Candles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

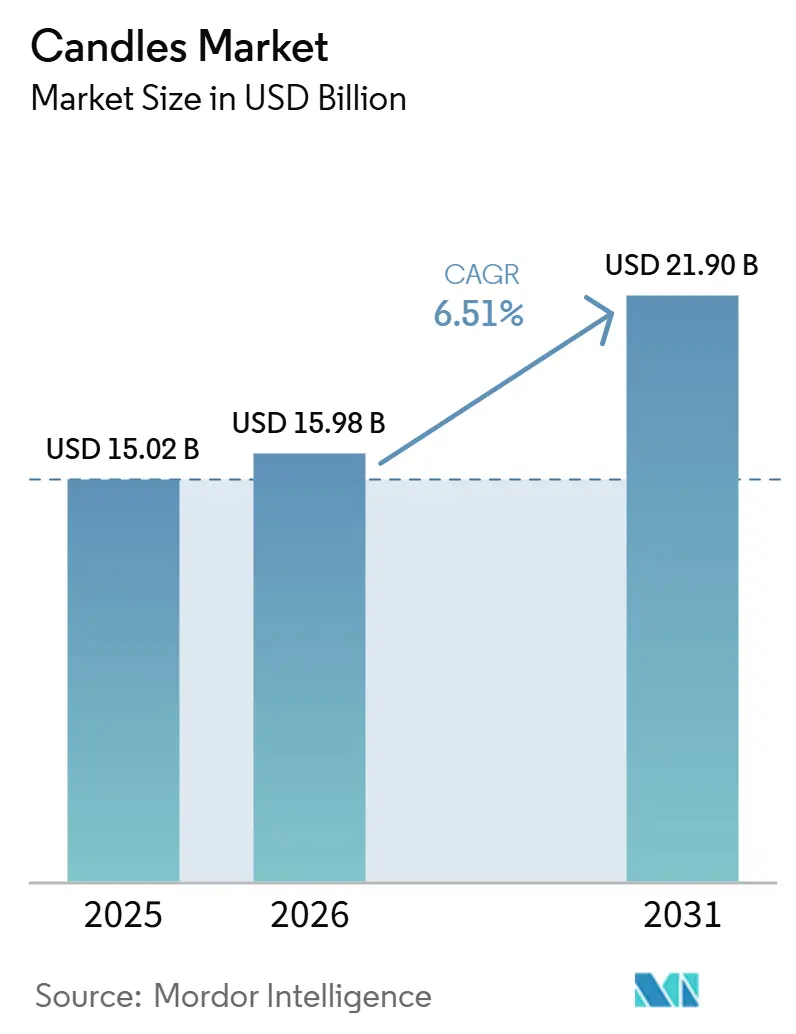

| Market Size (2026) | USD 15.98 Billion |

| Market Size (2031) | USD 21.90 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

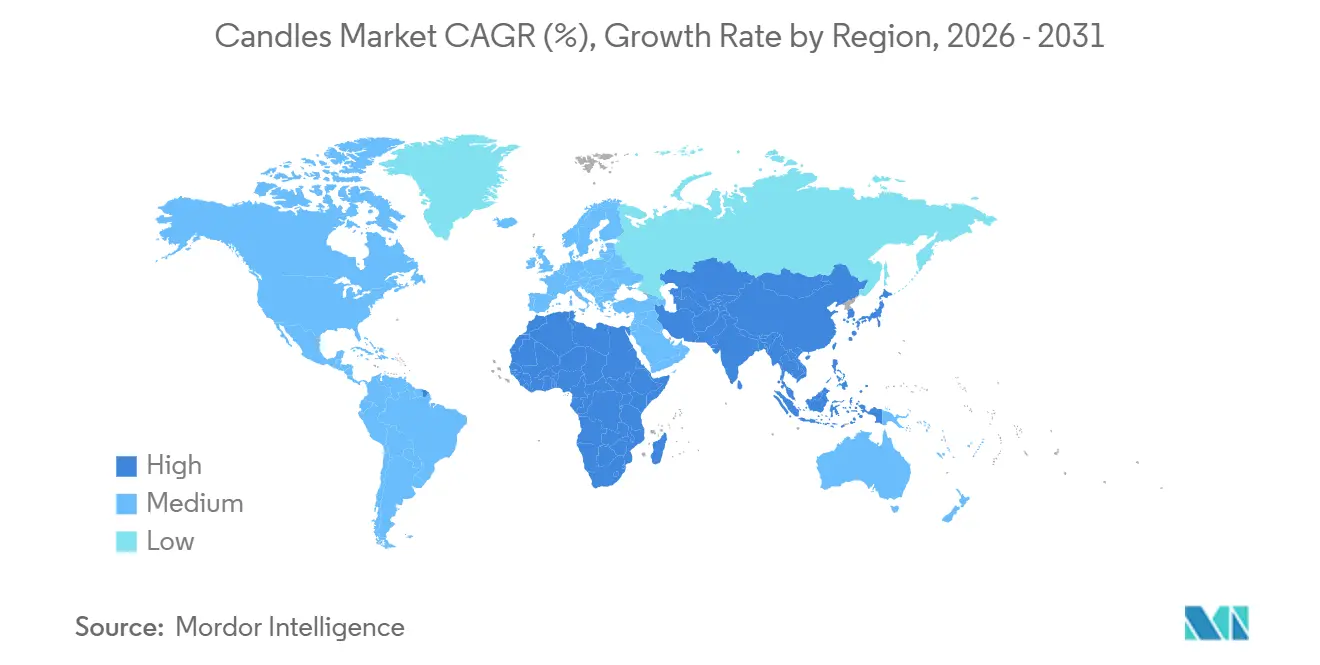

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Candles Market Analysis by Mordor Intelligence

The global candle market is expected to grow from USD 15.0 billion in 2025 to USD 16.0 billion in 2026, reaching USD 21.9 billion by 2031, reflecting a CAGR of 6.51% during 2026–2031. This growth trajectory indicates stable market expansion supported by increasing consumer demand in the home fragrance and lifestyle categories. The candles market now draws demand from home décor, wellness routines, and premium gifting, which keeps the category relevant even when household budgets are under pressure. The candles market is also being shaped by a firmer compliance environment in Europe, where product safety and chemical labeling rules have raised the entry bar for products sold in the block and favored better-prepared suppliers [1]Source: European Chemicals Agency, “Complying with CLP When Making or Importing Candles,” Publications Office of the European Union, op.europa.eu. Asia-Pacific is emerging as the primary growth hub for the candle market, supported by strong manufacturing capabilities alongside rising consumer demand for premium, fragrance-led products. The market remains highly fragmented, making brand equity, scent innovation, packaging differentiation, and sustainability positioning key competitive levers over scale alone. Meanwhile, volatility in raw material costs and increasingly stringent regulatory requirements are intensifying margin pressure, further advantaging large, integrated players that can better absorb input shocks and compliance costs compared to smaller manufacturers.

Key Report Takeaways

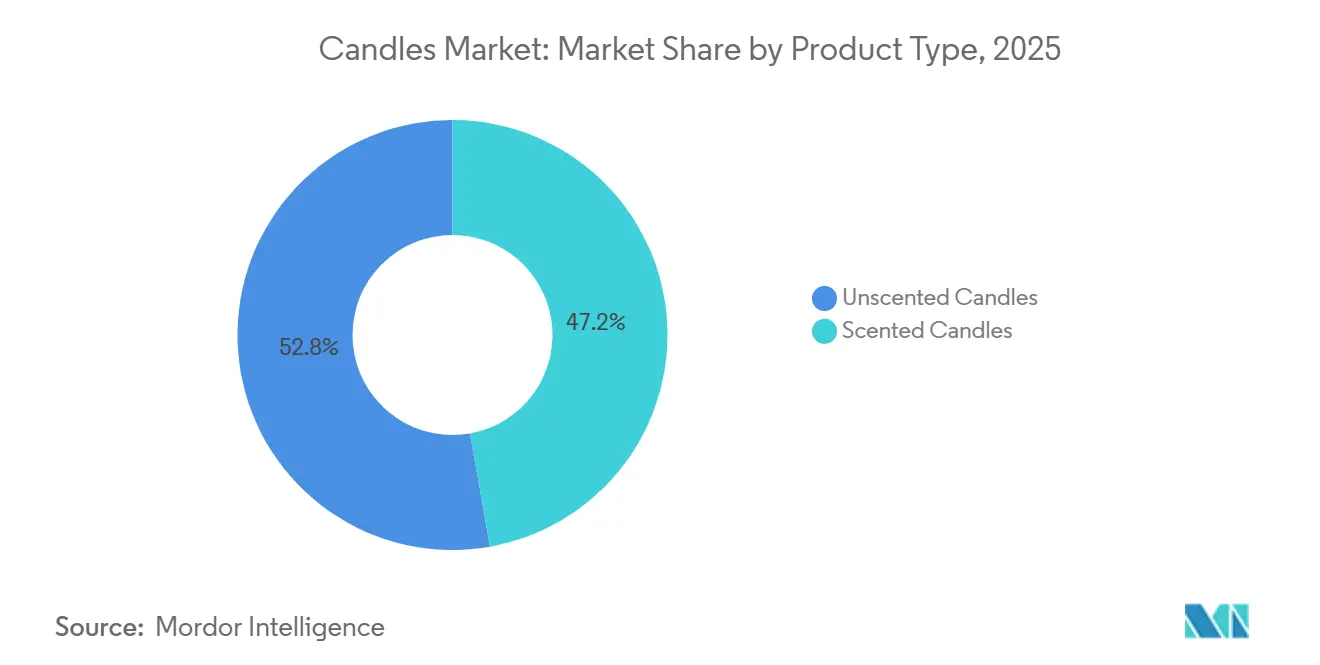

By product type, unscented candles led with 52.80% revenue share in 2025, and the scented candle segment is projected to grow at a 7.12% CAGR through 2031.

By wax type, paraffin wax held 42.2% of revenue in 2025, while beeswax recorded the highest projected CAGR at 7.5% through 2031.

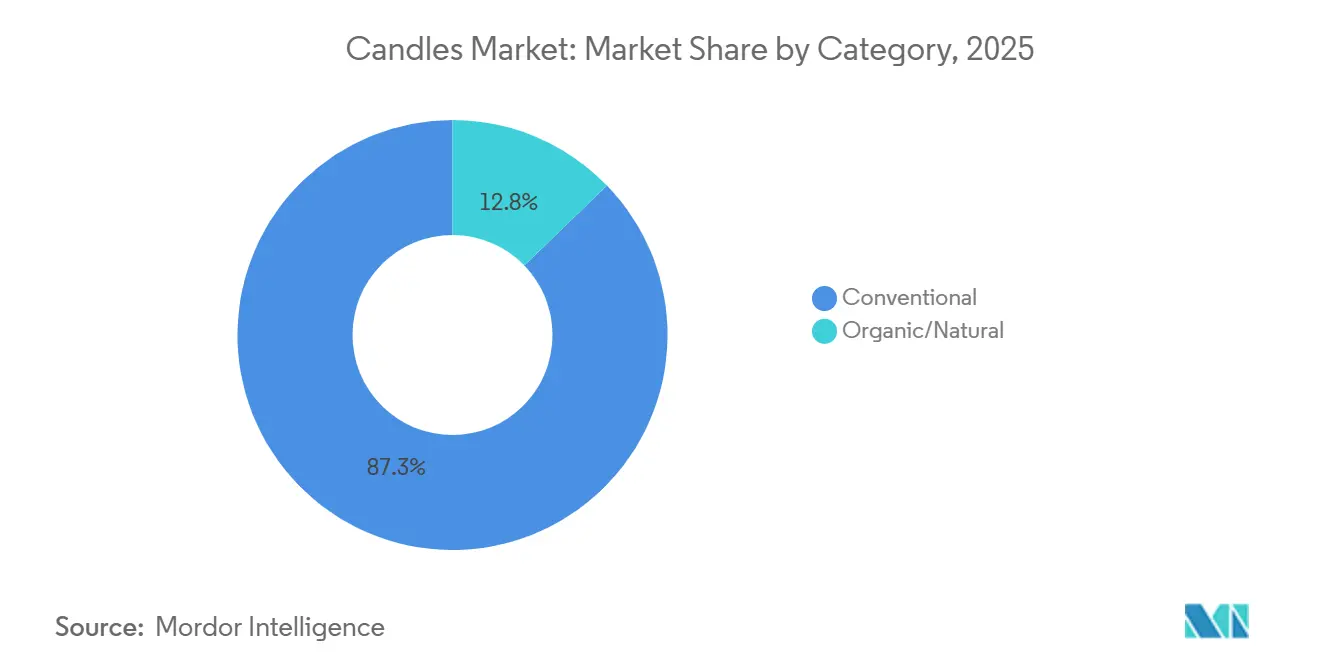

By category, conventional candles accounted for 87.3% of revenue in 2025, while organic and natural candles are advancing at a 6.8% CAGR through 2031.

By price tier, the mass segment captured 50.1% of revenue in 2025, while the premium segment is forecast to expand at an 11.3% CAGR through 2031.

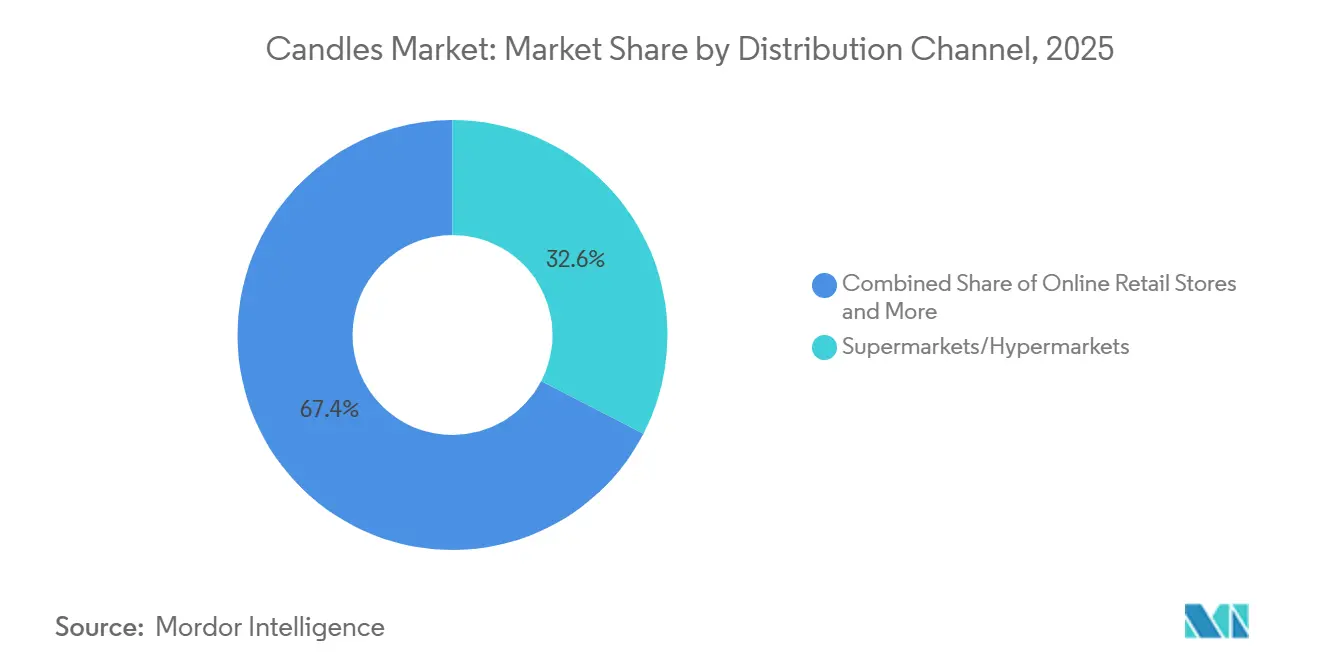

By distribution channel, supermarkets and hypermarkets represented 32.6% of revenue in 2025, while online retail is projected to grow at an 8.2% CAGR through 2031.

By geography, Asia-Pacific held 37.5% revenue share in 2025 and is also forecast to record the fastest CAGR at 8.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Candles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Home Fragrance Products | +1.5% | Global | Short term (≤ 2 years) |

| Rising Home Décor and Interior Design Spending | +1.2% | North America and Europe | Medium term (2-4 years) |

| Expansion of Wellness, Self-Care, and Aromatherapy Trends | +1.4% | Global, particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Premiumization and Luxury Product Adoption | +0.9% | Europe, North America, Asia-Pacific core | Long term (≥ 4 years) |

| Rising Use of Candles for Festive Decorations and Personal Gifting | +0.7% | Global, peaks in Asia-Pacific and Europe | Short term (≤ 2 years) |

| Product Innovation in Fragrances, Designs, and Sustainable Materials | +0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Home Fragrance Products

The candles market has surpassed a key inflection point, with home fragrance evolving from a discretionary household purchase into a recurring lifestyle category. Consumers are increasingly incorporating candles into their daily routines, driving more consistent replenishment cycles and reducing demand volatility associated with traditional holiday-driven sales peaks. This trend is reflected in Bath & Body Works' 14th Annual Candle Day, during which the company featured over 180 candle variants at a promotional price of USD 9.95 across both retail and e-commerce channels in December 2025 [2]Source: Bath & Body Works, “Bath & Body Works Announces the Return of Annual Candle Day,” BBW Investor Relations, bbwinc.com. The scale and success of this event underscore the ability of mature markets to sustain high purchase frequency when supported by broad product assortments and strategically timed promotions. As a result, the candles market benefits from a more resilient demand profile, characterized by stronger repeat-purchase behavior and reduced dependence on seasonal sales surges.

Rising Home Décor and Interior Design Spending

The candles market continues to benefit from the increasing consumer focus on home aesthetics, wellness, and personalized living environments. As interior styling becomes a more integral part of household consumption, candles have evolved beyond their traditional functional role to become a key element of home décor and atmosphere enhancement. Their ability to deliver both visual appeal and sensory experiences strengthens their value proposition and broadens their relevance across multiple consumer segments. This unique positioning enables candles to occupy a space between decorative and functional household products, supporting consistent demand even in periods of cautious consumer spending. Compared with many discretionary home accessories, candles offer an accessible way for consumers to refresh and elevate their living spaces, reinforcing their appeal as an affordable lifestyle enhancement product. As a result, the category benefits from enduring consumer interest in creating comfortable, aesthetically pleasing, and experience-driven home environments, supporting long-term market growth.

Expansion of Wellness, Self-Care, and Aromatherapy Trends

The candles market is increasingly benefiting from the growing consumer emphasis on self-care, mindfulness, and at-home wellness experiences. As consumers seek products that enhance relaxation, emotional well-being, and everyday comfort, scented candles have become an important component of wellness-oriented lifestyles. Fragrance selection is now closely associated with mood enhancement, stress relief, and the creation of personalized environments, elevating candles from simple home accessories to experience-driven products. This shift is influencing product innovation across the industry, with manufacturers placing greater emphasis on sophisticated fragrance profiles, sensory experiences, and premium positioning. In response to evolving consumer preferences, leading brands are investing in product development, brand revitalization, and enhanced retail experiences to strengthen engagement and maintain market relevance.

Product Innovation in Fragrances, Designs, and Sustainable Materials

The candles market is experiencing an accelerated pace of innovation, driven by evolving consumer expectations around product quality, sustainability, and brand authenticity. Competition is increasingly extending beyond traditional attributes such as fragrance and burn performance, with packaging design, ingredient transparency, material sourcing, and overall product presentation becoming critical factors in purchasing decisions. Consumers are placing greater value on brands that demonstrate clear commitments to quality, sustainability, and responsible manufacturing practices. In response, manufacturers are expanding their focus toward cleaner-burning wax alternatives, natural ingredients, eco-friendly packaging solutions, and premium vessel designs that enhance both product appeal and environmental credentials. Sustainability-oriented features, including renewable raw materials, recyclable containers, and thoughtfully designed accessories, are increasingly being incorporated into mainstream product portfolios rather than remaining confined to niche segments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.2% | Global | Short term (≤ 2 years) |

| Competition from Alternative Home Fragrance Products | -0.7% | North America and Europe | Medium term (2-4 years) |

| Availability of Low-Cost Unorganized and Private-Label Products | -0.6% | Asia-Pacific, South America, Middle East and Africa | Medium term (2-4 years) |

| Stringent Environmental and Sustainability Regulations | -0.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Raw Material Prices

The candles market faces a significant challenge from ongoing volatility in raw material costs, as wax remains a core input across virtually all product categories. Fluctuations in the availability and pricing of both conventional and natural waxes can directly impact production costs, creating pressure on manufacturers' profitability and operational planning. The industry's reliance on a limited range of scalable wax alternatives further increases exposure to supply chain disruptions and commodity market dynamics. Rising input costs can be particularly challenging in a competitive environment where the ability to pass higher expenses on to consumers is often constrained by pricing sensitivity and market positioning. This creates margin pressure across both mass-market and premium product segments, requiring manufacturers to balance cost management with product quality and brand value. As a result, procurement capabilities, supplier relationships, and supply chain resilience have become increasingly important competitive advantages.

Competition from Alternative Home Fragrance Products

The candles market is facing increasing competitive pressure from alternative home fragrance solutions, including diffusers, room sprays, and other flame-free formats. These products are gaining consumer acceptance due to their convenience, ease of use, continuous fragrance delivery, and alignment with evolving smart home and connected living trends. As consumers seek low-maintenance solutions that integrate seamlessly into modern lifestyles, alternative fragrance formats are expanding their presence within the broader home ambiance category. Despite this competition, candles continue to maintain a distinct value proposition through their decorative appeal, gifting potential, and ability to create immersive sensory and emotional experiences. The ritualistic nature of candle use, combined with its contribution to atmosphere and interior aesthetics, provides differentiation that many substitute products cannot fully replicate. Nevertheless, the growing availability of alternative fragrance products is intensifying competition for consumer spending, particularly in more mature markets where adoption of connected home technologies and convenience-oriented products is relatively advanced.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Unscented Candles Lead While Scented Segment Accelerates Growth

Unscented candles accounted for 52.8% of the candle market in 2025, making them the largest product segment by revenue. Their market leadership is supported by diverse end-use applications, including religious and ceremonial practices, household utility, hospitality settings, and decorative purposes. These use cases generate consistent demand and provide the segment with a level of resilience that is less dependent on changing consumer lifestyle trends. As a result, unscented candles continue to serve as the volume backbone of the broader candles market.

Meanwhile, scented candles are emerging as the fastest-growing segment, projected to expand at a CAGR of 7.12% through 2031. Growth is being driven by increasing consumer interest in home ambiance, wellness-oriented lifestyles, aromatherapy, and premium home décor products. For many consumers, scented candles have evolved from a functional product into a means of expressing personal style, enhancing mood, and creating immersive sensory experiences.

By Wax Type: Paraffin Leads While Natural Alternatives Scale

Paraffin wax accounted for 42.2% of the candles market in 2025, maintaining its position as the dominant wax type due to its cost efficiency, scalable supply chain, and suitability for large-scale manufacturing. Its established production infrastructure and consistent performance characteristics continue to support mass-market product offerings, making it a critical raw material across the global candles industry. As a result, paraffin wax remains central to manufacturers' efforts to balance production costs, product quality, and competitive pricing strategies.

In contrast, beeswax is emerging as the fastest-growing wax segment and is projected to expand at a CAGR of 7.5% through 2031. Growth is being driven by increasing consumer preference for natural, sustainable, and premium-positioned products, reflecting a broader shift toward ingredient transparency and environmentally conscious purchasing behavior. This trend highlights the growing strategic importance of raw material selection as consumers increasingly associate product composition with brand values and product quality. The broader adoption of alternative waxes, including soy, coconut, palm, and blended formulations, is further reshaping competitive dynamics within the market. Manufacturers are leveraging these materials to strengthen sustainability credentials, differentiate product portfolios, and align with evolving consumer expectations.

By Category: Conventional Base Narrows as Organic Scales

Conventional candles accounted for 87.3% of the candles market in 2025, underscoring their continued dominance across mainstream retail channels. Their strong market position is supported by cost-effective production, broad product availability, and widespread adoption in applications where affordability and functional performance remain primary purchasing considerations. Conventional candles continue to serve as the foundation of market demand, particularly across mass retail, hospitality, religious, and event-driven consumption segments.

The organic and natural candles are emerging as a key growth segment and are projected to expand at a CAGR of 6.8% through 2031. Rising consumer interest in sustainability, ingredient transparency, and wellness-oriented products is driving demand for candles made with natural waxes, plant-based ingredients, and environmentally responsible materials. This trend reflects a broader shift in consumer preferences toward products that align with personal values and lifestyle choices. While conventional candles are expected to retain their leadership position due to their accessibility and established distribution networks, the growing momentum behind natural and organic alternatives is reshaping product development and brand strategies. Manufacturers are increasingly expanding their portfolios to include cleaner-label and sustainability-focused offerings, enabling them to address evolving consumer expectations while maintaining broad market coverage.

By Price Tier: Mass Anchors Volume as Premium Reshapes the Margin Stack

Mass-tier candles accounted for 50.1% of the candles market revenue in 2025, reflecting the continued importance of affordability and broad accessibility in driving category demand. The segment benefits from extensive retail distribution, high purchase frequency, and strong appeal among price-conscious consumers, making it a critical contributor to overall market volume. As a result, mass-market products remain the foundation of the industry's revenue base and consumer reach.

Premium candles are emerging as the fastest-growing price segment and are projected to expand at a CAGR of 11.3% through 2031. Growth is being fueled by increasing consumer willingness to invest in higher-quality fragrances, elevated packaging, premium ingredients, and differentiated brand experiences. Candles are increasingly being positioned as lifestyle, wellness, and home décor products rather than purely functional items, supporting greater value realization across premium offerings. The evolving pricing landscape is also intensifying competitive pressure within the mid-market segment, where brands face challenges differentiating themselves against both value-focused mass-market offerings and premium products with stronger brand equity. Consequently, the candles market is becoming increasingly polarized, with clear segmentation between volume-oriented and premium value-driven products.

By Distribution Channel: Brick-and-Mortar Leads, Online Reshapes the Mix

Supermarkets and hypermarkets accounted for 32.6% of the candles market in 2025, maintaining their position as the leading distribution channel. Their dominance is driven by high consumer footfall, broad product availability, and the ability to capture impulse purchases, routine replenishment demand, and seasonal buying occasions within a single shopping trip. As a result, large-format retail continues to play a critical role in supporting market volume and brand visibility across mainstream consumer segments. Specialty stores also remain an important channel, particularly for premium, luxury, and artisanal candle brands. These retailers provide a more immersive shopping environment where consumers can evaluate fragrance profiles, product quality, and brand positioning firsthand.

Meanwhile, online retail is emerging as the fastest-growing distribution channel and is projected to expand at a CAGR of 8.2% through 2031. Growth is being driven by increasing consumer adoption of e-commerce, enhanced product discovery tools, and the ability of brands to engage customers through personalized digital experiences. Online platforms enable manufacturers to leverage targeted marketing, subscription programs, exclusive product launches, and data-driven consumer insights to strengthen customer acquisition and retention.

Geography Analysis

Asia-Pacific accounted for 37.5% of the candles market in 2025 and is projected to register the fastest growth rate through 2031, positioning the region as both the largest and most dynamic market globally. This leadership is supported by a unique combination of extensive manufacturing capabilities, expanding middle-class populations, rising disposable incomes, and increasing consumer interest in home décor, wellness, and premium lifestyle products. Key markets such as China, India, and South Korea are driving demand growth while simultaneously strengthening the region's role within global candle production and supply chains.

North America remains the second-largest regional market, supported by a well-established culture of candle consumption across home fragrance, gifting, seasonal décor, and self-care applications. Strong brand penetration, high consumer awareness, and a mature retail infrastructure continue to support stable demand for both mass-market and premium products. The region also remains an important center for product innovation, brand development, and premiumization strategies within the global candles industry.

Europe maintains a significant market position, characterized by a combination of premium heritage brands, established consumer demand, and a highly regulated operating environment. Increasing emphasis on product safety, sustainability, ingredient transparency, and regulatory compliance is shaping competitive dynamics across the region. These factors are encouraging manufacturers to strengthen sourcing practices, certification standards, and product documentation, creating opportunities for companies with robust compliance capabilities and sustainable product portfolios [3]Source: Euronews Deutschland, “Allerheiligen in Polen, Ein Meer Aus Lichtern Und Ein Milliardengeschäft,” Euronews, de.euronews.com.

Meanwhile, South America and the Middle East & Africa represent emerging growth opportunities within the global candles market. Demand in these regions is supported by a combination of cultural traditions, religious practices, gifting occasions, and increasing consumer interest in decorative and premium fragrance products. As disposable incomes rise and retail infrastructure continues to develop, manufacturers are increasingly tailoring product offerings, fragrance profiles, and pricing strategies to align with local consumer preferences and purchasing behaviors.

Competitive Landscape

The candles market remains highly fragmented, characterized by the presence of multinational brands, regional manufacturers, private-label suppliers, and independent artisanal producers. Leading industry participants continue to invest in product innovation, portfolio expansion, and brand revitalization initiatives to sustain growth in an increasingly crowded marketplace. Product launches, limited-edition collections, strategic partnerships, and enhanced consumer engagement strategies have become important tools for maintaining brand visibility and driving premium positioning. Across the industry, companies are leveraging storytelling, lifestyle branding, and experiential marketing to create stronger emotional connections with consumers and differentiate their offerings beyond functional product attributes.

The competitive landscape is also being shaped by the growing influence of premium, design-oriented, and sustainability-focused brands. These companies often benefit from greater agility in responding to emerging consumer trends, enabling them to introduce innovative formulations, natural ingredients, environmentally responsible products, and niche fragrance concepts more rapidly than larger competitors. Their ability to address evolving consumer expectations around authenticity, transparency, and wellness continues to create opportunities for market share expansion within higher-value segments.

The increasing consumer scrutiny of ingredient sourcing, sustainability claims, and product transparency is raising competitive standards across the industry. Manufacturers are under growing pressure to demonstrate responsible sourcing practices, clear product disclosure, and credible environmental commitments. Consequently, transparency and brand trust are becoming increasingly important competitive differentiators alongside traditional factors such as fragrance quality and pricing.

Candles Industry Leaders

Newell Brands, Inc.

Bath & Body Works Direct, Inc.

Bolsius International BV

S. C. Johnson & Son, Inc.

NEST Fragrances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Yankee Candle has reopened a refreshed Mall of Georgia store as part of Newell Brands’ broader brand modernization strategy, focusing on updated store design and improved customer experience. The move reflects ongoing efforts to strengthen the brand’s physical retail presence and enhance in-store engagement.

- December 2025: Vedlume has launched a luxury handcrafted scented candle range in India focused on festive home décor and gifting. The candles are made with 100% natural soy wax, premium fragrance blends, and eco-friendly materials like lead-free wicks, emphasizing sustainability and a clean burn.

- May 2025: NEST New York’s “Voyages by NEST” collection, which is positioned as a premium home fragrance expansion launched at Harrods. In the candle segment, the range includes luxury 2-wick scented candles inspired by travel-themed fragrances, designed with elevated packaging and fine fragrance formulation.

- February 2025: Diptyque has expanded its Orphéon line with a limited-edition collection inspired by the historic jazz club near its original Paris boutique. The release includes new fragrance formats, candles, and decorative home pieces that extend the brand’s storytelling around the scent’s cultural and artistic origins

Global Candles Market Report Scope

The candles market refers to the global industry involved in the production, distribution, and consumption of candles used for decorative, aromatic, religious, wellness, and functional lighting purposes across residential, commercial, and institutional environments.

The market is structured across multiple segmentation dimensions, including product type, wax composition, category, price tier, distribution channel, and geography. By product type, it includes unscented candles and scented candles. By wax type, it comprises paraffin wax, beeswax, and other natural or synthetic waxes. By category, the market is divided into conventional and organic/natural candles. By price tier, it is segmented into mass and premium categories. Distribution channels include supermarkets and hypermarkets, convenience stores, online retail platforms, specialty stores, and other retail formats. Geographically, the market spans North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. Market sizing and forecasts are typically conducted on a value basis (USD million).

| Scented Candle |

| Unscented Candle |

| Paraffin Wax |

| Bees Wax |

| Others |

| Conventional |

| Organic/Natural |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Norway | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Scented Candle | |

| Unscented Candle | ||

| By Wax Type | Paraffin Wax | |

| Bees Wax | ||

| Others | ||

| By Category | Conventional | |

| Organic/Natural | ||

| By Price Tier | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the candles market by 2031?

The candles market is forecast to reach USD 21.9 billion by 2031, rising from USD 15.98 billion in 2026 at a 6.51% CAGR.

What are the main risks affecting candle makers?

Raw material volatility, low-cost private-label competition, alternative home fragrance formats, and tighter EU compliance requirements are the main pressure points.

Which region is growing fastest in candles?

Asia-Pacific leads both current share and future growth, with 37.5% share in 2025 and an 8.5% CAGR projected through 2031.

Why are premium candles growing faster than mass candles?

Premium candles are benefiting from gifting, wellness use, fragrance sophistication, and stronger packaging appeal, which supports an 11.3% CAGR through 2031.

Page last updated on: