Cervical Dystonia Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

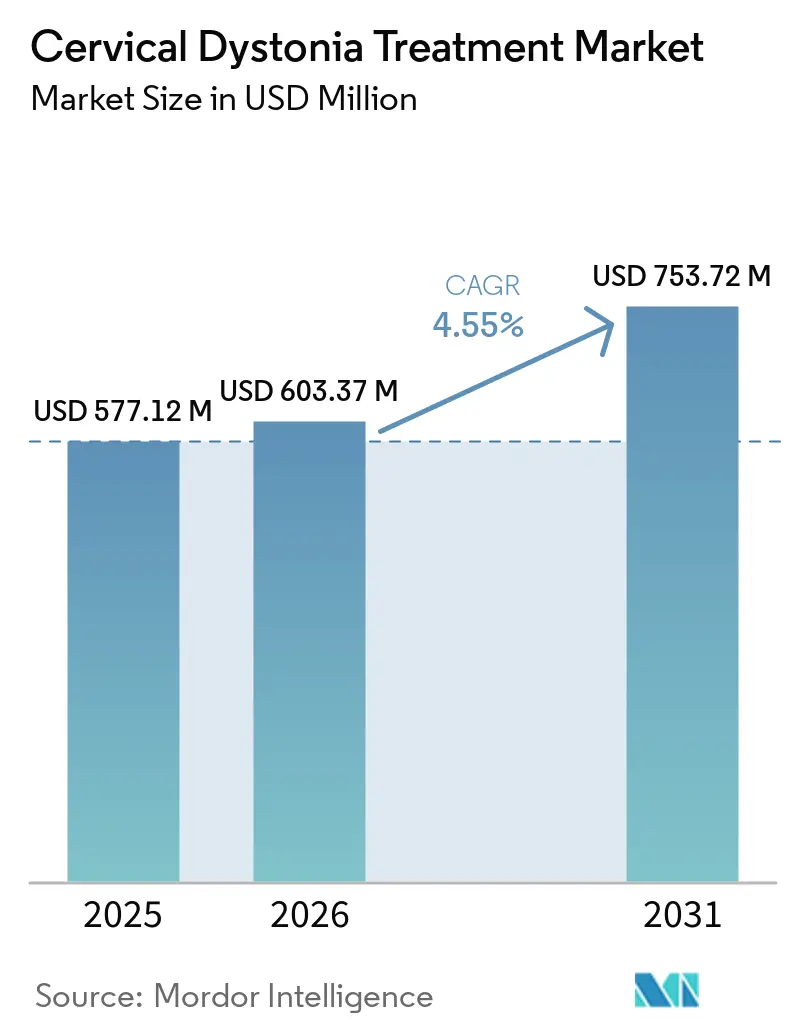

| Market Size (2026) | USD 603.37 Million |

| Market Size (2031) | USD 753.72 Million |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cervical Dystonia Treatment Market Analysis by Mordor Intelligence

The Cervical Dystonia Treatment Market size is expected to grow from USD 577.12 million in 2025 to USD 603.37 million in 2026 and is forecast to reach USD 753.72 million by 2031 at 4.55% CAGR over 2026-2031.

The cervical dystonia treatment market is expanding because treatment intensity is rising, as more patients who once cycled through weak symptom control are moving toward longer-acting formulations and guided injection protocols that shorten the retreatment gap. The cervical dystonia treatment market still loses part of its addressable demand because diagnostic delay remains long, and earlier screening in mid-life neurology settings can therefore lift revenue faster than the headline growth rate alone suggests. The treatment model remains anchored in botulinum toxin use, which gives established brands a durable revenue base and also makes oral adjunct growth dependent on injection therapy rather than separate from it. The cervical dystonia treatment market is also seeing competitive pressure widen at the edges, as longer-duration toxins gain backing and device-based therapy receives stronger regulatory support. The main risk remains reimbursement friction around retreatment timing, because payer rules built around older toxin cycles can limit uptake even when clinical evidence supports longer duration of effect.

Key Report Takeaways

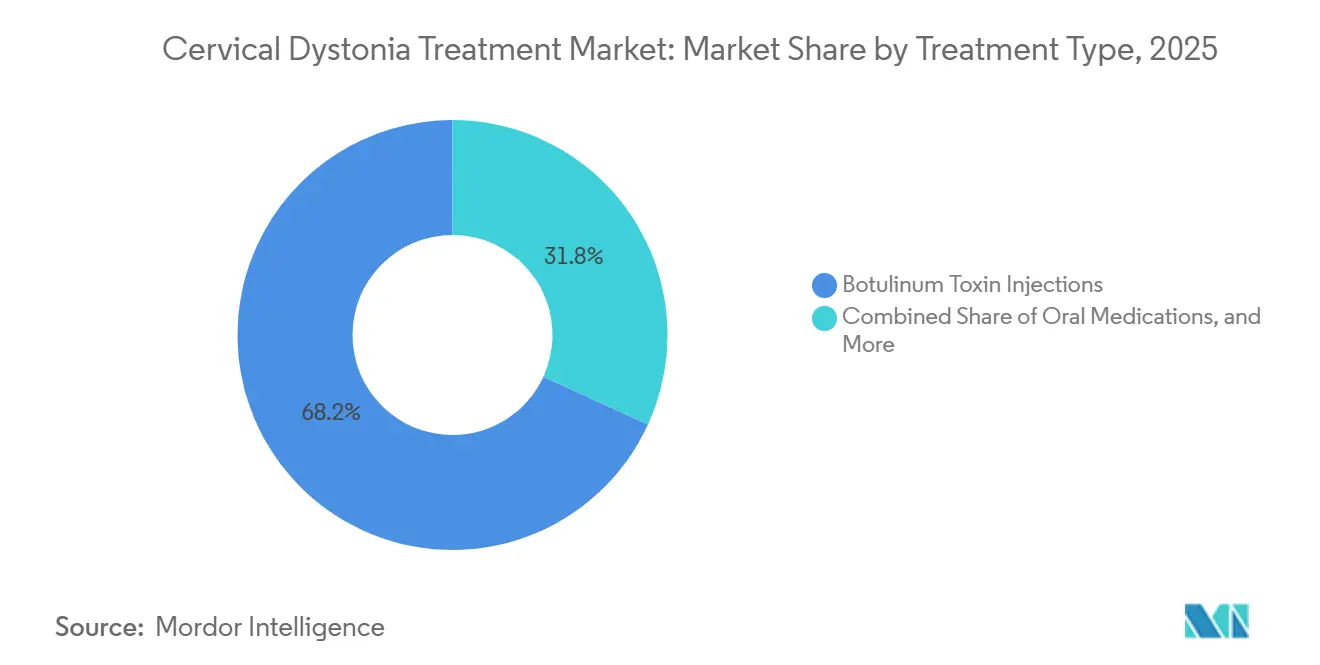

- By treatment type, botulinum toxin injections held 68.2% of the cervical dystonia treatment market share in 2025, and oral medications are forecast to expand at 7.0% through 2031.

- By care setting, hospitals accounted for 61.2% of the cervical dystonia treatment market size in 2025, and home care and rehabilitation centers are advancing at 7.5% through 2031.

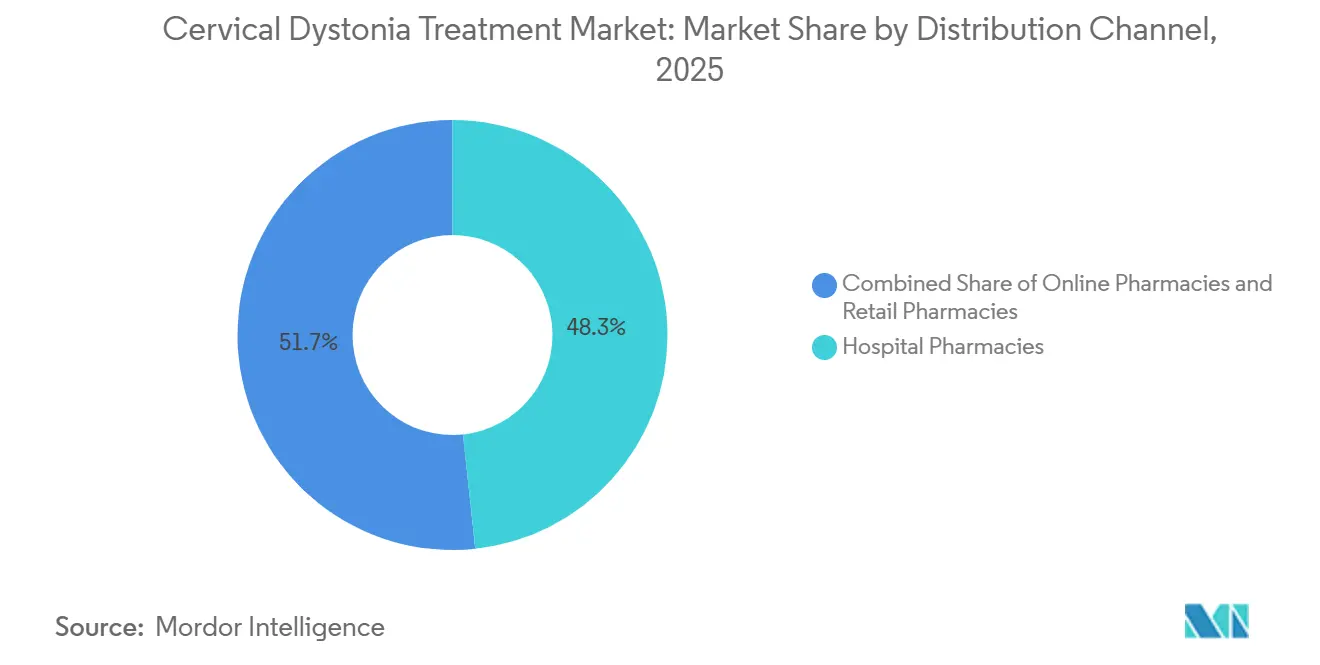

- By distribution channel, hospital pharmacies captured 48.3% share of the cervical dystonia treatment market size in 2025, and online pharmacies are projected to grow at 7.3% through 2031.

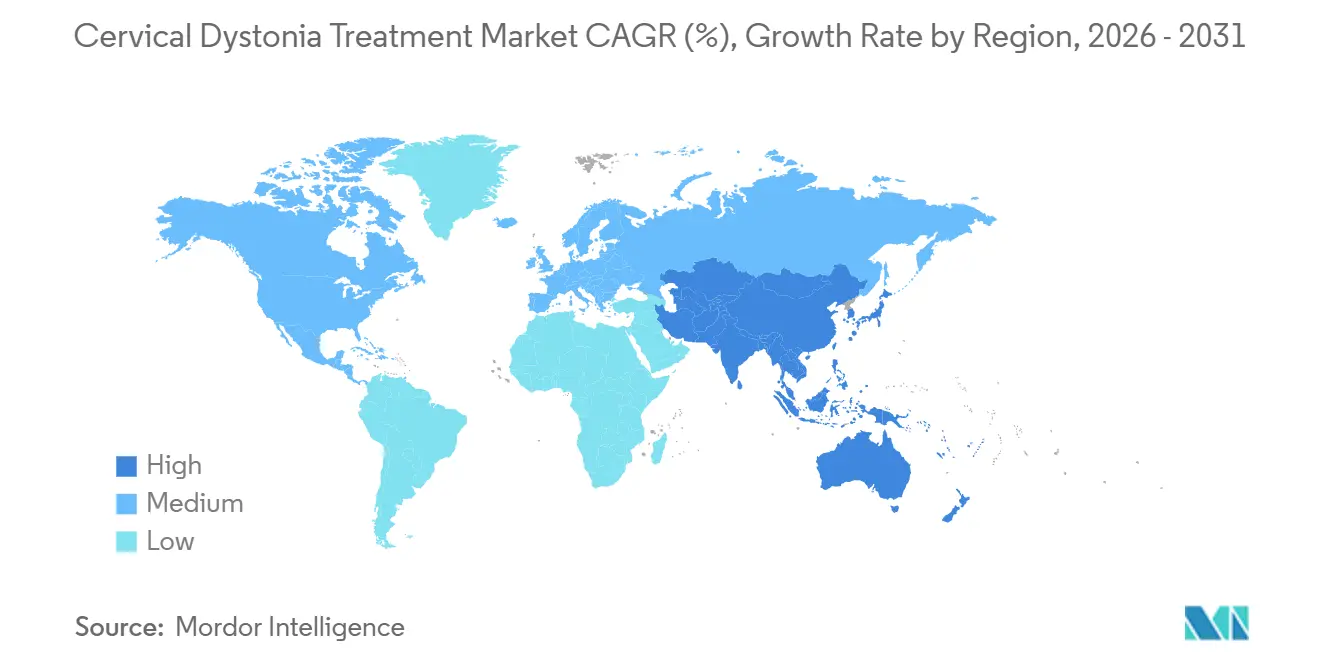

- By geography, North America held 41.2% of the cervical dystonia treatment market share in 2025, and Asia-Pacific is projected to expand at 6.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cervical Dystonia Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diagnosis Rates In Mid-Life Neurology Cohorts | +0.6% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| Longer-Acting Toxin Innovation And Label Expansion | +1.4% | North America, with spill-over to EU and APAC | Short term (≤ 2 years) |

| Chronic First-Line Positioning Of Botulinum Neurotoxins | +1.2% | Global | Long term (≥ 4 years) |

| Ultrasound And EMG-Guided Injection Precision Gains | +0.5% | North America, EU, Japan, South Korea | Medium term (2-4 years) |

| Patient Affordability And Reimbursement-Support Programs | +0.4% | North America, EU core markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis Rates in Mid-Life Neurology Cohorts

The cervical dystonia treatment market still leaves revenue on the table when patients spend years moving through general neurology visits before reaching a movement disorder specialist. Earlier diagnosis in mid-life cohorts matters because this is the stage when persistent abnormal posture, tremor, and pain are more likely to be recognized as a treatable dystonia pattern rather than a musculoskeletal complaint. Patients who enter treatment earlier often do so with less accumulated cervical degeneration and a lower baseline pain burden, which supports steadier follow-up and better continuity across injection cycles. That change has a direct commercial effect because recurring therapies depend on retention, not only on first diagnosis. The cervical dystonia treatment market therefore benefits when referral pathways shorten the lag between first symptoms and specialist confirmation. This effect is likely to emerge first in health systems that already have dense neurology networks and established referral routes.

Longer-Acting Toxin Innovation and Label Expansion

Longer-duration toxin development is the clearest formulation shift now shaping the cervical dystonia treatment market. DAXXIFY received U.S. approval for cervical dystonia in August 2023, and its commercial roll-out through 2024 introduced the first major therapeutic formulation advance in this class in more than 30 years. In the ASPEN-1 Phase 3 trial, the 125-unit dose showed a median duration of effect of 24 weeks, and dysphagia was reported at 1.6%, compared with the much shorter 10 to 12 week effect window often associated with older clinical practice patterns. Crown Laboratories completed its acquisition of Revance Therapeutics in February 2025 for USD 924 million, which showed that commercial infrastructure is now being built around extended-duration toxin use. Revance also reported that therapeutic revenue for DAXXIFY rose 318% in 2024 to USD 31.4 million, which was modest in absolute terms but meaningful for an asset that had only just entered commercial use. Ipsen added to the long-duration pipeline by initiating a Phase II study of corabotase in cervical dystonia in September 2025, which broadened the cervical dystonia treatment market beyond a single new entrant.

Chronic First-Line Positioning of Botulinum Neurotoxins

The cervical dystonia treatment market remains anchored by botulinum neurotoxins because they are the only treatment class with the strongest clinical recommendation base for this condition. This first-line position creates a durable revenue floor because many patients require repeat injections over long periods, and spontaneous remission is uncommon enough that therapy often becomes chronic. That structure also shapes adjacent categories, since oral agents are being added around toxin therapy rather than replacing it in routine practice. The 2025 valbenazine pilot study is important for that reason, because it used botulinum neurotoxin injection cycles as the treatment backbone and still showed statistically significant improvement on TWSTRS measures and end-of-cycle wearing-off[1]Salma Aziz, Erin Pellot, Laxman Bahroo, Abhishek Wajpe, and Martin T. Taylor, “Efficacy and Safety of Valbenazine in the Treatment of Cervical Dystonia: A Pilot Study,” Dystonia, frontierspartnerships.org. The same pattern appears in commercial performance, as Supernus reported MYOBLOC net product sales of USD 101.1 million in 2024, up from USD 91.9 million in 2023, reflecting stable demand for the Type B niche in secondary non-responders. The cervical dystonia treatment market therefore grows through layered therapy use, where injectables stay central and adjunct categories expand around them.

Ultrasound and EMG-Guided Injection Precision Gains

Guided injection practice is changing both outcomes and treatment economics in the cervical dystonia treatment market. A 2025 retrospective two-center study found that ultrasound-guided and EMG-guided injections each delivered 81% to 82% pain relief, compared with 40% using anatomical landmark guidance alone. A separate systematic review through December 2024 showed that ultrasound guidance improved anatomical accuracy, especially for deep neck muscles, and also reduced adverse events. Better targeting matters because it strengthens symptom control and can reduce the need for corrective follow-up in difficult muscle groups. CMS Medicare policy covers EMG guidance for botulinum toxin injection when clinically necessary, but ultrasound reimbursement remains less consistent across payers, which creates a cost barrier for smaller community neurology practices. As more injectors train on guidance-based protocols, the cervical dystonia treatment market is likely to concentrate more referrals in high-volume specialist centers that can support these techniques consistently.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Recurring Therapy Cost And Reimbursement Friction | -0.7% | North America, with spill-over to EU | Medium term (2-4 years) |

| Misdiagnosis And Limited Specialist Injector Capacity | -0.5% | Global, acute in APAC and MEA | Long term (≥ 4 years) |

| Secondary Non-Response And End-Of-Cycle Symptom Rebound | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Recurring Therapy Cost and Reimbursement Friction

Recurring cost remains one of the most important constraints on the cervical dystonia treatment market because branded toxin use requires repeat administration over long periods. In the United States, prior authorization under commercial and Medicare Advantage plans often requires diagnosis confirmation, muscle-level injection records, and proof of prior treatment response before another cycle is approved. When administrative delays push patients past planned retreatment timing, symptom control can fall sharply and disability can return, which raises the risk of discontinuation. CMS policy generally limits injections to every 12 weeks and was built around older toxin patterns, which creates a poor fit for products such as DAXXIFY that showed a 24-week median duration of effect in trial data[2]Centers for Medicare & Medicaid Services, “Billing and Coding: Botulinum Toxins (A57185),” Centers for Medicare & Medicaid Services, cms.gov. Physicians are then left to justify retreatment timing or manage expectations around a policy-driven care gap that does not always match clinical reality. Even when manufacturers provide support services, the cervical dystonia treatment market remains exposed to payer timing rules that can limit both utilization and satisfaction.

Misdiagnosis and Limited Specialist Injector Capacity

The cervical dystonia treatment market is also constrained by how often this disorder is confused with essential tremor, cervical radiculopathy, or functional movement disorders before a specialist assessment is made. Diagnostic confirmation usually requires a movement disorder specialist, and those clinicians remain concentrated in referral centers rather than spread evenly across community settings. That supply imbalance suppresses treatment starts even when approved products are available and reimbursed. It also lowers repeat-injection frequency when patients must travel far or wait long for specialized appointments. Training in EMG and ultrasound-guided injection technique is part of the same bottleneck, because skilled administration capacity matters as much as drug supply in this category. Unless the injector base broadens over time, the cervical dystonia treatment market will continue to show stronger revenue concentration around specialist centers than around broad community access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Oral Agents Emerge as Botulinum Toxin Adjuncts

Botulinum toxin injections accounted for 68.2% of revenue in 2025, which kept them firmly in the lead across treatment categories in the cervical dystonia treatment market. Their position reflects long-standing specialist familiarity, durable reimbursement pathways, and the fact that they remain the most established first-line option for symptom control. OnabotulinumtoxinA continues to hold brand leadership within this group because injector habit and formulary preference still matter heavily in routine practice. IncobotulinumtoxinA keeps a distinct role through its protein-free formulation, and that profile gained added commercial relevance when Merz Therapeutics enrolled the first patients in its Phase III MINT-E and MINT-C migraine prevention trials in August 2025. RimabotulinumtoxinB also keeps a structurally important place in the cervical dystonia treatment industry because it serves Type A secondary non-responders, and MYOBLOC net product sales reached USD 101.1 million in 2024, up 10% year over year.

Oral medications are projected to expand at 7.0% through 2031, making them the fastest-growing treatment class in the cervical dystonia treatment market. That growth reflects adjunct use rather than replacement, since valbenazine improved TWSTRS scores and reduced end-of-cycle wearing-off when added to botulinum neurotoxin treatment in a 2025 pilot study. Generic penetration in anticholinergics and benzodiazepines also supports uptake where access to toxin treatment is limited or delayed. Device-based and surgical options remain smaller because they are reserved for refractory patients, yet the December 2025 FDA labeling change for Medtronic DBS should broaden payer willingness to cover this part of the cervical dystonia treatment industry.

By Care Setting: Shift Toward Decentralized Delivery

Hospitals held 61.2% of care-setting revenue in 2025, which kept institutional care at the center of the cervical dystonia treatment market. This pattern fits current practice because botulinum toxin injections, especially with EMG or ultrasound guidance, often require neurophysiology equipment, trained staff, and escalation support that smaller offices cannot always provide. Specialty neurology clinics remain the second-largest segment because patients often move into ambulatory specialist care after their injection pattern becomes stable. Home care and rehabilitation centers are projected to expand at 7.5% through 2031, which makes them the fastest-growing care setting in the cervical dystonia treatment market. Their rise reflects the growing use of supportive therapies, including physiotherapy delivered through specialized rehabilitation environments rather than only through hospital outpatient departments.

Ambulatory surgical centers are also gaining relevance because payers have reason to steer selected DBS procedures toward lower-cost settings where operating workflows are more standardized. This change becomes more practical as neurostimulator systems reduce the ongoing management burden after implantation. Medtronic states that Percept PC and Percept RC neurostimulators include BrainSense technology and full-body MRI conditional access, which lowers some of the operational complexity around follow-up. Even with that shift, the cervical dystonia treatment market is likely to remain partly hospital anchored because specialist oversight and guided injection capability still shape referral behavior more than site-of-care cost alone.

By Distribution Channel: Online Pharmacies Gain Ground on a Fragile Base

Hospital pharmacies captured 48.3% of distribution-channel revenue in 2025, which kept institutional procurement dominant in the cervical dystonia treatment market. That concentration mirrors the care-setting structure, since injectable toxin products are usually purchased, stored, and administered through institutional channels rather than through open retail distribution. Retail pharmacies mainly serve the oral segment, where anticholinergics, benzodiazepines, and muscle relaxants provide a steady adjunct revenue stream between injection visits. Online pharmacies are projected to grow at 7.3% through 2031, but that growth starts from a narrow base in the cervical dystonia treatment market. Cold-chain handling, controlled dispensing rules, and payer requirements for institutional administration keep most toxin products outside standard e-pharmacy fulfillment.

Digital engagement still matters because it can support refill behavior, benefit coordination, and specialty-pharmacy routing for adjunct therapies. Supernus amended its manufacturing agreement with Merz Pharma GmbH in July 2025 by removing the annual minimum purchase requirement for MYOBLOC and replacing it with an annual reservation fee of EUR 3.0 million (USD 3.2 million), a change that pointed to a more flexible supply model. The same filing showed USD 26.9 million in 2025 sales within the Other category, which supports the view that specialty and direct-to-physician channels are becoming more important for selected products. The cervical dystonia treatment market is therefore seeing digital distribution grow mainly around oral adjuncts and specialized fulfillment, not around broad online access for injectable neurotoxins.

Geography Analysis

North America held 41.2% of revenue in 2025, which gave the region the largest share in the cervical dystonia treatment market. The United States remained the largest country base, and AbbVie reported USD 3.151 billion in U.S. therapeutic neurotoxin revenue in 2025 across its full therapeutic portfolio. Regional growth still faces a reimbursement ceiling because CMS timing rules do not fully align with the longer duration shown for DAXXIFY in clinical data. At the same time, North America benefits from dense specialist access, established prior authorization pathways, and early commercial adoption of new toxin formats. These factors keep the cervical dystonia treatment market strong in the region even when payer friction slows full use of extended-duration products.

Europe remained the second-largest regional block in the cervical dystonia treatment market, supported mainly by Germany, France, and the United Kingdom. Ipsen reported EUR 158.4 million in European Dysport Therapeutics revenue in 2025, equal to USD 168.1 million, with 6.8% constant-exchange-rate growth[3]Ipsen, “Ipsen Delivers Strong Results in 2025, Driven by Solid Execution Across All Therapeutic Areas, and Provides 2026 Guidance,” Ipsen, ipsen.com. The region benefits from broad specialist expertise and favorable reimbursement in core countries, though centralized referral structures can still limit throughput at the provider level. Merz also enrolled the first patients in 2 global Phase III migraine trials for Xeomin in August 2025, which reinforced its broader neurology positioning from a European base.

Asia-Pacific is projected to expand at 6.3% through 2031, which makes it the fastest-growing regional part of the cervical dystonia treatment market. Growth is being supported by broader specialist infrastructure, competitive activity from regional neurotoxin manufacturers, and a wider set of commercialization pathways than the region had a few years ago. Hugel has cervical dystonia in Phase I development for its botulinum toxin program, which shows that the regional pipeline is moving beyond cosmetic use into therapeutic positioning. South America and the Middle East and Africa remain early-stage, though Daewoong’s February 2025 launch of Nabota in Saudi Arabia shows that geographic expansion is continuing outside the largest established markets.

Competitive Landscape

The cervical dystonia treatment market is moderately concentrated around established botulinum toxin type A suppliers, AbbVie, Ipsen, Merz Pharma, and Revance, while Supernus keeps a separate position in type B. AbbVie remains the scale leader, as BOTOX Therapeutic generated USD 3.769 billion in global 2025 therapeutic neurotoxin revenue, far above the revenue disclosed for other toxin programs. That scale advantage matters because injector familiarity, multi-indication labeling, and preferred formulary placement create real switching costs in everyday specialist practice. Crown’s February 2025 acquisition of Revance gave DAXXIFY stronger commercial backing at the moment when longer-duration competition started to matter more. Ipsen is pushing the next formulation wave through corabotase, where cervical dystonia Phase II development started in September 2025, and Merz is widening neurological visibility through new Xeomin trial activity.

The cervical dystonia treatment market still has open space in guided-injection infrastructure, patient monitoring, and adjunct oral therapy support. Clinical evidence now shows materially better pain relief when injections are guided by EMG or ultrasound, yet this has not been converted into a standardized training model that scales evenly across community practice. Medtronic also changed the competitive frame in December 2025 when dystonia labeling for its DBS platform moved from humanitarian device exemption status to full effectiveness labeling, which should improve reimbursement access for refractory patients. This means the cervical dystonia treatment market is now competing on duration, precision, and access support, not only on the legacy strength of individual toxin brands.

Smaller entrants still face high technical and funding barriers because biologic toxin comparability is difficult and regulatory pathways remain demanding. Biosimilar development could eventually pressure pricing in the dominant type A segment, but the clinical and manufacturing hurdles in this class remain substantial. Supernus keeps a defensible niche because MYOBLOC is the only approved type B option, and that makes it valuable for secondary non-responders rather than for broad first-line switching. The cervical dystonia treatment market therefore looks open to selective disruption, but not to rapid commoditization.

Cervical Dystonia Treatment Industry Leaders

AbbVie Inc.

Ipsen S.A.

Merz Pharma GmbH & Co. KGaA

Revance Therapeutics, Inc.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: At the TOXINS 2026 conference in Madrid, Spain, Ipsen shared 14 presentations focusing on different neurological conditions. The findings highlighted the extensive research on movement disorders like post-stroke spasticity, cervical dystonia, and blepharospasm. These insights not only strengthened the existing evidence for Dysport (abobotulinumtoxinA) in improving patient care but also introduced potential new treatment options currently being explored.

- December 2025: Medtronic plc received U.S. Food and Drug Administration (FDA) approval of its expanded Dystonia clinical labeling for Medtronic Deep Brain Stimulation (DBS).

Global Cervical Dystonia Treatment Market Report Scope

As per the scope of the report, cervical dystonia treatment refers to the medical interventions and therapies aimed at alleviating the symptoms of cervical dystonia, a neurological movement disorder characterized by involuntary muscle contractions in the neck, leading to abnormal head postures and pain.

The segmentation of the cervical dystonia treatment market is categorized by treatment type, care setting, distribution channel, and geography. By treatment type, the market includes botulinum toxin injections, oral medications, device-based and surgical interventions, and supportive and adjunctive therapies. Botulinum toxin injections are further segmented into type A neurotoxins, which include onabotulinumtoxinA, abobotulinumtoxinA, incobotulinumtoxinA, and other type A neurotoxins, and type B neurotoxins, which include rimabotulinumtoxinB. Oral medications are classified into anticholinergics, benzodiazepines and GABAergic agents, muscle relaxants, and dopaminergic and VMAT-modulating agents. Device-based and surgical interventions include deep brain stimulation and selective peripheral denervation. By care setting, the market is divided into hospitals, specialty neurology clinics, ambulatory surgical centers, and home care and rehabilitation centers. By distribution channel, the segmentation includes hospital pharmacies, retail pharmacies, and online pharmacies.

Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Botulinum Toxin Injections | Type A Neurotoxins | OnabotulinumtoxinA |

| AbobotulinumtoxinA | ||

| IncobotulinumtoxinA | ||

| Other Type A Neurotoxins | ||

| Type B Neurotoxins | RimabotulinumtoxinB | |

| Oral Medications | Anticholinergics | |

| Benzodiazepines and GABAergic agents | ||

| Muscle relaxants | ||

| Dopaminergic and VMAT-modulating agents | ||

| Device-based and Surgical Interventions | Deep Brain Stimulation | |

| Selective Peripheral Denervation | ||

| Supportive and Adjunctive Therapies | ||

| Hospitals |

| Specialty Neurology Clinics |

| Ambulatory Surgical Centers |

| Home Care and Rehabilitation Centers |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Botulinum Toxin Injections | Type A Neurotoxins | OnabotulinumtoxinA |

| AbobotulinumtoxinA | |||

| IncobotulinumtoxinA | |||

| Other Type A Neurotoxins | |||

| Type B Neurotoxins | RimabotulinumtoxinB | ||

| Oral Medications | Anticholinergics | ||

| Benzodiazepines and GABAergic agents | |||

| Muscle relaxants | |||

| Dopaminergic and VMAT-modulating agents | |||

| Device-based and Surgical Interventions | Deep Brain Stimulation | ||

| Selective Peripheral Denervation | |||

| Supportive and Adjunctive Therapies | |||

| By Care Setting | Hospitals | ||

| Specialty Neurology Clinics | |||

| Ambulatory Surgical Centers | |||

| Home Care and Rehabilitation Centers | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the cervical dystonia treatment market?

The cervical dystonia treatment market was valued at USD 577.12 million in 2025 and is expected to reach USD 603.37 million in 2026 before rising to USD 753.72 million by 2031.

Which therapy type leads cervical dystonia treatment spending?

Botulinum toxin injections led revenue with 68.2% share in 2025, reflecting their entrenched first-line role and strong specialist familiarity.

Why are oral medications growing faster in cervical dystonia treatment?

Oral medications are projected to grow at 7.0% through 2031 because they are being added as adjuncts to toxin therapy, supported by valbenazine data and broad generic availability in older oral classes.

Which region is growing fastest for cervical dystonia treatment?

Asia-Pacific is the fastest-growing region, with a projected 6.3% CAGR through 2031, driven by expanding specialist infrastructure and increasing regional therapeutic activity.

How does reimbursement affect DAXXIFY uptake in cervical dystonia treatment?

Reimbursement remains a constraint because CMS timing rules are generally built around 12-week injection intervals, while DAXXIFY showed a 24-week median duration in clinical data.

Which companies shape competition in cervical dystonia treatment?

AbbVie, Ipsen, Merz Pharma, Revance, Supernus, and Medtronic are the main companies shaping competition through toxin brands, pipeline activity, support programs, and DBS expansion.

Page last updated on: