Dental Bone Graft Substitutes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Bone Graft Substitutes Market Analysis by Mordor Intelligence

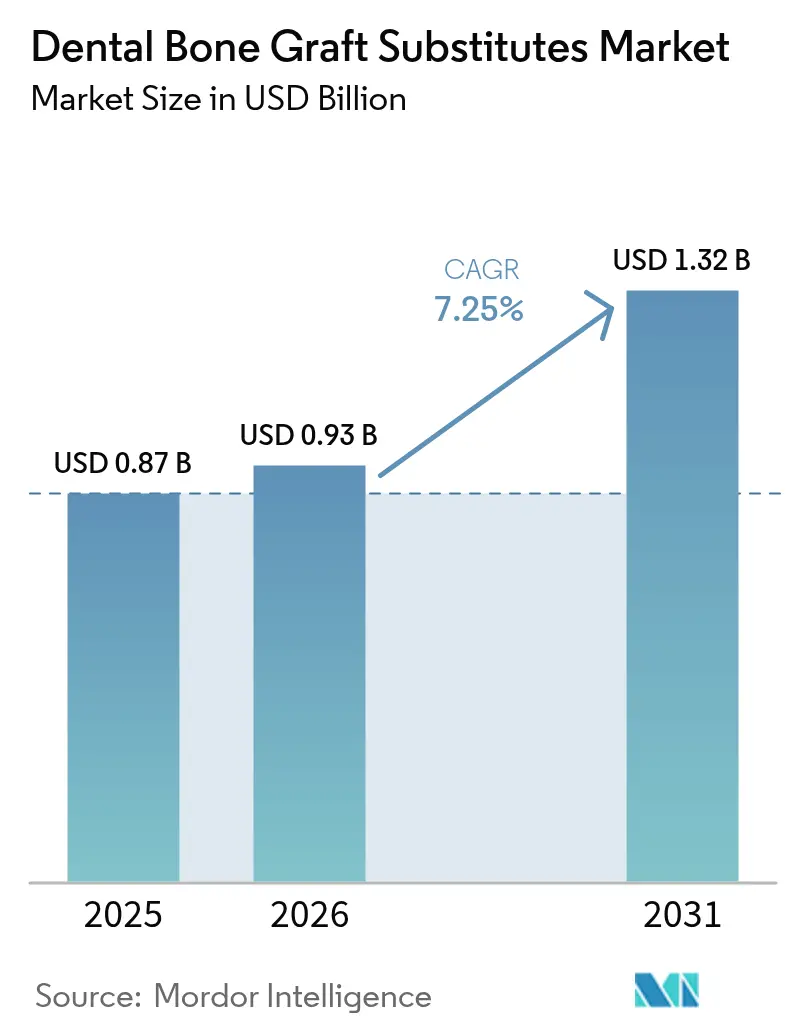

The dental bone graft substitutes market size is expected to grow from USD 0.87 billion in 2025 to USD 0.93 billion in 2026 and is forecast to reach USD 1.32 billion by 2031 at 7.25% CAGR over 2026-2031. Steady expansion reflects the shift from autograft dependency toward synthetic solutions that satisfy clinical, ethical, and supply-chain demands. Three macro forces underpin this growth: a rising elderly population prone to edentulism, an escalating global periodontal disease burden, and rapid adoption of CAD/CAM-enabled customization that improves surgical accuracy. Growing medical tourism—especially in Thailand, where the medical device sector totaled USD 7.2 billion in 2024—funnels international patients to high-quality yet affordable clinics. Meanwhile, payer policies such as UnitedHealthcare’s 2024 update increasingly reimburse ridge preservation, stimulating procedure volumes.

Key Report Takeaways

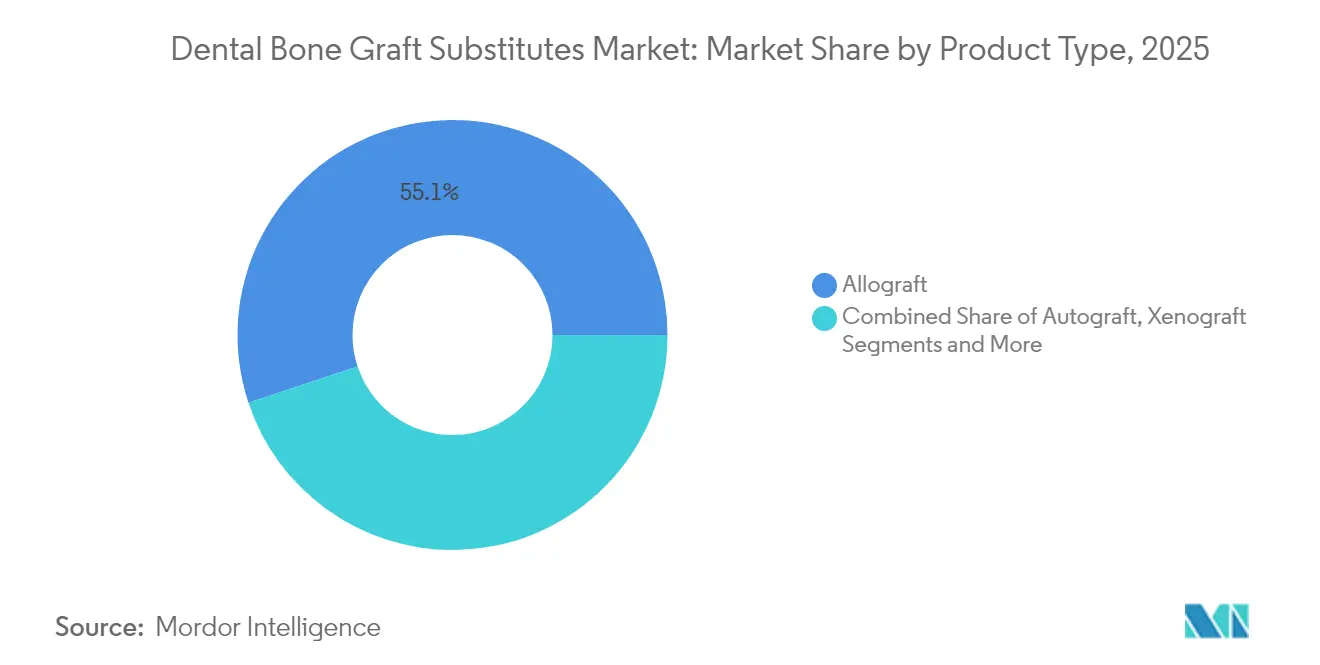

- By product type, allografts led with 55.10% revenue share in 2025; synthetic/alloplast materials are forecast to expand at a 9.78% CAGR to 2031.

- By mechanism, osteoconduction accounted for 60.10% of the dental bone graft substitutes market share in 2025, while osteoinduction is projected to rise at a 9.02% CAGR through 2031.

- By material, ceramic-based solutions held 43.30% share of the dental bone graft substitutes market size in 2025; growth factor-enhanced materials are set to climb at an 10.74% CAGR between 2026-2031.

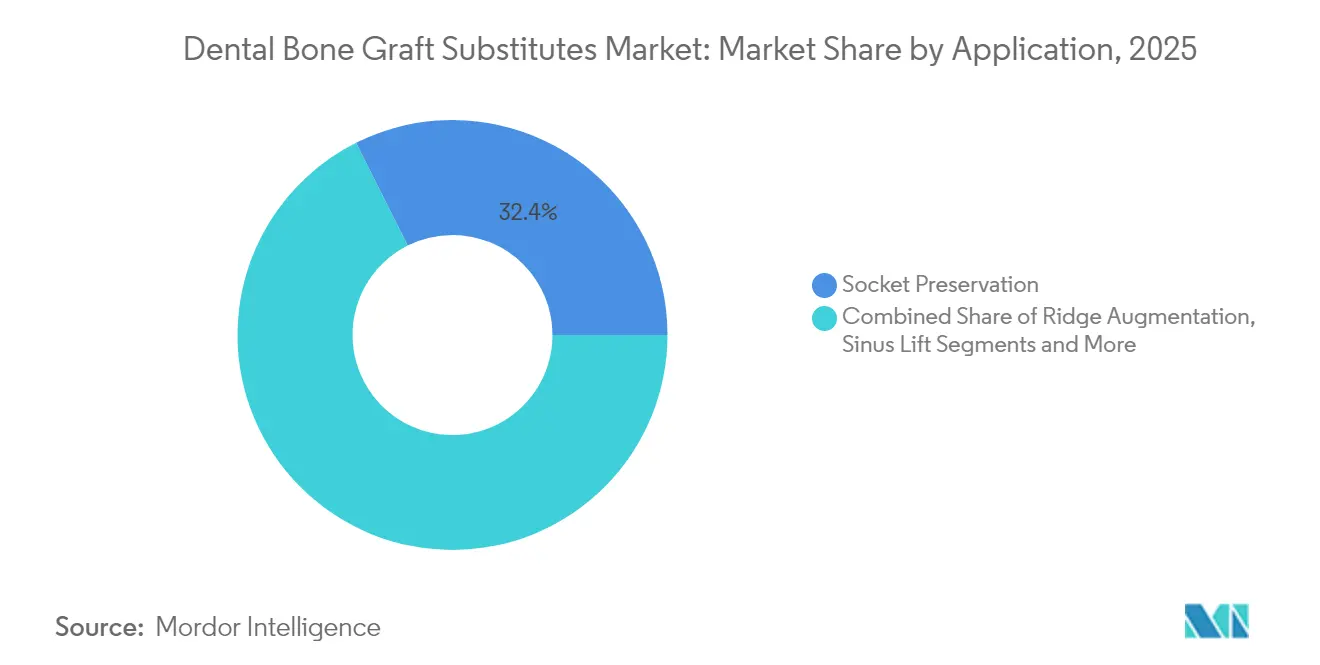

- By application, socket preservation captured 32.40% share in 2025; implant bone regeneration is poised for the fastest 12.05% CAGR to 2031.

- By end user, hospitals controlled 48.30% share in 2025, whereas dental clinics are advancing at a 9.28% CAGR through 2031.

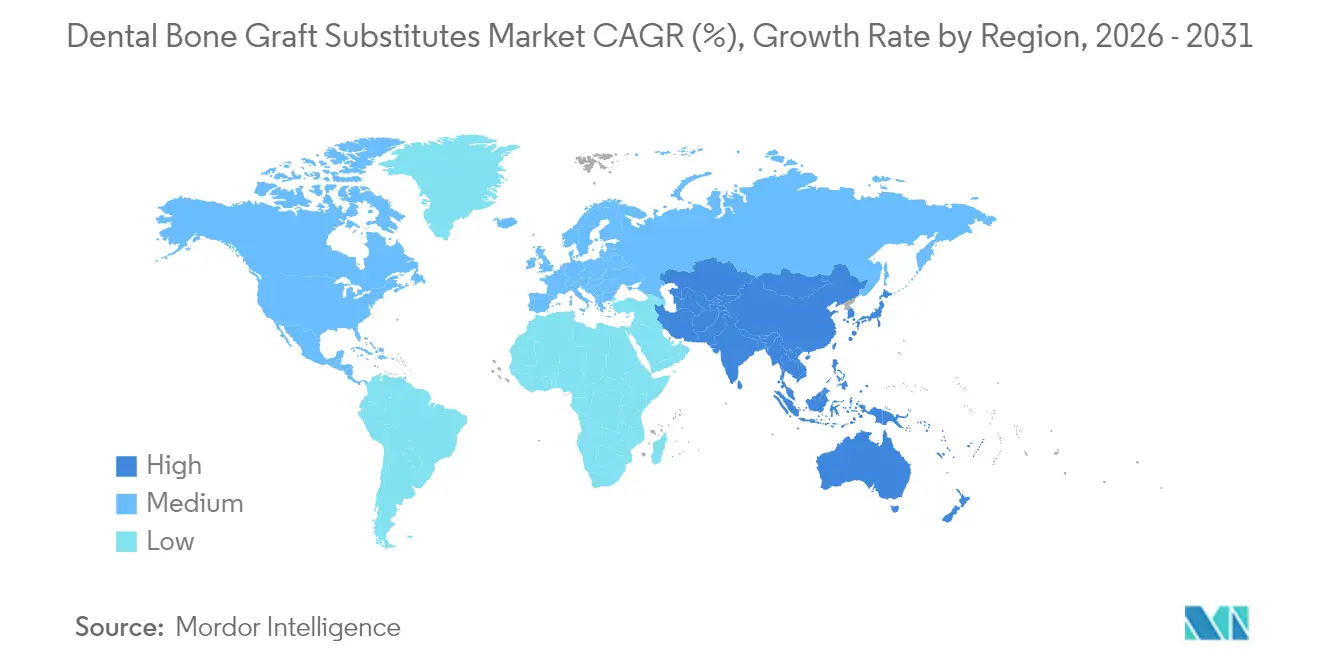

- By geography, North America captured 35.40% revenue share in 2025, yet Asia-Pacific is forecast to grow at a 11.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Bone Graft Substitutes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring outbound medical & dental tourism flows | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Escalating global burden of periodontal & edentulous disorders | +1.8% | Global | Long term (≥ 4 years) |

| Rapid adoption of CAD/CAM & 3-D printing-enabled custom grafts | +1.5% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Growing preference for synthetic alloplasts amid religious/ethical concerns | +0.9% | Global, strong in Middle East | Medium term (2-4 years) |

| Favorable reimbursement expansion for regenerative dental procedures | +0.8% | North America & EU | Medium term (2-4 years) |

| Emergence of growth-factor–laden biomimetic matrices | +1.1% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Periodontal & Edentulous Disorders

The World Health Organization reports that 3.5 billion people live with oral diseases, generating USD 387 billion in direct costs each year. Severe periodontitis accelerates alveolar bone loss, expanding the need for regeneration solutions. Clinical trials show 35.6% greater bone volume when FGF-2-impregnated atelocollagen sponges are used. An aging demographic exacerbates demand, as 353 million people were edentulous in 2024, with projections of 661 million by 2050. This demographic and clinical pressure directly fuels procedure volumes within the dental bone graft substitutes market.

Rapid Adoption of CAD/CAM & 3-D Printing-Enabled Custom Grafts

Nanoscale 3-D printing breakthroughs from the University of Sydney deliver bone-mimicking scaffolds with natural-like porosity and strength[1]Hala Zreiqat, “3D Printing Bones at the Nano Level Achieved,” sydney.edu.au. Open-source CAD/CAM software lets surgeons design titanium meshes that fit precisely, shortening operating times. Bioactive glass scaffolds fabricated through additive manufacturing yielded 43.93% bone volume fraction in atrophic ridges. These digital workflows command premium pricing yet curb revision rates, sustaining margin expansion for suppliers competing in the dental bone graft substitutes market.

Growing Preference for Synthetic Alloplasts Amid Religious/Ethical Concerns

Coral-inspired synthetic matrices achieve complete defect repair in 3-6 months without exogenous biologics. Religious constraints and disease transmission fears intensified after a 2023 tuberculosis outbreak from contaminated allografts in seven U.S. states[2]Centers for Disease Control and Prevention, “Second Nationwide Tuberculosis Outbreak Caused by Bone Allografts Containing Live Cells — United States, 2023,” cdc.gov. Beta-tricalcium phosphate–calcium sulfate blends re-mineralize 50% in 12 weeks and 85% by week 33. Producers such as Biomatlante have shipped synthetic grafts to 50+ countries, underscoring global traction.

Emergence of Growth-Factor–Laden Biomimetic Matrices

Recombinant PDGF-BB paired with osteoconductive matrices already claims FDA approval for alveolar repairs and matches autograft outcomes. Platelet-rich fibrin doubles as scaffold and biologic reservoir, enhancing stem-cell proliferation. Nano-sustained release platforms entering Phase II trials align growth-factor kinetics with tissue formation. A spinal fusion study reported 100% union at 12 months using an integrative matrix. High manufacturing costs limit uptake today but suit premium, complex reconstructions and strengthen differentiation across the dental bone graft substitutes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure & product cost vis-à-vis conventional dentures | -1.4% | Global, acute in emerging markets | Medium term (2-4 years) |

| Limited reimbursement in emerging markets | -1.1% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Scarcity & logistics issues in human-donor tissue supply chains | -0.8% | Global | Short term (≤ 2 years) |

| Persistent ethical push-back against xenograft sourcing | -0.6% | Middle East, parts of Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure & Product Cost Vis-à-Vis Conventional Dentures

Economic evaluations show retaining at-risk teeth is cheaper than replacing them with implants, especially once peri-implantitis maintenance is considered. Graft materials alone add USD 46.2–140 per case. Multiple visits and protracted healing magnify total spend, dampening uptake among cost-sensitive groups. Providers in the dental bone graft substitutes market mitigate sticker shock through bundled procedure pricing and in-house manufacturing that compresses overhead.

Limited Reimbursement in Emerging Markets

Coverage gaps leave patients self-funding advanced grafts despite widening middle-class incomes. Many payers lack specific codes for growth-factor matrices or 3-D printed grafts, forcing a two-tier system. Government insurance in Thailand or India often caps reimbursement at basic xenografts, leaving premium synthetics off-limits to average citizens. Private insurers either exclude dental procedures or set low annual maximums, curbing adoption even as the dental bone graft substitutes market grows on the premium end. Regional health-authority pilots aim to update codes, but progress lags technological innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Allografts Lead Despite Synthetic Surge

Allografts maintained a 55.10% share in 2025, driven by surgeon familiarity and extensive clinical evidence. However, the tuberculosis outbreak triggered stricter screening, nudging clinicians toward disease-free synthetics. Synthetic/alloplast innovations post a 9.78% CAGR, buoyed by coral-inspired designs and growth-factor additives that sidestep donor-tissue shortages. The dental bone graft substitutes market size for synthetic/alloplast products is slated to widen as 3-D printing streamlines custom shapes.

Autografts remain the biological benchmark yet suffer donor-site morbidity and limited volume. Xenografts serve niche complex reconstructions; segmented equine sheets achieved horizontal gains of 6.18 mm in 3-D defects. Emerging dentin-derived xenogeneic matrices extend indications by retaining organic components.

By Mechanism: Osteoconduction Dominance Challenged by Osteoinduction

Osteoconductive scaffolds accounted for 60.10% of the dental bone graft substitutes market in 2025. Reliability across socket preservation and ridge augmentation sustains volume. Osteoinductive products, led by recombinant growth-factor matrices, are tracking a 9.02% CAGR owing to superior defect fill: FGF-2 sponges produced 35.6% extra bone area in lab studies.

Hybrid constructs now merge osteoconduction, osteoinduction, and osteogenesis. An integrative matrix reached 100% spinal fusion at 12 months. As evidence accumulates, hospitals revise protocols, increasing the dental bone graft substitutes market share of multi-mechanism devices.

By Material: Ceramic Foundations Enable Growth-Factor Innovations

Ceramic matrices, chiefly hydroxyapatite and β-tricalcium phosphate, captured 43.30% share in 2025 thanks to predictable resorption. A β-TCP/calcium-sulfate mix resorbed 50% by week 12 and 85% by week 33. Growth factor-enhanced materials record an 10.74% CAGR as nano-controlled release prolongs biologic activity.

Collagen scaffolds accelerate vascularization; a hydroxyapatite/collagen composite matched autograft fusion in cervical surgeries. Polymer-ceramic hybrids tailor strength and degradation, while plant-derived apatites, validated for ethical compatibility, enter pilot use. These innovations enlarge the dental bone graft substitutes market size by tapping elective cosmetic cases.

By Application: Socket Preservation Dominates While Implant Regeneration Surges

Socket preservation held 32.40% share in 2025. Combining allograft and xenograft granules limited horizontal loss to 1.6 mm after 4 months. As global implant placement rises, implant bone regeneration exhibits a 12.05% CAGR. The dental bone graft substitutes market size for implant regeneration grows faster where peri-implant deficiencies demand tailored grafts.

Ridge augmentation benefits from customized titanium meshes printed via CAD/CAM, delivering predictable contour restoration. Sinus lifts rely on bioactive glass scaffolds for atrophic maxillae. Autologous tooth grafts demonstrated 100% 5-year implant success.

By End User: Hospital Dominance Shifts Toward Specialized Centers

Hospitals controlled 48.30% revenue in 2025 owing to infrastructure suited for multistage, comorbidity-laden cases. Yet specialized dental clinics advance at 9.28% CAGR as outpatient workflows lower cost and recovery time. Digital in-house 3-D printing empowers clinics to design grafts and guides within hours, supporting broader diffusion of the dental bone graft substitutes market.

Ambulatory surgical centers attract routine grafting with same-day discharge. Academic institutes pilot nano-release factors and biomimetic matrices, accelerating translation to commercial channels.

Geography Analysis

North America held 35.40% share in 2025, boosted by comprehensive reimbursement and early technology adoption. UnitedHealthcare’s 2024 policy clarified graft coverage, raising case volumes. The FDA’s 2024 breakthrough device awards to Renovos and CGBio signal continued innovation support. Nonetheless, the 2023 allograft-linked tuberculosis outbreak led to tighter donor screening, temporarily slowing allograft sales. These dynamics encourage synthetic uptake, reinforcing momentum for the dental bone graft substitutes market.

Asia-Pacific is the fastest-growing region at 11.05% CAGR on the back of enlarging medical tourism hubs and rising discretionary income. Thailand’s medical-device sector reached USD 7.2 billion in 2024, exemplifying supportive infrastructure. Super-aged profiles in Japan, South Korea, and Thailand elevate demand for implants and associated grafts. However, limited reimbursement hinders mass adoption, keeping price-sensitive segments reliant on lower-cost xenografts.

Europe maintains a mature yet innovation-friendly market. Rigorous CE-mark pathways favor companies with strong clinical dossiers, while public health systems emphasize ethical sourcing, fueling synthetic alternatives. Collaborative research networks expedite biomaterial breakthroughs that quickly reach German and Scandinavian clinics. Economic pressures temper expenditure growth but stable aging demographics ensure steady baseline demand for the dental bone graft substitutes market.

Competitive Landscape

The market is moderately fragmented. Geistlich Pharma’s Bio-Oss remains the world’s best-selling xenograft, backed by 30 years of clinical data. Straumann Group optimized its portfolio by divesting DrSmile in 2024 to concentrate on implants and regeneration, yet retained 20% equity to keep aligner exposure.

Regulatory strategy is an emerging differentiator. Amphix Bio, CGBio, and Renovos secured FDA breakthrough designations in 2024 for novel biomimetic gels and putties, accelerating U.S. entry. Coral-inspired synthetic developers focus on Middle-East markets where religious concerns amplify demand. 3-D printing specialists collaborate with OEM printer firms to bundle software, materials, and service, creating turnkey offerings.

Supply chain robustness shapes competitive standing. LifeNet Health launched OraGen in February 2024, a cryopreserved viable allograft blending corticocancellous bone with demineralized matrix, targeting hospitals that require live-cell performance. Synthetic entrants highlight predictable sourcing and sterility advantages, capturing share amid donor-tissue scrutiny.

Dental Bone Graft Substitutes Industry Leaders

Johnson & Johnson

Institut Straumann AG

Medtronic PLC

Dentsply Sirona

ZimVie Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is emerging for synthetic/alloplast and modified xenograft formats that reduce reliance on donor tissue, while offering more controllable remodeling kinetics for ridge preservation, sinus lift, and implant site regeneration. FDA 510(k) clearances in 2026 for synthetic maxillofacial/dental bone grafting materials, including Hudens Bio Co., Ltd. (BONTREE PLUS, K251818) and Bonalive, Ltd. (Bonalive Maxillofacial, K253883), reflect an active pathway for LYC-class devices and raise the bar for equivalence claims tied to porosity, handling, and sterilization specifications.

Clinical and translational activity also points to opportunities in patient-derived and biomimetic matrices that better align with site-specific healing windows, rather than one-size-fits-all graft selection. 2026 comparative evidence showing autogenous demineralized dentin matrix (DDM) delivering dimensional stability comparable to common xenograft references in alveolar ridge preservation supports reuse-and-recycle workflows for clinics with the right processing capability. In parallel, development on engineered microbeads and improved DBBM processing (deproteinization efficiency and particle porosity) continues to differentiate products through material science and manufacturing controls, leaving room for suppliers that package graft materials with digital planning and CAD/CAM-enabled customization for high-throughput implant and regeneration centers.

Recent Industry Developments

- May 2026: DePuy Synthes (Johnson & Johnson) entered an exclusive distribution agreement with CGBIO for NOVOSIS across the United States, Canada, and Australia. The deal expands access to a growth factor-containing bone graft substitute through a major orthopedic channel, increasing competitive pressure on premium biologics and supporting portfolio bundling by large strategics.

- February 2026: Medtronic received FDA premarket approval for expanded use of INFUSE Bone Graft in one- and two-level TLIF procedures (L2-S1), including use with PEEK and titanium interbody cages. While this is spine-focused, it reinforces how clinical evidence and label expansion in bone graft biologics can shift investment and partnering priorities across regeneration categories that share suppliers and enabling technologies.

- August 2024: LifeNet Health, together with Johnson & Johnson MedTech, launched PliaFX Pak, a 100% bone allograft solution for orthopedic spine and trauma procedures. The launch underscores continued commercialization of processed allograft formats and highlights how supply reliability and processing know-how can shape clinician confidence in human-tissue-based graft offerings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from dental bone graft substitutes used to rebuild or preserve alveolar bone as part of dental treatment, where products are used during procedures tied to implant placement and periodontal repair.

Scope exclusions: We exclude orthopedic bone void fillers and non-dental cranio-maxillofacial grafting that is not performed within routine dental care settings.

Segmentation Overview

- By Product Type

- Autograft

- Allograft

- Xenograft

- Synthetic/Alloplast

- Other Types

- By Mechanism

- Osteoconduction

- Osteoinduction

- Osteogenesis

- Osteopromotion

- By Material

- Ceramic-based

- Collagen-based

- Growth-factor-enhanced

- Polymer & Composite

- By Application

- Socket Preservation

- Ridge Augmentation

- Sinus Lift

- Periodontal Defect Regeneration

- Implant Bone Regeneration

- By End User

- Hospitals

- Dental Clinics & Implant Centers

- Ambulatory Surgical Centers

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping how demand is created, which usually links to dental implant treatment volumes, periodontal disease burden, and the mix of procedures where grafting is used. We used public sources to set the outer boundaries and sanity-check totals, including statistics and publications from the World Health Organization, the US CDC, and the US FDA device databases.

We also reviewed clinical guidance and peer-reviewed dental journals to understand which procedures commonly use graft substitutes, such as socket preservation, sinus lift, and ridge augmentation, and then translated that into a measurable demand pool. Company filings, investor presentations, reputable press, patent databases, and an import and export shipment-level database were used selectively to cross-check product availability, pricing direction, and regional momentum. These desk research sources are illustrative, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on dentists, periodontists, implant specialists, distributors, and product managers who see ordering patterns and procedure mix changes in real time. We used these discussions to confirm utilization rates for grafting across common dental procedures, to validate realistic average selling price ranges by material type, and to stress-test regional growth assumptions across major geographies.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | APAC: 43% |

| Mid tier: 49% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 16% | Managers: 53% | Americas: 21% |

Market-Sizing & Forecasting

Our sizing model begins with a top-down build that reconstructs the demand pool using dental implant placement activity, grafting penetration by procedure type, and typical product usage per case. Once procedure-linked demand is established, pricing is applied using realistic average selling prices that reflect mix shifts between xenografts, allografts, and synthetic materials, which are then adjusted for country purchasing patterns and channel markups.

To keep totals grounded, results are corroborated with selective bottom-up approximations, such as sampled ASP times volume checks through distributor feedback, and supplier-side revenue direction from public financial disclosures where dental exposure is clear. Inputs that shape the model include implant procedure growth, periodontal disease prevalence signals, the split between private clinics and hospitals, adoption trends for guided bone regeneration workflows, and reimbursement and out-of-pocket sensitivity by region. For forecasting, scenario analysis is used around procedure growth and price progression, including mix-driven ASP movement, and then aligned to what interviewees described as the most likely base case. Where direct volume or pricing points are missing for smaller countries, we fill gaps using proxy markets with similar procedure density and income levels, and then re-check the implied per-procedure spend for reasonableness.

Data Validation & Update Cycle

We validate outputs through multiple checks, starting with reconciliation between procedure-linked demand, implied per-case spending, and region-level revenue concentration. Outliers are flagged when growth, pricing, or penetration moves outside what clinical usage patterns and channel feedback would support, and then assumptions are revisited before sign-off.

A second analyst review is completed to confirm that key inputs were applied consistently across regions, and to ensure currency conversion timing and inflation handling are not distorting the time series. Reports are refreshed annually, with interim updates triggered when a material event changes procedure volumes, pricing, or product availability. Before delivery, we do a final pass so clients receive the most current view available at the time of publication.

Mordor Intelligence's Dental Bone Graft Substitutes Market Size Compared With Other Published Estimates

Published market values can vary because authors do not always count the same products, procedures, or geographies, and they may also use different year timing for currency conversion and pricing. In this market, the spread often comes from whether adjacent dental biomaterials are included, how implant-related procedure counts are estimated, and how fast price changes are assumed to flow through average selling prices.

Refresh cadence also matters here because procedure mix and premium material adoption can shift within a year, which changes the implied spend per case. When exchange rates are taken at different cutoffs and ASP progression is not rechecked with fresh channel feedback, totals can drift even if unit demand is similar, and those controls are applied in the update cycle followed by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.87 B (2025) | |

| Trade Journal A | USD 1.40 B (2026) | This figure uses a later starting year and can reflect a broader counted product set and a higher starting ASP, which lifts the total even if procedure volumes are similar. |

| Industry Data Provider B | USD 2.33 B (2025) | The scope appears to combine dental bone graft substitutes with other biomaterials, so revenues from adjacent dental biomaterials are likely included, which expands the market beyond graft substitutes alone. |

The table shows that the biggest differences come from what is included in the product boundary and how pricing and year timing are treated. We keep the scope limited to graft substitutes tied to dental procedures, and then apply repeatable checks on procedure demand and realistic ASP ranges so the final number is traceable and practical to update.

Key Questions Answered in the Report

What is the current value of the dental bone graft & substitutes market?

The market is valued at USD 0.93 billion in 2026 and is projected to hit USD 1.32 billion by 2031 at a 7.25% CAGR.

Which product segment is growing fastest?

Synthetic/alloplast materials are expanding at a 9.78% CAGR through 2031 as clinicians adopt coral-inspired and bioactive glass grafts.

Why are synthetic grafts gaining popularity?

They eliminate disease-transmission risk, satisfy religious-ethical concerns, and increasingly match or surpass allograft performance in bone regeneration timelines.

Which region will see the quickest market growth?

Asia-Pacific leads with an 11.05% CAGR, driven by medical-tourism hubs and aging populations seeking implant-based restorations.

How are CAD/CAM and 3-D printing influencing the market?

Digital workflows allow patient-specific grafts and titanium meshes, reducing operative time and revision rates while commanding premium procedure fees.

Page last updated on: