Home Fragrances Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 14.38 Billion |

| Market Size (2031) | USD 19.78 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

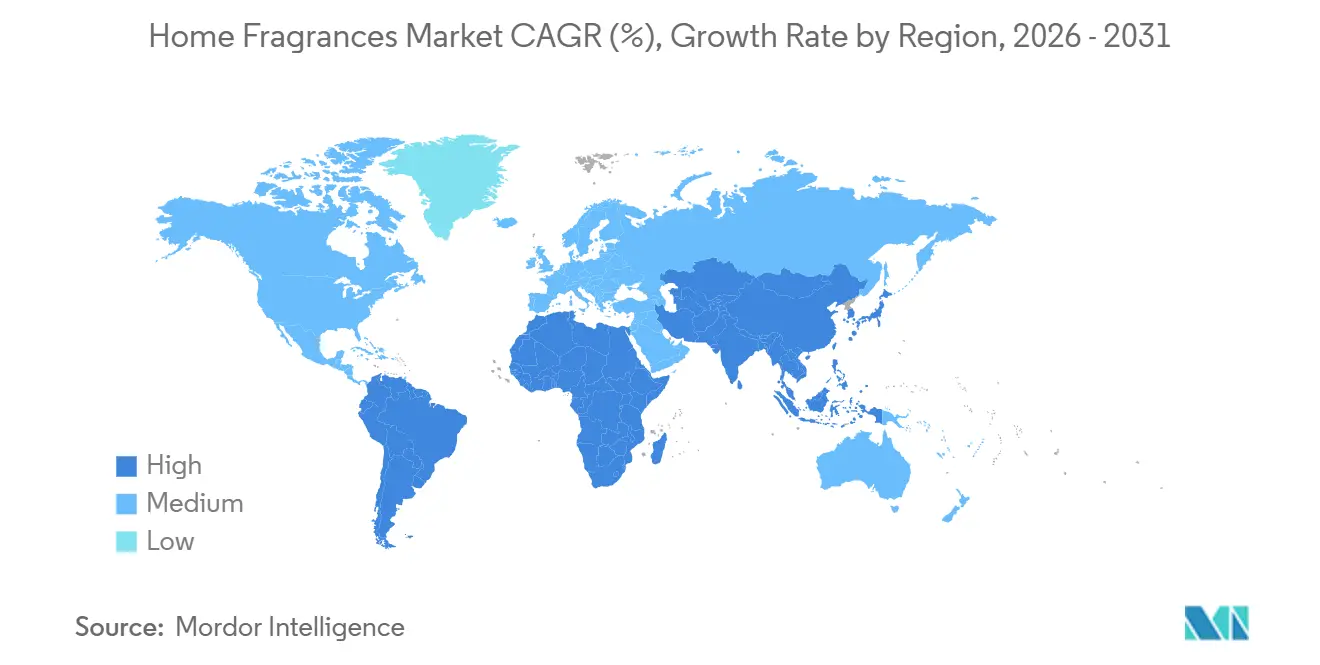

| Fastest Growing Market | South America |

| Largest Market | North America |

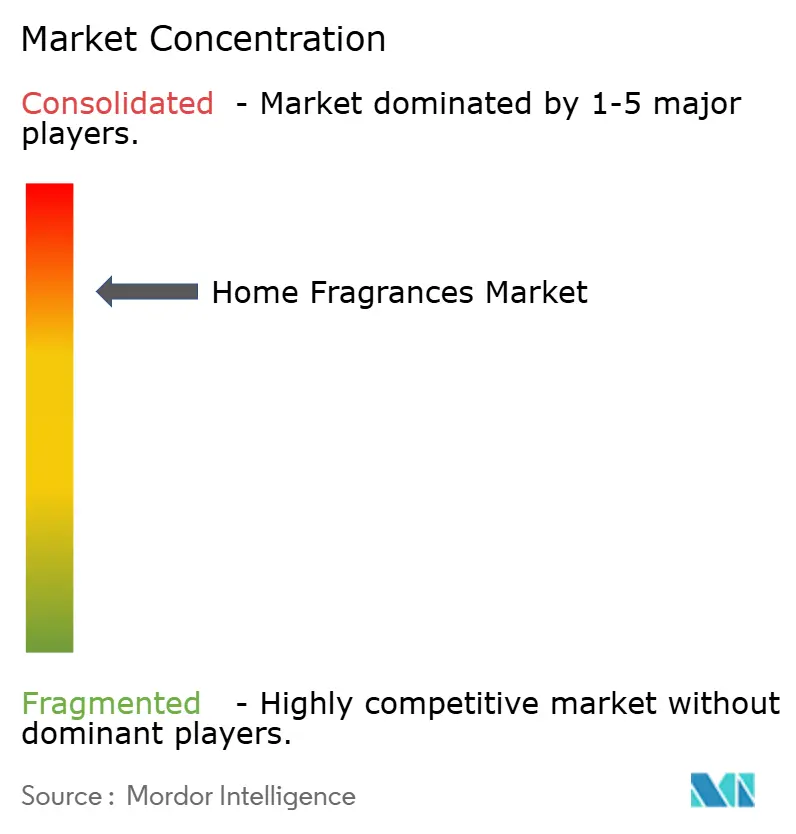

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Home Fragrances Market Analysis by Mordor Intelligence

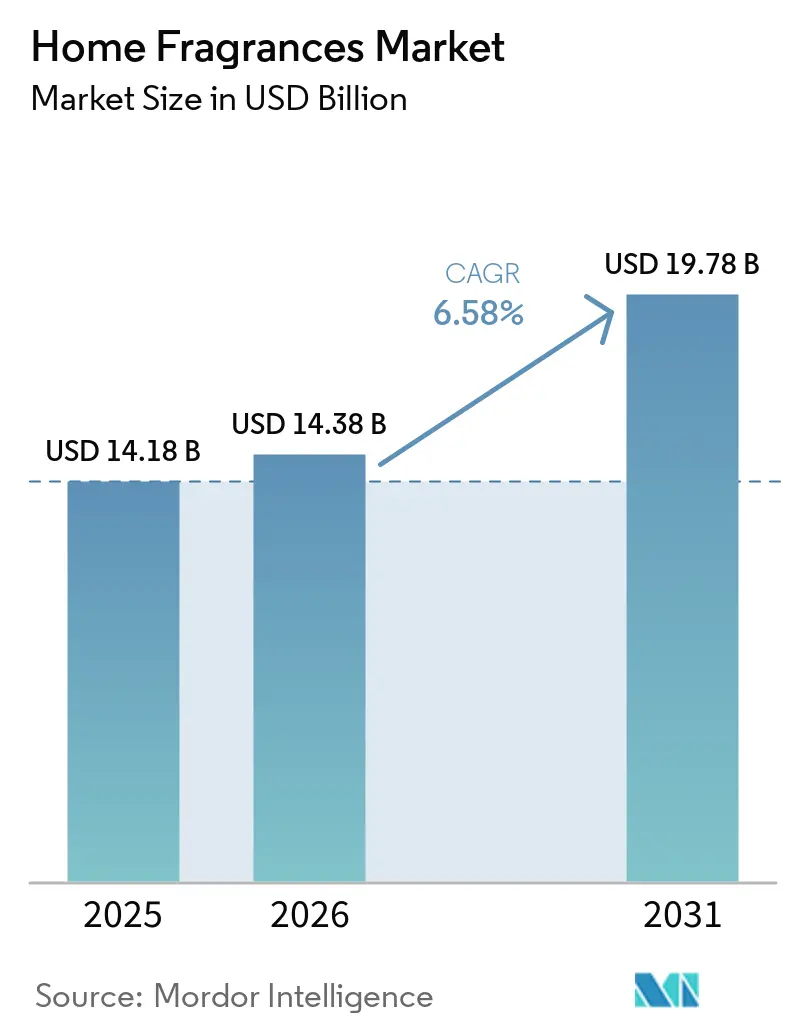

The home fragrances market was valued at USD 14.18 billion in 2025 and estimated to grow from USD 14.38 billion in 2026 to reach USD 19.78 billion by 2031, at a CAGR of 6.58% during the forecast period (2026-2031). This steady expansion reflects rising consumer confidence in scent-driven wellness and self-care routines. More households are moving beyond occasional odor control to adopting daily ambiance-enhancing and mood-setting rituals, resulting in sustained increases in discretionary spending on home-aroma solutions. Features such as app-controlled diffusers, programmable scent schedules, and integration with voice-activated ecosystems are likely to elevate the perceived value of home-fragrance devices and broaden the market’s premium segment. At the same time, tightening regulations around volatile organic compounds (VOCs) are encouraging manufacturers to shift toward cleaner, safer, and more transparent formulations. This regulatory push is prompting brands to adopt plant-based carriers and low-emission ingredients that align with consumer expectations for wellness-centric products.

Key Report Takeaways

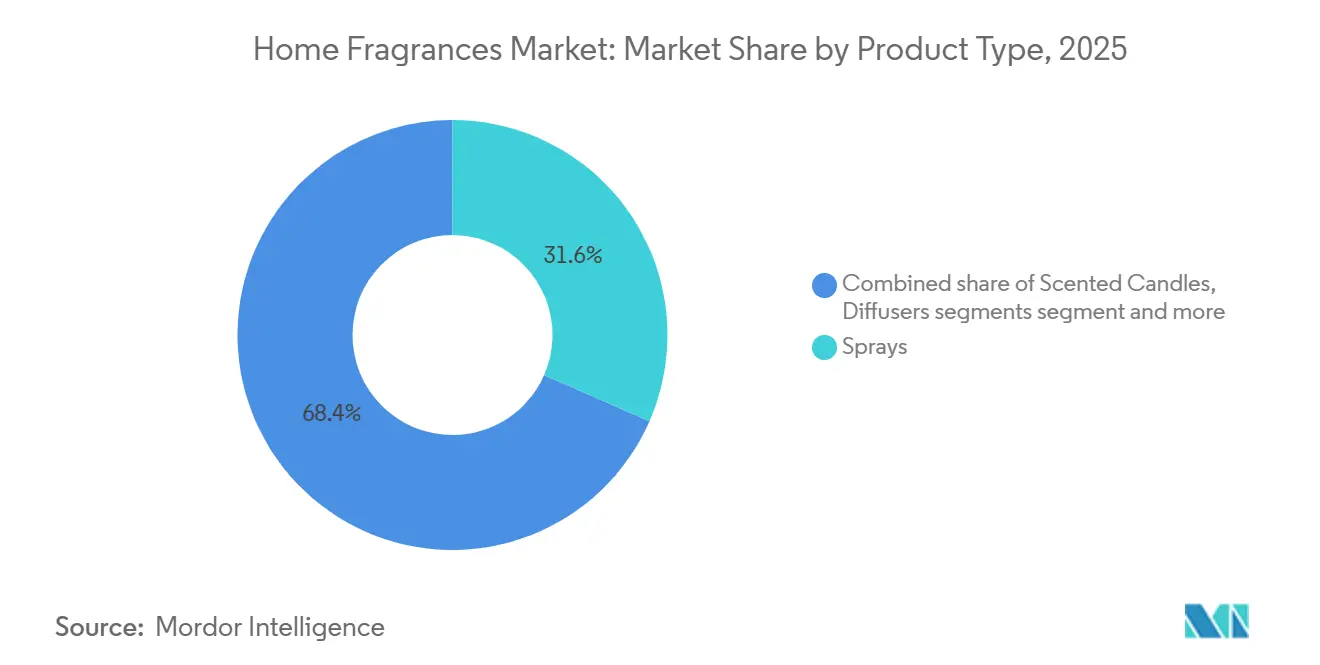

- By product type, sprays held a 31.57% revenue share in 2025; scented candles are forecast to register the highest 7.21% CAGR through 2031.

- By category, mass products captured 82.19% of sales in 2025, while premium lines are projected to grow at a 7.37% CAGR and outpace the total home fragrances market.

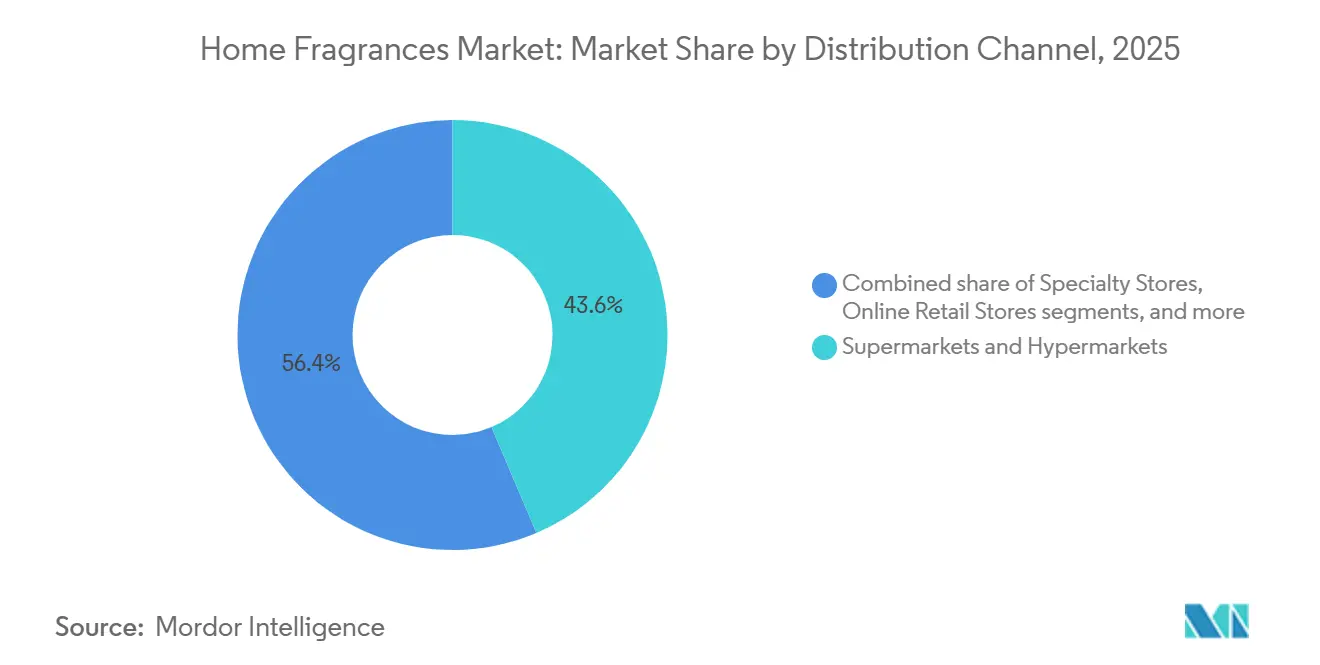

- By distribution channel, supermarkets and hypermarkets controlled 43.61% of 2025 revenue, whereas online retail is expected to post the fastest 7.84% CAGR through 2031.

- By geography, North America dominated with 49.58% of home fragrances market share in 2025; South America is on track for a 7.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Home Fragrances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for multifunctional home-fragrance solutions | +1.2% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Surge in premium and artisanal candle sales supported by a strong gifting culture | +1.1% | North America, Europe, and emerging affluent segments in Asia-Pacific | Long term (≥ 4 years) |

| Increasing consumer focus on home aesthetics and wellness-driven lifestyles | +0.9% | Global, particularly North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Growing impact of social media channels on home-aroma purchasing behaviour | +0.8% | Global, with strongest influence in North America and Asia-Pacific Gen Z cohorts | Short term (≤ 2 years) |

| Seasonal and limited-edition releases driving fresh buying occasions | +0.7% | North America and Europe, with spillover to South America and Middle East | Short term (≤ 2 years) |

| Expansion of e-commerce enhancing product availability and boosting direct-to-consumer sales | +1.3% | Global, with accelerated penetration in South America, Asia-Pacific, and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising preference for multifunctional home-fragrance solutions

Rising preference for multifunctional home-fragrance solutions is significantly driving growth in the home fragrances market, as consumers increasingly seek products that deliver both sensory appeal and practical benefits. Modern households favor fragrance formats that combine aroma with added functionalities such as air purification, odor neutralization, humidity control, or wellness support through aromatherapy. This shift aligns with growing demand for cleaner, healthier indoor environments and products that enhance overall home ambience. Brands are responding by integrating advanced diffusing technologies, natural essential oils, and antibacterial or mood-enhancing properties into their offerings. Multifunctional solutions also appeal to space-conscious consumers who prefer fewer, more effective products. Additionally, rising awareness of indoor air quality and holistic living strengthens adoption of these hybrid innovations.

Surge in premium and artisanal candle sales supported by a strong gifting culture

The premium candle market is undergoing a notable shift driven by the rapid rise of direct-to-consumer (DTC) brands. By eliminating traditional retail intermediaries, these brands are boosting margins while offering highly personalized and emotionally engaging gifting experiences. Once considered occasional luxuries, premium candles have become meaningful, year-round lifestyle statements. This evolution is closely linked to growing conscious consumerism, with buyers seeking eco-friendly, ethically crafted products. In response, premium brands such as Keap Candles and 1986 Home are adopting natural waxes like soy and coconut, creating visually appealing reusable containers, and investing in sustainable, biodegradable packaging. These changing dynamics are pushing mass-market companies to launch premium extensions, while niche artisanal makers broaden their presence through collaborations with gourmet and concept retailers, delivering curated sensory experiences that enhance brand perception and strengthen customer loyalty.

Increasing consumer focus on home aesthetics and wellness-driven lifestyles

Increasing consumer focus on home aesthetics and wellness-driven lifestyles is a key driver of the home fragrances market, as households increasingly view scent as a vital component of interior ambience and emotional well-being. Consumers are seeking products that elevate the visual appeal of living spaces while supporting relaxation, stress relief, and mood regulation. This trend is strongly shaped by the rise of self-care routines and the growing desire to create soothing, restorative home environments. These offerings particularly resonate with Millennials and Gen Z, who place strong emphasis on mental health and self-care; in 2024, Millennials accounted for 21.81% of the United States population, while Generation Z represented 20.81%[1]Source: US Census Bureau, "Population distribution in the United States", census.gov. As a result, home fragrances such as scented candles, diffusers, and aromatherapy blends are becoming integral to daily rituals like meditation and unwinding. Design-centric formats that complement home décor further attract style-driven consumers.

Growing impact of social media channels on home-aroma purchasing behaviour

The growing impact of social media channels is increasingly shaping home-aroma purchasing behavior, as visually driven platforms like Instagram, TikTok, and Pinterest heavily influence consumer preferences. With Instagram now used by half of United States adults and TikTok (37%) and WhatsApp (32%) also attracting significant audiences, fragrance trends are rapidly amplified through aesthetically curated posts, creator recommendations, and lifestyle content. According to the Pew Research survey conducted in June 2025, YouTube (84%) and Facebook (71%) remain the most widely adopted platforms, further broadening the reach of home-aroma inspirations and product discovery[2]Source: "Pew Research Center", pewresearch.org. Influencers and home décor creators frequently showcase candles, diffusers, and room sprays as essential components of modern living spaces, transforming them into aspirational lifestyle elements. User-generated content and short-form videos evoke sensory appeal, driving curiosity and impulse purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising presence of counterfeit and imitation home-aroma products | -0.6% | Global, with highest incidence in Asia-Pacific and online marketplaces | Short term (≤ 2 years) |

| Increasing consumer worries regarding chemical-based ingredients | -0.5% | North America and Europe, with growing awareness in urban Asia-Pacific | Medium term (2-4 years) |

| Tightening volatile organic compounds compliance standards restricting product formulation options | -0.7% | North America and Europe, with spillover to export-oriented manufacturers in Asia | Long term (≥ 4 years) |

| Supply chain volatility impacting the availability of key raw materials | -0.8% | Global, with acute pressure on natural-ingredient sourcing from climate-sensitive regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising presence of counterfeit and imitation home-aroma products

The rising prevalence of counterfeit and imitation home fragrance products is increasingly restraining the growth of the market, posing risks to both consumers and legitimate brands. These low-cost replicas often mimic the packaging and scent profiles of premium products but compromise on quality, safety, and ingredient integrity. Many counterfeit items contain harmful chemicals, unregulated additives, or substandard fragrance oils, raising concerns over indoor air quality and potential health effects. Their widespread availability across online marketplaces and informal retail channels fuels consumer confusion, dilutes brand trust, and reduces repeat purchases. Authentic brands face revenue losses and difficulties in protecting intellectual property as imitation products continue to circulate. Moreover, price-sensitive consumers may unknowingly choose cheaper counterfeit alternatives, further undermining demand for genuine offerings.

Increasing consumer worries regarding chemical-based ingredients

The rising presence of counterfeit and imitation home-aroma products is increasingly restraining the growth of the home fragrances market, posing risks to both consumers and legitimate brands. These low-cost replicas often mimic the packaging and scent profiles of premium products but compromise heavily on quality, safety, and ingredient integrity. Many counterfeit items contain harmful chemicals, unregulated additives, or substandard fragrance oils, raising concerns over indoor air quality and potential health effects. Their widespread availability across online marketplaces and informal retail channels further fuels consumer confusion, diluting brand trust and reducing repeat purchases. Authentic brands face revenue losses and challenges in protecting intellectual property as imitation products continue to circulate. Additionally, price-sensitive consumers may unknowingly opt for cheaper fake alternatives, undermining demand for genuine offerings. As counterfeiting intensifies, it creates significant obstacles for market expansion and erodes overall category credibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sprays Dominate, Yet Scented Candles Accelerate Fastest

Sprays accounted for 31.57% of total revenue in 2025, making them the most dominant segment in the home fragrances market. Their widespread adoption stems from their ability to deliver an immediate burst of fragrance, meeting consumer expectations for quick and convenient odor control. They are particularly effective in high-traffic zones such as bathrooms, kitchens, and entryways, where instant refreshment is valued. The portability and ease of use of spray formats also contribute to frequent household replenishment. Additionally, the wide availability of scent varieties and price points allows sprays to appeal to both mass-market and premium consumers. As a result, this category continues to hold a strong competitive edge and remains the preferred choice for everyday fragrance needs.

Scented candles are projected to grow at a CAGR of 7.21% through 2031, making them the fastest-expanding segment in the home fragrances industry. This growth rate surpasses the overall market, highlighting the strong consumer shift toward premium and experiential home aromas. Their momentum is fueled by rising premiumization trends, where consumers increasingly seek artisanal, design-forward, and long-lasting candle options. Social-media influence, particularly on aesthetic-driven platforms, has amplified candle visibility and shaped purchasing behavior. Additionally, candles remain a popular and recurring gifting choice across festive seasons, personal celebrations, and lifestyle occasions.

By Category: Mass Retains Share, Premium Outpaces on Affluence and Aspiration

The mass-market segment dominated the home fragrances industry in 2025, capturing 82.19% of total revenue. This strong lead is primarily supported by the broad availability of affordable products across supermarkets, hypermarkets, and drugstores. These retail channels cater to price-sensitive consumers who value convenience, familiarity, and immediate accessibility. Mass-market offerings also benefit from high purchase frequency, as consumers often replenish these products as part of their routine household shopping. The wide assortment of scents and formats at budget-friendly price points further reinforces their appeal. As a result, the mass-market category continues to anchor overall industry revenue and remains the preferred choice for everyday home-fragrance consumption.

The premium segment is expanding at a CAGR of 7.37% through 2031, making it the fastest-growing category within the market. This robust growth reflects a notable shift among affluent consumers who increasingly opt for high-quality, artisanal, and design-driven fragrance options. The market is also witnessing rising interest in limited-edition releases and small-batch formulations that convey exclusivity and craftsmanship. Premium brands often serve as lifestyle and status indicators, appealing to consumers who value aesthetics and elevated sensory experiences. Social trends, including wellness-driven purchasing and home decor inspirations, are further propelling the segment’s momentum. Consequently, the premium category is rapidly evolving into a key growth engine, offering higher margins and enhanced brand differentiation in the home fragrances market.

By Distribution Channel: Online Retail Surges as Supermarkets Plateau

Supermarkets and hypermarkets dominated distribution in 2025, accounting for 43.61% of total revenue in the home fragrances market. Their leadership is driven by consistently high foot traffic, which naturally supports frequent impulse purchases. These retail formats offer consumers the convenience of purchasing home-fragrance items during routine grocery shopping trips, reinforcing habitual buying behavior. Broad product visibility on shelves and attractive in-store promotions also strengthen their conversion rates. Additionally, the presence of both mass-market and mid-tier brands ensures that these outlets cater to a wide consumer base. As a result, supermarkets and hypermarkets remain the primary and most influential sales channel for home fragrance products.

Online retail is the fastest-growing distribution channel, projected to expand at a CAGR of 7.84% through 2031. This rapid growth reflects the increasing adoption of digital shopping and the rise of direct-to-consumer (D2C) home-fragrance brands. Subscription models offering curated scents and refill plans are further boosting customer retention in the online space. For instance, the International Telecommunication Union (ITU) reports that global internet users reached 5.5 billion in 2024, increasing by 227 million users from 2023[3]Source: International Telecommunication Union, "Global Internet Use Continues to Rise, But Disparities Remain, Especially in Low-income Regions", itu.int Third-party marketplaces are also accelerating growth by eliminating geographic limitations and providing unmatched product variety. Moreover, online platforms remove physical shelf-space constraints, enabling brands to showcase broader assortments and premium offerings. Together, these factors position e-commerce as the most dynamic and transformative channel in the home fragrances market.

Geography Analysis

North America remains the dominant region in the global home fragrances market, holding approximately 49.58% of the market share in 2025. This leadership is supported by strong consumer expenditure on home improvement and a mature, well-organized retail network. Seasonal fragrance rotation is deeply embedded in consumer culture, further reinforcing the region’s consistent demand. Although container-based scented candles continue to be widespread, there is a notable transition toward premium, artisanal, and design-driven products as consumers increasingly value uniqueness and quality. Battery-powered fragrance diffusers are also gaining popularity due to their convenience, portability, and flame-free operation, offering a modern alternative to traditional formats. Collectively, these factors help sustain North America's commanding position in the global market.

South America is projected to be the fastest-growing region, with a CAGR of 7.97% from 2026 to 2031, reflecting significant expansion opportunities for manufacturers. In Brazil, sprays currently dominate revenue contribution; however, scented candles are emerging as the fastest-growing category, showcasing evolving consumer preferences. The region’s momentum is fueled by rising disposable incomes, continued urbanization, and heightened interest in ambiance-enhancing and aesthetically appealing home fragrance products. Growing consumer exposure to global home décor trends is also influencing the adoption of diverse fragrance formats. This shift indicates a broadening market beyond functional products toward more premium and experiential offerings.

Europe demonstrates consistently high demand for eco-friendly, natural, and wellness-oriented home fragrance products, especially in the United Kingdom and Germany. This trend is supported by a health-conscious consumer base that increasingly scrutinizes ingredients and sustainability credentials. The Asia-Pacific region, including China, India, Japan, and Australia, is witnessing steady expansion driven by increasing disposable incomes, rapid urbanization, and long-standing cultural preferences for aromatic and ambiance-enhancing products. The Middle East and Africa are experiencing strong adoption of premium and traditional fragrance forms, such as incense, bakhoor, and ornate candles.

Competitive Landscape

In the home fragrances market, a blend of multinational giants and nimble specialty brands vie for dominance. Industry titans like Reckitt Benckiser Group, The Procter & Gamble Company, and Newell Brands Inc. are locked in fierce competition, channeling significant resources into product development. Their focus lies in crafting natural, wellness-centric fragrances and pioneering sustainable packaging solutions, aiming to align with the growing consumer demand for eco-friendly and health-conscious products. These efforts are part of a broader strategy to strengthen their foothold in an increasingly competitive market.

Meanwhile, the industry's landscape is being reshaped by technological strides. Smart diffusers, now app-controlled, are revolutionizing user experience by offering enhanced convenience and customization. With these devices, users can fine-tune fragrance intensity, set schedules, and mix scents, all from their smartphones. Brands such as Pura and Moodo lead this charge, presenting devices that not only allow scent customization and usage tracking but also effortlessly sync with voice platforms like Alexa and Google Home. These innovations are driving a shift in consumer expectations, emphasizing personalization and seamless integration with smart home ecosystems.

Simultaneously, industry heavyweights are honing in on the burgeoning markets of Asia-Pacific and South America. Bolstering distribution channels, both physical and digital, is paramount, supported by intensified online marketing campaigns and consumer engagement initiatives. Companies are leveraging these strategies to tap into the rising disposable incomes and changing lifestyle preferences in these regions. As the market pivots towards premium, bespoke, and experiential offerings, companies are amplifying their luxury fragrance lines, crafting products that resonate with the modern consumer's desire for personalization, exclusivity, and an enriched home atmosphere. This shift reflects a broader trend toward creating immersive and elevated sensory experiences within the home environment.

Home Fragrances Industry Leaders

-

Reckitt Benckiser Group plc

-

dōTERRA International LLC

-

Newell Brands Inc

-

Bath & Body Works Inc.

-

The Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bath & Body Works released two limited-edition candles for Summer 2025 through its membership program promotion. The company offered rewards members priority access and promotional pricing on the reintroduced Caribbean Escape candle, which incorporates tropical melon, raspberry nectar, and coconut fragrances, and the newly launched Orchid Blooms candle, comprising blush orchid, jasmine, and English ivy scents.

- May 2025: Nest New York debuted its premium fragrance collection, Voyages by Nest, exclusively at Harrods. The brand claims that each fragrance is designed to evoke the essence of a storied location, blending artful packaging and high-quality ingredients. The collection includes eau de parfums, perfume oils, candles, and diffusers.

- April 2025: WoodWick Candles introduced the Precious Metals Collection, a new line of elegantly crafted candles inspired by Earth's most treasured elements. According to the brand, it features a trending metallic aesthetic and rich, multi-layered scents. The new fragrances kindle a refined, multi-sensory experience perfect for the modern home.

- April 2025: ripple Home unveiled REED, a collection of residential fragrance diffusers. Crafted by master perfumers in Grasse, France, the collection boasts six premium scents. Each diffuser, housed in a crystal glass droplet vessel, comes with a single reed stick. Designed to last three months, these diffusers harness natural components and are packaged sustainably. With contemporary design elements, the product line is tailored for Generation Z and Millennial consumers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the home fragrances market as the sale value of finished consumer products, sprays, diffusers, scented candles, plug-ins, essential-oil blends, potpourri sachets, and wax melts that are purposely formulated, packaged, and promoted for scenting residential interiors.

Scope exclusion: Bulk air-care chemicals for institutional cleaning, automotive fresheners, and personal fine perfumes remain outside our accounting.

Segmentation Overview

-

By Product Type

- Sprays

- Diffusers

- Scented Candles

- Other Types

-

By Category

- Premium

- Mass

-

By Distribution Channel

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Retail

- Other Distribution Channel

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Indonesia

- Singapore

- Thailand

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- Nigeria

- United Arab Emirates

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews and short surveys with fragrance-oil blenders, contract candle manufacturers, specialty retailers, and e-commerce category managers across North America, Europe, Asia-Pacific, and South America helped us validate channel mix, typical price points, and growth pockets, filling gaps that desktop work alone could not bridge. Respondents also reviewed early model outputs, allowing iterative fine-tuning before finalization.

Desk Research

Mordor analysts first mapped the category using non-paywalled, tier-one datasets such as United Nations Comtrade export code 330749, Eurostat Prodcom 20422230, the US Census Bureau's Harmonized System mirror data, and Household & Commercial Products Association shipment indices. Trend color was added from peer-reviewed journals on indoor-air wellness, IFRA regulatory bulletins, and leading trade magazines that track candle wax and diffuser hardware innovations. Company 10-Ks, investor decks, and new-product press releases were screened through Dow Jones Factiva, while D&B Hoovers supplied revenue splits that anchor brand-level checks.

These sources illustrate our approach and are not exhaustive; numerous additional public records and proprietary notes supported fact finding and clarification.

Market-Sizing & Forecasting

A top-down and bottom-up construct underpins the model. We rebuilt 2025 demand from household counts and average scent-spend per dwelling, which are then adjusted for e-commerce penetration, regional disposable-income shifts, raw-material cost pass-through, and seasonality spikes around year-end gifting. Supplier roll-ups of factory shipments and sampled ASP × volume checks served as bottom-up reasonableness tests. Multivariate regression, applied to five key drivers, urban housing additions, wellness search interest, soy-wax price index, premium share drift, and online home-care basket size, projects values to 2030 under a most-likely scenario, with alternative views stress-tested during expert calls. Data gaps in country splits were interpolated using historical trade ratios before being smoothed.

Data Validation & Update Cycle

Outputs run through variance screens versus independent indicators, after which senior reviewers sign off. The study refreshes yearly, and any material event, major acquisition, regulatory clampdown, or raw-material shock triggers an interim update. A final sense-check is completed immediately prior to client release.

Why Mordor's Home Fragrances Baseline Commands Confidence

Published estimates often diverge because firms pick different product baskets, apply unlike price progressions, and refresh at varying cadences.

Key gap drivers in this space include whether plug-ins and wellness oils are bundled with candles, the aggressiveness of premium-mix uplift, currency conversion dates, and the frequency with which emerging-market data are revisited. Mordor's disciplined scope alignment and annual model rebuild narrow these variables, giving decision-makers a dependable anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 14.17 Bn (2025) | Mordor Intelligence | - |

| USD 26.00 Bn (2025) | Global Consultancy A | Includes personal-care body mists and commercial air fresheners, leading to larger base and steeper CAGR |

| USD 12.09 Bn (2024) | Consumer Goods Insights Publisher B | Uses pre-tax manufacturer revenues only, excludes online-only niche brands, last refreshed mid-2024 |

| USD 9.05 Bn (2025) | Trade Journal C | Relies on limited import statistics, omits premium artisanal candles and essential-oil diffusers |

Taken together, the comparison highlights how scope discipline, variable transparency, and an annual refresh cycle allow Mordor Intelligence to present a balanced, readily traceable baseline that withstands client and peer scrutiny.

Key Questions Answered in the Report

How big is the global home fragrances space in 2026 and how fast will it grow by 2031?

It is valued at USD 14.38 billion in 2026 and is forecast to reach USD 19.78 billion by 2031, expanding at a 6.58% CAGR.

Which region is expected to post the quickest growth through 2031?

South America is projected to register the fastest 7.97% CAGR, led by Brazil’s expanding middle class and modern retail build-out.

What product format is gaining share the fastest?

Scented candles are the quickest riser, projected to grow at a 7.21% CAGR on the back of premium gifting and social-media buzz.

How is e-commerce reshaping sales strategies for home fragrance brands?

Online channels are advancing at a 7.84% CAGR, prompting even large incumbents such as Bath & Body Works to list on Amazon and invest in subscription models for recurring revenue.

What regulatory shifts could constrain formulation choices?

Stricter VOC limits in the U.S. and EU plus expanded allergen labeling by July 2026 compel brands to reformulate sprays and diffusers or risk non-compliance.

Page last updated on: