Small Cell Networks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

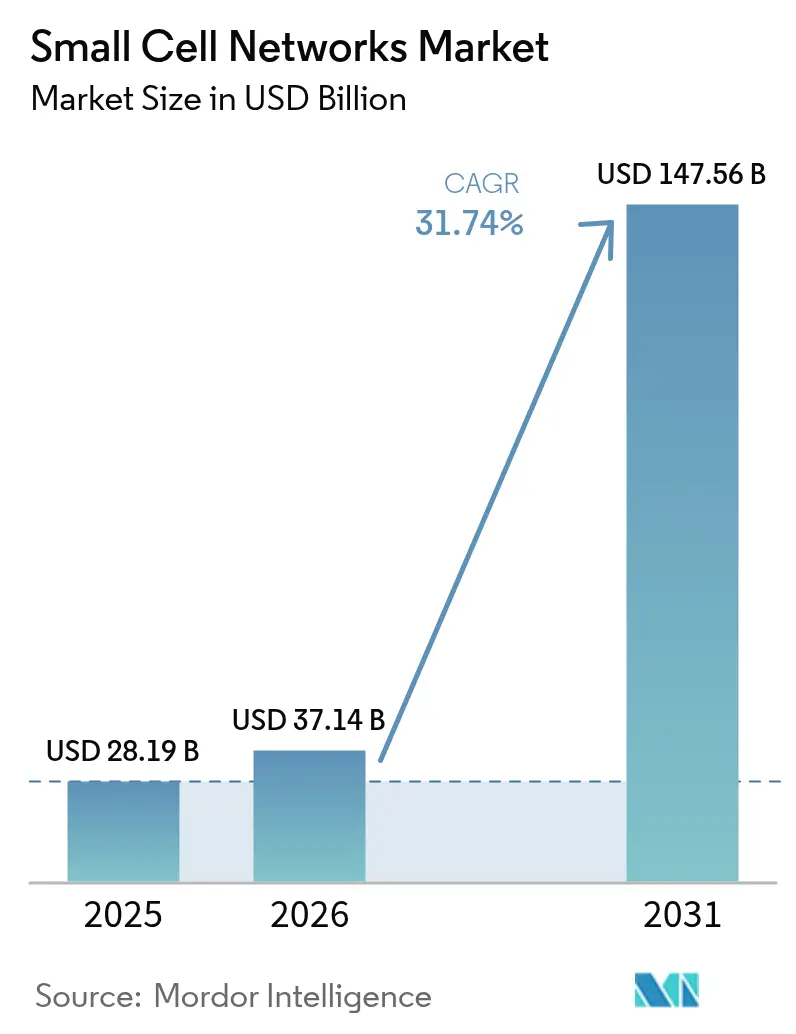

| Market Size (2026) | USD 37.14 Billion |

| Market Size (2031) | USD 147.56 Billion |

| Growth Rate (2026 - 2031) | 31.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Cell Networks Market Analysis by Mordor Intelligence

Small cell networks market size in 2026 is estimated at USD 37.14 billion, growing from 2025 value of USD 28.19 billion with 2031 projections showing USD 147.56 billion, growing at 31.74% CAGR over 2026-2031. Rising mobile-data volumes, the transition to higher-frequency 5G bands, and supportive spectrum policies have moved small cells from niche solutions to core network assets. Carriers now treat densification as a necessity because millimeter-wave and mid-band signals attenuate rapidly, especially indoors, where more than 80% of traffic originates.[1]Ericsson, “5G Indoor Coverage – Small Cell Solutions,” ericsson.com Early wins with shared and neutral-host models are lowering ownership costs, while AI-enabled self-optimizing features are cutting energy use by up to 45% relative to traditional distributed antenna systems. Consolidation is intensifying as incumbents seek scale advantages ahead of the AWS-3 auction mandated for completion by June 2026, a sale projected to redirect USD 3 billion–4.5 billion of mid-band spectrum into commercial hands.

Key Report Takeaways

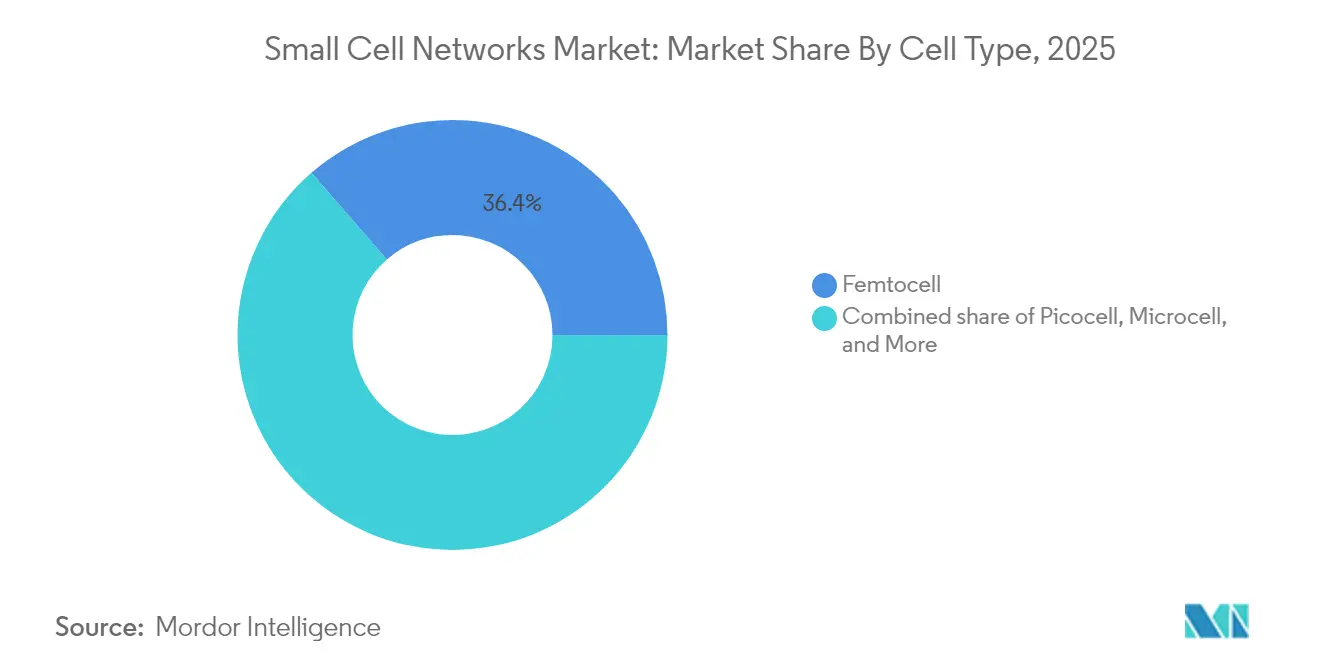

- By cell type, femtocells led with 36.40% of small cell networks market share in 2025; microcells are set to post the fastest 33.75% CAGR through 2031.

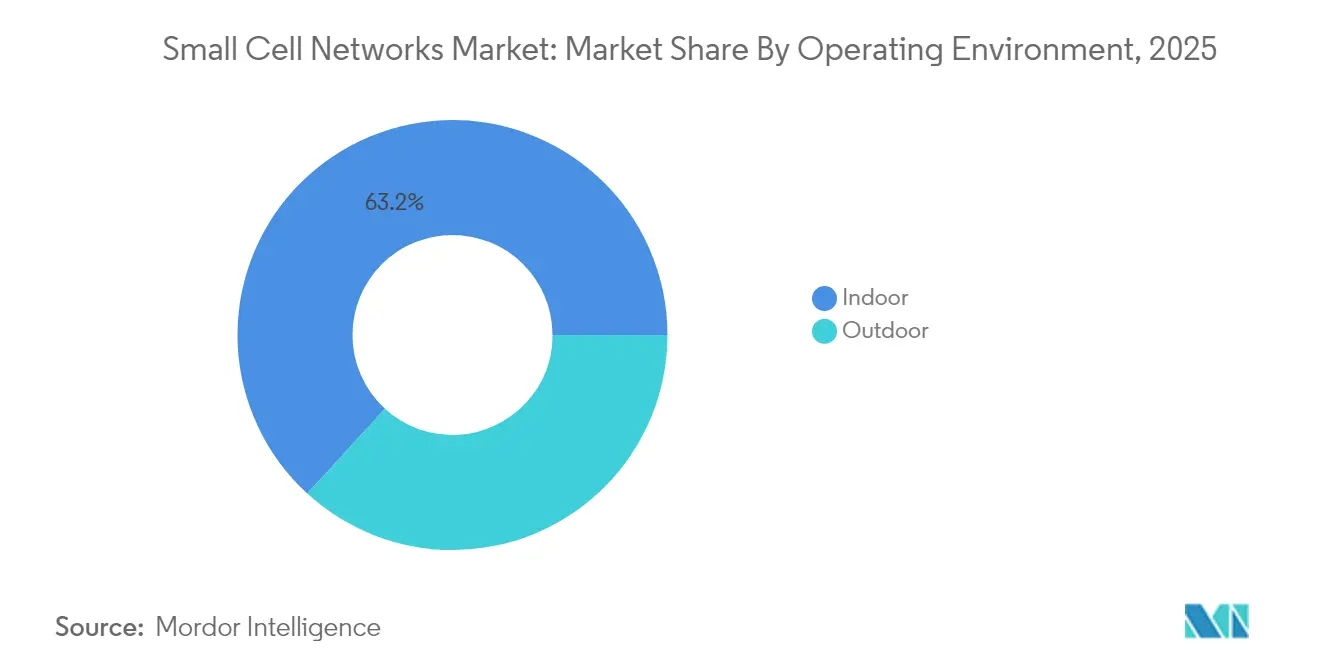

- By operating environment, indoor deployments accounted for 63.20% share of the small cell networks market in 2025, whereas outdoor sites are projected to advance at 36.20% CAGR up to 2031.

- By end-user vertical, IT & telecom held 31.60% share of the small cell networks market in 2025; smart city & government applications are primed for a 34.85% CAGR to 2031.

- By geography, North America commanded 34.20% of the small cell networks market share in 2025, while Asia Pacific is on track for a 36.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Small Cell Networks Market Trends and Insights

Drivers Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex site-acquisition and municipal permitting | -3.7% | Global dense cities | Short term (≤ 2 years) |

| Backhaul fibre / power availability gaps | -2.9% | Emerging markets & rural zones | Medium term (2-4 years) |

| RF front-end chipset export controls and supply risk | -2.1% | Cross-border supply chains | Medium term (2-4 years) |

| Rising energy-efficiency compliance costs | -1.8% | Europe, North America, advanced APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G spectrum auctions accelerate network densification

Mid-band allocations are unlocking the spectral headroom needed for 5G. Independent economic modelling shows that every extra 100 MHz could add USD 264 billion to GDP.[2]CTIA, “The Economic Impact of Allocating Mid-Band Spectrum to Mobile,” ctia.org The forthcoming AWS-3 sale will reinforce this effect. Faster permitting has trimmed U.S. approval cycles from several years to months, enabling operators to scale from macro sites to thousands of street-level nodes per city. Because millimeter-wave signals decay sharply, achieving contiguous coverage can demand up to 10 times more small cells than legacy macrocells, driving orders for compact radios and integrated antennas.

Mobile-data explosion drives adoption

Annual traffic is rising 20%, and 5G will carry 75% of bits by 2029, according to Ericsson. Streaming UHD video, XR content, and cloud gaming create hotspot demand profiles that strain sectorized macros. Targeted clusters of small cells deliver localized capacity without full-scale overlays, enabling operators to throttle capex while preserving user experience. Deployments have already quadrupled over the past decade; industry associations expect an eight-fold increase in the next ten years.[3]5G Americas, “Small Cell Siting Challenges & Recommendations,” 5gamericas.org

Enterprise private networks create new growth vectors

Industrial sites, hospitals and logistics hubs are adopting spectrum-sharing regimes such as CBRS to spin up private 5G. Early U.S. proofs of concept are now entering production, with brands in retail, automotive and aviation citing deterministic latency and improved security as decisive advantages. Small cells—often integrated with on-premise edge platforms—form the radio underpinning for AGV control, real-time analytics and immersive training.

Neutral-host models transform deployment economics

Shared infrastructure lets property owners host one grid of radios that supports multiple carriers, trimming total cost of ownership by up to 80% compared with separate in-building systems, according to Ericsson. Financing momentum is evident: a leading neutral-host provider secured USD 1.2 billion to scale U.S. venues in 2025.[4]Boldyn Networks, “Neutral Host Providers,” boldyn.com The concept is spreading to transport hubs, stadiums, and high-rise complexes where single-operator economics rarely work.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex site-acquisition and municipal permitting | -3.7% | Global dense cities | Short term (≤ 2 years) |

| Backhaul fibre / power availability gaps | -2.9% | Emerging markets & rural zones | Medium term (2-4 years) |

| RF front-end chipset export controls and supply risk | -2.1% | Cross-border supply chains | Medium term (2-4 years) |

| Rising energy-efficiency compliance costs | -1.8% | Europe, North America, advanced APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory hurdles impede deployment velocity

Even after federal streamlining, local rules vary widely. Historic districts often impose design reviews, stretching approvals to 12-24 months and inflating construction budgets. Roughly 20 U.S. states now have small-cell statutes, yet inconsistent interpretation complicates multi-state builds. Operators are standardizing pole-top enclosures and leveraging street furniture leases to shorten cycles, but friction remains a brake on outdoor rollout.

Semiconductor supply constraints threaten scaling

Lead times for RF front-end parts remain 26–52 weeks, according to a major electronics manufacturer, according to Jabil. Export controls have tightened access to advanced chipsets, pushing vendors to diversify foundry partners. Component scarcity lifted radio unit prices nearly 30% between 2023 and 2024, forcing carriers to phase projects and prioritize high-revenue zones while waiting for domestic fab capacity funded under the U.S. CHIPS Act to come online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cell Type: Microcells redefine urban coverage

Femtocells captured 36.40% of 2025 revenue, reflecting their affordability for homes and small offices. They handle up to six users within roughly 60 feet, making them the go-to for spot indoor remediation. Yet microcells are slated to grow fastest at 33.75% CAGR, benefiting from an ability to serve 200 users across 1,000 feet—ideal for dense shopping streets and transit stations. The small cell networks market size for the microcell tier is expected to expand swiftly as carriers combine these nodes with edge compute to support latency-sensitive use cases. Radio designs are also converging with Open RAN standards, enabling multi-vendor ecosystems that reduce lock-in and accelerate innovation.

Compatibility upgrades in picocells—covering 750 feet for mid-sized venues—are unlocking new enterprise contracts, while metrocells are rolling out along arterial roads to smooth hand-offs at pedestrian level. Indoor radio-dot architectures have passed 120 operators and deliver macro-parity speeds with minimal on-site equipment. Collectively, these trends underscore how the small cell networks market is becoming a multi-layered ecosystem rather than a single-device proposition.

By Operating Environment: Outdoor densification gains pace

Indoor systems held 63.20% of 2025 revenue as energy-efficient construction materials hinder macro penetration. Low-E glass and reinforced concrete create Faraday-like enclosures, compelling property owners to deploy dedicated radios that support enterprise mobility, IoT sensors and emergency services. Because more than four-fifths of data sessions start indoors, operators prioritize offices, hospitals and transportation hubs for early builds.

Outdoor deployments, however, will outstrip 36.20% CAGR through 2031 as mid-band 5G migrates from central business districts to suburbs. Forward-looking municipalities are integrating radios into smart streetlights, traffic signals and bus shelters—reducing both visual clutter and permitting obstacles. The small cell networks market size tied to outdoor infrastructure is projected to benefit from autonomous vehicle trials and citywide XR applications that need uniform millisecond latency. As spectrum auctions open additional bands, carriers are seizing the opportunity to overlay macro grids with tight canopies of outdoor nodes, ensuring seamless hand-offs and raising average downlink speeds.

By End-user Vertical: Smart cities set the innovation agenda

IT & telecom operators accounted for 31.60% revenue in 2025 as they race to unlock 5G monetization. Tier-1 carriers are targeting 70% of traffic to traverse open-capable platforms by 2026, a strategy that favors modular small cells for agile upgrades. Integration with massive-MIMO macrocells creates a layered architecture where capacity is dynamically steered to hotspots.

Municipal smart-city initiatives will post the fastest 34.85% CAGR. Cities deploy curbside radios to underpin intelligent transport systems that reduce congestion and emissions. Case studies show adaptive signal timing can cut travel times and lower particulate pollution. Regulatory frameworks in Japan, Singapore, and Hong Kong already encourage mounting on lampposts and traffic lights, accelerating the rollout . Parallel momentum in healthcare, retail, and utilities illustrates how the small cell networks market is broadening far beyond its telecom origins.

Geography Analysis

North America held 34.20% revenue in 2025, anchored by early C-band auctions and federal siting reforms. The United States alone counted more than 452,000 outdoor nodes by 2022 and is budgeted to invest USD 9 billion via the 5G Fund for Rural America to expand beyond metro cores. A landmark USD 14 billion modernization project is replacing legacy basebands with open-architecture radios, illustrating carrier commitment to vendor diversity.

Asia Pacific is projected to deliver a 36.95% CAGR, the steepest regional trajectory. China has deployed more than 500,000 5G base stations, and India’s Digital Communications Policy is easing right-of-way barriers nationwide. The regional mobile ecosystem added USD 880 billion to GDP in 2023, underscoring economic stakes. Flagship indoor small-cell implementations—such as KT’s Radio Dot roll-out for smart offices—demonstrate the business case for enterprise-grade indoor coverage.

Europe emphasizes sustainability, pursuing solutions that cut site energy by up to 45%. National roadmaps—Germany’s 5G Strategy being an example—prioritize tight-grid small cells to support automated driving and Industry 4.0. Operators in the region routinely embed compact radios on streetlamps; one London pilot added 80 cells across Westminster with minimal visual impact.

The Middle East and parts of Africa are scaling 5G for pilgrimage sites and smart-city corridors, as seen in Saudi Arabia’s multi-vendor program that combines macro and small-cell layers.

Regulatory Landscape

Small cell deployment is shaped by spectrum policy, siting rules, and access obligations that influence densification economics. In the United States, the Federal Communications Commission (FCC) opened a 2025 Notice of Proposed Rulemaking in WT Docket No. 25-276 to reduce state and local barriers for wireless facilities, aiming for faster approvals and more predictable fees and aesthetics requirements. Separately, the FCC adopted Report and Order FCC 25-38 to set new make-ready timelines for pole attachments, supporting street-level small cells that rely on utility and municipal structures.

In Europe, policy work focuses on harmonization and implementability. The European Commission published a 2025 status report on implementing EU rules for small-area wireless access points, and in 2026 proposed the Digital Networks Act to reduce fragmentation across national frameworks that affect permitting and access to infrastructure. In the United Kingdom, Ofcom initiated the Telecoms Access Review 2026-31 and updated its General Conditions of Entitlement in 2026, while also signaling a more granular approach to spectrum awards, including a January 2026 decision that mobile awards in the Upper 6 GHz band would be subnational, aligning licensing with high-density urban deployment needs.

Value Chain Analysis

The small cell networks value chain runs from silicon and RF components (baseband and RF SoCs, power amplifiers, filters, and timing) to radio unit and antenna manufacturing, software (RAN stacks, orchestration, and SON), systems integration, site acquisition and construction, and ongoing managed services. Equipment supply is led by integrated RAN vendors (Nokia, Ericsson, Huawei, ZTE, Samsung Networks) and Open RAN specialists such as Mavenir and Parallel Wireless, while deployment channels typically split between mobile operators, neutral-host providers, and enterprise/private network integrators.

Execution depends heavily on logistics and kitting discipline, since missing sub-components (cables, connectors, enclosures, or power units) can stop a site turn-up. The chain has also carried elevated risk from long RF component lead times and cross-border controls on advanced chipsets, which has pushed vendors and operators toward dual-sourcing and approved-vendor lists for high-risk parts. On the services side, ownership and operating models are changing as neutral-host and infrastructure investors recycle assets, including EQT and Zayo agreeing to acquire Crown Castle's fiber and small-cell business (about 115,000 nodes) announced in March 2025. At the vendor level, enterprise indoor propositions are being expanded, including InfiniG partnering with Nokia in April 2026 to integrate AirScale RAN into a neutral-host CBRS indoor service.

Competitive Landscape

Innovation and Adaptability Drive Market Success

Success in the small cell networks market increasingly depends on companies' ability to develop cost-effective, easily deployable solutions that address the growing demand for network densification and 5G capabilities. Incumbent players must focus on continuous innovation in areas such as network automation, integrated backhaul solutions, and multi-operator support to maintain their market positions. Companies need to establish strong partnerships with property owners, local authorities, and system integrators to overcome deployment challenges and accelerate market penetration. The ability to provide end-to-end solutions, including planning, deployment, and management services, has become crucial for maintaining competitive advantage.

New entrants and challenger companies can gain market share by focusing on specialized solutions for specific industry verticals or addressing particular technical challenges in small cell deployment. The market presents opportunities for companies that can effectively address issues such as cellular backhaul development, network management complexity, and integration with existing infrastructure. Regulatory frameworks regarding spectrum allocation, site acquisition, and deployment permissions significantly influence market dynamics and competitive strategies. Companies must also consider the increasing demand for private networks and enterprise solutions while developing their market approach.

Small Cell Networks Industry Leaders

Qualcomm Technologies Inc.

Huawei Technologies Co. Ltd.

Nokia Networks

Verizon

ZTE Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Indoor coverage remediation and capacity densification are the clearest whitespace areas, supported by traffic patterns where a large majority of sessions originate indoors and by property-led neutral-host models that limit duplicated infrastructure. Enterprise private networks also offer a parallel growth vector, particularly where shared spectrum regimes such as CBRS lower the barrier to deploying on-premise small cells integrated with local edge compute and automation tools. Virgin Media O2 provides a commercial proof point, reporting about 2,500 small cells in operation by June 2026 (up from 2,000 in 2025) while managing around 18% annual downlink traffic growth, and deploying targeted capacity additions such as Bath (March 2026).

Technology roadmaps are creating upgrade-led opportunities tied to 5G-Advanced and AI-driven RAN operations. 3GPP Release 19 (5G-Advanced) Stage 2 freeze was scheduled for June 2026, and operator modernization plans increasingly reference automation and Open RAN integration, where small cells can support modular upgrades and multi-vendor interoperability. Vodafone Germany disclosed a 2026 plan spanning 10,600 projects that includes densification and a large-scale O-RAN deployment, while regulator actions on infrastructure and spectrum access, including FCC permitting initiatives and Ofcom work on Upper 6 GHz awards, continue to reduce some of the friction points that previously slowed high-node-count rollouts.

Recent Industry Developments

- July 2026: Qualcomm began notifying the market of plans to stop selling its FSM100 and FSM200 small cell base station chip platforms to new customers. This shift changes the competitive landscape for small-cell silicon and can push OEMs and system vendors to requalify alternative chipsets and software stacks, with implications for product roadmaps and lead times.

- May 2026: Samsung and Qualcomm validated 5G Power Class 1 capability for fixed wireless access using Samsung's virtualized RAN and Qualcomm's FWA Gen 4 Platform. The result strengthens the performance case for vRAN-based deployments and highlights ongoing work on higher-power radio configurations that can complement dense small cell layers where capacity and coverage need to be balanced.

- March 2026: Nokia expanded its partnership with TIM Brasil to modernize its 5G network across 14 states, including deployment of AirScale Radio small cell solutions. The modernization links small cells with broader RAN upgrades and AI-ready network architecture, supporting higher-density rollouts through an incumbent vendor with end-to-end delivery capability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from purpose-built small cell network equipment used to add wireless coverage or capacity in indoor and outdoor locations, typically spanning femto, pico, micro, and metro class deployments for 4G and 5G networks.

Scope exclusions: Stand-alone Wi-Fi access points and unrelated radio access solutions that are not deployed as small cells are not counted.

Segmentation Overview

- By Cell Type

- Femtocell

- Picocell

- Microcell

- Metrocell

- Radio Dot Systems

- By Operating Environment

- Indoor

- Outdoor

- By End-user Vertical

- BFSI

- IT and Telecom

- Healthcare

- Retail

- Power and Energy

- Smart City and Government

- By Geography

- North America

- South America

- Europe

- Asia-Pacific

- Middle East and Africa

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the rollout context for small cells, since operator capex cycles and local permitting timelines directly shape deployment pace. We referenced public materials such as FCC spectrum and licensing updates, ITU releases on mobile network indicators, OECD telecom statistics, and national regulator publications on 5G rollouts and coverage obligations.

To keep the model grounded, we also reviewed company filings and investor presentations for direction on network spending, plus reputable press, standards updates, and technical literature in IEEE and similar peer-reviewed outlets to understand typical deployment patterns. In a few places, paid subscriptions were used only for company financials and news, and for patent databases to sense where product emphasis was moving. This desk source list is illustrative, and additional public and internal references were used for cross-checks, clarification, and validation as the work progressed.

Primary Interviews and Surveys

Primary interviews focused on what secondary data did not explain clearly, especially the pace of small cell densification, the indoor versus outdoor mix, and how pricing tends to step down as volumes scale. We spoke with a mix of network planners, deployment partners, solution teams, and enterprise connectivity stakeholders across major regions to challenge assumptions, revise gaps, and recheck the direction before final sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 19% | APAC: 48% |

| Mid tier: 46% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 21% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing begins from a top-down build where operator and enterprise rollout intensity is reconstructed using a demand pool view of planned coverage additions, densification needs in high-traffic zones, and the timing of 4G to 5G upgrades. The totals are then corroborated with selective bottom-up approximations, such as sampled shipment volumes by small cell class multiplied by typical selling prices, and channel checks on deployment programs, which are used to adjust the final totals when gaps appear.

Key inputs that were used as practical model drivers include 5G population coverage targets, spectrum availability and licensing milestones, site-level constraints like permitting and backhaul readiness, indoor enterprise adoption signals, and typical unit pricing progression by generation and form factor. Where a bottom-up signal was incomplete for a country, the missing portion was handled through penetration-based allocations tied to subscriber density and urbanization, and then revalidated through expert feedback.

For forecasting, scenario analysis was applied around rollout speed and pricing trajectories, supported by primary feedback on how quickly indoor programs and neutral-host builds are expected to scale. The outputs were checked against observable constraints so growth does not exceed practical deployment capacity or realistic pricing changes.

Data Validation & Update Cycle

Numbers are validated through cross-checks that compare model outputs with independent signals such as mobile capex direction, spectrum event timing, and reported network expansion milestones. Outliers are investigated, and assumptions are reworked when a country shows growth that conflicts with deployment constraints or recent policy changes.

Before publication, the full model is reviewed in multiple steps, and we re-contact sources when a large variance is found or when new public information materially changes a key input. Reports are refreshed annually, with interim updates when major spectrum actions, technology shifts, or macro events have a clear impact on rollout timing or pricing. Right before delivery, the latest data is scanned again so clients receive an updated view rather than an older snapshot.

Mordor Intelligence's Small Cell Network Market Size Measured Against Other Published Estimates

Published numbers for small cell networks often differ because the boundary of what is counted is not always the same, and because pricing and rollout assumptions can shift from one quarter to the next. Differences also show up when sources blend 4G and 5G definitions, handle indoor programs differently than outdoor densification, or convert currencies using different timing.

In our checks, the biggest gap drivers were refresh cadence and how average selling prices step down as deployments scale, followed by whether adjacent radio solutions get folded into the total. By running currency conversion on the same timing across regions, revalidating ASP movements with recent deployment feedback, and applying those updates in the latest model refresh, Mordor Intelligence arrives at a larger 2026 value than sources that rely on older price points or narrower rollout definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 37.14 B (2026) | |

| Industry Publisher A | USD 3.30 B (2025) | Uses a different time horizon and appears to anchor the market closer to early-stage deployment volumes, which can understate 5G densification phases and later-year price-volume scaling. |

| Global Research Group B | USD 0.51 B (2024) | Represents a much narrower starting base year and likely applies a tighter inclusion rule or limited deployment scope, which can exclude sizable operator programs and undercount multi-year rollouts. |

The spread in values is mainly explained by timing and scope, not by simple math errors. When the definition consistently covers purpose-built small cells across indoor and outdoor deployments, and when pricing and currency timing are kept current, the resulting market size remains traceable to rollout and ASP inputs and can be repeated as new data comes in.

Key Questions Answered in the Report

What is the current value of the small cell networks market?

The market is worth USD 37.14 billion in 2026 and is projected to reach USD 147.56 billion by 2031, reflecting a 31.74% CAGR.

Which segment is growing fastest within the small cell networks market?

Microcells are expanding at a 33.75% CAGR because they balance coverage and capacity for dense urban deployments.

Why are small cells essential for 5G rollouts?

Higher-frequency 5G bands attenuate quickly, so operators must deploy many low-power sites to maintain continuous coverage, especially indoors where over 80% of traffic originates.

How does a neutral-host model lower costs?

A single shared small-cell grid can serve multiple carriers, reducing total ownership expenses by up to 80% compared with separate in-building systems.

What are the main barriers to faster deployment?

Municipal permitting delays, fibre backhaul availability and semiconductor supply constraints are the chief factors holding back scale-out, collectively trimming forecast CAGR by about 10 percentage points.

Which region will account for the largest future growth?

Asia Pacific is forecast to post the highest regional CAGR at 36.95% through 2031, driven by large-scale densification in China, India and Southeast Asian economies.

Page last updated on: