netted out. Mordor analysts follow the same ABV threshold that regulators use, so beverages below roughly 15% ABV, such as wine, beer, or hard seltzer, sit outside this universe.

Scope Exclusion: The model deliberately ignores alcohol-free spirit analogues and spirit-based RTD cocktails because their pricing structures and taxation differ.

Segmentation Overview

-

By Product Type

- Brandy and Cognac

- Liqueur

- Rum

- Tequila and Mezcal

- Whiskies

- White Spirits

- Other Spirit Types

-

By End User

- Men

- Women

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Others Off Trade Channels

-

By Region

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Multiple structured interviews and short survey check-ins with distillers, distributors, regional control boards, bar managers, and packaging suppliers supplied live perspective on channel inventories, female consumption uptake, and agave-based line extensions. Those insights validate secondary ratios and temper outlier data points before numbers reach the model.

Desk Research

We begin by pulling multi-year consumption and pricing trends from tier-one public sources such as the Distilled Spirits Council, the U.S. Bureau of Economic Analysis, Census Bureau trade tables, and the Tax and Trade Bureau monthly reports. Company 10-Ks, investor decks, and trade press interviews help us capture brand mix shifts and promotional intensity. Subscription databases that Mordor licenses, including D&B Hoovers for distiller financials and Dow Jones Factiva for deal flow, complement those open datasets with granular revenue clues. Patent filings gathered through Questel add an innovation lens that signals upcoming capacity. This list is illustrative; many additional resources inform our continuous evidence loop.

Market-Sizing & Forecasting

We apply a top-down build in which production, import, and export statistics reconstruct total domestic supply; penetration rate-based demand pools by product type balance that supply. Select bottom-up approximations, sampled supplier roll-ups and regional average selling price times 9-liter case volumes, cross-check the totals. Key variables include disposable income, on-premise seat counts, agave spirits retail prices, supplier promotional spend, and legal drinking age population shifts. A multivariate regression coupled with scenario analysis projects those drivers forward to 2030, while gaps in bottom-up inputs are bridged with weighted averages from the nearest verifiable cohort.

Data Validation & Update Cycle

Outputs face variance screens against DISCUS revenue indices and Bureau of Labor Statistics pricing series, then move through a two-level analyst review. We refresh the model yearly, triggering interim revisions after tariff changes, tax hikes, or major M&A announcements.

Why Mordor's US Spirits Industry Size & Share Analysis Baseline Commands Reliability

Published market values often diverge because research firms pick different measurement layers, geographic cuts, and refresh cadences.

Key gap drivers include whether totals are reported at retail or supplier level, inclusion of RTDs, conversion from North America aggregates, and the frequency with which forecasts absorb fresh federal shipment data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 120.34 B (2025) | Mordor Intelligence | |

| USD 182.8 B (2024) | Regional Consultancy A | Scaled down from a North America total and counts full retail spend, with limited cross-checks |

| USD 83.41 B (2024) | Trade Journal B | Grocery channel sample omits on-premise turnover |

| USD 32.46 B (2025) | Global Consultancy C | Supplier shipment revenue only; narrower product slate |

Taken together, the comparison shows that Mordor's disciplined scope selection, dual-path modeling, and annual refresh cadence produce a balanced baseline that decision-makers can trace back to transparent variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the United States spirits market?

The United States spirits market size reached USD 123.48 billion in 2026.

Which product type leads sales in the United States spirits space?

Whiskies hold the top position with 34.58% market share in 2025.

Which region is growing the fastest for spirits in the United States?

The West is forecast to expand at a 3.87% CAGR between 2026 and 2031.

How are on-trade channels performing after the pandemic?

On-trade sales are recovering, posting a projected 2.86% CAGR through 2031 as experiential drinking gains momentum.

What is the main growth driver influencing premium spirits?

Premiumization, fueled by Millennials and Gen Z willingness to pay for quality, remains the leading driver.

Which regulatory hurdle most delays product launches?

TTB’s Certificate of Label Approval extends new-product timelines by 6–8 weeks.

Page last updated on: