Anticoagulant Rodenticides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anticoagulant Rodenticides Market Analysis by Mordor Intelligence

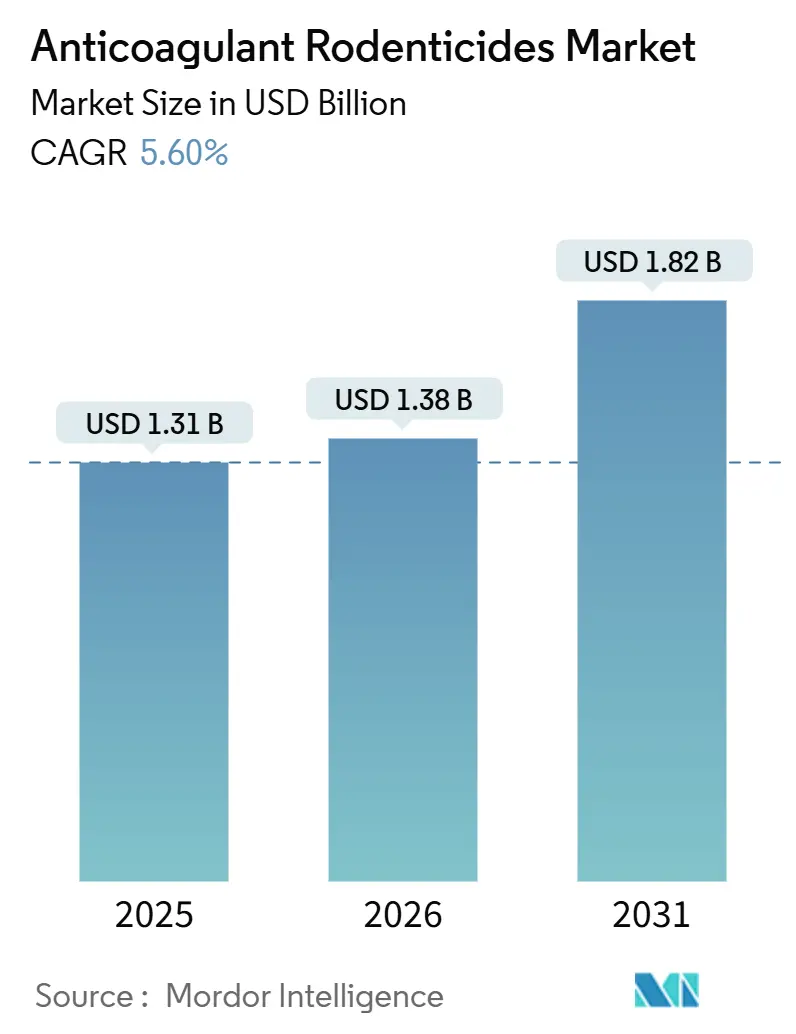

The anticoagulant rodenticides market size is projected to grow from USD 1.31 billion in 2025 to USD 1.38 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at 5.60% CAGR over 2026-2031. Warmer winters that lengthen rodent breeding seasons, and professionalization of pest-management services, are together expanding the addressable pool of commercial buyers. Uptake is strongest for second-generation actives because they deliver a lethal dose in a single feeding, offsetting widespread resistance to first-generation compounds. Digital telemetry embedded in bait stations is reducing service labor while providing auditable compliance data, thereby supporting premium pricing strategies. At the same time, shifting maximum residue limits and community campaigns against raptor poisoning are prompting regional product reformulations, rewarding suppliers with global regulatory expertise.

Key Report Takeaways

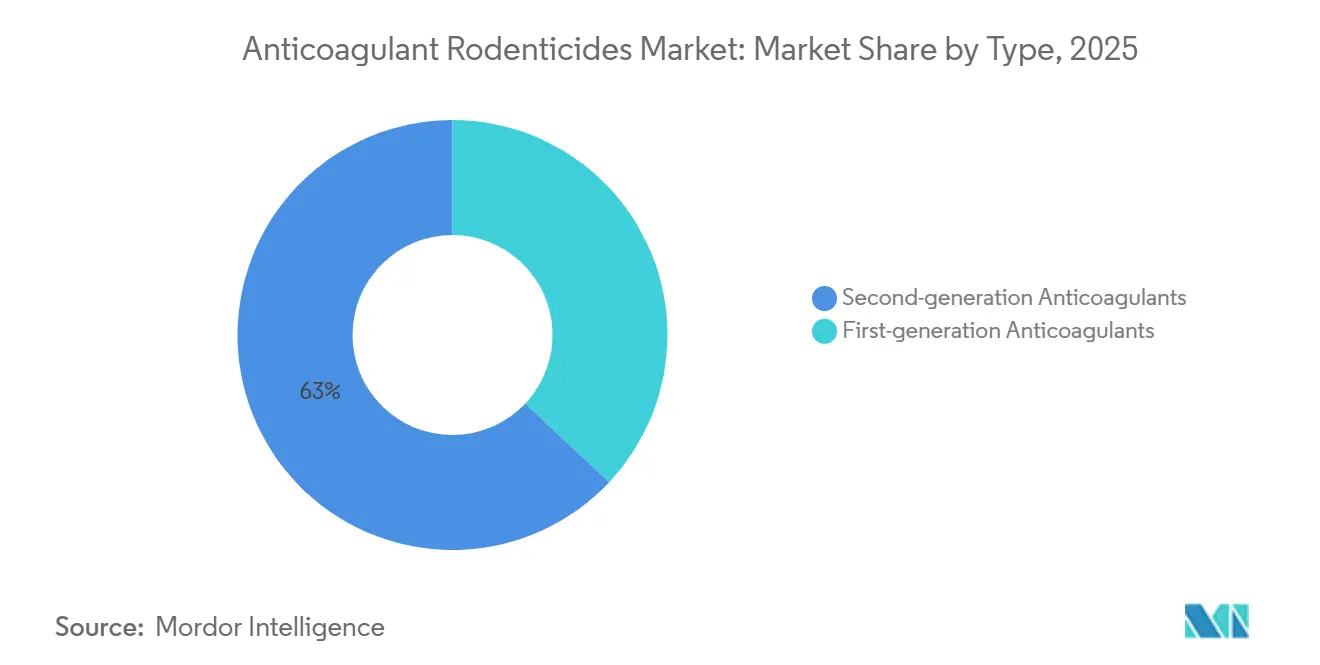

- By type, second-generation anticoagulants hold the largest segment, capturing 63% of the anticoagulant rodenticides market share in 2025, while the fastest-growing segment is projected to grow at 8.8% CAGR through 2026-2031.

- By formulation, pellets hold the largest segment, accounting for 41% of the anticoagulant rodenticides market share in 2025, and blocks are the fastest-growing segment, projected to grow at a 9.4% CAGR between 2026 and 2031.

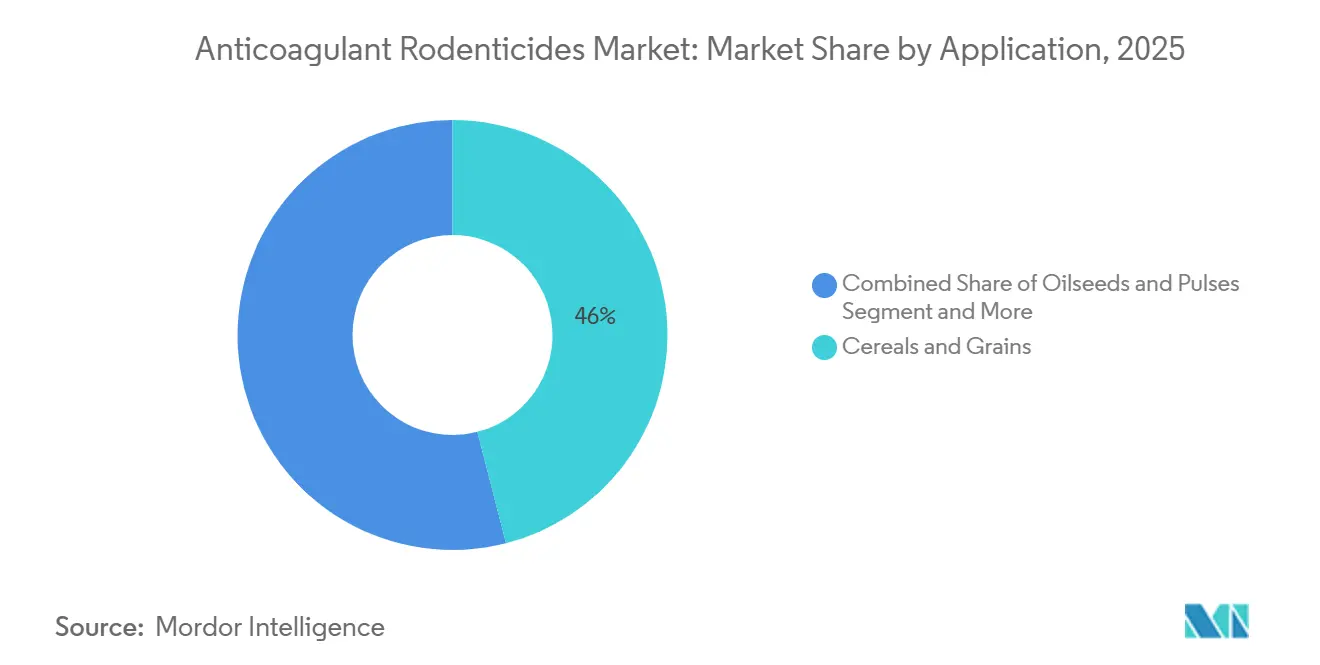

- By application, cereals and grains hold the largest share, accounting for 46% of the anticoagulant rodenticides market in 2025, while oilseeds and pulses represent the fastest-growing segment, projected to grow at a 7.9% CAGR through 2026-2031.

- By distribution channel, the direct distribution channel held 57% of the anticoagulant rodenticides market in 2025, while online platforms are forecast to grow at a 10.1% CAGR from 2026 to 2031.

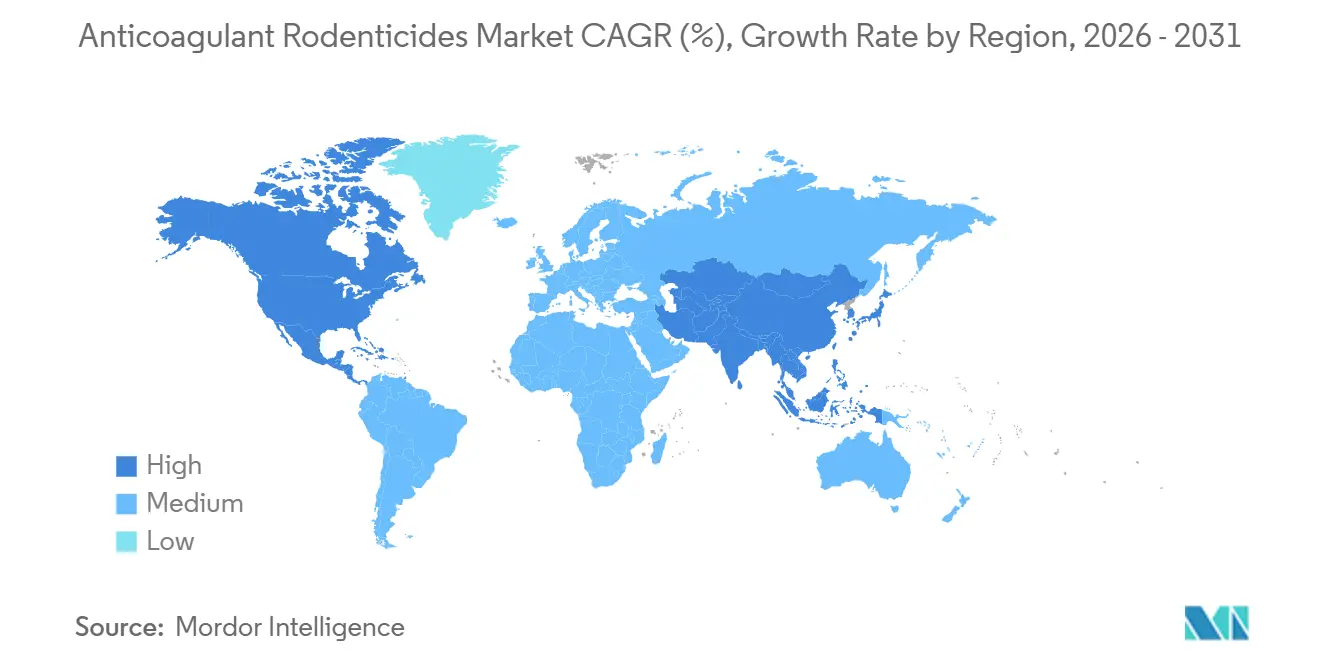

- By geography, North America accounted for the largest share of the anticoagulant rodenticides market, representing 38% in 2025. Meanwhile, the Asia-Pacific region is the fastest-growing market, with a projected CAGR of 8.5% during the period 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anticoagulant Rodenticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing focus on post-harvest loss prevention in agricultural storage | +1.2% | North America and the European Union are spreading worldwide | Medium term (2-4 years) |

| Climate-linked rodent population surges in temperate grain belts | +1.4% | Temperate grain belts on all inhabited continents | Long term (≥ 4 years) |

| Consolidation of farm-management service providers | +0.8% | North America, Europe, and emerging in the Asia-Pacific region | Medium term (2-4 years) |

| Internet of Things (IoT)-enabled bait-station telemetry adoption | +0.6% | North America, Europe, and pilot projects in the Asia-Pacific | Short term (≤ 2 years) |

| Gene-edited cereal cultivars increasing rodent palatability | +0.3% | China and India, and with selective trials in the United States | Long term (≥ 4 years) |

| Environmental, Social, and Governance (ESG) Guidelines set by asset owners for managing vertebrate pest welfare | +0.2% | Europe and North America's institutional capital networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Focus on Post-Harvest Loss Prevention in Agricultural Storage

The growing emphasis on minimizing post-harvest losses in agriculture is a significant driver for the anticoagulant rodenticides market. Rodent infestations in grain storage facilities, silos, and farm warehouses result in substantial quantitative and qualitative losses of cereals, pulses, and oilseeds, adversely affecting farmer profitability and national food security. As agricultural production scales up, safeguarding harvested crops during storage has become a critical operational priority. Large-scale grain handling systems are increasingly adopting structured rodent management programs to reduce spoilage, contamination, and infrastructure damage. Anticoagulant rodenticides are commonly employed in perimeter baiting and internal storage protection strategies due to their proven effectiveness in controlling persistent rodent populations in enclosed environments. Their ability to achieve sustained population reduction helps break recurring infestation cycles, thereby mitigating long-term storage losses.

Climate-Linked Rodent Population Surges in Temperate Grain Belts

Warmer winters are extending breeding windows, so rat colonies reach peak numbers earlier in the agricultural calendar. Multiyear studies confirm that Mus and Rattus genera are expanding their geographic ranges toward higher latitudes under shared socioeconomic pathway climate scenarios. When rodent pressure escalates inside storage facilities, operators shift from first-generation to single-feed second-generation actives to curb damage rapidly. Climate amplification, therefore, enlarges the total quantity of bait deployed and reduces waiting time between replenishment cycles, directly expanding the Anticoagulant Rodenticides Market demand in cereal-growing nations.

Internet of Things (IoT)-Enabled Bait-Station Telemetry Adoption

Internet of Things (IoT)-enabled bait-station telemetry is a significant driver of growth in the anticoagulant rodenticides market, particularly in commercial agriculture and large-scale food storage systems. These advanced bait stations utilize sensors, connectivity, and data analytics to monitor rodent activity, bait consumption, and station status in real time. This allows for more precise and efficient use of anticoagulant rodenticides. This trend is prompting manufacturers to focus on developing advanced formulations and forming partnerships with digital pest management platforms, which is driving market growth and encouraging innovation in the anticoagulant rodenticides market.

Environmental, Social, and Governance (ESG) Guidelines Set by Asset Owners for Managing Vertebrate Pest Welfare

European pension funds and North American endowments now include humane kill criteria in supply-chain audits. Single-feed second-generation actives and fast-acting non-anticoagulant alternatives score higher than multi-feed warfarin products due to shorter time to death. Manufacturers publicize single-feed efficacy as a Social, Governance(ESG) feature, aligning with asset-owner scorecards and nudging corporate grain buyers toward premium formulations. Though the impact on global volumes is modest, it strengthens margins and signals a long-term shift away from first-generation chemistry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for bio-secure food supply chains | -1.1% | Europe and North America's urban areas, emerging Asia-Pacific hubs | Short term (≤ 2 years) |

| Stricter residue limits in export commodity contracts | -0.9% | Major grain exporters in the Asia-Pacific and South America | Medium term (2-4 years) |

| Community-led bans after raptor secondary-poisoning events | -0.7% | North America, Europe, and Australia | Short term (≤ 2 years) |

| Volatile vitamin K antidote precursor pricing | -0.3% | Global supply chains centered in East Asia synthesis clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Bio-Secure Food Supply Chains

The increasing regulatory focus on ensuring bio-secure food supply chains is a key driver for the anticoagulant rodenticides market. Strict food safety standards enforced by regulatory authorities in major agricultural economies require effective rodent control measures across the value chain, including pre-harvest, storage, and distribution stages. The United States Environmental Protection Agency requires baiting records and carcass searches in endangered-species zones, forcing operators to adopt tamper-resistant stations that automatically log sensor data[1]Source: United States Environmental Protection Agency, “Rodenticide Strategy,” epa.gov. Australia has restricted consumer access to second-generation products and insists on the use of dyes and bittering agents, effectively professionalizing sales channels.

Volatile Vitamin K Antidote Precursor Pricing

Price volatility of vitamin K antidote precursors significantly impacts cost and risk management in the anticoagulant rodenticides market, particularly in agriculture-focused applications such as grain storage, silos, and field-edge pest control. Anticoagulant rodenticides work by disrupting blood clotting and are primarily used for rodent control in crop protection systems. However, regulatory and operational protocols in agricultural settings necessitate preparedness for unintended exposure that could affect non-target ecological components, such as beneficial wildlife near storage sites. This reliance on vitamin K as a mitigation measure is integral to integrated pest management frameworks. Factors such as agricultural variability, export concentration, and geopolitical conditions in sourcing regions periodically constrain supply, resulting in cost increases and procurement challenges. For instance, the vitamin K injection shortage reported by the American Society of Health-System Pharmacists underscored disruptions in precursor availability, which can lead to downstream supply limitations[2]Source: American Society of Health-System Pharmacists, “Vitamin K Injection Shortage,” ashp.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Second-Generation Dominance Amid Resistance Pressures

Second-generation anticoagulants hold the largest segment, capturing 63% of the anticoagulant rodenticides market share in 2025, while the fastest-growing segment is with an 8.8% CAGR through 2026-2031. This dominance is primarily due to their high efficacy and single-feed lethality, which enable them to control resistant rodent populations across agricultural fields, storage facilities, and urban environments. Their widespread adoption is driven by demand for rapid, reliable pest control solutions, particularly in large-scale, high-risk applications such as grain storage and food processing.

The first-generation anticoagulants market is largely driven by increasing regulatory restrictions on second-generation compounds due to concerns about environmental and secondary poisoning risks. Consequently, there is a shift toward safer, lower-toxicity alternatives, particularly in regions with stringent regulatory frameworks. First-generation anticoagulants are gaining popularity within integrated pest management (IPM) programs, where repeated, controlled dosing is preferred to reduce ecological impact. This trend highlights a broader market transition in which efficacy remains essential, but sustainability and regulatory compliance are becoming equally significant in shaping product demand.

By Formulation: Pellets Lead Despite Block Innovation

Pellets hold the largest segment, accounting for 41% of the anticoagulant rodenticides market share in 2025. Their widespread use is attributed to their ease of application, cost-effectiveness, and suitability for large-scale agricultural operations, particularly in open fields and broadcast applications where rapid deployment is critical. Farmers and pest control operators prefer pellets for their flexibility in covering extensive areas and their effectiveness in targeting a wide range of rodent species.

The blocks segment is the fastest-growing segment, projected to grow at a 9.4% CAGR between 2026 and 2031. This growth is driven by their durability, resistance to weather conditions, and compatibility with bait stations, particularly in controlled environments such as warehouses, food processing units, and storage facilities. Blocks are less susceptible to disintegration in moist or harsh conditions and provide longer-lasting efficacy, making them well-suited for compliance with stringent food safety regulations. As the market increasingly adopts structured, monitored pest control solutions, including IoT-enabled bait stations, demand for block formulations is projected to grow significantly.

By Distribution Channel: Direct Sales Maintain Dominance

The direct distribution channel holds the largest segment, accounting for 57% of the anticoagulant rodenticides market size in 2025. This dominance is attributed to strong relationships between manufacturers and large-scale end users, including commercial farms, grain storage operators, and pest control service providers. Direct sales channels facilitate bulk purchasing, offer customized solutions, provide technical support, and ensure competitive pricing, making them the preferred option for institutional buyers and agribusinesses that require consistent, large-volume supplies.

Online platforms are the fastest-growing segment, forecast to post the highest 10.1% CAGR through 2026-2031. The growth of e-commerce in the agricultural inputs sector, increasing digital adoption among farmers, and the convenience of product comparison and doorstep delivery are key drivers of this trend. Furthermore, online channels offer access to a broader range of products, including specialized and niche formulations that may not be readily available through traditional distribution networks. As digitalization continues to transform agricultural supply chains, online platforms are projected to play an increasingly significant role in expanding market access, particularly for small and medium-scale farmers.

By Application: Staples Lead, High-Value Horticulture Grows Faster

Cereals and grains hold the largest segment, accounting for 46% of the anticoagulant rodenticides market size in 2025. This significant share is primarily due to the high susceptibility of staple crops such as wheat, rice, and maize to rodent infestations during cultivation and storage. The combination of substantial economic losses and stringent food safety and storage regulations continues to drive the demand for effective rodent control solutions in this application segment.

The oilseeds and pulses represent the fastest-growing segment, projected at 7.9% CAGR through 2026-2031. This growth is attributed to the rising global demand for protein-rich crops, the expansion of oilseed cultivation, and advancements in storage infrastructure. These crops are also highly vulnerable to rodent damage, particularly during post-harvest storage, necessitating efficient pest management solutions. Furthermore, increasing awareness of crop protection and the importance of reducing post-harvest losses is bolstering the adoption of anticoagulant rodenticides in this segment.

Geography Analysis

North America held the largest region, accounting for 38% of the anticoagulant rodenticides market size in 2025. This dominance is attributed to the region's well-established agricultural and food storage industries, food safety regulations, and widespread adoption of modern pest management practices. Additionally, high awareness of post-harvest losses and the presence of major rodenticide manufacturers further strengthen North America’s position as the leading market. For instance, in the United States Midwest, grain elevators in Iowa and Illinois have increased the use of second-generation anticoagulant rodenticides during the storage season to control rising rodent infestations and prevent grain losses, supporting consistent market demand.

Asia-Pacific is the fastest-growing region, projected to grow at a 8.5% CAGR between 2026 and 2031. This growth is driven by the expansion of large-scale farming, increased investments in grain storage and processing infrastructure, and rising awareness of crop protection and food security. Furthermore, the growing population and increasing demand for staple and high-value crops are driving the adoption of anticoagulant rodenticides across emerging economies in the Asia-Pacific region, positioning the region as a critical growth area for the market. Australia’s one-year consumer suspension channels demand into licensed firms rather than eliminating it, sustaining volumes while improving data capture.

Europe benefits from an extensive grain storage infrastructure and well-established professional pest management networks. The implementation of stricter stewardship schemes and proof-of-competence requirements, along with ongoing hardware upgrades, helps vendors maintain profit margins. The prevalence of resistance has led to a shift toward flocoumafen and non-anticoagulant products, creating opportunities for reformulation. In Africa and the Middle East, the market is expanding as governments implement modern silos to reduce post-harvest losses and enhance food security.

Competitive Landscape

The anticoagulant rodenticides market displays moderate concentration in 2025, with the top five players including BASF SE, Bayer AG, Syngenta Group, UPL Limited, and De Sangosse SAS. Syngenta Group licensed its Talon brodifacoum brands to Neogen in May 2025, allowing Syngenta to reallocate research budgets toward next-generation chemistries while Neogen deepens professional channel ties[3]Source: Neogen Corporation, “Talon Licensing Agreement,” neogen.com.

Midsize challengers exploit local resistance profiles and supply-chain flexibility, particularly in Asia-Pacific, where tailored flavors and pack sizes drive market share gains. The rising regulatory costs and Environmental, Social, and Governance (ESG) reporting standards tilt the competitive advantage toward diversified multinationals with the capital to navigate evolving compliance and R&D demands in the anticoagulant rodenticides market.

Regulatory mastery is becoming a durable moat; companies that fund field-residue trials and provide bilingual stewardship training earn preferential listings in distributor catalogs. Those without dedicated regulatory teams struggle to keep pace with divergent national rules on bait-station design, dye use, and outdoor placement restrictions. Given these dynamics, competitive positioning hinges on three pillars: proprietary actives, digital monitoring ecosystems, and cross-border compliance infrastructure.

Anticoagulant Rodenticides Industry Leaders

BASF SE

Bayer AG

UPL Limited

Syngenta Group

De Sangosse SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: BASF SE relaunched its popular rodenticide brand, Neosorexa, featuring an improved active ingredient, flocoumafen. This update aims to provide pest control technicians with fast and effective solutions for managing house mice (Mus musculus), black rats (Rattus rattus), and brown rats (Rattus norvegicus).

- June 2024: The European Union extended approval timelines for several rodenticide active ingredients, postponing their expiry dates while comprehensive environmental reassessments are conducted. This extension was triggered by ongoing evaluations around the environmental and health risks associated with anticoagulant rodenticides.

- May 2024: Syngenta Group collaborated with a prominent North American pest control association to offer certified training programs on safe and effective rodenticide application techniques for professional exterminators.

Global Anticoagulant Rodenticides Market Report Scope

Anticoagulant rodenticides are chemical pest control agents used in agricultural systems to manage rodent populations that threaten crops and stored grains. The anticoagulant rodenticides market report is segmented by type (first-generation anticoagulants and second-generation anticoagulants), by formulation (pellets, blocks, powders, and liquids), by application (cereals and grains, oilseeds and pulses, fruits and vegetables, and other applications), by distribution channel (direct, agro-chemical retailers, online platforms), by geography (North America, Europe, South America, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| First-generation anticoagulants |

| Second-generation anticoagulants |

| Pellets |

| Blocks |

| Powders |

| Liquids |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Other Applications |

| Direct (Manufacturers to Co-operatives) |

| Agro-chemical Retailers |

| Online Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Type | First-generation anticoagulants | |

| Second-generation anticoagulants | ||

| By Formulation | Pellets | |

| Blocks | ||

| Powders | ||

| Liquids | ||

| By Application | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Other Applications | ||

| By Distribution Channel | Direct (Manufacturers to Co-operatives) | |

| Agro-chemical Retailers | ||

| Online Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Anticoagulant Rodenticides Market?

The Anticoagulant Rodenticides Market size is projected to grow from USD 1.31 billion in 2025 to USD 1.38 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at 5.6% CAGR over 2026-2031

Which region holds the largest share in 2025?

North America leads with 38% revenue share due to extensive grain infrastructure and established stewardship programs.

Why are second-generation anticoagulants growing faster than first-generation products?

Multi-species resistance genes have reduced first-generation efficacy, pushing growers toward more potent second-generation options that still meet residue limits.

How is climate change influencing demand?

Warmer temperatures and altered predator dynamics are driving rodent population surges, leading to year-round baiting and higher overall consumption.

What technologies are reshaping the market?

IoT-enabled bait-station telemetry and genome-based resistance diagnostics allow precision dosing and targeted active-ingredient rotation, lowering waste and improving compliance.

Page last updated on: