Contrast Enhanced Ultrasound Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

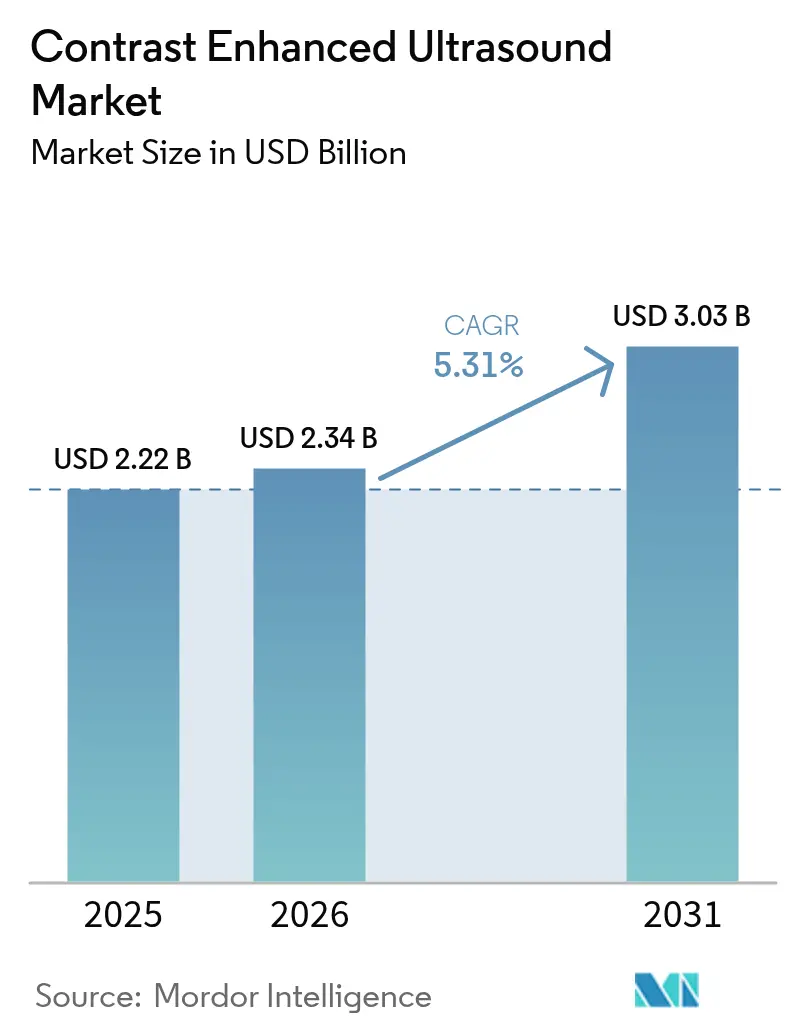

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 3.03 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contrast Enhanced Ultrasound Market Analysis by Mordor Intelligence

Contrast Enhanced Ultrasound Market size in 2026 is estimated at USD 2.34 billion, growing from 2025 value of USD 2.22 billion with 2031 projections showing USD 3.03 billion, growing at 5.31% CAGR over 2026-2031.

Demand is propelled by the rising use of radiation-free imaging, the growing burden of cardiovascular and hepatic disorders, and broader point-of-care adoption. Equipment sales remain the largest revenue generator, yet contrast-agent volumes are accelerating as new microbubble formulations deepen clinical utility. Asia is the fastest-growing geography on the back of infrastructure expansion in China and Japan, while oncology leads application growth as CEUS becomes integral to tumor characterization. Strategic investments by vendors and governments are shortening innovation cycles even as regulatory hurdles and workforce shortages temper near-term momentum.

Key Report Takeaways

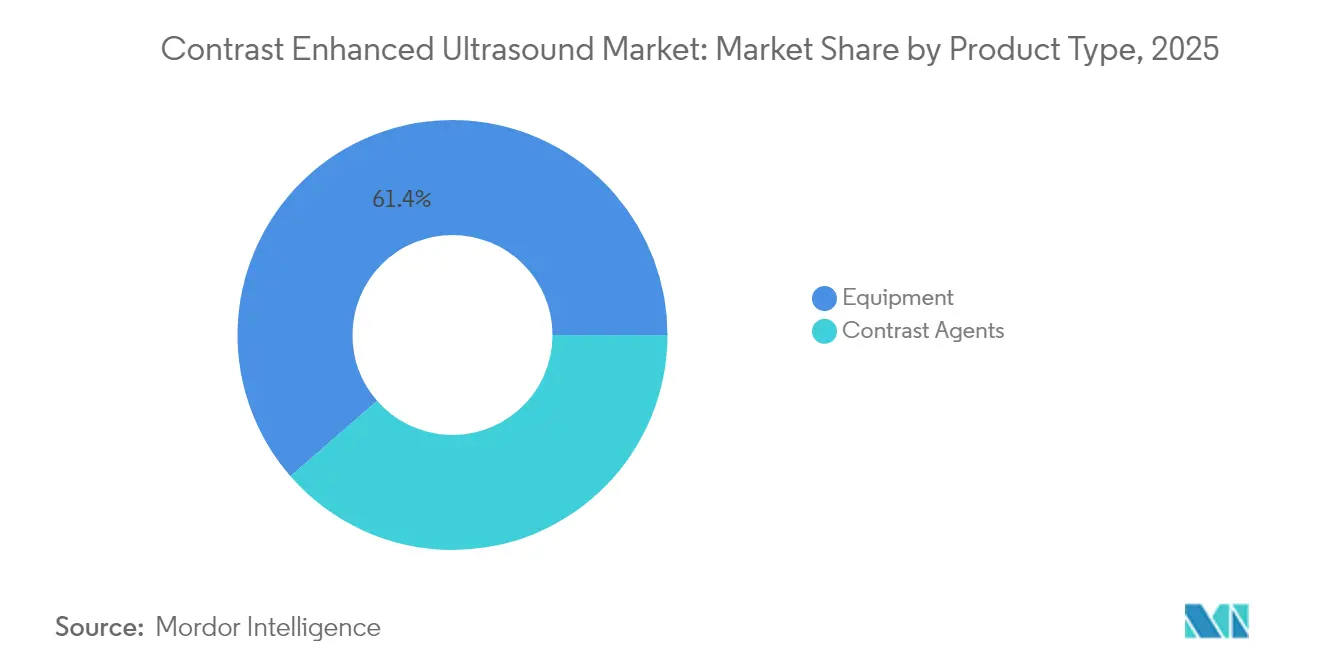

- By product type, equipment commanded 61.42% of the contrast-enhanced ultrasound market share in 2025; contrast agents are advancing at an 10.74% CAGR through 2031.

- By technology, non-targeted CEUS held 88.07% of the contrast-enhanced ultrasound market share in 2025, whereas targeted CEUS is projected to grow at 14.02% CAGR between 2026-2031.

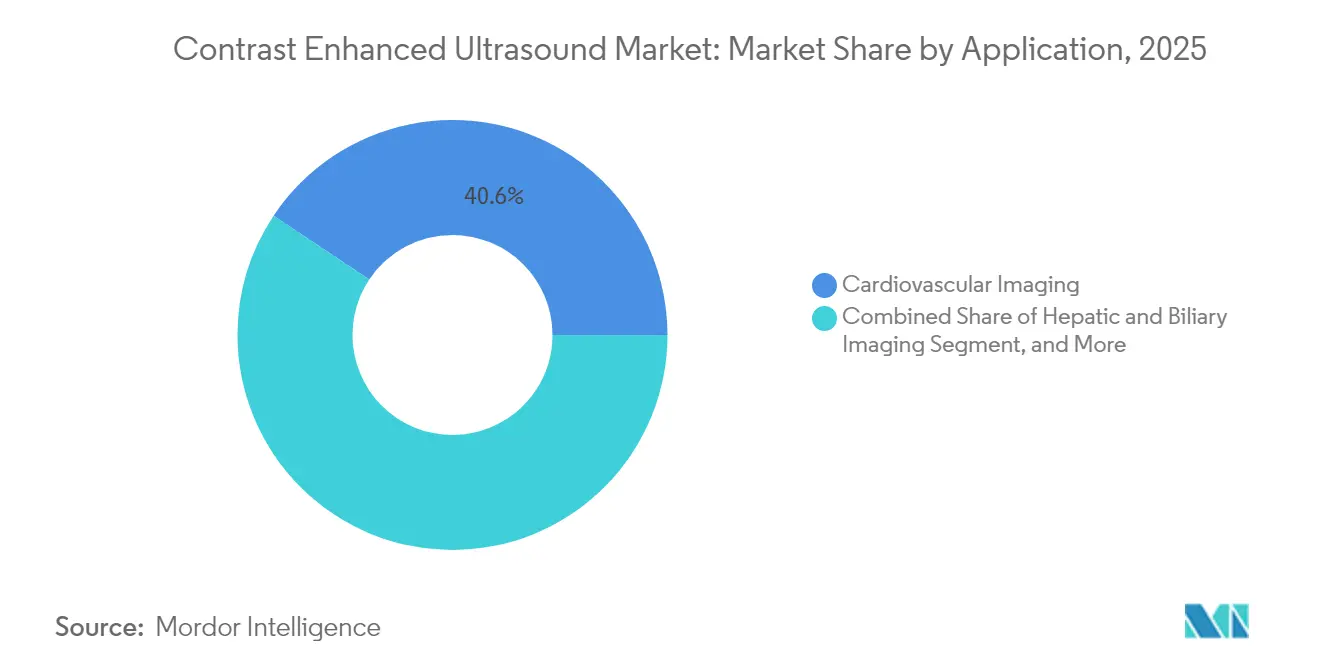

- By application, cardiovascular imaging captured 40.64% of the contrast-enhanced ultrasound market size in 2025, and oncology is expected to register the fastest growth rate of 12.11% from 2025 to 2031.

- By end-user, hospitals accounted for a 69.03% share of the contrast-enhanced ultrasound market size in 2025, while diagnostic imaging centers are expected to expand at a 10.04% CAGR through 2031.

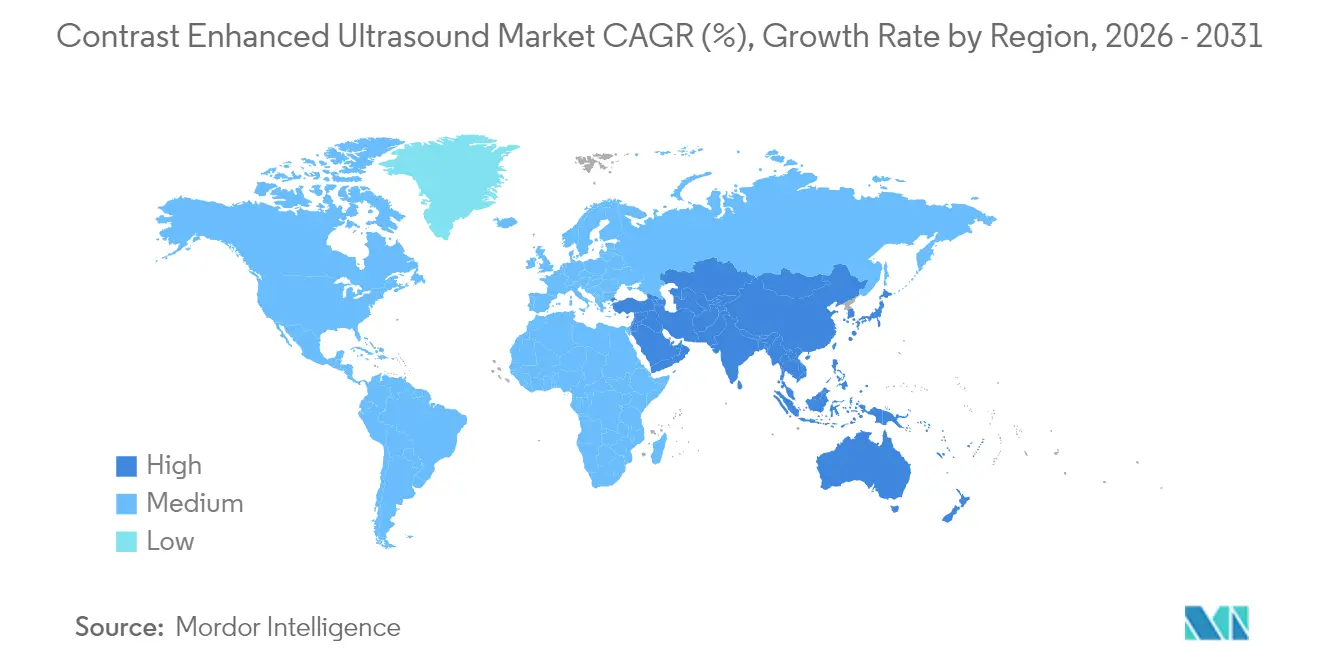

- By geography, North America commanded 36.88% of the 2025 contrast-enhanced ultrasound market share; Asia-Pacific is set to grow at 9.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contrast Enhanced Ultrasound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic cardiovascular & hepatic disease burden | +2.1% | North America, Europe, global emerging economies | Medium term (2-4 years) |

| Shift toward radiation-free imaging | +1.8% | Global (early uptake in North America & Europe) | Long term (≥ 4 years) |

| Expansion of point-of-care ultrasound | +1.2% | North America, Europe, major Asian metros | Medium term (2-4 years) |

| Government & private investment surge | +0.9% | North America, Europe, Asia | Short term (≤ 2 years) |

| Rising demand for minimally invasive diagnostics | +0.7% | Global | Long term (≥ 4 years) |

| Technological advances in microbubble agents | +0.6% | Global research hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Cardiovascular & Hepatic Diseases Necessitating Real-Time Perfusion Imaging

Steady growth in cardiac and liver pathologies heightens demand for dynamic perfusion assessment. CEUS delivers real-time visualization of microvascular flow that conventional B-mode ultrasound misses, achieving 86% sensitivity and 91.3% specificity for differentiating malignant from benign liver lesions in multi-center trials.[1]Tian-Hua Tian et al., “Diagnostic Performance of CEUS in Liver Lesions,” Journal of Clinical Medicine, jclinmed.com These performance gains reduce secondary imaging and support earlier interventions, promoting wider procedural adoption across tertiary centers in North America and Europe.

Shift Toward Radiation-Free Imaging for Pediatric & Pregnant Populations

Concerns over ionizing radiation continue to steer clinicians toward ultrasound. CEUS provides diagnostic performance comparable with CT or MRI while eliminating radiation and nephrotoxicity risks. Severe adverse reactions occur in fewer than 0.01% of administrations, according to the Cleveland Clinic.[2]Cleveland Clinic, “Ultrasound Contrast Agent Safety Update,” clevelandclinic.org Policy directives in Europe and updated pediatric guidelines in the United States further reinforce this transition, encouraging hospitals to embed CEUS pathways in routine pediatric liver and renal work-ups.

Expansion of Point-of-Care Ultrasound Platforms in Emergency & Critical Care

Bedside CEUS integrated into portable systems accelerates triage for trauma, stroke, and cardiac emergencies. Studies presented at RSNA 2024 showed 45-minute faster bleeding source identification compared with CT pathways in abdominal trauma cases.[3]Radiological Society of North America, “Contrast Ultrasound in Trauma,” rsna.org Vendors such as GE HealthCare have embedded AI tools into new point-of-care models, allowing generalists to obtain diagnostic-grade images rapidly, which reduces downstream imaging cascade and saves ICU resources.

Growing Investments by Government and Private Organizations

Capital projects and acquisitions are enlarging capacity and diversifying product lines. Bracco’s USD 90.1 million Hexagon facility in Geneva will triple global supply of ultrasound contrast vials, addressing earlier shortages. GE HealthCare’s USD 51 million purchase of Intelligent Ultrasound injects real-time AI analytics into its premium scanners, raising the competitive bar for workflow efficiency. Public research grants in China and the EU further underwrite translational trials that expand labeled indications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited pool of CEUS-trained sonographers | –1.5% | Emerging markets, rural North America & Europe | Medium term (2-4 years) |

| Regulatory delays for novel contrast agents | –0.8% | Highest in United States, moderate elsewhere | Long term (≥ 4 years) |

| High capital cost of premium systems | –0.7% | Asia, Africa, Latin America | Short term (≤ 2 years) |

| Adverse reaction & safety concerns | –0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Availability of CEUS-Trained Sonographers

A 2024 Journal of Diagnostic Medical Sonography survey found 42% of professionals cite inadequate training as the chief obstacle to CEUS deployment. Skill shortages lengthen exam scheduling and curb utilization, especially in smaller hospitals lacking structured mentorship. Large vendors now bundle e-learning modules with console purchases, yet adoption in emerging economies lags, constraining volume growth in regions that would benefit most from radiation-free imaging.

Stringent & Lengthy Regulatory Pathways for Novel Contrast Agents

Contrast agents are regulated as both pharmaceuticals and devices, extending approval timelines beyond 5 years in the United States. Although post-marketing surveillance shows strong safety records, targeted agents face extra scrutiny owing to biologic conjugates. These hurdles elevate development costs and discourage smaller entrants, slowing innovation velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Dominates but Agents Accelerate

In 2025, equipment generated 61.42% of revenue within the contrast enhanced ultrasound market. Hospitals prize multi-purpose premium consoles for their versatility across abdominal, cardiac, and obstetric imaging. The contrast enhanced ultrasound market size for equipment is projected to climb steadily alongside replacement cycles in North America and Europe. Meanwhile, contrast agents are expanding at 10.74% CAGR thanks to broader procedure counts and the approval of safer sulfur-hexafluoride microbubbles. Bracco’s Hexagon plant will remove historical supply bottlenecks and underpin double-digit shipment growth across Asia and Latin America. Innovation momentum is strongest in targeted agents that enable molecular imaging, an area attracting collaborative R&D between biotech firms and scanner OEMs.

Demand synergies are evident: every incremental console installation spurs recurring consumable sales, while new agents trigger software upgrades that differentiate vendors. Bundled service contracts that combine transducer warranties and agent purchasing agreements are creating stickier customer relationships. Emerging economies, however, still favor cost-effective mid-tier machines paired with generic microbubbles, hinting at a bifurcated purchasing landscape that challenges single-price global strategies.

By Technology: Targeted CEUS Emerges from Niche to Growth Engine

Non-targeted CEUS held 88.07% of revenue in 2025, anchored by broad regulatory clearance and established clinical protocols. The contrast enhanced ultrasound market size for non-targeted exams continues to rise, driven by cardiology and abdominal imaging volumes. Yet targeted CEUS is gaining traction as academic centers validate ligand-specific microbubbles for oncology and inflammation.

The segment’s 14.02% CAGR to 2031 reflects a pipeline of agents aimed at VEGF, integrins, and immune checkpoints. Early adopters in Europe are publishing encouraging results on drug-response monitoring, opening reimbursement discussions. Obstacles remain: longer regulatory reviews and interpretive complexity require tighter radiologist–clinician collaboration. Still, targeted imaging aligns with precision medicine trends, positioning the modality for outsized sampling in oncology trials and immune-therapy monitoring.

By Application: Cardiovascular Stable, Oncology Accelerating

Cardiovascular exams accounted for 40.64% revenue in 2025, supported by echo labs that rely on CEUS for endocardial border definition and myocardial perfusion. The contrast enhanced ultrasound market share for cardiology remains sizable as guideline revisions in 2025 recommend CEUS before nuclear studies in patients with suboptimal acoustic windows.

Oncology exhibits the sharpest trajectory, climbing 12.11% CAGR as microvascular characterization becomes pivotal in liver, renal, and breast tumor work-ups. CEUS accurately detects lesions under 2 cm with 88.9% accuracy, shrinking diagnostic delays. Additionally, CEUS guides ablation therapies and assesses early response, minimizing repeat CT scans. Hepatic and biliary uses remain core, while urology and obstetric applications are expanding through investigational studies that highlight safety in impaired renal function and pregnancy.

By End User: Hospitals Lead, Diagnostic Centers Gain Ground

Hospitals captured 69.03% of the contrast enhanced ultrasound market in 2025, leveraging consolidated budgets and multidisciplinary case mix. Academic hospitals pioneer new applications, securing research grants that finance high-end consoles. Nonetheless, diagnostic imaging centers show a 10.04% CAGR as outpatient volumes shift from inpatient settings.

Favorable reimbursement, shorter wait times, and increasing patient preference for community-based imaging drive this rise. The contrast enhanced ultrasound market size for independent centers in Asia could double by 2030 as governments encourage private participation to relieve public-sector loads. Ambulatory surgical centers adopt CEUS for immediate pre- and post-procedure evaluation, reinforcing the shift toward decentralized care.

Geography Analysis

North America commanded 36.88% revenue in 2025, supported by early FDA approvals and robust reimbursement. Numerous teaching hospitals lead CEUS guideline formulation, ensuring rapid diffusion into community practice. Canada’s inclusion of CEUS in national hepatocellular carcinoma pathways further cements leadership. Europe ranks second, with Germany and the United Kingdom emphasizing radiation-dose mitigation; the European Federation of Societies for Ultrasound in Medicine and Biology’s updated 2024 guidelines codify best practices and foster uniform quality across member states.

Asia delivers the highest growth at 9.41% CAGR. China’s Healthy China 2030 plan prioritizes advanced imaging, funneling subsidies toward provincial hospitals that adopt CEUS. Japan’s rapidly aging population drives cardiovascular and oncologic imaging, and local vendors introduce compact scanners tailored to clinic use. India remains nascent but exhibits strong potential as awareness grows and local distributors market competitively priced consoles.

Latin America and the Middle East & Africa trail in aggregate adoption, weighed by capital constraints and limited practitioner training. Multilateral development banks fund select pilot sites, hinting at gradual diffusion. Government partnerships with leading vendors could quicken momentum if bundled equipment-training packages lower entry barriers.

Competitive Landscape

The market is moderately concentrated. In the contrast-enhanced ultrasound market, global players maintain strong positions through diverse imaging portfolios and extensive service networks. Specialized firms lead in contrast-agent development, while regional manufacturers continue to expand their presence by capitalizing on local market strengths. GE HealthCare’s 2024 acquisition of Intelligent Ultrasound infuses real-time AI into its Versana and LOGIQ lines, differentiating workflows with automated border detection. Siemens’ Acuson Sequoia 3.5 integrates AI Abdomen packages that cut exam time by 20%.

Strategic alliances are intensifying. Samsung Medison’s 2024 MoU with Bracco pairs hardware innovation with consumable supply, promising bundled clinical solutions. Cost-focused Chinese manufacturers such as Mindray and SonoScape target rural markets with sub-USD 50,000 consoles, threatening incumbent share in price-sensitive segments. Companies are building competitive advantages through proprietary technologies, such as high-MI contrast modes and patented microbubble formulations. To address skill gaps among users, many also invest in training platforms for sonographers, helping strengthen customer loyalty and ecosystem integration.

Contrast Enhanced Ultrasound Industry Leaders

Siemens Healthineers AG

GE Healthcare

Bracco Diagnostic Inc.

Koninklijke Philips N.V.

Leriva Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: A new study by Canadian doctors highlights that contrast-enhanced ultrasound (CEUS) is a safe and accurate diagnostic imaging option for pregnant women who develop medical issues or suspicious tumors that would typically require contrast-enhanced CT or MRI scans.

- November 2024: Bracco, a global player in diagnostic imaging, has unveiled its state-of-the-art facility in Geneva, marking a significant milestone in advancing contrast-enhanced ultrasound (CEUS) technology. With an investment exceeding EUR 80 (USD 90.1) million, the new Hexagon building will triple the production capacity of Bracco’s innovative ultrasound contrast agents based on microbubble technology.

- July 2024: GE HealthCare has announced an agreement to acquire Intelligent Ultrasound Group PLC’s clinical artificial intelligence (AI) software business for approximately USD 51 million. Intelligent Ultrasound is recognized as a leader in integrated AI-driven image analysis tools that aim to make ultrasound smarter and more efficient. GE HealthCare plans to integrate these advanced AI solutions across its ultrasound portfolio, enhancing its technological capabilities to improve clinical workflows and ease of use. This strategic acquisition is expected to benefit both clinicians and patients by delivering more efficient, accurate, and user-friendly ultrasound imaging.

- July 2024: GE HealthCare has entered into an agreement to acquire Intelligent Ultrasound Group PLC’s clinical artificial intelligence (AI) software business for approximately USD 51 million. Intelligent Ultrasound specializes in integrated AI-driven image analysis tools that enhance ultrasound efficiency and intelligence. This acquisition will enable GE HealthCare to incorporate advanced AI solutions across its ultrasound portfolio, strengthening its technology to improve clinical workflows and ease of use, ultimately benefiting both clinicians and patients.

Global Contrast Enhanced Ultrasound Market Report Scope

As per the scope of the report, contrast-enhanced ultrasound (CEUS) involves the administration of intravenous contrast agents consisting of microbubbles/nanobubbles of gas to better visualize organs and blood vessels within the abdomen and pelvis.

The Contrast-Enhanced Ultrasound Market is segmented by Product Type (Equipment and Contrast Agents), Technology (Non-targeted and Targeted), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Equipment |

| Contrast Agents |

| Non-targeted CEUS |

| Targeted CEUS |

| Cardiovascular Imaging |

| Hepatic & Biliary Imaging |

| Renal & Urological Imaging |

| Obstetrics & Gynecology |

| Oncology & Tumor Characterisation |

| Others |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Equipment | |

| Contrast Agents | ||

| By Technology | Non-targeted CEUS | |

| Targeted CEUS | ||

| By Application | Cardiovascular Imaging | |

| Hepatic & Biliary Imaging | ||

| Renal & Urological Imaging | ||

| Obstetrics & Gynecology | ||

| Oncology & Tumor Characterisation | ||

| Others | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the contrast enhanced ultrasound market?

The market stands at USD 2.34 billion in 2026 and is projected to rise to USD 3.03 billion by 2031 at a 5.31% CAGR.

Which segment is growing fastest within the contrast enhanced ultrasound market?

Oncology applications are expanding the quickest, registering a 12.11% CAGR through 2031 as CEUS gains prominence in tumor detection and therapy monitoring.

Why are contrast agents expected to outpace equipment sales?

New microbubble formulations tailored to specific clinical tasks, coupled with rising procedure volumes, propel contrast-agent revenue at an 10.74% CAGR compared with more modest equipment replacement growth.

Which region shows the highest growth potential?

Asia Pacific is projected to achieve a robust 9.41% CAGR, bolstered by healthcare infrastructure upgrades and higher chronic disease prevalence in China and Japan.

What are the main hurdles restraining market expansion?

A shortage of CEUS-trained sonographers, stringent regulatory reviews for novel agents, and high capital costs for premium consoles collectively temper adoption, particularly in emerging economies.

How does CEUS benefit pediatric and pregnant populations compared with CT or MRI?

CEUS delivers diagnostic-grade imaging without ionizing radiation or nephrotoxic contrast, offering a safer alternative that aligns with radiation-dose reduction mandates for vulnerable groups.

Page last updated on: