Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

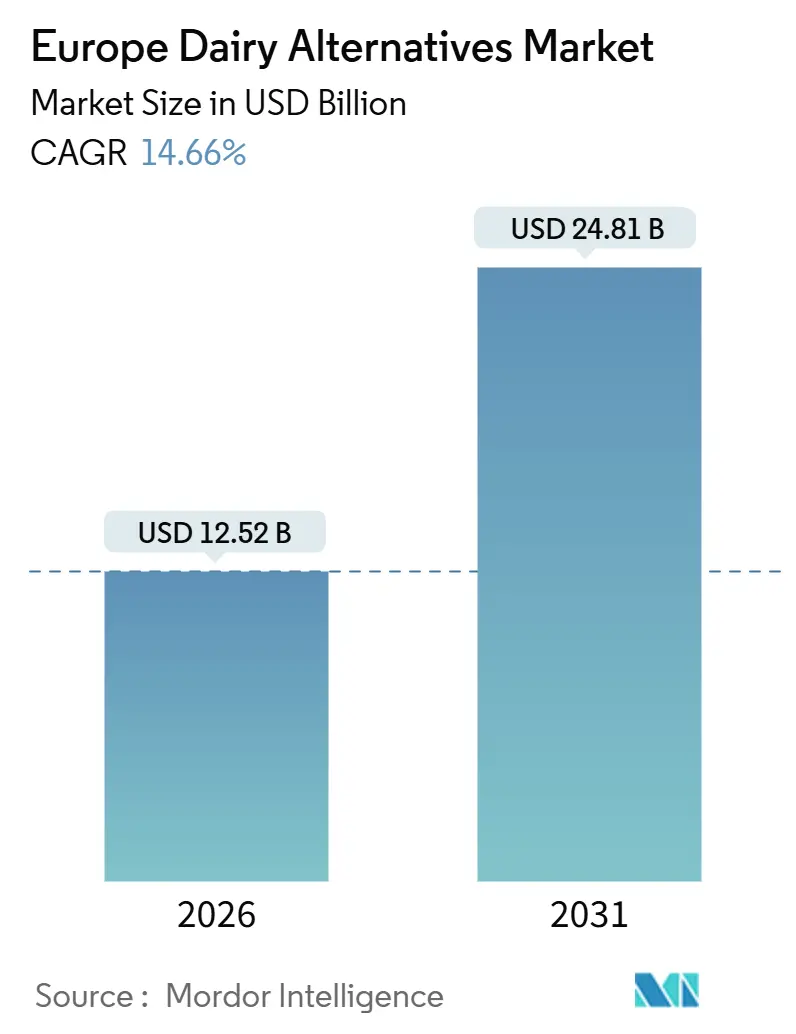

| Market Size (2026) | USD 12.52 Billion |

| Market Size (2031) | USD 24.81 Billion |

| Growth Rate (2026 - 2031) | 14.66% CAGR |

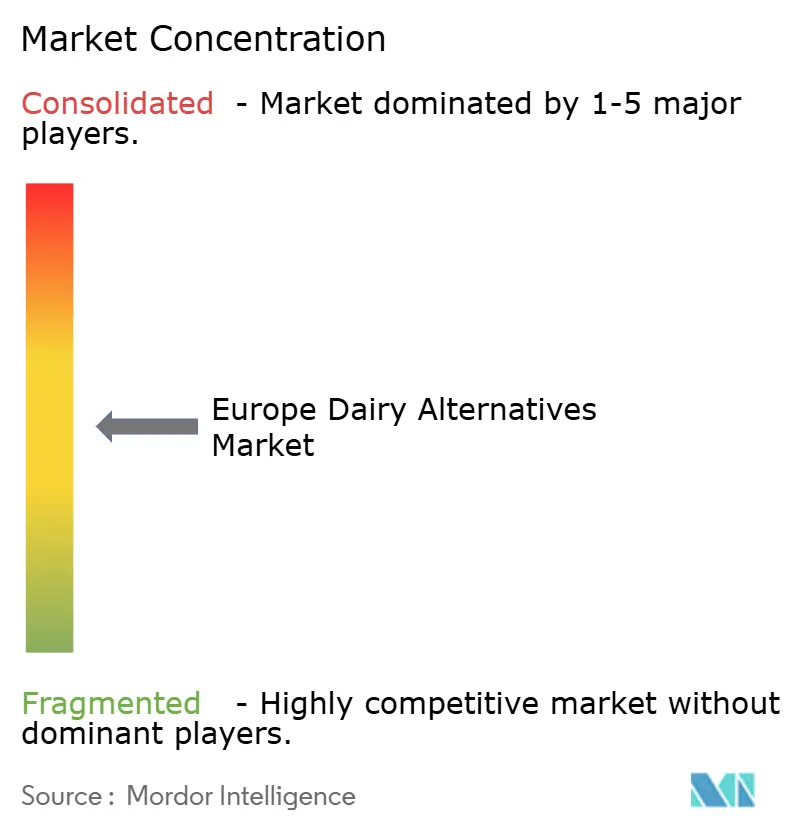

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Dairy Alternatives Market Analysis by Mordor Intelligence

The Europe dairy alternatives market, valued at USD 12.52 billion in 2026, is projected to reach USD 24.81 billion by 2031, growing at a CAGR of 14.66%. This growth reflects a significant structural shift in consumer dietary preferences rather than short-term demand changes. The market expansion is driven by the increasing adoption of plant-based consumption, with dairy alternatives becoming a regular part of daily diets. Rising awareness of lactose intolerance and dairy sensitivity, along with a growing focus on health and wellness, is prompting consumers to choose non-dairy options that are perceived as easier to digest, lower in cholesterol, and supportive of preventive health objectives. Additionally, continuous product innovation and improvements in sensory quality are helping to close the taste and texture gap between dairy alternatives and traditional dairy products.

Key Report Takeaways

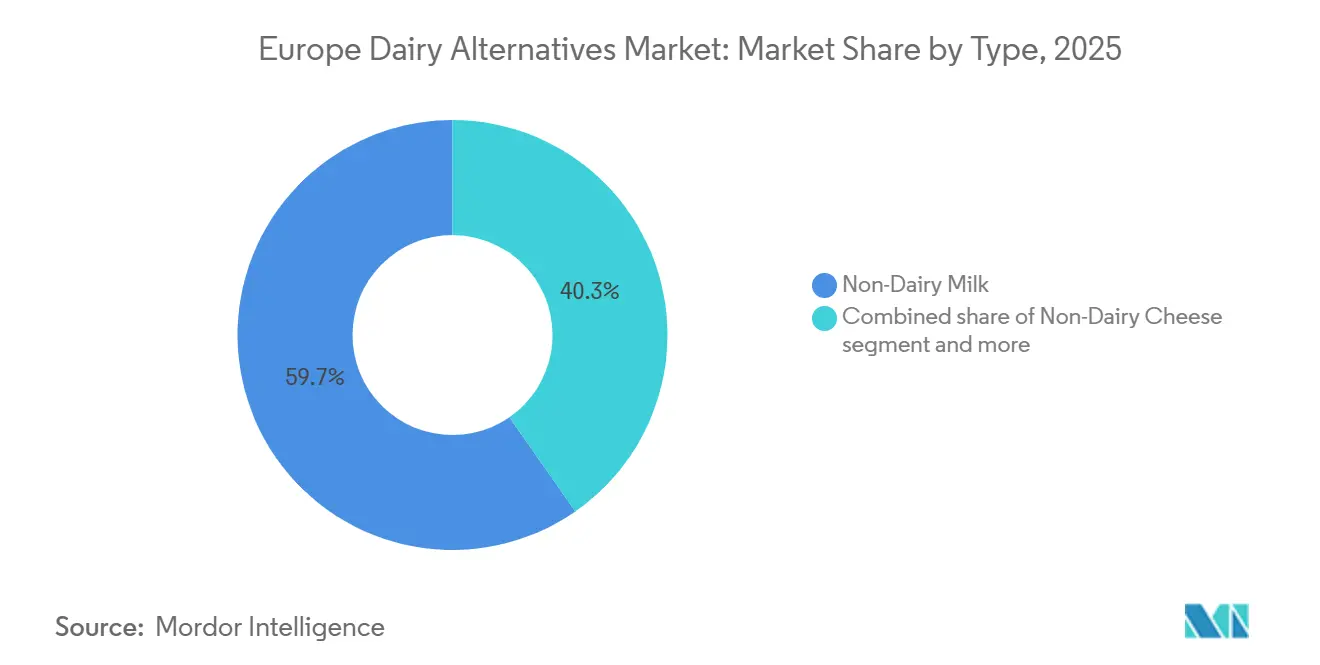

- By product type, non-dairy milk commanded 59.66% of the Europe dairy alternatives market share in 2025, while non-dairy cheese is forecast to expand at a 17.85% CAGR through 2031.

- By flavor, unflavored variants held 66.73% of the Europe dairy alternatives market in 2025; flavored options are set to grow at a 16.43% CAGR through 2031.

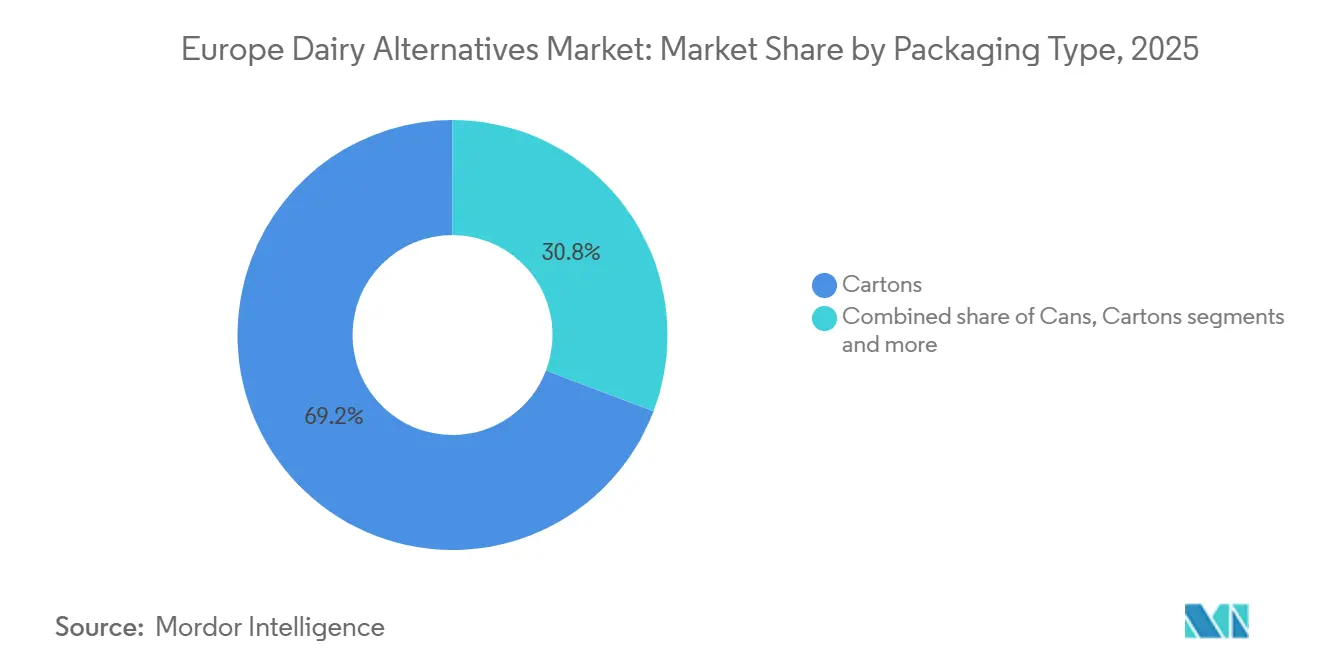

- By packaging type, cartons led with 69.23% of revenue in 2025, whereas PET bottles are advancing at a 14.87% CAGR over the forecast window.

- By distribution channel, off-trade outlets captured 97.22% of sales in 2025, yet on-trade venues are recovering at a 14.86% CAGR as foodservice menus expand plant-based options.

- By geography, Germany accounted for 22.54% of 2025 revenue, and Russia is on track for the fastest 17.81% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Dairy Alternatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lactose intolerance and dairy sensitivity awareness | +3.2% | Southern and Eastern Europe, with elevated prevalence in Italy, Spain, Poland | Medium term (2-4 years) |

| Rising flexitarian eating patterns | +4.1% | Western Europe core (Germany, United Kingdom, France, Netherlands), spillover to Nordic markets | Short term (≤ 2 years) |

| Increasing health and wellness focus | +2.8% | Pan-European, with premium segments in Germany, United Kingdom, Nordics | Long term (≥ 4 years) |

| Product innovation and improved sensory quality | +3.5% | Germany, Netherlands, United Kingdom (innovation hubs), scaling to Southern and Eastern Europe | Medium term (2-4 years) |

| Strong adoption among younger and urban consumers | +2.3% | Urban centers: Berlin, London, Paris, Amsterdam, Stockholm | Short term (≤ 2 years) |

| Sustainability and lower-impact positioning | +2.7% | Northern Europe (Sweden, Netherlands, Germany), expanding to France, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lactose intolerance and dairy sensitivity awareness

Awareness of lactose intolerance and dairy sensitivity is a key factor driving the growth of the dairy alternatives market. Increasing recognition of digestive issues linked to conventional dairy products is influencing consumer consumption patterns. Many individuals are reducing or eliminating lactose-containing products due to symptoms such as bloating, cramps, and digestive discomfort, even without a formal medical diagnosis. This heightened awareness has expanded the consumer base to include not only those diagnosed with lactose intolerance but also self-identified dairy-sensitive and health-conscious consumers. As a result, there has been a rise in the trial and repeat purchases of plant-based alternatives such as milk, yogurt, cheese, and cream. For instance, the Food Standards Agency reported in 2024 that approximately 12% of people in England, Wales, and Northern Ireland identified as having a food intolerance, underscoring the prevalence of digestive-related dietary changes [1]Source: Food Standards Agency, "Prevalence of different types of food hypersensitivity among consumers in the United Kingdom", food.gov.uk. This growing awareness of intolerance is driving demand for lactose-free and plant-based products, positioning digestive comfort as a sustained growth driver for the dairy alternatives market rather than a short-term dietary trend.

Rising flexitarian eating patterns

Flexitarian eating patterns are a key force driving the rapid expansion of the dairy alternatives market, as an increasing number of consumers actively seek to reduce, rather than completely eliminate, animal-based foods from their diets. These consumers prioritize a holistic balance of health, taste, sustainability, and convenience, making dairy alternatives an ideal solution for reducing dairy consumption without disrupting familiar eating habits. Products such as plant-based milk, creamers, and yogurts integrate seamlessly into everyday routines, including coffee preparation, breakfast, and cooking, enabling gradual dietary shifts without the need for strict lifestyle changes. This adaptability has significantly broadened the consumer base beyond vegans and lactose-intolerant individuals, transforming dairy alternatives into widely accepted mainstream products rather than niche offerings. As a result, the market is witnessing increased adoption across diverse demographic groups, further solidifying its position as a staple in modern diets.

Increasing health and wellness focus

Increasing consumer focus on health and wellness is a significant driver of the dairy alternatives market in Europe. Consumers are becoming more aware of the connection between diet, long-term health, and overall well-being. This growing emphasis on preventive health is prompting shoppers to choose foods perceived as lighter, easier to digest, and supportive of balanced nutrition, making dairy alternatives an appealing option compared to traditional dairy products. Plant-based milk, yogurt, and cream alternatives are often associated with lower saturated fat content, no cholesterol, and simpler ingredient lists, which appeal to individuals managing weight, heart health, or general wellness objectives. This health-focused approach is also driving demand for functionally enhanced dairy alternatives. Products fortified with calcium, vitamin D, vitamin B12, and added protein are increasingly sought after to support bone health and meet daily nutritional requirements. Additionally, reduced-sugar, clean-label, and allergen-conscious formulations are gaining popularity, particularly among families, older adults, and health-conscious consumers.

Product innovation and improved sensory quality

Product innovation and enhanced sensory quality are key drivers of the dairy alternatives market. Advancements in formulation science are progressively bridging the long-standing gaps in taste, texture, and functionality compared to conventional dairy products. Earlier versions of dairy alternatives often faced challenges such as chalky textures, poor meltability, or undesirable flavors, which limited their appeal beyond early adopters. Brands are now utilizing techniques such as fermentation, improved fat-protein structuring, and advanced ingredient blending to achieve a creamier mouthfeel, better melting properties, and more authentic dairy-like flavor profiles. These sensory advancements are broadening the range of applications, particularly in cooking, baking, and foodservice, transforming dairy alternatives from niche substitutes into viable everyday options for mainstream and flexitarian consumers. For example, in September 2025, Jay&Joy introduced one of its plant-based cheese alternatives in the United Kingdom for the first time. The product, made entirely from cashew nuts and French soy, underscores the use of premium ingredients and refined formulations to enhance taste and texture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and texture gap versus dairy | -2.1% | Pan-European, most acute in Southern Europe (Italy, Spain, France) with strong dairy culinary traditions | Medium term (2-4 years) |

| Higher price points and value perception | -1.8% | Eastern Europe (Poland, Czech Republic, Hungary), price-sensitive segments in Western Europe | Short term (≤ 2 years) |

| Regulatory restrictions on labeling and claims | -1.2% | Europe-wide, with stricter enforcement in France, Italy regarding dairy nomenclature | Long term (≥ 4 years) |

| Strong cultural attachment to traditional dairy | -1.4% | Southern Europe (Italy, France, Spain, Greece), rural regions across Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Taste and texture gap versus dairy

The taste and texture gap compared to dairy remains a significant restraint for the dairy alternatives market, as many plant-based products continue to face challenges in replicating the sensory experience of conventional dairy. Despite notable advancements, some consumers still perceive dairy alternatives as lacking the creaminess, richness, meltability, and mouthfeel associated with traditional milk, cheese, and yogurt. Additionally, off-notes linked to certain plant bases can negatively impact the eating experience, particularly for first-time or mainstream consumers. This sensory gap reduces repeat purchases and hinders conversion among flexitarian and dairy-attached consumers who prioritize taste parity over ethical or environmental factors. Furthermore, performance limitations in cooking applications also restrict the adoption of dairy alternatives in foodservice and traditional culinary uses. Significant improvements in these areas are essential to drive broader acceptance and growth in the market.

Higher price points and value perception

Higher price points and value perception represent significant structural restraints in the dairy alternatives market, particularly as the category shifts from niche consumption to regular household use. Plant-based dairy products, especially non-dairy cheese, yogurt, and fortified milk alternatives, are often priced at a noticeable premium compared to conventional dairy. This premium is attributed to higher raw material costs, more complex processing requirements, smaller-scale production, and additional investments in formulation and fortification. While early adopters may tolerate these higher prices, mainstream and flexitarian consumers increasingly assess dairy alternatives based on value for money, particularly when these products are intended for frequent, routine consumption rather than occasional use. The challenge of balancing affordability with quality and nutritional benefits remains a critical factor in driving broader adoption of dairy alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Milk Dominates, Cheese Accelerates

Non-dairy milk held a dominant 59.66% market share in the Europe dairy alternatives market in 2025, primarily due to its ability to effectively replicate the role of conventional dairy milk across various consumption scenarios. It is integrated into daily routines such as coffee and tea preparation, breakfast cereals, smoothies, cooking, and baking, resulting in higher purchase frequency and widespread household penetration. Continuous advancements in formulations, particularly barista-style variants with enhanced foaming, creaminess, and heat stability, have further driven its adoption in cafés and foodservice outlets. This shift has transformed non-dairy milk from a niche substitute to a mainstream beverage choice.

Non-dairy cheese is projected to grow at a robust CAGR of 17.85% during 2026–2031, making it the fastest-growing segment in the Europe dairy alternatives market. This growth is driven by significant advancements in product performance and an increase in consumption occasions. Innovations in fermentation technology, improved fat–protein structuring, and the use of functional ingredients have enhanced the sensory properties of non-dairy cheese, making it a closer substitute for conventional cheese. The segment's expansion is further fueled by rising demand for lactose-free and cholesterol-free cheese alternatives, particularly among flexitarians seeking to reduce, rather than completely eliminate, dairy consumption.

By Flavor: Unflavored Leads, Flavored Gains Momentum

Unflavored variants held a dominant 66.73% market share in 2025, highlighting their versatility and functional alignment within the Europe dairy alternatives market. Their strong market position is attributed to their ability to closely replicate the neutral taste of conventional dairy, making them suitable for a variety of everyday applications, including coffee, tea, breakfast cereals, cooking, baking, sauces, and savory recipes. These variants integrate seamlessly into both sweet and savory dishes without altering taste profiles, significantly broadening their usage occasions and driving higher repeat consumption. Additionally, retail placement alongside conventional plain milk and robust private-label offerings has normalized unflavored plant-based products as everyday staples rather than niche items.

Flavored dairy alternative variants are projected to grow at a strong CAGR of 16.43% during 2026–2031, establishing them as a high-growth segment within the Europe dairy alternatives market, despite their smaller base compared to unflavored products. This growth is fueled by increasing consumer demand for indulgent, taste-forward, and experiential plant-based products that go beyond basic dairy substitution to cater to snacking, on-the-go consumption, and dessert-style occasions. Flavored options are particularly appealing to younger consumers and first-time plant-based buyers, as they effectively mask plant-derived aftertastes and provide familiar, comfort-driven flavor experiences. Innovations in natural flavors, reduced-sugar formulations, and clean-label sweetening solutions have further enhanced their appeal among health-conscious consumers seeking a balance between indulgence and wellness.

By Packaging Type: Cartons Dominate, PET Bottles Rise

Cartons held a 69.23% market share in the Europe dairy alternatives market in 2025, establishing themselves as the most preferred and functional packaging format for plant-based dairy products. This dominance is attributed to their compatibility with liquid dairy alternatives, particularly non-dairy milk, where product protection, shelf stability, and ease of handling are essential. Aseptic carton packaging extends shelf life without requiring preservatives or continuous refrigeration, facilitating efficient distribution across urban and remote retail locations while reducing product spoilage. Their lightweight design and efficient cube utilization further enhance logistics efficiency throughout the supply chain. Moreover, cartons align with Europe’s sustainability goals, as they are predominantly paper-based, recyclable in many countries, and considered more environmentally responsible compared to rigid plastic packaging.

PET bottles are projected to grow at a CAGR of 14.87% during 2026–2031, highlighting their increasing role as a flexible and convenience-oriented packaging format in the Europe dairy alternatives market. This growth is driven by the rising demand for ready-to-drink and on-the-go consumption options, where PET bottles offer advantages such as being lightweight, resealable, and shatter-resistant, providing superior portability compared to cartons. PET packaging is particularly suitable for flavored dairy alternatives, protein-enriched plant-based drinks, smoothies, and single-serve formats targeting impulse purchases and convenience-focused channels like cafés, vending machines, gyms, and travel retail. The transparency of PET bottles allows consumers to visually assess product appearance, reinforcing perceptions of freshness and quality, while ergonomic designs improve handling and usability.

By Distribution Channel: Off-Trade Dominates, On-Trade Recovers

Off-trade channels accounted for a significant 97.22% market share in 2025, establishing themselves as the primary distribution network for the Europe dairy alternatives market. This dominance is attributed to the household-oriented nature of dairy alternative consumption, with supermarkets, hypermarkets, convenience stores, and online grocery platforms serving as the main points of purchase. Dairy alternatives are primarily purchased for home use, making off-trade retail the most accessible and routine channel for consumers. Strong shelf visibility alongside conventional dairy products has positioned plant-based alternatives as direct substitutes rather than niche products, encouraging both trial and repeat purchases. Furthermore, digital grocery platforms and click-and-collect services are enhancing off-trade reach by improving convenience and facilitating product discovery.

On-trade channels are experiencing a robust recovery, with a projected CAGR of 14.86% during 2026–2031, reflecting the normalization and renewed momentum of foodservice-led consumption in the Europe dairy alternatives market. This growth is driven by the resurgence of cafés, coffee chains, restaurants, and casual dining outlets, where plant-based dairy alternatives, particularly non-dairy milk, have become standard menu offerings rather than specialty items. Additionally, the increasing demand for inclusive menus catering to lactose-intolerant, vegan, and flexitarian consumers is prompting operators to integrate dairy alternatives into their core offerings. This recovery is further supported by a strong dining-out culture across key European markets. For example, according to IfD Allensbach, dining out remained a popular leisure activity in Germany, with nearly 51.06 million people occasionally dining out in 2025, underscoring the scale of foodservice engagement driving on-trade recovery [2]Source: IfD Allensbach, "Number of people who eat out in their leisure time in Germany", ifd-allensbach.de.

Geography Analysis

Germany is projected to remain the largest market in the European dairy alternatives sector, capturing 22.54% of the market share in 2025. This dominance is supported by its well-established plant-based ecosystem, advanced retail penetration, and high consumer familiarity with dairy-free products. Dairy alternatives are deeply integrated into daily consumption patterns, particularly non-dairy milk used for coffee, breakfast, and cooking. The market benefits from a strong private-label presence and wide SKU availability across supermarkets, discounters, and organic retailers. Product innovation focusing on improved taste, barista performance, and nutritional fortification has further driven repeat purchases. According to the Good Food Institute, 37% of German households purchased plant-based milk and drinks at least once in 2024, underscoring the mainstream acceptance that solidifies Germany’s leadership in Europe [3]Source: Good Food Institute, "Germany plant-based food retail market insights", gfieurope.org.

Russia is forecast to grow at a robust CAGR of 17.81% during 2026–2031, marking the fastest growth among European markets. This growth reflects the early-stage yet accelerating adoption of dairy alternatives. Key drivers include increasing awareness of lactose intolerance, rising interest in plant-based and functional foods among urban consumers, and expanding distribution through modern retail formats. The United Kingdom continues to exhibit steady growth in the dairy alternatives market. This is driven by its dynamic foodservice culture, strong café penetration of plant-based milk, and high visibility of dairy alternatives in both branded and private-label formats. The widespread availability of oat and soy milk in coffee chains, coupled with innovation in flavored and functional variants, is expanding the category beyond early adopters.

Sweden and Belgium are significant contributors to regional growth, supported by high sustainability awareness, openness to plant-forward diets, and strong retail organization. In Sweden, plant-based consumption aligns closely with environmental values, while Belgium benefits from increasing flexitarian behavior and the expansion of chilled plant-based assortments in mainstream retail. These factors are gradually strengthening household penetration in both countries. The Rest of Europe, encompassing Central, Eastern, and Southern European countries, represents a collective growth opportunity. This growth is supported by improving product availability, gradual cultural acceptance, and spillover effects from Western European plant-based trends.

Competitive Landscape

The European dairy alternatives market is moderately fragmented, driven by the presence of multinational food companies, specialized plant-based producers, and strong regional players. The competitive landscape is marked by high intensity, as no single company dominates all product categories. This dynamic has fostered continuous innovation and frequent product launches. Prominent players in the market include Danone S.A., Califia Farms LLC, The Hain Celestial Group Inc., Granarolo S.p.A., and Oatly Group AB. These companies compete across various segments, including non-dairy milk, yogurt, cream, and cheese alternatives, leveraging their brand strength, extensive distribution networks, and investments in product reformulation.

Hybrid product formats are emerging as a significant opportunity within the market. These products, which blend dairy and plant-based ingredients, aim to address sensory gaps while reducing environmental impact. Such innovations resonate with flexitarian consumers who are gradually reducing dairy consumption but still prioritize taste and functionality. This trend highlights the growing demand for products that balance sustainability with consumer preferences. Additionally, regional players are increasingly focusing on premium and niche offerings to differentiate themselves in a competitive market, further diversifying the product landscape.

Technological advancements are playing a critical role in shaping the future of the European dairy alternatives market. Precision fermentation, enzymatic processing, and AI-driven flavor optimization are becoming central to product development, enabling the creation of next-generation alternatives with improved mouthfeel, meltability, and nutritional profiles comparable to traditional dairy. These innovations are raising the bar for product quality and functionality, setting new benchmarks for the industry. As a result, technological capabilities and hybrid product innovations are expected to redefine competitive dynamics, positioning companies with advanced Research and Development (R&D) capabilities at the forefront of the market.

Europe Dairy Alternatives Industry Leaders

-

Califia Farms LLC

-

Danone S.A.

-

The Hain Celestial Group Inc.

-

Granarolo S.p.A.

-

Oatly Group AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Dreamfarm has introduced plant-based cheeses to supermarkets in Paris. The product range includes Mozzarella, Mini Mozzarella, Stracciatella, Plant-Based Spread, and Ricotta. All items are made with natural ingredients and have received a Nutri-Score A rating.

- September 2025: Alt-dairy and cereal brand Moma Foods has launched four innovative oat milk products in the United Kingdom: Salted Maple & Hazelnut Oat Drink, Pistachio Oat Drink, Immunity Support Oat Drink, and RTD Oat Chai Latte.

- August 2025: The Bridge has launched Plant-Based Yogurt under its ViaMia brand at major retailers in Italy. This fermented and organic product is produced using methods similar to conventional yogurt. The product has a shelf life of 80 days.

- January 2025: Califia Farms has introduced a new range of plant-based milks in United Kingdom supermarkets. The Simple and Organic range features almond milk and oat milk, each made with three ingredients: almonds or oats, water, and a hint of salt.

Europe Dairy Alternatives Market Report Scope

Dairy alternatives are plant-based, non-dairy products designed to replicate traditional dairy items. They cater to consumers avoiding lactose, dairy, or animal products due to allergies, intolerances, or dietary preferences such as vegan or health-conscious choices.

The Europe dairy alternatives market has been segmented by type, flavor, packaging, distribution channel, and geography. By type, the market studied is segmented into non-dairy milk, non-dairy cheese, non-dairy desserts, non-dairy yogurt, and others. The non-dairy milk segment is further segmented into oat milk, hemp milk, hazelnut milk, soy milk, almond milk, coconut milk, and cashew milk. By flavour, the market is segmented into flavored and unflavored. By packaging type, the market is segmented into PET bottles, cans, cartons, and others. By Distribution channel, the market is segmented into on-trade and off-trade. The off-trade is further segmented into convenience stores, supermarkets/hypermarkets, online retail stores, and others. By geography, the market is segmented into Germany, the United Kingdom, Italy, France, Spain, the Netherlands, Poland, Belgium, Sweden, and the Rest of Europe.

The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

By Type

| Non-Dairy Milk | Oat Milk |

| Hemp Milk | |

| Hazelnut Milk | |

| Soy Milk | |

| Almond Milk | |

| Coconut Milk | |

| Cashew Milk | |

| Non-Dairy Cheese | |

| Non-Dairy Desserts | |

| Non-Dairy Yogurt | |

| Others |

By Flavor

| Flavored |

| Unflavored |

By Packaging Type

| PET Bottles |

| Cans |

| Cartons |

| Others |

By Distribution Channel

| On-trade | |

| Off-trade | Convenience Stores |

| Supermarkets and Hypermarkets | |

| On-line Retail Stores | |

| Others (Warehouse clubs, gas stations, etc.) |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Type | Non-Dairy Milk | Oat Milk |

| Hemp Milk | ||

| Hazelnut Milk | ||

| Soy Milk | ||

| Almond Milk | ||

| Coconut Milk | ||

| Cashew Milk | ||

| Non-Dairy Cheese | ||

| Non-Dairy Desserts | ||

| Non-Dairy Yogurt | ||

| Others | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Packaging Type | PET Bottles | |

| Cans | ||

| Cartons | ||

| Others | ||

| By Distribution Channel | On-trade | |

| Off-trade | Convenience Stores | |

| Supermarkets and Hypermarkets | ||

| On-line Retail Stores | ||

| Others (Warehouse clubs, gas stations, etc.) | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms