United States Luxury Candles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

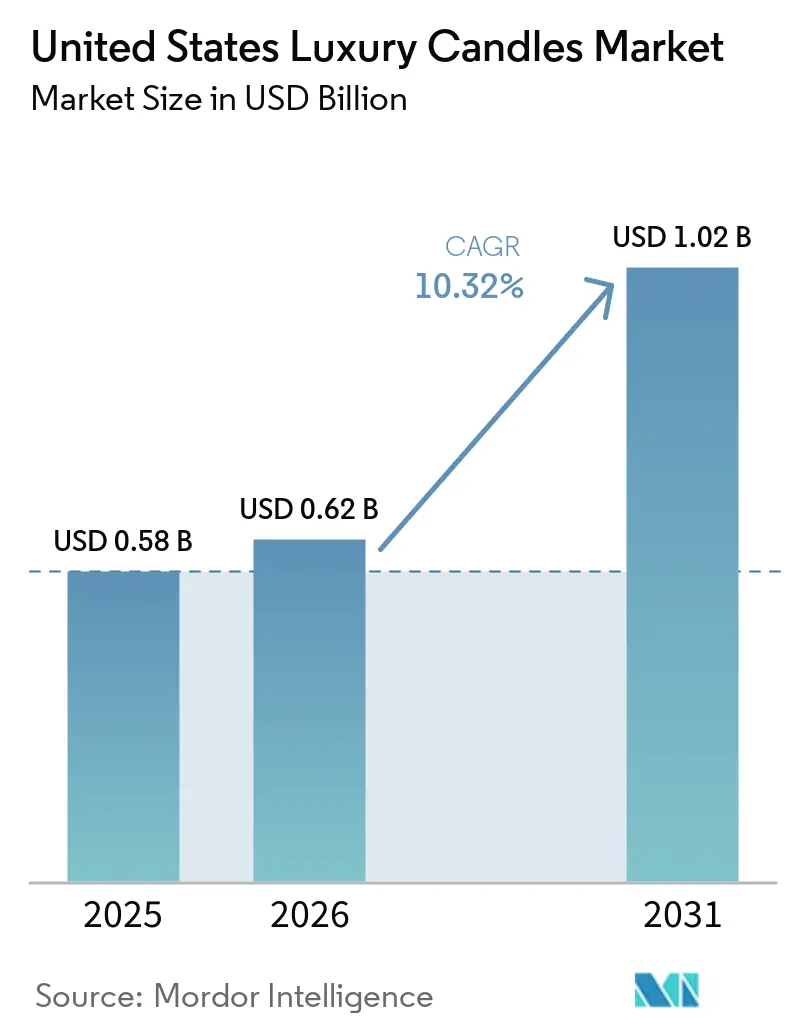

| Base Year Market Size (2025) | USD 0.58 Billion |

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 10.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Luxury Candles Market Analysis by Mordor Intelligence

The United States luxury candles market size was valued at USD 0.58 billion in 2025 and estimated to grow from USD 0.62 billion in 2026 to reach USD 1.02 billion by 2031, at a CAGR of 10.32% during the forecast period 2026-2031. The wider wellness backdrop remains supportive because the United States recorded a USD 2 trillion wellness economy in 2024, and Personal Care and Beauty accounted for USD 363.5 billion within that spend. The United States luxury candles market also benefits from its overlap with home ambiance, personal ritual, and gifting, which creates more than one reason to purchase across the year. Premium demand is increasingly shaped by fragrance depth, cleaner formulation expectations, and design value, which keeps the category distinct from more functional fragrance formats. The market is also moving toward a dual-channel model in which physical retail supports first discovery, while digital and brand-direct channels support selective launches and repeat orders. Growth opportunities remain strongest for brands that protect exclusivity, preserve pricing discipline, and convert broad wellness and home décor interest into repeat purchases across the United States luxury candles market.

Key Report Takeaways

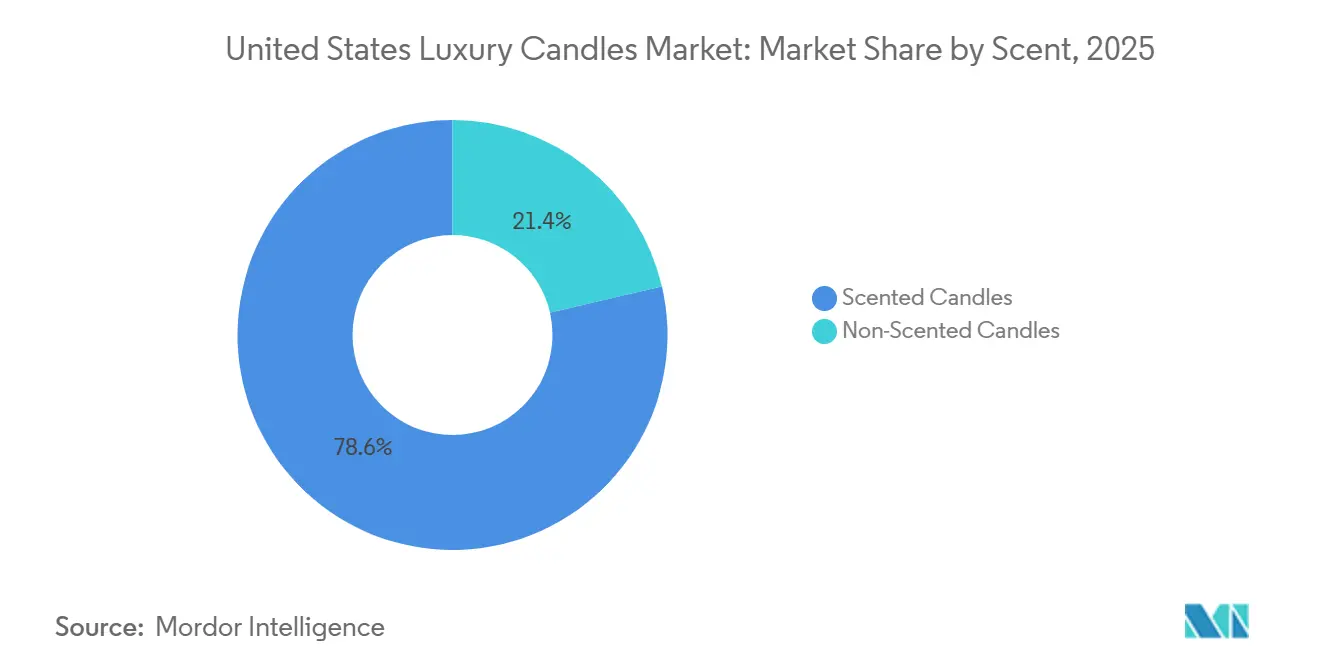

- By scent, scented candles held 78.63% of the market in 2025, while the same segment is forecast to expand at an 11.21% CAGR through 2031.

- By product type, containers accounted for 35.68% share of the United States luxury candles market size in 2025, while taper candles recorded the highest projected CAGR at 11.35% through 2031.

- By wax type, paraffin wax accounted for 82.38% share of the United States luxury candles market size in 2025, while beeswax is advancing at an 11.65% CAGR through 2031.

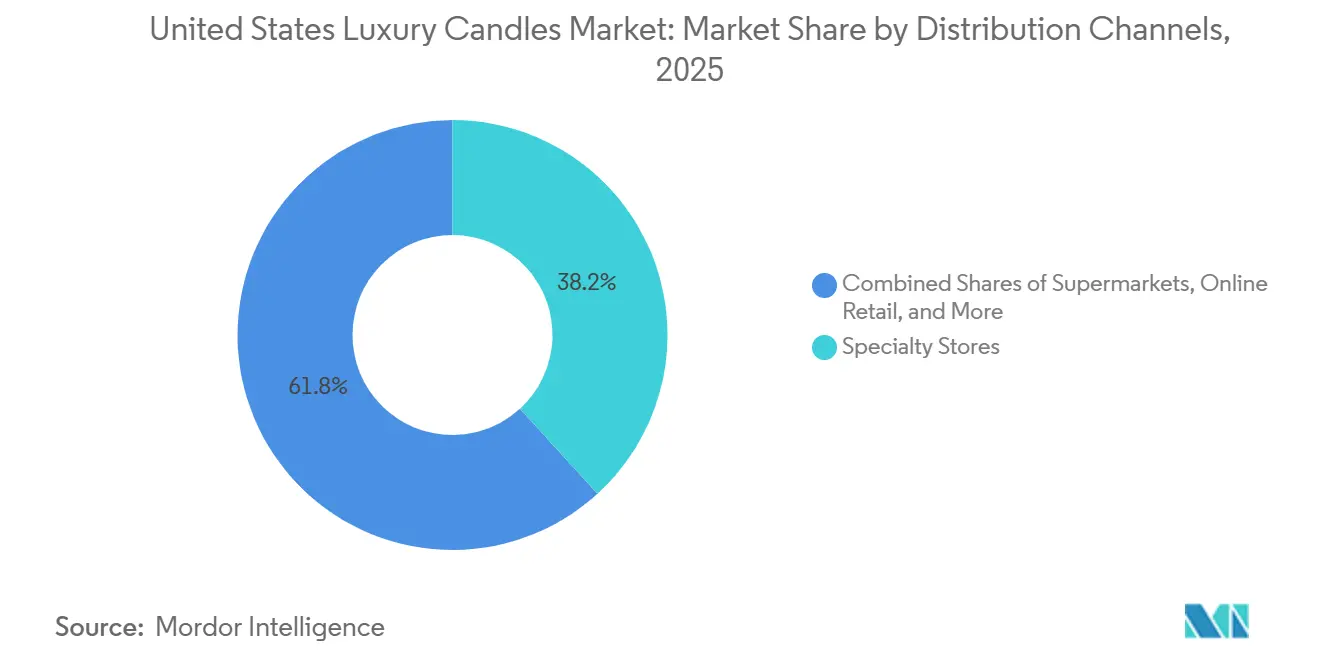

- By distribution channel, specialty stores held 38.21% of the United States luxury candles market share in 2025, while online retail is projected to grow at an 11.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Luxury Candles Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Interest in Home Ambiance and Wellness | +3.2% | Global, with the United States as the largest market, deepest penetration in the Northeast and West Coast | Medium term (2-4 years) |

| Increasing Disposable Income Among Affluent Consumers | +1.6% | National, with early gains in New York, Los Angeles, San Francisco, and Chicago metro areas | Medium term (2-4 years) |

| Expansion of the Luxury Home Décor Market | +1.5% | National, led by Northeast and West Coast design corridors | Long term (≥ 4 years) |

| Product Innovation in Fragrances and Formulations | +1.3% | Global, with United States brands leading commercial output | Medium term (2-4 years) |

| Influence of Social Media and Luxury Lifestyle Marketing | +1.1% | National, with heaviest engagement in urban concentrations | Short term (≤ 2 years) |

| Rising Demand for Sustainable and Clean-Burning Candles | +0.9% | National, with early regulatory and consumer gains in California, the Pacific Northwest, and the Northeast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Interest in Home Ambiance and Wellness

The wellness positioning of luxury candles has moved from brand language into a clear demand pattern across premium household and self-care spending. The United States wellness economy reached USD 2 trillion in 2024, and Personal Care and Beauty contributed USD 363.5 billion within that total[1]Source: Global Wellness Institute, “New Research Shows the US Wellness Economy Valued at USD 2 Trillion Now Represents One-Third of Entire Global Wellness Economy,” globalwellnessinstitute.org. The United States luxury candles market benefits because candles can draw spending from both home ambiance budgets and personal ritual budgets, which broadens purchase occasions across the year. A 2025 study in Scientific Reports found that scented candle use measurably altered indoor airborne microbiome composition, which has kept formulation quality and ingredient transparency in active consumer focus[2]Source: Adam Cheong et al., “Impact of Scented Candle Use on Indoor Air Quality and Airborne Microbiome,” Scientific Reports, nature.com. This has supported brands that pair fragrance mood, wax quality, and ritual use in one premium proposition instead of relying only on holiday gifting. It also helps move the category toward steadier replenishment behavior, which strengthens repeat demand in the United States luxury candles market.

Expansion of the Luxury Home Décor Market

The line between home fragrance and interior styling has become much thinner in the premium tier, and candles are increasingly chosen as visible décor objects. Buyers now expect vessel design, color fit, and room relevance to matter almost as much as the scent itself, which lifts the value of presentation. Bath & Body Works said in its FY2025 results that candles were a relatively bright spot, supported by better acceptance of 3-wick and single-wick formats and disciplined pricing execution. LAFCO New York expanded the e-commerce rollout of its Pink Paradise collaboration in November 2025 after the original candle sold out within one month, showing how design and hospitality cues can convert into direct product demand. The United States luxury candles market therefore gains from the broader rise of premium home styling because scent products are now judged as part of a room story. Brands that attach fragrance to a room, occasion, or visual identity usually hold stronger pricing power than brands built on scent alone.

Influence of Social Media and Luxury Lifestyle Marketing

Social platforms have changed how premium fragrance products are discovered, even when the final purchase does not happen inside the platform itself. In the United States luxury candles market, digital visibility matters most when it sends shoppers into controlled retail or brand-direct environments rather than uncontrolled discount channels. That matters because first purchase still depends heavily on fragrance evaluation, vessel inspection, and brand context, which remain stronger in curated physical settings. NEST New York’s May 2026 Maui Mango launch at Ulta Beauty showed how selective channel storytelling can widen reach without moving into broad-based discount distribution. The same pattern favors brands that treat online attention as a discovery tool while keeping distribution selective and premium. It also means lifestyle marketing works best when it builds aspiration and recognition without weakening scarcity or price discipline across the United States luxury candles market.

Rising Demand for Sustainable and Clean-Burning Candles

Sustainability in this category is no longer only a marketing theme, because regulatory pressure and consumer scrutiny are both shaping formulation choices. The California Air Resources Board has regulated volatile organic compound emissions from consumer products since 1989 and reported a 50% reduction in VOC emissions relative to uncontrolled levels[3]Source: California Air Resources Board, “Fragrance Use in Consumer Products,” arb.ca.gov. This backdrop improves the commercial standing of beeswax and plant-based blends because cleaner ingredient stories align more easily with stricter expectations. It also raises the importance of technical formulation capability, because premium fragrance performance still has to be maintained while ingredient choices become more selective. For the United States luxury candles market, that combination acts as a barrier against low-quality imitators that cannot match both compliance and sensory quality. It also supports premium pricing when clean-burning and safety claims are backed by credible product design and ingredient choices.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium Pricing Limits Mass-Market Adoption | -1.3% | National, most pronounced in Midwest, rural, and price-sensitive suburban markets | Long term (≥ 4 years) |

| Competition from Alternative Home Fragrance Products | -1.0% | National, with stronger substitution in tech-oriented urban markets | Medium term (2-4 years) |

| Risk of Product Counterfeiting and Brand Imitation | -0.6% | National, concentrated in e-commerce and third-party marketplace selling | Short term (≤ 2 years) |

| Volatility in Raw Material Costs | -0.9% | Global supply chain exposure with direct implications for the United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Pricing Limits Mass-Market Adoption

The USD 90-300 price band that defines the luxury tier is also the clearest limit on how widely the category can expand. Bath & Body Works said in its FY2025 results that consumers were cutting back on discretionary items such as candles and fragrances, and its 2026 outlook projected a further sales decline in the mid-market band. This pressure is weaker at the ultra-luxury end, where exclusivity and brand heritage can still support very high price points without the same resistance. It is more restrictive for brands trying to scale from niche specialty distribution into wider channels while keeping a clear premium identity. Gifting demand softens the effect because shoppers often cross their usual spending threshold for presents, but that support remains seasonal. The United States luxury candles market therefore grows fastest where luxury pricing is matched by strong design value, scent distinction, and tight channel control.

Competition from Alternative Home Fragrance Products

Luxury candles now compete with reed diffusers, room sprays, and smart-home fragrance systems for the same premium home ambiance budget. These alternative formats offer longer fragrance duration, programmable use, and no open flame, which can appeal to households willing to spend in the same premium range. The substitution risk matters most when the shopper is loyal to a fragrance profile or brand image rather than to the candle format itself. This is pushing the United States luxury candles market toward a wider home fragrance architecture in which brands need more than one format to hold the customer relationship. Brands that keep the fragrance house at the center of the purchase logic are better placed to limit switching. Brands that stay tied to a single format face more pressure when functional alternatives offer greater convenience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scent: Fragrance Complexity Sustains Dominant Scented Share

Scented candles held 78.63% of the United States luxury candles market share in 2025 and are also the fastest-growing scent segment, with an 11.21% CAGR through 2031. That dual position shows that fragrance has become both the main purchase trigger and the main premiumization lever in the category. Buyers are placing more value on layered scent profiles, room fit, and mood effect than on burn time alone, which keeps fragrance complexity at the center of brand differentiation. The segment also benefits from the fact that a scented candle can function as both a décor object and a sensory purchase, which supports use across gifting and self-purchase occasions. Non-scented candles continue to hold a role in display and occasion-based décor, but they remain structurally secondary because they do not deliver the same combined ambiance and ritual value.

Across the United States luxury candles market, the scented category is also moving toward more scenario-led fragrance storytelling rather than simple single-note positioning. Products built around a room, a time of day, or an emotional setting tend to hold stronger price resilience because the consumer is buying a setting rather than only a wax format. This supports higher repeat purchasing because shoppers can rotate scents by season, room, or occasion without leaving the same brand universe. It also helps explain why fragrance breadth has become a stronger sign of luxury positioning than vessel size alone. The United States luxury candles market therefore remains heavily scent-led, while non-scented formats preserve a narrower but still relevant decorative role.

By Product Type: Containers Lead While Tapers Define the New Aesthetic

Containers accounted for 35.68% share of the United States luxury candles market size in 2025, which reflects how strongly buyers value reusable vessels, visual presentation, and dependable scent throw. The container format also works well in self-purchase and gifting because the jar itself signals finish, permanence, and brand identity on a visible household surface. For the United States luxury candles industry, this matters because packaging is not a secondary feature, it is part of the luxury proposition that justifies the price. Votive and pillar candles still serve trial, travel, and decorative roles, but they do not usually match the same per-unit premium potential as a well-designed container candle. The category leader therefore remains the format that best combines fragrance performance, visual display, and brand recognition in one purchase.

Taper candles are projected to grow at 11.35% CAGR through 2031, making them the strongest product type by growth even though they trail containers in current value share. Their rise is tied to quiet-luxury interiors, tablescaping culture, and the broader use of candles as sculptural room accents rather than only as fragrance carriers. Within the United States luxury candles market, this gives taper formats a distinct aesthetic role that is less dependent on fragrance and more dependent on shape, finish, and styling relevance. The United States luxury candles industry is also seeing niche momentum in floating, novelty, and artistic formats that fit direct-to-consumer merchandising and seasonal gifting. These smaller formats remain limited in share, but they add creative range and help brands reach shoppers looking for collectible rather than standardized designs.

By Wax Type: Paraffin Maintains Volume Leadership as Beeswax Commands Premiumization

Paraffin wax held 82.38% of market value in 2025, which confirms that it still anchors current scale because of established manufacturing economics and strong fragrance load performance. Its leadership, however, sits beside growing pressure from cleaner ingredient expectations, tighter compliance needs, and rising consumer attention to what sits behind a luxury claim. The California Air Resources Board framework has kept emissions compliance visible, and that regulatory signal is especially important in a state that influences premium retail standards nationally. For the United States luxury candles market, this means paraffin remains commercially important but faces a more demanding image environment than it did in earlier premium candle cycles. Ingredient choice is becoming part of brand identity, not only a back-end production decision.

Beeswax is projected to grow at 11.65% CAGR through 2031, which makes it the fastest-growing wax segment in the category. That rate shows how strongly premium buyers now respond to clean-burning positioning, natural origin, and ingredient credibility when shopping inside the United States luxury candles market size. The United States luxury candles industry is also seeing steady traction for soy, coconut, and botanical blends as brands build proprietary formulations to stand apart without moving fully away from performance needs. This trend supports premiumization because alternative wax stories strengthen the link between luxury pricing and perceived product integrity. It also introduces a supply-side concern because beeswax availability can tighten when hive health or agricultural conditions constrain raw material supply.

By Distribution Channels: Specialty Stores Anchor Discovery While Online Accelerates Conversion

Specialty stores commanded 38.21% of the market in 2025, and their lead reflects the need for tactile discovery in a fragrance-led category. They allow shoppers to smell first, compare vessels, and understand the room or lifestyle narrative behind a candle before committing to a premium price. That role is especially important in the United States luxury candles market because first purchase often depends on confidence in scent quality and brand context rather than on convenience alone. Supermarkets and hypermarkets remain secondary for luxury candles and mostly matter during gifting periods or through value-tier extensions that sit near the category edge. Other channels such as hotel retail, spa boutiques, and museum stores have more relevance for ultra-premium brands that need an environment aligned with their positioning.

Online retail is projected to grow at 11.86% CAGR through 2031, which makes it the fastest-growing channel in the United States luxury candles market. The channel is expanding through brand-direct platforms, curated online partnerships, and selective digital launches that encourage repeat orders after the first trial. NEST New York’s selective channel communication, including its May 2026 Ulta Beauty exclusive, shows how brands can broaden visibility without weakening premium placement. For the United States luxury candles industry, the strongest model is increasingly physical discovery paired with digital replenishment, because that structure preserves brand context while improving convenience. The United States luxury candles market is therefore not moving away from stores, it is using online retail to deepen loyalty after sensory trust has already been established.

Geography Analysis

The Northeast remains the clearest launch corridor for ultra-premium candle brands because it combines prestige retail density, high discretionary spending, and strong influence from interior designers and tastemakers. That mix favors brands with heritage stories, refined vessel design, and tightly managed specialty distribution. For the United States luxury candles market, the Northeast continues to act as the most visible brand-equity zone, especially for labels that want early traction in high-credibility retail settings.

California and the broader West Coast present a different but equally important demand profile for the United States luxury candles market. High-income households, ingredient-conscious consumers, and stricter environmental expectations make the region a natural test bed for cleaner formulations and more selective wax choices. The California Air Resources Board regulatory framework has kept emissions compliance visible, which raises the strategic importance of formulation quality in premium candle development. The West Coast also supports broader home fragrance usage patterns, including interest in more than one premium format inside the same household. Success in California can therefore become a national positioning signal because the region combines retail relevance, consumer scrutiny, and strong lifestyle influence in one market environment.

The Sunbelt is emerging as the fastest-growing regional opportunity inside the United States luxury candles market because migration, household formation, and premium retail expansion are broadening the addressable base. Glasshouse Fragrances expanded into all 130 Anthropologie locations nationwide in October 2025, which underscored the importance of wider regional reach across the country rather than only traditional coastal flagship markets. Midwest and Mountain West markets still trail in absolute luxury candle spend, but they are gaining ground through specialty gift retail and curated boutique placement. The next phase of the United States luxury candles market is therefore likely to depend on broader geographic penetration rather than on a purely coastal growth model.

Competitive Landscape

The United States luxury candles market remains moderately concentrated, with a limited number of scaled players sitting above a wider field of differentiated specialists. LVMH, through Diptyque, Estée Lauder Companies through Jo Malone London, Tom Ford Beauty, and Le Labo, and Bath & Body Works all bring strong brand recognition, distribution reach, and pricing influence to the category. Alongside them, independent and specialist names such as NEST New York, Voluspa, LAFCO New York, Cire Trudon, and Maison Francis Kurkdjian compete through fragrance identity, vessel design, and selective distribution. This structure keeps the market competitive because manufacturing scale matters, but story depth and channel discipline still shape who can sustain a premium position.

Recent strategic activity shows that the category is developing through selective exclusives, brand elevation, and targeted expansion rather than through broad discount distribution. NEST New York launched Maui Mango as a summer exclusive at Ulta Beauty in May 2026, which supported reach expansion while preserving a controlled brand setting. LAFCO New York expanded the e-commerce rollout of its Pink Paradise collaboration in November 2025 after the original candle sold out within one month, which showed the value of hospitality-linked storytelling and demand extension. Yankee Candle introduced the YC Collection in October 2025 as a premium line inspired by quiet luxury, and then announced a Reese’s Book Club collaboration in January 2026 through quarterly exclusive releases. These moves show that growth is being pursued through curated partnerships and premium storytelling rather than through uncontrolled volume expansion.

The main competitive tension now sits between reach and exclusivity in the United States luxury candles market. Brands that move too far into off-price or overly broad third-party distribution risk weakening the price premium that supports the category. At the same time, white space remains open in refillable luxury formats and in wellness-linked fragrance products that can justify higher pricing through clearer product narratives. Brands with distinctive vessels, strong fragrance signatures, and disciplined channel strategy are better positioned to defend their place as imitation risk and format substitution both increase.

United States Luxury Candles Industry Leaders

LVMH (Moët Hennessy Louis Vuitton)

Estée Lauder Companies

Bath and Body Works, Inc.

Diptyque S.A.S.

Newell Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: NEST New York launched Maui Mango, a summer exclusive fragrance available only at Ulta Beauty, continuing its selective omnichannel strategy of using exclusive retail partnerships to reach new consumer segments while maintaining specialty-store brand positioning.

- April 2026: Meghan Markle expanded her lifestyle brand As Ever by launching a new collection of signature scented candles inspired by her children, Prince Archie and Princess Lilibet. The collection includes Candle No. 506 and Candle No. 604, named after their birth dates and featuring personalized fragrance profiles.

- October 2025: Yankee Candle, a subsidiary of Newell Brands, introduced the new YC Collection, a premium home fragrance range designed to capitalize on the growing consumer demand for luxury and design-focused home décor products. The collection features seven sophisticated fragrances developed by world-renowned perfumers and is offered in candle and reed diffuser formats.

United States Luxury Candles Market Report Scope

| Scented Candles |

| Non-Scented Candles |

| Containers |

| Votive Candles |

| Pillar Candles |

| Taper Candles |

| Others |

| Parafin Wax |

| Beeswax |

| Others |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Channels |

| Other Distribution Channels |

| By Scent | Scented Candles |

| Non-Scented Candles | |

| By Product Type | Containers |

| Votive Candles | |

| Pillar Candles | |

| Taper Candles | |

| Others | |

| By Wax Type | Parafin Wax |

| Beeswax | |

| Others | |

| By Distribution Channels | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Channels | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the United States luxury candles market in 2026 and where is it headed by 2031?

The United States luxury candles market stands at USD 0.62 billion in 2026 and is projected to reach USD 1.02 billion by 2031, growing at a 10.32% CAGR.

Which scent category leads demand in luxury candles across the United States?

Scented candles led with 78.63% share in 2025 and also posted the fastest scent growth at an 11.21% CAGR through 2031, which confirms that fragrance remains the main value driver.

What is driving beeswax growth in premium candles?

Beeswax is forecast to grow at 11.65% CAGR because clean-burning claims, natural origin, and ingredient credibility are becoming more important in premium purchase decisions.

Why are specialty stores still important if online retail is growing quickly?

Specialty stores held 38.21% share in 2025 because first purchase still depends on sensory trial and brand context, while online retail is growing faster at 11.86% CAGR by supporting repeat orders and selective launches.

Page last updated on: