Soft Tissue Allografts Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.21 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soft Tissue Allografts Market Analysis by Mordor Intelligence

The soft tissue allografts market size is expected to grow from USD 3.95 billion in 2025 to USD 4.21 billion in 2026 and is forecast to reach USD 5.82 billion by 2031 at 6.66% CAGR over 2026-2031. Demand grows steadily as allografts move from experimental use to routine surgical materials in orthopedics, dentistry, wound care, and vascular repair. Adoption is reinforced by improved processing technologies that extend shelf life, lower immunogenicity, and offer better biomechanical performance. At the same time, an aging population and climbing sports‐injury volumes expand the surgical candidate pool, while new reimbursement pathways reduce financial barriers. Heightened regulatory scrutiny—particularly six USFDA guidance documents released inJanuary2025—raises compliance costs yet standardizes quality, favoring processors with robust quality systems. In addition, mergers such as ZimmerBiomet’s USD1.1billion deal for Paragon28 illustrate a race to secure graft supply and distribution channels across diverse specialties.

Key Report Takeaways

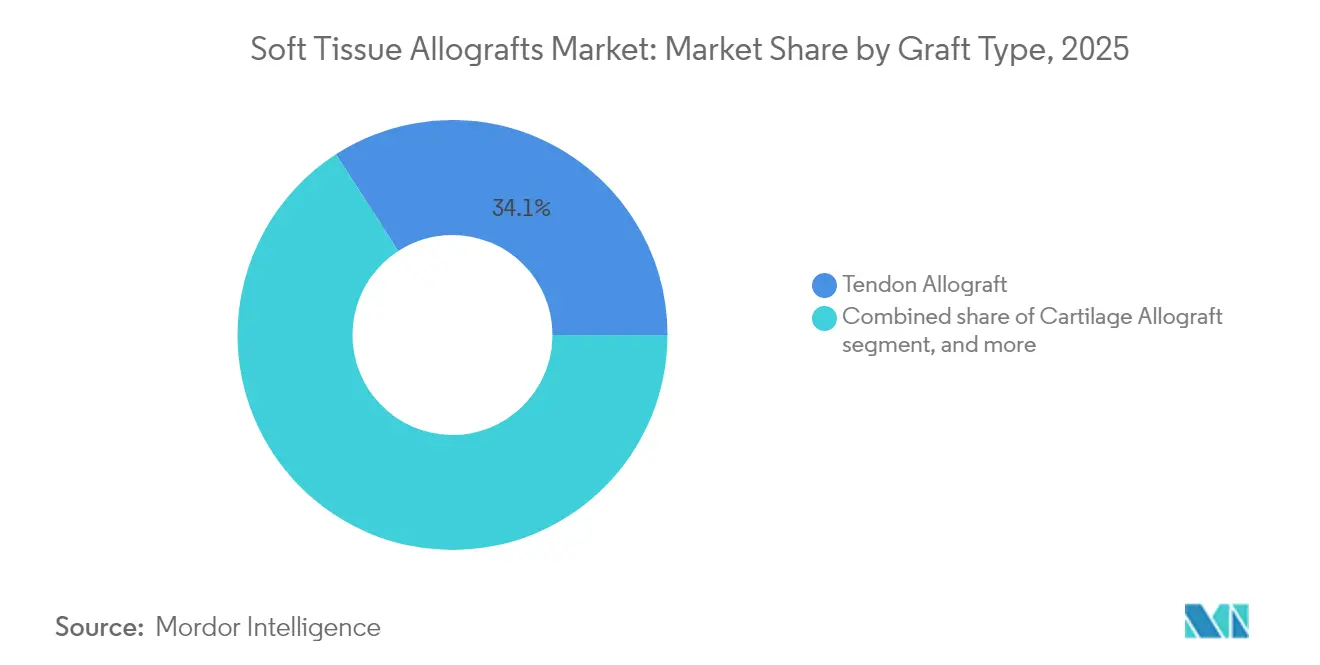

- By graft type, tendon allografts led with34.12% revenue share in2025; dental/periodontal grafts are projected to grow at an8.34% CAGR through2031.

- By processing method, fresh-frozen allografts held41.90% of the soft tissue allografts market share in2025, while decellularized and acellular grafts are poised for the fastest8.12% CAGR to2031.

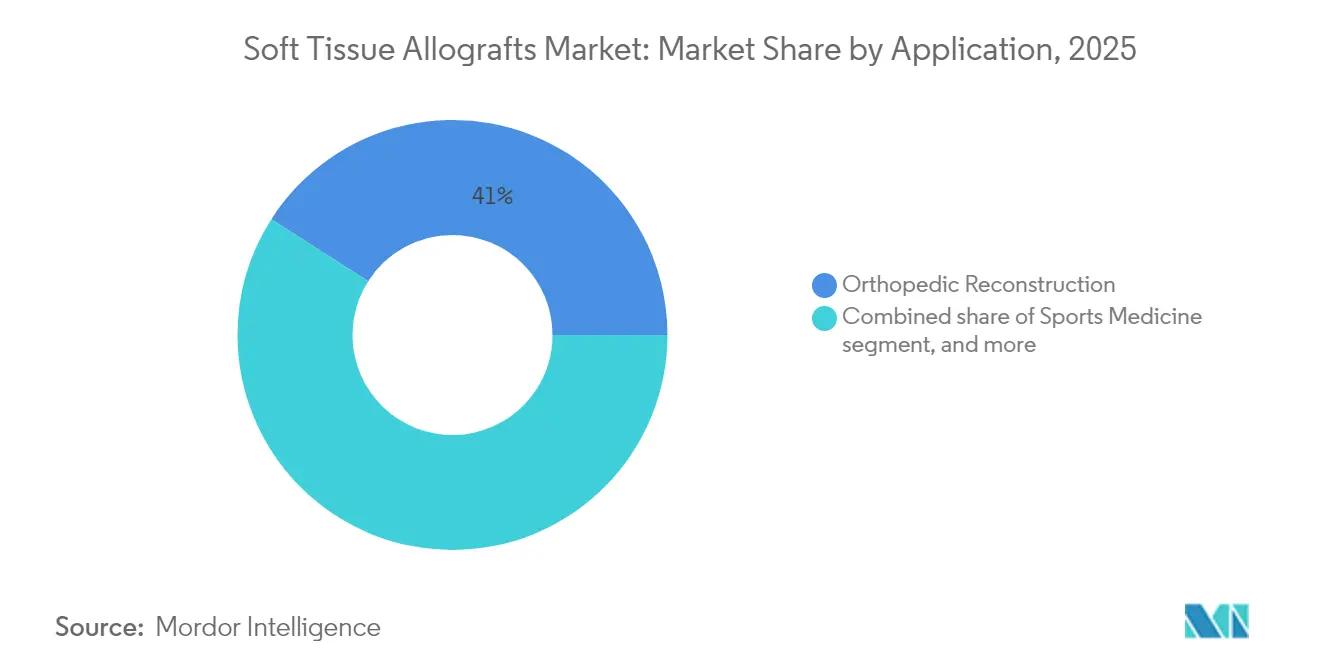

- By application, orthopedic reconstruction accounted for40.95% of the soft tissue allografts market size in2025, but wound and burn management is expanding at a8.95% CAGR to2031.

- By end user, hospitals captured56.70% of the soft tissue allografts market size in2025; ambulatory surgical centers (ASCs) register the highest9.18% CAGR to2031.

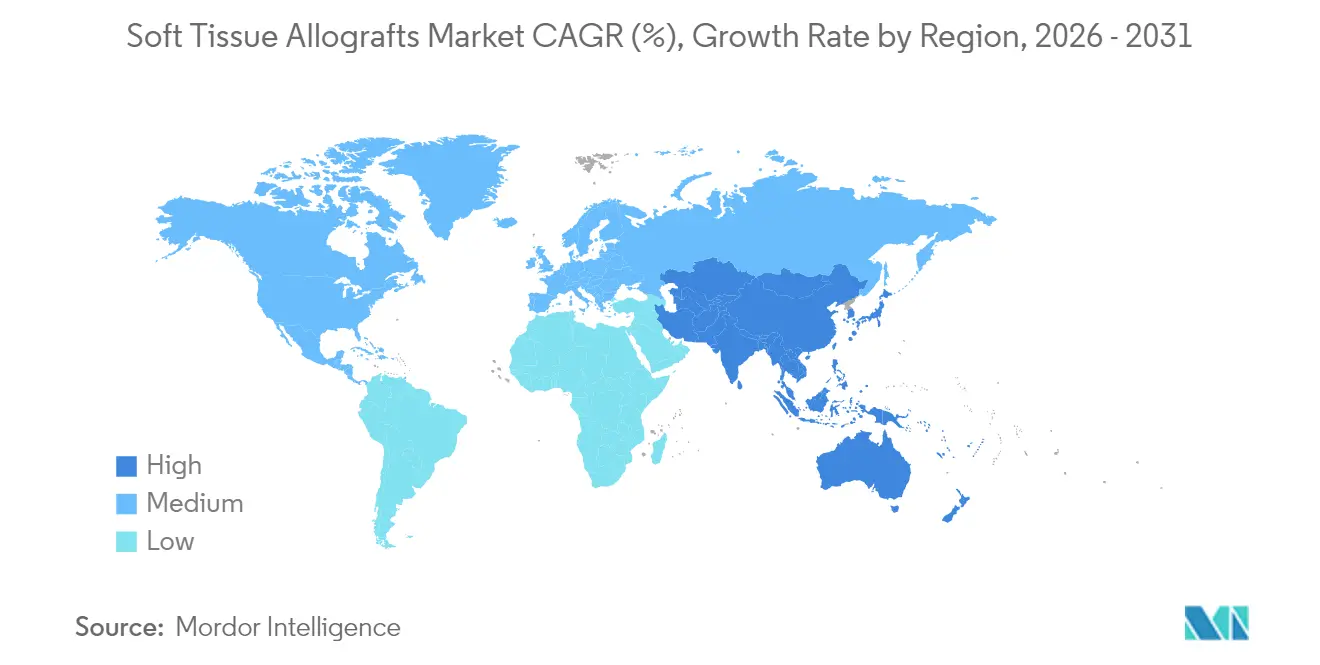

- By region, North America dominated with a45.10% revenue share in2025, whereas Asia-Pacific is the fastest-growing geography at7.32% CAGR through2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soft Tissue Allografts Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of musculoskeletal disorders | +1.8% | Global; strongest in North America & Europe | Long term (≥ 4 years) |

| Expanding geriatric population base | +1.5% | Global; highest in Asia-Pacific & North America | Long term (≥ 4 years) |

| Increasing sports and recreation injuries | +1.2% | North America & Europe; emerging Asia-Pacific | Medium term (2-4 years) |

| Rapid advances in tissue engineering technologies | +2.1% | Global; led by North America with spillover to Europe | Medium term (2-4 years) |

| Growing healthcare expenditure in emerging economies | +1.0% | Asia-Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Favorable reimbursement and policy support | +0.8% | North America & Europe; gradually expanding in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Musculoskeletal Disorders

Musculoskeletal conditions have shifted the soft tissue allografts market toward predictable, elective procedures instead of sporadic trauma-driven interventions. Chronic knee, shoulder, and spinal pathologies require planned reconstruction, enabling tissue banks to forecast demand, match donor characteristics to recipient needs, and reduce wastage. Aging demographics magnify this trend because degenerative tissue loss in seniors often rules out autografts. Surgeons therefore turn to pre-processed allografts that shorten operating times and avoid donor-site morbidity, producing clinical outcomes that compare favorably with autografts in elderly cohorts[1]National Institutes of Health, “Musculoskeletal Diseases,” nih.gov. The result is a durable demand curve that allows processors to optimize inventory and drives revenue visibility across the soft tissue allografts market.

Expanding Geriatric Population Base

Older patients exhibit limited healing capacity and insufficient autograft sites. Allografts thus become first-line options in complex foot, ankle, and spine surgeries. The FDA’s December2024 approval of Symvess, an acellular tissue-engineered vessel, illustrates a regulatory embrace of advanced allografts for vascular reconstruction in fragile patient groups[2]U.S. Food and Drug Administration, “FDA Clears Symvess Acellular Vessel,” fda.gov. Hospitals now prioritize shorter anesthesia times and fewer complications, favoring off-the-shelf grafts despite higher prices. Consequently, the geriatric demographic strengthens long-term growth for the soft tissue allografts market.

Increasing Sports and Recreation Injuries

Escalating participation in organized sports brings higher rates of ligament and tendon ruptures that demand biomechanically robust grafts. Professional teams and collegiate programs endorse soft tissue allografts for anterior cruciate ligament (ACL) repair because they eliminate donor-site morbidity and enable quicker return-to-play. Supercritical CO₂-sterilized grafts demonstrate outcomes paralleling autografts while trimming rehabilitation intervals[3]National Center for Biotechnology Information, “Supercritical CO₂-Sterilized Allografts in ACL Repair,” ncbi.nlm.nih.gov. Parallel growth in youth athletics cultivates a pipeline of future revision surgeries, reinforcing the expansion trajectory of the soft tissue allografts market.

Rapid Advances in Tissue Engineering Technologies

Decellularization retains extracellular matrices while stripping immunogenic cells, turning grafts into bioactive scaffolds that spur vascular ingrowth and remodeling. New cryopreservation and lyophilization protocols safeguard biomechanical integrity for years, granting tissue banks latitude to balance supply with demand spikes. Processors pioneering fast decellularization for split-thickness skin now cut lead times from weeks to days without compromising sterility. Such technical leaps differentiate premium suppliers and accelerate consolidation across the soft tissue allografts market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment and graft costs | –0.9% | Global; greatest drag in emerging markets | Short term (≤ 2 years) |

| Stringent and fragmented regulatory landscape | –0.6% | Global; variable intensity across regions | Medium term (2-4 years) |

| Limited availability of donor tissue | –0.7% | Global; acute in Asia-Pacific & Latin America | Long term (≥ 4 years) |

| Potential risk of disease transmission | –0.5% | Global; heightened scrutiny in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment and Graft Costs

Insurance payers compare allograft charges with autograft alternatives, triggering pre-authorization hurdles that slow adoption, particularly for elective digital nerve repair where median hospital billing reaches USD35,295, exceeding autograft procedures by USD11,224. Providers must now supply clinical data linking graft use to superior function or lower revision rates. Moreover, allografts require validated cold-chain logistics and traceability systems, inflating overhead for hospitals and ASCs. These factors temporarily temper uptake in price-sensitive regions but are unlikely to derail the long‐range expansion of the soft tissue allografts market.

Stringent and Fragmented Regulatory Landscape

The FDA’s six tissue-transplantation guidances, effective2025, tighten donor screening and sterility norms. Internationally, disparate rules for consent, testing, and distribution complicate global supply chains. Compliance lapses can shut facilities, as shown by the December2024 FDA warning letter to Integra LifeSciences for collagen implant issues. Smaller banks, unable to fund new quality systems, may exit or become acquisition targets, nudging the soft tissue allografts market toward larger, vertically integrated entities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Graft Type: Tendon Dominance Faces Dental Disruption

Tendon allografts accounted for34.12% of2025 revenue, cementing their role in ACL and rotator cuff reconstruction. This segment’s entrenched surgeon familiarity and strong biomechanical performance anchor the soft tissue allografts market. Dental/periodontal grafts, however, register an8.34% CAGR, rising on the back of implant dentistry and ridge augmentation. Dentsply Sirona’s Symbios portfolio underscores how rigorous donor screening and a Sterility Assurance Level of10⁻⁶ resonate with periodontists. Cartilage and meniscus grafts cater to niche joint-surface defects, while ligament grafts contend with autografts in active young adults. Adipose-derived matrices and specialty connective tissues mark early-stage niches but hint at broader reconstructive potential. Competitive emphasis in this graft-type landscape shows processors diversifying lines to de-risk reliance on a single clinical domain, thereby sustaining demand across the soft tissue allografts market.

Surgeons now weigh graft selection against patient age, activity, and healing profile. For example, meniscus allografts appeal to younger athletes needing shock-absorbing properties unavailable in synthetics. Across categories, continuous documentation of long-term outcomes bolsters payer confidence and streamlines reimbursement, feeding back into sustained use throughout the soft tissue allografts market.

By Processing & Preservation Method: Fresh-Frozen Legacy Meets Cellular Innovation

Fresh-frozen grafts held41.90% share in2025, benefiting from decades of clinical data and broad operating-room familiarity, positioning them as a staple in the soft tissue allografts market. Nonetheless, decellularized and acellular grafts accelerate at an8.12% CAGR because surgeons prioritize reduced rejection and improved integration. Cryopreservation maintains viable cells for orthopedic cartilage plugs, while lyophilization offers multi-year shelf life ideal for battlefield or rural care. Gamma irradiation remains a sterilization mainstay, though high doses may degrade collagen. In bone repair, demineralized bone matrix bridges classic allografts with synthetic substitutes, preserving osteoinductive proteins.

Selection criteria increasingly pivot on regenerative potential rather than simple availability. High-fidelity decellularization preserves biomechanical integrity and extracellular signaling, facilitating vascular invasion once implanted. Consequently, premium pricing aligns with outcome-focused purchasing, and processors finance R&D to compress processing time, guard growth factors, and scale manufacture. This technological arms race shapes competitive hierarchies inside the soft tissue allografts market.

By Application: Orthopedic Foundation Expands into Wound Innovation

Orthopedic reconstruction comprised40.95% of revenue in2025, confirming its status as the bedrock of the soft tissue allografts market. Yet wound and burn management accelerates fastest, clocking a8.95% CAGR through2031 as studies show skin allografts speed closure, reduce infection, and ease pain in chronic ulcers and burns. Sports medicine leverages sterility and strength to address tendon ruptures in high-performance athletes. Dental grafting outpaces broader dentistry as implant placement rises worldwide, aided by shorter treatment times when periodontal defects are resolved with off-the-shelf matrices. Cosmetic and plastic surgeons also adopt dermal grafts to limit visible scarring.

This diversification insulates suppliers from cyclical fluctuations in any single discipline. Hospitals and ASCs adjust inventory to carry multipurpose grafts compatible with orthopedics and wound care alike, reducing procurement complexity. Therefore, expanding indications and cross-disciplinary proof reinforce market breadth and depth for the soft tissue allografts market.

By End User: Hospital Stability Versus ASC Acceleration

Hospitals retained56.70% of2025 revenues, anchoring the soft tissue allografts market. Their broad caseloads, complex surgeries, and robust cold-chain storage sustain bulk purchases. Nevertheless, ASCs record a9.18% CAGR as payers push procedures into outpatient settings to curb costs. Orthopedic cases such as rotator cuff repair or bunion correction are increasingly scheduled at ASCs, which project21% volume growth to44million procedures by2034. For suppliers, decentralized demand requires smaller shipment lots, streamlined online ordering, and rapid turnaround. Specialty orthopedic clinics, research institutions, and even veterinary surgeons purchase niche grafts, rounding out a diverse customer base. Adapting fulfillment models to serve high-volume hospitals and agile ASCs concurrently becomes key to defending share in the soft tissue allografts market.

Geography Analysis

North America controlled45.10% of2025 revenue, reflecting mature tissue banks, sophisticated reimbursement, and a robust clinical research ecosystem. The presence of large processors such as LifeNet Health and MTF Biologics, together with integrated procurement organizations, ensures reliable donor pools and steady throughput. Despite dominance, value-based care initiatives urge surgeons to prove clinical superiority and cost offsets before selecting premium grafts. Upcoming federal compliance deadlines in2025 also press smaller US banks to merge or close, subtly reshaping regional supply dynamics and reinforcing the centrality of the soft tissue allografts market.

Asia-Pacific is the fastest riser, growing at7.32% CAGR through2031. Japan spearheads regenerative medicine with over60 iPS clinical trials, many intersecting with scaffold technologies that could dovetail with decellularized allografts. China’s regulatory green light for Artivion’s BioGlue in2024 signals openness to complex biologics, while urban hospitals modernize operating suites and cryogenic storage. Elsewhere, India and Southeast Asia benefit from expanding middle-class incomes and health insurance penetration, yet still grapple with fragmented regulations that slow cross-border tissue flow. Nonetheless, regional growth broadens the global footprint of the soft tissue allografts market.

Europe offers stable uptake, underpinned by harmonized directives under the European Union Tissues and Cells legislation that streamline supply across borders. National health systems favor quality-accredited grafts, and many surgeons participate in registries documenting long-term outcomes, strengthening evidence-based procurement. Mid-tier markets like the Middle East, Africa, and South America currently lag because of limited cold-chain infrastructure and higher out-of-pocket costs, yet represent long-range opportunities as private specialty hospitals proliferate. Consequently, strategic expansion plans increasingly balance the mature North American base with Asia-Pacific momentum, while nurturing footholds in emerging geographies to secure future share in the soft tissue allografts market.

Regulatory Landscape

Soft tissue allografts are governed by human tissue oversight frameworks focused on donor eligibility, traceability, and communicable-disease risk controls. In the United States, the FDA regulates human cells, tissues, and cellular and tissue-based products (HCT/Ps) mainly under 21 CFR Part 1271 (including establishment registration and product listing, donor screening/testing, and Current Good Tissue Practice requirements). A key commercial inflection occurs when products are deemed more than minimally manipulated or intended for non-homologous use, which can shift them into more stringent drug, device, or biologic pathways.

Regulatory tightening and harmonization efforts continue across major regions. The report period includes heightened US compliance focus tied to FDA tissue guidances effective in 2025, and, in Europe, adoption of Regulation (EU) 2024/1938 on substances of human origin (SoHO) in June 2024, which updates EU-wide quality and safety rules for tissues and cells intended for human application. Industry bodies also support compliance execution, including AABB's May 2026 release of an eHCTERS-focused FDA registration and listing toolkit, aimed at helping tissue establishments manage electronic registration workflows and reinforcing the value of audit-ready documentation and standardized listing practices.

Competitive Landscape

Global competition is moderately consolidated. Stryker, Johnson&Johnson, Medtronic, ZimmerBiomet, LifeNetHealth, and MTFBiologics lead, drawing strength from vertical integration—securing donor programs, proprietary processing, and global distribution. ZimmerBiomet’s January2025 acquisition of Paragon28 for USD1.1billion extends its foot-and-ankle graft catalog while diversifying beyond core arthroplasty. Device manufacturers pair implants with matched grafts to create procedure kits that simplify surgery and boost brand loyalty. Smaller tissue banks often pursue niche differentiation—such as neonatal skin grafts or adipose matrices—yet face swelling capital demands to maintain compliance.

Technology is an equally sharp wedge. Firms investing in decellularization, lyophilization, and supercritical sterilization gain premium price points. For instance, LifeNetHealth’s Matracell protocol removes ≥97% of donor DNA while retaining tensile strength, earning surgeon favor for shoulder repairs. Regulatory prowess is another moat; Integra LifeSciences’ December2024 FDA warning letter shows how lapses threaten US revenue streams. Competitive intelligence therefore focuses on pipeline innovations, facility audits, and geographic approvals that can swing share in the soft tissue allografts market.

Partnerships flourish as processors team with biotech or synthetic scaffold firms to co-develop hybrid products. MTFBiologics’ May2025 collaboration with Kolosis Bio introduces cardiac-specific grafts, unlocking an adjacency beyond orthopedics. Such moves underline a race to capture under-served procedures, reinforcing long-term growth avenues throughout the soft tissue allografts market.

Soft Tissue Allografts Industry Leaders

Stryker Corporation

CONMED Corporation

Integra LifeSciences Corporation

Smith & Nephew (Osiris Therapeutics Inc.)

BD (Becton Dickinson and Company)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Commercial opportunities are increasingly tied to ready-to-use allograft formats that shorten operating-room time and reduce procedural variability, especially in high-volume orthopedic reconstruction and ASC settings. That direction is visible in product development around pre-configured grafts and sterilization approaches that preserve biomechanics while meeting safety expectations. For example, AlloSource introduced ReConnex Pre-Sutured Tendon in July 2026 as an FDA 510(k) cleared, pre-sutured option for all-inside ACL reconstruction, which fits demand for procedural efficiency and standardized preparation.

Technology-driven differentiation continues to shape selection decisions as decellularization, cleansing, and sterilization protocols become more prominent alongside fresh-frozen supply. Suppliers with validated processes and accreditation alignment can translate regulatory rigor into commercial advantage. FDA CGTP requirements under 21 CFR Part 1271 establish mandatory baselines, while AATB accreditation and standards provide additional quality signaling through audits and inspections. As products increasingly sit near the boundary between traditional HCT/P oversight and device-like claims, companies that can support labeling, traceability, and safety documentation at scale are better positioned to compete for hospital system contracts and to build procedure-focused portfolios alongside fixation and repair implants.

Recent Industry Developments

- July 2026: AlloSource launched ReConnex Pre-Sutured Tendon, an FDA 510(k) cleared product for all-inside ACL reconstruction that leverages the AlloTrue cleansing process and low-dose electron-beam irradiation. The launch advances the market shift toward ready-to-use graft configurations that reduce intraoperative preparation steps. It also raises the competitive bar for processors that can pair sterility and handling advantages with consistent sizing and packaging.

- August 2025: CONMED launched BioBrace RC, an arthroscopic delivery system for the BioBrace implant designed for rotator cuff repair augmentation. By improving arthroscopic delivery and workflow, the system supports procedure-kit style offerings that combine implants with soft tissue reinforcement concepts. It also backs broader adoption in outpatient and hospital shoulder repair pathways where efficiency and reproducibility influence product selection.

- April 2024: Stryker announced a definitive agreement to acquire Artelon, Inc., expanding its footprint in soft tissue fixation and reinforcement solutions used alongside orthopedic repair procedures. The transaction aligns with portfolio strategies that bundle implants and soft tissue repair adjuncts to simplify surgeon ordering and inventory. It also highlights continued consolidation and capability expansion around procedure-based ecosystems that intersect with allograft utilization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenue generated from human donor derived soft tissue grafts that are processed and supplied for implantation in orthopedic, dental, and reconstructive procedures.

Scope exclusions: This sizing excludes autografts, xenografts, synthetic meshes, and biologic matrices used only as wound dressings.

Segmentation Overview

- By Graft Type

- Cartilage Allograft

- Tendon Allograft

- Meniscus Allograft

- Ligament Allograft

- Dental/Periodontal Allograft

- Other Graft Types

- By Processing & Preservation Method

- Fresh-Frozen

- Cryopreserved

- Lyophilized

- Gamma-Irradiated Sterilized

- Decellularized & Acellular

- Demineralized Bone Matrix (DBM)

- By Application

- Orthopedic Reconstruction

- Sports Medicine

- Dentistry & Periodontics

- Wound & Burn Management

- Cosmetic & Plastic Surgery

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Orthopedic Specialty Clinics

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping how tissues move from donation to processing and then into clinical use, because this flow determines where revenue is recorded for implantable grafts. We used public sources such as US FDA guidance and safety communications, CDC health statistics, WHO health indicators, and OECD health data to understand procedure environments and demand signals.

We also reviewed peer reviewed clinical literature on graft utilization, along with tissue bank and medical association publications that describe standards and processing practices. Company filings and investor presentations were checked to understand product mix wording, geographic exposure, and how pricing is discussed, which helps anchor assumptions. In a few places, we referred to paid subscriptions that provide company financials, news and filings, and patent databases to cross-check timelines and product positioning. These sources are illustrative, and we also used many other public references to collect data, validate assumptions, and clarify details.

Primary Interviews and Surveys

Primary work focused on expert interviews and structured surveys with tissue processors, distributors, and clinical stakeholders who influence product choice and case volume, including procurement and materials teams. Inputs were validated across APAC, EMEA, and the Americas so we could test differences in donor supply, reimbursement, and procedure mix, and then align assumptions to how buying happens in hospitals, ASCs, and specialty clinics.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 38% |

| Mid tier: 42% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 21% | Managers: 57% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where procedure volumes and treated case pools are reconstructed by geography, and then converted into graft demand using penetration rates and average units per procedure. Once that demand pool is formed, we apply price bands by graft category and channel, and totals are then adjusted based on what buyers report as typical contracting and mix.

To keep the model tied to observable buying behavior, it uses practical inputs such as orthopedic sports injury related surgery activity, dental implant and periodontal procedure activity, share of cases using allografts versus alternatives, tissue processing yield and discard rates, and observed pricing movement by processing type. Where a country has thin public data, gaps are handled by using proxy indicators such as hospital throughput and surgeon feedback on utilization patterns, followed by a recheck of the assumption in follow up calls.

Forecasts are produced using scenario analysis that tests donor supply constraints, compliance costs linked to regulatory actions, and procedure growth rates. The final outlook is aligned to what interviewees describe as the most likely path, and a selective bottom-up approximation is used as a reasonableness check through sampled ASP times volume and channel checks.

Data Validation & Update Cycle

Validation is done by comparing the modeled totals against independent signals such as procedure growth indicators, known shifts in setting of care between hospitals and ASCs, and reported pricing direction from procurement discussions. When large variances show up, we revisit the underlying drivers, and we re-contact sources if the difference cannot be explained by scope or timing.

Before sign-off, the model and assumptions go through stepwise analyst reviews so calculation logic, currency conversions, and regional splits are consistent. Reports are refreshed annually, with interim updates when major regulatory changes, supply disruptions, or meaningful pricing shifts occur. Right before delivery, a final pass is completed so clients receive the latest updated view based on the most recent public information.

Mordor Intelligence's Soft Tissue Allografts Market Size Compared With Other Published Estimates

Published market numbers can differ a lot even when the topic sounds the same, because each publisher chooses its own product boundaries, revenue point in the value chain, and year matching for currency and inflation. Differences in how procedure demand is converted into unit volumes, and how prices are averaged across graft types, also pushes estimates apart.

The table shows a wide spread for 2025, and under Mordor Intelligence's scope the count is limited to processed human donor soft tissue allografts sold for implantation, which excludes autografts, xenografts, synthetic meshes, and wound dressing only matrices. Other figures can look larger when related services are included at the manufacturer level, when adjacent biologic patch categories are grouped into the same total, or when price uplift is applied without being checked against procurement feedback by site of care.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.95 B (2025) | |

| Industry Publisher A | USD 5.48 B (2025) | This figure appears to apply a wider product basket across multiple allograft categories without clearly separating implantable graft revenue from adjacent biologics, which can lift the base-year total. |

| Global Research Group B | USD 4.87 B (2025) | This estimate is presented at factory gate values and can include related services sold by the creator of the goods, which shifts the revenue capture point versus an implant use based view. |

Across the three sources, the main drivers behind the gap are scope coverage and where revenue is counted in the chain, followed by pricing and mix assumptions by procedure type. By keeping the steps tied to observable procedure activity and buyer reported usage patterns, our numbers remain traceable and easier to update when inputs change.

Key Questions Answered in the Report

What is the current value of the soft tissue allografts market?

The market stands at USD 4.21 billion in 2026 and is projected to reach USD 5.82 billion by 2031.

Which graft type leads revenue today?

Tendon allografts command the largest 34.12% share, driven by ACL and rotator cuff repairs.

Who are the key players in Soft Tissue Allografts Market?

ASCs grow at a 9.18% CAGR and shift procurement from large hospital batches to smaller, rapid-turn orders, requiring new distribution models.

How will FDA guidance released in 2025 influence suppliers?

Stricter donor screening and processing rules raise compliance costs, pressuring smaller banks to merge or exit.

Which region is expanding fastest?

Asia-Pacific posts a 7.32% CAGR as healthcare access widens and regulatory approvals for biologics accelerate.

What technology trend most affects graft selection?

Decellularization and acellular processing improve integration and reduce rejection, prompting more surgeons to choose these advanced grafts over traditional fresh-frozen products.

Page last updated on: