Indonesia Insecticide Market Size and Share

Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.64 Billion |

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 2.28 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Insecticide Market Analysis by Mordor Intelligence

The Indonesia insecticide market size was valued at USD 1.64 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 2.28 billion by 2031, at a CAGR of 5.68% during the forecast period (2026-2031). A steady shift toward climate-resilient cultivation, the government’s Rp 124.4 trillion (USD 8.2 billion) input-subsidy overhaul, and rising pest pressure in rice and vegetable belts continue to underpin demand for premium formulations. Producers on Java and Sumatra are prioritizing dual-mode pyrethroid-neonic blends that tackle brown planthopper resistance and fall armyworm migration, while food-safety regulations have quickened the pivot to ultra-low-residue products for export-oriented horticulture. Multinational suppliers have reinforced their positions through localized manufacturing and distribution alliances, whereas smaller domestic firms face higher compliance costs and tighter registration timelines. Across the archipelago, precision application technologies, greenhouse expansion, and integrated pest-management (IPM) mandates are reshaping purchase decisions, keeping the Indonesia insecticide market on a durable growth path.

Key Report Takeaways

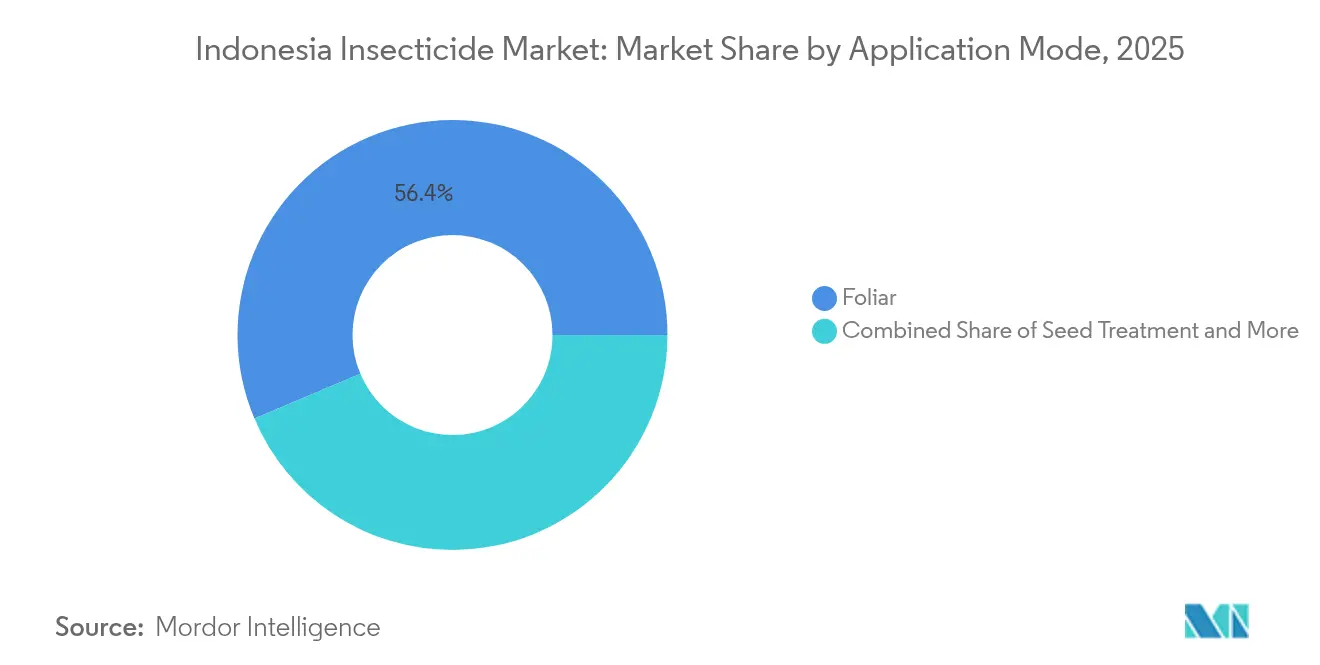

- By application mode, foliar sprays commanded 56.35% of the Indonesia insecticide market share in 2025, while seed treatment is projected to post the highest growth at a 5.78% CAGR to 2031.

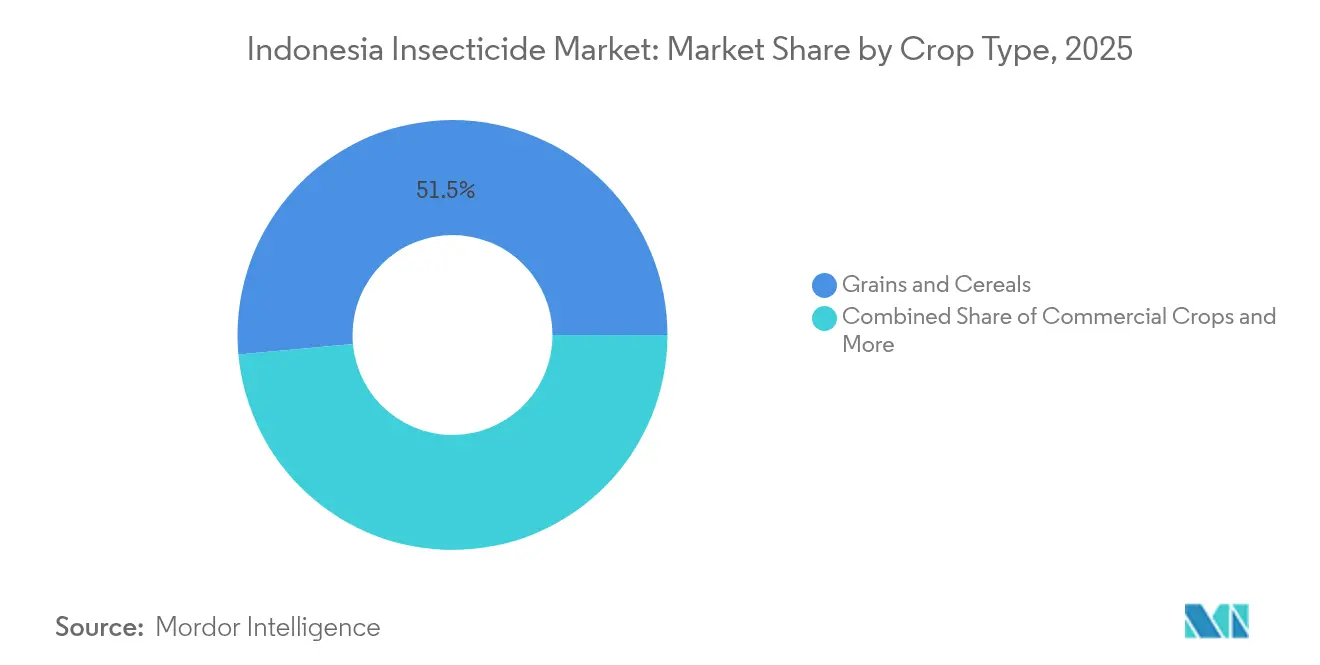

- By crop type, grains and cereals contributed 51.45% of the Indonesia insecticide market share in 2025, while Fruits and vegetables are poised to expand at a 5.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Insecticide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying rice-pest pressure in irrigated Java | +1.2% | Java rice zones, spillover into Sumatra | Medium term (2-4 years) |

| Government fertilizer and pesticide subsidy reform boosting input affordability | +0.8% | Nationwide, early gains in Java, Sumatra, Kalimantan | Short term (≤ 2 years) |

| Rapid expansion of protective-cultivation vegetable acreage | +0.6% | Java highlands, Sumatra commercial districts | Medium term (2-4 years) |

| Multinational launches of dual-mode pyrethroid-neonic blends tailored for tropical pests | +0.4% | National distributor networks | Short term (≤ 2 years) |

| Climate-driven spike in fall-armyworm migration into Sumatra and Kalimantan | +0.5% | Sumatra and Kalimantan expansion zones | Long term (≥ 4 years) |

| Emerging palm-pollinator stewardship programs mandating ultra-low-residue formulations | +0.3% | Sumatra and Kalimantan oil-palm estates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Rice-Pest Pressure in Irrigated Java

Java’s 3.2 million hectares of irrigated paddy recorded a 23% jump in pest-affected area in 2024, as brown planthopper populations gained resistance to standalone pyrethroids. Farmers have therefore adopted dual-mode pyrethroid-neonicotinoid mixtures that maintain efficacy and reduce repeat sprays. Without timely control, yield losses can reach 40-60%, so the willingness to pay for premium products remains high. Remote-sensing surveillance under the Ministry of Agriculture’s SISCrop 2.0 program now guides spray timing, cutting per-hectare volumes without compromising protection. Because Java supplies 55% of the national rice, innovations piloted here rapidly migrate to Sumatra and Kalimantan.

Government Fertilizer and Pesticide Subsidy Reform Boosting Input Affordability

The 2024 shift from blanket aid to farmer-verified subsidies has redirected Rp 124.4 trillion (USD 8.2 billion) toward certified growers, lifting purchasing power for legitimate pesticides.[1]Source: Badan Pusat Statistik, “Analisis Komoditas Ekspor, 2019-2023,” bps.go.id Java achieved 78% enrollment, versus 45% in eastern islands, widening regional uptake gaps yet curbing counterfeit flow in enrolled districts. Multinationals have benefited from required distributor registrations, whereas smaller firms must upgrade quality systems or exit. Subsidy rules bundle IPM training, nudging growers to reserve broad-spectrum sprays for threshold breaches and to trial biologicals where feasible.

Rapid Expansion of Protected-Cultivation Vegetable Acreage

Greenhouse and net-house acreage has risen 34% annually since 2024, especially for chili, tomato, and leafy greens destined for Singapore and Malaysia. These controlled environments favor drip chemigation and low-volume electrostatic misting that together trim total active-ingredient loads. Because foreign buyers impose residue limits that sit 50-70% below domestic maximums, demand has surged for selective molecules and microbial insecticides that pass strict testing. Government cost-sharing on greenhouse structures further accelerates adoption among mid-size operators transitioning from open-field plots.

Multinational Launches of Dual-Mode Pyrethroid-Neonic Blends Tailored for Tropical Pests

Syngenta’s 2024 alliance with Provivi to deploy pheromone-inclusive blends typifies the alignment of chemical and biological controls aimed at resistance mitigation.[2]Source: Syngenta, “Syngenta Biologicals and Provivi Partner on Pheromone Solutions,” syngenta.com New combinations show 15-25% price premiums yet deliver longer residual activity against brown planthopper, fall armyworm, and diamond-back moth. Temperature-stable adjuvants ensure droplet retention in high-humidity conditions. Commercial rice estates and export-oriented vegetable farms—where yield loss penalties outweigh extra costs—are early adopters. Accelerated National Food Agency review pathways for resistance-breakers have trimmed approval to 12 months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter 2024 NFA residue-testing rule raising compliance costs | −0.7% | National, export-oriented regions | Short term (≤ 2 years) |

| Accelerating insecticide resistance in brown planthopper and diamond-back moth | −0.5% | Java rice belts, national vegetables | Medium term (2-4 years) |

| Increasing counterfeit pesticide circulation in tier-2 districts | −0.4% | Remote Sumatra, Kalimantan, east islands | Long term (≥ 4 years) |

| Slow commercialization pathway for botanical actives due to registration fees | −0.3% | Nationwide, domestic manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter 2024 NFA Residue-Testing Rule Raising Compliance Costs

Permentan 43/2019 amendments now require third-party lab verification for every imported or domestically produced insecticide, adding USD 15,000-25,000 to annual distributor budgets[3]Source: Badan Pusat Statistik, “Statistik Lingkungan Hidup Indonesia 2024,” bps.go.id. Product launches face three-to-six-month delays while samples clear capacity-constrained labs. Medium-size firms pass costs onto farmers, lifting shelf prices 8-12% and nudging price-sensitive growers toward unregistered alternatives. Export-focused vegetable clusters carry the heaviest burden because they must meet dual standards. Over time, however, compliant suppliers gain clearer shelf space as non-conforming brands exit.

Accelerating Insecticide Resistance in Brown Planthopper and Diamond-Back Moth

Field assays in 2024 showed 40-60% efficacy slippage for legacy pyrethroids in Java rice belts and Bacillus thuringiensis tolerance in crucifer plots. Farmers respond with higher doses and shorter spray intervals, raising per-hectare costs and environmental load. Although multinationals invest in new modes of action, approval cycles of 18-24 months leave interim gaps. Extension-officer promotion of rotation schemes and refugia adoption gains limited traction because of complexity and input costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Mode: Foliar Dominance Drives Precision Adoption

Foliar sprays accounted for 56.35% of the Indonesia insecticide market share in 2025, underscoring a long-standing reliance on knapsack and motorized sprayers across rice, vegetable, and plantation systems. The Indonesia insecticide market size for foliar products is projected to track overall industry expansion due to ongoing pest pressure in irrigated valleys. Growers value immediate knockdown capability and crop-stage flexibility, especially in multi-cycle rice, where turnaround time between harvest and replanting is short. SISCrop 2.0 threshold alerts have started to smooth demand seasonality, with some districts reporting 15-20% spray-volume savings.

Seed treatment, though presently at 8.92% sales, is heading toward a 5.78% CAGR through 2031 as precision planters and treated hybrid seed adoption accelerate. Multinationals bundle polymer coatings with systemic actives that protect seedlings during the vulnerable two-week window, enabling farmers to delay first foliar sprays. Soil treatment is largely retained in Java rice zones where granular carbamates and phenylpyrazoles target root-feeding insects. Chemigation remains niche because many fields still rely on surface irrigation, yet greenhouse vegetable operators in Java highlands have standardized drip lines that accommodate water-soluble insecticides. Fumigation serves high-value fruit-fly management in enclosed packhouses and seed warehouses.

By Crop Type: Grains and Cereals Lead Traditional Markets

Grains and cereals held 51.45% of the Indonesia insecticide market share in 2025, reflecting rice’s primacy in food security and its triple-cropping pattern that intensifies pest exposure. The Indonesia insecticide market size for this crop group will continue to rise steadily, helped by subsidy‐backed access to premium chemistries. Farmers integrate systemic seed dressings, vegetative-stage foliar sprays, and ratoon crop soil drenches to safeguard yields.

Fruits and vegetables, though smaller at 18.60%, exhibit the quickest growth at 5.74% CAGR through 2031. Export hubs facing stringent residue caps demand low-dose actives and biological agents, spurring suppliers to introduce shorter pre-harvest-interval products. Commercial crops such as oil palm and rubber occupy a 21.90% slice, with estates embedding IPM and pollinator conservation. Pulses and oilseeds hold a 6.10% share, supported by dry-season soybean rotations in Java. Turf and ornamentals, at 1.95%, ride urban landscaping and tourism sector growth, yet require specialized packaging and service models tailored to professional applicators.

Geography Analysis

Java absorbed a significant share of Indonesia's insecticide market revenues in 2024, anchored by intensive rice and vegetable systems and the country’s densest distributor network. Tight land availability pushes yield maximization, so growers gravitate toward premium formulations and precision application tech. Java, facilitated by Ministry of Agriculture grants for drone spraying and smart traps.

Sumatra ranked second with a significant share in 2024. Large oil-palm estates enforce RSPO residue limits that favor ultra-low-residue actives. Commercial rice schemes in South Sumatra and Lampung add volume, while greenhouse projects aim at the Singapore markets. Sumatra outpaces Java as frontier districts open new farmland and employ mechanized spreaders through contract service models.

Kalimantan is buoyed by government food-estate ventures converting degraded forest to structured rice and vegetable blocks. Expansion necessitates reliable supply chains and training for newly settled farmers.

Eastern provinces—Sulawesi, Papua, and the Lesser Sundas—jointly contributed a significant share with a limited port infrastructure and counterfeit influx constraining growth, yet improved roads and digital extension platforms are closing the gap. NFA residue rules have lengthened product-approval lead times here, creating a lag of two planting seasons compared with Java.

Competitive Landscape

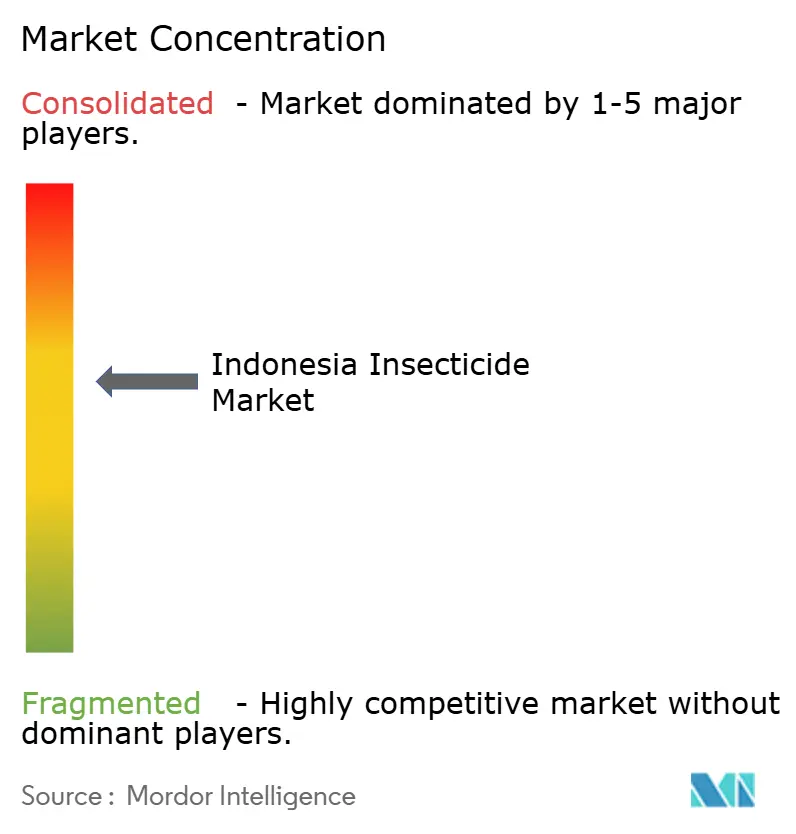

Syngenta Group, Bayer AG, UPL Limited, BASF SE, and FMC Corporation collectively captured a significant share of 2024 sales, giving the Indonesia insecticide market a moderately concentrated profile. Their edge stems from climate-adapted formulations, multilayered distributor alliances, and dedicated regulatory-affairs teams that navigate NFA protocols. Local firms such as PT Petrokimia Gresik and PT Agricon compete on generic labels and region-specific brands, but mounting registration fees and residue-testing costs strain margins.

Strategic thrusts revolve around integrated portfolios that bundle chemical, biological, and digital tools. Syngenta and Provivi’s pheromone-combination launch illustrates the move toward target-specific products that minimize non-target exposure. Bayer’s digital scouting app, piloted in East Java, links pest-density alerts with variable-rate drone spraying services operated by local cooperatives. Corteva’s treated-seed channel leverages its maize franchise to cross-sell systemic soil insecticides.

Competitive intensity also plays out in training initiatives. Multinationals sponsor IPM field schools, raising product stewardship while securing brand loyalty. Domestic challengers retaliate with smaller pack sizes and credit terms attractive to village retailers. Nonetheless, the regulatory barrier favors firms able to document entire supply chains, a trend likely to hasten consolidation.

Indonesia Insecticide Industry Leaders

Bayer AG

FMC Corporation

Syngenta Group

UPL Limited

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: In Q2 2025, Pangaea Biosciences introduced Booster, an insecticide enhancer that overcomes pest resistance, in Indonesia. The product, distributed by PT Bulindo Agro Teknologi, targets primary pests affecting rice, shallots, and vegetables.

- May 2023: BASF introduced Cimegra insecticide in Indonesia to control rice pests, including brown planthopper and rice stem borer. The product features a new mode of action and minimal environmental impact, supporting sustainable agricultural practices.

Indonesia Insecticide Market Report Scope

Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Insecticides are chemicals used to control or prevent insects from damaging the crop and prevent yield loss.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms