Canola Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 41.04 Billion |

| Market Size (2031) | USD 49.55 Billion |

| Growth Rate (2026 - 2031) | 3.84% CAGR |

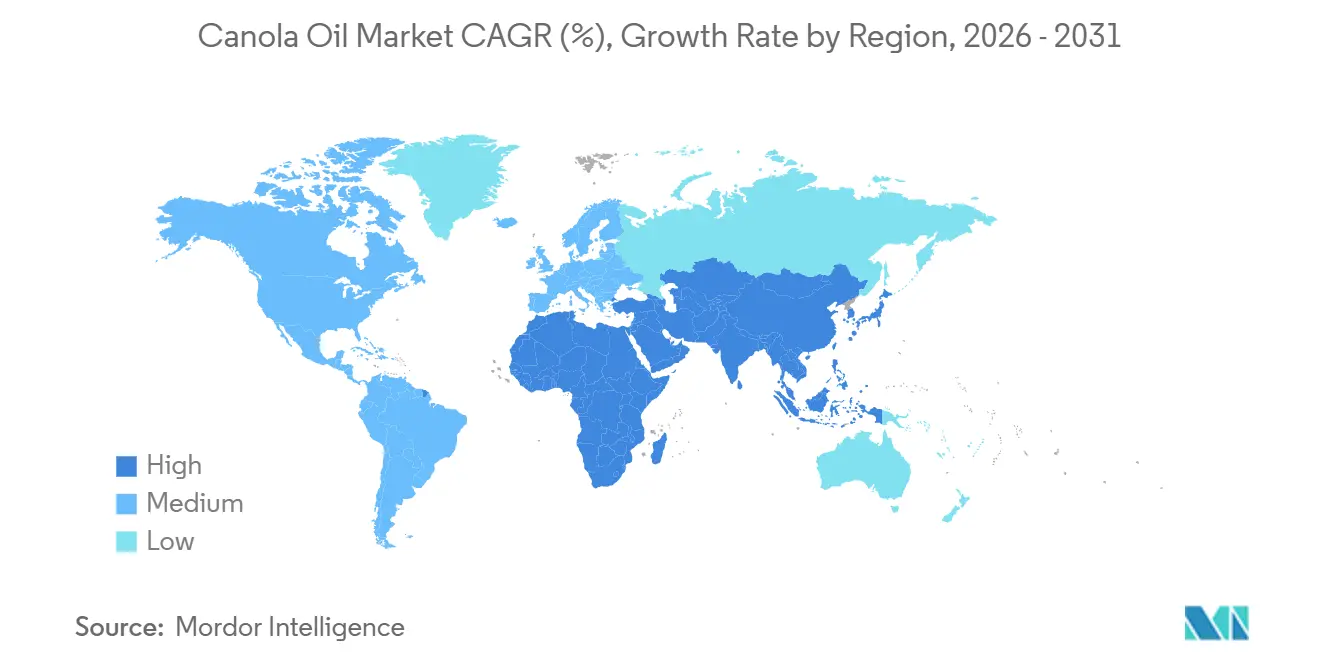

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

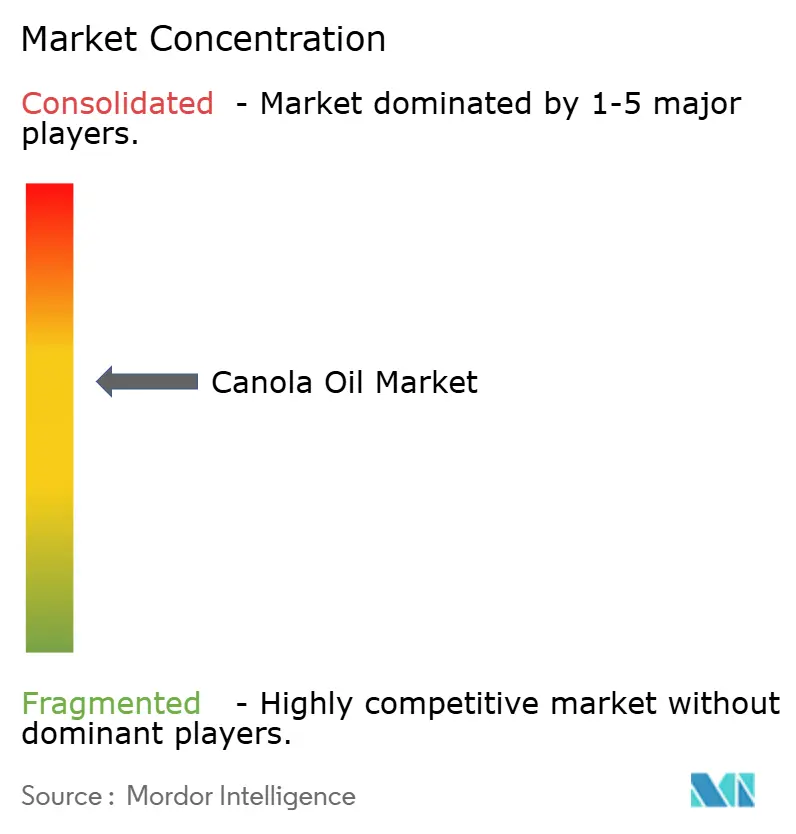

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canola Oil Market Analysis by Mordor Intelligence

The canola oil market size is projected to expand from USD 39.52 billion in 2025 and USD 41.04 billion in 2026 to USD 49.55 billion by 2031, registering a CAGR of 3.84% between 2026 to 2031. Neutral-flavored cooking oils are in high demand, fueling growth in packaged snacks, quick-service restaurant frying, and plant-based foods. Meanwhile, technology-driven extraction methods are boosting supply. The market is especially booming in renewable diesel production. Following EPA approval, U.S. imports of canola oil surged, elevating the U.S. share of Canadian canola oil exports from 50-60% to a striking 91% in 2024[1]Source: U.S Department of Agriculture, U.S. Renewable Diesel Production Growth Drastically Impacts Global Feedstock Trade", fas.usda.gov. In the Asia-Pacific region, Chinese and Indian processors are opting for RBD canola oil over soybean and palm oils for better oxidative stability. At the same time, manufacturers in North America and Europe are promoting premium high-oleic and organic variants to protect their profit margins. Despite facing setbacks from anti-seed-oil campaigns, farmers find hope in the FDA's revised "healthy" definition, which now endorses canola oil, potentially countering the spread of misinformation[2]Source: Canola Council of Canada, "Canola oil defined as healthy", canolacouncil.org. In the Middle East and Africa, rapid urbanization and retail modernization present a dual landscape: while affordability drives most purchasing decisions, a niche segment with higher disposable incomes seeks out premium offerings like omega-3 DHA blends. The competitive landscape remains moderately intense. In Canada and Australia, capacity expansions are helping to stabilize prices that often fluctuate due to weather. Simultaneously, global crushers are adopting vertical integration strategies to ensure seed availability, especially as sustainability standards tighten.

Key Report Takeaways

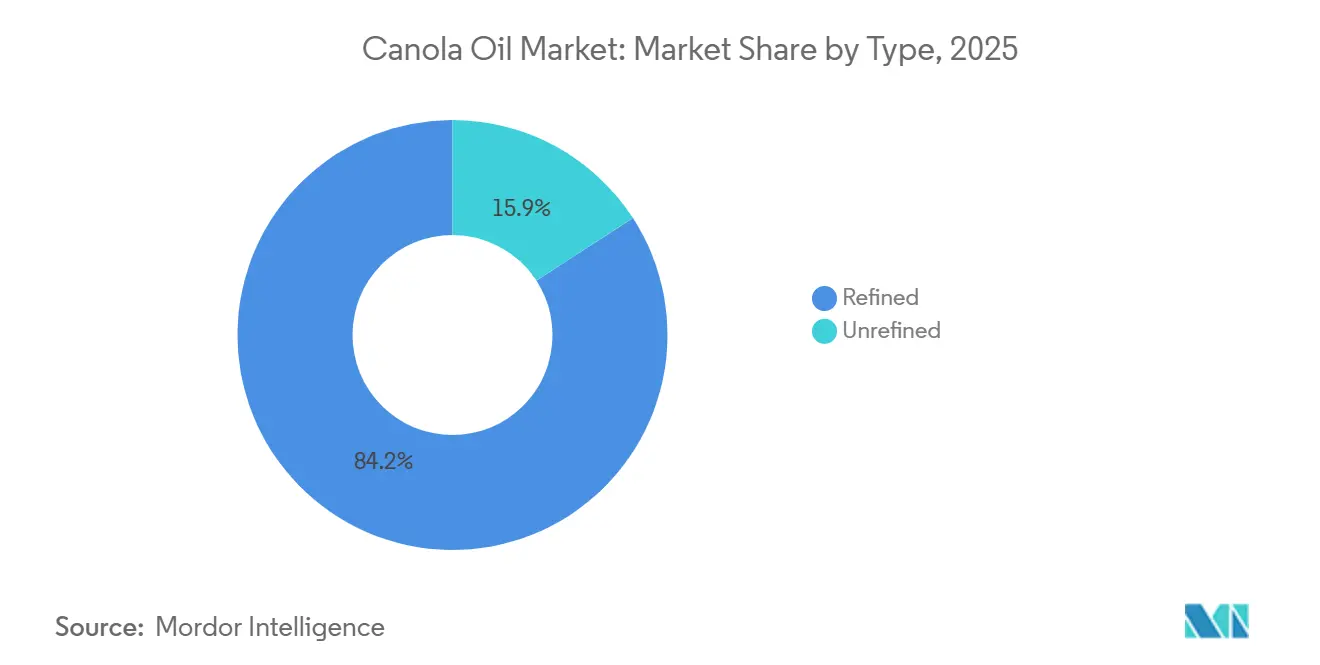

- By product type, RBD canola oil held 84.15% of the RBD canola oil market share in 2025, while high-oleic refined variants are forecasted to advance at a 5.21% CAGR through 2031.

- By nature, conventional grade dominated with 91.23% share in 2025; organic grade is forecasted to advance at a at a 5.90% CAGR from 2026-2031.

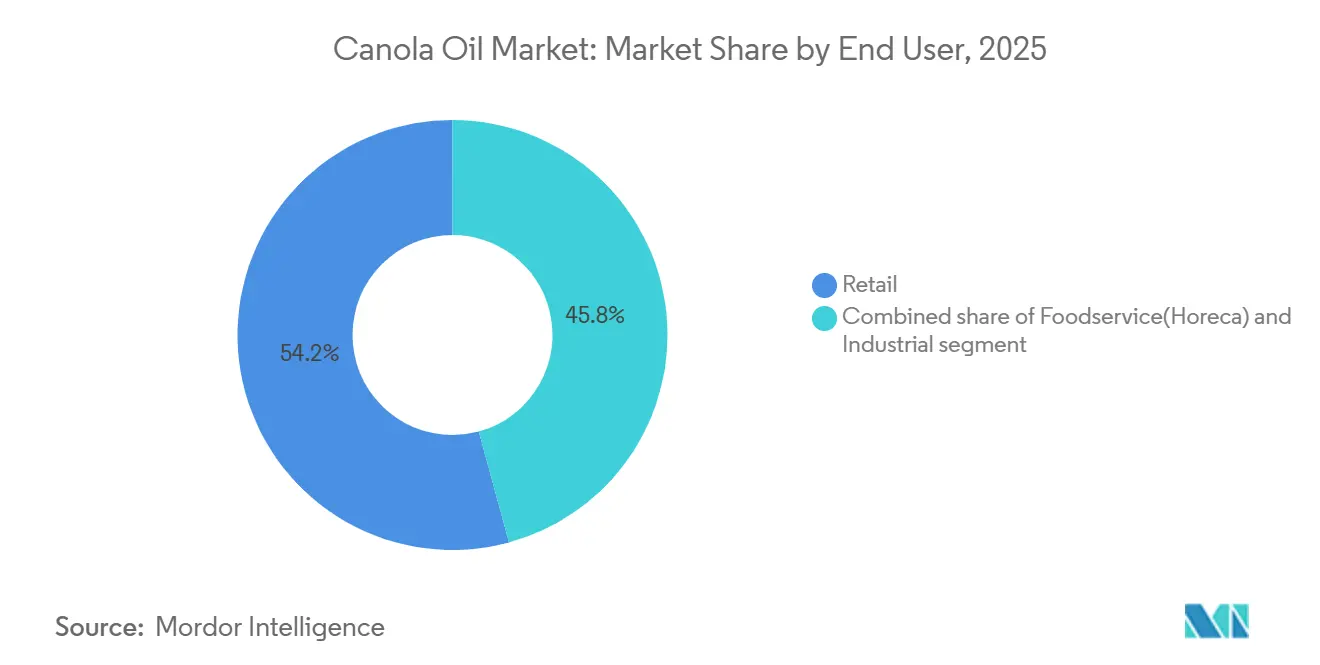

- By end user, retail channels captured 54.24% of 2025 revenue, whereas foodservice and HoReCa channels are forecasted to advance at a 5.14% CAGR to 2031.

- By geography, Asia-Pacific led with a 37.17% share in 2025, and the Middle East and Africa region is forecasted to advance at a 5.52% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Canola Oil Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing preference for low-fat and healthier edible oils | +0.8% | Global, strongest in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing demand for neutral-flavored oils in packaged and processed foods | +0.6% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Rising demand for plant-based and clean-label products | +0.7% | North America, Europe, affluent Asia-Pacific cities | Medium term (2-4 years) |

| Growing adoption in foodservice establishments supporting demand | +0.5% | Global, especially QSR expansion corridors | Short term (≤ 2 years) |

| Advancements in oil extraction and refining technologies | +0.4% | North America and Europe, with tech transfer to Asia-Pacific | Long term (≥ 4 years) |

| Product innovation, including fortified and blended variants | +0.5% | North America and Europe first, then Asia-Pacific premium tiers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing preference for low-fat and healthier edible oils

RBD canola oil is gaining traction as consumers prioritize cardiovascular health. With saturated fat levels at 7%, RBD canola oil stands in stark contrast to palm oil's 49% and coconut oil's hefty 87%. The U.S. Food and Drug Administration has greenlit on-pack statements linking canola oil use to reduced coronary heart disease risk. This endorsement is spurring reformulations in snacks, baked goods, and dressings, set to roll out between 2025 and 2026. A 2024 peer-reviewed clinical study found that substituting 5% of dietary energy from saturated fats with canola oil led to an 8-10% drop in LDL cholesterol. With 9-11% alpha-linolenic acid content, a tablespoon of canola oil meets 75% of the daily plant-based omega-3 requirement. This positions retailers to market canola oil as a heart-healthy alternative, rivaling the premium price tag of olive oil. Capitalizing on these nutritional benefits, private-label lines in North America and Europe are making significant inroads, challenging established brands in the mature, premium segment of the RBD canola oil market.

Growing demand for neutral-flavored oils in packaged and processed foods

Industrial processors prioritize flavor neutrality to maintain regional taste consistency. The refining cycle of RBD canola oil effectively reduces free fatty acids to below 0.05%, while also eliminating pigments and volatiles that might influence the product's flavor. From 2020 to 2025, China's processed-food sector saw an annual growth of 8.3%. Notably, the sector began replacing soybean oil with rapeseed oil in biscuits, noodles, and crackers, successfully doubling the shelf-life from 6 to 12 months at room temperature. Snack giants, with operations in over 50 countries, have embraced this oil to guarantee a consistent mouthfeel and crispness throughout their global supply chains. Data underscores this trend: by 2025, China's rapeseed oil consumption in food processing hit 3.2 million metric tons, marking an 18% increase over two years. Further solidifying this trend, McDonald's made a global shift to a canola-based frying blend in 2024, underscoring the push for standardization in the RBD canola oil market.

Rising demand for plant-based and clean-label products

In a 2024 survey by the International Food Information Council, 75% of participants reported closely examining ingredient lists. This trend has made single-ingredient, plant-sourced fats increasingly appealing. RBD canola oil, aligning with "clean-label" standards that ban synthetic additives and hydrogenated fats, boasts an environmental profile that sidesteps the deforestation controversies associated with tropical oils. By 2025, plant-based meat sales surged to USD 7.5 billion, with industry frontrunners Beyond Meat and Impossible Foods turning to canola oil to replicate the juiciness of animal fat. Europe's vegan demographic swelled to 78 million in 2025, amplifying the demand. Yet, constraints on organic acreage have limited the certified supply, resulting in sustained high premiums for organic RBD canola oil.

Growing adoption in foodservice establishments supporting demand

In 2025, quick-service restaurants (QSRs) and hotel-restaurant-café chains increasingly opted for high-oleic RBD canola oil due to its ability to extend fry-life to 7-10 days, which is double the duration offered by conventional oils. This strategic choice significantly reduced input costs and enhanced operational efficiency, contributing to improved profit margins. Foodservice revenues in North America exceeded 2019 levels by 12%, driven by increased consumer demand and operational optimizations. Urban cloud kitchens across the Asia-Pacific region relied heavily on the extended oil life to protect their slim 5-8% margins, ensuring sustainability in a competitive environment. The high-oleic oil's superior oxidative stability, demonstrated by peroxide values remaining below 2 meq/kg after 72 hours at 180 °C, played a critical role in reducing waste disposal requirements and cutting procurement budgets by up to 50%. Furthermore, in 2025, packagers increasingly favored 35-pound jugs and 400-pound totes, which together accounted for 42% of North America's foodservice volume. This shift in packaging preferences further reinforced RBD canola oil's penetration in the market, highlighting its growing importance in the foodservice industry.

Restraints Impact Analysis of Canola Oil Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of canola seeds due to weather and logistics | –0.4% | Canada, Australia, import-dependent Asia | Short term (≤ 2 years) |

| Strong competition from palm, soybean, and sunflower oils | –0.5% | Asia-Pacific, Africa, Latin America, North America | Medium term (2-4 years) |

| Stringent labeling and regulatory requirements | –0.2% | Europe, North America, emerging compliance adopters | Long term (≥ 4 years) |

| Risk of adulteration and quality inconsistency | –0.2% | South Asia, Southeast Asia, Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price volatility of canola seeds due to weather fluctuations and supply chain disruptions

In 2025, Canada exported 18.80 million metric tons of canola. However, with 80% of its canola acreage located in Alberta and Saskatchewan, the crops are highly susceptible to frost and drought, which can reduce yields by 15-25%. These regions are critical to Canada's canola production, and adverse weather conditions can significantly impact overall output. For instance, a heat dome in Western Canada in 2021 slashed the harvest to 12.6 million metric tons, causing ICE canola futures to surge by 45%, reaching CAD 900 per ton. Similarly, Australia's 2025 exports of 5.22 million metric tons face challenges from weather fluctuations, which can disrupt production and export volumes. Additionally, the ongoing conflict in Ukraine has disrupted sunflower oil supply routes, further emphasizing the fragility of global oilseed supply chains. In March 2026, China eliminated a 3% tariff on Canadian imports, a move projected to boost imports by an additional 500,000 metric tons annually. This increase is expected to intensify demand during planting seasons, which are particularly sensitive to weather changes, potentially exacerbating supply tightness in the market.

Strong competition from alternative edible oils such as palm, soybean, and sunflower oil

Palm oil, priced at USD 600-700 per metric ton, stands in stark contrast to canola's USD 1,100-1,200. This significant price advantage solidifies palm oil's dominance in the price-sensitive markets of ASEAN and Africa, where, in 2025, it constituted 38% of global edible-oil consumption. These regions rely heavily on affordable edible oils due to economic constraints, making palm oil the preferred choice. In the U.S., soybean oil's integrated crush revenue streams, which include by-products like soybean meal, facilitate aggressive discounting strategies. This contributed to a production volume of 11.8 million metric tons in 2025, significantly surpassing canola oil's 1.4 million metric tons. Meanwhile, sunflower oil, primarily sourced from Ukraine and Russia, boasts a smoke point of 230 °C, similar to canola oil, making it a highly suitable substitute for European industrial frying applications, especially in the food processing sector. Furthermore, studies on price elasticity reveal that a 10% uptick in RBD canola oil prices, when compared to palm oil, triggers a 6-8% shift towards substitution. This trend exerts pressure on canola oil producers, further squeezing profit margins in competitive markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Canola Oil Market Segment Analysis

By Product Type:

RBD Dominance Anchors Industrial DemandIn 2025, canola oil captured a commanding 84.15% market share, largely due to its effectiveness in industrial applications like baking, snack frying, and margarine production. Processors favor canola oil for its consistent quality, notably its stable color and peroxide values maintained below 1 meq/kg. Through a meticulous multi-stage refining process encompassing degumming, neutralization, bleaching, and steam deodorization, producers achieve low free fatty acids and oxidation levels. This refinement not only meets the extended shelf life demands of up to 12 months but also serves the reliability needs of global snack manufacturers. While premium alternatives exist, RBD oil remains the market anchor, celebrated for its scalability and cost efficiency.

High-oleic refined canola oil is on a growth trajectory, with projections indicating a CAGR of 5.21% through 2031. This surge is largely attributed to quick-service restaurants' demand for oils that offer a longer fry-life, thereby minimizing waste and cutting operational costs. Its superior oxidative stability means it can be used for extended periods, making it a favorite in high-volume frying settings. Although niche formats like cold-pressed and expeller-pressed oils boast a 10.64% market share and enjoy a 60–80% price premium, their limited scalability hinders wider adoption. On the innovation front, advancements like enzyme-assisted degumming are paving the way for organic-certified RBD production, bolstering competitive positioning across various segments.

By Nature:

Organic Growth Constrained by SupplyIn 2025, conventional grade accounted for 91.23% of revenues, driven by agronomic optimization, herbicide-tolerant seeds, and no-till practices that reduce costs and carbon intensity. These practices have been widely adopted due to their ability to enhance efficiency and sustainability in farming operations. The conventional supply of the RBD canola oil market is expected to grow steadily, aligning with overall demand trends. However, the premium segment continues to attract significant branding efforts, as companies aim to differentiate their products and capture higher-value market opportunities. This focus on premium branding highlights the evolving dynamics within the market, where innovation and consumer preferences play a critical role.

By 2025, organic acreage in Canada hit 185,000 acres, representing just 3.5% of total plantings. This limited share, despite a projected 5.90% CAGR, caps short-term expansion. Achieving USDA Organic or EU Organic certification necessitates a three-year land-transition period and associated inspection costs, which can be a barrier for many producers. However, producers often offset these costs, enjoying 30-40% premiums on shelf prices, making organic farming a lucrative option for those who can navigate the challenges. Yet, identity-preserved logistics pose challenges; without dedicated crush lines, traceability lapses could jeopardize certification, leading to potential revenue losses. In response, some mainstream crushers are investing in specialized cleaning and storage solutions, aiming to boost organic throughput. These investments present a cautious opportunity for the RBD canola oil sector, as they could help address supply chain bottlenecks and support the growth of the organic segment.

By End User:

Foodservice Gains Share Through QSR ExpansionIn 2025, retail claimed the top spot, generating 54.24% of global revenue, bolstered by the dominance of private-label oils priced 20–30% lower than their national counterparts. Supermarkets and hypermarkets are pivotal in maintaining this retail supremacy, ensuring products are easily accessible and consistently in demand. Consumers favor RBD canola oil in retail for its cost-effectiveness, neutral flavor, and perceived health advantages. This segment enjoys steady household consumption in both developed and emerging markets. Even amidst pricing challenges, retail holds its ground, buoyed by scale, brand substitution trends, and well-established supply chains.

Foodservice is the segment to watch, with projections indicating a robust CAGR of 5.14% through 2031. The resurgence of quick-service restaurants and the swift rise of cloud kitchens in urban hubs like India, Indonesia, and the Gulf are fueling this growth. By 2031, the segment is set to contribute an additional USD 2 billion in market value, driven by a demand for oils that promise extended fry life and economic savings. High-oleic oil variants boost operational efficiency, cutting down on oil replacement frequency and labor expenses. This blend of economic and functional advantages is propelling the foodservice sector's swift adoption of these oils.

Geography Analysis

APAC Canola Oil Market

In 2025, Asia-Pacific dominated the RBD canola oil market, claiming a 37.17% share, driven by China's rapeseed-oil consumption hitting 6.8 million metric tons and India becoming 70% dependent on edible-oil imports. With China set to lift tariffs on Canadian shipments in March 2026, an extra 500,000 metric tons annually is anticipated, tightening the global supply. India's Food Safety and Standards Authority greenlit mustard-canola blends, hastening the rollout of branded packaged oils in modern retail and e-commerce. Japan's J-Oil Mills, with a refining capacity of 450,000 metric tons, caters to the tempura and mayonnaise segments that demand a neutral flavor. Meanwhile, Australia's 5.22 million metric tons of canola oil exports primarily target Asian buyers in search of non-GMO supplies[3]Source: World Bank, "Socialist Economic Development", worldbank.org .

MEA Canola Oil Market

The Middle East and Africa are poised to witness the fastest growth at a 5.52% CAGR through 2031. This growth is bolstered by a 4% annual urbanization rate in Saudi Arabia, UAE, and Egypt. Hypermarket chains like Carrefour and Lulu are overtaking traditional trade, expanding shelf space for global brands. In 2025, UAE's imports surged to 1.2 million metric tons, with canola making up 18% of that volume. Concurrently, Saudi Arabia's Vision 2030 is channeling USD 4 billion (2023-2025) into food-processing investments, amplifying industrial demand. While Nigeria and Morocco exhibit early potential, challenges like logistics bottlenecks and currency volatility hinder immediate market penetration.

The Americas and Europe Canola Oil Market

In 2025, North America accounted for 28.50% of global revenue. Canada celebrated a record harvest of 21.8 million metric tons, leading to an 11.6 million metric-ton crush. Notably, 76.7% of Canada's canola oil exports found their way to the U.S. As U.S. policies tighten on trans-fat elimination, foodservice customers are increasingly pivoting from soybean oil to high-oleic RBD canola oil. In 2025, Mexico imported 380,000 metric tons, buoyed by the growth of quick-service restaurants (QSR) and a rising appetite for packaged snacks. Europe's rapeseed oil production of 9.2 million metric tons satisfied 85% of its self-demand, reducing its import reliance. In contrast, South America, constrained by soybean dominance and limited crushing infrastructure, lagged at a modest 180,000 metric tons.

Competitive Landscape

The canola oil market is witnessing a moderate consolidation. In June 2024, Bunge and Viterra's merger, valued at USD 8.2 billion, birthed the third-largest oilseed processor, boasting a canola capacity exceeding 5 million metric tons. Cargill, in February 2026, unveiled plans to boost Camrose's output by 30%, highlighting the industry's race for scale. Meanwhile, ADM invested USD 75 million in retrofitting Lloydminster, achieving a 99.8% hexane recovery, a move aimed at addressing sustainability concerns. Richardson International, not to be outdone, doubled Yorkton’s capacity to 2.5 million metric tons, introduced enzyme-based refining, and proudly claimed the title of the largest single-site crush, signaling a shift towards technology-driven efficiency.

Seed trait control stands as a pivotal stronghold: Corteva Agriscience’s Pioneer P523HO variety, boasting 78% oleic acid and a 10-day fry-life, secures royalty streams and deters competition with patent coverage extending to 2037. On the downstream front, Nuseed’s Nutriterra omega-3 DHA oil, after clinching FDA and Health Canada approvals, carves a niche in premium infant-nutrition markets. Meanwhile, smaller entities like India’s Jivo Wellness and Spain’s Borges International tap into the cold-pressed and organic segments, enjoying retail premiums of 60-80%, albeit on a limited volume. To counter seed volatility and ensure a consistent supply of high-oleic or organic crops especially vital in the face of climate-induced supply challenges vertical integration contracts with Canadian and Australian growers have become a strategic move.

Producers of RBD canola oil are feeling the pinch from palm oil’s structural cost disparities. In response, they're ramping up automation and expediting solvent-recovery paybacks, striving to stay competitive without eroding their margins. While capacity expansions in Saskatchewan, Alberta, and Western Australia are set to surpass 3 million metric tons by 2027, unpredictable weather patterns pose a threat to these projected gains. Given this volatility, the industry is leaning heavily on technology investments and product differentiation as key strategies for sustained growth in the RBD canola oil market.

Canola Oil Industry Leaders

-

Archer Daniels Midland Company

-

Cargill, Incorporated.

-

Bunge.

-

Wilmar International Ltd

-

Richardson International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Canola Oil Market Companies Covered in this Report

- Archer Daniels Midland (ADM)

- Cargill Inc.

- Bunge Ltd.

- Wilmar International

- Richardson International

- Louis Dreyfus Company

- Viterra (Bunge-Glencore)

- Corteva Agriscience

- COFCO Corp.

- J-Oil Mills Inc.

- Goodman Fielder Pty. Ltd.

- Conagra Brands Inc. (Wesson)

- Associated British Foods plc

- Jivo Wellness Pvt Ltd.

- Borges International Group

- Innovative Retail Concepts Pvt Ltd. (BB Royal)

- Modi Naturals Ltd. (Miller)

- B&G Foods (Crisco)

- Velona

- LouAna Oils

Recent Industry Developments in Canola Oil Market

- May 2026: Cargill Inc. bolstered its foothold in the market by inaugurating its Regina Canola Facility in Canada. This facility, boasting an annual processing capacity of 1 million metric tonnes of canola, not only amplifies local demand but also facilitates the domestic processing of the crop into premium products. These include oil for culinary use, renewable fuels, and high-protein meal intended for animal feed.

- April 2025: Good Earth Oils (GEO) has successfully integrated its canola oil into JD.com's supply chain, thanks to the efforts of Australian Oilseeds Holdings Limited, a company based in the Cayman Islands. With the company's dedicated coordination, GEO's canola oil now proudly meets the standards set by JD.com's self-operated platform.

- January 2025: Bayer has teamed up with Neste, a Helsinki-listed firm specializing in transforming waste into renewable fuels and circular raw materials. Together, they've inked a memorandum of understanding (MOU) to cultivate a winter canola ecosystem in the Southern Great Plains of the U.S.

- September 2024: In October 2024, Scoular launched its new facility, designed to crush canola and soybean oilseeds. This move positions producers to tap into expanding markets for renewable fuels and protein meals intended for animal feed. The facility's dual-processing capability for canola and soybeans enhances its versatility and ensures its long-term sustainability.

Global Canola Oil Market Report Scope

Canola oil is defined as a light, edible vegetable oil extracted from the seeds of the canola plant, which is a specially bred variety of rapeseed. The market is segmented by product type, by nature, by end user and by geography. By product type, the market is segmented into RBD(Refined, Bleached, and Deodorized), High-Oleic Refined and others. By nature, the market is segmented into organic and conventional. by end user, the market is segmented into industrial, foodservice, and retail. The study provides detailed analysis for major economies across North America, South America, Asia-Pacific, Europe and Middle East and Africa.

Segmentation Overview

| RBD (Refined, Bleached and Deodorized) |

| High-Oleic Refined |

| Others |

| Organic |

| Conventional |

| Industrial |

| Foodservice (HoReCa) |

| Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | RBD (Refined, Bleached and Deodorized) | |

| High-Oleic Refined | ||

| Others | ||

| By Nature | Organic | |

| Conventional | ||

| By End User | Industrial | |

| Foodservice (HoReCa) | ||

| Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the RBD canola oil market in 2026 and how fast is it growing?

It is valued at USD 41.04 billion in 2026 and is expected to reach USD 49.55 billion by 2031 at a 3.84% CAGR.

Which region holds the biggest share of global demand?

Asia-Pacific accounts for 37.17% of 2025 demand, led by China and India.

What segment expands the fastest between 2026-2031?

High-oleic refined canola oil grows the quickest, at 5.21% CAGR, driven by foodservice fry-life advantages.

How does organic supply affect overall availability?

Organic acreage represents only 3.5% of plantings, so despite a 5.90% CAGR, limited supply keeps premiums high.

Page last updated on: